Slide 5-1 Tax Treatment of Vacation and Second Homes CHAPTER 5.

10

Slide 5-1 Tax Treatment of Vacation and Second Homes CHAPTER 5

-

Upload

elinor-johnston -

Category

Documents

-

view

217 -

download

0

Transcript of Slide 5-1 Tax Treatment of Vacation and Second Homes CHAPTER 5.

Slide 5-1

Tax Treatment of Vacation and Second

Homes

CHAPTER 5

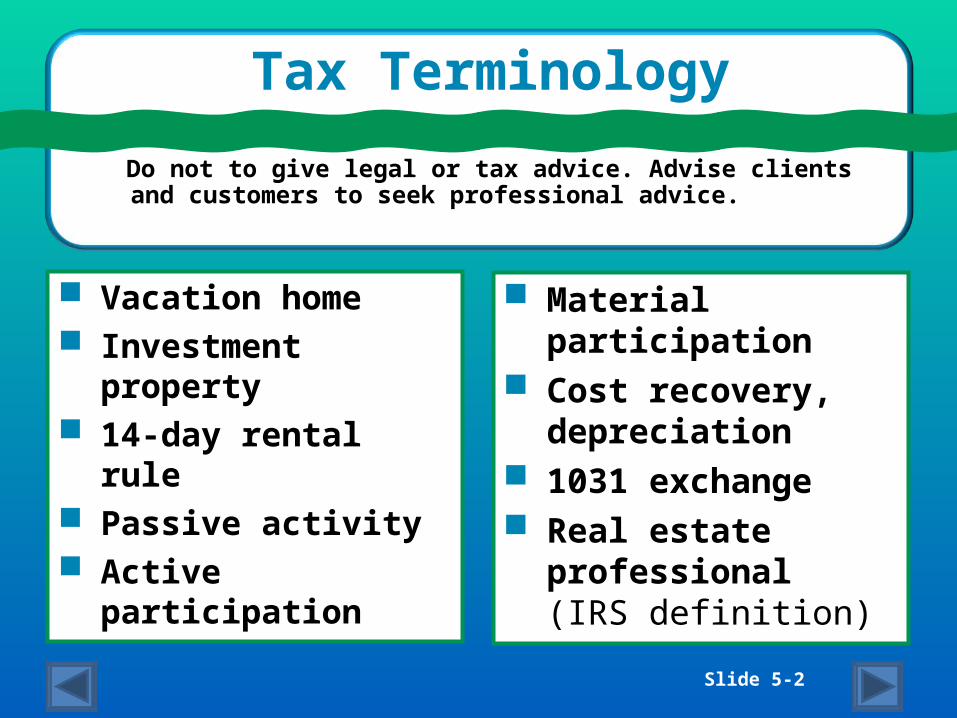

Slide 5-2

Vacation home Investment property 14-day rental rule Passive activity Active participation

Tax Terminology

Do not to give legal or tax advice. Advise clients and customers to seek professional advice.

Material participation Cost recovery,

depreciation 1031 exchange Real estate

professional (IRS definition)

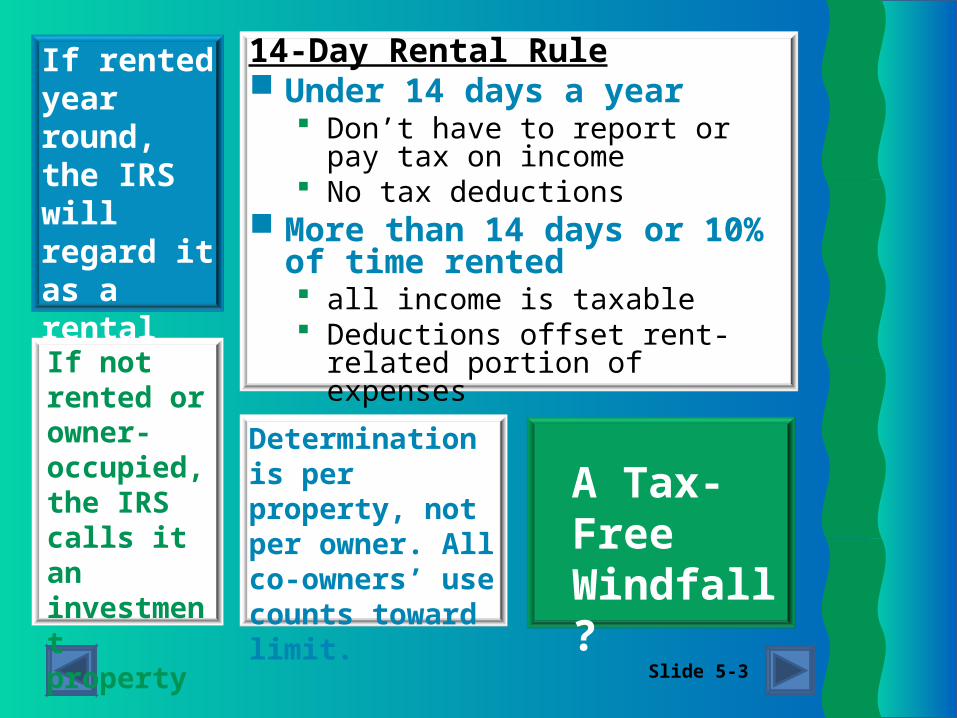

Slide 5-3

14-Day Rental Rule Under 14 days a year

Don’t have to report or pay tax on income

No tax deductions More than 14 days or 10% of time

rented all income is taxable Deductions offset rent-related portion

of expenses

If rented year round, the IRS will regard it as a rental property

If not rented or owner-occupied, the IRS calls it an investment property

A Tax-Free Windfall?

Determination is per property, not per owner. All co-owners’ use counts toward limit.

Slide 5-4

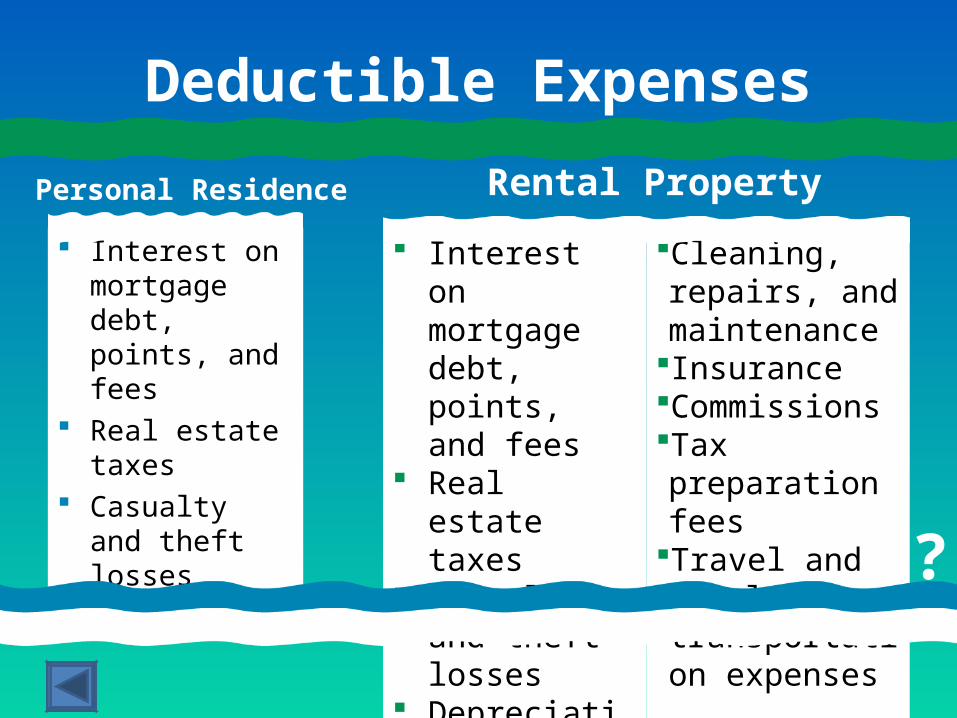

Deductible Expenses

Personal Residence

Interest on mortgage debt, points, and fees

Real estate taxes

Casualty and theft losses

Rental Property

Interest on mortgage debt, points, and fees

Real estate taxes

Casualty and theft losses

Depreciation Advertising

Cleaning, repairs, and maintenance

InsuranceCommissionsTax preparation fees

Travel and local transportation expenses ?

Slide 5-5

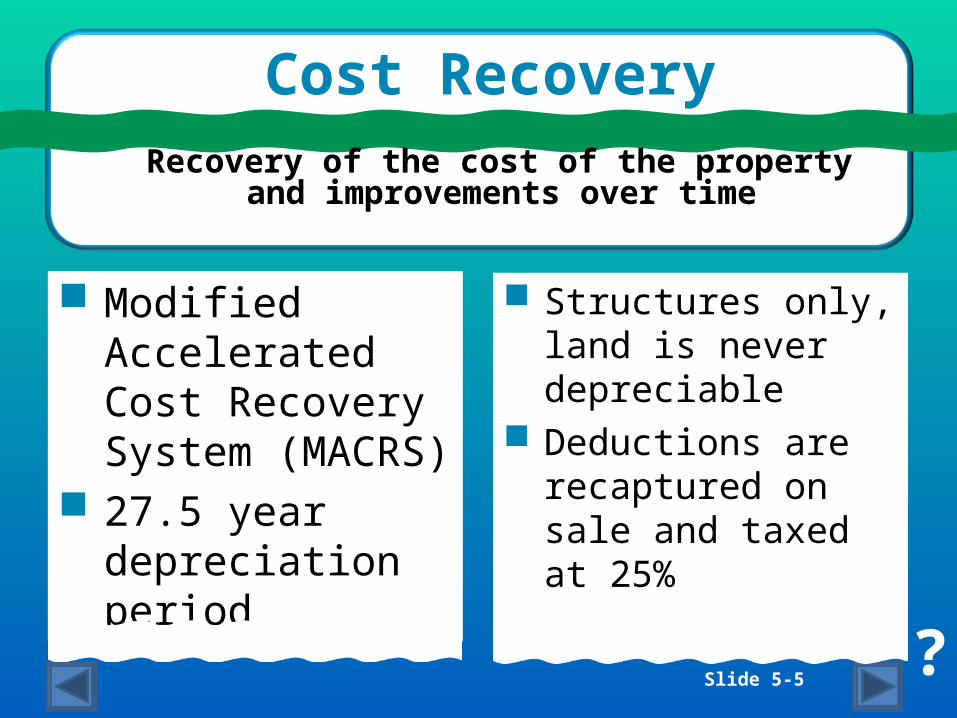

Modified Accelerated Cost Recovery System (MACRS)

27.5 year depreciation period

Cost RecoveryRecovery of the cost of the property and

improvements over time

Structures only, land is never depreciable

Deductions are recaptured on sale and taxed at 25%

?

Slide 5-6

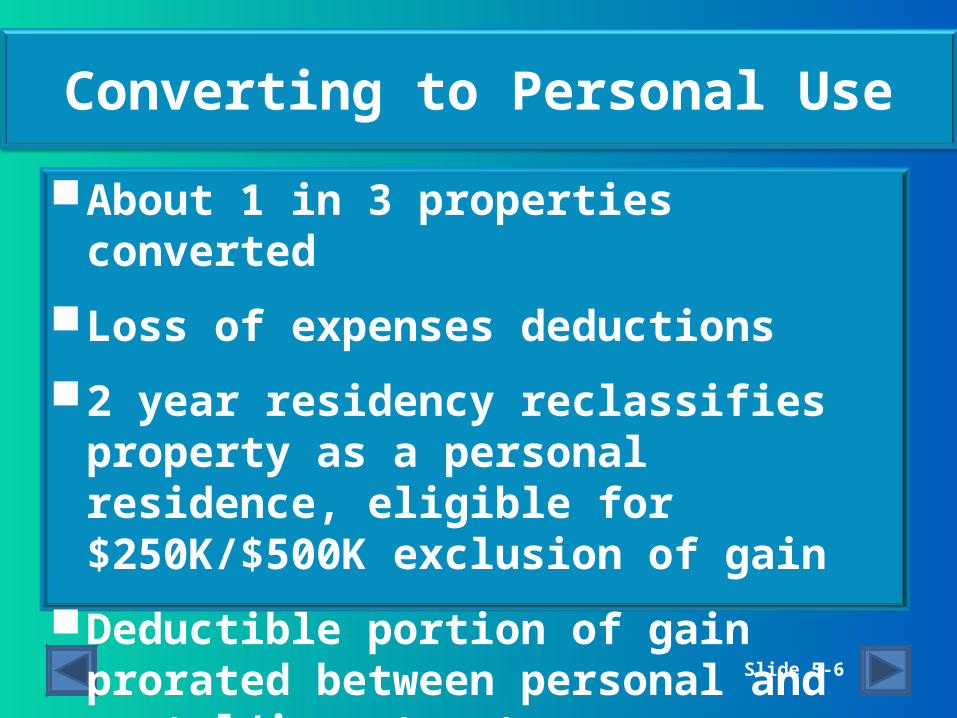

Converting to Personal Use

About 1 in 3 properties converted

Loss of expenses deductions

2 year residency reclassifies property as a personal residence, eligible for $250K/$500K exclusion of gain

Deductible portion of gain prorated between personal and rental/investment use

Slide 5-7

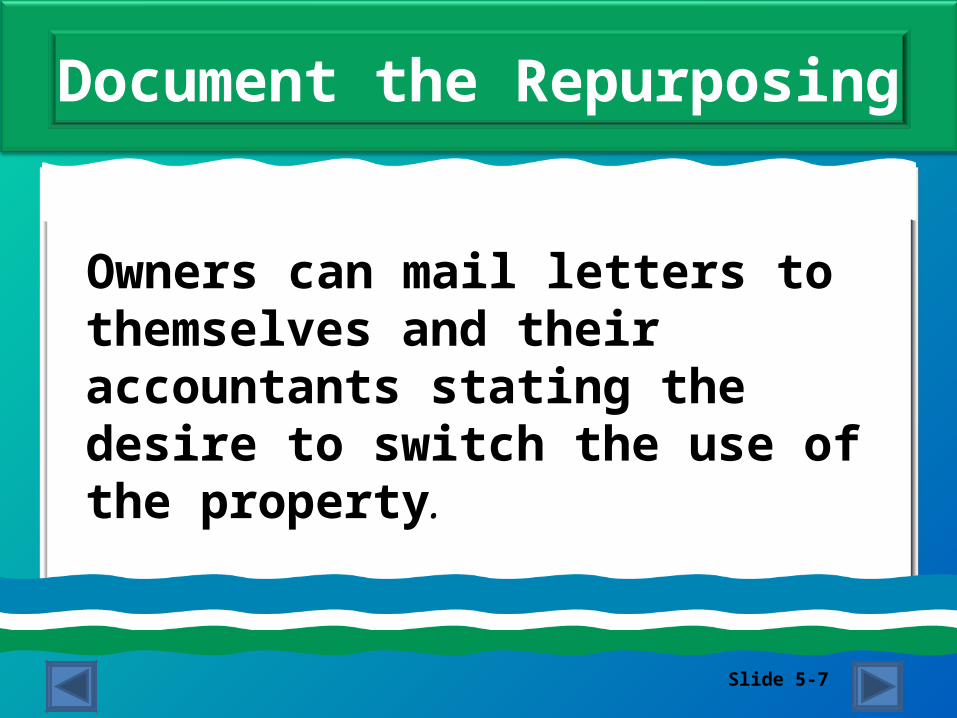

Owners can mail letters to themselves and their accountants stating the desire to switch the use of the property.

Document the Repurposing

Slide 5-8

Capital Gain Tax on Sale of a Converted Home

Effective 1/01/09

Sale of a primary residence used as a 2nd home (non qualified use) after 1/01/09 cannot claim full $250K/$500K gain exclusion

Taxable portions of gain based on % of non qualified use

Slide 5-9

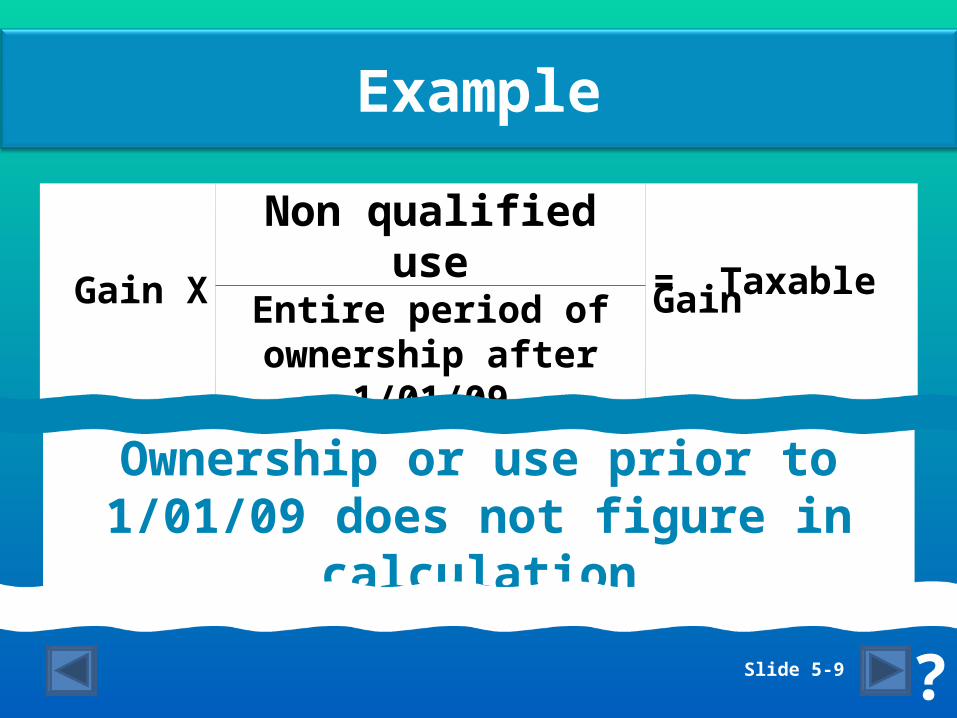

Example

Gain XNon qualified use

= Taxable GainEntire period of ownership

after 1/01/09

Ownership or use prior to 1/01/09 does not figure in calculation

?

Slide 5-10

Residence Received in an Exchange

Own for 5 years Rent for 2 years to

maintain exchangeeligibility

Occupy for 2 years to reclassify as a personal residence

Remember capital gains tax after 1/01/09