Entrepreneurship Series Review of Week 1. Many Types of Businesses Some Make or Grow things.

date post

20-Dec-2015Category

view

217download

0

Smart Policy for Innovative Regions

Grow your own

Entrepreneurship and business development

Startups and Entrepreneurship

Con High risk, high

failure per attempt

Can be resource intensive

Lack collateral for traditional finance

Pro Sticky Increasing returns

to scale High payoff

potential

Transforming Ideas Into New Companies

New Companies are transformed through a five stage transformation process to create a sustainable company – Start-Up Life Cycle

Each stage of the Start-Up Life Cycle represents the companies progressionof the business, management team, products (technology), markets, etc.

Discovery IdeaDevelopment

Start-UpCompany

EarlyGrowth

RapidGrowth

Increasing Costs / Effort

The Fore Systems Family Tree:The Region’s Economic Future

From 0 to 1500 jobs in 12 years, but the

region missed out on another 300+ jobs

that got away

Transarc / IBM Pittsburgh

1989 / 1999Laminar

1999

Spinnaker1999

FORE Systems / Marconi Networks

1990 / 1999Laurel

Networks1999

Comanage1998

CarnegieMellon

Mediasite1996

PanasasOpsware

LighteraNetworks

OnFiberCommunications

InFineraCorporation

WaveSmithNetworks

AcceLight

Legend

People

Tech

BothMoney

Sold

Missed

Closed

ScalableNetworks

The Picture of Success: San Diego 1980 - 2000

Hybritech

G e n sia1 9 8 6

C o rte x1 9 8 6

Im m u n eR e s p o n s e

1 9 8 6

G e n Pro b e1 9 8 3

ID EC1 9 8 5

C lo n e tics1 9 8 5

Bio ve st1 9 8 6

Pa cR imBio s cie n ce

1 9 8 5

Via g e n e1 9 8 7

Kimme l C a n ce rIn s titu te

1 9 9 0

Lipotec h1 9 8 7

C yp ro s1 9 9 2

No va d e x1 9 9 2

L ig a n d1 9 8 7

C o rva s1 9 8 7

F o rwa rdVe n tu re s

1 9 9 0

Amylin1 9 8 7

C yte l1 9 8 7

Bio s ite1 9 8 8

Pyxis1 9 8 7

Vica l1 9 8 7

Me d me tr ic1 9 8 9

Uro g e n1 9 9 6

Birn d o rfB io te ch n o lo g y

1 9 9 0

Na n o g e n1 9 9 1

G e n e sys1 9 9 0

So ma tix1 9 9 2

Se q u a n a1 9 9 2

C o mb i-C h e m1 9 9 4

C o rixa1 9 9 4

Ap p lie dGe n e tics

1 9 9 4

Tria n g lePh a rm a ce u tica ls

1 9 9 5

G e n Q u e st1 9 9 5

Firs t Denta l Health1995

G ryp h e n1 9 9 3

C yp h e rg e n1 9 9 3

D u ra1 9 9 0

C o lu mb iaHCA1990

Kin g s b u ryPar tners

1993

C h ro ma g e n1 9 9 4

D ig iR a d1 9 9 4

No va tr ix1 9 9 4

C h u g a lPh a rm a ce u tica ls

1 9 9 5

G e n ta1 9 8 8

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

0-50 50-250 250-1000 1000 or more

Initial Employment Size in 1998

Tota

l J

ob

s C

rea

ted

1,000 + Jobs

250 to 999

50 to 249

10 to 49

Less than 10 Jobs

Amount of Gain

Large firms added few jobs

60% of the jobs were created by small firms

Small firms that become big firms are how we get sustained growth

Technology Job Creation and Destruction, by Age of Firm, 1998-2002

-8,000

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

Firms more than 40 years old Firms less than 10 years old

Younger technology firms are the region’s growth drivers

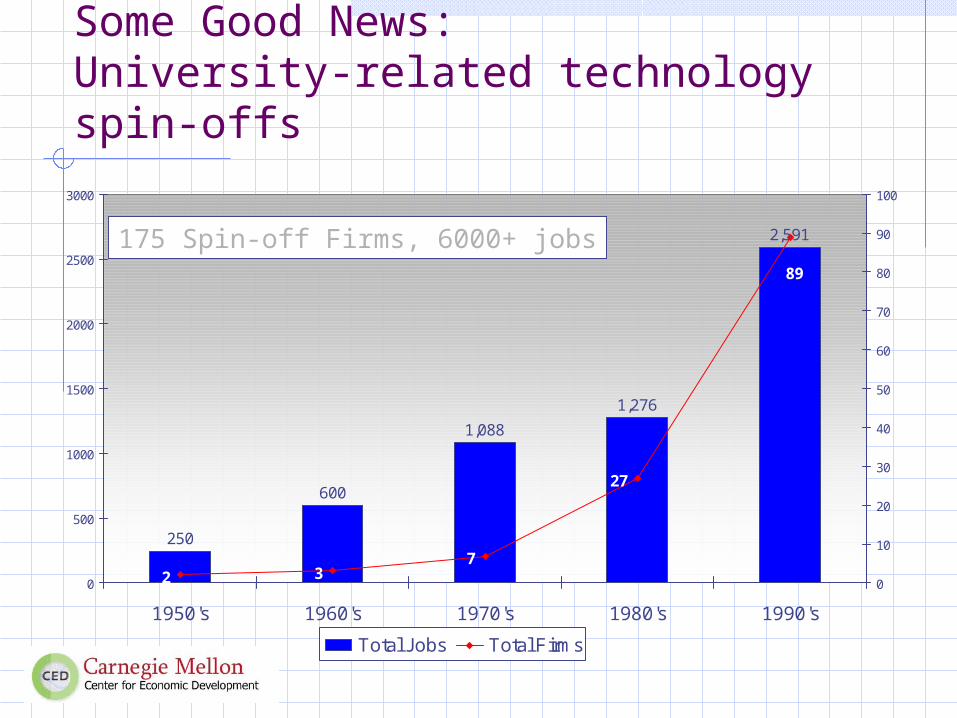

Some Good News:University-related technology spin-offs

250

600

1,088

1,276

2,591

2 37

27

89

0

500

1000

1500

2000

2500

3000

1950's 1960's 1970's 1980's 1990's

0

10

20

30

40

50

60

70

80

90

100

Total Jobs Total Firms

175 Spin-off Firms, 6000+ jobs

IT

Orbits

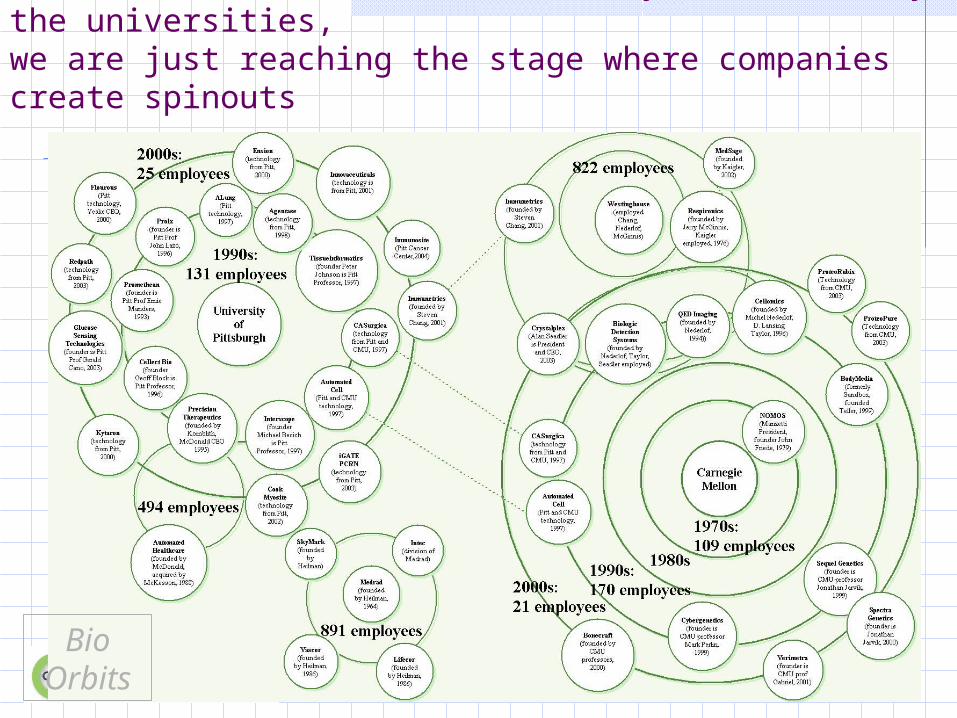

These new technology companies form “Orbits” over time, spinouts of existing companies are sustaining growth

Biotech “Orbits” have been heavily influenced by the universities,we are just reaching the stage where companies create spinouts

Bio Orbits

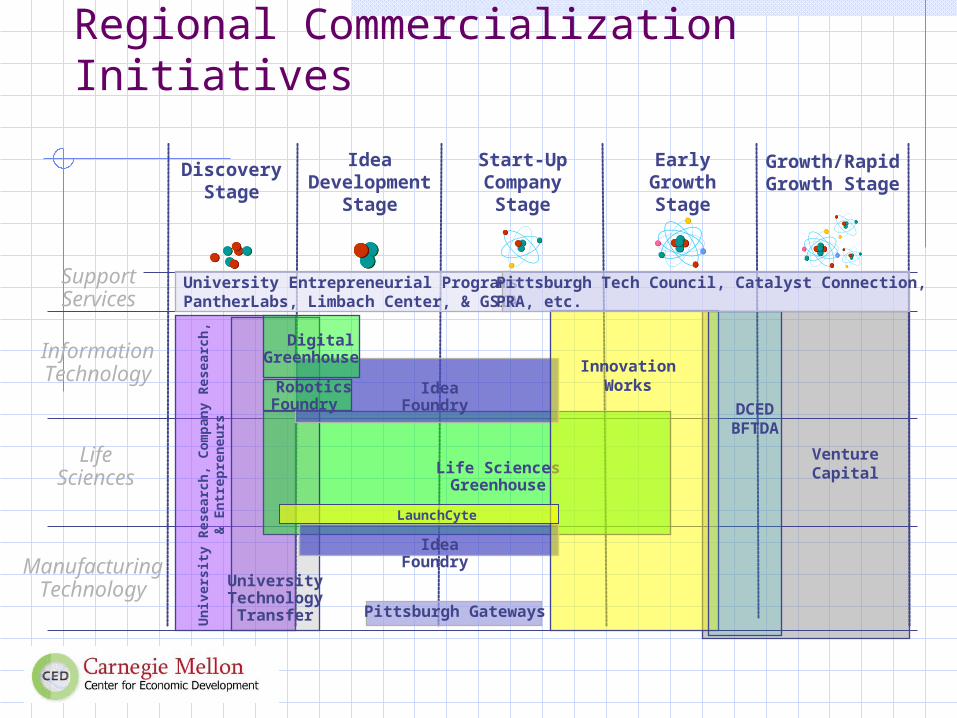

Regional Commercialization Initiatives

IdeaDevelopment

Stage

Start-UpCompany

Stage

Early GrowthStage

Growth/RapidGrowth Stage

DiscoveryStage

Life SciencesGreenhouse

Digital Greenhouse

Idea Foundry

Idea Foundry

InnovationWorks

Un

iver

sity

Res

earc

h, C

om

pan

y R

esea

rch

, &

En

trep

ren

eurs

UniversityTechnology

Transfer

VentureCapital

DCEDBFTDA

ManufacturingTechnology

InformationTechnology

LifeSciences

RoboticsFoundry

University Entrepreneurial ProgramsPantherLabs, Limbach Center, & GSIA

Support Services

Pittsburgh Tech Council, Catalyst Connection,PRA, etc.

Pittsburgh Gateways

LaunchCyte

Small Business Development

Business Plans – Small Business Development Centers (SBDCs) University of Pittsburgh Chrysler Center, Duquesne University St. Vincent College

Marketing Don Jones Center

Finance For StartupsFederal SBIR – Small Business Innovation

Research SBICs – Small Business Investment

Companies

State Opportunity Grants (PA) Ben Franklin Partners – Innovation Works

Venture Capital

Only ¼ is from Local Capital

Locations of Firms Funding Pittsburgh Biotech Companies, 1982-2001

Bergen-Passaic, NJ 3%

Boston, MA-NH 14%

Chicago, IL 5%

Hartford, CT 3%

Little Rock-North Little Rock, AR 3%

Minneapolis-St. Paul, MN-WI 3%

New York, NY 5%

Philadelphia, PA-NJ 8%

Pittsburgh, PA 26%

San Francisco, CA 19%

Rochester, MN 3%

Allentown-Bethlehem-Easton, PA

5%

Middlesex-Somerset-Hunterdon, NJ

3%

1996-2000 Venture Capital Flows IN and OUT of Pittsburgh

-$150 -$100 -$50 $0 $50 $100 $150 $200 $250 $300 $350 $400

DC

Unknown

Allentown

MD

OH

IL

CT

CO

NY

NC

NJ

VA

MA

FL

TX

CA

Other

P ittsburgh

Lo

cati

on

of

Ven

ture

Rec

ipie

nts

Amount of Investment ($ Mil)

IN OUT

Source: Venture Economics

Venture Capital Flows

Business Finance Quiz

$21 Billion

$135 Billion

$240 Billion

$9.9 Trillion

Federal contracts & procurement

Federal R&D funds

US business and consumer spending

Venture capital investment

Mentoring

Comprehensive Idea Foundry Launchcyte Innovation Works

Targeted Don Jones Center Duquesne / Chrysler SBDC

Networking

General Chamber or Tech Council Business association

Industry focused IT Network

Professional Focused CEO or CFO network, HR Assoc. TEC

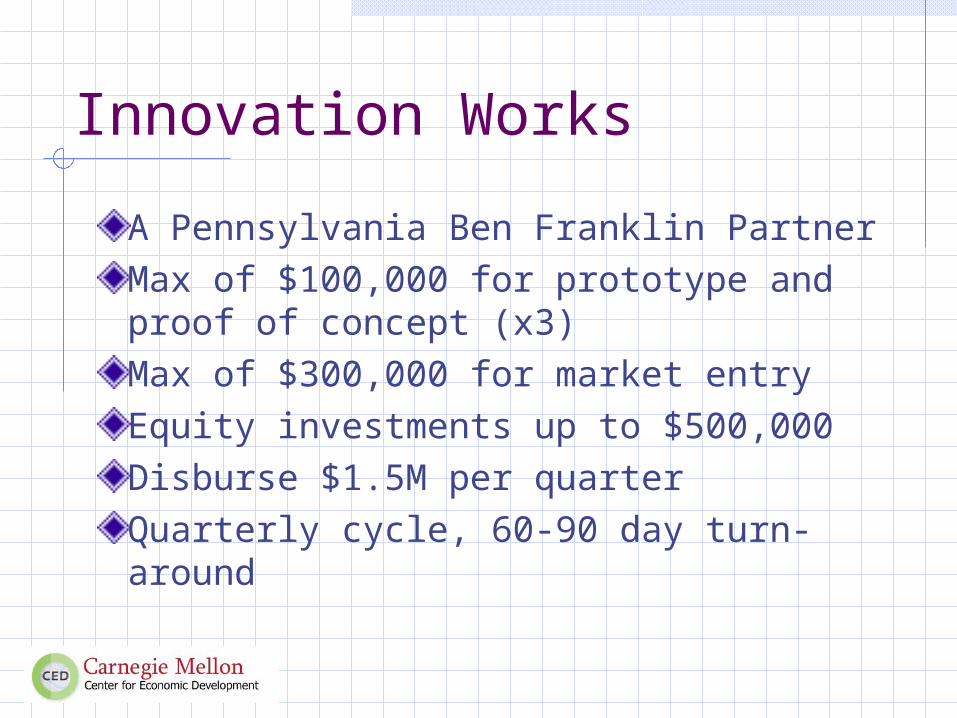

Innovation Works

A Pennsylvania Ben Franklin PartnerMax of $100,000 for prototype and proof of concept (x3)Max of $300,000 for market entryEquity investments up to $500,000Disburse $1.5M per quarterQuarterly cycle, 60-90 day turn-around

Smart Policy for Innovative Regions

Collaborating Partners

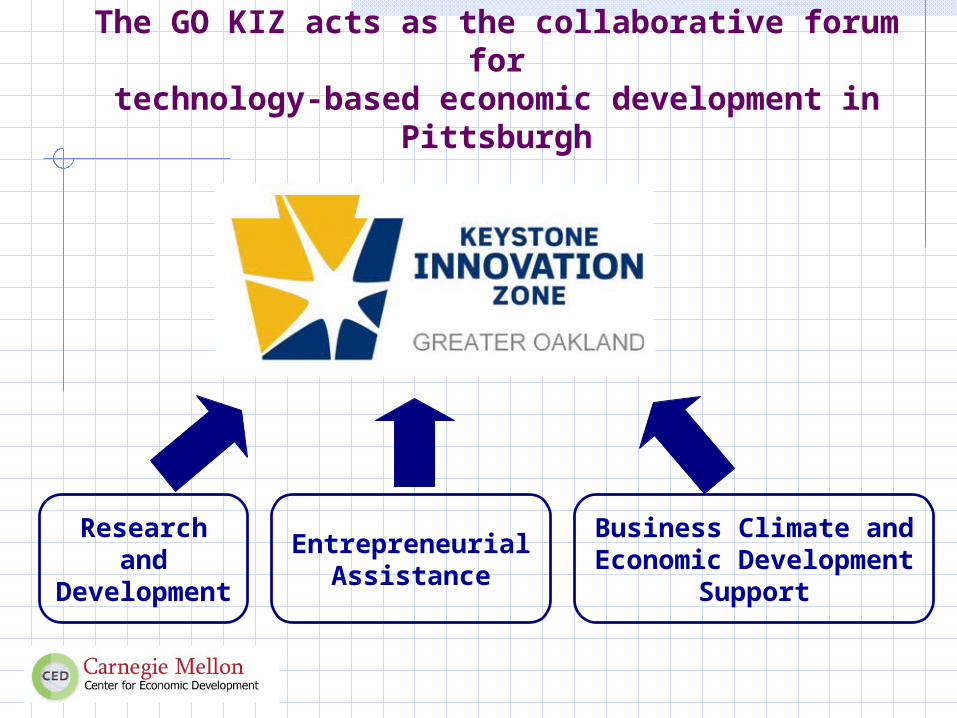

The GO KIZ acts as the collaborative forum for

technology-based economic development in Pittsburgh

Researchand

Development

EntrepreneurialAssistance

Business Climate andEconomic Development

Support

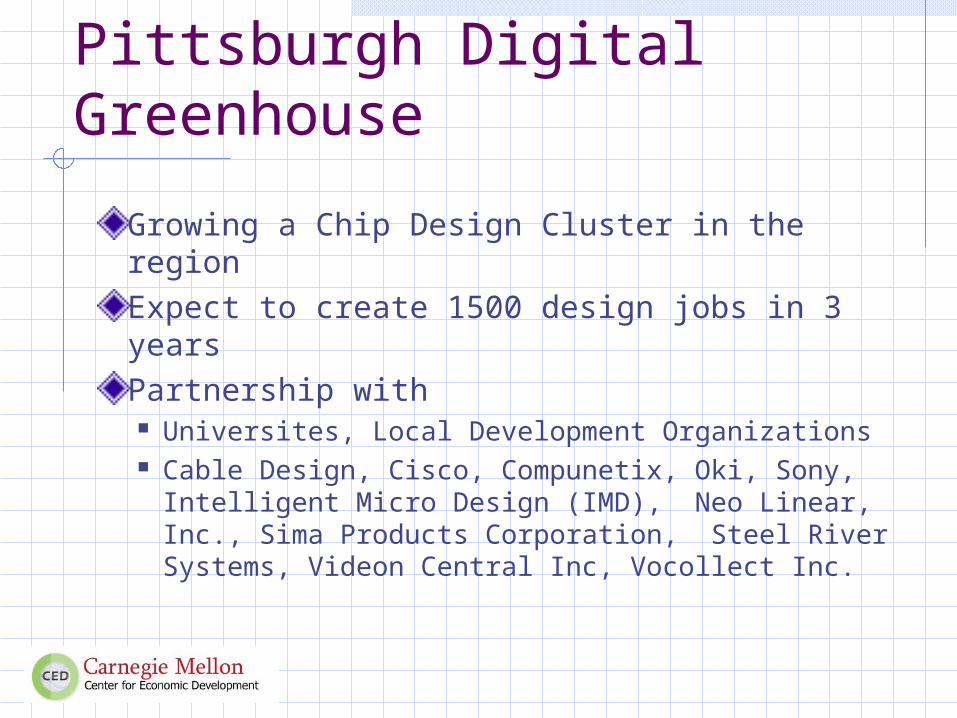

Pittsburgh Digital Greenhouse

Growing a Chip Design Cluster in the regionExpect to create 1500 design jobs in 3 yearsPartnership with Universites, Local Development Organizations Cable Design, Cisco, Compunetix, Oki, Sony,

Intelligent Micro Design (IMD), Neo Linear, Inc., Sima Products Corporation, Steel River Systems, Videon Central Inc, Vocollect Inc.

Pittsburgh Life Sciences Greenhouse

Focus on the four pillars Drug Discovery Tools and Targets Therapeutic Strategies for Neurological and

Psychological Disorders Tissue / Organ Engineering Medical Devices and Diagnostics

Programs cover ALL needs: Capital, Space, Business Expertise, Networking and Technical Assistance

©2004 Idea Foundry

24

Our bet: $5.7 million of private risk capital on local biotech

We start companies from scratch• Technology review (>100 annually)

• Application development (refocus)

• I.P. strategy (create monopoly)

• Seed funding ($150K-$500K)

• Licensing (equity up-front)

• Business development (early deals)

• Executive recruiting (top local talent)

Life. Science. Business

Our model: Taking the biggest, earliest risk

LaunchCyte

Biotech Convergence

IT joining a new wave of BiotechLeverages Region’s Life Sciences R&DCenter for Biomedical Informatics (University of Pittsburgh)Pittsburgh Tissue Engineering InitiativeBioVenture / Life Sciences Greenhouse

Intelligent Operating Room

Suite of state-of-art technologies to assist surgeons

surgical robots for minimally invasive procedures

voice-controlled ancillary equipment to decrease personnel & time

integrated at and in clinical trials at UPMC Presbyterian Hospital

Pearl - The Nurse Robot

Indoor mobile robot for elderly functions as assistant,

guardian, companion, and monitor

personality

collaborative project of Carnegie Mellon and Pitt

Example university spin-offCASurgica, Inc.

commercializing the HipNav™ surgical guidance system developed at CMU & UPMC Shadyside Hospital

Example large, established company

builds robotic pharmaceutical distribution systems and related equipment for tracking and dispensing medications

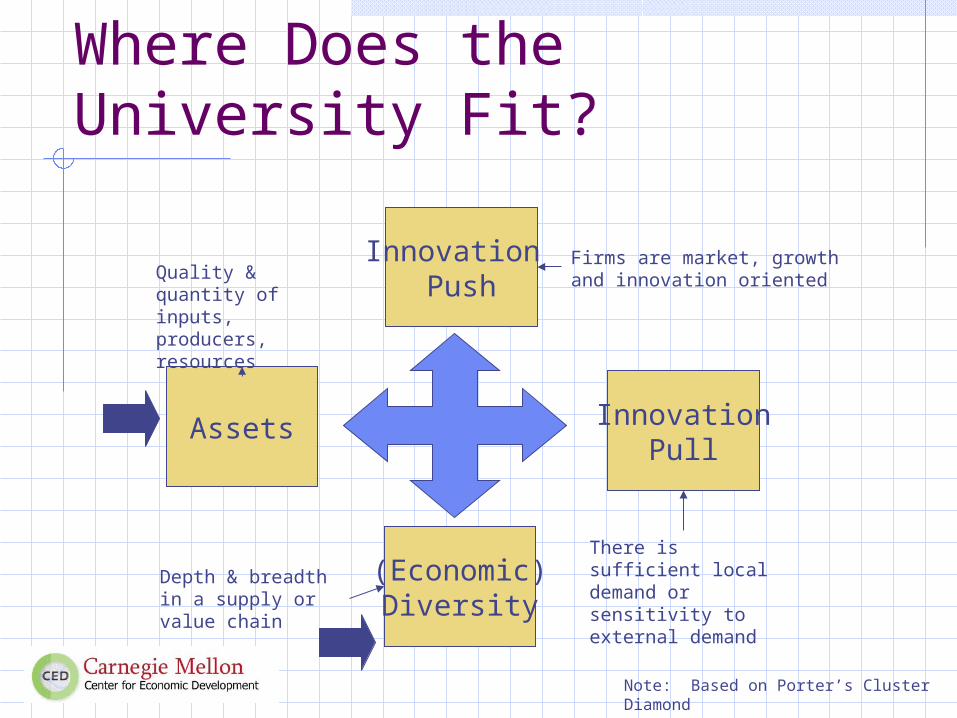

Where Does the University Fit?

Assets

Quality & quantity of inputs, producers, resources

Innovation Push

Firms are market, growth and innovation oriented

InnovationPull

There is sufficient local demand or sensitivity to external demand

(Economic)Diversity

Depth & breadth in a supply or value chain

Note: Based on Porter’s Cluster Diamond

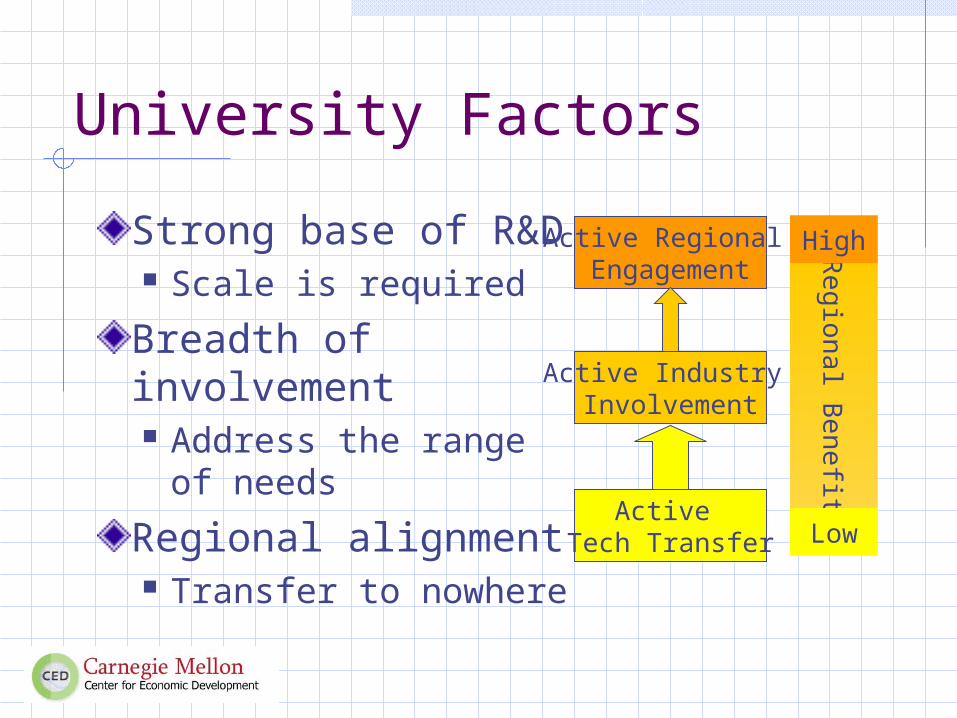

University Factors

Strong base of R&D Scale is required

Breadth of involvement Address the range of

needs

Regional alignment Transfer to nowhere

Active Regional Engagement

Active Industry Involvement

Active Tech Transfer

Regional B

enefit

High

Low

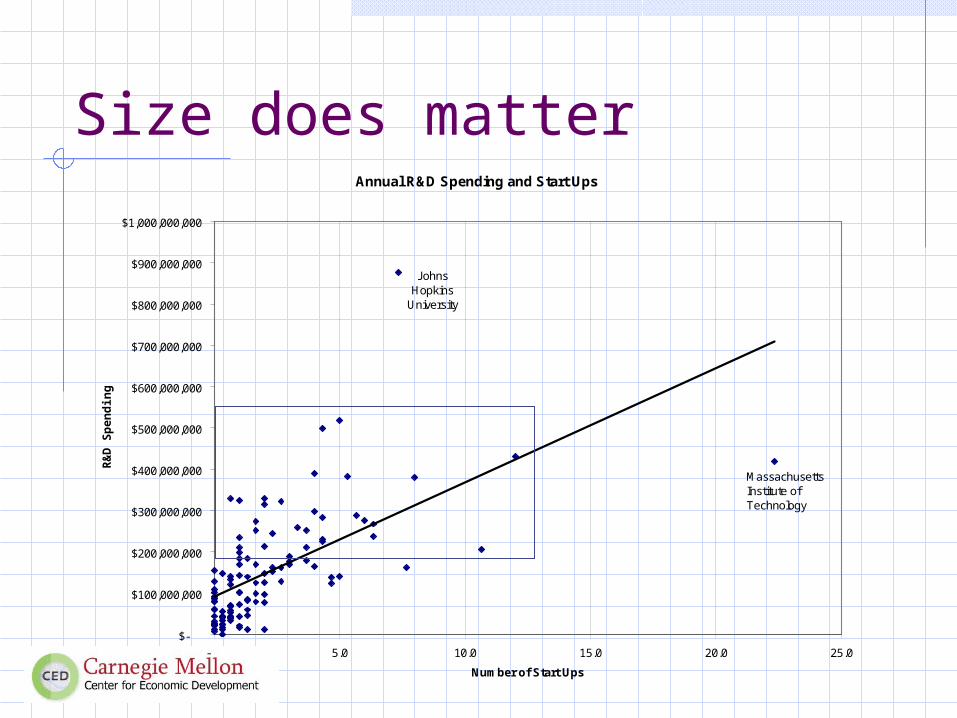

Size does matterAnnual R&D Spending and Start Ups

$-

$100,000,000

$200,000,000

$300,000,000

$400,000,000

$500,000,000

$600,000,000

$700,000,000

$800,000,000

$900,000,000

$1,000,000,000

- 5.0 10.0 15.0 20.0 25.0

Number of Start Ups

R&

D S

pen

din

g

Johns Hopkins

University

Massachusetts Institute of Technology

What’s good for the goose…

Industrial R&DLicensing incomeTechnology transfer Structure Staffing

Technology Transfer Options

Source: Gary Matkin, “Spinning off in the U.S.”, OECD Workshop on Research-based Spin-offs, 8 December 1999

Getting the most out of “U”

How many bets can you make, and how bigNot immune to the product cycle & marketBeware of false assetsWhat leverage does the university provide University provides the capacity to transform Requires broad involvement & alignment Stop the leaks and fill the gaps

Regional Impact ScorecardUniversity

State

Cluster

Market

Oriented

Innovative

Variety Region

Foc

used

Str

ateg

y

Tal

ent P

ool

Eco

nom

ic

Div

ersi

ty

Regional FocusSupport for Innovation

Effective Basic Services

R&D Base

Breadth of Involvement

Regional Alignment

High RegionalImpact

Least Critical

Most Critical