Singapore Rec

29

Renewable Energy Corporation SINGAPORE PRESS CONFERENCE October 26, 2007 Wafers Modules Cells Silicon Materials

Transcript of Singapore Rec

Renewable Energy

Corporation

Wafers

Modules

Silicon Materials

Cells

Renewable Energy

CorporationSINGAPORE PRESS CONFERENCE

October 26, 2007

Wafers

ModulesCells

Silicon Materials

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

2

Disclaimer

This Presentation includes and is based, inter alia, on forward-looking information and statements that are subject to risks and uncertainties that could cause actual results to differ. These statements and this Presentation are based on current expectations, estimates and projections about global economic conditions, the economic conditions of the regions and industries that are major markets for REC ASA and REC ASA’s (including subsidiaries and affiliates) lines of business. These expectations, estimates and projections are generally identifiable by statements containing words such as ”expects”, ”believes”, ”estimates” or similar expressions. Important factors that could cause actual results to differ materially from those expectations include, among others, economic and market conditions in the geographic areas and industries that are or will be major markets for REC’s businesses, energy prices, market acceptance of new products and services, changes in governmental regulations, interest rates, fluctuations in currency exchange rates and such other factors as may be discussed from time to time in the Presentation. Although REC ASA believes that its expectations and the Presentation are based upon reasonable assumptions, it can give no assurance that those expectations will be achieved or that the actual results will be as set out in the Presentation. REC ASA is making no representation or warranty, expressed or implied, as to the accuracy, reliability or completeness of the Presentation, and neither REC ASA nor any of its directors, officers or employees will have any liability to you or any other persons resulting from your use.This presentation was prepared for the Singapore press conference on October 26, 2007. Information contained within will not be updated. The following slides should be read and considered in connection with the information given orally during the presentation.The REC shares have not been registered under the U.S. Securities Act of 1933, as amended (the "Act"), and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the Act.

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

3

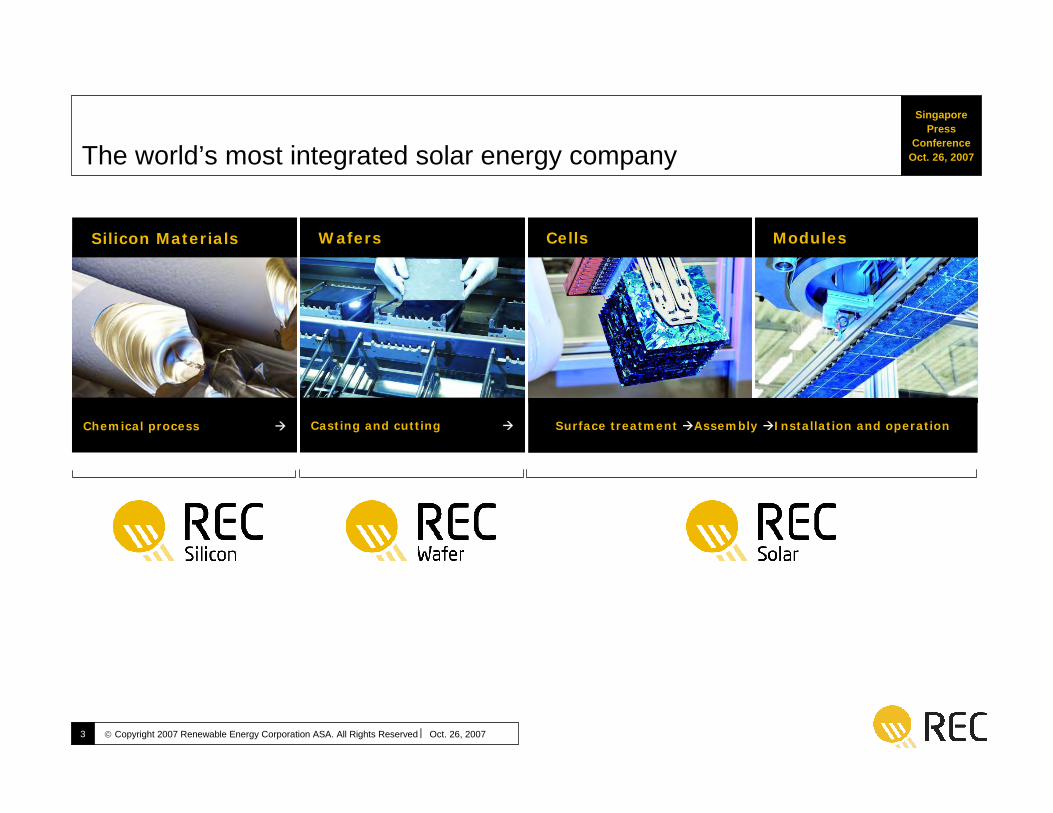

The world’s most integrated solar energy company

Cells Modules

Chemical process

Wafers

Casting and cutting

Silicon Materials

Surface treatment Assembly Installation and operation

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

4

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

(EJ/

Yea

r)

Oil Coal Gas Nuclear Hydro Bio Wind PV Solar - other Other

Solar energy opportunity

Declining stock of fossil fuels, climate changes and increasing competitiveness of PV systems will boost usage of solar energy over the next century

Source: solarwirtschaft.de

Unlimited renewable source of supply

Increasingly cost competitive

Decentralized power source

Peak power at peak time of usage

Environmentally friendly

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

5

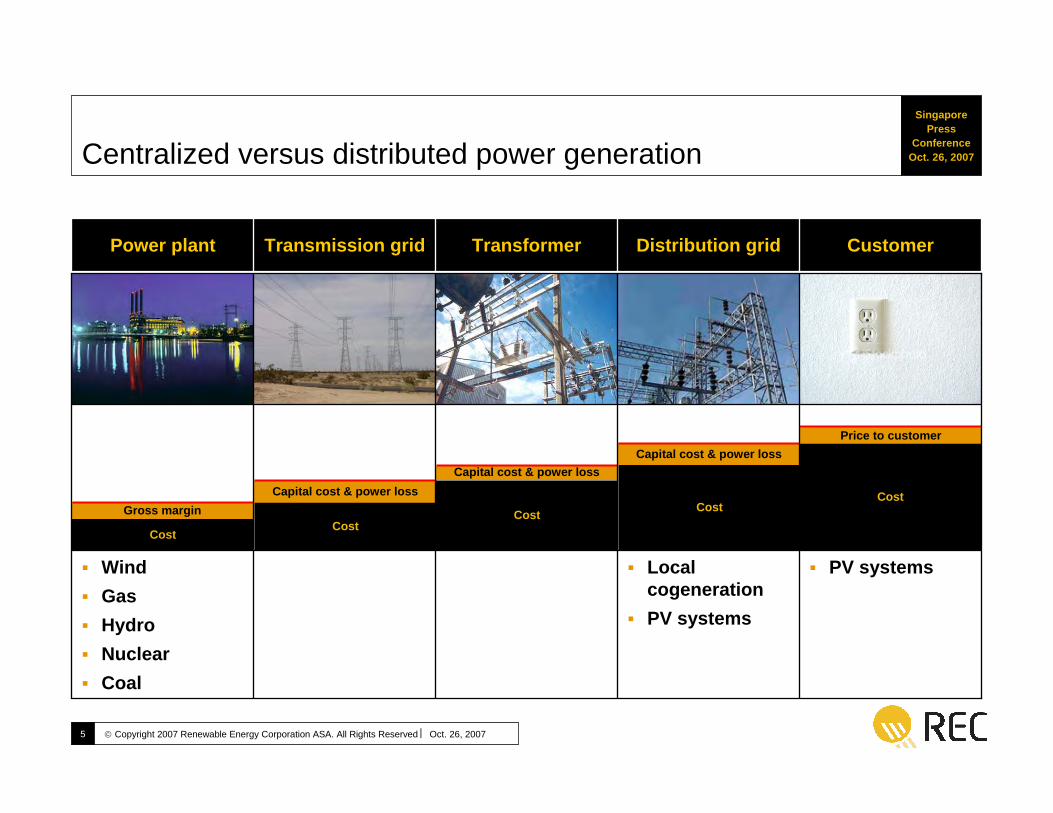

Capital cost & power lossPrice to customer

Cost

Gross marginCapital cost & power loss

Capital cost & power loss

CostCost Cost

Cost

Centralized versus distributed power generation

CustomerDistribution gridTransformerTransmission gridPower plant

PV systemsLocal cogenerationPV systems

WindGasHydroNuclearCoal

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

6

Broad range of solar power applications

Residential buildings Commercial buildings PV power plants

Home systems Water pumping Telecom Space

Grid connected

Off grid

88 percent of market

12 percent of market

Market size and segmentation by applicationMWp

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2 000

2001 2002 2003 2004 2005 2006

On Grid Off Grid

Source: Marketbuzz, 2007

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

7

Renewable Energy

Corporation REC GROUP

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

8

REC has outpaced the industry’s explosive growth

0

500

1 000

1 500

2 000

2 500

3 000

3 500

4 000

4 500

5 000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Capacity expansions

Start production in ScanWafer

Start production in

ScanCell Start production in ScanModule

EstablishedSolar Grade

Silicon

AquiredASiMI

AquiredSiTech

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

9

REC Group facts

Headquarters in OsloProduction facilities: 3 sites in Norway, 2 in the USA, 1 in Sweden1/3 JV ownership of EverQ in Germany

~1 650 employees~600 in REC Silicon

~600 in REC Wafer

~400 in REC Solar

~ 40 in REC Corporate

~900 employees in EverQ

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

10

Unchanged production target, except within REC Silicon

Q3 2007

Production ~1 500 MT polysilicon 106 MW multi10 MW mono

12 MW cells9 MW modules

2007 versus 2006 +4 % +52 % +11 %

First nine months 2007

Production ~4 200 MT polysilicon 337 MW multi28 MW mono

35 MW cells31 MW modules

2007 versus 2006 - 1 % + 75 % + 40 %

Targets 2007

Production ~5 700 MT polysilicon ~465 MW multi~35 MW mono

~50 MW cells~45 MW modules

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

11

REC Group - Financial highlightsRevenues (NOK million) EBITDA (NOK million) EBIT (NOK million)

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2005 367 474 755 8572006 872 1003 1139 13202007 1616 1673 1480

Q1 Q2 Q3 Q4

Growth: +85 % +67 % +30 % Growth: +129 % + 110 % + 23 % Growth: +147 % +124 % +17 %

0

100

200

300

400

500

600

700

800

900

1 000

2005 85 131 250 3642006 380 387 522 6762007 869 812 643

Q1 Q2 Q3 Q40

100

200

300

400

500

600

700

800

2005 53 88 185 2752006 298 303 422 5522007 737 679 495

Q1 Q2 Q3 Q4

Margin: 33 % - 4%p Margin: 43 % - 3%p

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

12

Renewable Energy

Corporation WAFERS, CELLS AND MODULES

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

13

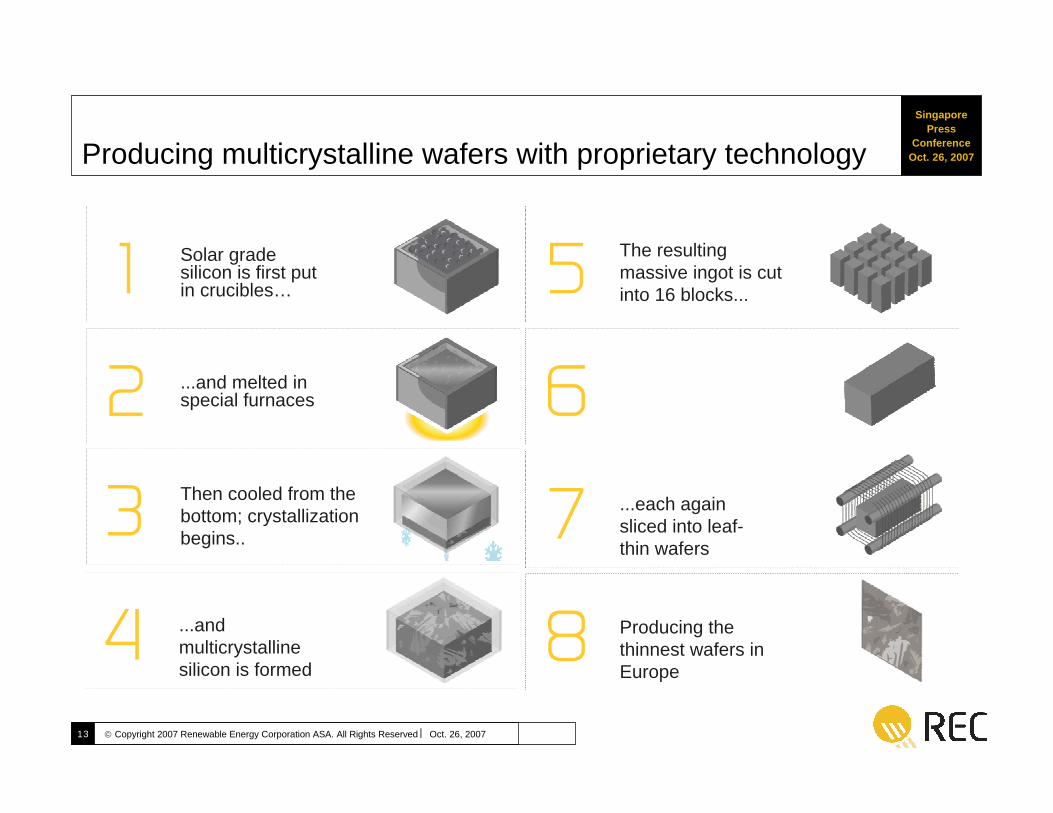

Producing multicrystalline wafers with proprietary technology

Then cooled from the bottom; crystallization begins..

...and melted in special furnaces

Solar grade silicon is first put in crucibles…

...and multicrystallinesilicon is formed

The resulting massive ingot is cut into 16 blocks...

...each again sliced into leaf-thin wafers

Producing the thinnest wafers in Europe

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

14

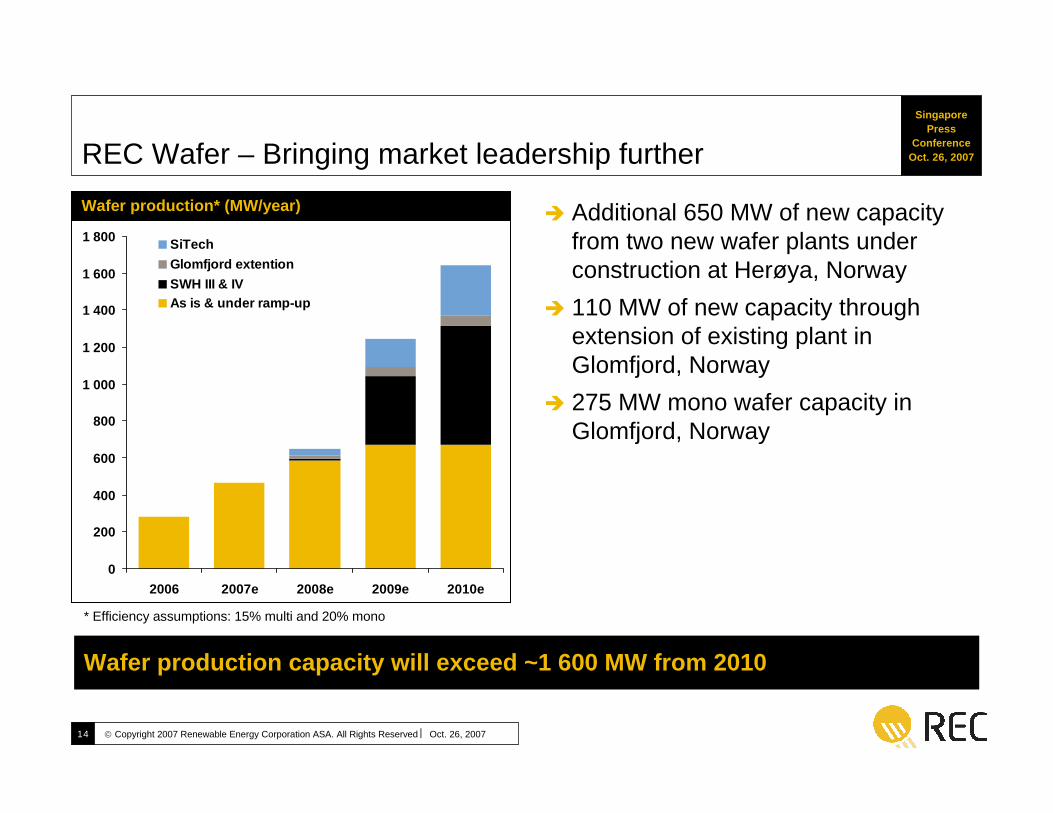

REC Wafer – Bringing market leadership further

0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

2006 2007e 2008e 2009e 2010e

SiTechGlomfjord extentionSWH III & IVAs is & under ramp-up

Additional 650 MW of new capacity from two new wafer plants under construction at Herøya, Norway110 MW of new capacity through extension of existing plant in Glomfjord, Norway275 MW mono wafer capacity in Glomfjord, Norway

Wafer production* (MW/year)

Wafer production capacity will exceed ~1 600 MW from 2010

* Efficiency assumptions: 15% multi and 20% mono

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

15

Doping

Anti reflective coating

Soldering

Screen printing

Encapsulation and testing

Distribution

Wafer

Wet chemistry

From wafers to modules … and into the market

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

16

REC Solar – Climbing up the ranks

180 MW of new cell capacity in NarvikAdditional 105 MW module capacity in Glava, SwedenFurther growth initiatives will focus on:

– Economies of scale

– Increased level of automation

– Proprietary technology development

JV, M&A, toll-production and outsourcing opportunities being evaluated

0

50

100

150

200

250

2005 2006 2007e 2008e 2009e 2010e

CellModule

Cell and module production (MW/year)

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

17

Renewable Energy

CorporationMAIN FOCUS AREAS

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

18

Main focus areas1. Cost competitiveness of PV electricity, slide 1 of 2

Source: REC, based on EC Vision Report 2005 (EPIA: Towards an Effective Industrial policy for PV (RWE Schott Solar))

900 hrs/year:~0.50 €/kWh

1990 2000 2010e 2020e 2030e 2040e

1.0

0.8

0.6

0.4

0.2

0.0

(€/k

Wh)

Photovoltaic Utility peak cost Bulk cost

1 800 hrs/year:~0.25 € /kWh

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

19

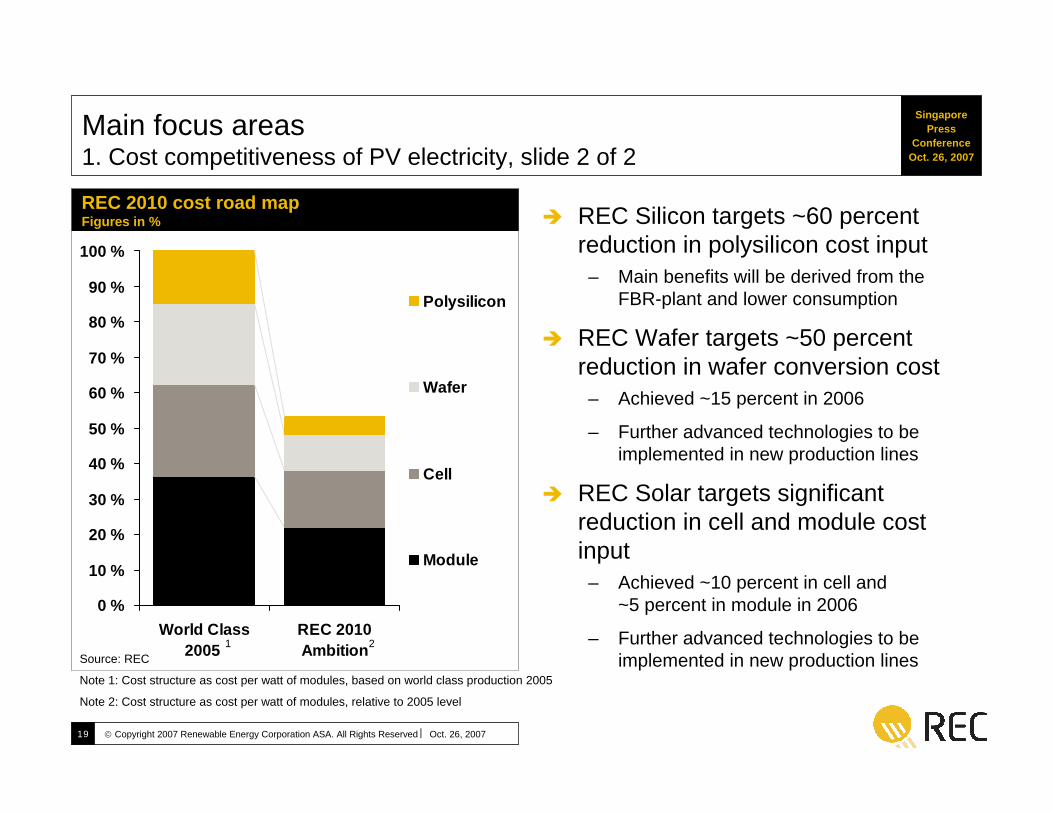

REC 2010 cost road mapFigures in %

0 %

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

World Class2005

REC 2010Ambition

Polysilicon

Wafer

Cell

Module

Source: REC

Note 1: Cost structure as cost per watt of modules, based on world class production 2005

Note 2: Cost structure as cost per watt of modules, relative to 2005 level

1 2

REC Silicon targets ~60 percent reduction in polysilicon cost input– Main benefits will be derived from the

FBR-plant and lower consumption

REC Wafer targets ~50 percent reduction in wafer conversion cost– Achieved ~15 percent in 2006

– Further advanced technologies to be implemented in new production lines

REC Solar targets significant reduction in cell and module cost input– Achieved ~10 percent in cell and

~5 percent in module in 2006

– Further advanced technologies to be implemented in new production lines

Main focus areas1. Cost competitiveness of PV electricity, slide 2 of 2

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

20

Main focus areas2. Technology development

RECWafer

RECSolar

Furnace technologyAutomated waferingprocessesThin wafers

State-of-the-art production technologiesHigh level of automation

RECSilicon

Silane technologyUnsurpassed polysiliconpurityNew polysilicon technology breakthrough (FBR)

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

21

Putting safety firstLeveraging organizational capacity and effectiveness Infusing, retaining and developing talentEnhancing goal- and result-orientation at all levelsFocusing on strong leadership capabilityEmbracing diversity while Building a unified teamLiving our Values!

Main focus areas3. Organizational development

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

22

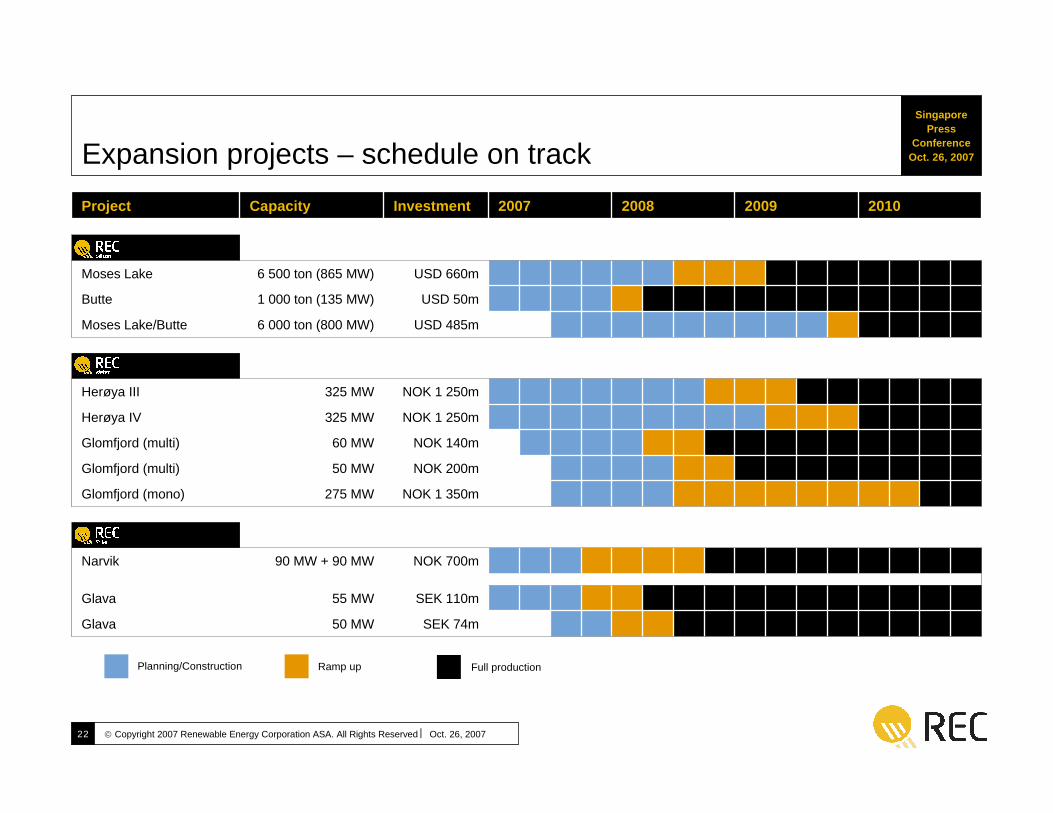

Expansion projects – schedule on trackProject Capacity Investment 2007 2008 2009 2010

Moses Lake 6 500 ton (865 MW) USD 660m

Butte 1 000 ton (135 MW) USD 50m

Moses Lake/Butte 6 000 ton (800 MW) USD 485m

Herøya III 325 MW NOK 1 250m

Herøya IV 325 MW NOK 1 250m

Glomfjord (multi) 60 MW NOK 140m

Glomfjord (multi) 50 MW NOK 200m

Glomfjord (mono) 275 MW NOK 1 350m

Narvik 90 MW + 90 MW NOK 700m

Glava 55 MW SEK 110m

Glava 50 MW SEK 74m

Planning/Construction Ramp up Full production

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

23

Renewable Energy

Corporation

SINGAPORE SELECTED FORNEW SOLAR SITE

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

24

Comprehensive process towards selecting Singapore

A long process - of nine monthsScreening of more than 200 possible locations in 18 countries on 3 continentsDue diligence of almost 20 locations and Final negotiations with a handful of sites

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

25

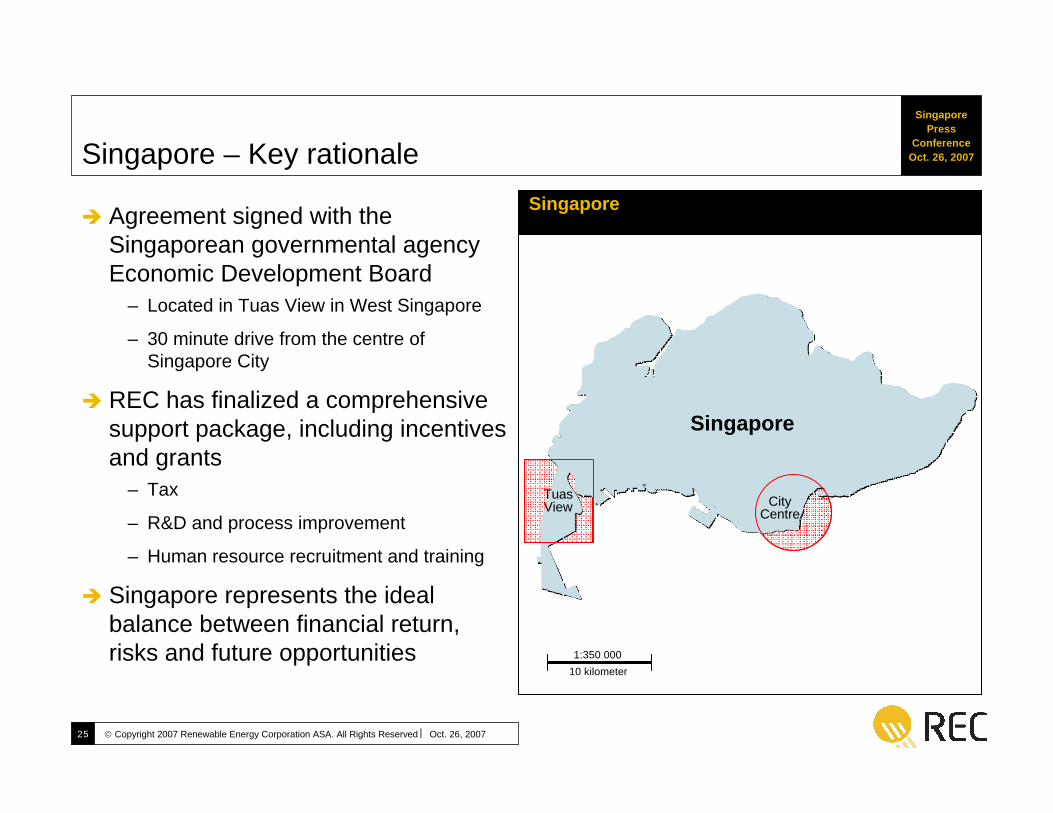

Singapore – Key rationale

Agreement signed with the Singaporean governmental agency Economic Development Board

– Located in Tuas View in West Singapore

– 30 minute drive from the centre of Singapore City

REC has finalized a comprehensive support package, including incentives and grants

– Tax

– R&D and process improvement

– Human resource recruitment and training

Singapore represents the ideal balance between financial return, risks and future opportunities

TuasView

Singapore

City Centre

1:350 00010 kilometer

Singapore

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

26

REC activities in Singapore

Manufacturing – Solar wafers

– Solar cells

– Solar modules

R&D activities, incl.– Process innovation

– Factory automation

Solar value chain cost optimization processesIncorporates utilities, infrastructure and support facilities, as well as an on-site supplier park

Birds Eye View from South – West

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

27

Worldscale integrated solar manufacturing complex

Street View from South – WestSite description– Possibly the world’s largest integrated solar

manufacturing complex

Complex will be integrated– Will be developed in stages

– Production capacity may reach 1.5 GW

– Value chain will not be balanced

– Investment could reach around EUR 3 billion over 5 years

– Total number of employees could be around 3 000 people

Pre-engineering has commenced– First investment decision will be taken

when pre-engineering is completed

Production expected to start no later than 2010

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

28

Exciting careers in a future oriented industry

Great need for competencies– Engineers and technicians

– Skilled production operators

– Business managers

Comprehensive training programs Planned collaboration with Singapore research institutions

© Copyright 2007 Renewable Energy Corporation ASA. All Rights Reserved ⎮ Oct. 26, 2007

SingaporePress

Conference Oct. 26, 2007

29

Renewable Energy

CorporationDelivering on the promise of solar