Singapore Budget 2017 Synopsis - EY - United StatesFILE/ey-singapore-budget-2017-synopsis.pdf ·...

56

Singapore Budget 2017 Synopsis

Transcript of Singapore Budget 2017 Synopsis - EY - United StatesFILE/ey-singapore-budget-2017-synopsis.pdf ·...

Singapore Budget 2017 Synopsis

MCI (P) 013/01/2017Printed by Hock Cheong Printing Pte Ltd

Introduction The Singapore way 3

Business tax Corporate income tax rate and rebate 7

Enhancing the Global Trader Programme 9

Introducing an intellectual property regime that 11 encourages the exploitation of IP arising from R&D activities of the taxpayer

Introducing a safe harbour rule for payments under 14 Cost Sharing Agreements for R&D projects

ExtendingandrefiningtheAircraftLeasingScheme 15

Extending the withholding tax exemption on payments 17 for international telecommunications submarine cable capacity under an Indefeasible Rights of Use agreement

RefiningtheFinanceandTreasuryCentreScheme 18

Extending the tax incentive schemes for project 20 andinfrastructurefinance

ExtendingandrefiningtheIntegratedInvestment 21 Allowance Scheme

Extending the withholding tax exemption on payments 22 made to non-resident non-individuals for structured productsofferedbyfinancialinstitutions

Withdrawing the tax deduction for computer 23 donation scheme

Withdrawing the Accelerated Depreciation Allowance 24 forEnergyEfficientEquipmentandTechnologyScheme

Allowingtheacceleratedwriting-downallowances 25 foracquisitionofintellectualpropertyrightsformedia and digital entertainment content scheme to lapse

Allowing the International Arbitration Tax Incentive 26 to lapse

At a

gla

nce

1Singapore Budget 2017 Synopsis

At a

gla

nce

Personal income tax

Personal income tax rebate and tax rate 29

Goods and services tax

Imposing GST on the digital economy 33

Withdrawing the GST Tourist Refund Scheme for tourists 37 departing by international cruise

Miscellaneous Strengthening enterprises’ capabilities through 39

scaling up globally

Digitalisation and innovation 40

Defering foreign worker levy changes 43

Allowing property tax exemption for Approved 43 Building Project Scheme to lapse

Additional Special Employment Credit 44

Final thoughts 46

Tax services in Singapore 48

Singapore Tax Partners, Executive Directors 50 and Directors

Glossary of terms 52

Singapore Budget 2017 Synopsis2

The world is undergoing a period of great uncertainty and rapid technological change. Inthisyear’sbudget,theFinanceMinisterreaffirmsthe Singapore way to respond to such challenges. Singapore must take a learning and adaptive approach, try new methods, draw on feedback, adjustandrefineourplansaswemoveforwardtogether with a can-do spirit.

Budget 2017 builds on the foundation laid out in Budget 2016. The Industry Transformation Maps have been launched for six sectors and will continue to be rolled out for the remaining 17 sectors within FY2017.TheAdaptandGrowinitiativeintroducedlast year will be enhanced for both Professionals, Managers, Executives and Technicians, and rank-and-fileworkersintransition.

It is not surprising that the measures taken to build our capabilities for the long term are largely based on the strategies and recommendations putforthbytheCommitteeontheFutureEconomy(CFE)twoweeksago.

Our journey towards SG100 story from Budget 2016 continues with moving forward together — the Singapore way — in Budget 2017.

Go digital, go internationalSmall-and-medium enterprises (SME) form the bulk of our enterprises and we can only be successful in transforming our economy if SMEs are able to use digital technology, embrace innovation and scale up. SMEs will receive support in adopting digital technologies to transform their businesses. Under the SMEs Go Digital Programme, SMEs will receive step-by-step advice, in-person help and funding on the technologies to use at each stage of their growth.

Enterprises can also tap on the enhanced InternationalFinanceSchemetoco-sharerisk oncross-borderprojectfinancing.Anew S$600mInternationalPartnershipFundwill co-invest with enterprises to help them scale up and internationalise.

IntroductionThe Singapore way

3Singapore Budget 2017 Synopsis

“ Budget 2017 placed great emphasis on building partnerships between different parts of society to create a more dynamic and resilient economy. The government is also committed to building an inclusive and caring society, which is important for the fruits of our growth to be enjoyed by all people in Singapore. ”

Go greenWe are beginning to feel the effects of climate change, such as prolonged drier and warmer weather. The government is planning to introduce carbon tax in 2019 to reduce greenhouse gas emissions. The proposed carbon tax will be applied upstream on power stations and other large direct emitters and the impact on most businesses and households is expected to be modest. The carbon tax will be implemented after consultation with stakeholders. We hope the upstream industries take steps to reduce emissions by adopting clean energy and newer technologies.

Changes are also made to the pricing and tax regime of diesel, motor vehicles and water to curb their consumption and usage. Water prices — last adjusted in 2000 — will now increase by 30%.

Go deepThe efforts to re-skill and up-skill our workers continue.FundingsupportforSingaporeanstotake approved courses will continue to be available throughSkillsFuture.

A Global Innovation Alliance will be set up for Singaporeans to gain overseas experience and collaborate with their counterparts in other innovative cities. There will be programmes to enable our tertiary students to connect with

start-ups overseas. This will hopefully help to change the mindset of our students and cultivate the entrepreneurial spirit in them.

Tax reformOneoftheCFErecommendationscallsfora review of Singapore’s tax system, so that it remains broad-based, progressive and fair, and at the same time, be competitive and pro-growth.

Countries, large and small, are reviewing their corporate tax regimes to keep them competitive. No major changes have been introduced in this budget to reform our tax system, but the Minister alluded to what is coming. We can expect tax refinementsinresponsetotheBaseErosion andProfitShiftingproject.

Businesses can also expect the government to raise revenues through new taxes or raise tax rates in order to fund rising expenditure in the mid to long term. One such option being studied by the governmentistherequirementforforeign-basede-commerce businesses to be GST-registered, as digital transactions are expected to boom.

With the creation and loss of jobs in different fieldsarisingfromtheincreaseduseofrobotsandartificialintelligence,thedaymaycomewherewecannotruleoutthatrobotsandartificialintelligence will be subject to taxation too.

Singapore Budget 2017 Synopsis4

Go togetherBudget 2017 placed great emphasis on building partnerships between different parts of society to create a more dynamic and resilient economy. The government is also committed to building an inclusive and caring society, which is important for the fruits of our growth to be enjoyed by all people in Singapore.

Oureconomicstrategiesforthenextfivetoten years will be shaped by the strategies recommendedbytheCFE.Whetherwecanachieve the long-term economic growth target of two to three percent per year will depend on how well we partner one another to implement them.

As Martin Luther King Jr. said: “If you can’t fly, then run; if you can’t run, then walk; if you can’t walk, then crawl; but whatever you do you have to keep moving forward.”

And the reason is simple.

BorrowingthewordsofHenryFord,“If everyone is moving forward together, then success takes care of itself.”

Chung-Sim Siew Moon Partner and Head of Tax 20February2017

5Singapore Budget 2017 Synopsis

Business tax

Busin

ess

tax

6 Singapore Budget 2017 Synopsis

Business tax

CurrentThe corporate income tax rate is 17% with a partial tax exemption for normal chargeable income of up to S$300,000 as follows:

► 75%exemptionofuptothefirstS$10,000.

► 50%exemptionofuptothenextS$290,000.

Companiesenjoya50%corporateincometaxrebateforYA2016 andYA2017,withacapofS$20,000rebateperYA.

ProposedThe Minister did not propose any change to the corporate income tax rate and the partial tax exemption threshold remains the same.

To help companies cope with the economic uncertainty and continue restructuring, the corporate income tax rebate will be enhanced and extended:

(a) Corporate income tax rebate cap will be raised from S$20,000 to S$25,000forYA2017(withtherebaterateunchangedat50%).

(b) Corporate income tax rebate will be extended for another year to YA2018,butatareducedrateof20%oftaxpayableandcappedat S$10,000 rebate.

Points of view ► The corporate income tax rate has remained at 17% since YA2010.At17%,Singapore’sheadlinecorporateincometaxratecontinues to be one of the lowest in the world. This rate is only 0.5%higherthanthecurrentHongKongcorporateincometax rateof16.5%.

► In the current changing international tax environment where countriesarecomingtogethertoaddressBaseErosionandProfitShifting (BEPS), there is increasing attention and focus on a country’s corporate income tax rate. Going forward, Singapore thus faces the challenge of managing its corporate income tax rate to remain competitive while addressing the concerns of BEPS.

Corporate income tax rate and rebate

The enhancement of the corporate tax rebate withaS$25,000capforYA2017isindeedwelcomed news and the extension of the rebate toYA2018withacap of S$10,000 is a bonus to businesses.“

“

7Singapore Budget 2017 Synopsis

Business tax

► The effective tax rate of a company in Singapore withS$500,000ofnormalchargeableincomewillbeonly11.8%.Itisfurtherreducedto6.8%(YA2017)and9.8%(YA2018)ifwefactorinthefullcorporateincometaxrebateforYA2017andYA2018.Thisisnotablylowerthantheexistingtaxrateof16.5%inHongKong.Withthetax rebate, a company in Singapore would need to have normal chargeable income exceeding S$9.2m to have an effective tax rate higher than 16.5%.TheeffectivetaxrateinSingaporecouldalso be reduced further through tax incentives.

► The difference between the current corporate income tax rate of 17% and the top marginal personal income tax rate of 22% (with effect fromYA2017)isfivepercent.Self-employedindividuals, depending on their level of income, may consider corporatising their businesses in view of the lower corporate income tax rate and partial tax exemption. However, the tax benefitmaybereducedoreliminatedsinceanarm’s length salary will need to be paid from the company to an owner working in the business. In addition, the costs of operating a company (e.g., audit and secretarial fees) should be taken into account before such a decision is made.

► TheIRAShasclarifiedthat:

► The corporate income tax rebate will be given to all companies including registered business trusts, non-resident companies and companies that receive income taxed at a concessionary tax rate. The rebate, however, will not apply to the income derived by a non-resident company thatissubjecttofinalwithholdingtax.

► Companies need not factor in the corporate incometaxrebatewhenfilingtheirestimatedchargeable income and income tax returns (FormC/C-S)astheIRASwillcompute and allow the corporate income tax rebate automatically.

► ForcompaniesthathavealreadyreceivedtheirnoticesofassessmentforYA2017andYA2018reflectingthelowerornocorporateincome tax rebate, they do not have to submit a revised estimated chargeable income. They arehoweverrequiredtomakepaymentof

the tax payable by the due date according to these notices of assessment. The IRAS will issue revised notices of assessment to affected companies by May 2017 and refund any excess tax paid. If a company is paying taxes by instalments, it will need to continue with the payment schedule based on the instalment plan. The revised notices of assessment and instalment plan will be issued by the IRAS to the company by May 2017.

► The proposed increase in the corporate income taxrebatecaptoS$25,000forYA2017(withtherebaterateunchangedat50%)andtheproposedextensionforanotheryeartoYA2018(butata reduced rate of 20% capped at S$10,000) are part of the continued measures to support businesses, in particular targeted at SMEs as they cope with the current uncertain economic conditions. The proposed changes also recognise thatSMEsmayneedmoreimmediatecashflowrelief, thus the increase in corporate income tax rebateforYA2017andareducedamountinYA2018.However,theproposedincreaseandextensionwillonlybenefitthosethatare tax-paying since the corporate income tax rebate is computed on tax payable.

► Companies may consider deferring capital allowances claims or planning their group loss relief claims to optimise the amount of corporate income tax rebate.

► If the corporate income tax rebate is not extended afterYA2018andwiththephasingoutofthePICScheme, companies, especially SMEs, may need to look towards other avenues such as grants to easetheircashflowpressuresgoingforward.

8 Singapore Budget 2017 Synopsis

Business tax

CurrentThe Global Trader Programme (GTP) grants a concessionarytaxrateof5%or10%onqualifyingincome derived by approved global trading companiesfromqualifyingtransactions.

ProposedTo facilitate and encourage more trading activities in Singapore and to simplify the GTP, the GTP will be enhanced as follow:

a) Therequirementforqualifyingtransactionstobecarriedoutwithqualifyingcounterpartieswillberemoved.Consequently,concessionarytax rate will be granted to approved global trading companies on income derived from qualifyingtransactionswithanycounterparty.

b) Concessionary tax rate will be granted to approved global trading companies on physical trading income derived from transactions in which the commodity is purchased for the purposes of consumption in Singapore or for the supply of fuel to aircraft or vessels within Singapore.

c) Concessionary tax rate will be granted to approved global trading companies on physical trading income attributable to storage in Singapore or any activity carried out in Singapore, which adds value to the commodity by any physical alteration, addition orimprovement(includingrefining,blending,processing or bulk-breaking).

d) ThesubstantiverequirementtoqualifyfortheGTP will be increased.

Enhancing the Global Trader Programme

The enhancements in (a) to (c) will apply to qualifyingincomederivedonorafter21February2017 by approved global trading companies fromqualifyingtransactions.

The enhancement in (d) will apply to new or renewal incentive awards approved on or after 21February2017.

The IE Singapore will release further details of the change by May 2017.

Points of view ► The proposed enhancements in (a) to (c) above

will certainly simplify the overall tax compliance andreportingrequirementsandrelatedcostsfor approved global trading companies. These enhancements have addressed the concerns faced by the approved global trading companies and is therefore a welcomed move. They also resonate well with Singapore’s important role as a commodity trading hub for Asia and will encourage more activities to be anchored out of Singapore. Such trading activities are expected to have a multiplier effect for the economy.

► Before21February2017,approvedglobaltradingcompaniesarerequiredtokeeptrackof all trading transactions and ensure that only qualifyingincomefromqualifyingtransactionswithqualifyingcounterpartiesaretaxedattheconcessionary tax rate. Currently, where a GTP companybuysandsellswithbothqualifyingandnon-qualifyingcounterparties,thecompanyisrequiredtotrackthatbothitsbuyandselllegofitstradingtransactionsarewithqualifyingcounterparties. This can be a challenge where transactions are voluminous and are not back-to-back arrangements. Hence, we applaud this bold movetoremovethecounterpartyrequirementas it takes into consideration the practical challenges faced by GTP companies.

9Singapore Budget 2017 Synopsis

Business tax

► Theremovalofthecounterpartyrequirementalso helps to address mismatch in tax treatment incertaintransactions.Forinstance,inhedgingtransactions, the tax treatment between the derivative transaction and the corresponding underlying physical trading transaction may differ, depending on whether the counterparties are approved or not. This can result in a mismatch in the tax treatment of the derivative profitorlossandthephysicaltradingprofitorloss and in some cases, can be undesirable if a profitononesideistaxedat17%andthelossonthe other side is deductible at the concessionary tax rate. The removal of the counterparty requirementinsuchcaseswillremovesuchmismatch in tax treatment.

► The granting of concessionary tax rates to approved global trading companies on physical trading income derived from the supply of fuel to vessels within Singapore will further enhance and complement Singapore’s status as a major regional bunkering hub, as such tax savings may translate into more competitive bunker prices in the region, besides easing the tracking requirementsfordeterminationofGTPversusnon-GTP income.

► The determination of the value-add income attributable to commodities by any physical alteration, addition or improvement through any activities carried out in Singapore has in practice posed challenges for GTP companies in terms of the methodology to adopt for determining the attributable value-add income and is often a subject of controversy with the IRAS. The removalofthisrequirementwillprovidecertaintyinthedeterminationofqualifyingincome.

► TheincreaseinsubstantiverequirementtoqualifyfortheGTP,giventheenhancementsin(a) to (c) above, is likely to translate into higher thresholdsonthesubstancerequirementsofheadcount, total local business spending and activities conducted in Singapore, in addition to the value of gross annual physical turnover. Dependingonhowsignificanttheincreasesinthe thresholds will be, new GTP applicants and existing approved global trading companies seeking to renew their applications will need to evaluate their abilities to meet the increased

demands. Having said the above, the increased substancerequirementscanbeseentobeinline with Singapore’s status as a Base Erosion andProfitShiftingAssociate,whereoneofthestandardsrequirestaxincentivestobealignedwith the location of economic substance and nexus of value creation.

10 Singapore Budget 2017 Synopsis

Business tax

CurrentCurrently,thePioneer-Services/HeadquartersIncentive and the Development and Expansion Incentive(DEI)-Services/Headquarterscoverintellectual property (IP) income if the income arisesfromqualifyingactivities.

ThePioneer-Services/HeadquartersIncentiveandtheDEI-Services/Headquartersencouragecompanies to use Singapore as a base for conductingheadquartersmanagementactivitiesto oversee, manage and control their regional and global operations and businesses.

The incentives are awarded for carrying out substantiallevelofregionalorglobalheadquartersactivities in Singapore and offer concessionary tax ratesof0%,5%or10%onqualifyingincome.

Qualifying income under the incentives include sales, service fees, licensing fees, franchise fees, commissions and management fees from qualifyingactivities.

Qualifying activities covered under the incentives include, amongst others:

► Strategic business planning and development.

► Marketing control, planning and brand management.

► General management and administration.

► Corporate training and personnel management.

► IP management.

Introducing an intellectual property regime that encourages the exploitation of IP arising from R&D activities of the taxpayer

ProposedTo encourage the use of IPs arising from taxpayer’s R&D activities, IP income will be incentivised under a new IP regime named the IP Development Incentive (IDI). The IDI incorporates the Base Erosion andProfitSharing(BEPS)-compliantmodified nexus approach.

Accordingly, such income will be removed from the scopeofPioneer-Services/HeadquartersIncentiveandtheDEI-Services/Headquartersfornewincentive awards approved on or after 1 July 2017. Existing incentive recipients will continue to have such income covered under their existing incentive awards until 30 June 2021.

The IDI will take effect on 1 July 2017 and will be administered by the EDB.

The EDB will release further details of the change by May 2017.

11Singapore Budget 2017 Synopsis

Business tax

Points of view ► AdoptingBEPS-compliantmodified

nexus approach:

► As a BEPS associate, Singapore is committed to implementing the four minimum standards underBEPS,oneofwhichisBEPSAction5–countering harmful tax practices. Through the adoptionofthemodifiednexusapproachinthe IDI, it sends a strong signal of Singapore’s commitment to maintaining and improving transparency and its proactive support of the BEPS initiative.

► UnderBEPSAction5,preferentialIPregimesshould not be regarded as harmful tax practicesifthetaxbenefitsarelinkedto“substantial activities” being carried on. ThemodifiednexusapproachwhereR&Dspend is used as a proxy for substantial activities was determined to be the most appropriateapproachtodefinesubstantialactivityrequirementinrelationtoIPregimes.

► TheproposedIDIintroducesaspecificIPregime that carves out IP income into a stand-alone incentive, which incorporates the modifiednexusapproachtodeterminetheamountofincomethatmaybenefitfromthetax incentive.

► Underthemodifiednexusapproach,theproportionofincomethatmaybenefitfroman IP regime (the nexus ratio) is the same proportionasthatofqualifyingexpenditurescompared to overall expenditures. The nexus ratio is determined using the following formula:

A + B (*)

A + B + C + D

where:

► “A” represents R&D expenditures incurred by the taxpayer itself

► “B” represents expenditures for unrelated-party outsourcing

► “C”representsacquisitioncostsofIP ► “D” represents expenditures for related-

party outsourcing

► (*)–a30%upliftmaybeappliedon “A” and “B” but only to the extent where therearenon-qualifyingexpenditures (i.e., “C” and “D”)

► As noted from the above formula, R&D expenses paid to third party R&D service providers are included in the numerator but not R&D expenses paid to related party R&D service providers. It is unclear how payments under Cost Sharing Agreements (CSA) will be treated.

► ThetaxbenefitunderIDImaybelimitedfortaxpayers who outsource R&D to related parties, especially for multinationals, which typicallyhavesignificantR&Doperationsworld-wide. The ability to combine the IDI with other incentives such as the DEI, will be important to ensure that Singapore remains attractive as a location to host other critical functions that are complementary to IP ownership.

► Design and features of IDI

► The EDB will release further details of the IDI by May 2017. We expect the details to includehowqualifyingIPincomeisdefined,the applicable concessionary tax rate or tax benefit,whetherR&Dworkcanbeperformedoutside Singapore and how the regime may complement the existing Pioneer-Services/HeadquartersIncentiveandtheDEI-Services/Headquarters.

► UndertheBEPSrecommendation,qualifyingincome should only include income derived from the IP asset and may include royalties, capital gains, other income from the sale of an IP asset and embedded IP income from the sale of products and the use of processes directly relating to the IP asset. If the scope of IP income under the IDI were to include sales income, there will be a need to implement a consistent and coherent method (e.g., based on transfer pricing principles) for separating income unrelated to IP (e.g., marketing and manufacturing returns) from the income arising from IP.

12 Singapore Budget 2017 Synopsis

Business tax

► However, it is noted that the UK Patent Box regimemayapplytoprofitsfromsalesofpatented products (i.e., sales of patented product or products incorporating the patented invention or bespoke spare parts) and not just to embedded IP income. In designing the IDI, one key consideration ought to be whether or not to include sales incomeasqualifyingIPincomeandifso,whether or not to restrict it to just embedded IPincome.Perhapssomeflexibilitycanberetained in this respect for sales income to be covered under other appropriate tax incentive schemes, which are also targeted at attracting substantive activities into Singapore.

► IPincomefromqualifyingactivitieswillberemoved from the scope of Pioneer-Services/ HeadquartersIncentiveandtheDEI-Services/Headquarters.Wenotethatotherincentivessuch as the Pioneer Manufacturing Incentive and DEI Manufacturing Incentive are not impacted. Therefore, for businesses which have been awarded these incentives, their IP income from licensing of IP that are also used in their own manufacturing operations ought to be covered under their existing tax incentives and not subject to the removal arising from the introduction of IDI.

► Given the direction of the government in carving out the IP income from the Pioneer-Services/HeadquartersIncentiveandthe DEI-Services/HeadquartersandsincetheIDIwill be administered by the EDB, it appears likely that there may be conditions attached to the granting of the IDI and the incentive may be granted on a case-by-case approval basis. It is noted that similar IP regimes, such as the UK Patent Box regime, are broad-based and non-discretionary incentives. To encourage innovation across the board, it may be worthwhile to consider whether the IDI regime can be administered in the same manner such that all taxpayers can avail of the tax incentive aslongastheymeetthespecifiedconditions.

► DefinitionofR&D

► To-date, it has been rather challenging for companiestoqualifyfortheR&Ddeductionundersection14DoftheITA.Forexample,ithasbeenimmenselydifficultforsoftwareprojectstoqualifyforsection14D/DAR&Denhanced deduction. In this respect, it is noted that copyrighted software is recognised undertheBEPSAction5guidelinesasqualifyingIPunderthenexusapproachasit shares the fundamental characteristics of patents such as being novel, non-obvious, and useful.

► ItishopedthatthedefinitionofR&Dunderthe IDI will be broader so as to make the IDI more attractive.

► Strengthening Singapore tax treaties

► The introduction of IDI should send a strong signal of Singapore’s intent to develop itself as an IP hub. To complement this, there is also a need to refresh Singapore tax treaties or expand its tax treaty network such that a favourable royalty withholding tax rate is granted on royalties derived by Singapore tax residents. Currently, a majority of Singapore tax treaties provides for royalty withholding taxratesofmorethanfivepercent,whichis not that attractive and may erode the attractiveness of the IDI.

13Singapore Budget 2017 Synopsis

Business tax

CurrentThe IRAS has adopted the position that taxpayers claiming tax deductions for R&D expenditure under section 14D of the ITA for payments made under Cost Sharing Agreements (CSA) are subject to specificrestrictionrulesforcertaincategoriesofexpendituredisallowedundersection15oftheITA.As such, the breakdown of the expenditure covered by CSA payments is examined by the IRAS so as to exclude the disallowed expenditure.

ProposedTo ease compliance, taxpayers may opt to claim taxdeductionundersection14Dfor75%ofthepaymentsmadeunderaCSAincurredforqualifyingR&D projects instead of providing a breakdown of the expenditure covered by the CSA payments. The change will apply to the CSA payments made onorafter21February2017.

The IRAS will release further details of the change by May 2017.

Points of view ► The deduction of CSA payments for R&D projects

has been a contentious issue between taxpayers and the IRAS. Taxpayers have objected to the position taken by the IRAS on the basis that the ITA allows for a 100% tax deduction on CSA payments without having the need to look beyond the payments to strip out disallowable expenditures (such as stock-based compensation expenses). This basis is consistent with that underlying the IRAS’ current treatment of payments made to outsourced R&D service providers claimed under section 14D and in line with the IRAS’ previous treatment of approved CSA payments for R&D projects under section 19C of the ITA, i.e., before deduction for such payments was subsumed under section 14D.

► Accordingly, the proposed safe harbour rule appears to have been introduced as a compromise for taxpayers who disagree with the IRAS’ position. However, it remains to be seen how this proposed safe harbour rule would be receivedasa25%disallowanceofdeductionsrelating to CSA payments appears to be significantlyhigherthanthetypicalproportionof expenditure included in CSA payments that relates to certain expenditure disallowed under section15oftheITA.ItishopedthattheIRASwillprovidedetailsonthetypesofspecificexpenditure items within a CSA payment that willbedisallowedundersection15oftheITAto help taxpayers assess if they should opt for the proposed safe harbour rule and how current deduction claims for CSA payments prior to 21February2017underdisputewiththeIRASwill be resolved.

► It should also be noted that the proposed safe harbour rule only applies to CSA payments for qualifyingR&Dprojects.Fromanadministrativepoint of view, taxpayers who opt to apply the safeharbourrulemaystillberequiredtoprovidebreakdownsofCSApaymentsbyqualifyingR&D projects and furnish information to the IRAStoverifythateachprojectindeedqualifiesas an R&D project in accordance with current tax law and practice. This could be challenging practically as many R&D organisations track costs at an R&D department or facility level and not on a per project basis.

► The IRAS’ current position and the proposed safeharbourruletolimitdeductionto75%ofCSA payments could be viewed as a negative factor by businesses when considering the attractiveness of Singapore as an intellectual property hub to anchor R&D activities.

Introducing a safe harbour rule for payments under Cost Sharing Agreements for R&D projects

14 Singapore Budget 2017 Synopsis

Business tax

CurrentUnder the Aircraft Leasing Scheme (ALS), approved aircraft lessors and aircraft investment managers canenjoythefollowingtaxbenefits:

► Approved aircraft lessors enjoy concessionary taxrateof5%or10%onincomederivedfromthe leasing of aircraft or aircraft engines and qualifyingancillaryactivitiesundersection43Yof the ITA.

► Approved aircraft managers enjoy concessionary tax rate of 10% on income derived from managing the approved aircraft lessor and qualifyingactivitiesundersection43ZoftheITA.

Qualifyingancillaryactivitiesundersection43Yofthe ITA include incidental income derived from the provisionoffinanceintheacquisitionofanyaircraftor aircraft engines by any airline company.

In addition, automatic withholding tax (WHT) exemptionisgrantedonqualifyingpaymentsmadeby approved aircraft lessors to non-tax residents (excluding a permanent establishment in Singapore) inrespectofqualifyingloansenteredintoonorbefore31March2017tofinancethepurchaseofaircraft and aircraft engines, subject to conditions.

The scheme is scheduled to lapse after 31 March 2017.

ProposedTo continue encouraging the growth of the aircraft leasing sector in Singapore, the ALS will be extendedandrefinedasfollows:

a) The ALS will be extended until 31 December 2022.

b) Thescopeofqualifyingancillaryactivitiesforapprovedaircraftlessorsundersection43Yof the ITA will be updated to cover incidental incomederivedfromtheprovisionoffinanceintheacquisitionofaircraftoraircraftenginesbyany lessee.

c) The concessionary tax rate on income derived from leasing of aircraft or aircraft engines and qualifyingancillaryactivitieswillbestreamlinedfrom5%and10%toasinglerateof8%.

The enhancement for (b) will apply to income derivedonorafter21February2017forallincentive recipients.

Therefinementin(c)willapplytoneworrenewalincentive awards approved on or after 1 April 2017.

In addition, the automatic WHT exemption regime willbeextendedtoqualifyingpaymentsmade onqualifyingloansenteredintoonorbefore 31 December 2022.

The EDB will release further details of the change by May 2017.

Extending and refining the Aircraft Leasing Scheme

15Singapore Budget 2017 Synopsis

Business tax

Points of view ► The extension of the ALS is welcomed,

especially in view of the competition from other jurisdictions to attract aircraft lessors (e.g., Ireland and Hong Kong).

► Theenhancementfor(b)simplifiestheadministrative burden of approved aircraft lessors in that they no longer need to segregate incomefromtheprovisionoffinanceintheacquisitionofanyaircraftoraircraftenginetonon-airline companies to bring it to tax at the prevailing corporate tax rate.

► Currently, many approved aircraft lessors do not have to pay any current taxes as the amount of capital allowances that they can claim on the costofacquisitionoftheiraircraftismorethanthe aircraft leasing income. The streamlining of theconcessionarytaxratefrom5%and10%toasinglerateof8%isthereforeunlikelytohavean adverse impact on the current tax liabilities of approved aircraft lessors.

► The ALS is subject to the approved aircraft leasing companies meeting certain conditions. Currently, approved aircraft lessors that are grantedtheconcessionarytaxrateof5%aresubject to more extensive conditions than those that are granted the concessionary tax rate of 10%. It remains to be seen whether theconditionstobemettoqualifyfortheconcessionarytaxrateof8%willbemoderateddownwards from the set of more extensive conditions.

► In January this year, Hong Kong announced a proposed dedicated tax regime to attract companies to domicile their aircraft leasing business in Hong Kong. Under this proposed dedicated tax regime:

► Qualifyingaircraftlessorsandqualifyingaircraft leasing managers will be taxed at 8.25%(i.e.,50%ofthecurrentHongKongprofitstaxrateof16.5%)ontheirqualifyingprofitsderivedfromleasingofaircrafttonon-Hong Kong aircraft operators.

► The8.25%taxratewillbeappliedondeemedtaxable amount of rentals calculated at 20% of net rentals (i.e., gross rentals less deductible expenses, but excluding depreciation), thus resultinginaneffectivetaxrateof1.65% (i.e.,20%x8.25%).

► The Hong Kong dedicated tax regime, unlike the ALS, does not cover onshore leasing and aircraft engine leasing. In addition, an approved aircraft lessors under the ALS is not likely to pay any current taxes as a result of claiming capital allowancesonthecostoftheaircraftacquired.The scope for aircraft lessors to not pay any current taxes in Hong Kong is, however, limited. However, unlike Singapore, the effective deemed deduction feature of the proposed dedicated tax regime in Hong Kong (in lieu of tax depreciation on the aircraft) will not result in a recapture of tax depreciation upon the disposal of the aircraft and may as such accord more certainty to aircraft lessors.

► To accord similar level of certainty and make the ALS more attractive, we hope the government canconsidertorefinetheschemefurther such that any recapture of tax depreciation (i.e., balancing charge) claimed under the incentive will be subject to tax at the concessionary tax rate even if the recapture occurs after the tax incentive period expires.

16 Singapore Budget 2017 Synopsis

Business tax

CurrentThe withholding tax (WHT) exemption on payments for international telecommunications submarine cable capacity under an Indefeasible Rights of Use (IRU) agreement was introduced to encourage telecommunications operators to provide international connectivity.

The scheme is scheduled to lapse after 27February2018.

ProposedIn line with the government’s thrust to grow the digital economy and continue to build Singapore intoakeyhubfordataflow,theWHTexemptionon payments for international telecommunications submarine cable capacity under an IRU agreement will be extended until 31 December 2023.

Extending the withholding tax exemption on payments for international telecommunications submarine cable capacity under an Indefeasible Rights of Use agreement

Points of view ► TheaboveWHTexemptionwasfirstintroducedin2003andhasbeenextendedeveryfiveyearssince then.

► The extension of the WHT exemption is in line with the government’s initiative to keep Singapore competitive in the digital and telecommunications sector. It is a welcomed move on the part of the government to announce the proposed extension well in advance of the reviewdateof27February2018.Itassuresbusinesses of the continued government support for the sector.

► Writing down allowance (WDA) is currently available under section 19D of the ITA on the capitalexpenditureincurredontheacquisitionofan IRU of any international telecommunications submarine cable system. The WDA is scheduled to lapse by 31 December 2020. Although the WDA under section 19D and the WHT exemption were both introduced at the same time in Budget 2003, they are not scheduled for review or renewal at the same time.

► The current WHT exemption applies to a contract for IRU, which takes effect or is renewed on or before27February2018.Similarly,weexpectthe proposed extension to also apply to IRU contracts that take effect or are renewed at any time on or before 31 December 2023.

17Singapore Budget 2017 Synopsis

Business tax

CurrentTheFinanceandTreasuryCentre(FTC)Schemegrants concessionary tax rate of eight percent on qualifyingincomederivedbyanapprovedFTCfromcarryingoutqualifyingactivitiesonitsownaccountorprovidingqualifyingservicestoapprovedofficesor associated companies (hereinafter referred to as “approved network companies”).

Toqualifyfortheconcessionarytaxrate,theFTCmustobtainfundsfromqualifyingsourcessuchasfinancialinstitutionsinSingapore,banksoutsideSingapore and approved network companies.

Withholding tax exemption under section 13(4) of the ITA is also granted, subject to conditions, on prescribedpaymentsmadebytheapprovedFTCtoqualifyingnon-residents(includingapprovednetworkcompaniesoftheFTC).

ProposedThequalifyingcounterpartiesforcertaintransactionsofapprovedFTCswillbestreamlined.This will help to ease the compliance burden of approvedFTCs.

The change will apply to new or renewal incentive awardsapprovedonorafter21February2017.

The EDB will release further details of the change by May 2017.

Refining the Finance and Treasury Centre Scheme

Points of view ► There are no details provided on the extent of the streamliningofthequalifyingcounterpartiesforcertaintransactionsofapprovedFTCs.

► Currently,toqualifyfortheconcessionarytax rate and the withholding tax exemption, approvedFTCsarerequiredtocarryoutqualifyingactivitiesorqualifyingservicesusingfundsobtainedfromqualifyingsources.Trackingthe sources of funds and the usage of the funds isasignificantadministrativechallenge.

► Qualifying sources are funds obtained by an approvedFTCfrom:

► FinancialinstitutionsinSingapore.

► Its paid-up capital.

► Itsaccumulatedprofitsderivedfromqualifyingactivitiesandqualifyingservices.

► Approved network companies of the approved FTC,providedthefundsareobtainedbythemfromqualifyingsources.

► The issuance of any bond, note, debenture or otherdebtsecurity,whichisnotbeneficiallyheld or funded, directly or indirectly, at any timeduringthelifeoftheissuebyanyofficeorassociatedcompanyoftheapprovedFTC,which is not an approved network company.

► Banks outside Singapore.

► Non-bankfinancialinstitutionsoutsideSingapore,whicharenotitsofficesorassociated companies.

18 Singapore Budget 2017 Synopsis

Business tax

► Where the funds are obtained by the approved FTCindirectlyfromanapprovednetworkcompany, all of the following conditions must befulfilled:

► All parties involved in the arrangement must be approved network companies of the approvedFTC.

► The approved network company must have bonafideoperations.

► The approved network company must not be a company incorporated or branch registered in Singapore.

► Thereisabonafidecommercialreasonto flowthefundsthroughmultipleapprovednetwork companies.

► Inaddition,theapprovedFTCmustbeabletotrack the funds through all the intermediate approved network companies to the ultimate qualifyingsourceofthefundsandisexpectedtomaintain proper documentation to substantiate to the Comptroller that the funds obtained directly or indirectly from the approved network companiesoriginatefromqualifyingsources.In the absence of such documentation, the Comptroller reserves the right to tax the income arising at the prevailing corporate tax rate.

► Thisposesasignificantadministrativechallengeto ensure that the sources of funds obtained byanapprovedFTCarequalifying,particularlywhere funds are fungible and may be co-mingled in terms of its usage in scenarios where anapprovedFTChastransactionswithbothapproved network companies and non-approved network companies. In the event the approved FTCobtainedfundsindirectlyfromapprovednetworkcompanies,whichcouldflowthroughmultiple chains of entities, this administrative challenge is further exacerbated.

► Itishopedthatthestreamliningofqualifyingcounterparties will remove the need for tracing of fundstoitsultimatequalifyingsourcesandhenceeasethecomplianceburdenoftheapprovedFTC.

► It is noted that the changes will only apply to new or renewal incentive awards approved on or after21February2017.Hence,theproposedstreamliningofcounterpartieswillnotbenefittheexistingapprovedFTCs.

► Given that the proposed streamlining of counterparties is to ease the administrative burdenofapprovedFTCs,itwillbegoodfortherefinementtoalsoapplytonewtransactionsenteredintobyexistingapprovedFTCsonorafter21February2017.

19Singapore Budget 2017 Synopsis

Business tax

CurrentThe package of tax incentive schemes for project andinfrastructurefinanceincludes:

a) Exemptionofqualifyingincomefromqualifyingproject debt securities (QPDS).

b) Exemptionofqualifyingincomefromqualifyinginfrastructure projects or assets received by approved entities listed on the Singapore Exchange (SGX).

c) Concessionarytaxrateof10%onqualifyingincome derived by an approved infrastructure trustee manager or fund management companyfrommanagingqualifyingSGX-listedbusiness trusts or infrastructure funds in relationtoqualifyinginfrastructureprojects or assets.

d) Remission of stamp duty payable on the instrumentoftransferrelatingtoqualifyinginfrastructureprojectsorassetstoqualifyingentities listed, or to be listed, on the SGX.

The scheme is scheduled to lapse after 31 March 2017.

ProposedWith the exception of the stamp duty remission, the existing package of tax incentive schemes for projectandinfrastructurefinancewillbeextendeduntil 31 December 2022.

The stamp duty remission will be allowed to lapse after 31 March 2017.

All other conditions of the schemes remain the same.

The MAS will release further details of the extension by May 2017.

Extending the tax incentives schemes for project and infrastructure finance

Points of view ► Infrastructure development in the emerging

markets remains a key focus area for governments in Asia. With economic uncertainties and global economic slowdown, governments need to ensure that sustained growth in infrastructure continues in the next 10to15years.Therefore,relyingsolelyonbank lending and government funding for infrastructureprojectsmaynotbesufficient.Singapore,asaregionalfinancialcentre,iswellplaced to position itself in the capital markets to facilitate and promote alternative sources of funding.

► The extension of the tax exemption on qualifyingincomefromQPDSisexpectedtofurther promote the attractiveness of non-bank infrastructurefinancingforinvestorsseekingalternatives for long-term investments in infrastructure-related projects in Asia.

► This is the second time that the tax incentive schemesforprojectandinfrastructurefinancehave been extended, signalling Singapore’s intention to continue its growth and momentum asahubforholding,developingandfinancinginfrastructure projects or assets in Asian emerging markets.

► With the discontinuance of the stamp duty remission for real estate investment trusts in 2015,thestampdutyremissionfortransfersrelatingtoqualifyinginfrastructureprojectsorassets has similarly been allowed to lapse.

20 Singapore Budget 2017 Synopsis

Business tax

CurrentThe Integrated Investment Allowance (IIA) Scheme was introduced to keep pace with the evolving business environment. The scheme grants a qualifyingcompanyanadditionalallowanceinrespectofthefixedcapitalexpenditureincurred onqualifyingproductiveequipmentplacedwith an overseas company for an approved project.

Forthepurposeofthescheme,oneofthequalifyingrequirementsisthatthequalifyingproductiveequipmenthastobeusedbytheoverseas company solely to manufacture productsforthequalifyingcompanyunder the approved project.

The EDB administers the scheme.

The IIA Scheme is scheduled to lapse after 28February2017.

ProposedThe IIA Scheme will be extended until 31 December 2022.Also,thequalifyingproductiveequipmentmay be used by the overseas company primarily to manufactureproductsforthequalifyingcompanyunder an approved project.

Theaboveliberalisationinthequalifyingrequirementwillapplytoexpenditureincurredonaqualifyingproductiveequipmentforaprojectapprovedonorafter21February2017.

Extending and refining the Integrated Investment Allowance Scheme

Points of view ► TheIIASchemewasfirstintroducedin2012.Theextensionoftheschemesignifiesthegovernment’s continued support for local companies to globalise and venture overseas.

► The liberalisation of the IIA Scheme to extend to qualifyingproductiveequipmentusedprimarilyfor the approved project is a pro-business move.

► The proposed enhancement raises the following practicalquestions:

► Whatisthedefinitionoftheterm“primarily”?

► WilltheEDBrequirethetaxpayertoidentifyandtrackusageoftheproductiveequipmentfor the approved project over the useful life of theequipment?

► Iftheproductiveequipmentisnotusedsolelyto manufacture products under an approved project,willthisaffectthequantumofinvestmentallowancegrantedbytheEDB?

21Singapore Budget 2017 Synopsis

Business tax

CurrentCurrently, withholding tax (WHT) exemption is allowed on payments made to non-resident non-individuals for structured products offered by financialinstitutionsforcontractsthattakeeffect,arerenewedorextendedduringthequalifyingperiod from 1 January 2007 to 31 March 2017, subject to conditions.

ProposedTocontinuepromotingSingaporeasafinancialhub,thequalifyingperiodfortheWHTexemptionon payments made to non-resident non-individuals for structured products will be extended until 31 March 2021.

All other conditions of the scheme remain the same.

Points of view ► This extension is in line with the government’s

continual effort to encourage further growth in the derivatives market and to strengthen Singapore’spositionasaleadingfinancialcentrein Asia.

► The extension of the WHT exemption will reduce the administrative burden and compliance costs incurredbyfinancialinstitutionsinconnectionwiththeSingaporeWHTrequirements.

Extending the withholding tax exemption on payments made to non-resident non-individuals for structured products offered by financial institutions

► The above WHT exemption is extended by four yearsinsteadofthetypicalfiveyears.Itislikelythat the expiry date on 31 March 2021 is to coincide with that of the WHT exemption on payments falling under section 12(6) of the ITAmadetonon-residentsbybanks,financecompanies and certain approved entities. This is in line with the government’s intention to simplify and consolidate the WHT exemption regime forfinancialinstitutions.

22 Singapore Budget 2017 Synopsis

Business tax

CurrentA250%taxdeductionisgrantedondonationof computers (including computer software and peripherals) by any company to an Institution of Public Character (IPC), or prescribed educational, research or other institution in Singapore.

ProposedAs the objective of the scheme has been achieved, the scheme will be withdrawn after 20February2017.

Withdrawing the tax deduction for computer donation scheme

Points of view ► Thisconcessionwasintroducedin1989to

allow companies to enjoy a tax deduction fordonatingcomputerequipmentandperipherals to prescribed educational and research institutions to help upgrade the qualityoftrainingininformationtechnologyinSingapore. The concession took effect from the YA1990.In2005,thiswasextendedtoincludedonations made to an IPC.

► As the population becomes more tech savvy and computerequipmentandsoftwarearecommonlyused by IPCs, and educational and research institutions, the objective of the scheme to upgrade the information technology knowledge in Singapore appears to have been met.

► To keep up with the rapid rate of change in technological advancements, any organisation, including educational and research institution andIPCs,willfindthatcomputerequipmentbecomesobsoleteveryquickly.Inaddition,thecost of a computer is generally more affordable and more easily available to educational, research institutions and IPCs. Such institutions willfindthatdonatedequipmentmaynotfullyserve their purposes and it is essential for them todeterminewhatequipmentandsoftwarewillmeet their needs to stay relevant, current and connected.

► It is therefore timely for the concession to be withdrawn now.

23Singapore Budget 2017 Synopsis

Business tax

CurrentCapitalexpenditureincurredforcertified energy-efficientandenergy-savingequipment mayqualifyforanacceleratedwritingdownperiodof one year under section 19A(6) of the ITA.

ProposedOver the years, new incentives, such as the InvestmentAllowance—EnergyEfficiencySchemeand the Productivity Grant — were introduced to promoteenergyefficiency.

To streamline incentives that promote energy efficiency,theAcceleratedDepreciationAllowanceforEnergyEfficientEquipmentandTechnology(ADA-EEET) Scheme introduced in 1996 will be withdrawn after 31 December 2017. No ADA-EEET willbegrantedforequipmentinstalledonorafter 1January2018.

Points of view ► Inefficientequipmentgenerallyconsumesmore

energy, resulting in higher operating costs being incurred and causing harm to the environment due to emission of pollutants. Administered by the National Environment Agency, the ADA-EEETwasoneofthefirstfewinitiativesintroduced by the government to promote energyefficiencybyencouragingcompanies toreplaceold,energy-consumingequipmentwithmoreenergy-efficientonesandtoinvest inenergy-savingequipment.

Withdrawing the Accelerated Depreciation Allowance for Energy Efficient Equipment and Technology Scheme

► To-date, an array of programs and incentive schemes aimed to promote and facilitate energy efficiencyinSingaporehasbeenintroducedinline with the Sustainable Singapore Blueprint. These include cash grants, co-fundings and investment allowances, which offer additional taxsavingstoqualifyingtaxpayers.

► The ADA-EEET, on the other hand, only offers a cashflowadvantageforqualifyingtaxpayersbyallowing them to claim accelerated depreciation forapprovedequipmentoveroneyearinsteadof three years. The proposed withdrawal of the ADA-EEET is therefore not anticipated to have a significantimpactonbusinesses.

24 Singapore Budget 2017 Synopsis

Business tax

CurrentAn approved media and digital entertainment (MDE) company or partnership is allowed to claim writing-down allowances (WDA) over a period of two years for capital expenditure incurred in respect of intellectual property rights (IPR) pertainingtofilms,televisionprogrammes,digital animation or games, or other MDE content acquiredforuseinitsbusiness.

The accelerated WDA for the MDE content scheme isscheduledtolapseinrespectofIPRsacquiredforMDE content after the last day of the basis period forYA2018.

ProposedAs the scheme is assessed to be no longer relevant and to simplify our tax regime, the accelerated WDA for the MDE content scheme will be allowed to lapse,inrespectofIPRsacquiredforMDEcontentafterthelastdayofthebasisperiodforYA2018.

MDE companies or partnerships may elect to claim WDAoverawriting-downperiodof5,10or15yearsonthecapitalexpenditureincurredtoacquirethequalifyingIPRs1 under section 19B of the ITA.

Allowing the accelerated writing-down allowances for acquisition of intellectual property rights for media and digital entertainment content scheme to lapse

Points of view ► The accelerated WDA for the MDE content

scheme was introduced in Budget 2009 to allow approved MDE companies to accelerate the writing-down period for MDE content.

► The withdrawal of the accelerated WDA for the MDE content scheme may have an impact on the cash tax payable for MDE companies as WDA for their IPRs will now be claimed over a longer periodoftime(5,10or15years)insteadof over a period of two years.

► In view of the above, MDE companies intending to acquireIPRsshouldplantomaketheacquisitionfor MDE content on or before the last day of the basisperiodforYA2018toqualifyfortheaboveaccelerated two-year claim period before the scheme lapses.

► On the other hand, a longer writing-down period for IPR may allow MDE companies with foreign taxcredittomaximisethebenefitoftheforeigntax credit claim, which could otherwise be limited if a shorter writing-down period results in little or no Singapore tax payable.

► The option of a longer writing-down period will also minimise the risk of forfeiture of unabsorbed WDA if there is a substantial change in the shareholders of the company.

► Since PIC could not be claimed on IPRs of approved MDEs, which is claimed over two years, MDEs may already have opted for WDA over the 5,10or15yearsinsteadoftheaccelerated two-year claim period.

1 ThequalifyingIPRsundersection19BoftheITAarepatents,trademarks,registereddesigns,copyrights,geographicalindications,lay-outdesigns of integrated circuits, trade secret or information that has commercial value, and plant varieties, but exclude IPRs specified under section 19B(11A) of the ITA.

25Singapore Budget 2017 Synopsis

Business tax

CurrentThe International Arbitration Tax Incentive (IArb) was introduced to encourage the provision of international arbitration services and attract overseas law practices to set up international arbitration services in Singapore. The incentive grantsapprovedlawpractices50%taxexemptiononqualifyingincrementalincomederivedfromthe provision of legal services in connection with international arbitration. Law practice means a Singaporelawpractice,foreignlawpractice,FormalLaw Alliance or Joint Law Venture. The maximum taxreliefperiodisfiveyears.TheIArbisscheduledto lapse after 30 June 2017.

ProposedOver the past decade, Singapore has grown as an international arbitration hub. As part of the government’s regular review of tax incentives, the IArb will be allowed to lapse after 30 June 2017.

The government will continue to develop and strengthen our arbitration landscape by:

► Strengthening our legislative framework.

► Expanding Maxwell Chambers, our integrated dispute resolution complex.

► Supporting local dispute resolution institutions and top international institutions seeking to base in Singapore or use Singapore as a venue for arbitration activities.

Allowing the International Arbitration Tax Incentive to lapse

Points of view ► The IArb was introduced to boost international

arbitration held in Singapore. Since the IArb was introduced in 2007, Singapore has developed as an international arbitration hub and experienced remarkable growth in the number of international arbitrationcasesheardinSingapore.In2015,as noted by the Ministry of Law, Singapore was ranked as the number one seat of International Chamber of Commerce Arbitration in Asia and fourth most preferred seat of arbitration in the world.

► Internationallawfirmshavealsotakennoteofthese developments and found Singapore an attractive location to build their bases.

► As the IArb has served its purpose to grow the international arbitration services in Singapore, it is allowed to lapse. There are other measures that can be taken in place to further strengthen Singapore’s arbitration landscape.

► Forinternationallawpracticesthatarekeen to do more international legal services work fromSingaporeandtosetupofficesinSingapore, there is still an applicable tax incentive scheme under the Development and Expansion Incentive (DEI).

► The DEI for International Legal Services (DEI-Legal) scheme provides for a 10% concessionary tax rate on incremental income derived from the provision of international legalservicesforfiveyears.Internationallegalservicesmeansanyqualifyingactivitycomprisinglegalservicesthatqualifyforzero-ratingundersection 21(3) of the GST Act. This scheme was introduced in 2010 and has been extended until31March2020inBudget2015.

26 Singapore Budget 2017 Synopsis

© 2

017

EYG

M L

imite

d. A

ll R

ight

s Re

serv

ed. E

D N

one.

If we buy abroad but 3D print at home, will there be indirect tax to pay?Find out how EY tax professionals can help buyers, vendors and governments navigate complexity.ey.com/tax #BetterQuestions

Personal income tax

Pers

onal

inco

me

tax

28 Singapore Budget 2017 Synopsis

Personal income tax

Personal income tax rebate and tax rate

Current The income tax rates for Singapore tax resident individualswitheffectfromYA2017rangefromzeropercentforthefirstS$20,000ofchargeableincome to 22% for chargeable income exceeding S$320,000. There was no income tax rebate accordedforYA2016.

ProposedThe government has announced that a personal income tax rebate of 20% of tax payable, capped atS$500pertaxpayer,willbegrantedtoalltaxresidentindividualtaxpayersforYA2017.There are no further changes to the income tax rates.

2 Active national service reservist man married to a non-working spouse with two dependent children

Points of view ► The income tax rebate announced in the Budget2017willbenefittaxresidentindividualtaxpayers who earn an annual income of more thanS$42,500.Taxresidentindividualtaxpayerswho earn an annual income of at least S$97,7602

willenjoythemaximumrebateofS$500.

► Personal income rebates have been given in the past and have ranged from S$1,000 to S$2,000. ThelastrebatewasgiveninYA2015,whichwas50%oftaxpayable,cappedatS$1,000.TherebateofS$500isthelowestsuchrebategivenin recent years.

► The new personal income tax rate structure announcedinBudget2015willapplywitheffectfromthisYAforalltaxresidentindividualtaxpayers. As such, there was no expectation of any change to these tax rates. In the past, tax rebates were given as a temporary measure to ease tax burdens rather than changing the tax rate structure. Although a tax rebate is not expected to be given with a new tax rate table, the announcement of a tax rebate is welcomed with the continuing challenges of a slowing economy and job security concerns as this will ease the tax burden of all tax resident individual taxpayers, especially those impacted by the increased tax rates under the new personal income tax rate structure.

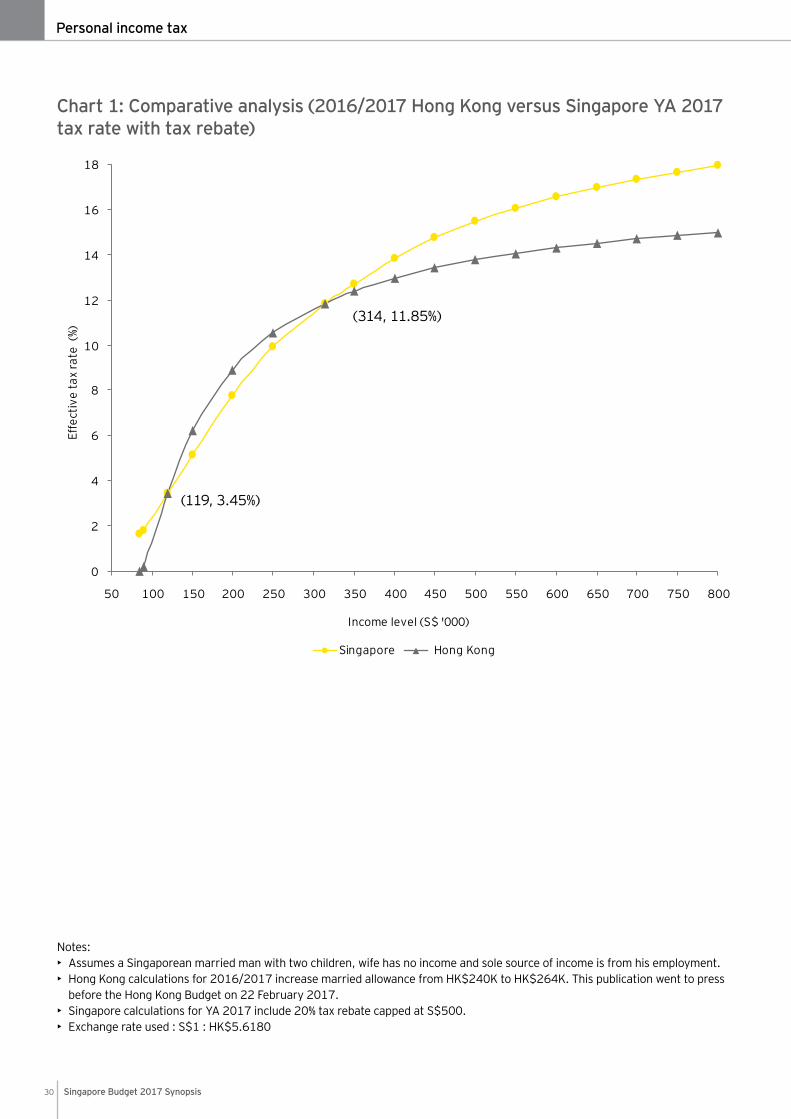

► Despite the introduction of higher tax rates for those earning more than S$160,000 under the new personal income tax rate structure, the Singapore tax regime remains one of the most competitive in the region, with its closest competitor being Hong Kong. Please refer to Chart 1. Currently, an individual earning income between S$119,000 and S$314,000 pays lower tax in Singapore, although very highly paid individualsmaynowpaysignificantlymoretaxinSingapore compared to Hong Kong.

In challenging times, it is reassuring that the government has not made immediate changes to raise income tax and GST. At the same time, the stage is set for impending changes over the next few years, which arerequiredtofundthevariousinitiatives for Singapore’s next phase of growth.“

“

29Singapore Budget 2017 Synopsis

Personal income tax

Chart 1: Comparative analysis (2016/2017 Hong Kong versus Singapore YA 2017 tax rate with tax rebate)

Notes:• Assumes a Singaporean married man with two children, wife has no income and sole source of income is from his employment.• Hong Kong calculations for 2016/2017 increase married allowance from HK$240K to HK$264K. This publication went to press

beforetheHongKongBudgeton22February2017.• SingaporecalculationsforYA2017include20%taxrebatecappedatS$500.• Exchangerateused:S$1:HK$5.6180

Singapore Hong Kong

0

2

4

6

8

10

12

14

16

18

50 100 150 200 250 300 350 400 450 500 550 600 650 700 750 800

Income level (S$ '000)

Effe

ctiv

e ta

x ra

te (

%)

(119,3.45%)

(314,11.85%)

30 Singapore Budget 2017 Synopsis

Personal income tax

Personal income tax rates in selected countries in the region

Note:The above rates are the top marginal personal income tax rates prevailing as at December 2016*Excludes local inhabitant tax

17

22

25

28

30

30

32

35

35

38

45*

45

45

45

0 10 20 30 40 50

Hong Kong

Singapore

Myanmar

Malaysia

Indonesia

India

Philippines

Vietnam

Thailand

Korea

Japan

Taiwan

China

Australia

Country

%

31Singapore Budget 2017 Synopsis

Goods and services tax

Good

s an

d se

rvic

es ta

x

Singapore Budget 2017 Synopsis32

Goods and services tax

Current The Minister has mentioned in his Budget speech that “with increasing digital transactions and cross-border trade, some countries have taken steps to adjust their GST system, to ensure a level playing fieldbetweentheirlocalbusinesses,whichareGST-registered, and foreign-based ones, which are not. We are studying how we can do likewise”. It is timely to take stock of the GST/VAT3 developments around the world and consider whether it is time for Singapore to impose GST on the digital economy.

On5October2015,theOECDreleaseditsfinalrecommendationsontheBaseErosionandProfitShifting (BEPS) Project. Among the actions recommended,Action1specificallyaddressesthe tax challenges of the digital economy. It is recognised that the evolution of technology has dramatically increased the ability of private consumers to shop online and the ability of businesses to sell to consumers around the world without the need to be present physically or otherwise in the consumer’s country. This has an adverse impact on a country’s GST/VAT revenue collection and puts GST-registered resident suppliers at a disadvantage. Recommendations were put forth inthefinalreportforAction1toaddressthese GST/VAT challenges.

Imposing GST on the digital economy

What are the issues in Singapore context?

Singapore has generally adopted a pragmatic and pro-business approach in the design of its GST system. This approach helps to reduce the GST compliance costs of taxpayers and are welcomed by taxpayers. However, this approach has also resulted in tax leakages brought forth by the digitaleconomy.Morespecifically,Singaporecurrently does not levy GST on the following online transactions:

► Supplies of services (e.g., downloadable software, e-book, music) by overseas online suppliers to Singapore businesses or consumers. These services are considered as made outside Singapore and do not fall within the scope of the SingaporeGSTregime.Furthermore,thereisnorequirementforbusinessesinSingaporetoself-accountforGSTontheacquisitionofservicesfrom overseas suppliers as the reverse charge mechanism is currently not operative in Singapore.

► Sales of low value goods (e.g., sale of fashion items through online stores) by overseas suppliers to Singapore consumers where such goods are imported by post or by air into Singapore and the import value falls below the GST import exemption threshold of S$400.

3 GST is known in some countries as VAT

In deciding whether or not to impose GST on the digital economy, the government will have to evaluate the amount of tax revenue tobecollected,theneedtoleveltheplayingfieldbetweenSingapore suppliers and overseas online suppliers and the ease of implementing and administering any new GST rules.““

Singapore Budget 2017 Synopsis 33

Goods and services tax

What are the actions taken by other countries?

Most developed economies operate a “reverse charge” mechanism. Reverse charge is a GST collection mechanism whereby domestic businesses (usually applies only to GST registered businesses) step into the shoes of the overseas service providers and account for GST on the supplies of services from the overseas service providers. At the same time, the domestic businesses would be allowed to claim the “GST incurred” as their input tax credits. If the domestic business is entitled to claim the input tax credit in full, the tax authorities will effectively collectzeroGSTrevenuefromthetransactionastheself-imposition of the GST would essentially be offset by the same amount of input tax credits.

Actions taken by other countries to address the supply of services by overseas online suppliers to local consumers were only implemented in recent years. On 1 July 2011, Norway implemented new rules to tax the digital economy. Under the new rules, overseas suppliers who sell digital goods andservicestoconsumersinNorwayarerequiredto register for VAT in Norway and charge VAT on their online sales to Norwegian consumers. The VAT collected is then remitted to the Norwegian authoritiesthroughthefilingofasimplifiedVATreturn. The VAT registration process for the overseasonlinesuppliershavebeensimplifiedtoencourage compliance.

Similar actions have been taken by the European Union,SouthKorea,JapanandNewZealandon1January2015,1July2015,1October2015and1October2016,respectively,whichrequireoverseas online suppliers to register for VAT/GST in these countries and remit the VAT/GST collected on their online sales to domestic consumers. To encourage compliance by the overseas online suppliers,simplifiedcompliancerulessuchassimplifiedonlineVAT/GSTregistration,simplifiedonline VAT/GST returns with no input tax credit and online payment arrangements were introduced. The European Union has gone a step further to implement a “Mini One Stop Shop”, which allows an online supplier to register for VAT only in one member country and remit the VAT collected from

the consumers in all the European Union member countries to the designated member country where the online supplier is VAT-registered. This approach relieves online suppliers from the need to apply for VATregistrationandfileVATreturnsinmultipleEuropean Union member countries. Australia has similarlyannouncedplanstorequireoverseasonline suppliers or electronic platform operators who supply digital goods and services to its domestic consumers to register for GST with effect from 1 July 2017.

Recommendation was also made under the OECD BEPS Project Action 1 to reduce or remove the VAT/GST import exemption for low value goods so that consumers will need to pay import GST when they receive goods purchased from overseas online suppliers. Currently, many countries have a low VAT/GST import exemption threshold of less than US$30.CountriessuchasAustralia,NewZealandand Singapore have a relatively high GST import exemptionthresholdofapproximatelyS$1,080,S$412 and S$400 respectively. Australia intends tointroducenewGSTrulesthatrequireoverseassuppliers, electronic platform operators or goods forwarders to register and account for GST on the supply of low value goods to its domestic consumers where the goods are imported into Australia.NewZealandisalsostudyingtheoptionof reducing its GST import relief threshold.

Should Singapore follow the footsteps of the other countries?

In deciding whether or not to tax the digital economy, we believe the following are some key considerations:

► The amount of tax revenue to be collected.

► The ease of implementing and administering the new rules.

► TheneedtoleveltheplayingfieldbetweenSingapore suppliers and overseas online suppliers.

Singapore Budget 2017 Synopsis34

Goods and services tax

Amount of tax revenue to be collectedAs most GST-registered businesses in Singapore are able to recover the full amount of GST incurred on their expenses, it is unlikely that the implementation of a reverse charge on online business transactions willyieldasignificantamountoftaxrevenue.Whilstthe IRAS may consider the implementation of reverse charge on a broader context, it is unlikely to do so solely to tax the digital economy.

ItwasreportedthatAustraliaandNewZealandexpect to collect an average of approximately AUD$175mandNZ$40mperyearrespectivelyfrom the implementation of new rules to tax digital products and services during the initial years. As theSingaporepopulationissignificantlysmallerthan the population in Australia, it is unlikely that Singapore will be able to collect as much additional GST revenue as Australia if we were to introduce new GST rules to tax the digital economy given our GST revenue base of approximately S$10b a year. The collection of additional tax revenue from the digital economy may not be a compelling reason for introducing new rules to tax the digital economy.

Ease of implementationEverychangeintheGSTruleswillrequire efforts from the tax authorities and the business community.

Comparing the various options to tax the digital economy, reducing the GST import exemption threshold of S$400 appears to involve the least changesasitdoesnotrequiretheintroductionofnew GST legislation and the system for collecting import GST is already in place.

Whilst the legislative framework for implementing reverse charge is currently in place, the implementation of reverse charge will inevitably requireadditionalcomplianceeffortsonthepart of businesses to change their systems and processes toaddressthisnewrequirement.

Lastly,theoptionofintroducingsimplifiedGSTregistration for overseas suppliers of digital goods andservicesislikelytobethemostdifficultmeasureamongtheoptions.Thismeasurewillrequiretheintroduction of new legislation, changes to the systems and processes of the IRAS and additional

compliance efforts on the part of the overseas online suppliers.

Leveling the playing field between Singapore suppliers and overseas online suppliersAnother motivation for taxing the digital economy istoensurelevelplayingfieldbetweenSingaporesuppliers and overseas online suppliers. The current GST rules in Singapore are not entirely “tax neutral” as it gives a price competitive edge to overseas online suppliers vis-a-vis our domestic GST-registeredsuppliers.Forinstance,adomesticGST-registeredsupplierwillberequiredtocharge7% GST on the sale of movie-on-demand services to Singapore consumers. On the other hand, an overseas online service provider is able to provide the same services to Singapore consumers free of Singapore GST as the overseas online service providerisnotrequiredtoregisterforGST in Singapore.

Based on the Budget speech given by the Minister, it would appear that this is one of the key considerations of the government in its decision to tax the digital economy.

ConclusionAs more countries take steps to tax the digital economy, it may become inevitable for Singapore to do so.

TheoptionofintroducingsimplifiedGSTregistration for overseas suppliers of digital goodsandserviceswillrequiretheintroductionofnew legislation, changes to the processes of the IRAS and compliance efforts on the part of the overseas online suppliers. Consultations with key stakeholders should be made to study the impact and effectiveness of the new measures before these measures are introduced.

On the other hand, as there is an existing framework for collecting GST on the importation of goods, reducing or removing the current GST import exemption threshold may be the starting point in moving towards the taxation of the digital economy.

Singapore Budget 2017 Synopsis 35

Goods and services tax

Prevailing standard GST/VAT rates in selected countries as at 1 January 2017

Note:(a) Until 30 September 2017, pending an extension of the period by the Thai government

Asia-Pacific

Europe

5

6

7 (a)

7

8

10

10

10

10

12

15

17

0 2 4 6 8 10 12 14 16 18

Taiwan

Malaysia

Thailand

Singapore

Japan

Vietnam

Korea

Indonesia

Australia

Philippines

New Zealand

China

%

Country

%

Country

8

19

20

20

21

22

25

25

0 5 10 15 20 25 30

Switzerland

Germany

France

UK

Netherlands

Italy

Sweden

Denmark

Singapore Budget 2017 Synopsis36

Goods and services tax

Withdrawing the GST Tourist Refund Scheme for tourists departing by international cruise

Current

Under the GST Tourist Refund Scheme (TRS), departing tourists may claim GST refunds on their goods purchased in Singapore from participating retailers, subject to the tourists’ eligibility and conditions of the GST TRS.

Since 21 January 2013, the GST TRS is also available to tourists who are departing from Singapore by international cruise (excluding cruise-to-nowhere, round-trip cruise and regional ferry) from the Marina Bay Cruise Centre Singapore and the International Passenger Terminal at Habourfront Centre (cruise terminals).

ProposedDue to the very low transaction volume at the cruise terminals for tourist refunds, the GST TRS will be withdrawn for tourists who are departing by international cruise from the cruise terminals and whose purchases are made on or after 1 July 2017. Tourists who are departing by international cruise from the cruise terminals will have until 31 August 2017 to claim refunds on purchases made before 1 July 2017. Thereafter, the e-TRS facilities at the cruise terminals will be removed.

Points of view ► The extension of the GST TRS in 2013

(announced in Budget 2012) to tourists departing by international cruise from the cruise terminals was intended to capitalise on the growth of international cruise tourism.

► Nevertheless, the proposed withdrawal of the GST TRS for tourists departing by international cruise from the cruise terminals should not have a major impact on our international cruise tourism given the low transaction volume at the cruise terminals for GST refunds.

Singapore Budget 2017 Synopsis 37

Miscellaneous

Misc

ella

neou

s

38 Singapore Budget 2017 Synopsis

Miscellaneous

Strengthening enterprises’ capabilities through scaling up globally

International Partnership FundTosupportSingapore-basedfirmstoscaleupandinternationalise, the government will set aside up toS$600mfortheInternationalPartnershipFund(IPF).Thefundwillco-investalongsideSingapore-basedfirmsinopportunitiesforscale-upandinternationalisation, with a focus on Asian markets. Such a joint investment will allow Singapore-based firmstopartnerotherpromisingAsiancompaniestoextend product lines, brands or value chains or gain access to markets, channels and technologies.

QualifyingfirmsshouldbeheadquarteredinSingapore with annual revenues of no higher thanS$800m.

TheIPFwillbemanagedbyHeliconiaCapitalManagement Pte. Ltd. (Heliconia)

Points of view ► Thisisawelcomeannouncementandreflectsafirmcommitmentbythegovernmenttocatalysethe expansion of Singapore-based companies’ footprint beyond Singapore.

► This announcement is consistent with the report recentlyreleasedbytheCommitteeontheFutureEconomy(CFE),whichidentifiessevenstrategiesto chart Singapore’s next phase of growth.

► TheCFErecommendedthatmore“smart and patient growth capital” is needed for Singapore-based enterprises to scale up. Thegovernment-fundedIPFprovidesoneimportant source of such capital and enhances thefinancingecosystem.

► The attractiveness of this scheme is enhanced by the ideas and expertise that would be brought to the table by the professional fund managers at Heliconia, a wholly owned subsidiary of Temasek Holdings.

► Adeparturefrompastschemes,theIPFisflexibleinpartneringwithfairlylargeSingapore-basedfirms,notjustSMEs,hencecastinga widernettohelpsuchfirmscompeteintheglobal arena.

► Together with the enhancements to the InternationalisationFinanceScheme,theIPF willfurtherbridgegapsinthefinancialmarketsfor Singapore-based companies to make strategic qualityoverseasinvestments.

The measures to deepen our partnerships internationally and enhance capabilities and international exposure will be widely appreciated. Given the diverse region Singapore is in and the growth opportunities ASEAN presents, fostering a close and deep understanding of the region is imperative.”“

39Singapore Budget 2017 Synopsis

Miscellaneous

Digitalisation and innovation

To keep Singapore relevant even as the world changes, ideas put forth by the Committee on the FutureEconomy(CFE)includedbroadstrategiesto deepen digital capabilities and build strong capabilities in innovation.

Enterprises are at the heart of vibrant economies. Forourenterprisestostaycompetitiveandgrow,therearecapabilitiesthatmanyfirmswillneedin common — being able to use digital technology and embracing innovation.

DigitalisationDigitaltechnologyhasuniquepotentialtotransform businesses, large and small, across theeconomy.Thefirstwaytostrengthenourenterprises, especially SMEs, is to help them adopt digital solutions.

SMEs Go Digital ProgrammeThe SMEs Go Digital Programme will be introduced to help SMEs build digital capabilities. The Info-communications Media Development Authority (IMDA) will work with SPRING and other sector lead agencies in this effort. The SMEs Go Digital Programme encompasses three components:

► Sectoral Industry Digital Plans on technologies to use at each stage of growth:

► The step-by-step advice will start with sectors where digital technology can significantlyimproveproductivity.