Sistema Universitario Ana G. Méndez, Inc. School of ... · y el ciclo de pagos, ciclo de...

62

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 1 Sistema Universitario Ana G. Méndez, Inc. School of Business Program Title: Continental USA Branch Campuses Universidad Metropolitana Auditoría y Garantía Contemporánea Contemporary Assurances and Audit Services ACCO 711 © Ana G. Méndez University System, Inc. 2018 All rights reserved.

-

Upload

trinhkhuong -

Category

Documents

-

view

213 -

download

0

Transcript of Sistema Universitario Ana G. Méndez, Inc. School of ... · y el ciclo de pagos, ciclo de...

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 1

Sistema Universitario Ana G. Méndez, Inc.

School of Business

Program Title:

Continental USA Branch Campuses

Universidad Metropolitana

Auditoría y Garantía Contemporánea

Contemporary Assurances and Audit Services

ACCO 711

© Ana G. Méndez University System, Inc. 2018

All rights reserved.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 2

TABLA DE CONTENIDO/TABLE OF CONTENTS

PÁGINA/PAGE

Información General Del Curso.................................................................................................3

General Course Information.......................................................................................................9

Taller Uno.................................................................................................................................13

Workshop Two ........................................................................................................................22

Taller Tres……………............................................................................................................29

Workshop Four…………........................................................................................................36

Taller Cinco/Workshop Five...................................................................................................41

Apéndice I/Appendix I............................................................................................................47

Apéndice II/Appendix II.........................................................................................................51

Apéndice III/Appendix III .....................................................................................................55

Apéndice IV/Appendix IV ....................................................................................................59

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 3

I. INFORMACIÓN GENERAL DEL CURSO

A. Descripción del curso

Este curso describe la responsabilidad de los auditores y servicios de garantía en el ámbito financiero,

el mismo está enfocado desde una perspectiva de la alta gerencia. Se concentra en las obligaciones

éticas y legales de los profesionales de auditoría, los estándares de la práctica, la evaluación de los

riesgos de una empresa, la evaluación de los controles internos, la evidencia de la auditoría, los

niveles de seguridad, los requisitos de certificación y el impacto de la tecnología de la información

en la práctica de auditoría.

B. Objetivos de contenido del curso

Al finalizar el curso, el estudiante será capaz de:

1. Analizar la historia de la profesión de auditoría contemporánea, la diferencia entre auditoría

y contabilidad, la importancia y demanda de las mismas, las diferentes clases de auditoría y

auditores, los reportes de auditoría, la ética profesional que conlleva y la responsabilidad

legal de la misma.

2. Conocer la importancia de los controles internos, el control del riesgo, el fraude y sus

diferentes categorías.

3. Conocer el impacto de la tecnología en el proceso de auditoría.

4. Desarrollar las destrezas necesarias en el proceso de auditoría, desde el propósito, la

planificación, el análisis de las transacciones, la evaluación de evidencia, la materialidad y

los diferentes niveles de riesgos hasta comunicar los resultados de la auditoría a la gerencia.

5. Aplicar el proceso de auditoría en el ciclo de ventas y colección de pago, procuraduría y el

ciclo de pagos, ciclo de inventario y almacén, así como el proceso de nómina y recursos

humanos.

6. Diferenciar la importancia de otros servicios de garantía y no garantía.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 4

Objetivos de lenguaje del curso

Al finalizar el curso, el estudiante será capaz de:

1. Analizar el proceso de auditoría en el ciclo de ventas y colección de pago, procuraduría

y el ciclo de pagos, ciclo de inventario y almacén, así como el proceso de nómina y

recursos humanos, mientras participa activamente en los discursos orales de los talleres

al reaccionar a estímulos auditivos como videos, presentaciones y actividades

interactivas.

2. Defender oralmente la importancia de los controles internos, el control del riesgo, el

fraude y sus diferentes categorías y la importancia de otros servicios de garantía y no

garantía, mientras expresa sus ideas sucinta, concisa y precisamente.

3. Investigar, los datos que recopile de las diversas fuentes de información sobre el tema la

historia de la profesión de auditoría contemporánea, la diferencia entre auditoría y

contabilidad, la importancia y demanda de las mismas, las diferentes clases de auditoría

y auditores, los reportes de auditoría, la ética profesional que conlleva y la

responsabilidad legal de la misma

4. Integrar las destrezas necesarias en el proceso de auditoría, desde el propósito, la

planificación, el análisis de las transacciones, la evaluación de evidencia, la

materialidad y los diferentes niveles de riesgos hasta comunicar los resultados de la

auditoría a la gerencia, mientras prepara informes escrito utilizando la terminología

correcta des la disciplina.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 5

C. Detalles del curso

1. Nombre del curso: Auditoría y Garantía Contemporánea

2. Codificación: ACCO 711-O

3. Créditos: Tres (3)

4. Duración: Cinco semanas

5. Prerrequisito: ACCO 503-O

6. Correquisito: Ninguno

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 6

Reglas de administración del curso

Este curso no cuenta con reglas especiales que deba considerar. Por favor, estudie la Guía del

estudiante para que obtenga detalles acerca de las políticas y reglas generales del curso.

D. Evaluación

Escala para la calificación final del curso

A = 100 - 90 B = 89 - 80 C = 79 – 70 D = 69 - 60 F = 59 o menos

Recuerde que cada actividad a ser evaluada tiene dos componentes:

Componente de contenido con un valor de 70 %

Componente de lenguaje con un valor de 30 %

Estos componentes se suman por actividad y su total se multiplica por el peso en el criterio que le

corresponda.

TABLA DE EVALUACIÓN

CRITERIOS DESCRIPCIÓN

ESPECÍFICA

TALLER(ES) PESO

Participación en clase El estudiante participará

activamente en todas las

actividades de contenido,

liderazgo y desarrollo

lingüístico en todos los

talleres.

1 -5

5%

Portafolio El facilitador especificará

los trabajos que se incluirán

en el portafolio digital.

Además utilizará la rúbrica

del Apéndice R del Digital

Performance Portfolio

Assessment Handbook para

evaluar este criterio.

1 -5

5%

Tareas y trabajos en clase Trabajos escritos,

presentaciones. Actividades

que utilizan los recursos

como: E-Lab, VoiceThread,

Foros de discusión escrita en

Blackboard.

1 -5

20%

Presentaciones/Escritos o Ensayos, Análisis de caso 1 -5 40%

Ejercicios de aplicación de

conceptos

Ejercicios durante talleres

específicos de aplicar

conceptos de auditoria.

1 -5

30%

Total 100 %

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 7

E. Libros de texto

Boynton, W.C and Johnson, R.N. (2012), Modern Auditing: Assurance Services and the

Integrity of Financial Reporting, 8th ed. IBSN: 978-0-471-23011-3

Arens, A.A., Elder, R.J. and Beasley, M.S. (2014) Auditing and Assurance Services, 15th ed.

ISBN: 978-0-133-12563-4

Louwers, T., Ramsay, R., Sinason, D., Strawser, J. and Thibodeau, J. (2015) Auditing &

Assurance Services 6th ed. ISBN: 978-0-077-86234-3

F. Referencias/Recursos

American Psychology Association. (2010). Quick answers-References.

Recuperado de http://www.apastyle.org/learn/quick-guide-on-references.aspx#Websites

Cambridge Dictionaries Online. (n.d.). Cambridge dictionaries make your words meaningful.

Recuperado de http://dictionary.cambridge.org/us

Education First. (n.d.). English grammar guide. Recuperado de

http://www.edufind.com/english-grammar/english-grammar-guide/

Fundación del Español Urgente BBVA. (n.d.). Recuperado de Fundéu BBVA. Recuperado de

http://www.fundeu.es

Grammarly Blog. (2017). Grammarly handbook. Recuperado de

http://www.grammarly.com/handbook

How to Pronounce Click, Hear & Learn. (n.d.). Click, hear & learn with howtopronounce.com.

Recuperado de https://www.howtopronounce.com/

LearnThat Foundation. (n.d.). List of English suffixes. Recuperado de

https://www.learnthat.org/pages/view/suffix.html

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 8

LearnThat Foundation. (n.d.). Root words & prefixes: Quick reference. Recuperado de

https://www.learnthat.org/pages/view/roots.html

Online Merriam-Webster Dictionary. (2017). Search the Merriam-Webster dictionary (11va

ed.). Recuperado de http://www.merriam-webster.com/

Online Talking Dictionary of English Pronunciation. (n.d.) Talking dictionary of English

pronunciation. Recuperado de http://www.howjsay.com/

Online Webster’s New World College Dictionary. (2017). Browse Webster’s new world college

dictionary (5th ed.). Recuperado de http://websters.yourdictionary.com/

OWL Purdue Online Writing Lab. (2017). APA General Format. Recuperado de

http://owl.english.purdue.edu/owl/resource/560/01/

Real Academia Española. (2014). Diccionario de la lengua española. (23a ed.). Recuperado de

http://dle.rae.es/

Real Academia Española. (2005). Diccionario panhispánico de dudas. Madrid, España.

Recuperado de http://www.rae.es/recursos/diccionarios/dph

Sistema Universitario Ana G. Méndez. (n.d.). Biblioteca virtual. Recuperado de

http://bibliotecas.suagm.edu/SG4.aspx

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 9

I. GENERAL COURSE INFORMATION

A. Course Description

This course describes and dictates the role of the auditors and providers of assurance services in

the financial markets, as it is studied from the perspective of the professional manager. It focuses

on the ethical and legal obligations of audit professionals, practice standards, risk assessment,

and the evaluation of internal controls, audit evidence, levels of assurance, attestation

requirements, and the impact of information technology on audit practice.

B. Course Content Objectives

Upon completing this course, the student will be able to

1. Analyze the history of contemporary auditing, the difference between auditing and

accounting, the importance and demands of each, the different types of audits, audit

reports, and the professional ethics and legal responsibilities of the audit professionals.

2. Know the importance of internal controls, risk assessments, and different types of fraud.

3. Know the impact of technology on the auditing process.

4. Develop the necessary skills in the audit process, from its purpose, planning, transaction

analysis, evaluation of evidence, and its different risks, to communicate the results of

the audit to management.

5. Apply the audit process on the sales cycle and payment collection, the procurement and

payment cycles, inventory and storage, as well as in payroll and human resources.

6. Differentiate the importance of guarantee and non-guarantee services.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 10

C. Course Language Objectives

Upon completing this course, the student will be able to

1. Analyze the audit process on the sales cycle and payment collection, the procurement and

payment cycles, inventory and storage, as well as in payroll and human resources, through

oral workshop discourse by reacting to auditory stimuli such as videos, presentations and

interactive activities and by actively participating in the discussions of the course.

2. Defend orally the importance of internal controls, risk assessments, and different types of

fraud, the importance of other guarantee and non-guarantee services, while conveying

ideas clearly and coherently.

3. Examine information compiled by reading about the history of contemporary auditing, the

difference between auditing and accounting, the importance and demands of each, the

different types of audits, audit reports, and the professional ethics and legal responsibilities

of the audit professionals.

4. Integrate the necessary skills in the audit process, from its purpose, planning, transaction

analysis, evaluation of evidence, and its different risks, to communicate the results of the

audit to management, while creating business reports using the appropriate core course

terminology.

D. Course Details

1. Course Name: Contemporary Assurances and Audit Services

2. Code: ACCO 711-O

3. Credits: Three (3)

4. Duration: 5 weeks

5. Prerequisite: ACCO 503-O

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 11

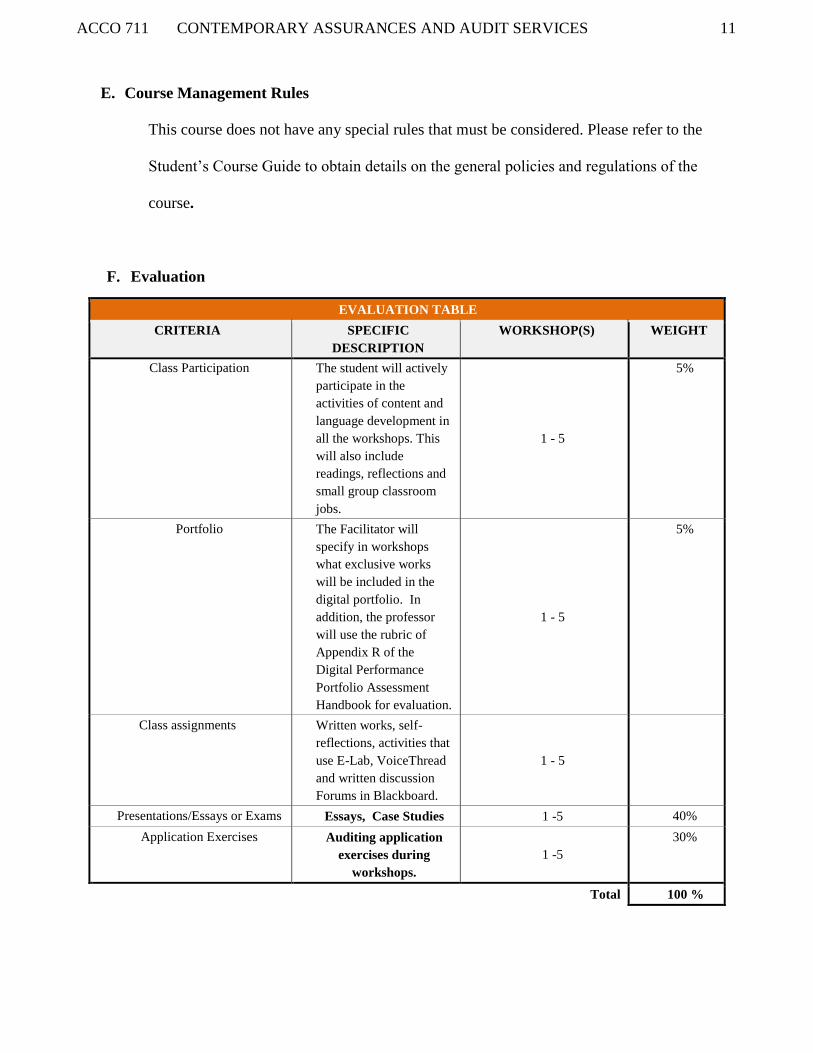

E. Course Management Rules

This course does not have any special rules that must be considered. Please refer to the

Student’s Course Guide to obtain details on the general policies and regulations of the

course.

F. Evaluation

EVALUATION TABLE

CRITERIA SPECIFIC

DESCRIPTION

WORKSHOP(S) WEIGHT

Class Participation The student will actively

participate in the

activities of content and

language development in

all the workshops. This

will also include

readings, reflections and

small group classroom

jobs.

1 - 5

5%

Portfolio The Facilitator will

specify in workshops

what exclusive works

will be included in the

digital portfolio. In

addition, the professor

will use the rubric of

Appendix R of the

Digital Performance

Portfolio Assessment

Handbook for evaluation.

1 - 5

5%

Class assignments Written works, self-

reflections, activities that

use E-Lab, VoiceThread

and written discussion

Forums in Blackboard.

1 - 5

Presentations/Essays or Exams Essays, Case Studies 1 -5 40%

Application Exercises Auditing application

exercises during

workshops.

1 -5

30%

Total 100 %

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 12

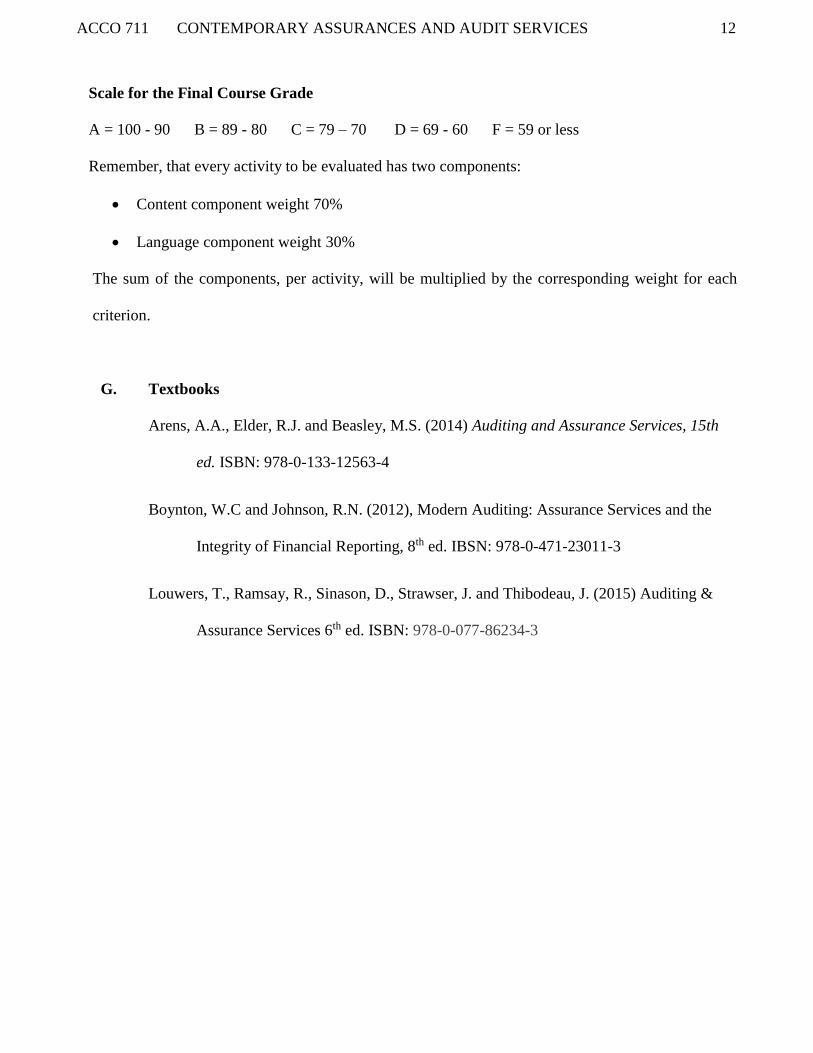

Scale for the Final Course Grade

A = 100 - 90 B = 89 - 80 C = 79 – 70 D = 69 - 60 F = 59 or less

Remember, that every activity to be evaluated has two components:

Content component weight 70%

Language component weight 30%

The sum of the components, per activity, will be multiplied by the corresponding weight for each

criterion.

G. Textbooks

Arens, A.A., Elder, R.J. and Beasley, M.S. (2014) Auditing and Assurance Services, 15th

ed. ISBN: 978-0-133-12563-4

Boynton, W.C and Johnson, R.N. (2012), Modern Auditing: Assurance Services and the

Integrity of Financial Reporting, 8th ed. IBSN: 978-0-471-23011-3

Louwers, T., Ramsay, R., Sinason, D., Strawser, J. and Thibodeau, J. (2015) Auditing &

Assurance Services 6th ed. ISBN: 978-0-077-86234-3

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 13

TALLER UNO

A. Objetivos de contenido

Durante el taller, el estudiante será capaz de:

1. Diferenciar los conceptos “auditoría y contabilidad” y los aspectos que competen a

cada disciplina.

2. Desglosar las características y funciones de los diversos procesos de auditorías y los

servicios de garantía contemporáneas en un organizador gráfico.

3. Argumentar ideas acerca de las diferencias que existen entre la labor que realizan las

agencias reguladoras de auditoría y contabilidad, gubernamentales y privadas (por sus

siglas en inglés GAAP, GAAS, AICPA, ISA, SEC, SOX) en un foro de discusión

escrita.

4. Analizar la relevancia de realizar auditorías (objetivos y su alcance), acompañarlas de

su informe final y las ventajas de contar una opinión calificada.

5. Detectar las violaciones éticas que se desprendan de un caso real relacionado con los

dilemas que enfrentan los auditores profesionales como parte de un análisis escrito.

B. Objetivos de lenguaje

Durante el taller, el estudiante será capaz de:

1. Discutir los conceptos “auditoría y contabilidad” y los aspectos que competen a cada

disciplina, según se desprende de la discusión en parejas de manera que fortalezca sus

destrezas auditivas.

2. Defender oralmente la relevancia de realizar auditorías (objetivos y su alcance),

acompañarlas de su informe final y las ventajas de contar una opinión calificada, en un

VoiceThread, mientras emplea el vocabulario apropiado con el fin de persuadir una

audiencia.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 14

3. Desglosar las características y funciones de los diversos procesos de auditorías y los

servicios de garantía contemporáneas en un organizador gráfico, de manera que

evidencie su comprensión de lectura en una discusión en clase.

4. Evaluar, por medio de un informe analítico, las violaciones éticas que se desprendan

de un caso real relacionado con los dilemas que enfrentan los auditores profesionales,

mientras domina el desarrollo del tema.

Vocabulario/terminología técnica de la disciplina

1. Auditoría

2. Garantías

3. Riesgo de auditoría

4. Control interno

5. Atestación

6. Opinión adversa

7. Opinión calificada

8. Materialidad

9. Ética

10. Independencia

11. Generally Accepted Accounting Principles

(GAAP)

12. Generally Accepted Accounting Standards

(GAAS)

13. American Institute of Certified Public

Accountants (AICPA)

14. International Standards on Auditing (ISA)

15. Securities and Exchange Commission (SEC)

16. Sarbanes-Oxley Act (SOX)

17. Deontología

C. Actividades antes del taller

1. En cada taller, como estrategia de preparación para todas las actividades, estudie

cuidadosamente los objetivos de contenido del taller y anote sus dudas para que, junto

al facilitador, pueda aclararlas durante la clase. Familiarícese con las rúbricas de

evaluación, tanto las de contenido como las de lenguaje, así como con los enlaces

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 15

electrónicos, libros y cualquier otra referencia que se relacione al material del taller.

Dicho material se encuentra en la sección de Referencias específicas del taller (al final

de este taller).

2. Acceda la Biblioteca Virtual, y las referencias específicas de este taller, para que

distinga detalladamente los procesos de auditoría y garantías contemporáneas.

a. Aplique el conocimiento que adquiera a todas las actividades que realice.

3. Investigue las características y funciones de los diversos procesos de auditorías y los

servicios de garantía contemporáneas.

a. Diseñe un organizador gráfico en el que desglose la información y llegue

preparado a clase para que aplique sus conocimientos en una actividad

constructivista.

4. Lea acerca de la labor que realizan las agencias reguladoras de auditoría y contabilidad,

gubernamentales y privadas (por sus siglas en inglés GAAP, GAAS, AICPA, ISA, SEC,

SOX) y la regla de independencia e interpretación.

a. Prepare un resumen o bosquejo en el que distinga la labor que realizan dichas

agencias.

b. Acceda el foro de discusión escrita de Blackboard y exprese, a su entender, qué

agencia superpone (overlap) las labores de otra. Es decir, si dos agencias o más

tienen la misma misión/enfoque. Si no es así, cree una agencia hipotética cuya

misión regule un aspecto actual que no cubra ninguna de las instituciones

reguladoras que estudió.

i. Debata respetuosa y sustantivamente las ideas que expresen al menos

dos compañeros. Aplique las siguientes guías en los foros (escritos y

orales) de este y todos los talleres del curso:

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 16

1. Comparta sus ideas tal como se espera de un alumno de

maestría. Sencillamente no parafrasee lo que expresen sus

compañeros.

2. Reaccionar sustantivamente significa a que usted demostrará

(con calidad y cantidad) que domina el tema al profundizar no

solo en el los temas, sino en los puntos de vista que ofrezcan sus

compañeros.

3. No escriba frases sencillas y escuetas como “estoy de acuerdo

contigo” o “muy buena contestación”.

ii. Llegue preparado a clase para que abunde al respecto.

5. Investigue acerca de la relevancia de realizar auditorías (objetivos y su alcance), la

importancia de complementar dichas investigaciones con su informe final y las ventajas

de contar una opinión calificada (auditor certificado).

a. Acceda el VoiceThread del taller para que exprese las desventajas y el impacto

que acarrea el no contar con la opinión de un auditor certificado, cuando se

investiga un caso.

b. Asegúrese de comprender bien el material para que lo aplique al análisis del caso

del taller (siguiente actividad) y durante las actividades relacionadas al mismo.

6. Acceda recursos académicamente confiables para que seleccione un conocido caso en el

que las auditorías hayan jugado un papel importante al detectar violaciones éticas (por

ejemplo Enron, Madoff, Healthsouth, etcétera).

a. Estudie el caso detalladamente, escriba un informe investigativo, cumpla con los

principios de redacción y siga la siguiente estructura:

i. Introducción

1. Establezca el problema claramente.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 17

2. Identifique los objetivos y el alcance de la auditoría/investigación

que se realizó.

ii. Desarrollo

1. Señale cómo y por qué se descubrió el caso.

2. Analice y especifique los datos, hallazgos, las discusiones, reglas,

violaciones, agencias involucradas, noticias, el impacto del

problema que planteó.

iii. Conclusión

1. Señale qué rol jugaron las auditorías, las agencias reguladoras y los

investigadores calificados en la investigación del caso.

2. Exprese cuáles son los resultados del caso y qué medidas (si

alguna) tomó la profesión para mitigar, minimizar y evitar que se

repita la historia.

b. Envíe su documento al NetTutor Paper Center:

i. Acceda el E-Lab, escoja NetTutor y la opción “Laboratorio de escritura en la

red”. Luego, seleccione NetTutor Paper Center Submission Form.

1. Clique Citations and References & Word Choice para que garantice la

calidad del escrito.

2. Cargue su documento en formato PDF y seleccione Upload.

c. Para detectar casos de plagio, el facilitador enviará los trabajos escritos a

SafeAssignTM.

d. Finalmente, y como en todos los talleres, coloque una copia del trabajo

corregido en el portafolio digital, junto a sus rúbricas, bajo la semana que le

corresponde.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 18

e. El facilitador evaluará los componentes de contenido y lenguaje de esta

actividad con el Apéndice I, Rúbrica de trabajos escritos antes del taller.

f. Llegue preparado a clase para que resuma su caso individualmente.

7. Comience a preparar su Portafolio Digital siguiendo las instrucciones estipuladas en el

“Digital Performance Portfolio Assessment Handbook”.

a. Lea detalladamente el Digital Performance Portfolio Assessment Handbook que

se encuentra en Blackboard y siga los siguientes pasos:

b. Prepare la portada, según indica la sección titulada Performance Portfolio

Template.

i. Salte la sección de la tabla de contenido.

ii. Redacte su introducción en inglés.

iii. Escriba su autobiografía en español.

c. Oprima el enlace llamado Digital Portfolio, que se encuentra en el menú del

curso en el margen izquierdo de la pantalla.

i. Seleccione la carpeta que corresponde a los cinco talleres que tiene su

curso.

ii. Descargue el Digital Portfolio Zip Folder.

d. Ahí encontrará por lo menos cinco carpetas. Si su curso dura más de cinco

semanas, entonces necesita crear el resto de las carpetas que falten. Al final, esta

sección contará con una carpeta por taller.

e. Semanalmente guardará todos los trabajos que usted realizó y el facilitador

evaluó, junto a sus respectivas rúbricas, según la semana y la actividad que

corresponda. De esa manera, su portafolio digital está listo para que lo

enriquezca con el material educativo que usted genere, semana tras semana, a lo

largo del curso.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 19

D. Actividades de aplicación durante el taller

1. El facilitador proveerá a los estudiantes su información de contacto, y se elegirá al

representante estudiantil.

2. El facilitador explicará detenidamente los requisitos y objetivos de contenido y

lenguaje del curso, así como los componentes teóricos. Además, aclarará el propósito

del portafolio digital y aprovechará la ocasión para especificar aquellas actividades

(antes y durante el taller) que se incluirán en el mismo, así como los recordatorios que

dará semanalmente.

3. El facilitador se cerciorará de que los alumnos tengan acceso a los recursos de

Blackboard y el E-Lab. También se asegurará de que los estudiantes entiendan las

expectativas generales y las normas específicas del curso. Igualmente, destacará la

importancia de familiarizarse con todo el contenido del módulo y la forma en que se

evaluará su desempeño.

4. Reunidos en parejas, los alumnos analizarán el material que incluyeron en los

organizadores gráficos que prepararon sobre las características y funciones de los

diversos procesos de auditorías y los servicios de garantía contemporáneas. Anotarán

la información importante para que guíen al facilitador quien irá diseñando un nuevo

organizador gráfico con la información que los estudiantes provean y justifiquen.

a. Como parte de la actividad, los estudiantes diferenciarán conceptos y

aspectos que competen a los términos “auditoría y contabilidad.

b. El facilitador evaluará esta actividad con el Apéndice III, Rúbrica de

discusiones en clase.

5. Basados en el tema del foro de discusión escrita, y los bosquejos o resúmenes que

prepararon antes de la clase, los estudiantes confirmarán o cambiarán las opiniones

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 20

vertidas antes del taller y justificarán sus puntos de vista. El facilitador comentará

acerca de las opiniones de los alumnos, basado en las teorías y los estudios de

reconocidos autores de la profesión.

6. Individualmente, y basados en el informe investigativo que redactaron como parte de

las actividades previas al taller, los estudiantes presentarán una clase demostrativa.

a. Además de demostrar el dominio de los temas, los alumnos prestarán

atención especial a la aplicación del vocabulario técnico de la disciplina e

implementarán técnicas efectivas al presentar una clase para profesionales

de los ámbitos de la contabilidad y la auditoría.

b. En caso de que más de un estudiante realice su trabajo investigativo acerca

del mismo caso, el facilitador promoverá la participación activa con

distintas preguntas de discusión que fomentarán el pensamiento crítico y

analítico.

i. Después de cada clase demostrativa, habrá una sesión de preguntas y

respuestas.

ii. El facilitador proveerá retroalimentación instantánea al evaluar el

componente lingüístico y el de contenido con el Apéndice III, Rúbrica

de discusiones en clase.

7. Como parte de su autorreflexión, conteste la siguiente pregunta y envíela al

facilitador vía Blackboard:

a. ¿Si tuviera la oportunidad de trabajar para alguna de las agencias

reguladoras (GAAP, GAAS, AICPA, ISA, SEC, SOX), cuál sería su puesto

ideal y por qué?

E. Referencias específicas del taller

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 21

Del Cid Gómez, J. M., La contabilidad y la función de auditoría. Laboris.net.

Recuperado de http://www.laboris.net/static/ca_busqueda_contabilidad.aspx

Symes, S. (n.d.). ¿Cuál es la función de la auditoría contable? La Voz de Houston.

Recuperado de

https://pyme.lavoztx.com/cul-es-la-funcin-de-la-auditora-contable-8714.html

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 22

WORKSHOP TWO

A. Content Objectives

During the workshop, the student will be able to

1. Identifying the four phases of the financial statement audit and the relation of these phases

to the audit objectives.

2. Evaluate the objectives and purpose of conducting a financial statement audit.

3. Distinguish the management’s responsibilities from the auditor’s responsibilities during

the financial statements audit and implementation of internal controls.

4. Examine different types of audit evidence, while recognizing the nature of the evidence.

B. Language Objectives

During the workshop, the student will be able to

1. Contrast different types of audit evidence, while recognizing the nature of the evidence,

by reacting to different auditory stimuli.

2. Differentiate orally the management’s responsibilities from the auditor’s responsibilities

during the financial statements audit and implementation of internal controls, in a short

class presentation, in an organized manner that captures the audience’s attention.

3. Interpret the objectives and purpose of conducting a financial statements audit, while

identifying the four phases of the audit and the relation of these phases to the objectives,

in a graphic organizer, while applying concepts presented in the readings completed for

the workshop.

4. Elaborate, various audit risks while adhering to the Sarbanes-Oxley Act requirements, in

an informative essay reflecting, which reflects proper use of the core course terminology,

syntax, and flow of ideas.

C. Core Course Terminology

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 23

1. Analytical procedure

2. Cycle approach

3. Error

4. Fraud

5. Assertion

6. Evidence

7. Judgement

8. Materiality

9. Misstatement

10. Risk of evidence

11. Misappropriation

12. Control risk

13. Engagement risk

14. Professional skepticism

15. Fraud risk factor

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 24

D. Activities before the Workshop

1. Carefully study the content objectives of the workshop and write down your doubts so that,

together with the facilitator, you can clarify them during the class. Familiarize yourself with

the terms and come prepare to the workshop to share knowledge developed with other

students.

2. Read about financial statement audit objectives and the audit process. Identify the four

phases of the audit and the relation of these phases to the objectives of a financial statement

audit. Create a graphic organizer to answer the following questions and be prepared to

discuss them in a group activity.

a. What is the overall objective of the financial statement audit?

b. What are the six transaction class audit objectives?

c. What are the four account balance audit objectives?

d. What are the four disclosure audit objectives?

e. Why is understanding the entity and its environment important to planning the

audit? Illustrate with an example.

3. Investigate about the difference between management’s responsibilities and the auditor’s

responsibilities during the financial statements assessment and the implementation of

internal controls. Go to Voice Thread link created by the facilitator in Blackboard and orally

discuss management and the auditor’s responsibilities while conducting an audit.

a. Record yourself and upload the recording by clicking on the Submit Assignment

icon. Be sure to select the Share with class feature.

b. Afterward, listen to and provide feedback to the delivery of at least two of your

colleagues’ recordings. Make sure to take notes on fundamental aspects of the

information you searched and that of your colleague’s contributions. Bring the

notes to class to elaborate during a group activity.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 25

4. The facilitator will create a written discussion forum using the Discussion Board tool in

Blackboard. Create a summary about audit evidence using the following guide:

a. Identify the three aspects associated with evaluating audit evidence.

b. Explain the purpose of evaluating deviations from prescribed control procedures

as part of evaluating audit evidence.

c. If the auditor finds only one instance of unintentional error during the audit, can

the auditor assume that this is an isolated instance? Why or why not?

d. What should be documented as part of the auditor’s working papers?

After posting your initial response, respond to a minimum of two comments posted by

your classmates in a way that is conducive to a thought-provoking discussion.

5. Research information about audit risk and the Sarbanes Oxley Act. Write an informative

essay of a minimum of 1000 words following the outline below and submit the assignment

through the blackboard tool.

a. Define audit risk.

i. Define the three components of audit risk.

ii. How do the fraud risk factors relate to the components of audit risk?

iii. Explain how the audit risk model is used to make decisions about audit

evidence.

iv. Explain the difference between fraudulent financial reporting and

misappropriation of assets

b. Be sure to write according to APA, include citations and references, and proofread

your written work to ensure correct grammar and usage of punctuation in order to

express your ideas with clarity.

c. Save your document and upload it to the E-Lab tool known as NetTutor.

i. Select two areas to receive specific feedback.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 26

ii. Incorporate NetTutor’s feedback into your paragraphs and submit your

revised document by uploading it to the assignment area of the course in

Blackboard.

a. The facilitator will send written works to SafeAssignTM to check for plagiarism.

The facilitator will evaluate this activity using Appendix I: Evaluation Rubric for

Essays and Written Material.

E. Application Activities during the Workshop

1. The students will lead the class in a review of the topics discussed in the previous

workshop, or clarify the doubts they have about the current workshop, to ensure students’

comprehension. Students will share one concept learned so far that was challenging to

understand and explain what helped them learn the concept.

2. Gathered in a round table format, the facilitator will guide the discussion in the differences

between the managerial and responsibilities of the auditor. In addition, the class will

discuss the Analytical Procedures (Managerial Responsibilities), using the following

guidelines.

a. State three uses of analytical procedures in an audit engagement.

i. Which uses are required in all audits?

ii. List the steps involved in the effective use of analytical procedures in

the planning phase.

iii. What premise underlies the use of analytical procedures in auditing?

iv. Identify four sources of information that the auditor may use in

developing expectations.

3. Debate time! The facilitator will divide the class in 2 groups and will present the following

question: the SEC does not require public companies to have their quarterly financial

statements audited. What responsibilities, if any, do audit firms have with regard to the

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 27

quarterly financial statements of their clients? In your opinion, should quarterly financial

statements be audited? One group will agree with auditing the quarterly statements;

another group will be against it. How does assessing the risk of material misstatement and

the concept of “fair presentation, in all material respects” affect each side of the debate?

4. Divided in subgroups, the facilitator will present each group with a short case about fraud

schemes. Based on the previous research of fraudulent financial reporting and

misappropriation of assets, each group will:

a. Identify the three risk factors that are related to the case.

b. Identify and explain ways that the auditor can use his or her understanding

of the entity’s system of internal controls.

c. Conclude with a solution or recommendation to prevent or minimize the

fraudulent activity from occurring.

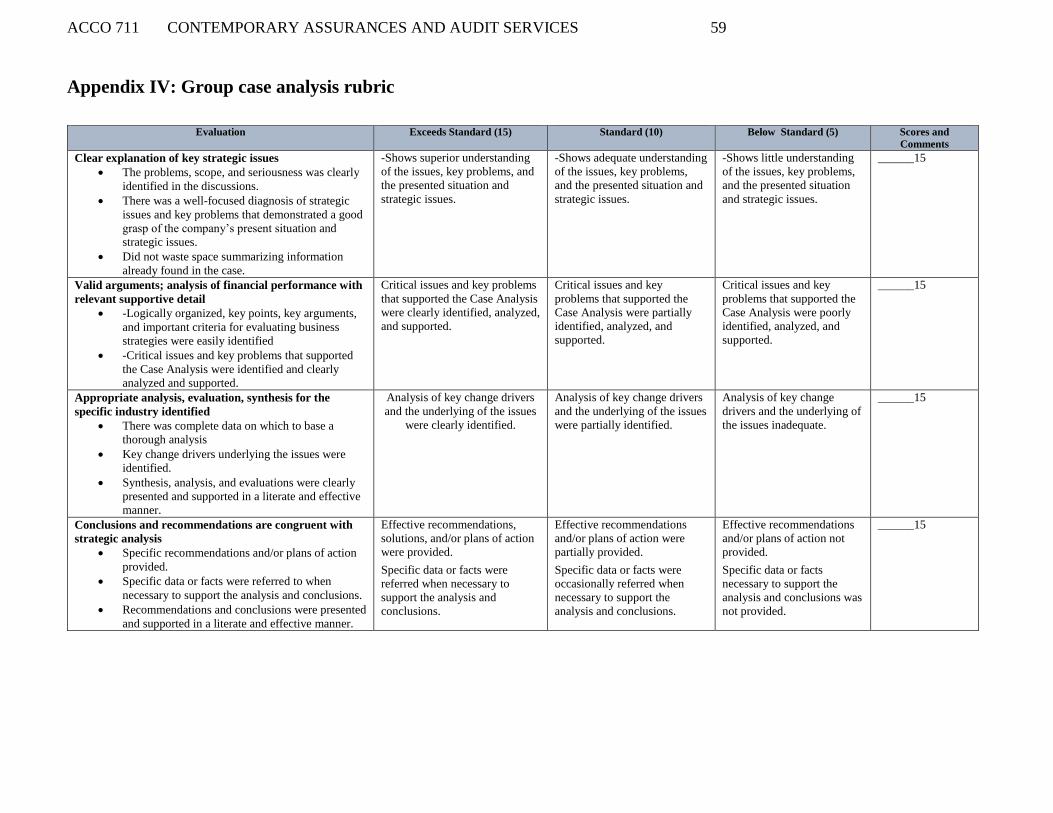

i. The facilitator will evaluate this activity using Group Case Analysis

Rubric (Appendix IV) and will provide immediate feedback, while

guiding a session of questions and answers after each discussion.

5. The facilitator will divide the class in small groups to discuss aspects associated with

evaluating audit evidence. The groups will prepare a five (5) minute presentation of the

most relevant points of their discussion. After the presentations, the facilitator will

review the most important strategies.

6. The students will write a self-reflection on the auditor’s responsibilities. The facilitator

may select a different topic discussed during the workshop. If deemed necessary, the

facilitator may ask students to send this activity after Workshop Two, but before

Workshop Three (Taller Tres).

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 28

F. Specific Workshop References

Accounting-Simplified. (2013). Purpose & Objectives of Auditing Financial Statements.

Accounting Simplified.com. Retrieved from http://accounting-

simplified.com/audit/introduction/purpose-of-audit.html

American Institute of Certified Public Accountants. (2017). Audit Risk and Materiality

in Conducting an Audit. AICPA-AU-C Section 312 Retrieved from

https://www.aicpa.org/Research/Standards/AuditAttest/DownloadableDocuments/AU-

00312.pdf

American Institute of Certified Public Accountants. (2017). Generally Accepted Auditing

Standards. AICPA-AU-C Section 150. Retrieved from

https://www.aicpa.org/Research/Standards/AuditAttest/DownloadableDocuments/

AU-00150.pdf

American Institute of Certified Public Accountants. (2017). Overall Objectives of the

Independent Auditor and the Conduct of an Audit in Accordance With Generally

Accepted Auditing Standards. AICPA-AU-C Section 200 Retrieved from

https://www.aicpa.org/Research/Standards/AuditAttest/DownloadableDocuments/AU-C-

00200.pdf

West Virginia University. (2017). Audit Phases. West Virginia University, Audit

Services. Retrieved from https://internalaudit.wvu.edu/audit-services/audit-phases

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 29

TALLER TRES

A. Objetivos de contenido

Durante el taller, el estudiante será capaz de:

1. Evaluar los componentes del modelo de riesgo de auditoria.

2. Justificar porque es importante establecer límites de riesgo en un ensayo.

3. Analizar el triángulo de fraude y examinar los factores de riesgo de fraude, a través de

un ensayo.

4. Distinguir los cambios que se pueden realizar en los enfoques de auditoría para áreas de

mayor riesgo, utilizando la herramienta de VoiceThread.

B. Objetivos de lenguaje

Durante el taller, el estudiante será capaz de:

1. Interpretar las discusiones que se generen durante el análisis de los componentes del

modelo de riesgo de auditoria, tomando notas sobre aspectos que requieran

profundización.

2. Distinguir, oralmente, los cambios que se pueden realizar en los enfoques de auditoría

para áreas de mayor riesgo, mientras aplica correctamente el vocabulario de la

disciplina.

3. Elaborar un informe sobre el triángulo de fraude y sus componentes, mientras investiga

datos y recursos académicos coherentes y confiables.

4. Justificar por qué es importante establecer límites de riesgo en un ensayo, al mismo

tiempo que afina detalles del formato y la gramática en general.

C. Vocabulario/terminología técnica de la disciplina

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 30

1. Procedimientos analíticos 9. Procedimientos de auditoría

2. Modelo de riesgo de auditoría 10. Riesgo de auditoría

3. Controles antifraude 11. Documentación de auditoría

4. Riesgo del negocio 12. Controlar el riesgo

5. Riesgo de detección 13. Errores

6. Riesgo inherente 14. Riesgo de detección

7. Fraude 15. Problemas de la empresa en marcha

8. Riesgo

D. Actividades antes del taller

1. Utilice la Biblioteca Virtual, y otros recursos académicos del E-Lab, como libros

electrónicos, para investigar sobre los componentes del triángulo de fraude. Prepare un

resumen de no menos de seis párrafos y llévelo a clases para contribuir a la discusión

del material y aclarar dudas.

2. El facilitador creará un foro de discusión escrita en Blackboard, ubicado dentro del

curso.

a. De manera completa y utilizando referencias concretas y confiables, defina los

conceptos fraude, riesgo, modelo de riesgo de auditoria, riesgo inherente y controles

antifraude.

b. Publique su contribución en el foro de discusión y reaccione a los ejercicios de por

lo menos dos colegas con comentarios y preguntas relevantes.

c. Imprima una copia de sus definiciones y llévela a clase para participar en una

actividad de aprendizaje cooperativo.

3. El facilitador creará un foro de discusión oral en Blackboard utilizando la herramienta

de VoiceThread.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 31

a. En dos minutos, y utilizando un tono educativo, el estudiante justificará

oralmente las razones por las que los enfoques de la auditoría pueden

cambiar para áreas de mayor riesgo.

b. Comente y tome notas sobre las aportaciones de sus compañeros, y

llegue preparado a clase para que abunde al respecto.

4. Redacte un ensayo de un máximo de 750 palabras y un mínimo de 500 palabras acerca

de por qué es importante establecer un límite de aceptación de riesgo, utilizando el

modelo de riesgo. Asegúrese de redactar según APA, incluya las citas y referencias.

a. Recuerde enviar su trabajo a NetTutor, e incorpore las sugerencias antes de enviar

su ensayo final a través de Blackboard.

b. Esta actividad se evaluará utilizando el Apéndice I: Rúbrica para ensayos y material

escrito.

5. En un documento Word, conteste las siguientes preguntas:

a. Supongamos que le preocupa que su cliente haya registrado ingresos que no

ocurrieron. ¿Qué objetivo de auditoría consideraría que tiene un alto riesgo de

error material?

b. ¿Por qué el fraude que comete la gerencia siempre se considera material,

incluso si la cantidad no es cuantitativamente material?

c. ¿Cuáles son algunas limitaciones del modelo de riesgo de auditoría?

Procure mantener el vocabulario apropiado durante las respuestas a sus preguntas.

Traiga una copia de su ejercicio a clase.

6. Continúe trabajando en la organización del portafolio digital de acuerdo con las

directrices estipuladas en el Manual de evaluación del Digital Performance Portfolio.

E. Actividades durante el taller

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 32

1. El facilitador repasará los temas que se cubrieron en el taller anterior para asegurarse de

que los alumnos comprendan el material.

2. Reunidos en formato de mesa redonda, la clase discutirá el ensayo que escribieron

acerca de la importancia de establecer un límite de riesgo que trabajaron como parte de

las actividades antes del taller. El facilitador abrirá una discusión en pleno, donde los

estudiantes elegirán cuál sería su límite de riesgo en una auditoria y defenderán su

decisión ante la clase.

3. La clase se dividirá en grupos de tres estudiantes. El facilitador le asignará un

componente del modelo de riesgo los estudiantes utilizarán el internet para investigar

acerca del componente asignado. Cada grupo preparará un recurso audiovisual que

apoyará una breve presentación sobre sus hallazgos. El facilitador evaluará esta

actividad usando el Apéndice II: Rúbrica de Evaluación para Presentaciones en Clase.

4. La clase se dividirá en dos grupos y analizarán el siguiente problema:

a. Usted es senior en un equipo de auditoría para una gran empresa pública.

Este es su segundo año auditando esta empresa, y ha establecido una

buena relación de trabajo con parte del personal del cliente. Su empresa

solo ha sido el auditor independiente de esta compañía durante cuatro

años, y la compañía tiene un historial de fraude antes de convertirse en

cliente de su empresa.

Durante el almuerzo con algunos empleados del cliente, escuchas que

Danilo, el asistente de controlador de las operaciones de la compañía en

Suramérica, ha tenido problemas para pagar su hipoteca. Incluso puede

enfrentar el perder su casa si no encuentra una oportunidad para obtener

un ingreso suplementario. Además, a través de la reunión de intercambio

de ideas sobre fraude realizada al comienzo de la auditoría del año fiscal,

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 33

se enteró de que se pensaba que la división de América del Sur era

responsable del fraude en el pasado. Danilo y su departamento incluso

fueron investigados por el departamento de auditoría interna, pero todas

las investigaciones anteriores no fueron concluyentes debido a la falta de

evidencias.

Al revisar las pruebas de control interno sobre informes financieros

(ICFR por sus siglas en inglés) del año en curso realizadas por un

contador de la compañía, verá que los resultados de las pruebas indican

que los controles internos sobre informes financieros son efectivos. El

plan de auditoría para la auditoría de los estados financieros se basa en la

efectividad operativa de los controles para todo el año fiscal. Las pruebas

de control del interno sobre informes financieros no dan ninguna

indicación de que el plan de auditoría de los estados financieros deba ser

revisado.

Cada grupo discutirá el caso y dará su opinión en cuanto si todos los elementos del

triángulo de fraude están presentes. La clase en conjunto determinará cual sería la mejor

manera de manejar la situación. El facilitador evaluará esta actividad usando el

Apéndice III: Rúbrica de evaluación de discusiones orales

5. Los estudiantes trabajarán en pareja los siguientes ejercicios:

i. Este problema requiere que acceda al Estándar de auditoría PCAOB n. ° 12,

Identificación y evaluación de riesgos de errores materiales (pcaobus.org). Use

este estándar para responder cada una de las siguientes preguntas. Para cada

respuesta, documente el / los párrafo (s) en AS N. ° 12 que apoya su respuesta.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 34

a. ¿Qué tipo de información sugiere el estándar de auditoria No. 12 que el

auditor debe considerar al obtener una comprensión de la compañía y su

entorno?

b. ¿Qué tipos de mediciones de rendimiento pueden afectar el riesgo de

error material?

c. ¿Qué cuestiones específicas deberían incluirse en la discusión entre los

miembros del equipo de auditores con respecto al riesgo de error

material?

d. ¿Qué factores debe considerar el auditor para determinar si un riesgo es

un "riesgo significativo"?

e. ¿Qué orientación se proporciona sobre la revisión de la evaluación de

riesgos a medida que continúa la auditoría?

f. Los estudiantes intercambiarán pareja para comparar y discutir sus

contestaciones. Las parejas se intercambiarán cada 5 minutos y

compararán las contestaciones. Una vez terminados los intercambios,

colectivamente, los estudiantes determinarán las mejores contestaciones.

El facilitador evaluará esta actividad usando el Apéndice II Rúbrica para

Evaluar Análisis de Casos en Grupo.

6. Los estudiantes escribirán su autorreflexión en donde diferenciarán los requisitos de

comunicación del auditor sobre el fraude para la gerencia, el comité de auditoría y otros.

El facilitador podrá elegir otro tema que promueva la autorreflexión individual. Si el

tiempo apremia y el facilitador lo estima necesario, el estudiante podrá entregar su

autorreflexión luego de culminado el taller, y deberá entregarlo en la fecha estipulada,

antes de comenzar el próximo taller (Workshop Four).

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 35

7. Finalmente, el facilitador mencionará y aclarará las tareas que realizarán antes del

próximo taller.

F. Referencias específicas del taller

Arens, Alvin & Elder, Randal (2017). Auditing and Assurance Service (16th edition)

Pearson

Messeir, William F. & Glover, Steven M. (2017). Auditing (10th edition) MC Graw Hill

Riesgo en la Auditoria. Recuperado de https://www.gestiopolis.com/riesgos-en-auditoria/

Estándar de Auditoria. Recuperado de https://www.isaca.org/Knowledge-

Center/Standards/Documents/1001_std_Spanish_1113.pdf

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 36

WORKSHOP FOUR

A. Content Objectives

During the workshop, the student will be able to

1. Explain how general controls and application controls reduce information technology

risks.

2. Discuss the value of effective internal control, while analyzing a short case study of a

particular company.

3. Analyze the relationship between management’s assertions, internal control over

financial reporting (ICFR), and activities of an integrated audit.

4. Evaluate the approach and steps an auditor uses to understand a company’s ICFR and

assess its design effectiveness, in a self-reflection exercise.

B. Language Objectives

During the workshop, the student will be able to

1. Examine the importance of how general controls reduce information technology risk,

while paying close attention to the information orally presented by peers in oral

discussions

2. Orally evaluate the relationship between management’s assertions, internal control over

financial reporting (ICFR), and activities of an integrated audit.

3. Conclude, during a short case study, value of effective internal control, while analyzing

a short case study of a particular company, while applying concepts presented in the

readings.

4. Justify the importance of a walkthrough, using a variety of English language

vocabulary, with correct grammar, punctuation, syntax and correct use of verbs, to

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 37

detail the steps an auditor uses to understand a company’s ICFR and assess its design

effectiveness.

C. Core Course Terminology

1. Application controls 8. Audit evidence

2. Application service providers (ASPs) 9. Classification assertion

3. Control activities 10. Design effectiveness

4. COSO principles

5. Cybersecurity

6. Encryption techniques

7. Accuracy assertion

D. Activities before the Workshop

1. Access the Digital Performance Portfolio folder of the previous workshop in

Blackboard and upload the graded documents or artifacts that correspond to Workshop

Three (Taller Tres). Follow any other instructions stipulated by the facilitator for the

effective completion of this activity.

2. Using the VoiceThread link created by the facilitator in Blackboard, orally discuss the

relationship between management’s assertions, internal control over financial reporting

(ICFR), and activities of an integrated audit.

a. After you record yourself, listen to and provide feedback to the delivery of at least

two of your colleagues’ recordings.

b. Make sure to take notes on fundamental aspects of the information you searched and

that of your colleague’s contributions. Bring the notes to class to elaborate during a

group activity.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 38

3. Using the Virtual Library, and/or other academic resources from the E-Lab, research

information on the value of effective internal control. Write a summary of your findings

and bring a copy to class for further discussion, in collaboration with your classmates.

4. The facilitator will create a written discussion forum using the Discussion Board tool in

Blackboard. Students will answer the following questions:

a. Describe which of the three categories of broad objectives for internal controls

are considered by the auditor in an audit of both the financial statements and

internal control over financial reporting.

b. Explain the importance of a walkthrough, how one is performed, and list five

relevant questions that the auditor might ask during a walkthrough. What types

of responses to your questions might the auditor receive that would cause

concern about the effectiveness of ICFR?

5. Prepare a graphic/chart with the five components of COSO’s Internal Control

Framework. Also read about the vision, mission and history of the organization and be

prepared to discuss the framework and share the information in class.

6. Continue working on your digital portfolio; follow the instructions in the Digital

Performance Portfolio Assessment Handbook found on Blackboard.

E. Activities during the Workshop

1. The facilitator will lead the class in a review of the topics covered in the previous

workshop to ensure students’ comprehension. Students will share one concept learned

so far that has drawn their attention the most and explain why.

2. Roll the dice! The facilitator will have a box or bag with numbers. As students arrive,

they will select a number from the box or bag. The facilitator will select the first student

to roll the dice and call the number; the student with that number will state the list of five

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 39

relevant questions that the auditor might ask during a walkthrough of effective internal

controls. The rest of the class have discussions based on those questions.

3. The facilitator will divide the class in two groups for a debate activity. One group will

research how general controls reduce technology information risk, while the other group

will research how application controls could reduce technology information risk. The

groups will then defend each of their points of view and the class will discuss the

advantages and disadvantages of each option. Students are invited to take a side they are

least inclined to select, as a way of intersecting subjective outlooks with potential

learning topics. Make sure to keep the use of correct language at all times, carefully

listening to each colleague’s intervention and building up a structured and feasible

argument. The facilitator will evaluate this activity using Appendix III: Oral discussion

evaluation rubric.

4. The class will be divided into groups of three students each, to work on the following

problem:

Roran is a staff-level auditor assigned to evaluate the ICFR for the XYZ

Corporation audit. Roran follows his firm’s audit plan to assess ICFR. Step

1.3 of the audit plan says: “the auditor should evaluate the overall attitude

and awareness of an entity’s board of directors concerning the importance

of internal control.”

a. With which component of internal control is Step 1.3 concerned?

b. Draft specific audit steps that Roran might find in his plan, in

addition to the general direction.

c. What would Roran include in his work papers to document his

work?

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 40

d. Each group will present their opinions and defend their points in

front of the entire class. The facilitator will evaluate this activity

with Appendix IV: Group case analysis rubric

5. The students will write a self-reflection on the approach and steps an auditor uses to

understand a company’s ICFR and assess its design effectiveness. The facilitator may

select a different topic discussed during the workshop. If deemed necessary, the

facilitator may ask students to send this activity after Workshop Four, but before

Workshop Five/Taller Cinco.

6. Each group will designate the leader for the next workshop and students will discuss the

activities to be completed before the next workshop.

F. Specific Workshop References

Arens, Alvin & Elder, Randal (2017). Auditing and Assurance Service (16th edition)

Pearson

AS 2201: An Audit of Internal Control Over Financial Reporting. Retrieved from

https://pcaobus.org/Standards/Auditing/Pages/AS2201.aspx

Guidance on Internal Control. Retrieved from https://www.coso.org/Pages/ic.aspx

Internal Controls. Retrieved from

https://www.investopedia.com/terms/i/internalcontrols.asp

Messeir, William F. & Glover, Steven M. (2017). Auditing (10th edition) MC Graw Hill

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 41

TALLER CINCO/WORKSHOP FIVE

NOTA: Este taller será en español y en

inglés. Tanto el facilitador como los

estudiantes deberán utilizar el idioma

asignado para actividades antes y durante

el taller. No mezclen los dos idiomas.

Utilicen solamente un lenguaje a la vez.

Las primeras dos horas del taller serán

en español y las últimas dos horas serán

en inglés.

NOTE: This workshop will be in Spanish

and in English. Both the facilitator and the

students must use the language assigned

for activities before and during the

workshop. Do not mix the two languages.

Use only one language at a time. The first

two hours of the workshop must be

conducted in Spanish and the last two

hours in English.

A. Objetivos de contenido/Content Objectives

1. Objetivos en español

Durante el taller, el estudiante será capaz de:

a. Diferenciar los tipos de información para los cuales un CPA puede emitir informes

certificando una opinión, enumere los requisitos para que un servicio de

certificación sea posible.

Definir que otros servicios auditores pueden proveer a empresas públicas.

2. Objectives in English

During the workshop, the student will be able to

a. Evaluate the four general stages in an audit-related legal dispute.

b. Analyze the auditor’s liability to clients and to third parties under common law.

c. Examine how an auditor can be held criminally liable under various federal and

state laws.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 42

B. Objetivos de lenguaje/Language Objectives

1. Objetivos en español

Durante el taller, el estudiante será capaz de:

a. Distinguir los servicios de certificación prestados por un CPA, basado en lo que

escuche con atención de las presentaciones audiovisuales y discusiones en clase.

b. Explicar oralmente otros servicios prestados por los auditores a empresas públicas.

2. Objectives in English

During the workshop, the student will be able to

a. Analyze the legal liability of the auditors to their clients, by researching academic

and reliable sources of information.

b. Examine, in a written report, how an auditor can be held criminally liable under

various federal and state laws, using the appropriate course terminology.

C. Vocabulario/terminología técnica de la disciplina/Core Course Terminology

1. Vocabulario/terminología en español

a. Incumplimiento de contrato

b. Ley civil

c. Acción de clase

d. Debido cuidado profesional

e. Carta de compromiso

f. Garantía razonable

2. Vocabulary/Terminology in English

a. Attest engagement

b. Attribute standards

c. Assertions

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 43

d. Comfort letter

e. Compilation

D. Actividades antes del taller/Activities before the Workshop

1. Actividades en español

a. El facilitador creará un foro de discusión oral en la herramienta VoiceThread. de

Blackboard. En dicho foro, el estudiante discutirá oralmente los servicios prestados

por los auditores a empresas públicas. Recuerde reaccionar oralmente a al menos

dos comentarios de los compañeros.

b. Utilice la Biblioteca Virtual, entre otros recursos académicos del E-Lab, para

investigar sobre los requisitos para que un servicio de certificación sea posible.

Prepare un bosquejo detallado y llévelo a clases para contribuir a la discusión del

material y aclarar dudas.

c. Continúe trabajando en la organización y finalización del portafolio digital

siguiendo los lineamientos estipulados en el manual de evaluación de Portfolio

Digital.

2. Activities in English

a. The facilitator will create a written discussion forum using the Discussion Board tool

in Blackboard. Students will answer the following questions:

i. Briefly describe the four stages of the auditor’s dispute process.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 44

ii. For what types of actions are auditors liable to a client under common law?

Why would the client prefer to sue the auditor for a tort action rather than

for a breach of contract

React to the contributions of at least two classmates with substantial comments and

follow up on the thread making sure not to leave unanswered questions or ideas.

b. Write a one-page essay about how an auditor can be held criminally liable under

various federal and state laws. Be sure to use APA style, include bibliographic

citations and references. This activity will be evaluated with Appendix I: Evaluation

Rubric for Essays and Written Material.

c. Prepare for the final exam, an individual case study, which the facilitator will

administer in English, at the time deemed most appropriate, during the last two

hours of the workshop.

E. Actividades durante el taller/Activities during the Workshop

1. Actividades en español

a. La clase se dividirá en cuatro grupos de cuatro estudiantes cada uno (o menos,

dependiendo del tamaño de la clase). El facilitador asignará a cada estudiante un

color (verde, rojo, amarillo o azul) y a cada grupo se le asignará una identificación

(mano derecha, mano izquierda, pie derecho y pie izquierdo). Utilizando el tablero

del juego Twister, el facilitador girará la manecilla y llamará la combinación de

color e identificación. El estudiante que corresponda al color y a la identificación

elaborará sobre los tipos de información para los cuales un CPA puede emitir

informes certificando una opinión. El facilitador se asegurará que todos los

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 45

estudiantes participen de la actividad. Al final, todos los grupos enumerarán los

requisitos para que un servicio de certificación sea posible.

b. Reunidos en parejas, los estudiantes repasarán lo aprendido en clase. Luego cada

pareja presentará los puntos más importantes que ellos discutieron, a todos los

colegas en la clase.

c. Los estudiantes escribirán su autorreflexión sobre el reto principal que enfrentaron

durante la clase, haciendo énfasis en los retos personales que han tenido que

superar para lograr cumplir con todas las actividades del curso. El facilitador

podrá elegir otro tema que promueva la autorreflexión individual.

2. Activities in English

a. In the last two hours of the workshop, the facilitator will administer the final test,

which will consist of a case study where students individually apply the concepts

learned in class.

b. Access the Digital Performance Portfolio folder of the previous workshop in

Blackboard and upload the graded documents or artifacts that correspond to

Workshop Four. The facilitator will indicate the weekly graded works to be

included in the digital portfolio, including the weekly self-reflection.

F. Referencias específicas del taller/Specific Workshop References

Accountant’s Liability. Retrieved from https://www.investopedia.com/terms/a/accountant-

liability.asp

AICPA Completes Clarity Project for Attestation Standards. Retrieved from

https://www.aicpa.org/press/inthenews/aicpa-completes-clarity-project.html

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 46

Arens, Alvin & Elder, Randal (2017). Auditing and Assurance Service (16th edition)

Pearson.

Messeir, William F. & Glover, Steven M. (2017). Auditing (10th edition) McGraw Hill.

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 47

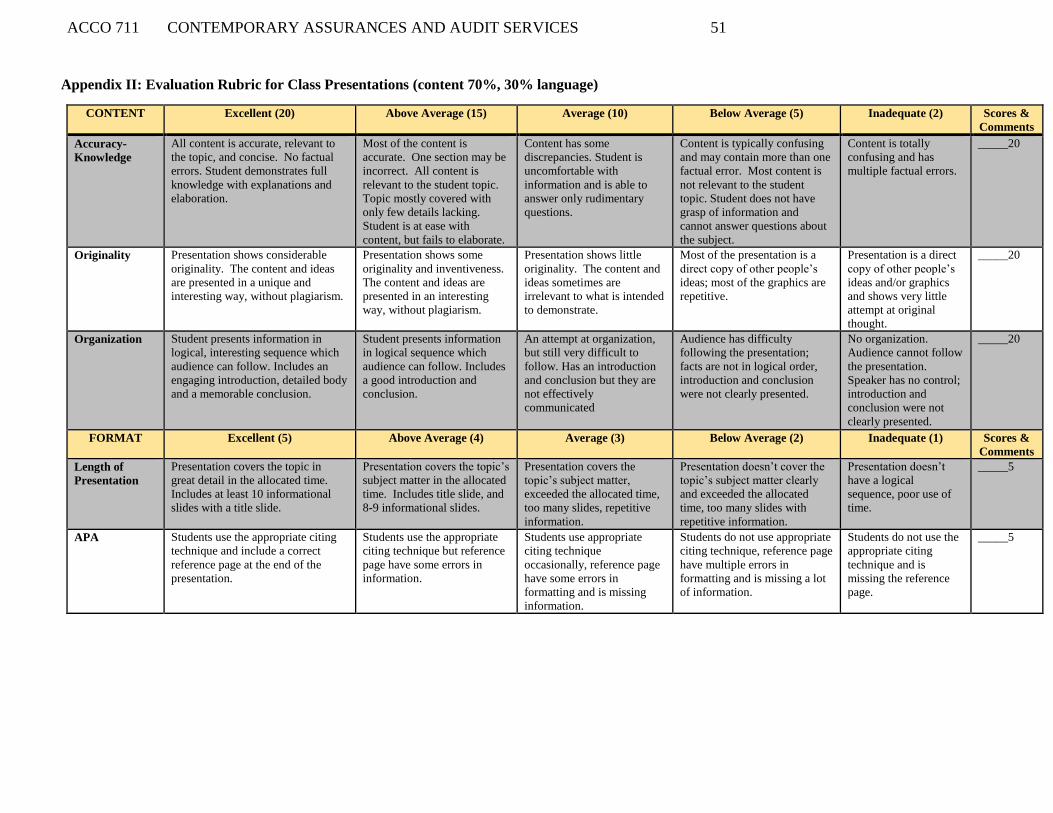

I: Evaluation Rubric for Essays and Written Material (70% content, 30% language)

CONTENT/

PREPAREDNESS

Exceptional (20) Skilled (15) Proficient (10) Developing (5) Inadequate (2) Scores &

Comments

Analysis &

Critical Thinking

Exhibit strong higher-order,

critical thinking and analysis

skills.

Exhibits adequate higher-

order, critical thinking, but

needs improvement on

analysis fundamentals.

Exhibits limited higher-order

critical thinking and analysis,

but able to defend some

arguments.

Exhibit simplistic or

reductive thinking and

analysis, rarely

justifies facts or

relevant arguments.

Often fails to identify strong

relevant arguments; poor

ability to justify results or

facts.

_____20

Logic & Flow of

Thought

Development is logical and

clear to reader; topics are

addressed individually and

linked appropriately, complete

focus on topic.

Exhibits main ideas well

supported by details,

adequate sentence style but

few transitions, word choice

adequate to convey meaning

but few precise or vivid

words.

Clear but uneven

development/narrative details

sketchy, details may appear to

be listed rather than integrated

into coherent flow.

Development is

unclear to reader;

topics may be

inadequately linked,

some details are

irrelevant, order of

ideas not effective.

Development is flawed

(reasoning isn’t sound);

topics are insufficiently

linked.

_____20

Structure &

Organization

Structure & organization are

strong and systematically

organized: introduction and

conclusion are effective;

paragraphs are well developed

and have strong topic

sentences.

Adequately organizes data

/knowledge; focuses on the

important unknown factors;

does not confuse

assumptions with facts;

accurately describes

relationships; able to

independently draw

reasonable conclusions.

Structure & organization are

adequate, the main idea or

story sequence is clear; the

writing has some unity and

coherence, and topic

sentences are weak.

The ideas or events are

not presented in an

effective order,

introduction and

conclusions are not

clear, too many

assumptions.

Flawed structure and

organization: introduction

or conclusion is missing;

paragraphs are

underdeveloped; topic

sentences are missing or

unfocused.

_____20

FORMAT Exceptional (10) Skilled (8) Proficient (6) Developing (4) Inadequate (2) Scores &

Comments

APA Format Complete use of APA

formatting guidelines

throughout the whole

document, inclusive of citations

and references, meets all fonts

and margins as specified.

Minor errors in required

APA sections, citations, or

other APA formatting, all

sources properly cited in

both paper and reference

page

Missing some of the APA

formatting requirements,

incorrect APA paper sections,

some sources not properly

cited, few errors in citation

format

Missing too many of

the APA formatting

requirements, most

sources not properly

cited, missing most of

APA required

sections.

Inadequate use of APA

format, inclusive of

citations and references;

frequency of errors

obstructs clarity for reader,

more than 4 errors per page.

_____10

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 48

LANGUAGE Exceptional (30) Skilled (25) Proficient (20) Developing (15) Inadequate (10) Scores &

Comments

Scholarly Writing

Style/Grammar

Usage

Sentences are consistently

clear, concise and direct; tone

is appropriately

formal/informal. Skills on

grammar usage and mechanics

are strong, rich vocabulary, not

more than 2 errors per page.

Sentences are clear in most

instances, very good

capitalization, adequate use

of language in general, few

or no punctuation errors,

adequate work choice, no

fragments or run-ons present,

not more than 3 errors per

page

Most sentences are simple but

clear, few spelling,

capitalization, or usage errors,

some errors in punctuation,

contain relevant details but

vocabulary is limited, not

more than 5 errors per page

Sentences are

generally wordy

and/or ambiguous;

tone is too informal for

academic writing.

Skills with grammar

usage and mechanics

need much

improvement, not

more than 7 errors per

page.

Sentences are extremely

wordy and the number and

type of errors may interfere

with meaning at some

points. Weaknesses in

command of English

language, too many

spelling, capitalization, or

usage errors, too many run-

ons or fragments.

_____30

Appendix I: Evaluation Rubric for Essays and Written Material (70% content, 30% language)

Points: (content: _____ /15 = _______ x .70) + (Language: __/30 =______x .30) =___________

*The final grade will be obtained from the sum of the 70% content and 30 % language of this rubric.

Comments:

Facilitator’s name:______________________________ Date:____________________________

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 49

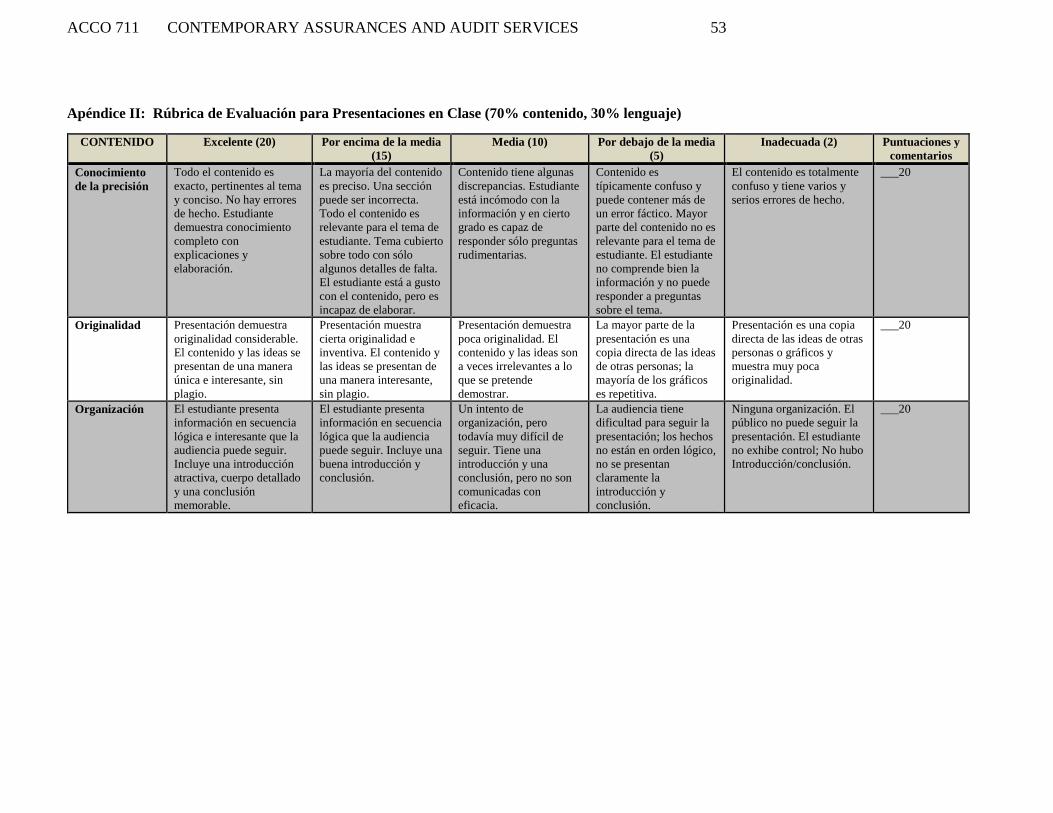

Apéndice I: Evaluación rúbrica para ensayos y material escrito (contenido de 70%, 30% lenguaje)

CONTENIDO

PREPARACION Excepcional (20) Especializado (15) Domina (10) En desarrollo (5) Inadecuado (2) Puntuaciones y

comentarios

Análisis &

Pensamiento Crítico

Exhibe fuertes habilidades

de pensamiento y análisis

crítico, de un orden

superior.

Exhibe adecuado orden de

pensamiento crítico, pero

necesita mejorar en

fundamentos de análisis.

Exhibe limitado orden de

pensamiento crítico y

nivel de análisis, pero está

capacitado para defender

sus argumentos.

Exposición simple o de

pensamiento y análisis

limitado, raramente

justifica los hechos o

argumentos pertinentes.

A menudo es incapaz de

identificar argumentos

fuertes y pertinentes;

pobre capacidad de

justificar los resultados o

los hechos.

___20

Lógica y Flujo de

Pensamiento

Desarrollo es lógico y

claro para el lector; los

temas se tratan

individualmente y están

relacionados

apropiadamente,

demuestra completo

enfoque en el tema.

Expone ideas principales

apoyadas por los detalles,

estilo de oración adecuada

pero pocas transiciones,

selección de palabras

adecuada y transmiten

significado, pero con poca

precisión y orden de

argumentos.

Datos claros pero

incompletos los datos de

desarrollo la narrativa es

desigual y los detalles

aparezcan listados en

lugar de integrar un flujo

coherente.

Desarrollo es confuso al

lector, los temas podrían

relacionarse

adecuadamente, pero

algunos detalles son

irrelevantes, orden de

ideas no es efectivo.

Desarrollo es deficiente

(razonamiento no es

sólido); temas tienen muy

poca vinculación.

___20

Estructura y

Organización

Estructura y organización

son fuertes y

sistemáticamente

organizada: introducción y

conclusión son eficaces;

los párrafos están bien

desarrollados y tienen

fuertes tema oraciones.

Organiza adecuadamente

los datos /conocimientos;

se centra en los factores

importantes y

desconocidos; no

confunde la hipótesis con

los hechos; describe con

precisión las relaciones;

independientemente

conclusiones razonables.

Estructura y organización

son adecuados, la

secuencia principal de la

idea o historia está clara;

la escritura tiene cierta

unidad y coherencia, y las

oraciones del tema son

débiles.

Las ideas o eventos no se

presentan en un orden

eficaz, introducción y

conclusiones no son

claras, demasiadas

suposiciones.

Deficiente estructura y

organización: introducción

o conclusión es falta; los

párrafos son

subdesarrollados; tema

frases son falta o

desenfocado.

___20

ACCO 711 CONTEMPORARY ASSURANCES AND AUDIT SERVICES 50

FORMATO Excepcional (20) Especializado (15) Domina (10) En desarrollo (5) Inadecuado (2) Puntuaciones y

comentarios

Formato APA Uso completo de APA

formato guías a lo largo de

todo el documento,

incluyendo las citas y

referencias, cumple con

todas las fuentes y

márgenes especificados.

Errores menores en las

secciones requeridas de

APA, citas u otro formato

APA, todas las fuentes

correctamente citan en

página de papel y

referencia

Faltan algunos de la APA

formato requisitos,

incorrecta APA papel

secciones, algunas fuentes

no citadas, algunos errores

en el formato de citación

Faltan muchos de la APA

formato requisitos,

mayoría de las fuentes no

correctamente citado, falta

la mayor parte de la APA

requiere secciones.

Inadecuado uso del

formato APA, las citas y

referencias; frecuencia de

errores obstruye la

claridad para el lector, más

de 4 errores por página.

___10

IDIOMA Excepcional (20) Especializado (15) Domina (10) En desarrollo (5) Inadecuado (2) Puntuaciones y

comentarios

Escritura académica

estilo/ uso de

gramática

Las oraciones son siempre

claras, concisas y directas;

el tono es apropiadamente

formales/informales.

Habilidades en el uso de la

gramática y mecánica son

vocabulario fuerte, rico,

no más de 2 errores por

página.

Oraciones son en mayoría

de casos, muy buena

capitalización, uso

adecuado del lenguaje en

general, pocos o ningunos

errores de puntuación,

opción de trabajo

adecuada, sin fragmentos

no más de 3 errores por

página.

Mayoría de las condenas

es simple pero claro,

pocos ortografía,

mayúsculas, o errores de

uso, algunos errores de

puntuación, contienen

detalles relevantes pero

vocabulario es limitado,