SME/MSE Lines of Credit Belarus - ebrd.com · TC7 TCS-2005-02-01 Project implementation support,...

21

Operation Performance Evaluation Review SME/MSE Lines of Credit Belarus (A technical cooperation operation) April 2007 ab0cd Evaluation Department (EvD)

Transcript of SME/MSE Lines of Credit Belarus - ebrd.com · TC7 TCS-2005-02-01 Project implementation support,...

Operation Performance Evaluation Review

SME/MSE Lines of Credit

Belarus(A technical cooperation operation)

April 2007

ab0cdEvaluation Department (EvD)

OPERATION PERFORMANCE EVALUATION REVIEW (OPER)

PREFACE

The subject of this OPER is the technical cooperation (TC) operation: MSME Sector Development Project Preparation in Belarus in the committed amounts of EUR TC1 (248,900) TC2 (159,028), TC3 (16,248), TC4 (28,582), TC5 (84,620), TC6 (67,058), TC7 (3,355), TC8 (106,484), TC9 (11,425) funded respectively through the TC1-6 (Taipei China), TC7 (Technical Cooperation Special Fund), TC8 (US government) and TC9 (UK government). The Operation Leaders (OLs) of the above TCs were successively TC1 (Irina Kravchenko), TC2, TC3, TC5, TC8 and TC9 (Oksana Pak), TC4, TC5 and TC6 (Inna Yabbarova). The Operation Team and other relevant Bank staff commented on an early draft. The Basic Data Sheet on page iii of this report is complementary to this OPER and designed to be read together. The evaluation was carried out by Nicolas Mathieu, Senior Economist of the Evaluation Department (EvD). Information on the operation was obtained from relevant teams and departments of the Bank and its files as well as from external sector and industry sources. Fieldwork was carried out in November 2006. Post-evaluation selection and process Selection of an operation for post-evaluation by EvD uses the following criteria: relevance to the Bank’s likely future operations; lessons-learned potential; size of the Bank’s investment commitment/exposure; balance among countries of operation; balance among sectors and types of operations; relative priority of investment operation OPERs within EvD’s overall work programme priorities and resources. The Bank’s post-evaluation process is described in Chapter 8 of the Operations Manual. The responsible OL first writes a TC PCR. The PCR report serves a self-evaluation function and establishes the basic facts and lessons from the operation’s implementation outcome and future prospects. EvD’s independent evaluation follows, using the PCR as one of several inputs.

BELARUS SME/MSE CREDIT LINES TECHNICAL COOPERATION PROGRAMME

TABLE OF CONTENTS

Page PREFACE ABBREVIATIONS AND DEFINED TERMS ii BASIC DATA SHEET iii 1. INTRODUCTION 1 2. PROJECT RATIONALE 2 3. ACHIEVEMENT OF OBJECTIVES 3 3.1 Objectives 3 3.2 Achievement of objectives 4 4. OVERALL ASSESSMENT 5 5. TRANSITION IMPACT AND ADDITIONALITY 7 6. BANK PERFORMANCE 10 7. KEY ISSUES AND LESSONS LEARNED 11 7.1 TC project design and implementation 11 7.2 Sector policy dialogue 12 LIST OF APPENDICES

Appendix 1 Operations Performance Ratings Appendix 2 Transition Impact Analysis

BELARUS SME/MSE CREDIT LINES TECHNICAL COOPERATION PROGRAMME

ii

ABBREVIATIONS

EvD Evaluation Department FIAC Foreign Investment Advisory Committee IFC International Finance Corporation IFI International Financial Institution MSEs Micro and small enterprises MSMEs Micro, small and medium enterprises NBB National Bank of Belarus OPER Operation Performance Evaluation Review PB Participating Bank PCR Project Completion Report PMU Project Management Unit SMEs Small and medium enterprises TC Technical cooperation TOR Terms of Reference USD United States dollar XMR Expanded Monitoring Report

DEFINED TERMS

the Bank European Bank for Reconstruction and Development the Client Participating Banks (PBs): eligible Belarussian private banks the OPER Team Staff of the Project Evaluation Department who carried out

the post-evaluation the Operation Team The staff in the Banking Department and other respective

departments within the Bank responsible for the Operation appraisal, negotiation and monitoring, including the PCR

the Project The overall objectives of the TCs were to assist the

participating private banks in setting up internal procedures for SME/MSE credit lines, and strengthen the qualifications of their staff in project appraisal and administration of credit.

OPERATION PERFORMANCE REVIEW

BASIC DATA SHEET Operation codes TC1 7370

TC2 12251 TC3 12251 TC4 26684 TC5 26684 TC6 26684 TC7 27496 TC8 35387 TC9 35387

Location: Belarus Operation: Belarus SME line of credit/micro lending programme/finance framework – 2005

regional expansion Sector: Financial institutions Type: Technical cooperation Facilitators: Taipei China, United Kingdom, United States, Technical Cooperation Special

Fund Bank Unit: Group for Small Business, Minsk Resident Office and ETC Initiative A. Funding TC TC Commitment

Commitment number Commitment title Total

amount disbursed (€)

TC1 TAI-1999-07-06 SME line of credit – extension project implementation support

248,900

TC2 TAI-2000-06-02 Pilot micro lending programme

159,028

TC3 TAI-2002-02-05 Pilot micro lending programme

16,248

TC4 TAI-2002-08-15 Project implementation support, Belarus SME line of credit

28,582

TC5 TAI-2002-08-17F Belarus micro lending programme

80,062

TC6 TAI-2004-05-08 Project implementation support, Belarus SME line of credit

67,058

TC7 TCS-2005-02-01 Project implementation support, Belarus SME line of credit

3,355

TC8 USAD-2005-05-02 Belarus SME/MSE finance framework –2005 regional expansion

106,484

TC9 UKD-2005-11-08 Belarus SME/MSE finance framework-2005 regional expansion

11,425

iii

OPERATION PERFORMANCE REVIEW

B. Procurement Mode Sources by country Consultant services TC1 Direct selection United Kingdom TC2 Selection from shortlist France TC3 Direct selection Russia TC4 Selection from shortlist France TC5 Direct selection Russia TC6 Selection from shortlist France TC7 Selection from shortlist Russia TC8 Direct selection Russia TC9 Direct selection Russia C. Visits Type of visit No. of visits Person-days EvD/OPER 1 5

iv

OPERATION PERFORMANCE EVALUATION REVIEW

BELARUS SME/MSE CREDIT LINES TECHNICAL COOPERATION

1. INTRODUCTION 1.1 The Bank’s involvement The first SME line of credit to Belarus (sovereign) became effective in March 1995. The loan proceeds were ‘lent-on’ through qualifying private participating banks (PBs) to private small and medium enterprises (SMEs). At that time, a Project Management Unit (PMU) was established within the National Bank of Belarus (NBB) to administer the SME line of credit. The project implementation was managed by the PMU and was supported by a technical cooperation (TC) project. The TC support ended in November 1994 and was evaluated by EvD one year later. In 1999 the EBRD resumed its advisory services to the PBs to further strengthen their credit administration and ensure quality of the sub-loans through a new technical cooperation project (TC1). Given the demand for micro loans, the Bank decided in July 2000 to re-allocate US$ 1 million from the existing SME loan to support micro and small enterprises (MSE) lending in Belarus. Consequently, a pilot programme was started with two of the existing PBs under the SME loan. The pilot programme started in Minsk and later on expanded to a second region – Brest. The pilot programme was accompanied by a technical cooperation project (TC1) financed by the government of Taipei China to train loan officers, set up new micro-lending operations and, as in TC1, ensure the quality of the final product. Except for TC4, which was addressed to SMEs, the subsequent technical cooperation projects (TC2 to TC9) supported MSE lending. They built on the lessons of experience from TC2 in further tailoring the TC programme to the local conditions in Belarus. They were implemented over the period 2002-2006 to assist the increasing EBRD lending activity to MSMEs in Belarus. The funds from the Recycling Account of the 1995 SME credit became increasingly insufficient to meet the demand of the MSMEs. Therefore, in December 2004, the EBRD launched a new MSME finance facility to continue financing the private Belarussian MSEs through local participating banks. The sequence of TC components TC1 to TC9 that supported the 1994 and 2004 lending operations programme is summarised below:1

1 As of 6 December 2006, all committed amounts were fully disbursed, expect for TC5 where the total amount of disbursements was €80,062.

Page 2 of 13 Belarus SME/MSE credit lines (TC)

Table 1: EBRD TC programme for MSME lending in Belarus 1999-2006

Lending programme Label TC reference name Commitment Commitment amount date

TC1 TAI 1999-07-06 248,900 1999 TC2 TAI 2000-06-02 159,028 2000 TC3 TAI 2002-02-05 16,248 TC4 TAI 2002-08-15 28,582

1994 SME credit line with pilot MSE credit line starting in 2000

TC5 TAI 2002-08-17F 84,620

2002

TC6 TAI 2004- 05-08 67,058 2004 TC7 TCS 2005-02-01 3,355 TC8 USAD 2005-05-02 106,484

2004 SME/MSE credit facility

TC9 UKD 2005-11-08 11,425

2005

2. PROJECT RATIONALE In 1999 the preparation mission for the project found a number of very promising partner banks with whom a TC programme could work. Whilst the partner banks had shortcomings, all indicated a strong commitment and readiness to address their problems and develop a long-term capacity to serve the microfinance market. In addition to the advantages resulting from the formal support of the EBRD and the possibility of accessing long-term foreign exchange funding at advantageous rates, a good selection of a pilot branch in any of these banks would help to ensure that adequate delivery channels were in place. By contrast, small and micro businesses were so battered by the legal and regulatory environment that they went ‘underground’. The possibility of their emerging from the underground economy that many of these businesses had created for themselves to access a new banking product targeted at the microfinance sector was unlikely to be appealing in that policy environment. In addition, no bank, however committed or enthusiastic, could operate independently of the macro context. The prevailing legal, regulatory and exchange rate problems were so acute that launching a microfinance programme at that time amounted to a significant risk that the programme would fail to reach the necessary critical mass. A common theme to all the banks was the need for a microfinance programme to be launched in the framework of long-term, dedicated advice. Many technical assistance providers, however, were not willing to put funds into Belarus. It was no coincidence that much of the donor community’s unwillingness to provide funding was linked to the same underlying political issues that made a microfinance programme difficult to launch in the first place. Even if some donor funding could be found, building up a sustainable programme was going to be at best a long-term goal and at worst an impossibility to bring about. In addition, the Bank policy for Belarus was to forbid the recourse to any publicly owned financial intermediary, on the ground of multi-party democracy requirements of Article One of the Agreement Establishing the Bank. To succeed in getting enough business volume to reach profitability, private banks had to take considerable risk.2 They were in a relatively better position than public banks to find guarantees other than collateral for MSE loans and make decisions on more objective private sector grounds. They were able to accept demand

2 The lack of branches from private banks was not the only obstacle to mass scale SME/MSE lending. The complicated legal environment was also a major constraint.

Page 3 of 13 Belarus SME/MSE credit lines (TC)

from clients who may not meet the all credit regulation requirements of public banks but had the ability and the willingness to repay. Private banks, however, were not sheltered from governance issues, directed lending pressures and volume of lending constrained by the size of their capital. Given the circumstances in which it was to be implemented, this SME/MSE operation and the related TC had to be designed to fully fit the local conditions. Therefore it was to be handled by bank staff with high experience in both microfinance and policy dialogue. Bank senior management had to be proactive in supporting the policy dialogue at high levels and facilitate the search for donor funds. The TC also needed a highly receptive and committed private sector client group. All these conditions, in addition to the well understood constraint of Article One, were rendering the SME/MSE operation and its TC highly risky: missing one of them would endanger the entire initiative. 3. ACHIEVEMENT OF OBJECTIVES 3.1 Objectives The objective of TC1 and TC4 on SMEs was to continue to advise the PBs on strengthening their credit administration, with emphasis on the monitoring of sub-projects financed under the SME line of credit.3 Given the difficult business environment, there was a need for a project co-ordinator to ensure quality control of the final product. The objectives on the other components TC2 to TC9 on MSEs were similar in substance. Some features were added as they were greenfield operations: (i) implementation of an MSE lending programme with PBs selected by the EBRD, and when appropriate, assist in selecting new PBs/branches for implementation of the programme; (ii) establish high turnover lending operations with a focus on the economy’s smallest borrowers; (iii) build up a diversified and commercially viable micro loan portfolio with an average loan size below US$ 5,000/20,000;4 (iv) institution building and staff training within PBs – within the duration of the assignment at least 5/25 loan officers should be trained;5 (v) representation of the EBRD in sub-loan decisions, portfolio monitoring and loan recoveries; and (vi) regular and detailed reporting to the EBRD on progress of the programme. Three key items were added in 2005 for TC8 and TC9: (i) graduation of PBs from the programme6 (ii) implement management information systems (MIS); and (iii) actively engage in policy dialogue with the relevant Belarussian authorities to remove obstacles to efficient MSE lending and act as an intermediary between the EBRD and the government of Belarus.

3 Credit assessment including site visits by the PB and consultant, approval, procurement, loan disbursement, training needs, post-disbursement monitoring, valuation of collateral, management of overdue payments, financial reporting and integrity checks. 4 US$ 5,000 in TC3, US$ 10,000 in TC5 and TC 6, and US$ 20,000 in TC8 and TC9. 5 Ten loan officers in TC3, an additional 20 in TC 5, 10 in TC 6, 10 in TC7, 25 in TC8 and 5 in TC9. Scholarships were given for six months at 150 per months out of TC funds. 6 Graduation was required within 12-18 months (except for regional centres). A gradual slowdown of technical assistance input should begin approximately 9-12 months after the start of training and institution building at a given PB/branch). Graduation benchmarks were (i) the gradual increase in loan limits given to the PB, i.e. the amount that the PB/branch credit committee can decide by itself; (ii) the growth in number and volume of loans after removal of Western experts; and (iii) the level of arrears.

Page 4 of 13 Belarus SME/MSE credit lines (TC)

3.2 Achievement of Objectives 3.2.1 Credit advisory and administration TC1 and TC4 were fully disbursed and greatly facilitated long-term lending for high quality SME projects. The consultants performed numerous monitoring site visits to the sub-projects; developed a new format of Credit Appraisal Report and new sub-project database system; reviewed the PMU reporting requirements and suggested improvements. Long-term institution building programmes of the PBs established in the mid-1990s under the previous TCs were further implemented. The PMU successfully improved the administration procedures and reporting system. For quality control purposes, the consultants reviewed and approved the sub-projects. The professional skills of the consultants and their knowledge of the Russian language ensured a quick assessment and approval of the proposals. In the same way, TC3 to TC9 were implemented to effectively support the MSE programme whose implementation accelerated after 2003. The TC hiring panel selected a Russian-born individual with a solid track record in implementing a similar assignment in Russia. The consultancy services were fully provided to the partner banks, assisting them with the establishment of their credit procedures, with overcoming the main deficiencies in their credit appraisal skills and with the development of policy statements and institution building programmes. While there were some discrepancies in meeting the annual targets of the number of loan officers trained, the objectives were met on a cumulative basis over the period covering TC3 to TC9.7 Specific training in financial modelling was added to the programme. Graduation from the programme has been implemented according to schedule. The graduated branches of the PBs were left with sustainable business structures and growing lending activities, owing to tight graduation benchmarks.8 Except for TC2 in which the consultant did not perform as expected in a context where outcomes of the policy dialogue were still pending, the credit advisory, training and administrative objectives at the corporate level for MSE lending were fully achieved. Policy dialogue The policy dialogue started in 2001 and with the usual delays that occur in difficult business environments, specific results were achieved in 2003-2005. Achievements in the later years were supported by technical assistance through TC8 and TC9. The Bank operational staff and management in charge of implementing the micro-lending programme did not wait for the formal technical assistance in this area to start the policy dialogue on items that were essential to releasing some major constraints to micro lending in Belarus. Already in 2002, under TC5, progress had been made in the area of streamlining regulations as a result of an intensive policy dialogue between the NBB, PBs, the Operation Team and the Resident Office. So far, the course of policy dialogue has directly helped remove the following major impediments to successful MSE lending in Belarus in the area of foreign exchange availability, lending procedures and guarantees:

7 For example, 12 persons were trained under TC3, above a target of 10, and 14 persons were trained under TC5, below a target of 20. 8 Graduation benchmarks were (i) the gradual increase in loan limits given to the PB, i.e. the amount that the PB/branch credit committee can decide by itself; (ii) the growth in number and volume of loans after removal of Western experts; and (iii) the level of arrears.

Page 5 of 13 Belarus SME/MSE credit lines (TC)

• Use of foreign exchange cash. Disbursements and repayments in foreign exchange cash for legal entities and individual entrepreneurs has been authorised in the framework of the EBRD SME/MSE line of credit.

• Simplified MSE lending procedures. New instructions on lending from the NBB were provided to simplify micro-lending procedures: 9

o cancellation of mandatory inspections on the purpose of the loan o banks are allowed to set their own micro-lending procedures o banks can decide on micro loan maturities.

• Tax Agency papers are no longer required. Previously, to open a credit account, a

company had to obtain in 10 days a duplicate of the taxpayer’s account number, which was chargeable. According to the new rules for opening a credit account, documents from tax agencies are no longer required.

• Collateral not compulsory. As a result of the policy dialogue, changes were made to a Presidential Decree in 2005, which allowed guarantees of third parties not secured by collateral.10 The time for loan processing and disbursement was shortened significantly, due to the possibility to issue loans secured by guarantees other than collateral. The clients do not spend time any longer for the registration of pledge agreements, which saves from two to six days.

• Elimination of the 30 per cent of compulsory conversion to local currency.

Previously, according to Belarus legislation, foreign exchange cash collected by legal entities and individual entrepreneurs was to be partially sold to the state. Therefore, in order to repay a loan, the borrower had to deposit an additional 30 per cent of cash. This requirement was abolished.

The policy dialogue objective has been fully achieved because its coverage and intensity was enough to trigger the very minimum of changes in regulations that were needed to keep the MSE programme running. 4. OVERALL ASSESSMENT SME Credit Advisory in TC1 and TC4 was essential for successful project implementation. It provided technical assistance to the banks in project appraisal and monitoring, and helped to ensure sound banking principles in project selection. Most of the proposed sub-projects were approved. The loan portfolio improved as well as the credit skills of the PBs staff. The SME Line of Credit remained the main source of foreign exchange term financing for Belarusian SMEs. While the objectives of TC2 in support of MSE credit administration were partly achieved, TC3 was clearly successful. Through its skilled implementation, the assignment demonstrated the ability and willingness of PBs to focus on the target group via institution building and training measures. The activities of TC6 to TC9 contributed to further improvement of the PBs’ project appraisal and monitoring procedures and facilitated the 9 Micro loans are identified by the NBB regulation as loans below US$ 108,594 equivalent. 10 Previously, in accordance with the legislation, the guarantees of third parties were to be supported by collateral. However, the new guarantees attached to the lending procedures supported by the TC no longer require the use of collateral.

Page 6 of 13 Belarus SME/MSE credit lines (TC)

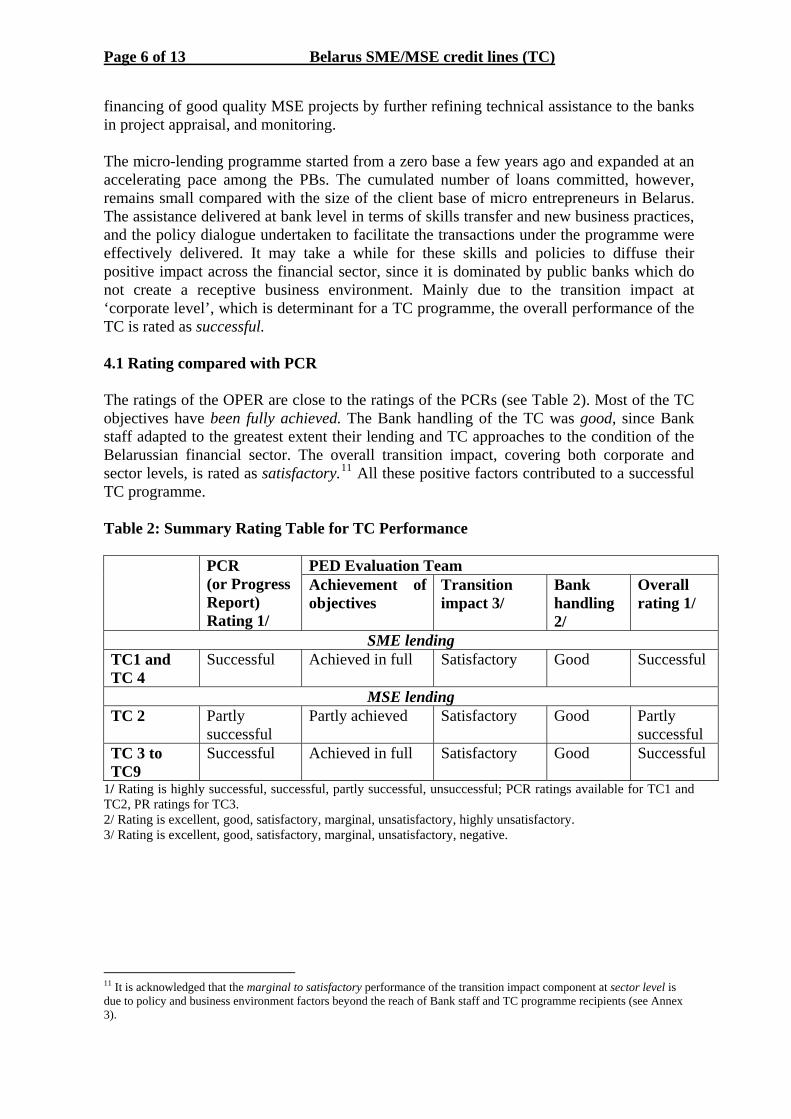

financing of good quality MSE projects by further refining technical assistance to the banks in project appraisal, and monitoring. The micro-lending programme started from a zero base a few years ago and expanded at an accelerating pace among the PBs. The cumulated number of loans committed, however, remains small compared with the size of the client base of micro entrepreneurs in Belarus. The assistance delivered at bank level in terms of skills transfer and new business practices, and the policy dialogue undertaken to facilitate the transactions under the programme were effectively delivered. It may take a while for these skills and policies to diffuse their positive impact across the financial sector, since it is dominated by public banks which do not create a receptive business environment. Mainly due to the transition impact at ‘corporate level’, which is determinant for a TC programme, the overall performance of the TC is rated as successful. 4.1 Rating compared with PCR The ratings of the OPER are close to the ratings of the PCRs (see Table 2). Most of the TC objectives have been fully achieved. The Bank handling of the TC was good, since Bank staff adapted to the greatest extent their lending and TC approaches to the condition of the Belarussian financial sector. The overall transition impact, covering both corporate and sector levels, is rated as satisfactory.11 All these positive factors contributed to a successful TC programme. Table 2: Summary Rating Table for TC Performance

PED Evaluation Team PCR (or Progress Report) Rating 1/

Achievement of objectives

Transition impact 3/

Bank handling 2/

Overall rating 1/

SME lending TC1 and TC 4

Successful Achieved in full Satisfactory Good Successful

MSE lending TC 2 Partly

successful Partly achieved Satisfactory Good Partly

successful TC 3 to TC9

Successful Achieved in full Satisfactory Good Successful

1/ Rating is highly successful, successful, partly successful, unsuccessful; PCR ratings available for TC1 and TC2, PR ratings for TC3. 2/ Rating is excellent, good, satisfactory, marginal, unsatisfactory, highly unsatisfactory. 3/ Rating is excellent, good, satisfactory, marginal, unsatisfactory, negative.

11 It is acknowledged that the marginal to satisfactory performance of the transition impact component at sector level is due to policy and business environment factors beyond the reach of Bank staff and TC programme recipients (see Annex 3).

Page 7 of 13 Belarus SME/MSE credit lines (TC)

5. TRANSITION IMPACT AND ADDITIONALITY 5.1 Impact at corporate level The impact at corporate level is felt in the areas of skills transfer and new standards for business conduct that strengthened existing credit lines to SME and to a much larger extent created new MSE lending opportunities. The EvD mission visited three private banks which have not yet received any assistance but might be eligible to participate in an expanded MSE lending programme. The mission noted significant differences in lending experiences and practices between these banks and those which did receive TC support.12

The assistance delivered in TC1 and TC4 for SMEs was very valuable for the know-how transfer through the formal seminars held by the consultants and on the job training during actual project evaluation by the PBs. The PBs gained theoretical and practical knowledge of project evaluation and financial modelling. The exposure of the banks to the western-style approach in project evaluation helped to ensure transparency of operations and the introduction of sound banking principles. The PBs applied the knowledge not only to the SME line of credit, but to the procedures, which have become part of their own standards of financing. The activities carried out by the consultants from the beginning of the assignment have assured the transfer of high standard banking skills to the PBs and the PMU, contributed to the further improvement of the PBs’ project appraisal and monitoring procedures, and facilitated the financing of bankable SME projects. These efforts to improve the credit functions contributed to transforming the PBs into sounder commercial banks. In the same way, the training and institution building assistance for MSE lending starting from TC2 and ending with TC9 have resulted in a substantive transfer of know-how and expertise to PBs’ local bank staff. Already with TC3, the training had generated higher productivity in the loan process through delegation of authority to departments/branches and the creation of MSE lending working groups, which later became MSE lending departments. New loan officers were recruited both within and outside PBs and trained in similar projects in Russia and were exclusively involved in MSE lending activities. While the level of lending operations was satisfactory at head office, lending operations through branches were at times constrained by the availability of training and distant monitoring with only one consultant on the ground. The transition impact at corporate level is rated as good. 5.2 Impact at sector and national levels The impact of TC at sector and national levels is closely related to the degree of the ‘presence’ of the new MSE lending programme in Belarus, measured by its scale of activity. The micro-lending programme started from a zero base a few years ago and expanded relatively fast. The cumulated number of loans committed, however, remains small compared with the size of the client base of micro entrepreneurs in Belarus.13 This tends to 12 The banks that received TC could show a substantive comparative advantage at least in two areas directly related to the assistance received: (i) the large extent and degree of application of knowledge in client pre-screening procedures, loan information and analysis, financial ratios and effective conduct of client interviews; and (ii) the presence of a new business attitude noted by the increased comfort level with the overall loan process, a better understanding of responsibility for the results vis-à-vis the goals of the bank, as well as an increased ability to work as a team. 13 The lending programme and its associated TC grew to a cumulated number of 5,167 loans up to September 2006, while the client base is estimated at 187,000 small and micro entrepreneurs in Belarus.

Page 8 of 13 Belarus SME/MSE credit lines (TC)

limit the impact of the TC programme ‘at sector level’. Nevertheless, some structural impact has occurred within the financial sector of Belarus through additional competition, further market expansion, a new regulatory framework for microfinance, skills transfer beyond the PBs, and emerging new business practices to lend effectively to small business customers. Market expansion. The TCs have been doing more than supporting a lending activity. They created a new lending activity and a new client base through a know-how transfer of procedures and skills. It provided a framework, monitoring devices and quality control to a new category of loan in the PBs. The transition impact of the TC8 and TC9 project is intrinsically linked to the impact of the investment project. The scale of the micro-lending operation and its associated TC, however, remained low when assessed at sector level. This has considerably limited the market expansion effect. Frameworks for markets. The transition impact stems from the positive results of the policy dialogue with the NBB started under TC5 and pursued in TC8 and TC9. The cooperation with NBB has been relatively productive. New regulatory measures ranged from foreign exchange decontrol to freeing interest rates and streamlining lending procedures for MSE lending. The measures had a spill-over effect on the whole banking sector of Belarus. The project in TC8 was helpful in maintaining policy dialogue with the Belarussian authorities on the elimination of obstacles for efficient SME/MSE lending. However, a number of major issues remain: cumbersome procedures in enterprise registration, licensing and permits, unplanned tax inspections, frequent changes in legislation,14 and price controls. Costs remain unusually high for loans below US$ 10,000 due to still excessive documentation and registration requirements beyond the PBs’ control. Skills transfer. The activities carried out by the consultants in TC6 from the beginning of the assignment have assured the transfer of high standard banking skills to the PBs and the PMU, contributed to further improvement of the PBs’ project appraisal and monitoring procedures and facilitated the financing of good quality MSE projects.15 But so far apparently little of that has spread into the public sector banks and other private banks. Potential demonstration effects. The pilot micro-lending programme has shown the ability and willingness of participating banks to focus on the MSE target group via institution building and training measures. The programme can further demonstrate to other banks that lending to the MSE niche is commercially viable and therefore encourage other banks to enter the market, improving the overall level of financial services provided to Belarus entrepreneurs. The assistance given in TC7 and TC8 further enhanced the design of the pilot programme to offer a complete package that can be implemented on a larger scale to private local banks. The demonstration effects were also triggered by an active marketing campaign of the Bank staff to potential client banks. These effects, however, have been hampered by the persisting adverse business environment and legal restrictions.

14 The legislation regarding small business has been continuously changing at three levels: Civil Code, Tax Code and Corporate Law. 15 The activities carried out by the consultants in TC3 to TC9 have assured the transfer of high standard of MSE lending skills including the loan analysis, monitoring, work-out procedures and marketing. More than 100 members of the management and credit staff have been trained under TC3-TC9, of which 50 per cent is retained within the framework and another 20 per cent continues to work in the Belarussian banking sector.

Page 9 of 13 Belarus SME/MSE credit lines (TC)

New standards for business conduct. While the TC programme provided the PBs with some protection from the government’s interference and generated more commercially oriented behaviour on the part of potential borrowers, the relative segmentation of the private sector banking in Belarus did not allow these benefits to spread beyond the PBs to other private banks and public banks. 5.3 Risks to transition The major risk for the project and all related TC projects implementation has been the high uncertainty and slow pace of economic reforms pursued by the government of the Republic of Belarus. Although international pressure and the demands of the Union Treaty with Russia have brought some positive, albeit very gradual, changes (foreign exchange rate unification, liberalisation of foreign exchange market), the government has yet to generate tangible improvements in the country’s economy and prove its commitment to reforms. To mitigate this risk, the Bank has been constantly involved in policy dialogue with the government and carefully monitors the performance of both PBs and SMEs in order to identify any emerging or potential problems including those which could jeopardise successful implementation of the TC projects. The impact of the policy dialogue remains limited to the immediate boundaries of the MSME programme. In addition, the progress, while significant, has been relatively slow. It takes time to process even limited legal changes in Belarus because the clearance process of the Belarus authorities, including at some point parliament and presidential administration, is currently slow. Instructions to cooperate from high levels of governments on these matters do not permeate easily to the lower levels of the public administration. While the realised transition impact at sector level has been marginal so far, the remaining potential for transition is more promising and therefore rated satisfactory. When considering the combined results of the various components at corporate and sector levels the overall transition impact of the programme is rated as satisfactory. 5.4 Additionality

Already under TC1, the borrower and the PBs were fully aware of the unwillingness of the Western donor community to offer grants to Belarus in support of small business. Therefore the funding obtained with repeated efforts from TC2 to TC9 was highly regarded by the borrower and PBs.. The relative scarcity of the funds, however, made it difficult to leverage them with the additional on-lending funds which were to mobilise donor funds to continue successful implementation of MSE lending and the associated institution building. Additionality is rated as verified in full.

5.5 Environment The national catastrophe of Chernobyl and its impact on Belarus made the country acutely aware of environmental issues. Therefore the transactions of the banking sector have incorporated all the necessary safeguards against environmental damages in the projects they finance and the related TC. The safeguards are strictly enforced by the authorities.

Page 10 of 13 Belarus SME/MSE credit lines (TC)

6. BANK PERFORMANCE The Bank adopted a highly participatory approach to the design and implementation of the projects and related TCs for SMEs. In the TC1 and TC4 assistance, the PBs and PMU participated in the TOR drafting and consultants’ selection. Specific TORs were prepared for each consultant visit to address the specific needs of the project. The outcome of the assignment was discussed with the PMU and the PBs. The client was then fully committed to the project. The information was submitted in a timely manner. The counterparts for the project were duly appointed and available throughout the project implementation. The consultants’ knowledge of the project and experience in similar projects in other CIS countries was helpful and enabled them to work in an efficient manner. Their relationship with the Bank and the clients was excellent.

By contrast, in the TC2-TC9 for MSEs it was believed that intermediary involvement could dilute the strong actions which are often required when the consultant must achieve successful institution building for MSEs. The Bank then contracted directly with the consultant.16 This was to minimise the potential for government interference17 and maintain strict control over the programme.18 The consultant was receptive to the lessons learned in similar EBRD assignments and information flowed well between the EBRD and the consultant. Since the consultant was acting individually and there was no backstopping support from a management of a consultancy firm, his assignment was closely monitored by the EBRD and the operation team provided extensive input for bank institution building and staff training. The donor’s role was highlighted in press conferences. Most of the public documents of the pilot programme were mentioned the donor’s special initiative. In addition, joint receptions on the occasion of the launch of micro lending component were held in Minsk, during which donor visibility was ensured. To be successful in Belarus, the policy dialogue had to be carried out at early stages of the Bank’s operations, handled with equal strength at both high and lower levels of the government, and coordinated with other IFIs. While many aspects of the policy dialogue are effectively handled when decentralised, the role of Bank senior management is determinant to generate a critical level of government commitment and public administration compliance to apply the new policies. TC is an on-going requirement in Belarus. Country, sector, and top management have been aware of it and were actively involved in the policy dialogue to ensure that proper change of the legislation could be obtained in a timely manner. Through a limited number of visits to Belarus,19 senior management was able to hold high level meetings with the government to discuss the reform issues and related issues. Senior management also coordinated with other international institutions. It participated in FIAC meetings,20 carried correspondence and

16 The PBs were not involved in the preparation of the TOR design, consultation selection and implementation. 17 Actually, government intervention did not occur in the process. 18 The consultant had failed to deliver the monthly lending statistics for November 2001 and consequently the fees for the corresponding month were withheld. 19 The reduced number of official visits mainly reflects the limited overall activity of the Bank in Belarus as a result of lack of compliance of the current government with the principles of Article I of the Agreement Establishing the Bank and the related Board guidance. 20 The Bank cooperates closely with the IFC on investment climate issues discussed in FIAC forums.

Page 11 of 13 Belarus SME/MSE credit lines (TC)

handled coordination meetings with the European Community.21 Country and sector management continue to meet on a regular basis with local embassies and Directors of the EBRD Board, and attend meetings in Brussels for the purpose of further developing the policy dialogue. Overall the Bank performance is rated as good. 7. KEY ISSUES AND LESSONS LEARNED In this particular business environment of the overwhelming presence of the public sector, the government incentives are naturally oriented to support and develop operations in publicly owned enterprises and public procedures are slow and cumbersome. The SME and MSE programmes must therefore be designed to protect the programme from the downward risks that this type of environment tends to create. The ultimate success of the TC depends on the PBs’ ability to sustain MSE lending operations after the TC is completely phased out. This particular challenging situation tends to be more demanding for the Bank and the donors in terms of financial and time commitments, project staff and consultant qualifications, forceful policy dialogue, and quantity and quality of project monitoring, than for similar projects in more liberalised economies. It requires a unique combination of well targeted commitments, talents and financial resources. 7.1. TC project design and implementation 7.1.1 Listening to the client. It was essential to discuss the design of the SME projects and obtain input from PBs and the NBB at the TOR preparation stage to address their needs. In order to ensure the most cost-effective use of funds, the staff from the Headquarters, the Resident Office and the local consultants were actively involved. Lesson: The client is to be involved in project design. Participation of stakeholders in project design is a key factor of the programme’s effectiveness for SME lending, especially in a difficult business environment. 7.1.2 Finding resources for the entire duration of the TC programme. One precondition for sustained impact was a continuous and thorough training of staff in the partner banks. It was therefore absolutely necessary to keep finding donor resources to support the continuity and quality in the MSE training programmes. The Bank staff recognised openly the problem and addressed it at high management levels which reacted positively in proposing to use part of Bank profit for cases like Belarus. In addition, the Bank at critical times provided bridge financing out of its own consultancy budget. Lesson: TC financing as a subsidiary function for the Bank. When operating in an environment where donors are not in favour of providing grants for TC, the Bank should be more entrepreneurial than usual and not hesitate to provide complementary financing when necessary. The subsidiary function of the Bank in that case is vital.

21 The policy work and coordination with other IFIs performed by senior management is not reflected in the TC reports, but documented in Bank correspondence and BTORs.

Page 12 of 13 Belarus SME/MSE credit lines (TC)

7.1.3 What happens when very few project counterparts speak English. The staff of local banks had little or no exposure to Western methods in MSE lending which are usually diffused by consultants in the English language. It was therefore essential to tailor the programme to specific local expertise requirements and the level of knowledge in foreign languages and find consultants who could meet these requirements. Lesson: Find consultants that speak the national language. When TC project recipients have initially little knowledge of advanced lending management techniques and do not speak English well, the Bank should be proactive in finding qualified and competent consultants that speak fluently the local language, rather than relying on highly qualified international consultants that may have great experience but do not have easy contact in the field. 7.1.4 Potential conflict of interest of advisers who also clear project applications. In both SME and MSE projects, the adviser who helped establish procedure and train local staff was also acting upon representing the interests of the EBRD. In the context of Belarus, this is well understood, because initially qualifications of local staff were inadequate and there was a high risk of government interference. In principle, however, this arrangement tends to reduce the level of commitment and accountability of local staff because the presence of an ‘outside controller’ is a form of guarantee that the project is bound to work. In addition, because of the potential conflict of interests of the ‘adviser’ being also ‘controller’ in spite of protective contractual statements, the adviser could be held de facto accountable by the client on loan failures. Lesson: Separate advisory from control functions. If for some well understood practical reasons the adviser and the controller are one person, at the beginning of a TC programme for MSE lending in order to put the programme on the right track, the separation of the two functions must be implemented as soon as possible. In this way (i) accountability is not blurred and (ii) we can trace out better the advisory impact of TC as compared with the impact of corrective actions as a result of client (or EBRD) due diligence.22

7.1.5 How long the Bank should support TC in a project that does not perform well. For a while the focus was on SMEs. Then after six years, when it was discovered that lending activity was very slow, the focus shifted onto MSEs. TC money was spent without expected impact for a while until it was reoriented to the MSE programme.23 Lesson: Quickly react to market signals. The Bank should be prompt and pragmatic in reacting when the underlined lending activity of the TC programme does not work as well as expected. One reaction could be to switch the TC support to a more dynamic and profitable lending category, such as moving from SME to MSE lending in this case. 7.2 Sector policy dialogue 7.2.1 The best time to carry the policy dialogue. The TC project had a long gestation period 22 Some changes in this direction are already happening in the current TC programme. The MSE consultant is still sitting on the loan committee but a lot of delegation is already operating for small amounts. In every region at least one loan officer can make decisions alone. On other occasions a mini local loan committee of two persons is put in charge of decision-making. 23 The Bank’s management notes that when the disbursement under the SME line of credit slowed down, the Bank restructured the TC funds’ utilisation: instead of having permanent credit advisers for each participating bank, the level of TC was reduced such that one credit adviser provided assistance to all participating banks.

Page 13 of 13 Belarus SME/MSE credit lines (TC)

due to the difficult macroeconomic and political situation in Belarus. In spite of all the considerable efforts undertaken by management and staff, the impact of the policy dialogue remains limited to the immediate boundaries of the MSME programme. In addition, the progress, while significant, has been relatively slow. Lesson: Carry the policy dialogue ahead of the project. In difficult business environments, it appears more effective to front load the technical assistance for the policy dialogue before starting an operation, in addition to developing it while the operation is being implemented. 7.2.2 The extent to which the policy dialogue should be recorded. The EvD team did not find clear indications of policy dialogue either in PCRs or progress reports, or in project files available at the headquarters. It was only during the EvD mission in Belarus in November 2006 that serious initiatives and tangible results were found in detail. Lesson: Regularly document progress in policy dialogue. No matter how delicate and confidential the policy dialogue is, it should be regularly documented and disclosed in one way or another, so that its progress can be assessed by the relevant stakeholders on its content and timing, and corrective actions can be taken. Finding niches where the EBRD can both channel investment funds and TC with an ad hoc policy dialogue does not free the Bank from seeking higher and more intensive policy dialogue that could further strengthen the TC programme. Sooner or later the programme will need to expand beyond the boundaries of the niche and that could not be done without dialogue beforehand to prepare the ground for more changes. 7.2.3 Sharing the policy dialogue with other IFIs. Past and current sector policies in Belarus appear to provide a strong relative advantage to public banks’ lending to SMEs. Belarus is certainly not the only case among the countries at early stages of transition, and there is well known acquired experience on the matter. The EvD mission found little evidence, either at headquarters or in the field, of significant consultation with the other IFIs that would lead to a common action in the field.24 Lesson: Common dialogue among IFIs should lead to well targeted common policy recommendations. Given the magnitude of the reforms required in a low transition country to move to a full market economy and the apparent inertia within the system to do so, it is hardly conceivable that one IFI alone would be capable of breaking the ground in opening the door alone to reforms in the financial sector. More consultation and coordination is seriously needed. The best way to begin would be create a systematic coordination among IFI Resident Offices in Minsk. Soon or later these initiatives would need to be supported by the Headquarters of each IFI to produce and negotiate common recommendations.

24 The Bank’s management notes that this co-ordination was not part of the TC assignment under evaluation and was not therefore documented in any TC project-related literature. However, the results of the policy dialogue achieved and noted in the OPER over a number of years with the government of Belarus speak for themselves. The fact that the EBRD has a strong presence at the FIAC and is invited to the Advisory Counsel of UNDP’s microfinance project in Belarus, where the Bank has been actively involved and has advised the project in its preparation stages, is additional evidence of an on-going process of cooperation. Finally, the Bank’s initiative that was started in 2006 to establish a microfinance bank with IFIs active in Belarus speaks of the close coordination on this front.

APPENDIX 1

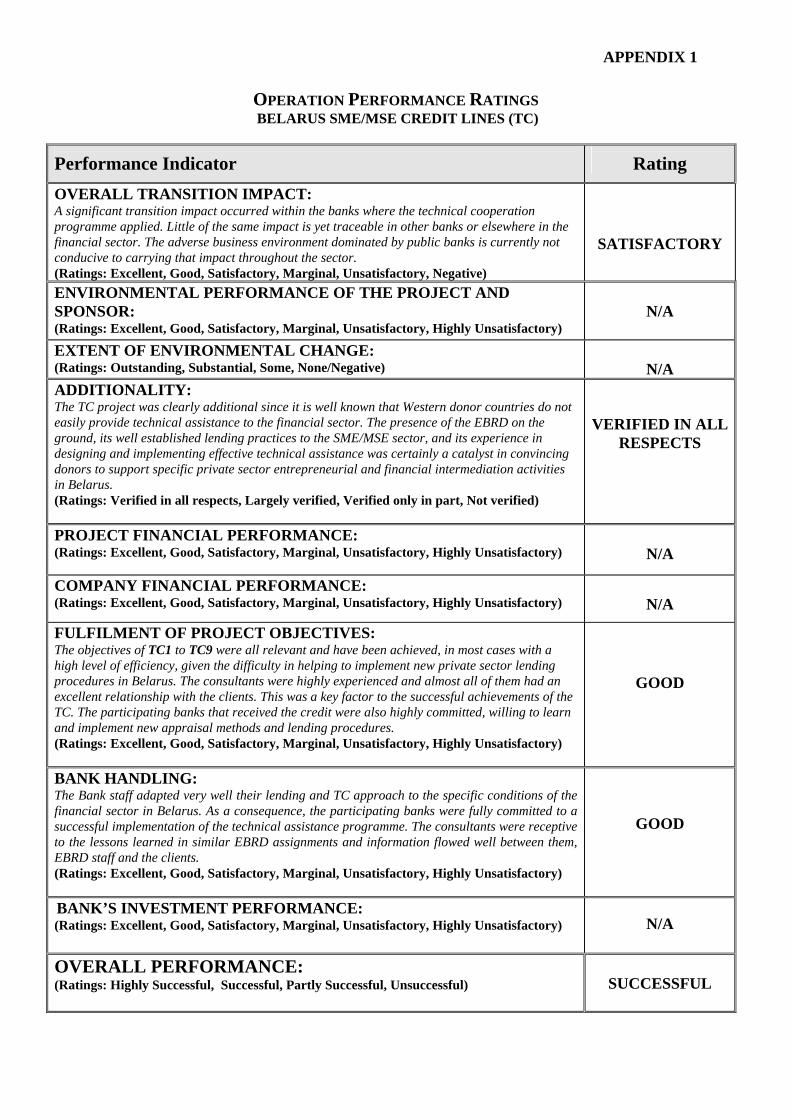

OPERATION PERFORMANCE RATINGS BELARUS SME/MSE CREDIT LINES (TC)

Performance Indicator

Rating OVERALL TRANSITION IMPACT: A significant transition impact occurred within the banks where the technical cooperation programme applied. Little of the same impact is yet traceable in other banks or elsewhere in the financial sector. The adverse business environment dominated by public banks is currently not conducive to carrying that impact throughout the sector. (Ratings: Excellent, Good, Satisfactory, Marginal, Unsatisfactory, Negative)

SATISFACTORY

ENVIRONMENTAL PERFORMANCE OF THE PROJECT AND SPONSOR: (Ratings: Excellent, Good, Satisfactory, Marginal, Unsatisfactory, Highly Unsatisfactory)

N/A

EXTENT OF ENVIRONMENTAL CHANGE: (Ratings: Outstanding, Substantial, Some, None/Negative)

N/A

ADDITIONALITY: The TC project was clearly additional since it is well known that Western donor countries do not easily provide technical assistance to the financial sector. The presence of the EBRD on the ground, its well established lending practices to the SME/MSE sector, and its experience in designing and implementing effective technical assistance was certainly a catalyst in convincing donors to support specific private sector entrepreneurial and financial intermediation activities in Belarus. (Ratings: Verified in all respects, Largely verified, Verified only in part, Not verified)

VERIFIED IN ALL RESPECTS

PROJECT FINANCIAL PERFORMANCE: (Ratings: Excellent, Good, Satisfactory, Marginal, Unsatisfactory, Highly Unsatisfactory)

N/A

COMPANY FINANCIAL PERFORMANCE: (Ratings: Excellent, Good, Satisfactory, Marginal, Unsatisfactory, Highly Unsatisfactory)

N/A

FULFILMENT OF PROJECT OBJECTIVES: The objectives of TC1 to TC9 were all relevant and have been achieved, in most cases with a high level of efficiency, given the difficulty in helping to implement new private sector lending procedures in Belarus. The consultants were highly experienced and almost all of them had an excellent relationship with the clients. This was a key factor to the successful achievements of the TC. The participating banks that received the credit were also highly committed, willing to learn and implement new appraisal methods and lending procedures. (Ratings: Excellent, Good, Satisfactory, Marginal, Unsatisfactory, Highly Unsatisfactory)

GOOD

BANK HANDLING: The Bank staff adapted very well their lending and TC approach to the specific conditions of the financial sector in Belarus. As a consequence, the participating banks were fully committed to a successful implementation of the technical assistance programme. The consultants were receptive to the lessons learned in similar EBRD assignments and information flowed well between them, EBRD staff and the clients. (Ratings: Excellent, Good, Satisfactory, Marginal, Unsatisfactory, Highly Unsatisfactory)

GOOD

BANK’S INVESTMENT PERFORMANCE: (Ratings: Excellent, Good, Satisfactory, Marginal, Unsatisfactory, Highly Unsatisfactory)

N/A

OVERALL PERFORMANCE: (Ratings: Highly Successful, Successful, Partly Successful, Unsuccessful)

SUCCESSFUL

APPENDIX 2

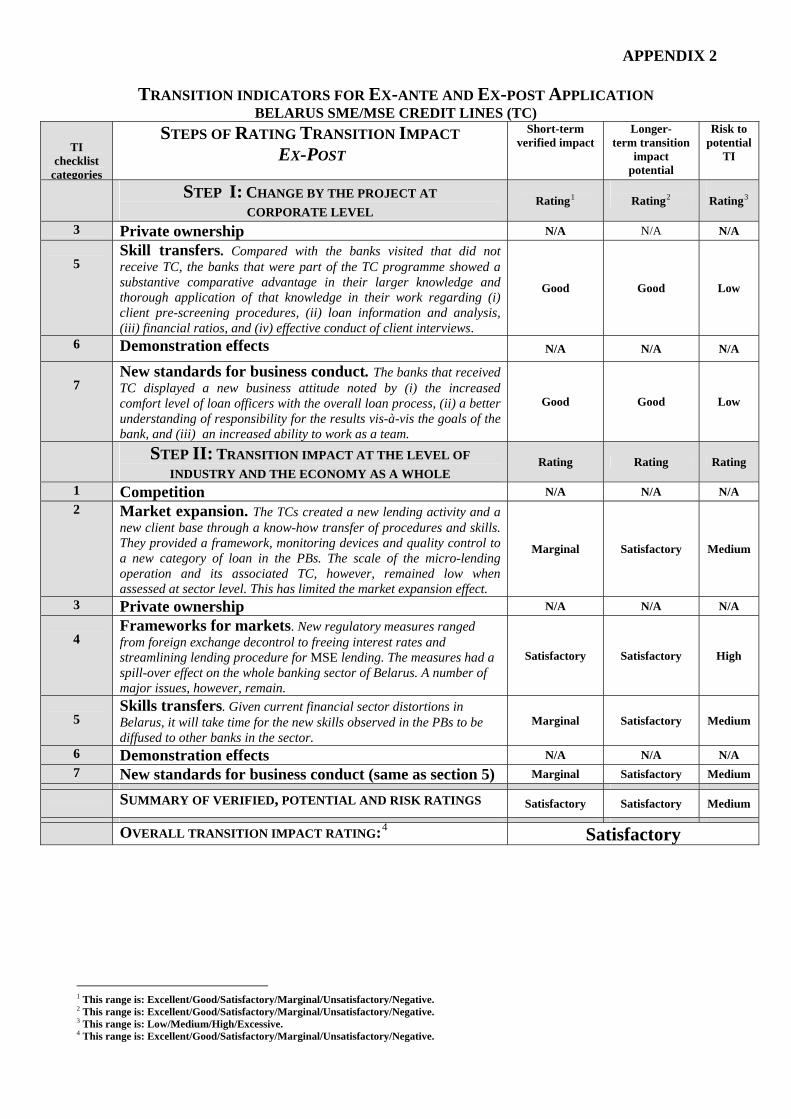

TRANSITION INDICATORS FOR EX-ANTE AND EX-POST APPLICATION BELARUS SME/MSE CREDIT LINES (TC)

TI

checklist categories

STEPS OF RATING TRANSITION IMPACT EX-POST

Short-term verified impact

Longer- term transition

impact potential

Risk to potential

TI

STEP I: CHANGE BY THE PROJECT AT CORPORATE LEVEL

Rating1

Rating2

Rating3

3 Private ownership N/A N/A N/A

5 Skill transfers. Compared with the banks visited that did not receive TC, the banks that were part of the TC programme showed a substantive comparative advantage in their larger knowledge and thorough application of that knowledge in their work regarding (i) client pre-screening procedures, (ii) loan information and analysis, (iii) financial ratios, and (iv) effective conduct of client interviews.

Good Good Low

6 Demonstration effects N/A N/A N/A

7

New standards for business conduct. The banks that received TC displayed a new business attitude noted by (i) the increased comfort level of loan officers with the overall loan process, (ii) a better understanding of responsibility for the results vis-à-vis the goals of the bank, and (iii) an increased ability to work as a team.

Good Good Low

STEP II: TRANSITION IMPACT AT THE LEVEL OF INDUSTRY AND THE ECONOMY AS A WHOLE

Rating Rating Rating

1 Competition N/A N/A N/A 2 Market expansion. The TCs created a new lending activity and a

new client base through a know-how transfer of procedures and skills. They provided a framework, monitoring devices and quality control to a new category of loan in the PBs. The scale of the micro-lending operation and its associated TC, however, remained low when assessed at sector level. This has limited the market expansion effect.

Marginal Satisfactory Medium

3 Private ownership N/A N/A N/A

4 Frameworks for markets. New regulatory measures ranged from foreign exchange decontrol to freeing interest rates and streamlining lending procedure for MSE lending. The measures had a spill-over effect on the whole banking sector of Belarus. A number of major issues, however, remain.

Satisfactory Satisfactory High

5

Skills transfers. Given current financial sector distortions in Belarus, it will take time for the new skills observed in the PBs to be diffused to other banks in the sector.

Marginal Satisfactory Medium

6 Demonstration effects N/A N/A N/A 7 New standards for business conduct (same as section 5) Marginal Satisfactory Medium

SUMMARY OF VERIFIED, POTENTIAL AND RISK RATINGS Satisfactory Satisfactory Medium

OVERALL TRANSITION IMPACT RATING:4 Satisfactory

1 This range is: Excellent/Good/Satisfactory/Marginal/Unsatisfactory/Negative. 2 This range is: Excellent/Good/Satisfactory/Marginal/Unsatisfactory/Negative. 3 This range is: Low/Medium/High/Excessive. 4 This range is: Excellent/Good/Satisfactory/Marginal/Unsatisfactory/Negative.