SMEs/SMIs Financing via Shari'ah Compliant Instrument · NIDAL ALSAYYED, CEO WWW ... SMEs/SMIs...

38

CASABLANCA STOCK EXCHANGE MOROCCO MAY 20 TH , 2014 BY DR. NIDAL ALSAYYED, CEO WWW.INAYAH.ORG AMMAN, JORDAN SMEs/SMIs Financing via Shari'ah Compliant Instrument www.inayah.org Prepared by iNayah CEO: NIDAL ALSAYYED ( Email: [email protected] )

Transcript of SMEs/SMIs Financing via Shari'ah Compliant Instrument · NIDAL ALSAYYED, CEO WWW ... SMEs/SMIs...

C A S A B L A N C A S T O C K E X C H A N G E

M O R O C C O

M A Y 2 0 T H , 2 0 1 4

B Y

D R . N I D A L A L S A Y Y E D , C E O

W W W . I N A Y A H . O R G A M M A N , J O R D A N

SMEs/SMIs Financing via Shari'ah Compliant Instrument

www.inayah.org Prepared by iNayah CEO: NIDAL ALSAYYED ( Email: [email protected] )

Introduction

About INAYAH.org &Dr. Nidal Alsayyed

Background

Contribution to Islamic Finance

Strengths and Focus areas

Industry recognition

2

Brief Introduction on the Topic

May, 2014 INAYAH RESEARCH & CONSULTING| www.inayah.org

3

Socio-Economic ventures

المحاور الداعمة لتمويل الشركات الصغيرة

MICRO

FINANCE

SME

WAQF

مباحث التمويل الصغير واألصغر من منظور شرعي

(شأة ويرادم ويهجياث وتجارب. )انفهىو وانظرة انؤسساتيت

والع انتىيم انصغير في انغرب وتجارب يك انمياس عهيها.

يمترح صذوق ألغادير ويهجيت انتذىل.

:يتطهباث ويفاتيخ انذراست

يستىي دخم األفراد

تذذيذ االدتياجاث.

انبرايج اإلائيت نأليى انتذذة في انبهذا انختهفت.

يثم..انراكز وانصاديك انذونيت نألبذاث :ICARDA

WWW.INAYAH.ORG

Why SME’s?

Policymakers and bankers worldwide are increasingly focusing on micro-, small and medium-sized enterprises.

(IDB) is making important efforts to nurture the micro-enterprise and SME sector and its export activities. Three important subsidiaries serving the sector: the

International Islamic Trade Finance Corporation (ITFC), Islamic Corporation

for the Development of the Private Sector (ICD) and the Islamic Corporation

for Insurance of Investments and Export Credit (ICIEC). Each of the IDB

WWW.INAYAH.ORG

(الصورة العامة)تحديات التمويل الصغير في المغرب

The brief survey of possible funding gaps affecting smaller enterprises suggested that SMEs in the developed world could generally expect to receive funding if they have a commercially viable proposition. The banks are the principal source of funding and a lack of collateral might result in credit rationing in some cases. ها يأتي دول انتىيم اإلساليي

Islamic Banking for SME الصيرفة اإلسالمية في الشركات الصغيرة

Wide range of Islamic financial instruments, each with a specific purpose:

ensure that the instrument used is suitable for the economic purpose that a company seeks to achieve.

There are two main categories of transaction types:

❑ Profit- and loss-sharing partnership equity investments; and

❑ Transactions with a predictable or fixed return structure.

SME’s in Morocco

SMEs is a natural niche for Islamic banking as it deals directly with the real economy, creates employment, involves the productive use of resources, especially capital and finance, and contributes to the alleviation of poverty.

Ethical and moral values. Islamic banking also advocates entrepreneurship and risk

sharing. In the profit-sharing concept of a financed project, the financier and the beneficiary share the actual or net profit/loss, rather than leaving the risk burden to the entrepreneur.

The principle of fairness and justice requires that the actual output of such a project be fairly distributed between the two parties.

For micro-enterprises and SMEs looking for financing, Islamic banking can help promote entrepreneurial development

WWW.INAYAH.ORG

What are Sukuk

AAOIFI: “Investment Sukuk are certificates of equal value representing undivided shares in ownership of tangible assets, usufruct and services or (in the ownership of) the assets of particular projects or special investment activity, however, this is true after the receipt of the value of Sukuk, the closing of subscription and the employment of funds received for the purpose of which the Sukuk were issued” (standard no. 17, clause 2) Further reading: AAOIFI Sharia Standard No. 17

10

DAY ONE : SESSION I – BRIEF INTRODUCTION ON THE TOPIC

Sukuk return/pricing and payment

Fixed Return Vs. Variable return: Choosing the right underlying structure;

Mapping cash flows to the transaction, Sukuk is not an interest paying instruments, therefore a clear link must be established between the return and the underlying transaction;

Documentation perspective –

Commercial consideration – matching requirement with limitations

Assessing the role of security / Collaterals

11

DAY ONE : SESSION IV – EXAMINING RETURN OR PRICING IN SUKUK AND SECURITIZATION TRANSACTIONS

Structuring an SME Sukuk Transaction

•Availability of Asset

•Nature of the Asset

•Risk assessment

Asset Type

•Selecting a right jurisdiction for tax efficiency and other purposes

Jurisdiction and Regulations •Tenure

•Fixed Vs Variable

•Maturity terms

Return

Investor considerations

12

DAY ONE : SESSION III – SUKUK STRUCTURING AND DOCUMENTATION: A STEP BY STEP GUIDE

Asset Backed vs. Asset Based Sukuk

Asset Backed Sukuk (ABS) = Securitization + Certificates Backed by Assets + SPV (independent)

(So the recourse to the Assets due to True Sale)

Asset Based Sukuk (AbS) = Securitization + Certificates Backed by Collaterals+

SPV (credit interlinked)

(So the recourse to the Originator)

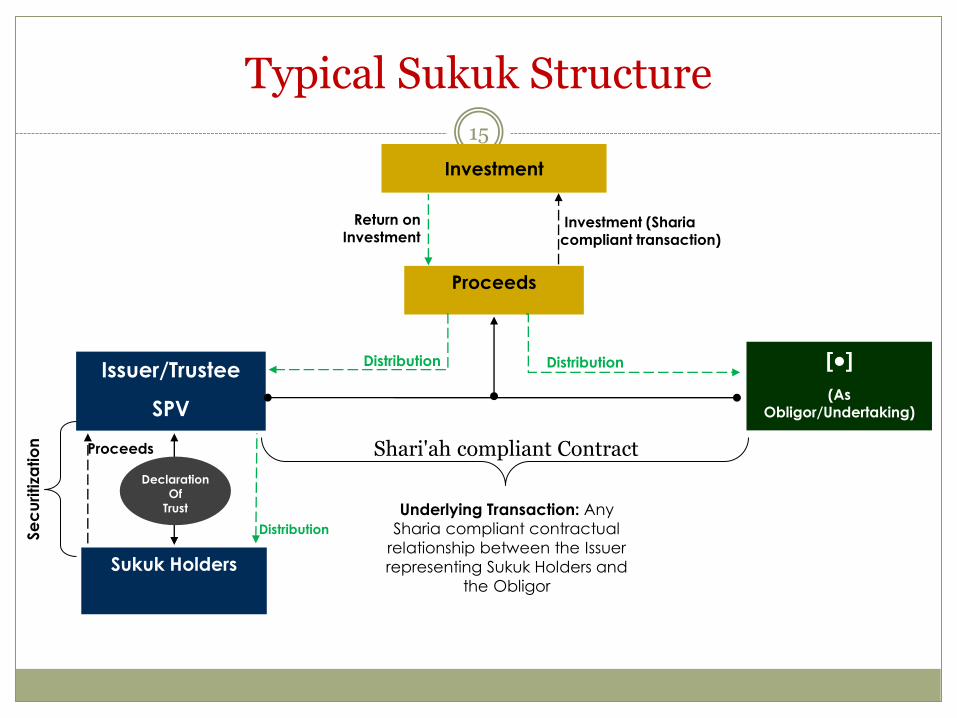

Typical Sukuk Structure 15

Distribution

Distribution

Sukuk Holders

Declaration

Of

Trust

Proceeds

Distribution

Return on Investment

Issuer/Trustee

SPV

[●]

(As Obligor/Undertaking)

Proceeds

Investment

Investment (Sharia compliant transaction)

Underlying Transaction: Any

Sharia compliant contractual

relationship between the Issuer

representing Sukuk Holders and

the Obligor

Se

cu

ritiza

tio

n

Shari'ah compliant Contract

Sukuk Vs. Other Investments الصكوك وأدوات االستثمار األخرى

Characteristics Sukuk Equity Bonds Securitizat

ion

Covered

Bonds

Ownership of

Assets √ √ X

X/√

X/√

Performance

linked return √ √ X

√

X

Underlying

transaction √ √ X √

X/√

Equity Risk √ √ X √

X/√

Fixed Returns √ X √ √ √

Risk Mitigation √ X √ √ √

16

Shari'ah Compliant for SMEs/SMIs

Based on approved Shari'ah compliant structures/contracts/instruments

Mimic the commercial aspects of the conventional instruments, however structurally and documentation wise significantly different

Meet the short & long term liquidity and investment needs of the SME project

Fund generation for various stakeholders in a Shari'ah compliant way

Essential component for Society overall Economics growth

17

DAY ONE : SESSION I – BRIEF INTRODUCTION ON THE TOPIC

Fundamental Shariah requirements for SMEs Sukuk

issuances

18

Outline

A. Structuring a Sukuk?

B. Various parties and their role.

C. What corporate structure is required?

D. What assets are required? A distinction between asset based and asset backed Sukuk

E. Securitization vs. Sukuk – differences and similarities

F. Innovation and the factors driving innovation

19

DAY ONE : SESSION II – FUNDAMENTAL SHARIA REQUIREMENTS FOR THE ISSUANCE OF SUKUK

How Sukuk transaction is structured?

Basic requirement to decide the structure of the Sukuk include the following: Asset: Availability/non availability, nature and type,

Return: Fixed, floating, ….

Risk Appetite:

Jurisdiction / Regulatory framework:

Nature of Obligor/Issuer :

Utilization of proceeds:

Convertibility, multiple issuances, and other special features:

Redemption:

Enforcement:

Other considerations for Morocco?

20

DAY ONE : SESSION II – FUNDAMENTAL SHARIAH REQUIREMENTS FOR THE ISSUANCE OF SUKUK

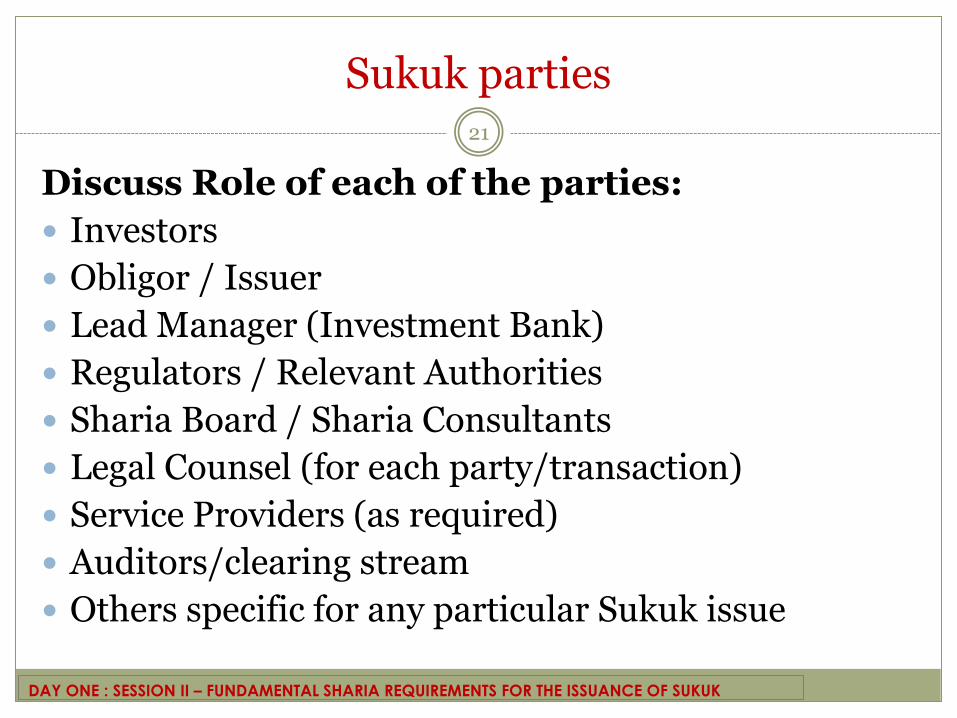

Sukuk parties

Discuss Role of each of the parties:

Investors

Obligor / Issuer

Lead Manager (Investment Bank)

Regulators / Relevant Authorities

Sharia Board / Sharia Consultants

Legal Counsel (for each party/transaction)

Service Providers (as required)

Auditors/clearing stream

Others specific for any particular Sukuk issue

21

DAY ONE : SESSION II – FUNDAMENTAL SHARIA REQUIREMENTS FOR THE ISSUANCE OF SUKUK

What assets are required? Asset based Vs Asset backed

What is meant by Asset Based / Asset Backed

Based on availability of Asset Sale of Asset?

Lease of Asset?

Other Investments (Musharakah, Mudarabah, Wakalah)

Regulatory requirement Issues with fees and taxes for Asset transfer

Based on the underlying transaction type Discuss the requirement based on transaction type: Ijara,

Mudarabah, Wakalah, Salam etc (more details and discussions will follow when we deal with the transaction type)

22

DAY ONE : SESSION II – FUNDAMENTAL SHARIA REQUIREMENTS FOR THE ISSUANCE OF SUKUK

Islamic Securitization vs. Sukuk: Differences & Similarities

Sukuk is in essence securitization of the underlying transaction;

However there exists a very important difference between a simple Islamic Securitization and Sukuk;

Recourse to the Asset:

In securitization the recourse of the investors is only to the asset securitized

Whereas in a Sukuk the recourse for the investors is both to the Obligor and the underlying assets/receivables

23

DAY ONE : SESSION II – FUNDAMENTAL SHARIA REQUIREMENTS FOR THE ISSUANCE OF SUKUK

SMEs Sukuk Challenges

Market operational and Regulatory framework.

Fixed Income mentality!

Debt based Sukuk Training.

Restructuring of Defaulted Sukuk.

Innovations in Islamic Finance

11/05/2014

25

Innovation in Islamic Finance

Questions for Discussion

Why is there a need for innovation - Are the basic structures in Islamic Finance able to address the commercial requirements?

Is replicating conventional structures actually innovation?

What is the scope for innovation in Islamic Finance and what are the parameters and rules for such innovation?

26

DAY ONE : SESSION II – FUNDAMENTAL SHARIA REQUIREMENTS FOR THE ISSUANCE OF SUKUK | INNOVATION

Innovation and the factors driving innovation

Need for continuous innovation

Major hindrances to adaptability – Challenges and Solutions

Regulations and legal framework

Conventional approach of the market players

Risk mitigation techniques

External Vs Internal Factors

External environment

Internal Islamic financial institutions readiness

27

DAY ONE : SESSION II – FUNDAMENTAL SHARIA REQUIREMENTS FOR THE ISSUANCE OF SUKUK | INNOVATION

Factors Driving Innovation

Innovation under Islamic Finance

Need for Innovation

Commercial considerations

Specific requirements of the Parties.

Commercial viability.

Legal considerations

Local law restrictions.

Enforcement issues.

Taxation issues

Limitations of the various basic Sharia structures

28

DAY ONE : SESSION II – FUNDAMENTAL SHARIA REQUIREMENTS FOR THE ISSUANCE OF SUKUK | INNOVATION

Sukuk based on Sale

11/05/2014

29

DAY ONE : SESSION III – SUKUK STRUCTURING AND DOCUMENTATION: A STEP BY STEP GUIDE

Issuer/Trustee

Pursuant to Declaration of

Trust

Company

(As Purchaser )

Sukuk Holder

Declaration of Trust

Assets / Property

Sale Agreement

Deferred Sale Price

Assets /

Property

Distribution Cash

Proceeds

Third Party

(Seller)

Purchase

Price

التمويل الصغير بصكوك اإلجارة30

DAY ONE : SESSION III – SUKUK STRUCTURING AND DOCUMENTATION: A STEP BY STEP GUIDE

شركة ذات غرض خاص

SME’s SPV

SME’s Company

(As Lessee المستأجر )

Public Sukuk

Holders

اتفاقية قانونية

رأس المال والممتلكات

اتفاقية تأجير

عوائد اإليجارات

Purchase

Undertaking

مساهمات توزيع األرباح

نقدية وعينية

Company

(As Seller)

ثمن الشراء

Company

(وعد ملزم من طرف ثالث)

Sukuk al-Ijarah 31

DAY ONE : SESSION III – SUKUK STRUCTURING AND DOCUMENTATION: A STEP BY STEP GUIDE

Issuer/Trustee

Pursuant to Declaration of

Trust

SME Company

(As Lessee)

Sukuk Holder

Declaration of Trust

Assets / Property

Lease Agreement

Lease Rentals

Purchase

Undertaking

Distribution Cash

Proceeds

Company

(As Seller)

Purchase

Price

Company

(As Obligor)

Sukuk al-Mudarabah 32

DAY ONE : SESSION III – SUKUK STRUCTURING AND DOCUMENTATION: A STEP BY STEP GUIDE

First Distribution (Pro-rata)

First Distribution

(Pro-rata) Second

Distribution

(Mudaraba

Agreement) (Tacit Musharaka)

Purchase Undertaking

Sukuk Holders

(As Rab Al Maal)

Declaration

Of

Trust

Rab Al Maal Contribution

Second Distribution

(Mudaraba

Agreement)

((Rab Al Maal Share)

(Capital at Marturity)

1 9

Return on Investment

(& Joint Cap)

Mudaraba Agreement

Issuer/Trustee

(As Rab Al Maal)

[●]

(As Obligor)

Mudarib Contribution

Joint Capital

Common Investment Pool

Investment

[●]

(As Mudarib)

2

3

4

5 6

7 7

8

Mudaraba Contribution

Sale Undertaking

Sukuk al-Musharakah 33

DAY ONE : SESSION III – SUKUK STRUCTURING AND DOCUMENTATION: A STEP BY STEP GUIDE

Issuer/Trustee

Pursuant to Declaration of

Trust

Company

Sukuk Holder

Declaration of Trust

Contribution in-kind/cash Contribution in-cash

Musharaka Agreement

Management

Agreement Managing Partner

(Company)

Musharaka

Entity

Investments as per

Musharaka Business Plan

Return on

Investment

Distribution Distribution

Purchase

Undertaking Distribution Cash

Proceeds

Sukuk Wakala

11/05/2014

34

Master

Wakala

Agreement

$ Returns $

Investments

Sukuk Holders

Funding Declaration

of Trust

Issuer SPV Trustee & Muwakkil (Principal)

Company Wakil (Agent) & Obligor

Master

PU

Master

SU

Portfolio of Wakala Assets

Financing

Returns – S/A; On Maturity or Exercise of the relevant

PU or SU Investments – Payments by the Sukuk Holders & pursuant to Wakala Agreement through Trustee investment into Wakala Assets

PU – Purchase Undertaking

SU – Sale Undertaking

DAY ONE : SESSION III – SUKUK STRUCTURING AND DOCUMENTATION: A STEP BY STEP GUIDE

Distinction between various Sukuk structures – Pricing/Return/Risk

Fixed Return Variable Return Valuation Risk

Musharaka Yes* Yes Underlying Assets High risk

Mudaraba Yes* Yes Underlying Assets

High risk

Wakala Yes* Yes Underlying Assets

High risk

Istisna Yes No Receivable Low Risk

Salam

Yes No Receivable

Low Risk

Murabaha Yes No Receivable Low Risk

Ijara Yes Yes Underlying Assets /

Receivables Moderate Risk

35

DAY ONE : SESSION IV – EXAMINING RETURN OR PRICING IN SUKUK AND SECURITIZATION TRANSACTIONS

Shariah position on shortfall, default and documentation requirements

Remedies available to investors: AAOIFI guidelines and Sharia position

Discuss concept of return based on underlying transaction

Events of Default: Shariah position and limitations

Triggering the Event of Default

Establishing default of the obligor under various underlying transaction types: Ijara, Musharaka, Mudaraba, etc

Mitigation of risk – return shortfall and default

Additional documents?

36

DAY ONE : SESSION IV – EXAMINING RETURN OR PRICING IN SUKUK AND SECURITIZATION TRANSACTIONS

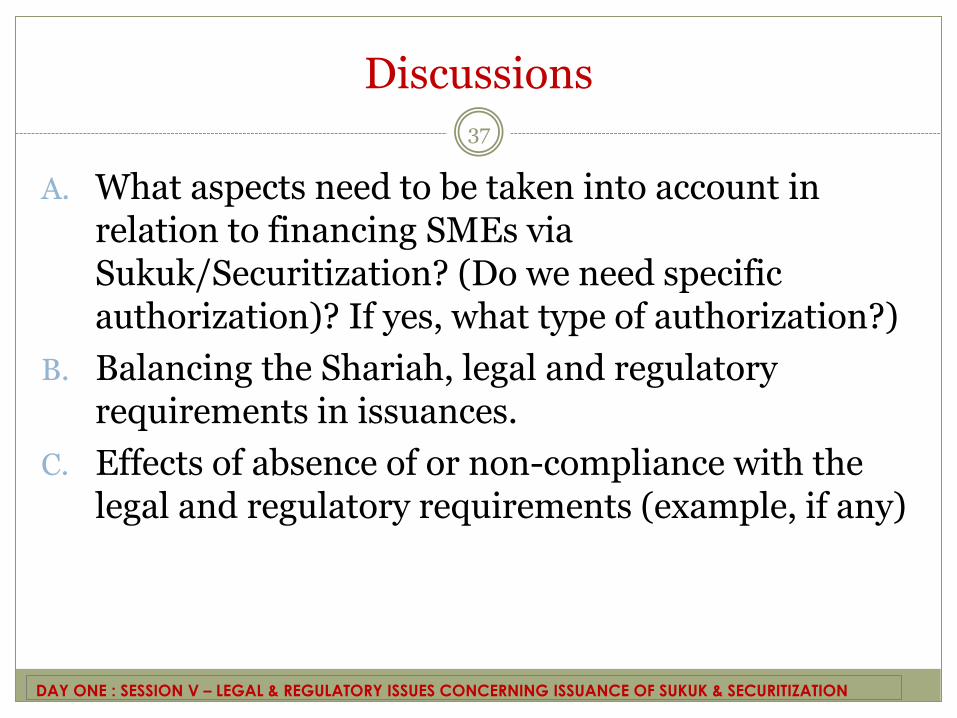

Discussions

A. What aspects need to be taken into account in relation to financing SMEs via Sukuk/Securitization? (Do we need specific authorization)? If yes, what type of authorization?)

B. Balancing the Shariah, legal and regulatory requirements in issuances.

C. Effects of absence of or non-compliance with the legal and regulatory requirements (example, if any)

37

DAY ONE : SESSION V – LEGAL & REGULATORY ISSUES CONCERNING ISSUANCE OF SUKUK & SECURITIZATION

Thank you

Dr. Nidal Alsayyed, PhD

CEO Inayah Research and Consulting

Jordan, UK, and Qatar

Tel. 0096279 782 0837