Sintex Industries - Motilal Oswal · improve FCF and balance sheet, to (1) enable USD290m FCCB...

24

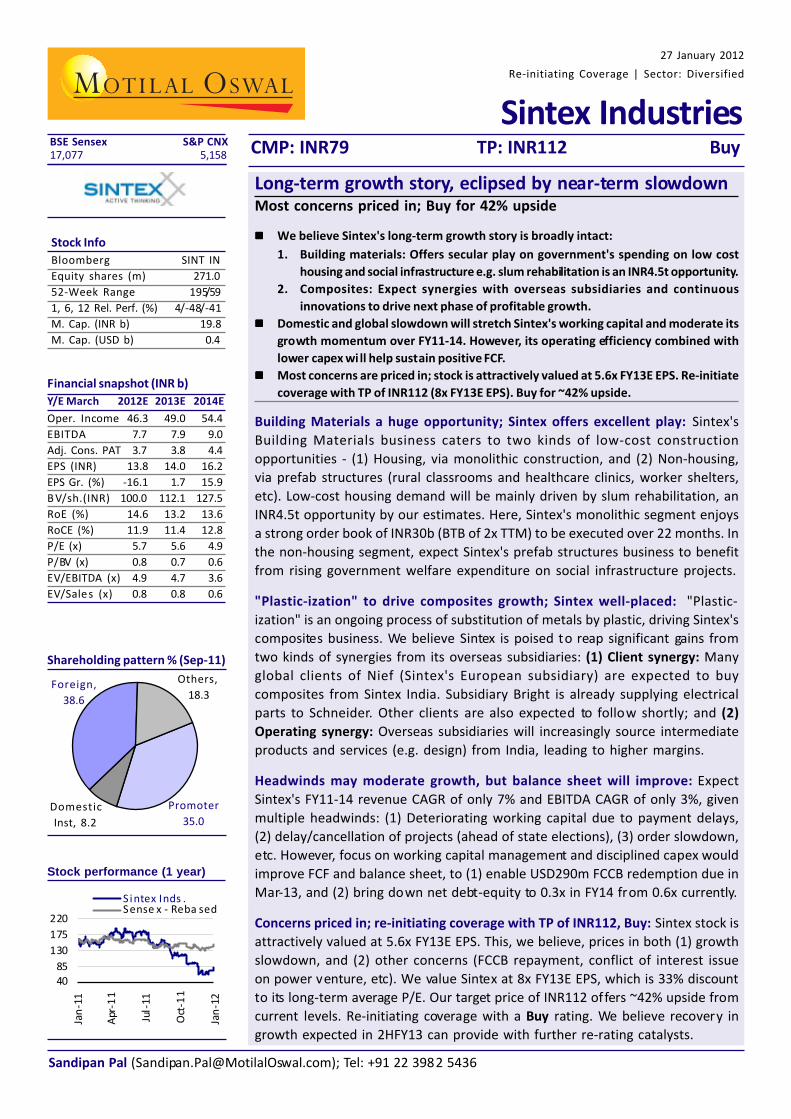

Sintex Industries CMP: INR79 TP: INR112 Buy Stock performance (1 year) Shareholding pattern % (Sep-11) Y/E March 2012E 2013E 2014E Oper. Income 46.3 49.0 54.4 EBITDA 7.7 7.9 9.0 Adj. Cons. PAT 3.7 3.8 4.4 EPS (INR) 13.8 14.0 16.2 EPS Gr. (%) -16.1 1.7 15.9 BV/sh.(INR) 100.0 112.1 127.5 RoE (%) 14.6 13.2 13.6 RoCE (%) 11.9 11.4 12.8 P/E (x) 5.7 5.6 4.9 P/BV (x) 0.8 0.7 0.6 EV/EBITDA (x) 4.9 4.7 3.6 EV/Sales (x) 0.8 0.8 0.6 Domestic Inst, 8.2 Others, 18.3 Foreign, 38.6 Promoter 35.0 Long-term growth story, eclipsed by near-term slowdown Most concerns priced in; Buy for 42% upside We believe Sintex's long-term growth story is broadly intact: 1. Building materials: Offers secular play on government's spending on low cost housing and social infrastructure e.g. slum rehabilitation is an INR4.5t opportunity. 2. Composites: Expect synergies with overseas subsidiaries and continuous innovations to drive next phase of profitable growth. Domestic and global slowdown will stretch Sintex's working capital and moderate its growth momentum over FY11-14. However, its operating efficiency combined with lower capex will help sustain positive FCF. Most concerns are priced in; stock is attractively valued at 5.6x FY13E EPS. Re-initiate coverage with TP of INR112 (8x FY13E EPS). Buy for ~42% upside. Building Materials a huge opportunity; Sintex offers excellent play: Sintex's Building Materials business caters to two kinds of low-cost construction opportunities - (1) Housing, via monolithic construction, and (2) Non-housing, via prefab structures (rural classrooms and healthcare clinics, worker shelters, etc). Low-cost housing demand will be mainly driven by slum rehabilitation, an INR4.5t opportunity by our estimates. Here, Sintex's monolithic segment enjoys a strong order book of INR30b (BTB of 2x TTM) to be executed over 22 months. In the non-housing segment, expect Sintex's prefab structures business to benefit from rising government welfare expenditure on social infrastructure projects. "Plastic-ization" to drive composites growth; Sintex well-placed: "Plastic- ization" is an ongoing process of substitution of metals by plastic, driving Sintex's composites business. We believe Sintex is poised to reap significant gains from two kinds of synergies from its overseas subsidiaries: (1) Client synergy: Many global clients of Nief (Sintex's European subsidiary) are expected to buy composites from Sintex India. Subsidiary Bright is already supplying electrical parts to Schneider. Other clients are also expected to follow shortly; and (2) Operating synergy: Overseas subsidiaries will increasingly source intermediate products and services (e.g. design) from India, leading to higher margins. Headwinds may moderate growth, but balance sheet will improve: Expect Sintex's FY11-14 revenue CAGR of only 7% and EBITDA CAGR of only 3%, given multiple headwinds: (1) Deteriorating working capital due to payment delays, (2) delay/cancellation of projects (ahead of state elections), (3) order slowdown, etc. However, focus on working capital management and disciplined capex would improve FCF and balance sheet, to (1) enable USD290m FCCB redemption due in Mar-13, and (2) bring down net debt-equity to 0.3x in FY14 from 0.6x currently. Concerns priced in; re-initiating coverage with TP of INR112, Buy: Sintex stock is attractively valued at 5.6x FY13E EPS. This, we believe, prices in both (1) growth slowdown, and (2) other concerns (FCCB repayment, conflict of interest issue on power venture, etc). We value Sintex at 8x FY13E EPS, which is 33% discount to its long-term average P/E. Our target price of INR112 offers ~42% upside from current levels. Re-initiating coverage with a Buy rating. We believe recovery in growth expected in 2HFY13 can provide with further re-rating catalysts. Stock Info Bloomberg SINT IN Equity shares (m) 271.0 52-Week Range 195/59 1, 6, 12 Rel. Perf. (%) 4/-48/-41 M. Cap. (INR b) 19.8 M. Cap. (USD b) 0.4 27 January 2012 Re-initiating Coverage | Sector: Diversified BSE Sensex S&P CNX 17,077 5,158 Financial snapshot (INR b) Sandipan Pal ([email protected]); Tel: +91 22 3982 5436 40 85 130 175 220 Jan-11 Apr-11 Jul -11 Oct-11 Jan-12 Sintex Inds. Sensex - Reba sed

Transcript of Sintex Industries - Motilal Oswal · improve FCF and balance sheet, to (1) enable USD290m FCCB...

Sintex IndustriesCMP: INR79 TP: INR112 Buy

Stock performance (1 year)

Shareholding pattern % (Sep-11)

Y/E March 2012E 2013E 2014E

Oper. Income 46.3 49.0 54.4

EBITDA 7.7 7.9 9.0

Adj. Cons. PAT 3.7 3.8 4.4

EPS (INR) 13.8 14.0 16.2

EPS Gr. (%) -16.1 1.7 15.9

B V/sh.(INR) 100.0 112.1 127.5

RoE (%) 14.6 13.2 13.6

RoCE (%) 11.9 11.4 12.8

P/E (x) 5.7 5.6 4.9

P/BV (x) 0.8 0.7 0.6

EV/EBITDA (x) 4.9 4.7 3.6

EV/Sales (x) 0.8 0.8 0.6

Domestic

Inst, 8.2

Others,

18.3Foreign,

38.6

Promoter

35.0

Long-term growth story, eclipsed by near-term slowdownMost concerns priced in; Buy for 42% upside

We believe Sintex's long-term growth story is broadly intact:

1. Building materials: Offers secular play on government's spending on low cost

housing and social infrastructure e.g. slum rehabilitation is an INR4.5t opportunity.

2. Composites: Expect synergies with overseas subsidiaries and continuous

innovations to drive next phase of profitable growth.

Domestic and global slowdown will stretch Sintex's working capital and moderate its

growth momentum over FY11-14. However, its operating efficiency combined with

lower capex wi ll help sustain positive FCF.

Most concerns are priced in; stock is attractively valued at 5.6x FY13E EPS. Re-initiate

coverage with TP of INR112 (8x FY13E EPS). Buy for ~42% upside.

Building Materials a huge opportunity; Sintex offers excellent play: Sintex's

Building Materials business caters to two kinds of low-cost construction

opportunities - (1) Housing, via monolithic construction, and (2) Non-housing,

via prefab structures (rural classrooms and healthcare clinics, worker shelters,

etc). Low-cost housing demand will be mainly driven by slum rehabilitation, an

INR4.5t opportunity by our estimates. Here, Sintex's monolithic segment enjoys

a strong order book of INR30b (BTB of 2x TTM) to be executed over 22 months. In

the non-housing segment, expect Sintex's prefab structures business to benefit

from rising government welfare expenditure on social infrastructure projects.

"Plastic-ization" to drive composites growth; Sintex well-placed: "Plastic-

ization" is an ongoing process of substitution of metals by plastic, driving Sintex's

composites business. We believe Sintex is poised to reap significant gains from

two kinds of synergies from its overseas subsidiaries: (1) Client synergy: Many

global clients of Nief (Sintex's European subsidiary) are expected to buy

composites from Sintex India. Subsidiary Bright is already supplying electrical

parts to Schneider. Other clients are also expected to follow shortly; and (2)

Operating synergy: Overseas subsidiaries will increasingly source intermediate

products and services (e.g. design) from India, leading to higher margins.

Headwinds may moderate growth, but balance sheet will improve: Expect

Sintex's FY11-14 revenue CAGR of only 7% and EBITDA CAGR of only 3%, given

multiple headwinds: (1) Deteriorating working capital due to payment delays,

(2) delay/cancellation of projects (ahead of state elections), (3) order slowdown,

etc. However, focus on working capital management and disciplined capex would

improve FCF and balance sheet, to (1) enable USD290m FCCB redemption due in

Mar-13, and (2) bring down net debt-equity to 0.3x in FY14 from 0.6x currently.

Concerns priced in; re-initiating coverage with TP of INR112, Buy: Sintex stock is

attractively valued at 5.6x FY13E EPS. This, we believe, prices in both (1) growth

slowdown, and (2) other concerns (FCCB repayment, conflict of interest issue

on power venture, etc). We value Sintex at 8x FY13E EPS, which is 33% discount

to its long-term average P/E. Our target price of INR112 offers ~42% upside from

current levels. Re-initiating coverage with a Buy rating. We believe recovery in

growth expected in 2HFY13 can provide with further re-rating catalysts.

Stock Info

Bloomberg SINT IN

Equity shares (m) 271.0

52-Week Range 195/59

1, 6, 12 Rel. Perf. (%) 4/-48/-41

M. Cap. (INR b) 19.8

M. Cap. (USD b) 0.4

27 January 2012

Re-initiating Coverage | Sector: Diversified

BSE Sensex S&P CNX17,077 5,158

Financial snapshot (INR b)

Sandipan Pal ([email protected]); Tel: +91 22 3982 5436

4085

130

175

220

Jan

-11

Apr

-11

Jul-

11

Oct

-11

Jan

-12

S intex Inds .Sense x - Reba sed

Sintex Industries

27 January 2012 2

Sintex Industries: Re-initiating Coverage

Page No.

Building Materials a huge opportunity; Sintex offers excellent play ...................... 3-8

Plasticization to drive composites growth; Sintex well-placed ............................. 9-14

Headwinds to moderate growth, balance sheet to improve ............................... 15-17

Concerns priced in; Buy with TP of INR112, 42% upside ....................................... 18-19

Key risks and mitigants ............................................................................................... 20

Financials and valuation ........................................................................................ 21-22

Note: All exhibits sourced from Company and MOSL, unless otherwise stated;

Stock prices and indices as of 25 January 2012

Sintex Industries

27 January 2012 3

Building Materials a huge opportunity;Sintex offers excellent play Sintex's Building Materials business caters to two kinds of low-cost construction

opportunities - (1) Housing, via monolithic construction, and (2) Non-housing, via prefab

structures (rural classrooms and healthcare clinics, sanitation, army barracks, worker

shelters, etc).

Low-cost housing demand will continue to be mainly driven by slum rehabilitation, an

INR4.5t opportunity by our estimates. Here, Sintex's monolithic segment enjoys a

comfortable order book of INR30b (BTB of 2x TTM) to be executed over 22 months.

However, delay in payments by state governments, policy inaction, state elections, etc,

could stretch working capital and dent pace of execution.

In the non-housing segment, we expect Sintex's prefab structures business to benefit

from rising government welfare expenditure on social infrastructure projects through

various programs, viz, JNNURM, SSA, NRHM, etc.

Excellent play on low cost construction technologiesSintex's Building Materials business caters to two kinds of low-cost construction

opportunities -

1. Housing, via monolithic construction: A relatively new construction technology,

which involves pouring concrete into a hollow plastic framework to build the

entire floor plan. This is well-suited for low-cost, massing housing - both in terms

of lower cost of construction and faster project completion.

2. Non-housing, via prefab structures: This involves assembling of concrete-

reinforced plastic panels, to create simple structures such as rural classrooms and

healthcare clinics, army barracks, worker shelters, sanitation blocks, etc.

Sintex offers excellent play on low cost construction technologies

Concept

Advantages

Faster execution

Cost advantage

Other advantages

Key usages

Key clients

Cost structure

Monolithic

An unconventional construction methodology by

pouring fluid concrete into light weight plastic

framework to construct wall/slab, with metallic bars

for strengthening. 5-8 storey structures can be built,

which have lifespan of ~25 years.

60-70% faster than conventional brick and mortar

system, especially for large repetitive structures.

Monolithic is 8-10% cheaper than conventional

process. All inclusive cost of INR900-1,100/sf (INR600/

sf for structure only).

No maintenance cost, eco-friendliness (use of fly ash

in mix), low labor intensity.

Low-mid cost housing, slum rehabilitation, housing

for police/army, student hostels etc

Majorly governments - various housing boards,

railways, defense, etc

RM 30-40%; Framework 5-7%; Labor 7-9%; Site

management 20-30% (smaller sites) and 12-13%

(bigger sites); Margin 18-19%

Prefabs

Simple structures built by assembling panels made of

concrete-reinforced plastic. Sintex offers end-to-end

solution in prefabs - manufacturing, logistics, and

installation at site.

Takes 10-12 days' time for setting up a simple school

structure under prefab.

Prefab is 15-25% cheaper than conventional process.

All inclusive cost of INR530-580/sf for a fully built

prefab structure is strongly competitive in Indian

scenario.

Typicality, reusability, low labor dependency

Public schools, healthcare clinics, site offices, Base

Transfusion (BT) shelter for telecom tower, agri sheds

70-75% government, rest private

RM 25-30% (incl purchased products, viz, asbestos,

paints, etc, and manufactured products); Kit-making

cost 18-20%; Logistics incl labor: 20-25%; Margin 20%

Extremely low

penetration of housing,

classrooms and

healthcare in India, offers

huge opportunity and

revenue visibility for

Sintex

Sintex Industries

27 January 2012 4

Monolithic: Key growth driver; Sintex well-placed with INR30b order bookMonolithic business has been the key growth driver for Sintex over FY08-11, with 85%

revenue CAGR and 87% EBITDA CAGR. Its share in revenue and EBITDA mix has

increased from 9/10% in FY08 to 30/32% in FY11. Further, order book has growth from

INR14b in FY09 to INR30b (flat for the past few quarters), 2x TTM sales.

In monolithic, Sintex enjoys superior margin compared to other construction

companies. Rising entry of other players could moderate margins, going forward.

However, we believe Sintex will continue to have an edge over others due to

(1) in-house production of plastic framework, (2) early mover advantage and long

track record, providing (3) scale advantage and a strong client network.

Sintex's Building Materials - 5-force analysis

2. Suppliers' Power LOW

3. Risk of Substitutes MODERATE

1. Customer Power HIGH

R/ms (cement,

asbestos, paints, PVC

etc) are typical

commodities, vendors

have limited

bargaining power

High, given a) Government

organization renders high

ticket projects with tighter

credit days, and b)

presence of large number

of players in the

conventional space

Monolithic and prefab offer comparatively faster and cheaper

solution, albeit it works better only for repetitive and standardized

large structures.

5. Competition MODERATE

Several players in the conventional space. Some global and local

companies offer similar technology based solutions, viz, L&T,

Ahluwalia, Maninfra, Billimoria, etc

4. Entry barrier HIGH

Execution is the key to competitive costing and faster delivery - which

requires: (a) High speculative upfront capacity investment with wider

reach within the country, (b) Optimization of material utilization.

Prefab is viable only for <1000km radius from manufacturing

locations. 2-3 day delay in logistics and erection process can eat

away viability in Prefab business.

Both the above segments put together offer a huge business opportunity in India e.g.

low-cost housing demand will continue to be driven by slum rehabilitation, an INR4.5t

opportunity by our estimates. We have tabled below key points of the two construction

technologies. We also apply Porter's 5-force framework to these businesses, and

assess Sintex's positioning in the same.

Housing boards together

make up 40% of

monolithic order book,

INR7.5b under SRA,

JNNURM, Rajiv Awas

Yojna etc. INR2-3b under

railways, while defence

and private players make

up the rest

Sintex's positioning: Sintex

has established execution

credibility with

government bodies in

Gujarat, Rajasthan, UP.

Sintex's positioning: Sintex's prefab plants are situated in 6

locations across the country to maximize coverage and logistics

advantage.

Sintex's positioning: Together, L&T and Sintex enjoy equal share

amounting to a total of 70% of the monolithic low cost housing

done in India.

Sintex Industries

27 January 2012 5

Current slowdown could stretch receivable cycle, dent capex and growthSintex's excellent track record notwithstanding, the ongoing slowdown presents

several near-term challenges for this vertical. Key issues are:

1) Rising delay in government processes: Various government bodies including

housing boards, railways, police, etc, are the major customers in monolithic

segment. Thus, under current challenging economic and political conditions,

monolithic business is adversely affected by pressure points like (1) delay in

government payments, (2) postponement of orders or re-tendering, (3) delay in

site clearance/handover (due to growing agitation), and (4) delay in technical

clearances. About 45% of Sintex's INR30b order book - slum rehab (INR7.5b),

railways (INR2.5b), defense (INR2.5b) - is facing execution slowdown or stoppage.

2) Stretched working capital cycle also affects execution: Monolithic business is

working capital intensive with average net working capital days over 140 days.

Dealing with several government bodies keeps the receivable cycle naturally high.

While the company's increasing focus on collection management process is

positive, we expect no major improvement in working capital cycle over FY12-13,

given the economic slowdown. The upcoming state elections in UP (Sintex has

INR4.5b of order book from the state) could also lead to some collection delays.

Stretched working capital also affects execution.

We expect the segment to de-grow 15% in FY12 and grow 10%/15% in FY13/14. EBITDA

margin is expected to decline to 19%/17.5%/18% in FY12/13/14 v/s 19.5% in FY11.

Order book comfortable at 2x TTM sales Meaningful rise in average order size/site (INR m)

Source: Company/MOSL

150

350

480

700800

FY08 FY09 FY10 FY11 FY12E

18 14 17 22 30 25 26 29 30 30 30

2.22.02.12.22.3

2.7

3.73.1

2.1

1.31.4

1Q

FY10

2Q

FY10

3Q

FY10

4Q

FY10

1Q

FY11

2Q

FY11

3Q

FY11

4Q

FY11

1Q

FY12

2Q

FY12

3Q

FY12

Order Bo ok (INR b) Boo k to Bi l l (x)

Monolithic has been key growth driver for Sintex (%) Enjoys superior margin than construction peers

13.2

9.6 9.1 9.6

19.5

HCC NCC IVRCL Simplex Sin tex

FY11 margin (%)

915

22

3025 25 26

10

16

25

32

28 28 29

FY08

FY09

FY10

FY11

FY1

2E

FY1

3E

FY1

4E

Sales contribu tion EBITDA contributio n

Management has also

adopted a strategy to

prioritize working capital

management over

growth by not deploying

cash in execution of a

monolithic project with

lower receivable

visibility

Sintex Industries

27 January 2012 6

New order growth witnessed moderation (INR b) Growth at Monolithic to moderate

Source: Company/MOSL

4.94.2

8.99.8

4.5

8.7

3.82.8 2.6

(2.6)(2.8)

1QFY

10

2QFY

10

3QFY

10

4QFY

10

1QFY

11

2QFY

11

3QFY

11

4QFY

11

1QFY

12

2QFY

12

3QFY

12

4.5 7.2 13.4 11.4 12.5 14.4

18%18%

19%20%

19%

18%

200

9

201

0

201

1

201

2E

201

3E

201

4E

Monol i thic Revenue(INR b) EBITDA margin(%)

Prefabs: Government's social spending continues to drive demandFor Sintex's prefabricated structures business, two major revenue contributors are:

(1) Classrooms under the Sarva Shiksha Abhiyan (SSA i.e. Education For All), and (2)

Healthcare centers under the National Rural Health Mission (NRHM). The budget for

SSA has increased from INR72b in 2006 to INR210b in 2012. A significant portion (30-

35%) of the SSA budget gets used up in the construction of classrooms in rural areas.

Similarly, the government has stated its objective of having a primary hospital in

every village in India under the NRHM. The budget for NRHM has grown at a CAGR of

18% over the last six years to INR178b in 2012. Thus, the size of the opportunity is huge

with central and state governments allocating funding to a wide range of social

schemes. In addition to government contracts (70-75%), there is also significant

opportunity in private sector projects such as cold chains, bunk houses, agricultures

sheds, etc.

27.9

46.261.8

93.0

1981 1991 2001 2011

Slum population (m) 93

Persons per house 6

Houses required 15.5

Avg House Area (sqf) 300

Cost per psf 1,000

Cost per house (INR m) 0.3

Slum rehab opportunity (INR b) 4,650

Monolithic: Huge long-term potential Slum rehabilitation, an INR4.5t opportunity: A recent government study

estimated India's slum population in 2011 at ~93m. This presents a housing

opportunity of at least INR4.5t. The government is committed to reduce

population residing in slums. This is evident in the rising budgets for initiatives

like Jawaharlal Nehru National Urban Renewal Mission (JNNURM) and the

recently launched Rajiv Awas Yojna, specifically aimed at slum rehabilitation.

Fast increasing slum population... ...presents a huge housing opportunity

Source: Industry/MOSL

Significant opportunity with Railways and Army: Railways intends to build

houses for 1.4m employees by FY20; This is a significant opportunity since land

and funding are not that problematic for Railways. Likewise, every year, the

Indian Army plans to build 15,000-20,000 houses.

A significant portion

(30-35%) of the SSA

budget gets used up in

the construction of

classrooms in rural areas

Sintex Industries

27 January 2012 7

Increasing budgets in social schemes, viz, SSA, NRHM, etc (INR b)

Source: GoI/MOSL

Established track record bestows competitive advantageSintex has already erected several schools and hospitals under various government

schemes. It is now one of the very few players with the ability to erect a structure in

half the time usually taken by traditional contractors, which, in turn, helps the state

to meet its annual deadline. The company has approvals in place for 17 states, of

which 12-13 states are active. At present, projects from UP, Bihar and Gujarat account

for a major chunk of Sintex's prefab revenue.

Logistics accounts for a significant share of prefab construction costs. Hence, an

established capacity and wide geographical reach hold the key to cost-effective

execution. Sintex's prefab plants are situated in 6 locations across the country to

maximize coverage. The gestation period for the business is 2-3 years; hence, currently,

L&T remains the only competitor at the national level, with both Sintex and L&T

enjoying a combined market share of 60-70% (on equal basis).

0

50

100

150

200

250

Sarv

a S

hiks

ha

Abh

iyan

(S

SA)

Nat

ion

al R

ural

Hea

lth

Mis

sion

(NR

HM

)

Indi

ra

Aw

as

Yoj

ana

JNN

UR

M

BSU

P

(urb

an

poo

r)

JNN

UR

M IH

SDP

(slu

m

reha

b/h

ousi

ng

Raj

iv

Aw

as

Yoj

ana

2006 2007 2008 2009 2010 2011 201220% CAGR

18% CAGR

24% CAGR

Huge completive positioning due to first mover's advantage and wide plant network

Source: Company/MOSL

Dadri

Baddi

Nagpur

Salem

KalolKolkata

Sintex has approvals in

place for 17 states, of

which 12-13 states

are active

Sintex's prefab plants are

situated in 6 locations

across the country to

maximize coverage

Sintex Industries

27 January 2012 8

6.75.6 6.5 7.0

7.88.8

19.5%19%20%21%

17%

20%

2009 2010 2011 2012E 2013E 2014E

Pre-fab Revenue (INR b) EBITDA margin

Impact of slowdown: expect only a limited moderation in growthSintex's prefab segment has witnessed an 8% CAGR over FY07-11. This is despite a

sharp cutback in BT (base transfusion) shelter business, due to slowdown in roll-out

of telecom towers. Ex BT shelters, the CAGR would be much higher at 25-30%. This is

helped by strong social spending by governments on rural improvement projects, viz,

education, healthcare, sanitation, etc.

As in monolithic, Sintex's pre-fab business is also witnessing slowdown with only 5%

YoY growth in 9MFY12. But unlike monolithic, we expect a limited impact of project

slowdown due to the following reasons -

a) Continuous product and geographic diversifications with multiple projects from

same customer/geography offering resilience to capacity utilization and margin.

Unlike monolithic, prefab business involves several shorter gestation projects

with smaller ticket size, which reduces the risk of cancellation/delay.

b) There are no significant payment delays, as small orders (~INR1m for prefab as

against INR700-800m in monolithic) can be cleared at the collector level itself.

c) Virtual duopoly creating a high entry barrier (gestation period for a new entrant

would be 2-3 years).

Going forward, we model in a much more moderated revenue CAGR of 11% over

FY11-14. We also model in EBITDA margins to decline 100bp from 20.5% in FY11 to

19.5% in FY14. This, we believe, captures both positives and negatives.

Positives: (1) Sintex's entry into new states like UP (FY11), Bihar, Maharashtra (FY12),

and (2) huge opportunity in newer segments like cold chain which could get further

boost with FDI allowance in multi-brand retail.

Negatives: Approvals and collections in FY13 could be impacted by the outcome of

elections in several states viz. UP, Punjab etc.

Expect revenue CAGR of 11% over FY11-14

Source: Company/MOSL

We expect a limited

impact of project

slowdown due to

continuous product and

geographic

diversification and cost

savings on logistics by

servicing repeat

customers

Sintex Industries

27 January 2012 9

Plasticization to drive composites growth;Sintex well-placed

"Plastic-ization" is an ongoing process of substitution of metals by plastic, driving Sintex's

composites business. We believe Sintex is poised to reap significant gains from two kinds of

synergies from its overseas subsidiaries:

1. Client synergy: Many global clients of Nief (Sintex's European subsidiary) are expected to

buy for their Indian operations, composite parts from Sintex India and its Indian subsidiary,

Bright Autoplast. Bright is already supplying electrical parts to Schneider in India. Other

clients like Areva, ABB, Bombardier, etc are also expected to have India operations shortly;

and

2. Operating synergy: Overseas subsidiaries will increasingly source intermediate products

and services (e.g. design) from India, leading to higher margins.

"Plasticization" trend to continueSintex will continue to benefit from the rising trend of "plasticization", i.e. substitution

of metals by plastic composites across industries, mainly autos, electrical, aerospace,

and healthcare, defense, etc. Plastic composites are gaining preference in various

industries over metal due to their sheer advantageous properties , viz, (1) low weight

but high strength (renders better fuel efficiency for Auto), (2) temperature resistance

and electrical insulation, (3) low corrosion and chemical inertness, etc. While

comparatively the growth is low overseas due to near-saturation in the rate of

substitution, significant opportunity exists in emerging countries like India.

Sintex's domestic positioning is strongSintex has established itself as a leading plastic composites molding player in India

with -

(1) A vast product range across segments, viz, household products, electrical and

automotive;

(2) A strong client base including auto OEMs (original equipment manufacturers),

engineering companies, state electricity boards, local governments, etc;

(3) Integrated processors and fabricators with as many as twelve plastic processes

(blow molding, injection molding, roto molding, extrusion, etc), and

(4) Manufacturing facilities across the country.

Key product segments:

Household products: Interior, kitchen cabinets, waste bins, solar cookers, furniture,

crates, etc.

Electrical - Meter boxes, pillar boxes, junction boxes, fiber-reinforced plastic

insulators, etc

Bright Auto: Bumper systems, acoustic management systems, seating systems,

instrument panel, trims and pillars, exterior trims, radiator grills, air vent grab

handles, fuel tank, air ducts, two-wheeler parts, etc.

Plastic composites are

gaining preference in

various industries over

metal due to their sheer

advantageous properties

Sintex Industries

27 January 2012 10

Poised to enjoy synergies with overseas subsidiariesBetween mid-2007 and mid-2008, Sintex embarked on an inorganic growth strategy

in composites, through a series of acquisitions both in India and overseas. The major

acquisitions include (1) Bright Autoplast in India, (2) Nief Plastics, France, and (3)

Wausaukee Composites, USA (see table below for full details on acquisition in custom

molding/composites business).

The rationale behind Sintex's acquisitions was (1) foray into new verticals and clients,

(2) moving up the product value chain, (3) gaining technological prowess, and (4)

exploiting synergies. Post acquisitions, there was a major global slowdown. So,

overseas subsidiaries did not grow as expected. However, we believe, Sintex is now

poised to reap significant gains from two kinds of synergy: (1) Client synergy and (2)

Operating synergy.

Overseas subsidiaries: Key products and target segments

Nief Plastics: 35% electrical, 27% auto, 26-30% aerospace/defense as major

segments as on FY11 revenue of INR9.2b. Dependence on auto segment has declined

from ~60% in FY07 to ~28%, while concentration on France has come down to ~55%

(v/s. ~90% in FY07).

Wausaukee Composites: Medical imaging, industrial trucks and tractors and mass

transit accounted for ~25% each to revenues of INR4b (including Nero Plastics).

Revenue is predominantly from the US.

Sintex embarked on an

inorganic growth strategy

in composites, through a

series of acquisitions

both in India and

overseas

Acquisitions in custom moldings to provide a strong client base

Company Date Stake Currency Price Products Clients Remarks

(%) (m)

Geiger Technik, 31-Jul-08 90 Euro 6.9 Precision plastic BMW, VW, Daimler, 67% of revenue

Germany (Written parts Audi, TRW, Bosch, from Tier l; off post

fi l ing Siemens 37% fromOEMs;

of Bankruptsy) 4 plants

Nero Plastics 3-Dec-07 100 USD 4.8 Structural plastic and Global OEMs Acquired by

(Merged with composite components Wausaukee

Wausaukee) Composites Inc

Nief Plastic, 28-Sep-07 100 Euro 30.7 Plastic products for auto, ABB, Areva, 11 manufacturing

France electrical and electronics, EADS, Faurecia, plants - 7 in France;

aeronautics, defence, Legrand, Schneider, others in Hungary,

household appliances, Siemens, Snecma, Tunisia, Morocco,

bui lding ThyssenKrupp Slovakia

Automotive, Valeo,

Visteon

Bright Autoplast 6-Sep-07 100 INR 1,489 Bumper systems, Maruti Suzuki, 5 plants - Pune,

Pvt Ltd Acoustic management Tata Motors, Sohna, Chennai,

systems, seating Honda, M&M, Pithampur, Nashik

sytems, etc Hyundai

Wausaukee 31-May-07 100 USD 20.5 Composite plastic Philips, Siemens, 3 plants in the US

Composites and fibreglass Alstom, GE Medical,

components Rail Plan Intl

Source: Company/MOSL

Sintex Industries

27 January 2012 11

Client synergy: Dedicated plant for Schneider; others may followWhat is Client synergy: Many global clients of Nief (Sintex's European subsidiary) are

expected to buy for their Indian operations, composite parts from Sintex India and its

Indian subsidiary, Bright Autoplast. Bright is already supplying electrical parts to

Schneider in India. Other clients like Areva, ABB, Bombardier, etc are also expected

to have India operations shortly.

The Schneider experience: Schneider Electric, a major client of Nief, has been investing

heavily in India since 2008. Recently, it acquired 74% stake in Luminous Inverters to

enter the business to customer (B2C) segment. Schneider plans to increase its exposure

to India by (1) serving institutional clients, and (2) growing retail presence through

organic and inorganic means. Nief has convinced Schneider to source its requirement

of composites in India from Sintex Group. A dedicated plant for Schneider is already

functional under Sintex's domestic subsidiary, Bright Autoplast.

More clients to follow: Sintex is replicating the Schneider model with Nief's other

clients like Areva and Legrand. Areva has become an anchor customer (dedicated

plant required, with 50-70% assured sales). Legrand, another French major, has signed

a contract with Sintex for outsourcing of electrical parts. Talks with ABB Alstom,

Bombardier, and other Nief customers are at advanced stages and the management

expects positive outcomes. We believe client synergy will meaningfully enhance

composites revenue growth for the Sintex Group as a whole.

Client synergy: Current and future

Client Relationship Vertical Geography

Schneider Anchor customer Electricals India and Africa

Areva Anchor customer Electricals India

Legrand Contract customer Electricals Outsourcing

ABB Contract customer Electricals India

ABB Alstom Expected to materialize Mass Transit India

Bombardier Expected to materialize Mass Transit India

Source: Company/MOSL

Snapshot: convincing growth visibility from Nief's clients

Schneider's revenue of INR1.3b includes Nief (INR1b) and Schneider India

(INR300m) in FY11

Schneider is expected to place orders worth INR1.5-1.8b over next 2-3years.

Areva is expected to place orders worth INR0.6-1b over FY12-FY14, while ABB

Alstom is expected to place an order of similar size, followed by Bombardier

Operating synergy: Provides resilience to overseas marginsWhat is operating synergy: Sintex is tapping operating synergies between Indian and

overseas operations: (1) in the first phase, by outsourcing intermediate processes

such as design and common services such as HR, finance and accounting from India,

and (2) in the next phase, by sourcing semi-finished goods from India.

Benefit - scope for margin expansion: Overseas, composite vertical involves high-

cost labor (25-38% of revenue compared to 9-11% in India). Thus, there is tremendous

scope for margin expansion in Sintex's overseas subsidiaries through outsourcing to

India non-core, labor-intensive processes, and also sourcing from India intermediate/

semi-finished products.

Sintex is replicating the

Schneider model with

Nief's other clients like

Areva and Legrand

Overseas, composite

vertical offers

tremendous scope for

margin expansion

Sintex Industries

27 January 2012 12

Besides, Sintex is also adopting various other margin-optimization and de-risking

steps in Nief, viz, (1) lowering production share of high-cost France facilities from

90% in FY08 to ~55% currently, by increasingly shifting production to low-cost

geographies such as Slovakia, Hungary, Tunisia, and Morocco, and (2) lowering

dependence on auto (down to 27% of revenue from 60% in FY08) by diversifying to

other verticals, viz, electrical, aerospace, defense, etc.

Slowdown likely to hurt growth, delay synergy benefitWe expect the prevailing domestic and global slowdown to hurt revenue growth, and

also delay the expected synergy benefits, as explained below.

Nief, Wausaukee: They account for ~64% of Sintex's composite revenue. Sovereign

debt crisis in Europe and slowdown in the US will affect topline growth for both.

Bright Autoplast: About 85% of Bright's revenue comes from the Auto sector. Our

Auto team expects flat volume growth in FY12 and muted 10-15% growth in FY13.

Business from selling electrical parts to Nief clients like Schneider and Areva are

no longer expected to clock hyper growth expected earlier.

Sintex composites: Major clients include industrial sector, State Electricity Boards

and Auto sector, all of which are in the midst of a slowdown.

Sintex expects clarity on client budgets to emerge in 1HCY12. However, we believe

the probability of slowdown is fairly high. We accordingly model in muted sales growth.

We also do not model in synergy benefit, and actually expect Composites EBITDA

margin to contract 150-200bp over FY11-14. The drop in margins could have been

much higher but for margin-optimization and de-risking steps described earlier.

Custom molding assumptions

Composit Business Break-up FY08 FY09 FY10 FY11 FY12E FY13E FY14E

Nief [Auto, Electrical, Aerospace, Defence]

Revenue 3,489 7,400 8,040 9,246 9,986 8,987 9,436

EBITDA 298 850 965 1,110 974 854 944

EBITDA Margin (%) 8.5 11.5 12.0 12.0 9.8 9.5 10.0

Sales Growth (%) 112 9 15 8 (10) 5

Wausaukee + Nero [Electrical, Mass Transit, Medical, Wind energy, Agri equipments, Trucks etc]

Revenue 1,017 2,200 1,509 2,664 2,930 2,930 3,077

EBITDA 32 115 151 269 278 278 292

EBITDA Margin (%) 3.1 7.0 10.0 10.1 9.5 9.5 9.5

Sales Growth (%) 116 (31) 77 10 - 5

Bright Brother (majorly Auto components ~85%, Electrical parts)

Revenue 404 1,270 1,910 2,750 3,300 3,796 4,365

EBITDA 80 203 267 443 462 531 611

EBITDA Margin (%) 19.8 16.0 14.0 16.1 14.0 14.0 14.0

Sales Growth (%) 214 50 44 20 15 15

Domestic Ex Bright

Revenue 4,120 3,470 3,548 4,050 4,860 5,588 6,427

EBITDA 923 500 836 985 1,142 1,257 1,446

EBITDA Margin (%) 22.4 14.4 23.6 24.3 23.5 22.5 22.5

Sales Growth (%) (16) 2 14 20 15 15

Total Domestics

Revenue 4,524 4,740 5,458 6,800 8,160 9,384 10,792

EBITDA 1,003 703 1,103 1,428 1,604 1,789 2,057

EBITDA Margin (%) 22.2 14.8 20.2 21.0 19.7 19.1 19.1

Sales Growth (%) 84 5 15 25 20 15 15

The hyper growth

expectation from Bright's

new and potential clients

such as Schneider, ABB,

Areva has also been

impacted significantly

leading to a delay/

moderation of

expansion/spending plan

De-growth in domestic/

EU car volume and

slowdown in order

inflow from light

electrical segment

foreign geographies

would be the key

challenges for FY13

Sintex Industries

27 January 2012 13

Nief: Due to higher dependence on Auto sector (27-30%), which has shown a

strong negative outlook, we model in ~10% sales de-growth in FY13, coupled with

250-300bp margin contraction. Higher contribution from electrical segment, cross-

border outsourcing synergy with Bright could ameliorate margin from current

level.

Wausaukee: Relatively healthier trend in electrical, medical, agricultural segments;

we expect sales to witness higher resilience than Nief. We assume a flattish FY13,

albeit we do see some margin contraction. Higher capacity utilization in Wind

energy segment could improve margin.

Bright: Again a higher dependence on domestic automobile segment would lead

to moderation in sales growth (estimated at 20% against management guidance

of 25% in FY12, and is further expected to moderate to15% in FY13). In electrical

segment too, a sharp slowdown in Schneider business, delay in order

commencement from other Nief clients (ABB, Areva etc) are likely to impact

capacity utilization and could drive margin contraction. We model in ~200bp margin

reduction over FY12-13.

Domestic car sales moderated over FY12 ('000) …so is Europe car volume, luxury segment relatively stable (m)

Wind energy outlook bearish, while medical imagingGlobal auto components sales posted declining trend (Biotech), Agri mechanic maintained growth

0

75

150

225

300

FY0

2

FY0

3

FY0

4

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

Apri l May June July

Augus t September October November

December January February March

(40)(20)

-

2040

6080

100

Ma

r-02

Dec

-02

Sep

-03

Jun-

04

Ma

r-05

Dec

-05

Sep

-06

Jun-

07

Ma

r-08

Dec

-08

Sep

-09

Jun-

10

Ma

r-11

Dec

-11

(40)

(20)

-

20

40

60

80

Automobi le vehicle mfg Auto Parts

Auto Reta i l

12

(2)

1(5

)(4

)8

(8)

(17

) (10

)(1

4)

(2)

(3)

6 6 72 1

10

1 01

65

(1)

(2)

0.0

1.0

2.0

3.0

De

c-09

Feb

-10

Apr

-10

Jun

-10

Au

g-1

0

Oct

-10

De

c-10

Feb

-11

Apr

-11

Jun

-11

Au

g-1

1

Oct

-11

-40

-30

-20

-10

0

10

20

EU car s ales Luxury CarCar sa les Growth (%) Luxury Car sa les Growth (%)

-30

0

30

60

Jun

-06

Oct

-06

Feb

-07

Jun

-07

Oct

-07

Feb

-08

Jun

-08

Oct

-08

Feb

-09

Jun

-09

Oct

-09

Feb

-10

Jun

-10

Oct

-10

Feb

-11

Jun

-11

Oct

-11

Wind Energy Biotech

Agri Machinaries AerospaceYoY growth(%)

Source: Bloomberg/MOSL

Almost 65-70% of

composite revenue is

driven by US and

European clients - a)

foreign subsidiaries

accounts for ~64%, b)

cross-client synergy

accounts for 2-3% of

Bright's sales

Sintex Industries

27 January 2012 14

FY11-14E Earning CAGR estimates of key clients depicts muted outlook for Auto and relativelybrighter scenario for electrical

2 %

5 %6 %

5 %

4 %

8 %

3 %

- 1 %Pe

ugeo

t

Ren

aul

t

Sch

neid

er

Are

va

Als

tom

AB

B

Val

eo

Sie

men

s

4,5

24

4,7

40

5,45

8

6,80

0

8,16

0

9,3

84

10,7

92

4,5

06 9,60

0

9,54

9

11,

910

12,9

16

11,9

18

12,5

13

2,46

0FY

07

FY08

FY09

FY10

FY11

FY1

2E

FY1

3E

FY1

4E

Domes tic Rev (INR m) Foreign Rev (INR m)

17.9

%

22.2

%

14.

8% 20

.2%

21.

0%

19.

7%

19.1

%

19.1

%

0.0%

7.3%

11.

4%

11.7

%

11.6

%

9.7%

9.5% 9.9

%

17.9

%

14.8

%

12.

5%

14.8

%

15.

0%

13.

6%

13.

7%

14.1

%

FY07

FY08

FY09

FY10

FY11

FY1

2E

FY1

3E

FY1

4E

Doemes tic Margin Foreign Margin Blended Margin

Slowdown in order inflow and lower capacity utilizations to moderate revenue growth and contract margins

Source: Bloomberg/MOSL

Source: Company/MOSL

Automobiles

Sintex Industries

27 January 2012 15

Headwinds to moderate growth, balance sheet to improve Deteriorating working capital in monolithic and order slowdown in custom molding could

be the key growth deterrents over 4QFY12 through 1HFY13, with some stability in

2HFY13-14. Over FY11-14, we see muted revenue CAGR of 7% and EBITDA CAGR of 3%.

However, stronger focus on receivable management, cash conservation, and lower capex

would improve FCF (cumulative INR8.1b over FY12-14) and strengthen balance sheet -

(1) this will support USD290m FCCB redemption due in Mar-13, and (2) Lower net debt-

equity to 0.3x in FY14 from 0.6x currently.

Near-term growth outlook dented considerablyWe expect Sintex to post muted revenue CAGR of ~7% over FY11-14 (v/s 25% over

FY08-11), driven by 2% CAGR in monolithic construction (85% over FY08-11), 11% CAGR

in prefabricated structures (8% over FY07-11) and 8% CAGR in composites (27% over

FY08-11). With lower capacity utilization hurting margins across segments, we estimate

EBITDA CAGR of 3% and adjusted PAT CAGR at 0%.

Revenue growth moderation is largely attributable to monolithic and composites segments

11.722.9

31.4 33.244.8 46.3 49.0 54.4

171617181617

1719

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY12

E

FY13

E

FY14

E

Revenue (INR b) EBITDA Margin (%)

Expect a de-growth in net profit over FY11-13

FCF to improve with moderating capex, better WC management

Y/E March 2008 2009 2010 2011 2012E 2013E 2014E

Cashflow before WC Change 3,491 5,030 4,981 6,990 6,898 7,118 7,920

(Inc)/Dec in WC -1,049 -3,664 -7,480 1,172 -3,637 -3,052 126

CF from operations 2,442 1,366 -2,499 8,162 3,261 4,066 8,046

Cepex -11,656 -5,286 -2,315 -8,253 -2,982 -1,610 -1,903

Free Cash Flow -8,984 -3,726 -4,327 99 -145 2,148 6,143

Interest/Dividend paid 804 996 921 1,295 1,669 1,642 1,708

Inc/(Dec) in Debt 12,372 3,702 3,339 1,434 2,471 -5,342 571

Ner cash flow 9,812 -2,028 -2,390 566 693 -4,805 5,037

2,27

3

3,98

1

5,21

9

5,38

0

8,15

5

7,65

2

7,92

5

9,01

71,30

4

2,12

6

3,09

6

2,8

96

4,4

57

3,7

39

3,8

01

4,4

05

FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E

EBITDA PAT

8%

38%

2% 2%12%

-1%

8%15%

85%

11%6%

17%

Text

ile

Mon

olit

hic

Pref

ab

Dom

esti

c

Com

pos

ites

Ove

rse

as

Com

pos

ites

Tank

s

FY08-11 FY11-14EGrowth CAGR

Sintex Industries

27 January 2012 16

Working capital improvement process to be delayedOver the past 3 years, sharp growth in working capital intensive monolithic business

has deteriorated operating cash flows. The net working capital (NWC) days rose from

42 in FY07 to 152 in FY10, before retreating substantially to 102 in FY11, but rising again

to 126 days in 3QFY12. However, NWC in the other verticals is relatively lower - prefab

(50-65 days), custom molding (foreign 30-40 days, domestic 50-60 days), textiles (80-

90 days), water tanks (90 days), etc.

The management aims to improve balance sheet quality by stabilizing NWC at 120-

125 days. In the backdrop of payment delays from governments, Sintex is likely to

forego some growth in monolithic segment by selectively executing only those

projects with cash flow visibility, and conserve cash for FCCB redemption due in FY13.

Even in verticals other than monolithic, Sintex is focusing on (a) stabilizing business

composition, (b) better capacity utilization and (c) greater discipline in receivables

management (e.g. use of letters of credit, dedicated relationship management with

government departments, etc).

Still, we expect NWC to stretch further to 127/143 days over FY12/13, before a possible

trend reversal in FY14.

Expect receivable days to deteriorate over FY12/13 NWC days to be stretched further

73

127

96113 116

127 128 134

FY07

FY08

FY09

FY10

FY11

FY1

2E

FY1

3E

FY1

4E

46 41

74

152

102

127 143

128

FY07

FY08

FY09

FY10

FY11

FY1

2E

FY1

3E

FY1

4E

Source: Company/MOSL

(1,0

49)

(3,6

64)

1,17

2

(3,8

92)

(2,0

09)

(61)

(3,7

26)

(4,3

27)

(145

) 2,14

8 6,14

3

(7,4

80)

99

(8,9

84)

FY08 FY09 FY10 FY11 FY12E FY13E FY14E

Working capi ta l change FCF

But lower share of WC intensive monolithic business and lower capex commitment to improve FCF

Source: Company/MOSL

915

22

3025 25 26

10

16

25

32

28 28 29

FY0

8

FY0

9

FY1

0

FY1

1

FY12

E

FY13

E

FY14

E

Sa les contribution EBITDA contribution

Sintex Industries

27 January 2012 17

Expect positive FCF on the back of moderated capexWe expect Sintex to generate positive free cash flow over FY12-14, largely on account

of (1) improved emphasis on working capital management, and (2) moderating capex.

Sintex has already set up enough capacity in almost all the verticals. Accordingly,

management has guided for substantial moderation in capex from the earlier planned

INR10b over the next 3 years.

We model in capex of INR3.4b in FY12 (INR1.9-2b in 1HFY12) and a total of INR3.5b

over FY13-14. Decline in capex would improve the likelihood of positive FCF; we

estimate FCF at INR8.1b over FY12-14.

FCF to improve balance sheet; FCCB redemption under controlIn FY08, Sintex had raised USD225m of FCCBs (mainly for overseas acquisition), which

are maturing in Mar-13 with redemption value of ~USD290m. The company expects to

finance the same as follows -

1. USD110m of unused FCCBs in the form of overseas deposit;

2. USD70m from internal accruals; and

3. USD110m re-finance though ECB.

The redemption of FCCBs coupled with rising FCF would lower debt on the balance

sheet. Our estimates suggest Sintex's net DER will decline from 0.6x in FY11 to 0.3x in

FY14. Nonetheless, lower asset utilization and declining margin could dent RoE/RoCE

to 13.2%/11.4% in FY13 and 13.6%/12.8% in FY14 (v/s 20.5%/14.3% in FY11).

Du Pont: Lower assets turn and declining margins to impact RoE

FY07 FY08 FY09 FY10 FY11 FY12E FY13E FY14E

Net income / PBT 0.78 0.70 0.76 0.71 0.73 0.81 0.81 0.75

Interest burden (PBT/EBIT) 0.90 0.94 1.01 1.04 0.91 0.77 0.77 0.84

EBIT margin (EBIT/Revenue) 0.16 0.14 0.13 0.12 0.15 0.13 0.12 0.13

Asset turnover (Revenue/Avg TA) 0.87 0.95 0.83 0.77 0.92 0.85 0.87 0.94

Leverage (Avg TA/Avg equtiy) 2.06 2.20 2.32 2.36 2.25 2.13 1.96 1.78

RoE (%) 20.0 19.4 19.1 15.9 20.5 14.6 13.2 13.6

RoCE (%) 15.2 14.2 12.6 10.0 14.3 11.9 11.4 12.8

Source: Company/MOSL

Generation of FCF would

partly addresses the

accrual required for FCCB

redemption

0.3

0.5

0.6

0.8

0.60.6

0.20.2

FY07

FY08

FY09

FY10

FY11

FY1

2E

FY1

3E

FY1

4E

16%

15%14%

13%14%

12% 11%13%

10%

14%13%15%

19%19%20% 20%

FY07

FY08

FY09

FY10

FY11

FY1

2E

FY1

3E

FY1

4E

RoCE RoE

Net DER to decline from 0.6x in FY11 to 0.3x in FY14 RoE/RoCE to decline to 12.6%/12.2%

Source: Company/MOSL

Sintex Industries

27 January 2012 18

Concerns priced in; Buy with TP of INR112, 42% upside Sintex's current valuation reflects both (1) growth moderation, and (2) other concerns

(FCCB repayment, conflict of interest in power venture).

The company is expected to generate positive FCF over FY12-14, which should boost

investors' confidence.

We value Sintex at 8x FY13E EPS to arrive at a target price of INR112, 42% upside from

current levels. Buy.

Current valuation discounts unsustainableHistorically, Sintex has traded almost at par with Midcap CNX P/E, barring recent times

when concerns over FCCB repayment, MTM forex loss and conflict of interest issue on

power venture raised the discount. At current valuation, the stock trades at 5.6x

FY13E EPS and 4.9x FY14E EPS, which we believe adequately prices in most risks and

concerns (see page 20 for details).

Historically Sintex has traded almost at par with CNX Mid-cap Long-term average P/E stands at 11.9x

Source: Company/MOSL

2

6

10

14

18

22

26

30

De

c-06

Jun-

07

De

c-07

Jun-

08

De

c-08

Jun-

09

De

c-09

Jun-

10

De

c-10

-12

-8

-4

0

4

8

12Pre mi um Si nte x CNX Mi dca p

4.7

11.9

27.1

4.1

0

7

14

21

28

35D

ec-0

6

Jul-0

7

Dec

-07

Jun-

08

Dec

-08

Jun-

09

Dec

-09

Jun-

10

Dec

-10

Jun-

11

Dec

-11

P/E (x) Avg(x) Peak(x) Min(x)

Sales Growth assumptions (%)

FY08 FY09 FY10 FY11 FY12E FY13E FY14E

Textiles 10.2 6.5 -6.7 25.8 6.0 6.0 6.0

Plastics 126.0 39.7 9.3 37.5 2.9 5.9 11.6

Building Materials 68.9 22.9 14.5 50.9 -5.5 10.8 13.6

Prefab 38.9 1.2 -15.7 14.4 8.0 12.5 12.5

Monolithic 115.0 59.1 86.0 -15.0 10.0 15.0

Tanks 18.0 -9.5 14.9 22.4 15.0 10.0 10.0

Composites 267.1 58.8 4.7 24.7 12.6 1.1 9.4

Domestic 83.9 4.8 15.1 24.6 20.0 15.0 15.0

Foreign 113.0 -0.5 24.7 8.4 -7.7 5.0

Source: Company/MOSL

EBITDA Margin assumptions (%)

FY08 FY09 FY10 FY11 FY12E FY13E FY14E

Textiles 27.6 27.8 20.0 24.0 22.0 22.0 22.0

Plastics 16.1 15.5 15.9 17.5 15.9 15.5 16.0

Building Materials 17.2 18.1 17.1 19.0 18.3 17.2 17.7

Prefab 18.6 20.1 16.6 20.5 20.0 19.0 19.5

Monolithic 19.0 18.0 19.0 19.5 19.0 17.5 18.0

Tanks 9.0 9.0 10.1 11.0 10.0 10.0 10.0

Composites 14.8 12.5 14.8 15.0 13.6 13.7 14.1

Domestic 22.2 14.8 20.2 21.0 19.7 19.1 19.1

Foreign 7.3 11.4 11.7 11.6 9.7 9.5 9.9

Source: Company/MOSL

Sintex Industries

27 January 2012 19

Valuing Sintex at INR112/share, 42% upside; BuyWe value Sintex at 8x FY13E EPS, which is 33% discount to its long-term average P/E,

and also 20% discount to prevailing one-year forward multiple of 10x for CNX Mid-

cap. Our target price of INR112 offers 42% upside from current levels. We re-initiate

coverage on Sintex with a Buy rating.

SOTP based value is close to our P/E-based target price

FY13 EBITDA EV Remarks

Texti les 1,077 5,921 Textile peers trading at average 5.5x

one year forward

Prefab 1,489 8,934 Major construction companies IVRCL, HCC,

Monolithic 2,188 13,126 NCC trading at 5.5-6x one year forward EBITDA

Tanks 251 1,003 Nilkamal and Supereme trading at average 4x

on one year forward EBITDA

Domestic Composits 1,789 10,733 Auto sector average 7-8x EBITDA, valuing at 6x

Foreign Composits 1,132 4,529 Auto, electrical clients average multiple 5-8x,

valuing at 6x

Total 7,925 44,245

Net debt 16,598

Equity value 27,648

Value per share 102

Source: MOSL

Sintex Industries

27 January 2012 20

Key risks and mitigants

Severe domestic and/or global slowdownSintex's revenue growth and EBITDA margin for 2Q/3QFY12 and the downward trend

in management guidance reflect the impact of domestic political/economic uncertainty

and global slowdown. Domestic monolithic construction is seeing delayed payments

and execution slowdown. Overseas subsidiaries are facing muted growth and

pressure on margins. If this situation prolongs, there could be downside risks to our

estimates and target price.

Mitigant: Conservative estimates

We believe we have modeled in conservative assumptions for our estimates.

Accordingly, FY11-14E CAGR for both monolithic and overseas composites revenue

works out to 2%. Further, over the period, we have assumed margin contraction of

150bp in monolithic and 170bp in overseas composites.

Deterioration in working capital, FCCB redemption, balance sheet qualityIn YTDFY12, Sintex's working capital situation has deteriorated to 120+ days v/s 102

days as on March 2011. This is mainly due to (1) Rising share of working capital intensive

monolithic revenue, and (2) Delayed payments by state governments. This has caused

reversal of debt-equity correction - rising from 0.62x in March 2011 to 0.66x in

September 2011. This situation coupled with FCCB redemption (USD290m) overhang

and firm interest rates may pose risk to our estimates and target prices.

Mitigant: Management focus on cash conservation

The management has stated its current focus is on working capital management and

cash conservation through (1) selective execution in monolithic projects, (2) improving

collection efficiencies, and (3) lowering capex plan from INR10b over FY12-14. In fact,

our estimates suggest Sintex will start generating meaningful positive FCF of INR8b

over FY12-14. This should help Sintex in redeeming its FCCBs with low recourse to re-

financing (e.g. management targets ECB of USD100-110m).

Concerns on Sintex group power ventureMarkets have been concerned about the Sintex group power venture at two levels.

First, that Sintex itself would invest in the project. This was categorically denied by

the management, which said that the promoters of Sintex were putting up the project

under Shirpur Power Company, where Sintex would not even invest. Once this was

clarified, the second concern was that of conflict of interest i.e. Shirpur Power place

non-remunerative EPC orders with Sintex Infra, 100% subsidiary of Sintex.

Mitigant: Sintex Infra not to compromise on margins

The management clarified that Sintex Infra will execute the INR6b order through its

associate company Durha with expected margin of 14-15%. Durha currently operates

at 18-19% margin (power vertical margin of 15-16%), and hence confident of managing

14-15% margin in the Shirpur Power order as well. Even going forward, Sintex Infra

will only consider taking power orders if margins sustain at this guided level. We

believe management's assurance on future dealing mechanism with the power

venture and expected margin reasonably mitigate the concern.

Sintex Industries

27 January 2012 21

Financials and Valuation

Income Statement (INR Million)

Y/E March 2009 2010 2011 2012E 2013E 2014E

Operating income 31,358 33,192 44,837 46,303 49,041 54,444

Change (%) 37.0 5.8 35.1 3.3 5.9 11.0

EBITDA 5,219 5,380 8,155 7,652 7,925 9,017

EBITDA Margin (%) 16.6 16.2 18.2 16.5 16.2 16.6

Change (%) 31.1 3.1 51.6 -6.2 3.6 13.8

Depreciation 1,144 1,445 1,491 1,711 1,897 2,029

EBIT 4,075 3,936 6,664 5,941 6,028 6,988

Interest 820 731 1,089 1,448 1,420 1,486

Other income 650 392 327 532 367 372

Extraordinary items 194 486 190 -423 -308 0

PBT 4,100 4,083 6,092 4,602 4,667 5,874

Tax 826 772 1,508 1,256 1,143 1,439

Tax / PBT (%) 20.2 18.9 24.8 25.0 24.5 24.5

PAT before MI 3,274 3,311 4,584 3,346 3,523 4,435

PAT margin (%) 10.7 10.1 10.2 7.2 7.2 8.1

Change (%) 41.0 1.2 38.4 -27.0 5.3 25.9

MI + Share of profit/loss 23 21 -16 30 30 30

Consolidated PAT 3,251 3,290 4,600 3,316 3,493 4,405

Adj. Con. PAT 3,096 2,896 4,457 3,739 3,801 4,405

Change (%) 45.6 -6.5 53.9 -16.1 1.7 15.9

Balance Sheet (INR Million)

Y/E March 2009 2010 2011 2012E 2013E 2014E

Equity share capital 271 271 271 271 271 271

Reserves 16,778 19,198 23,745 26,839 30,111 34,295

Net Worth 17,049 19,469 24,016 27,110 30,383 34,566

Minority Interest 263 190 0 30 60 90

Total Debt 22,964 26,303 27,738 30,209 24,868 25,439

Net deferred tax 1,420 1,693 2,057 2,062 2,062 2,062

Capital employed 41,696 47,655 53,811 59,412 57,373 62,157

Gross fixed assets 23,788 25,581 33,276 37,999 39,609 41,512

Less: Acc. Depn. 6,366 7,746 9,156 10,867 12,764 14,793

Net fixed assets 17,422 17,834 24,120 27,132 26,845 26,719

Goodwil l 2,198 2,665 2,190 2,190 2,190 2,190

Capital WIP 2,377 1,716 1,363 0 0 0

Investments 1,819 2,470 3,775 3,398 3,398 3,398

Curr. assets 27,226 30,983 33,007 37,605 36,325 42,062

Inventory 3,771 3,411 3,770 4,978 5,988 5,621

Debtors 8,094 10,121 14,229 16,238 18,004 18,943

Cash & Bank 11,685 9,295 9,861 10,554 5,749 10,786

Loans, Adv. & Others 3,676 8,157 5,147 5,835 6,584 6,712

Current liab. & prov. 9,348 8,015 10,644 10,913 11,385 12,212

Creditors 5,147 4,029 6,522 7,413 7,885 8,712

Other Liabilities 518 479 497 0 0 0

Provisions 3,683 3,507 3,625 3,500 3,500 3,500

Net current assets 17,878 22,969 22,362 26,692 24,940 29,850

Misc. exp. 2 0 0 0 0 0

Total Assets 41,696 47,655 53,811 59,412 57,373 62,157

E: MOSL Estimates

Sintex Industries

27 January 2012 22

Financials and Valuation

Ratios

Y/E March 2009 2010 2011 2012E 2013E 2014E

Basic (INR)

EPS 11.4 10.7 16.4 13.8 14.0 16.2

Growth (%) 45.6 -6.5 53.8 -16.1 1.7 15.9

Cash EPS 16.2 17.4 22.5 18.5 19.8 23.7

Book value 62.9 71.8 88.6 100.0 112.1 127.5

Divd. Per Share 0.6 0.6 0.7 0.7 0.7 0.7

Payout incl. Div. Tax (%) 5.4 5.8 4.5 6.7 6.3 5.0

Valuation (x)

P/E 4.8 5.7 5.6 4.9

Cash P/E 3.5 4.3 4.0 3.3

Price/Book value 0.9 0.8 0.7 0.6

EV/Sales 0.8 0.8 0.8 0.6

EV/EBITDA 4.4 4.9 4.7 3.6

Dividend yield (%) 0.8 0.9 0.9 0.9

Profitability ratios (%)

Average RoE 19.1 15.9 20.5 14.6 13.2 13.6

Average RoCE 12.6 10.0 14.3 11.9 11.4 12.8

Turnover ratios

Debtors (days sales) 94 111 116 128 134 127

Inventory (days sales) 44 38 31 39 45 38

Creditor (days total exp) 79 59 70 70 70 70

Asset turnover (x) 0.8 0.7 0.9 0.8 0.9 0.9

Leverage ratio

Debt/Equity (x) 0.6 0.8 0.6 0.6 0.5 0.3

Cash Flow Statement (INR Million)

Y/E March 2009 2010 2011 2012E 2013E 2014E

PBT before EO items 3,883 3,576 5,918 4,995 4,944 5,844

Add: Depn. & Amort. 1,153 1,446 1,491 1,711 1,897 2,029

Interest 820 731 1,089 1,448 1,420 1,486

Less: Direct taxes 826 772 1,508 1,256 1,143 1,439

(Inc)/Dec in WC -3,664 -7,480 1,172 -3,637 -3,052 126

CF from operations 1,366 -2,499 8,162 3,261 4,066 8,046

CF from opn. incl. EO 1,560 -2,013 8,352 2,838 3,758 8,046

(Inc)/Dec in FA -6,719 -1,663 -6,948 -3,360 -1,610 -1,903

(Pur)/Sale of invts. 1,433 -651 -1,305 378 0 0

CF from invt. activity -5,286 -2,315 -8,253 -2,982 -1,610 -1,903

FCF -3,726 -4,327 99 -145 2,148 6,143

Inc/(Dec) in Net Worth -1,417 -680 153 0 0 0

Inc/(Dec) in Debt 3,702 3,339 1,434 2,471 -5,342 571

Inc/(Dec) in Minority Int. 60 -74 -190 30 30 30

Inc/(Dec) in deferred tax liab. 350 274 364 5 0 0

Less: Interest paid 820 731 1,089 1,448 1,420 1,486

Divd & Divd Tax 177 191 206 221 221 221

CF from fin. activity 1,699 1,938 467 837 -6,953 -1,106

Inc/Dec in cash -2,028 -2,390 566 693 -4,805 5,037

Add: Beginning balance 13,713 11,685 9,295 9,861 10,554 5,749

Closing balance 11,685 9,295 9,861 10,554 5,749 10,786

E: MOSL Estimates

Sintex Industries

27 January 2012 23

N O T E S

DisclosuresThis report is for personal information of the authorized recipient and does not construe to be any investment, legal or taxation advice to you. This research report does not constitute an offer, invitation or inducementto invest in securities or other investments and Motilal Oswal Securities Limited (hereinafter referred as MOSt) is not soliciting any action based upon it. This report is not for public distribution and has beenfurnished to you solely for your information and should not be reproduced or redistributed to any other person in any form.

Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. The person accessing this information specifically agrees to exempt MOSt or any of its affiliates

or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold MOSt or any of its affiliates or employees responsible for any such misuse and further agrees to hold MOStor any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays.

The information contained herein is based on publicly available data or other sources believed to be reliable. While we would endeavour to update the information herein on reasonable basis, MOSt and/or itsaffiliates are under no obligation to update the information. Also there may be regulatory, compliance, or other reasons that may prevent MOSt and/or its affiliates from doing so. MOSt or any of its affiliates or

employees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report . MOSt or any of its affiliatesor employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitnessfor a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations.

This report is intended for distribution to institutional investors. Recipients who are not institutional investors should seek advice of their independent financial advisor prior to taking any investment decision

based on this report or for any necessary explanation of its contents.

MOSt and/or its affiliates and/or employees may have interests/positions, financial or otherwise in the securities mentioned in this report. To enhance transparency, MOSt has incorporated a Disclosure of InterestStatement in this document. This should, however, not be treated as endorsement of the views expressed in the report.

Disclosure of Interest Statement Sintex1. Analyst ownership of the stock No2. Group/Directors ownership of the stock Yes3. Broking relationship with company covered No4. Investment Banking relationship with company covered No

Analyst CertificationThe views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or issues, and no part of the compensation of the research analyst(s) was, is, orwill be directly or indirectly related to the specific recommendations and views expressed by research analyst(s) in this report. The research analysts, strategists, or research associates principally responsiblefor preparation of MOSt research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues.

Regional Disclosures (outside India)This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary tolaw, regulation or which would subject MOSt & its group companies to registration or licensing requirements within such jurisdictions.

For U.K.This report is intended for distribution only to persons having professional experience in matters relating to investments as described in Article 19 of the Financial Services and Markets Act 2000 (Financial

Promotion) Order 2005 (referred to as "investment professionals"). This document must not be acted on or relied on by persons who are not investment professionals. Any investment or investment activity towhich this document relates is only available to investment professionals and will be engaged in only with such persons.

For U.S.MOSt is not a registered broker-dealer in the United States (U.S.) and, therefore, is not subject to U.S. rules. In reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange

Act of 1934, as amended (the "Exchange Act") and interpretations thereof by the U.S. Securities and Exchange Commission ("SEC") in order to conduct business with Institutional Investors based in the U.S.,Motilal Oswal has entered into a chaperoning agreement with a U.S. registered broker-dealer, Marco Polo Securities Inc. ("Marco Polo").

This report is intended for distribution only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the Exchange Act and interpretations thereof by SEC (henceforth referred to as "major institutionalinvestors"). This document must not be acted on or relied on by persons who are not major institutional investors. Any investment or investment activity to which this document relates is only available to major

institutional investors and will be engaged in only with major institutional investors.

The Research Analysts contributing to the report may not be registered /qualified as research analyst with FINRA. Such research analyst may not be associated persons of the U.S. registered broker-dealer, MarcoPolo and therefore, may not be subject to NASD rule 2711 and NYSE Rule 472 restrictions on communication with a subject company, public appearances and trading securities held by a research analyst account.

Motilal Oswal Securities Ltd3rd Floor, Hoechst House, Nariman Point, Mumbai 400 021

Phone: (91-22) 39825500 Fax: (91-22) 22885038. E-mail: [email protected]