Sir, I have a cunning plan. Baldrick - Hinde Capital...Concerns about the UK economy in the...

31

HINDESIGHT DIVIDEND UK LETTER / AUG 16 Mark Mahaffey Ben Davies 1 Aalok Sathe OVERVIEW The Bank of England governor, Mark Carney, took a well-earned rest at the Wilderness festival last weekend where he was seen sporting a glitter eye tattoo and buying a Che Guevara T-shirt. The UK’s central banker had made the bold decision to cut interest rates to 0.25% and add £70bn to the bond-buying programme the prior Wednesday. “Success is the ability to go from one failure to another with no loss of enthusiasm.” ― Winston Churchill Concerns about the UK economy in the aftermath of Brexit have been used as an excuse to continue the grand monetary experiment being employed worldwide from the US to Japan, and Mark Carney was not going to be left out. He has led interest rates towards negative territory and devalued the host currency, £. The reality is that most people, employers and employees alike, are reverting to a time-honoured tradition with regard to difficult discussions, such as Brexit. Namely putting their heads in the sand and pretending it is not really happening. Certainly no one, especially the French, wants it to ruin their ‘Grandes Vacances’ on the beaches of ‘Ile de Rey’ this summer. It reminds me of a friend of mine’s divorce a few years ago. Due to monetary and children concerns, he remained under the same roof with his wife while they lived separate lives for the best part of a year in ‘amicable harmony’. Needless to say, the time came where both parties had to face up to reality and it went downhill very quickly after that. I expect we can look forward to that with regards to Brexit as time goes on. August is often a month where the equity markets are out of favour. In fact, many a financial crisis has started in August. Not this year so far, however, it would appear. Equity markets are leading the charge higher with bond markets not far behind, as they continue to benefit from the central bankers’ money printing and currency devaluations. The innocent bystander might assume that all was thriving in the economic world, but the fundamentals look strangely at odds with stock prices. AUG 16 Sir, I have a cunning plan. ― Baldrick UNIQUE WATERMARK: CBC1F9BF

Transcript of Sir, I have a cunning plan. Baldrick - Hinde Capital...Concerns about the UK economy in the...

HINDESIGHT DIVIDEND UK LETTER / AUG 16

Mark Mahaffey Ben Davies

1

Aalok Sathe

OVERVIEW

The Bank of England governor, Mark Carney, took a well-earned rest at the Wilderness festival last weekend where he was seen sporting a glitter eye tattoo and buying a Che Guevara T-shirt. The UK’s central banker had made the bold decision to cut interest rates to 0.25% and add £70bn to the bond-buying programme the prior Wednesday.

“Success is the ability to go from one failure to another with no loss of enthusiasm.”

― Winston Churchill

Concerns about the UK economy in the aftermath of Brexit have been used as an excuse to continue the grand

monetary experiment being employed worldwide from the US to Japan, and Mark Carney was not going to be left out.

He has led interest rates towards negative territory and devalued the host currency, £. The reality is that most people,

employers and employees alike, are reverting to a time-honoured tradition with regard to difficult discussions, such as

Brexit. Namely putting their heads in the sand and pretending it is not really happening. Certainly no one, especially the

French, wants it to ruin their ‘Grandes Vacances’ on the beaches of ‘Ile de Rey’ this summer. It reminds me of a friend

of mine’s divorce a few years ago. Due to monetary and children concerns, he remained under the same roof with his

wife while they lived separate lives for the best part of a year in ‘amicable harmony’. Needless to say, the time came

where both parties had to face up to reality and it went downhill very quickly after that. I expect we can look forward to

that with regards to Brexit as time goes on.

August is often a month where the equity markets are out of favour. In fact, many a financial crisis has started in

August. Not this year so far, however, it would appear. Equity markets are leading the charge higher with bond markets

not far behind, as they continue to benefit from the central bankers’ money printing and currency devaluations. The

innocent bystander might assume that all was thriving in the economic world, but the fundamentals look strangely at

odds with stock prices.

AUG 16

Sir, I have a cunning plan.

― Baldrick

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 2

UK Purchasing managers – manufacturing index

According to standard observations of GDP growth, industrial production and manufacturing, economies look poised to

go into recession in the near future.

Earlier in the year, we wrote about the potential for corporate profits (earnings) to continue to decline and the evidence

is clear that this phenomenon is very real and ongoing, especially with regard to wage rises cutting into margins. The

chart below (from our friends at the top research house of Variant Perception) demonstrates the point acutely.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 3

Source: Variant Perception

Few stocks can demonstrate that fundamentals are currently playing only a bit part in their share prices more ably than

the case of ExxonMobil Corp, one of the largest companies in the world. Oil prices have dropped from $120 per barrel

in April 2011 to a low of $30 earlier this year, currently trading at $42. As you would expect Exxon’s earnings fell, from

$9.70 in 2012 to $3.85 last year. The 60% drop was the same as the oil price, not really a surprise. What you wouldn’t

expect is for the share price to be unchanged or higher, but that is exactly what has happened. As a result, the

Price/Earnings ratio has exploded higher. This is not an isolated case, as many stocks are seeing reduced earnings,

yet their share prices are not dropping to reflect the worsening conditions. Instead, P/E ratios are being forced higher.

Obviously, a potential conclusion is that with zero interest rates, investors are being forced to seek returns elsewhere

with lessening regard for risk from a historical basis. Chris Dillow’s section in the Investors Chronicle (Aug 11) recently

discussed a study at MIT and Harvard that was based on the decision to invest in risky or risk-free assets with differing

return expectations. The result was clear that with much lower risk-free rates of interest, investors felt compelled to

reach for yield in risky assets in the hope of making a normal historical return.

We should be worried when share prices trade far higher than their fundamentals, based on historical norms. Equity

valuations should be backed up by robust earnings and the less paid for those earning streams the better. With the

economic winds looking distinctly less favourable as well, we do not think it is wise to overstay the party in the equity

markets.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 4

CONTENTS

Inside this edition of the UK Dividend Letter you’ll find:

OVERVIEW 1

INVESTMENT IDEA #1 LLOYDS BANKING GROUP PLC 5

INVESTMENT INSIGHTS 10

PORTFOLIO UPDATE - WHAT HAPPENED? MARKET & SECTOR ANALYSIS 17

HINDESIGHT DIVIDEND UK PORTFOLIO # 1 (AUGUST 2016) 19

ORIGINAL INVESTMENT IDEA SAINSBURY’S (J) PLC 23

APPENDIX I THE WAY WE THINK 28

APPENDIX II HOW WE THINK 29

Our main investment ideas this month are:

1. Lloyds Banking Group PLC

2. Sainsbury’s (J) PLC

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 5

INVESTMENT IDEA #1 LLOYDS BANKING GROUP PLC by Mark Mahaffey

Lloyds Banking Group PLC

Price (£) 52.0

Turnover (£mm) 25,163.0

Net Income (£mm) 860.0

Market Cap (£mm) 37,978.2

Fwd P/E Ratio 7.3

Dividend Yield (%) 4.24%

Payout Ratio (%) -

Total Debt to Total Equity (%) 275.6%

FCF to Market Cap (%) -

ROIC (%) 1.3%

Lloyds Banking Group is a government-backed financial institution that was established after Lloyds TSB acquired HBOS during the depths of the financial crisis in 2009. It is the second oldest banking institution in the UK, after the Bank of Scotland and is currently led by Antonio Horta Osorio. Lloyds Banking Group is listed in the FTSE100 with a market capitalisation over £38bn. In 2015, the firm generated over £11bn in revenues, employing over 88,000 individuals.

Lloyds Bank originally began as Taylor & Lloyds in Birmingham in 1765 when John Taylor (a button maker) and

Sampson Lloyd II (a Quaker iron dealer) formed an alliance to set up their own private banking business. The group’s

association with the Taylor family was later severed in 1852, with the firm then changing its name to Lloyds Banking

Company Ltd. It became a joint-stock bank and opened its first branch in Oldbury in 1864.

Lloyds was the last commercial note-issuing bank in the England & Wales, having bought out Fox, Fowler & Company.

After the 1844 act was implemented, the bank lost its legal right to issue banknotes and so the Bank of England

became the sole note-issuing bank in England & Wales. While some banks in Scotland retained their right to issue

bank notes, the Bank of England was the only entity authorised to issue sterling denominated bank notes. Following a

series of mergers, which included names such as Cunliffe Brooks, Wilts & Dorset Bank and Capital & Counties, Lloyds,

it became one of the four largest clearing banks in the UK. By 1923, it had acquired approximately 50 firms, forming

one of the largest private firms in the UK.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 6

In 1968, Lloyds almost created the biggest banking corporation in the UK, attempting to merge with Barclays and

Martins Bank. Unfortunately for the group, this deal was not authorised as the Monopolies and Mergers Commission

deemed it unfair and not in the public’s interest. The Joint Card Company, which launched the Access credit card in

1972, was formed with Lloyds being one of the founding members, along with National Westminster Bank, Midland

Bank and the National & Commercial Banking Group. Eventually, the Joint Card Company went on to become what is

now known as MasterCard. In the same year that the Access credit card was launched, Lloyds introduced the

‘cashpoint’, which was the first cash machine to use a plastic card with a magnetic strip in the UK, five years after the

first ATM arrived at the Barclays bank branch in Enfield, North London.

By 1995, Lloyds had acquired Cheltenham & Gloucester Building Society, making the combined group one of the

largest UK mortgage lenders. This was quickly followed by its merger with TSB bank. This transaction was slightly

different, as it ended up being a reverse takeover that saw Lloyds Bank plc delist itself from the stock exchange and

TSB Group being renamed as Lloyds Bank plc. This move formed the largest bank in the UK by market share and

second largest by market capitalisation, behind Midland Bank, which is now part of HSBC. The group carried on

growing with further acquisitions, including the Scottish Widows Fund and Life Assurances Society.

More recently, the Lloyds TSB Group acquired HBOS in 2008 and the combined group was renamed as the Lloyds

Banking Group during the financial crisis. The acquisition put the group under major pressure during the liquidity crisis,

at which point the UK government took a 43.4% stake in Lloyds Banking Group, rescuing it from near collapse. The

government’s stake was, however, dependent on the Lloyds selling a proportion of its business by a given time as the

government’s stake was registered as a rescue package. By 2013, TSB Bank was spun off and listed on the London

Stock Exchange, having been bought by the Sabadell Group. TSB Bank is now led by its CEO Paul Pester. With

Banco Sabadell purchasing TSB in March 2015, this meant that Lloyds had finally sold its final holding in TSB. Since

2013, the government has sold back all but 9.2% of its holding in Lloyds. The final sale was scheduled for this spring

but was postponed due to market conditions.

Lloyds generates its revenues through four major divisions:

Retail Banking

Commercial Banking

Insurance

Consumer Finance

The banking industry has been decimated since the financial crisis, being hit with bad loans and PPI payouts. It has

never really recovered as central banks, despite low interest rate policy regimes. Margins have quickly compressed

and equity prices have remained depressed. Last year, it seemed as though the Lloyds share price had started to show

some form of recovery. However, this year its value has been hit once again following the UK’s decision to leave the

EU. Lloyds Banking Group’s share price is down over 25% this year alone. Having traded down violently, its share

price is now expected to strengthen, as its negative move seems to be overdone.

Lloyds Banking Group enters the HindeSight Dividend portfolio this month. We believe the clearly negative factors,

detailed below, are built into its depressed share price. This UK banking giant has been around for centuries and it is

likely to recover over the long term. It currently trades with a forward P/E and P/TBV of 7.46x and 1x respectively. The

firm’s restructuring and recovery have been well documented, having reinstated their dividend scheme for the first time

last year. It is currently offering a yield of 4.27%.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 7

The underperformance in its share price can be attributed to:

Low Rate Environment/Flattening Yield Curves

Brexit & Banking Contagion

Technological Threat

Low Rate Environment/Flattening Yield Curves

Banking is a fairly simple business. Banks borrow money from depositors and the short term funds markets in order to

make loans, usually in the longer-term market. ‘Borrow short, lend long,’ as the saying goes. The interest that they

make on their long-term loans relative to what they have to pay for their short-term borrowings decides the revenue

that they generate. This is the net interest margin (NIM) and the amount of NIM is the main source of revenue, while

the losses, (PPI and fines aside), and are usually the amount of bad debts that have to be covered.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 8

The net interest margin is dependent on the yield curve, the plotted interest rates (y axis) with respect to their maturity

date. Most crises, and 2008 was no different, see the central banks cutting the base rates. This typically steepens the

yield curve, improving margins for the banks. This gives them extra income with which to cover the loan losses that

have resulted from the crisis. As the recovery takes hold, the short-term interest rate is then gradually raised and the

reverse happens. In these troubled times, the central banks have felt the need to maintain rates at zero or even

negative for longer. As a result, the yield curve has flattened considerably as investors are forced out the curve looking

for yield. Historically, a flatter yield curve has always impaired a banking institution’s ability to generate revenues as the

spread in yield compresses, which lowers their net interest margins. Academics at the Bank of England and the BIS

have shown that there is a positive correlation between high interest rate periods and a larger net interest income being

generated (having taken non-interest income and bank loss provisions in to account). With the Bank of England and

other central banks across the world providing an accommodative monetary environment, this has had a significant

impact on the profitability of banking institutions, such as Lloyds Banking Group, over the past few years. Arguably,

despite the reduced ability to generate NIM revenue at low interest rates across the maturity, these same low rates

stem the loan losses, as serviceability of the loan is far easier.

It is evident from the chart above that as the yield curve starts to steepen (10Y yield - 2Y yield >0), equity market

returns within the banking sector also turn positive. It can be seen that over the past five years, we have we have been

in a situation where the spread between the 10Y and 2Y has been getting smaller month-by-month, leading to banks

generating less revenues and posting very poor equity returns as suggested by academics and historical evidence.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 9

Despite the BOE governor Mark Carney cutting rates to a new low of 0.25% last week in the UK and adding £70bn to

the QE bond buying programme, we believe he is less determined than his central bank counterparts elsewhere to

charge into negative territory. He is quoted saying that pushing rates below zero is self-defeating since banks are

unlikely to pass negative rates on to their customers and would then be forced to increase lending rates to aid their

already weak margins. While most investors do not think interest rates are going up anytime soon, we are far into the

world of unknown. Strangely, a burst of inflation that would see bond investors head for the exit as the yield curve

steepens night well be the most bullish news for banking stocks.

Brexit & Banking Contagion

The result of the EU referendum immediately saw an aggressive negative reaction in the share price of most banking

stocks. The vote left the sector trailing once again, having suffered last year as commodity prices and emerging

markets fell sharply. The financial services were the worst hit across all industry groups with banking stocks topping the

list. The five subsequent days following the Brexit vote saw UK banks down on average over 22%, with Lloyds Banking

Group being hit hard as investors have been worried by its exposure to the retail mortgage market and the potential

impact that the decision to leave the EU would have on the institution’s business.

Brexit has only added to the fragility of the banking system because the markets have already seen global tremors as

participants have been concerned about the level of bad loans being held by many institutions across Europe. At the

heart of these worries sit the Italian banks, where investors have been spooked by the £300bn in bad loans, £80bn of

which have already been written down. Fears of contagion have regularly sent jitters across Europe and there are

many who feel that these could spread into the UK banking system, which has suppressed prices over the past two

years.

The management team at Lloyds have been working hard as they implement a restructuring programme that is helping

the firm to save costs across its business. The initiative involves shedding jobs and closing over 200 branches by the

end of 2017. The team also intends to generate further savings by reducing its non-branch property portfolio by 30%,

which will help to save an extra £400m and bring its overall savings to £1.4bn.

With Lloyds’ share price having already faced a significant devaluation, the damage may already be done. This will

leave investors in a position where the risk/reward in its share price as the bank is to the upside. There was better

news recently when the bank performed the best out of all the UK banks during the stress tests carried out, registering

10.1% for its common equity tier one ratio.

Technology Threat

The financial crisis in 2008 left many individuals reconsidering the lending business as a whole and has left traditional

banks facing greater competition. Many retailers are also teaming up with financial technology companies and building

their own payment systems. The big four banks cannot afford to ignore the threat of challenger banks and new

payment technology. Consultancies have estimated that this will reduce the market share of the banks by a third by

2020. Other threats scaring the market include the Bank of England’s research into a bitcoin-style electronic pound.

Several papers have already been written about this topic, with the news worrying banking investors as, in time, this

could reduce deposits across the sector.

To address this situation, Lloyds have been working on four core points that include making better use of consumer

data, trust, security and humanising banking/innovation. Executives said that Lloyds are looking to build on their current

digital relationships with consumers and they are doing this by investigating ways in which they can help over five

million mobile banking users to balance their finances through mobile applications. Up until now, Lloyds have been in a

technological ‘stone age’ but it has significantly invested in implementing big data. The bank offers clients a

customised/humanised service by giving big data a larger role in the way it operates. It is hoped that Lloyds will

generate greater revenues going forward with this more hands-on offering, as well as an increasing customer retention

rate.

Analysts’ Corner

Lloyds Banking Group has a long history within the UK and historically been a strong business with excellent dividends.

It is well covered by the analyst community with 22 out of 28 individuals giving the stock a buy or hold rating. Our

scoring system suggests that the stock has an average 12-month target price (TP) of 67.85p, representing an upside of

over 23%.

Summary

Lloyds trades at a discount to itself however it is in line with its peer group. The banking business has suffered greatly

over the past eight years, as a result, of a series of events that started with the 2008 crisis. The stock has traded down

significantly over the past year; however, it is still a high-quality retail and commercial bank that generates attractive

returns relative to its peer group. While there is uncertainty surrounding the UK economy, the banking giant’s

valuations are trading at attractive levels. With the institution implementing its restructuring programme and still firmly

backed by the UK government, we believe that less negative or even good news will translate into a positive rerating of

its share price from its current depressed levels while also collecting a healthy dividend.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 10

INVESTMENT INSIGHTS

Barclaycard was launched 50 years ago this year, becoming the first credit card introduced in the UK. While American

Express and Diners Club issued their charge cards a few years prior, Barclaycard enjoyed a credit monopoly in the UK

until the arrival of the Access card in 1972. Many people will remember those early Barclaycard adverts with Alan

Whicker travelling across the globe, followed by the later Rowan Atkinson’s Johnny English antics.

Today, Barclaycard has over 10 million customers in the UK alone, issuing one in five of the UK’s credit cards.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 11

Access to credit has revolutionised people’s spending abilities. There is no need to save and wait for that exciting

purchase. One swipe of the plastic and hey presto, all your immediate desires are realised today and no payment until

tomorrow!

Unfortunately, the increasing growth in credit card balances is not the only explosion of debt. Despite the belief that the

world has recovered from the 2008 financial crisis, nothing could be further from the truth with regards to our growing

indebtedness. Whether it is government, corporate or personal debt, it is has grown at alarming rates in the last 50

years, especially in the last decade. In David Graeber’s book, Debt: The First 5000 years, he tells us that debt

preceded coinage by 600 years in around 3500 BC. The promise to pay later for already handed over goods was the

basis of trade.

In the famous scene from the hysterically funny series, Blackadder Goes Forth, Captain Blackadder is asked to explain

the causes of World War I as the troops sit in the trenches waiting to go over the top. The dialogue is too good not to

write out in full.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 12

That’s the problem with many plans, they turn out to be total bollox. If you are looking for the current example of an

exceptionally poor plan, you needn’t look any further than the interest rate policies of most countries around the world.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 13

Most countries have lowered their interest rates towards and even through zero in the last decade while also employing

quantitative easing in many forms (money printing) in the belief that it is the best response to try and stimulate

weakening economies. Unfortunately, our central bankers and politicians – who tend to spend their whole lives in

academia or government, rarely venturing out into the real world – have taken a basic economic concept and run with it

to the Nth degree.

In their world, lower interest rates mean that indebted entities can reduce their interest cost burdens by either paying

down the debt or borrowing money to invest in long-term productive enterprises, which will generate greater future

cash flow than the cost today and future interest cost.

However, in the real world, the results are entirely different and will be associated with the causes of the coming

disaster when the historians write a record of it.

Lower interest rates increase debt levels, with the lower the interest rate, the greater the debt taken on in some

short-term belief that servicing debt is the only relevance. Capital repayment is barely considered.

Debt taken out today is spending tomorrow’s earnings, irrespective of who is taking out that debt. Unless that debt is

going to produce a reliable future cash flow, the debt will need to be repaid from earnings or defaulted on at some time.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 14

UK Government Debt as % of GDP

While the ageing population and immigration may be the root cause of the increase in government borrowing, the basic

inability to maintain a budget is central to any argument. Governments are not immune from increasing their borrowing

as interest rates decline. (One of the most dramatic episodes of this phenomenon was the Greek tragedy, as their

entrance to the EU saw interest rates drop to German levels and debt levels increase dramatically. The party lasted for

a while before the piper had to be paid.)

Source: Variant Perception

In the corporate world, lower interest rates allow companies to increase profits by replacing share equity for debt. In the

short term, share buybacks or increased debt levels relative to equity (gearing) mask the risks, as valuations stay

elevated. Unfortunately, any return to normal P/E levels or higher interest rates will quickly show the error of their ways.

Another result of low interest rates in the corporate world is the ability for ‘zombie’ companies to remain in business.

These ‘zombie’ companies have very marginal profitability. In normal times their inefficient businesses would not

survive as they just don’t produce enough income relative to cost. Arguably, even ‘zombie’ companies employ people

but it should be obvious that the system is inherently unstable at the margin as a result.

At a personal level, most people’s largest debt by far is the mortgage on their home. Low interest rates have fuelled

increased debt levels, forcing people to accept far higher home values than income alone would dictate despite new

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 15

‘tighter’ regulation. If interest rates were to rise, most mortgage holders would be in severe trouble of servicing their

loans and property values would tumble and worsen the situation.

Lower interest rates go hand in hand with an increase in debt levels at every level but they also carry another worrying

outcome.

James Grant of the Grant Observer is one of the longest-serving financial journalists, but when he was recently asked

about how an investment return could be made, he replied: ‘I’m stumped.’ He is not alone. With trillions of government

debt worldwide trading at negative yields that are guaranteed to make an investment loss, just breaking even is proving

to be hard for many. Let us not forget that negative interest rates and ballooning central bank balance sheets have

NEVER been tried before in the last 5000 years.

CalPERS (The California Public Employees’ Retirement System) has $300bn under management and is the largest

public pension fund in the US. It recently announced it had made less than 1% investment returns for the last 12

months. It has annual commitments for retirement and health benefits for 1.6 million employees over $20bln, yet it can’t

make a dime!

While fixed income has made up a large percentage of less risky assets for most portfolios historically, investors are

being forced into much higher risk assets to have any hope of an investment income. Unfortunately, these come with a

far greater potential for capital loss than was historically the case. Stocks and property trade on such obscene multiples

in exchange for a meagre income, offering the real possibility of 50% capital losses in the future.

It all seems a far cry from yesteryear. Older readers might remember the late 1980s adverts for the Leeds Building

Society, the Liquid Gold account that was advertised by George Cole from the long-running Minder TV series.

It offered 10%+ annual returns in a boring building society.

UK annuity rates for pensioners have been declining every year.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 16

UK Annuity rates

Source: The Telegraph

Whether you are CalPERS or an individual, it becomes clear quite quickly that if you are not able to make an income

on your savings, the most likely scenario is that you will end up drawing down on capital when you need it. The

likelihood of being able to enjoy your retirement care free will be a thing of the past, as most pensioners will be forced

to work into old age and ill health. The papers may be full of stories about Sir Philip Green having blown a deficit in

BHS’s pension pot, but the reality is that worldwide, the zero interest rate policy is destroying most people’s pension

plans.

While most people have a general idea that house prices are really high, they can’t make any money on their savings

and they maybe have too much debt on their credit cards, they don’t understand the current situation is unprecedented

in history.

Zero or negative interest rates have blown up a debt balloon of humongous proportion, for savers there is no risk-free

income (at negative rates it is a tax on your savings) and most of the asset classes backed by this debt build-up have

risen to levels that are completely unsustainable against the fundamentals in the long run. (Whether it is equity P/E

ratios or property/income ratios.)

The central bankers and politicians, who have employed this zero interest rate and crazy monetary policies, have no

history to guide them. This is a first-time live experiment. One principle even a central banker should be able to

understand, debt like negative interest rates must have a limit. Once that limit is breached, catastrophe can be the only

outcome. It is not a question of if, but when. We believe that we are in the very last stages of that stability, as the

cracks are already showing.

The historians will not be kind to the planners of this monetary experiment. As Blackadder would say, there was a tiny

flaw with the plan – it was total bollox.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 17

PORTFOLIO UPDATE - WHAT HAPPENED? MARKET & SECTOR ANALYSIS

UK Market Valuations

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 18

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 19

HINDESIGHT DIVIDEND UK PORTFOLIO # 1 (AUGUST 2016)

Portfolio Update and Construction

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 20

PORTFOLIO UPDATE

Greene King plc

Greene King plc had an ex-dividend date on 11th of August 2016 for 23.60p.

GKN PLC

GKN plc had an ex-dividend date on 11th of August 2016 for 2.95p.

Sainsbury’s (J) Recommendation (Again)

Readers of the HindeSight Letter will have received a buy alert from Sainsbury’s on 4th August at 224.50p. Sainsbury’s

has featured in the dividend portfolio previously from December 2014 (with a similar purchase price of 226.40p as this

recommendation) until March 2016 making a total return of 30.1% including 5.3% of dividends.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 21

As we mentioned last month with the re-introduction of TalkTalk to the portfolio, over time we will invest in many stocks

several times over the years as we believe not just in the cyclicality of stocks and industry groups but also that stock

prices tend to move far more than the fundamentals might suggest in the short term. If we look at the chart of

Sainsbury’s we can see that over the last 8 years, the price has ranged between 200-400p and more recently 220-

300p. The previous trade analysis suggested that Sainsbury’s was cheap on purchase in 2014 at 226p and fair on exit

at 280p and there are similarities to today’s market. We continue to understand the general poor performance of the

big supermarkets as they compete with the discounters like Aldi and adjust to the changing shopping habits of

consumers. Current margins are under pressure despite solid revenue and relatively unchanged market share for

many years.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 22

Sainsbury’s recently approved takeover of Argos/Home Retail group has had mixed reviews within the investor

community after it had only just closed the doors on its joint venture with Danish discount supermarket Netto with costs

of £20mil closing the 16 joint stores. However, Argos might prove to be the turnaround in fortunes that Sainsbury’s are

looking for as Argos actually enjoy rising total sales both from new stores and online sales.

Looking at the Price/Earnings ratio on the chart below, we feel that we are hardly overpaying for earnings especially

when many large cap stocks have P/E ratios closer to 20 times as low interest rates force valuations higher. Food

suppliers have generally been seen as defensive investments by nature and margins have proved to be cyclical in the

past as they may well be again.

With a dividend yield of 5% and an entry price of 224.50p, we believe that Sainsbury’s offers us a reasonable margin of

safety at these levels on an outright and relative basis. Our path analysis that measures each individual stock against

every other component of the FTSE 100 index suggests that Sainsbury’s is in the top ten of cheapest stocks

collectively.

We have attached the full write of Sainsbury’s from last year at the back for the letter for further reading.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 23

ORIGINAL INVESTMENT IDEA (DECEMBER 2014) SAINSBURY (J) PLC

Sainsbury’s (J) PLC

Price (£) 241.0

Turnover (£mm) 23,949.0

Net Income (£mm) 716.0

Market Cap (£mm) 16,874.6

Fwd P/E Ratio 129.7

Dividend Yield (%) 8.2%

Payout Ratio (%) 45.9%

Total Debt to Total Equity (%) 54.2%

FCF to Market Cap (%) -4.9%

ROIC (%) 1.5%

Sainsbury’s (SBRY) needs no introduction. A staple part of most shoppers’ diets over the decades, it has

navigated the stagflation of the 70s, the 90s price wars and has embraced internet shopping online. Shopping

habits have changed in recent years as efficiencies in distribution technology have enabled more competition

and more consumer choice. We all know about the price sensitivity of the 99% – as the Occupy movement

refers to the majority who experience income inequality – and this has seen an emergence of the discount

stores’ winning market share. However, you may be surprised to know that Sainsbury’s has lost no market

share on a revenue per share basis! Although Tesco may be down 44% year to date, at its lows Sainsbury’s

was down nearly 40%. So what gives with Sainsbury’s?

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 24

The UK grocery market has been the subject of two major competition inquiries in recent years. In October 2000, the

Competition Commission completed the first of these and it led to the creation of a Code of Practice to regulate the

relationship between the largest supermarkets and their suppliers.

However, the OFT received many complaints that the Code was not preventing supermarkets exploiting some of their

suppliers, and putting many small shops out of business. In May 2006, the OFT referred the market to the Commission

for a second time. In April 2008, the Commission completed its inquiry, concluding that in many respects UK grocery

retailers were “delivering a good deal for consumers”, but that action was “needed to improve competition in local

markets and to address relationships between retailers and their suppliers”, including a strengthened and revised Code

of Practice to be enforced by an independent ombudsman.

The outcome of this inquiry has benefited supplies by preventing supermarkets from passing on unexpected costs to

suppliers, which means in the latest price wars they cannot price gouge their suppliers anywhere to the extent that they

used to be able to. Of course, this means they cannot maintain their margins so easily in these new price wars. This

has a structural impact on the sector, but we believe SBRY is more immune and can survive and thrive in this

environment.

The last albatross in the Antarctic is most probably aware now of the dismal state of affairs of the UK supermarket

sector and the price wars with the dreaded discounters Lidl and Aldi. Whilst Tesco has seemingly borne the brunt of

the problems, Morrisons and SBRY have had their fair share of misery.

They have all managed to take the standard non-cyclical defensive business model – selling the basic

essentials of foodstuffs (yes we know, there is more to them than selling food) – and turned their businesses

into troubled going concerns.

Current Market Share vs 2007 Market Share for the Supermarkets

SBRY currently is our highest ranked stock from the FTSE 100 on the Hinde Dividend Value Matrix ® with an

outstanding score of 62.40. Despite the high-rating ‘accolade’ HDVM ® has given it, this is partly a reflection

of the dire share price performance over various time frames, down over 32% year to date.

A backgrounder on Sainsbury’s

Established in 1869 at 173 Drury Lane in Holborn, London, as a partnership by John James Sainsbury and his wife, the

trading motto was “Quality perfect, prices lower”. At the time of his death in 1928, there were 128 shops and when the

now limited company went public in 1973, it was at the time the largest flotation on the London Stock Exchange.

Today, SBRY has 161,000 employees referred to as ‘colleagues’, almost £25bn in revenue and £800 mm in net

income with 16.1 % of the UK supermarket share. Its store sizes’ vary from 10,000 to a colossal 100,000 square feet.

While much has been written about the huge, out-of-town hypermarkets and how most of them are not suited to the

needs of today’s shoppers, almost half of their stores are Sainsbury’s ‘Local’ convenience stores.

SBRY isn’t just a food store. Its diversification seems unending from Sainsbury’s fuel, pharmacy to bank and mobile

services – it truly caters to a broad spectrum of our daily necessities.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 25

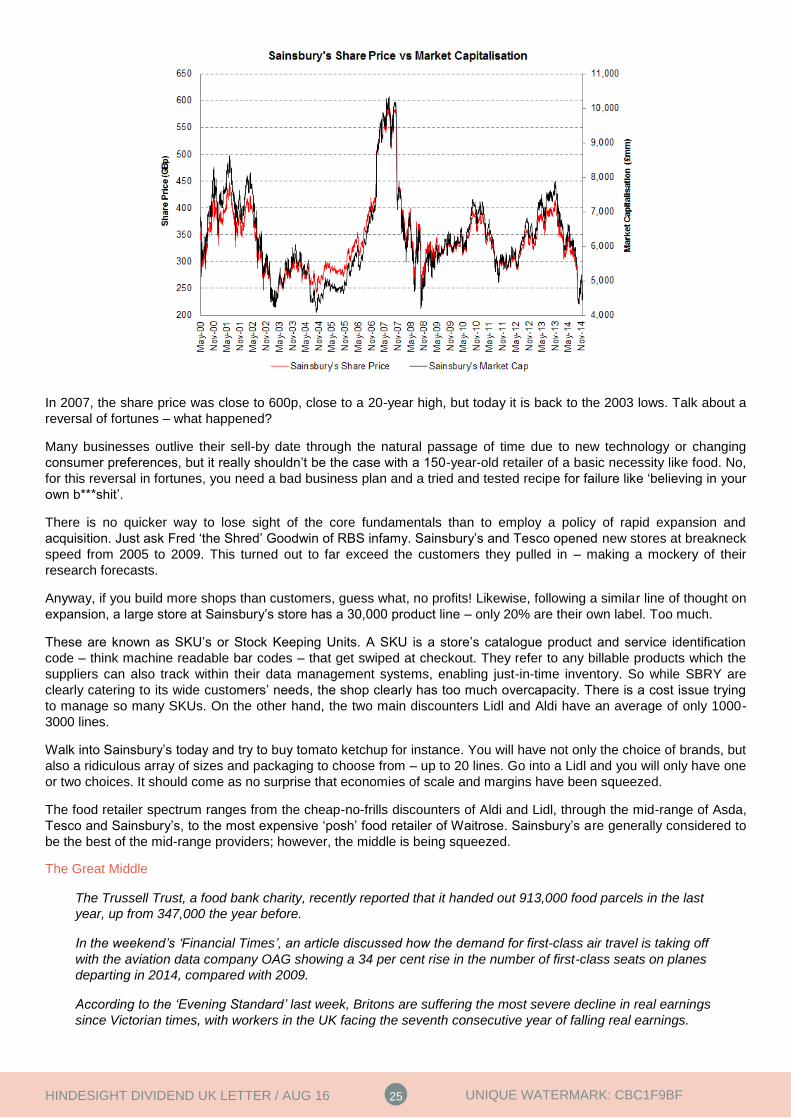

In 2007, the share price was close to 600p, close to a 20-year high, but today it is back to the 2003 lows. Talk about a

reversal of fortunes – what happened?

Many businesses outlive their sell-by date through the natural passage of time due to new technology or changing

consumer preferences, but it really shouldn’t be the case with a 150-year-old retailer of a basic necessity like food. No,

for this reversal in fortunes, you need a bad business plan and a tried and tested recipe for failure like ‘believing in your

own b***shit’.

There is no quicker way to lose sight of the core fundamentals than to employ a policy of rapid expansion and

acquisition. Just ask Fred ‘the Shred’ Goodwin of RBS infamy. Sainsbury’s and Tesco opened new stores at breakneck

speed from 2005 to 2009. This turned out to far exceed the customers they pulled in – making a mockery of their

research forecasts.

Anyway, if you build more shops than customers, guess what, no profits! Likewise, following a similar line of thought on

expansion, a large store at Sainsbury’s store has a 30,000 product line – only 20% are their own label. Too much.

These are known as SKU’s or Stock Keeping Units. A SKU is a store’s catalogue product and service identification

code – think machine readable bar codes – that get swiped at checkout. They refer to any billable products which the

suppliers can also track within their data management systems, enabling just-in-time inventory. So while SBRY are

clearly catering to its wide customers’ needs, the shop clearly has too much overcapacity. There is a cost issue trying

to manage so many SKUs. On the other hand, the two main discounters Lidl and Aldi have an average of only 1000-

3000 lines.

Walk into Sainsbury’s today and try to buy tomato ketchup for instance. You will have not only the choice of brands, but

also a ridiculous array of sizes and packaging to choose from – up to 20 lines. Go into a Lidl and you will only have one

or two choices. It should come as no surprise that economies of scale and margins have been squeezed.

The food retailer spectrum ranges from the cheap-no-frills discounters of Aldi and Lidl, through the mid-range of Asda,

Tesco and Sainsbury’s, to the most expensive ‘posh’ food retailer of Waitrose. Sainsbury’s are generally considered to

be the best of the mid-range providers; however, the middle is being squeezed.

The Great Middle

The Trussell Trust, a food bank charity, recently reported that it handed out 913,000 food parcels in the last

year, up from 347,000 the year before.

In the weekend’s ‘Financial Times’, an article discussed how the demand for first-class air travel is taking off

with the aviation data company OAG showing a 34 per cent rise in the number of first-class seats on planes

departing in 2014, compared with 2009.

According to the ‘Evening Standard’ last week, Britons are suffering the most severe decline in real earnings

since Victorian times, with workers in the UK facing the seventh consecutive year of falling real earnings.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 26

It would appear that QE programmes employed by the world’s central banks are really making the rich richer

and the poor poorer while wiping out the middle classes.

Human nature as it is, unfortunately makes poor decisions when everything is going well and much better decisions

when the proverbial has hit the fan. Today, let’s just say the fan is fairly messy to say the least. According to 'Healey’s

Law', named after British politician Denis Healey, the best way to dig oneself out of a hole is to stop digging.

In the latest interim report, Sainsbury’s CEO Mike Coupe announced it would be undertaking a complete strategic

review covering dividends, business strategy and capital expenditure. The group has stated that they are confident in

their accounting process – it's a very ‘rigorous process’ – and will:

Deliver cost savings of £500mm over the next 3 years

Reduce capital expenditure to two per cent of sales

Fix dividend cover at 2.0 times underlying earnings

Continue to diversify into growing non-food areas

New pricing policy will Brand Match to Asda and no longer Tesco

SBRY are on average 50% cheaper on brand match comparison

It appears the digging may have stopped and better decisions will prevail, as a result of the low share price.

The recent joint venture with Danish discount chain Netto is SBRY's move to capture more of the £10 bn a year UK

discount sector. With Netto initially based in the north of England where SBRY is weak, this looks a reasonable

venture.

Although Tesco’s dividend cut came to a resounding fanfare, Sainsbury’s have made sure all the analysts have revised

down their final dividend payment to 8p from 12.3p, despite the interim being unchanged recently. This will still make

the dividend yield around 5.5%.

SBRY might not have lost market share like Tesco, but again analysts are concerned that margins can’t regain the

+5% level of a few years ago for the industry as a whole. However, despite the low EBIT margin we believe the

differentiation we mentioned means SBRY doesn’t have to enter into price wars as much as the other players of the

Big Four – Tesco, Asda and Morrison’s.

Analysts’ Corner

In our External Analyst scoring system, Sainsbury’s lies at 44.55, which is in the bottom third of the index. The general

analyst consensus has been very bearish (with 17 out of 24 analysts giving a hold or sell recommendation). However,

the score has been turning more positive over the past month. The average 12-month target price (TP) is 262.35p, a

12.4% upside from current levels. The firm’s current valuation metrics look severely beaten up due to structural

changes that the grocery industry is going through.

Our external analyst scoring system* places Sainsbury’s at 44.55 (range 30-70), which is a negative position.

This score has become more positive relative to a month ago with analysts seeing improved conditions.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 27

*(Please see the Portfolio section for a description).

Summary

Is Sainsbury too contrarian an investment play? Is it a value trap? In short, has the price fallen to bargain basement

levels?

It may well be seen as a contrarian play but some of the best investments often are. Sainsbury’s is paying a dividend of

over 5% for the time being. It is not at the mercy of the price wars. It is cutting costs, it is taking note of what the

growing competitors are doing and continues to diversify. The current price provides excellent protection – a margin of

safety with a tremendous amount of bad news priced in. We believe SBRY is a very cheap defensive high yielder and

so is a good addition to the HindeSight portfolio this month.

HOT OFF THE PRESS

At the time of publishing this letter we saw rumours of activist’s buying stakes in SBRY:

UK activist investment fund Crystal Amber (CRSL.L) is in talks with several overseas investors about buying

shares in Sainsbury's (SBRY.L), as part of a plan to shake up the food retailer that could cause a takeover bid to

be made, The Sunday Telegraph newspaper said

Some 26 per cent of Sainsbury’s equity is owned by the Qatar Investment Authority, which walked away from a

possible takeover in 2007, while the different parts of the Sainsbury family own around 11 per cent

We think the activist talk is just that, mainly ‘talk’, but it does highlight the vulnerability of SBRY’s to aggressive

external interest seeking corporate restructuring and break-up value

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 28

APPENDIX I

THE WAY WE THINK

We passionately believe that dividends really, really matter.

William Thorndike in his fascinating book ‘The Outsiders - Eight Unconventional CEOs and Their Radically Rational

Blueprint for Success’ examined one of the most important aspects of running a business a CEO must undertake:

Capital Allocation. He summarised how a CEO deploys capital in order to best utilise cash flow generated from his or

her business operations. Essentially, CEOs have 5 ways of deploying capital:

Investing in existing operations

Acquiring other businesses

Repaying debt

Repurchasing their own stock (buybacks)

Paying dividends

Dividend payments are a crucial operation in creating stakeholder wealth. It is this aspect of a business that we are so

fixated by – the propensity for a company to produce and continue to grow dividends so that we may accrue wealth

over a generation. But as readers will know we can’t just grab stocks with the highest yield for fear that this signals

some cash flow or even solvency issues for the firm. So it is with this very real threat in mind we explore only well-

capitalised FTSE 350 companies.

This letter’s purpose is to help inform readers on dividend investing so that they can construct a portfolio of sound UK

dividend stocks based on our recommendations.

Our prerequisite is that any stocks selected for this letter must be liquid, well-capitalised with a strong free cash flow

and a progressive dividend policy.

Our System

Every month we will provide a write up of 3 to 4 stocks until we create a portfolio of 25 UK dividend stocks. This

will be the HindeSight UK Dividend Portfolio #1

You will be alerted by subscriber email intra-month when these stocks become a buy. Timing is critical to the

strategy, not only buying quality stocks but buying them at the right time

The entry points will then be recorded in the next monthly in the HindeSight UK Dividend Portfolio section and the

stock(s) written up in full

We will run our winners but tend to rotate every 6 months depending on specific criteria which would elevate

cheaper companies into the portfolio relative to stocks that had performed

The basis for stock and portfolio selection is derived from our quantitative systematic methodology which screens

these companies using the Hinde Dividend Value Matrix®, (HDVM®), a proprietary stock-rating system

In the section on ETPs we will highlight our investment philosophy and the investment process behind our stock

selections. This is the basis of our dynamic risk and money management in our portfolio construction for you. You

can also read the stand-alone Hinde Dividend Value Strategy document to see the methodology behind our stock

selection

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 29

APPENDIX II

HOW WE THINK

“We have met the enemy, and he is us.” Walt Kelly

Our key to long-term performance investing is premised on the following:

Systematic rule-based strategy

Systematic risk and money management

Occam’s razor, aka ‘K.I.S.S.’, Keep It Simple Stupid

Consistency

Discipline

All our investment ideas are rule-based methodologies driven by systematic and quantitative models.

Hinde Dividend Value Strategy

Hinde Dividend Value Strategy seeks to generate a total return from an actively managed basket of UK dividend-

paying stocks. The strategy selects 20 highly liquid, mid-to-large capitalised stocks on an equally-weighted basis,

which offer the highest total return potential. The 50% Hedge version of the strategy would then be subject to a

strategic Beta Hedge*, which is designed to cover 50% of the value of the UK stock basket at all times.

The 50% hedge is maintained using UK equity benchmark indices to reduce exposure to overall market volatility, but

without reducing overall total returns to the market over the long run. The Hinde Dividend Value Strategy (100%

Hedge) would deploy a full beta hedge at all times.

Hinde Dividend Value Matrix®

The strategy employs a quantitative, systematic methodology, whereby FTSE 100 and FTSE 250 constituent stocks

are screened using the Hinde Dividend Value Matrix®, a proprietary stock-rating system. We use the same system to

select stocks for any of our strategies, long-only, 50% Hedge or 100% Hedge. The only difference is clearly the extent

of the hedge on the exposure to the overall market.

The basic premise of the strategy is to accelerate returns by selecting relatively high yielding stocks which offer the

highest potential for capital revaluation. The dynamic rotation of stocks each quarter enables us to sell stocks where

the capital revaluation and dividend has been captured, and use this additional capital to invest in more undervalued

quality companies. If successful, this cycle of capture and re-investment offers the chance to significantly improve the

total return generated by the Dynamic Portfolio.

The basis of the stock selection process is the Hinde Dividend Value Matrix®, which is a derived process that looks at

3 crucial variables:

* Beta is the stock’s sensitivity to market movements, e.g. if a share has a beta of 1.5 its price tends to move by 1.5% for each 1% move in the index

1. Dividend Screen

The top ranking stocks will be those offering a relatively high dividend. A composite of the following criteria comprises

the Dividend Rank:

Relative Dividend Yield

Dividend Capture

Payout ratios

The Relative Dividend Yield assesses if a company pays a higher dividend than the Index it derives from (the FTSE

100 or FTSE 250). The Dividend Capture criteria explain how quickly and how much of the dividend is paid at any point

in time. The Payout Ratio gives a snapshot of whether a company will be able to maintain and grow its dividend. It

helps us to assess how much of a company’s revenue, profit or cashflow is paid out in dividends.

The lower the amount of dividends paid out as a percentage of profits, the healthier future dividend potential will be.

History is for once a good guide as to whether companies will continue to pay and grow their dividends. A stock with an

excessively high yield relative to its sector or the overall market is invariably showing signs of heightened risk to its

dividend sustainability and often the viability of the company itself. The screen incorporates a limit on yield dispersions

from the overall market.

The strategy is emphatically not a yield chaser. It is the Performance and Value screens that are used to assess the

total return potential of a stock by analysis of how undervalued it is relative to its fundamentals, sector and overall

market index.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 30

2. Performance Screen

The top ranking stocks have the poorest relative performance to their index over multiple time horizons.

A composite rank of the following criteria provides the Performance Rank:

Stock relative performance ranked over multiple time periods

Average of time periods taken to select rank of stocks

3. Value Screen

The top ranking stocks by key fundamental criteria show stable fundamentals and exhibit upside momentum growth

potential. The following are some of the criteria that provide the Value Rank:

Value - Price to Book (intangible book adjustment), Free Cash Flow metrics

Quality - Return on Investment and Earnings metrics

Financial Stability - Debt levels, Coverage and Payout ratios

Volatility - Stock variance, Dividend variance

Momentum - Sales Growth, Cashflow metrics

Liquidity - Minimum market capitalisation relative to index, Shares outstanding

Implementing the Hinde Dividend Value Matrix®

The FTSE 100 and FTSE 250 stocks are ranked using the Dividend, Performance and Value screens. An equally-

weighted composite rank is then taken of these 3 ranks, which provides a final ranking from which a selection of 20

stocks is made for the portfolio.

The stocks with the highest ranking are compiled for the FTSE 100 and the FTSE 250. The top 10 from each index are

then taken, subject to diversification rules, which entail that normally only 1 stock per sector per index can be invested

in. For example, if the top 10 stocks are all mining companies, the selection process would take the first of these and

then move on to select the next top stock from another sector. As long as a stock has the highest score in its sector,

the fact that it has appeared in the final ranking means it is already eligible for investment. In exceptional

circumstances, it may be that more than one stock has to be selected from an individual sector.

UNIQUE WATERMARK: CBC1F9BF

HINDESIGHT DIVIDEND UK LETTER / AUG 16 31

External Analyst Score (EAS)

This score is derived from 3 inputs that have been obtained from all the external analysts at leading institutions who are

covering the stock:

1. The 12 month target price in relation to current price

2. The number of analysts covering the stock

3. The recommendation analysis, e.g. STRONG SELL, SELL, UNDERPERFORM or HOLD

This score is used to observe the other analysts’ view of the stock and is helpful when understanding the methodology

that other analysts use to determine their 12-month target price. We ultimately get a blend of price targets that is based

on different valuation metrics.

EAS Score Output:

1. The combined score will vary from 30-70

2. A stock with a lowest score of 30 shows the majority of analysts not only have a full sell/underweight

recommendation, but also a low 12-month target price in relation to current price.

3. A stock with the highest score of 70 shows the majority of analysts not only have a full buy/overweight

recommendation, but also a high 12-month target price in relation to current price.

Note:

- On a standalone basis, the EAS score must be viewed in the following context:

Equity analysts issue far more positive recommendations than negative

If all analysts are overwhelmingly bearish or bullish, then this can signal a contrarian position be held, but this is

determinate on the where the stock is valued.

- However, in conjunction with the HDVM®, we have found the score to be useful when it is high or momentum is

turning higher, as this suggests that the stock offers deep value.

Disclaimer This newsletter is intended to give general advice only on the importance of dividends within the equity space. The investments mentioned are not necessarily suitable for any individual, and you

should use this information in conjunction with other advice and research to determine its suitability for your own circumstances and risk preferences. The value of all securities and investments, and the income from them, can fall as well as rise. Your investments may be subject to sudden and large falls in value and you may get back nothing at all. You should not buy any of the securities or other investments mentioned with money you cannot afford to lose. In some cases there may be significant charges which may reduce the value of your investment. You run an extra risk of losing

money when you buy shares in certain securities where there is a big difference between the buying price and the selling price. If you have to sell them immediately, you may get back much less than you paid for them. The price may change quickly, particularly if the securities have an element of gearing. In the case of investment trusts and certain other funds, they may use or propose to use the borrowing of money to increase holdings of investments or invest in other securities with a similar strategy and as a result movements in the price of the securities may be more volatile than the

movements in the price of underlying investments. Some investments may involve a high degree of ‘gearing’ or ‘leverage’. This means that a small movement in the price of the underlying asset may have a disproportionately dramatic effect on your investment. A relatively small adverse movement in the price of the underlying asset can result in the loss of the whole of your original investment. Changes in rates of exchange may have an adverse effect on the value or price of the investment in sterling terms, and you should be aware they may be additional dealing, transaction and custody

charges for certain instruments traded in a currency other than sterling. Some investments may not be quoted on a recognised investment exchange and as a result you may find them to be ‘illiquid’. You may not be able to trade your illiquid investments, and in certain circumstances it may be difficult or impossible to sel l or realise the investment. Investment in any of the assets mentioned may have tax consequences and on these you should consult your tax adviser. The opinions of the authors and/or interviewees of/in each article are their own, and are not necessarily those of the

publisher. We have taken all reasonable care to ensure that all statements of fact and opinion contained in this publication are fair and accurate in all material respects. All data is from sources we consider reliable but its accuracy cannot be guaranteed. Investors should seek appropriate professional advice if any points are unclear. Ben Davies and Mark Mahaffey the editors of this newsletter, are responsible for the research ideas contained within. They or any of the contributors or other associates of the publisher may have a beneficial interest in any of the investments mentioned in this

newsletter. Disclosures of holdings: None relevant to any content discussed within this issue of the newsletter

UNIQUE WATERMARK: CBC1F9BF