Since , 1937 TAX imp FOUNDATION TAX FEATURES · 2 National Conference Focuses on Marginal Tax Rates...

12

Sinc e , 1937 TAX imp , FOUNDATIO N TAX FEATURE S www.taxfoundation .org December 1999/January 2000 Volume 44, Number 1 Comparison of Tax Plans from Bush and McCai n Shows Great Similarities, Great Differences Bush and McC'ain's ta x plans differ most in their effect on elderly singl e filers at both ends of th e income spectrum. A Tax Foundation analysis of how the Bush an d McCain tax plans would affect taxpayers onc e the plans were fully effective in 2006 show s some similarities, and some striking differences . Both would provide significant tax relief to mil - lions of middle-class taxpayers, and both would increase the proportion of the total tax burde n paid by the taxpayers who earn the most . The great difference between the two plan s is that Senator McCain provides virtually no ne t tax relief to the lowest income married taxpay- ers, and effectively levies a large tax increase o n low-income single retirees . The source of thi s tax hike is the set of corporate tax break s McCain would eliminate . As is common practice, the Tax Foundatio n attributes the burden of corporate taxes, an d therefore corporate tax hikes, to the owners o f the companies . A recent study by the Federal Reserve Board showed that 48 .8 percent of fami- lies own stock and that the median value of thei r holdings is $25,000 . Many low-income elderl y taxpayers receive a large share of their livelihoo d from pensions and other saving they di d throughout their working lives . Much of thi s saving is invested in corporate equities, eithe r directly, through mutual funds, or through thei r pensions . Increasing corporate income taxe s reduces the value of these companies and re- duces the after-tax income received by the com- panies' owners . Said J .D . Foster, Executive Director an d Chief Economist of the Tax Foundation,"I' m sure Senator McCain didn't intend this, but hi s See Candidates on page 8 Figure 1 : Total Income Tax Relief for Single Filers b y Income Class in Tax Year 2006 Bush ® McCai n $20K- $30K- $40K- $50K- $75K- $100K- $200K- $500K- Ove r $20K $30K $40K $50K $75K $100K $200K $500K $1M $1 M Adjusted Gross Incom e Note : Totals don't add to one because taxpayers with zero AGI and heads of households are omitted . Source: Tax Foundation FRONT & CENTE R Inside: ♦ Annual Dinner, Conferenc e and Silent Auctio n ♦ Domenici on the Tax Cod e ♦ New Study of the Inlan d Waterway Excise Ta x ♦ Foster on Trade Policy ♦ Conference on March 9 The Federal Income Tax Law : A Code At War with Itsel f US. Senator Pete Domenici (1Z-NM) G-7

Transcript of Since , 1937 TAX imp FOUNDATION TAX FEATURES · 2 National Conference Focuses on Marginal Tax Rates...

Sinc e, 1937

TAX imp,FOUNDATION

TAX FEATURESwww.taxfoundation.org

December 1999/January 2000 Volume 44, Number 1

Comparison of Tax Plans from Bush and McCai nShows Great Similarities, Great Differences

Bush and McC'ain's taxplans differ most in theireffect on elderly singlefilers at both ends of theincome spectrum.

A Tax Foundation analysis of how the Bush an dMcCain tax plans would affect taxpayers onc e

the plans were fully effective in 2006 showssome similarities, and some striking differences .

Both would provide significant tax relief to mil -lions of middle-class taxpayers, and both would

increase the proportion of the total tax burdenpaid by the taxpayers who earn the most .

The great difference between the two plansis that Senator McCain provides virtually no ne t

tax relief to the lowest income married taxpay-ers, and effectively levies a large tax increase onlow-income single retirees . The source of thi s

tax hike is the set of corporate tax break s

McCain would eliminate .As is common practice, the Tax Foundatio n

attributes the burden of corporate taxes, andtherefore corporate tax hikes, to the owners of

the companies . A recent study by the FederalReserve Board showed that 48 .8 percent of fami-

lies own stock and that the median value of thei rholdings is $25,000 . Many low-income elderlytaxpayers receive a large share of their livelihoo d

from pensions and other saving they didthroughout their working lives . Much of this

saving is invested in corporate equities, eitherdirectly, through mutual funds, or through thei r

pensions . Increasing corporate income taxe sreduces the value of these companies and re-

duces the after-tax income received by the com-panies' owners .

Said J .D . Foster, Executive Director an dChief Economist of the Tax Foundation,"I' m

sure Senator McCain didn't intend this, but hi s

See Candidates on page 8

Figure 1 : Total Income Tax Relief for Single Filers b yIncome Class in Tax Year 2006

Bush

® McCai n

$20K- $30K- $40K- $50K- $75K- $100K- $200K- $500K- Ove r$20K $30K $40K $50K $75K $100K $200K $500K $1M $1 M

Adjusted Gross IncomeNote : Totals don't add to one because taxpayers with zero AGI and heads of households are omitted .

Source: Tax Foundation

FRONT & CENTER

Inside:♦ Annual Dinner, Conferenc e

and Silent Auctio n♦ Domenici on the Tax Code♦ New Study of the Inlan d

Waterway Excise Ta x♦ Foster on Trade Policy

♦ Conference on March 9

The Federal Income Tax Law: A CodeAt War with Itself

US. Senator Pete Domenici (1Z-NM)

G-7

2

National Conference Focuses on Marginal Tax RatesAt noon on November 18th, J .D . Foster,Ph .D., the Tax Foundation ' s Executive Di-rector and Chief Economist, welcomed thecrowd at the 62nd National Conferenceand introduced the keynote speaker, WayneStruble, Staff Director of the House Com-mittee on the Budget, who spoke on "Statu-tory vs . Effective Tax Rates—The Realityand How We Got There "

The first panel of speakers then too kthe stage to address "Marginal Tax Rates an d

Executive director and chief economist, Investment" Moderator J.T.Young, Ph .D . ,JD. Foster, Ph.D., introduces the theme,

Chief Economist/Budget &Tax Policy Ana -"Do Marginal Tax Rates Matter?" and

lyst with the Senate Republican Policythe speakers at the Tax Foundation's

Committee introduced panelists Stephen J .62nd National Conference.

Entin, Executive Director and Chief Econo-mist, Institute for Research on the Econom-ics of Taxation ; R . Glenn Hubbard, Ph .D . ,Russell Carson Professor of Economics an dFinance, Columbia University ; and Marg oThorning, Ph .D., Senior Vice President andChief Economist,American Council fo rCapital Formation .

After a break, the second panel wa sintroduced by moderator Peter M .Taylor,Ph .D., Senior Economist with the Join tCommittee on Taxation, to speak on "Incen-tives to Work/Incentives to Hire ."

The three panelists were Rober tCarroll, Ph .D ., Economist, Office of TaxAnalysis, Department of the Treasury ; DavidR . Malpass, Chief International Economistand Senior Managing Director, Bear Stearn s& Co ., Inc . ; and Jane G . Gravelle, Ph .D .,

Senior Specialist in Economic Policy, Con-gressional Research Service .

With Congressman Phil Crane (R-IL)scheduled to give the closing remarks, along series of roll call votes was held onthe floor of the House, preventing hi mfrom appearing in person . His remarkswere sent by courier, and J .D . Foster closedthe conference by reading them .

Several Tax Foundation donors madespecial contributions to sponsor th eFoundation's 62nd National Conference :Arthur Andersen LLP ; Baker & Hostetler,LLP ; Bell Atlantic Corporation; Caterpilla rInc . ; Citibank, N .A . ; Distilled Spirits Counci lof the United States ; Ernst & Young, LLP ;Exxon Corporation ; General Motors Corpo-ration; Georgia-Pacific Corporation ; House-hold International, Inc . ; Koch Industries ,Inc . ; KPMG Peat Marwick LLP; MetropolitanLife Insurance Company; Microsoft Corpo-ration; Miller & Chevalier, Chartered ;Northrop Grumman Corporation ; Mr. an dMrs . George A . Peterkin, Jr. ; Philip Morri sManagement Corp . ; Praxair, Inc . ;PricewaterhouseCoopers LLP; Mr. James Q .Riordan ; R.J. Reynolds Tobacco Company ;Sears, Roebuck and Co . ; 60 Plus Association ;Skadden,Arps, Slate, Meagher & Flom LLP ;Texaco Inc . ; John E . and Fran Thomson ;TRW Inc . ; UST Public Affairs Inc . ; USXCorporation ; Washington Counsel, PC . ; andthe Wine and Spirits Wholesalers o fAmerica. 0

Columbia University Professor Glen nHubbard is silhouetted against hischart of marginal tax rates.

At center, Tax Foundation co-chairman and former Director ofOMB Jim Miller talks with two college students who attended th econference thanks to the Foundation's College Classroom Project .

From left: Tony Saggese of Texaco, Mike DeLuca of HouseholdInternational, Catherine Porter of Miller & Chevalier, andDave Williams of BellSouth.

3

Tax Foundation Celebrates 62nd AnnualDinner While Honoring Kerrey and FeldsteinThe Tax Foundation celebrated its 62ndannual dinner on November 18, 1999, a tthe Four Seasons Hotel in Washington, DC .

Senator Bob Kerrey, recipient of theTax Foundation's DistinguishedService Award for the Public Sector.

Earlier in the day, the Foundation'sNational Conference revisited the im-portance of marginal tax rates (story o npage 2), and during a reception beforethe dinner, the Foundation held a silen tauction (sidebar on page 4) .

Each year the Tax Foundation hon-ors two people who have distinguishedthemselves in the field of tax policy,one from government and one from th eprivate sector. This year those tw opeople were United States Senator BobKerrey (D-NE) and Dr. Martin Feldstein ,President and CEO of the National Bu-reau of Economic Research (NBER) .

Senator Bob Kerrey's service on theFinance Committee has shown him tobe a man of unwavering principle .Widely respected on a bi-partisan basisfor his vision, Senator Kerrey brings totax policy a common-sense approachand a rare ability to work well with

Martin and Kate Feldstein at the TaxFoundation's annual dinner where Dr.Feldstein received the Foundation'sDistinguished Service Award ,for hisprivate sector contributions to taxpolicy as president of the National Bu-reau of Economic Research .

College Classroom Project Brings Students Together with Corporat eAnd Capitol Hill Tax Policy Community at National Conferenc eThanks to the Tax Foundation's Colleg eClassroom Project, students and profes-sors attended the Tax Foundation's 62ndNational Conference, "Do Marginal TaxRates Matter?" on November 18, 1999, atthe Four Seasons Hotel in Washington, DC .

The conference gave students theopportunity to meet business leaders ,well-known analysts, and other promi-nent policymakers who shape tax policy.

Donors who made earmarked con-tributions to sponsor students from al lover the east coast to come to Washing-ton were : The Air Products Foundation ;Bechtel Group, Inc . ; Cabot Oil & GasCorporation; Celanese Americas Corpo-ration; Chevron Corporation ; CoorsBrewing Company ; Johnson & Johnson ;PricewaterhouseCoopers LLP ; Tele-phone and Data Systems, Inc . ; Texac oInc . ; and Westvaco Corporation .

Please contact Jan Rogers(jrogers@taxfoundation .org) about be -coming a sponsor next year. 0

In the front row, Professor George Agbango (far left), Tax Foundation Executive Di-rector J.D. Foster (third from left) and Tax Foundation Co-Chairman Jim Miller (farright) are surrounded by ProfessorAgbango's students from Bloomsburg Universitywho camefrom Pennsylvania to Washington, DC for the Tax Foundations NationalConference. The Foundation's donors made special contributions to sponsor the tripas part of the annual College Classroom Project

4

Wayne Gable (right) and Rob Hall (center) of Koch Indus -tries chat with Senator Kerrey at the reception .

Members on both sides of the aisle .His co-chairmanship of the Bipartisan

Commission on Entitlement and Tax Re -form led to a final report, released in Janu -ary 1995, that is often cited as the defini-tive analysis of the nation's entitlementsystem .

His recent work as co-chairman ofthe National Commission on Restruc-turing the Internal Revenue Service hasestablished Kerrey as a national leade rin efforts to reform our nation's taxcollection system, enhance its effi-ciency, and increase protections agains ttaxpayer abuse .

Martin Feldstein is George E Bake rProfessor of Economics at Harvard Uni-versity, and NBER is a private, non-profi tresearch organization that has special -ized for more than 75 years in produc-ing nonpartisan studies of the Americaneconomy.

Dr. Feldstein had received the TaxFoundation Distinguished Service

Award for hi spublic secto raccomplishment sin 1983 during hi stenure as head o fPresident Reagan'sCouncil of Eco-nomic Advisors .His selection a srecipient of thePrivate Sectoraward for his 16years of work atNBER makes himthe only person towin both awards .

A graduate o fHarvard Collegeand Oxford University, Dr. Feldstein is aFellow of the Econometric Society an dthe National Association of Busines sEconomists .

Dr. Feldstein and Senator Kerre yjoined a long and distinguished list of

American business and political leaders .Two U .S . Presidents have been so

honored: Herbert Hoover in 1948 (for hi srole as head of the Commission on Organi-zation of the Executive Branch) an dDwight Eisenhower in 1960 . Numerou s

Silent Auction Added to Annual Dinner FestivitiesThe 62nd Annual Dinner was the firs tyear that the Foundation held a silentauction as part of the event . Guests par-ticipated by donating items in advanc eand coming prepared to bid on the won-derful items that others had donated .

The money raised from the auc-tioned items expands the Foundation' sresearch and educational programs at

the local, state and federal levels .The generous donors were

Brunswick Corporation ; Circuit City Foun-dation, Congressman Bill Archer ; Coor sBrewing Company ; Distilled Spirits Coun -cil of the United States ; Four SeasonsHotel; General Motors Corporation ; LawFirm of Herman B . Bouma; Hershey FoodsCorporation ; National Fruit Product Co . ;

Nestle USA : Northrop Grumman Corpora -tion; On the Border Mexican Café ; PhilipMorris Management Companies Inc . ;Philip Morris Management Corp . ; Saint-Gobain Corporation ; Sears, Roebuck an dCo . ; Southwest Airlines Co. ;TupperwareCorporation ; IJnited Parcel Service, Inc . ;UST Public Affairs Inc . ;Vinson & Elkin sLLP; and The Washington Redskins .

Y

At right, Mtn I1('rman of the Wall Street f) uX points I iz'd From left; Enjoying the silent auction are Richard Belas oGoldberg of skadden, Arps, Slate, Meagher & Flom to one

Davis Harman with Tim Tammany of CIGNA, and Barbara

of the gifts that Tax Foundation donors provided for the

Washburn and Bill Latinen of General Motors .silent auction while Mn and Mrs. George Peterkin look on .

5Secretaries of Treasury have been honored ,George Shultz (1974),William Simon(1975), and James Baker III (1985) . Someof the most notable congressional leader sto accept the Tax Foundation award includ eSenator Robert Taft (1949), Chairman of th eHouse Ways & Means Committee Wilbu rMills (1958, 1968), Senator Everett Dirkse n(1965), and the father-son team of Senato rHarry F Byrd (1941, 1955) and Senato rHarry F. Byrd, Jr. (1973) .

In addition, four chairmen of the Fed-

eral Reserve System have been honored b ythe Tax Foundation at its annual dinner :William McChesney Martin, Jr . (1961), PaulMcCracken (1971), Paul Volcker (1980), an dAlan Greenspan (1992) .

Many members of the private sectorhave also taken leadership positions inpromoting sound tax policies, thereb yearning the esteem of the Tax Foundation .AT&T Chairman Frederick Kappell (1967) ,GM Chairman Richard Gerstenberg(1972), and GE Chairman Reginald Jones

(1977) have been recognized at the an-nual dinner. In recent years, such distin-guished business leaders as Alcoa Chair -man Paul O'Neill (1991), Mobil Chairma nAlan Murray (1992) and Hewlett-Packar dChairman John Young (1994) have beenhonored for their contributions to th enational fiscal policy discussion . In 1996,the Tax Foundation chose to honor Dr .Norman Ture, long one of the nation' smost respected public policy analysts, an da driving force behind the 1981 tax cut . e

Smiles all around as Tax Foundation Co-Chairman Ji mMiller (right) and Executive Director JD. Foster (left) pre-sent Dr. Martin Feldstein his award.

Executive Director JD. Foster (right) presents Senator Bo bKerrey the Tax Foundation's award for Distinguished Ser-vice in the Public Sector.

Tax Foundation Distinguished Service Award WinnersSelected Years

1941 U .S. Senator Harry F. Byrd 1980 Fed Chairman Paul Volcker 1993 USX Chairman Charles A . Corr y1948 President Herbert C . Hoover 1981 Sec . of Defense Caspar W. Weinberger U .S . Rep . Sam M . Gibbon s1949 U .S . Senator Robert A . Taft 1982 U .S . Rep . James R . Jones 1994 Hewlett-Packard Chairman John Young1954 Sec . of Agriculture Ezra Taft Benson 1983 CEA Chairman Martin Feldstein U .S . Senator William Roth1956 White House Chief of Staff Sherman Adams 1985 Sec . of Treasury James A . Baker III 1995 Texaco Chairman Alfred C . DeCrane, Jr.1960 President Dwight D. Eisenhower 1987 U .S . Senator Daniel Patrick Moynihan U .S . Senator Sam Nun n1961 Fed Chairman William McChesney Martin, Jr . 1988 U.S . Rep . Bill Archer 1996 Dr. Norman Tur e1962 Gov. Nelson A. Rockefeller 1989 USX Chairman David Roderick U .S . Rep . Phil Cran e1965 U .S . Senator Everett M . Dirksen U .S. Senator Lloyd Bentsen 1997 GTE Chairman Charles R . Lee1968 U .S . Rep . Wilbur Mills 1990 Young & Co . Chairman William S . Kanaga U .S . Senator John Breau x1971 CEA Chairman Paul W. McCracken U .S . Senator Bob Packwood 1998 CSX Chairman John Snow1973 U .S . Senator Harry F. Byrd, Jr. 1991 Alcoa CEO Paul H . O'Neill U .S . Rep . Bill Arche r1974 Sec . of Treasury George P. Schultz U.S. Senator Max Baucus 1999 NBER President Dr. Martin Feldstei n1975 Sec . of Treasury William E . Simon 1992 Mobil Chairman Allen E . Murray U .S . Senator Bob Kerrey1976 U .S . Senator Russell B . Long Fed Chairman Alan Greenspan1977 GE Chairman Reginald H . Jones

6

The FederalIncome TaxLaw: AC~• • atWar with Itself

By U.S. Senator Pete Domenici (R-NM)

The federal income tax law is a code a twar with itself. It is a war between chap-ters and subchapters, titles and subtitles ,parts and subparts, sections and subsec-tions . The baffling complexity of thecode and the growing angst it fosters forfamilies and American businesses onlyunderscores the need for Congress t oreform the tax code . We simply cannotgo on with a tax code that, in the end, i sat war with American families .

The tax code is replete with inexpli-cable contradictions . The code, for ex-ample, provides a $500 child credit tohelp a family afford raising children . Atthe same time, it imposes an averag e$1,400 marriage penalty on the mothe rand father for getting married and stayingmarried while raising the supposed ben-eficiaries of the federal child tax credit .

Sixty-three provisions in the cod epenalize couples for being married, tw oof the most prominent being the stan-dard deduction and the tax bracket struc-ture . The dependent credit, the elderlycredit, the IRA deduction, and educationloan interest expense deductions arephased out based on income, and there-

Sixty-three provisions in the code penalize couplesfor being married, two of the most prominent beingthe standard deduction and the tax bracket structure .

fore, are marriage penalties for modestincome couples . In fact, Congress con-tributes to the marriage penalty everytime it enacts income phase-out provi-sions—some of which start as low as$10,000 of income .

The federal tax code diminishes aworking wife's contributions to he rfamily's finances by taxing her incom eat the highest rate imposed on herhusband's income. This is hard tojus-tify under any circumstances, but it isunconscionable when the federal gov-ernment is collecting record surpluse sfrom taxpayers .

The tax code war with itself is per-petuated by the Alternative Minimum Ta x(AMT), which Congress enacted to en -

Pete Domenici is a Republican United sure everyone pays their fair share . In-States Senator from New Mexico and

tended to affect only a few thousandthe chairman of the Senate Budget

taxpayers, it could penalize an estimate dCommittee .

33 million Americans by 2009 . More and

FRONT & CENTE R

more taxpayers are already experiencin gthe pain of the AMT, which could stan dfor the Awful Monstrosity of a Tax ."

Every tax credit Congress enactspushes more families into the AMT.Prior to enactment of last year's taxextenders bill, the AM I' was projectedby 2009 to force three in tour families toreceive less than the full HOPE educa-tion, child,or other tax credits . To ad-dress this tax code inconsistency, Con-gress passed a stopgap exemption t oprotect most families from the AMT. Butthis action begs the obvious : why notjust repeal the AMT, revenues fromwhich rose 39 .2 percent in 1997, th elargest increase since 1993? Or why no tenact a simple and fair tax system thatdoes not need an AMT ?

The tax code war against itself alsoextends into the various Individual Re-tirement Account (IRA) and pensionprovisions that encourage people to savefor retirement, first home purchases, andcollege educations, These "worthy pur-poses" provisions are battlegrounds i nthe conflict between the subsections . Ifthe rollover and distribution rules are no tstrictly followed, up to 70 percent of theretirement savings could be lost to taxes .

Americans are living and workinglonger, yet the war between the tax cod esections ignores this biological fact . Itpenalizes people for staying in the workforce . Taxable Social Security benefitshave increased each year since 1988 . It i sbad tax and Social Security policy torequire up to 85 percent of Social Secu-rity benefits to be included in taxableincome for some beneficiaries .

Our gift and estate taxes, with rate sranging from 18 to 55 percent, are an -other vicious front in the tax code war.Milton Friedman summed up the gift andestate tax when he said,"The estate ta xsends a bad message to savers, to wit :that it is O.K. to spend your money onwined women and song, but don't try t osave it for your kids : The moral absurdityof the tax is surpassed only by its eco-nomic irrationality." When the generationskipping tax is also triggered, the com-bined gift and estate tax rates can reach

7

80 percent . For this reason, the estat etax is often called the most confiscatorytax of all . It is one of the greatest bur-dens on our most successful small busi-nesses . It is a tax on job creation. TheHeritage Foundation found that over a 1 0year period, economic output wouldincrease 511 billion per year on average,and create 115,000 new jobs if the estat etax were repealed .

To arrive at good tax policy and findtax code peace, we need to ask the righ tquestions . Policy makers, news makersand others tend to start each tax debatewith the same questions: Who benefits ?What percentage of the benefit goes tothe top 1 percent or 5 percent? "

We cannot ignore that our currentcode is a progressive tax rate system .Under our progressive rate structure, anytax cut is going to give the biggest sav-ings to those who pay the largest taxbills . It is unavoidable that the bigges ttax cut goes to those who shoulder theheaviest tax burden . Asking the wrongquestion leads to the wrong tax policy.Let me repeat the tax burden facts .

According to 1997 IRS data, the to p10 percent of taxpayers shoulder 6 0percent of the federal income tax burden.'Iwo percent of taxpayers (thos ewith adjusted gross incomes of morethan $200,000) paid more than 37 per-cent of all federal income taxes. Thebottom 50 percent of taxpayers paid only5 percent . And 50 million Americans payno federal income tax at all .

The question of"who benefits? "shifts the focus to wealth redistributioninstead of wealth creation . It further sclass warfare instead of advancing goodeconomic and tax policy.

Tax revenues have grown by 7 . 6percent annually since 1992, nearly 250percent faster than the 2 .2 . percent an-nual rate of inflation . High federal taxe sseize nearly 40 percent of the wealthadded to the U .S . economy by America'smost productive individuals . When com-bined with state and local income taxes ,this represents government's power t ocontrol half of the additional incomeearned by entrepreneurs and other high-income taxpayers, dramatically reducingtheir incentives to build businesses an dcreate jobs .

Total taxable income and total in -come tax increased faster than AGI in

1997 . Net capital gains increased over40 percent for the second consecutiveyear, with $356.1 billion being realizedfor 1997 .

We should consider lowering thecapital gains rate. Some advocate lower-ing it to zero . I am not sure I would gothat far, but the capital gains tax is a ta x

on capital formation. It is a tax on risktaking, and it should be applied pru-dently so that our economy can functio nmore efficiently .

In conclusion, marriage, saving fo rretirement, risk taking, and dyin gshould not be taxable events as webegin the new century. The AMTshould not turn the child care, educa-tion, and foster care tax credits int oworthless and useless credits .

The price of civilization has becom edramatically more expensive since Jus-tice Oliver Wendell Holmes called taxe sthe price we pay for a civilized society .

American workers now work until Ma y11 every year just to pay their taxes . Thi sis the highest tax burden since WWII .People are paying more in taxes thanthey spend on food, shelter and educa-tion, pouring more revenue into th efederal coffers than is needed to fundcurrent government services . The taxburden is too high, and taxes should notbe collected for more government ser-vices that are not needed, wanted oreven created yet .

To end the tax code battle, we mustsimplify a code that is too complicated .There are 7 million words in the Federa lInternal Revenue Code and regulationsrelated to its 703 accompanying taxforms . When Money magazine asked 4 6professional tax preparers to calculate ahypothetical family's tax return, eachprofessional arrived at a different answer.

We need to move toward a simpler ,lower and flatter tax system . We need a taxsystem that moves toward taxing incom ethat is consumed and not income that i searned, saved and invested . We need a taxsystem that recognizes that not all familyspending is equal . It should appreciate th eimportance of investing in education .

We need tax equity so that everyon e

will get a tax break for health care regard -less of who they work for—a big com-pany, small business or one-man shop .

We need generational equity, includ-ing tax credits for child care as well a slong term care credits for the elderly.

Finally, and probably most impor-tantly, Americans need a tax cut .

The Mx Foundation invites a nationa lleader to provide a "Front and Center "column each month in Tax Features.The views expressed are not necessarilythose of the Mx Foundation .

We need a tax system that moves toward taxingincome that is consumed and not income that isearned saved and invested. We need a tax systemthat recognizes that not all family spending i sequal It should appreciate the importance ofinvesting in education.

8

Figure 2: Total Income Tax Relief for Marrie dFilers by Income Class in Tax Year 2006

$30K- $40K- $50K- $75K- $100K- $200K- $500K- Ove r$40K $50K $75K $100K $200K $500K $1M $1 M

Adjusted Gross Incom e

Note : Totals don't add to one because taxpayers with zero AGI, married filin gseparately, and heads of households are omitted .

Source : Tax Foundation

t-) $5cc

g $4

$3

$2

$ 10

0m07 -$ 1

-$2

m -$ 3

m -$40E –$5

$1 -$20K

$20K -$30K

Bush

n McCain

Candidates

front page 1

tax plan would really hurt many low -income retirees ."

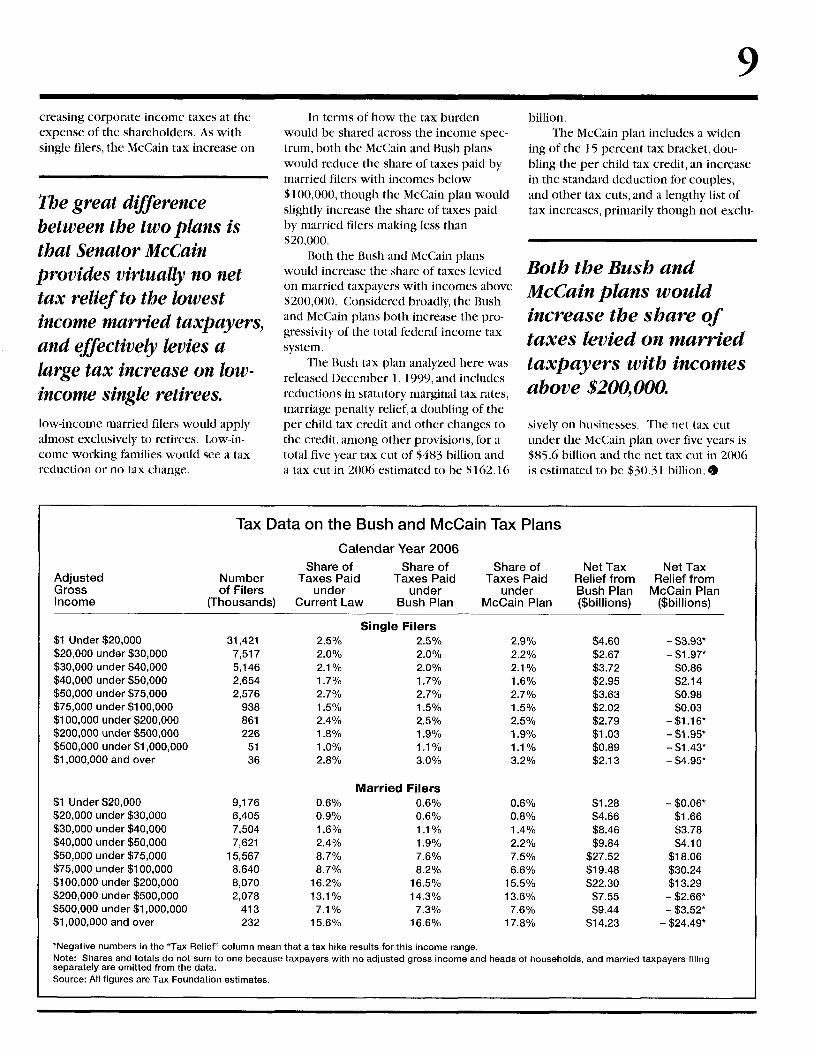

The Tax Foundation examined thetax plans advanced by Governor Bus hand Senator McCain in terms of th eshares of total federal taxes (individua land corporate income) paid by single andby married taxpayers, and in terms of theamount of tax relief or tax increase fo rboth groups, and presented the analysi sby standard income ranges .

In dollar terms, Figure 1 on page 1shows that for single taxpayers the Bushplan gives most of the tax relief to indi-viduals with incomes below $75,000 . A sshown in Figure 3A below, the Bush planshows a slight reduction in the share oftaxes paid by single filers with income sbelow $20,000 and minor changes fo rhigher income levels, and a modest in -crease for tax filers with incomes over$200,000 .

In contrast, while the McCain pro-posal does provide significant relief fo rsingle taxpayers with incomes betwee n$30,000 and $75,000, the plan's corpo-rate income hikes would hit single tax-payers hard at both ends of the incomespectrum (see Figure 1) . The plan's effec ton the income distribution of the tax

burden would b esimilar. The shareof total federalincome taxes pai dby single taxpay-ers with income sbelow $30,000 orabove $100,000would rise (seeFigure 3A).

As shown inFigure 2, the Bus hplan providesmarried filers mos tof its tax relief indollar terms t othose with in-comes betwee n$50,000 and$200,000, withmore modest ta xrelief going tomarried filers wit hhigher and lowerincomes. TheMcCain planwould also provide most of its relief inthe $50,000 to $200,000 range, thoug hmuch more of it would be concentrate din the $75,000 to $100,000 range .

The McCain plan departs from theBush plan, however, in that his tax relief

going to married filers with income sbelow $50,000 would be slight, and hewould increase the tax burden on mar-ried filers with incomes in excess of$200,000 . This tax increase, like the oth-ers in the McCain plan, results from in -

Figure 3: Share of Total Income Taxes Paid by Income Class, Single Filers and Married Filer s

Calendar Year 200 63A: Single Filers

Current Law

q Bush

El McCai n

3 .5% 20%

18%3.0%

16%

2 .5% 14%

12 %2.0%10 %

1 .5% 8 %

1 .0% 6%

4%0.5%

2%

0% 0%$1- $20K- $30K- $40K- $50K- $75K-$20K $30K $40K $50K $75K $100K

Adjusted Gross Incom e

Note: Shares do not sum to one because taxpayers with no adjusted gross income and heads of households, and married taxpayers filing separately ar eomitted from the data .

3B: Married Filers

q Current Law q Bush

• McCai n

--

$100K- $200K- $500K- Over

$1- $20K- $30K- $40K-$200K $500K $1M $1M

$20K $30K $40K $50 K

FT HP.1$50K- $75K- $100K- $200K- $500K - Over$75K $100K $200K $500K $1M $1 M

Adjusted Gross Incom e

9creasing corporate income taxes at th eexpense of the shareholders . As withsingle filers, the McCain tax increase o n

The great differencebetween the two plans isthat Senator McCainprovides virtually no nettax relief to the lowestincome married taxpayers,and effectively levies alarge tax increase on low -income single retirees.low-income married filers would applyalmost exclusively to retirees . Low-in-come working families would see a taxreduction or no tax change .

In terms of how the tax burde nwould be shared across the income spec-trum, both the McCain and Bush planswould reduce the share of taxes paid bymarried filers with incomes below$100,000, though the McCain plan woul dslightly increase the share of taxes paidby married filers making less than$20,000 .

Both the Bush and McCain planswould increase the share of taxes leviedon married taxpayers with incomes above$200,000 . Considered broadly, the Bus hand McCain plans both increase the pro-gressivity of the total federal income ta xsystem .

The Bush tax plan analyzed here wa sreleased December 1, 1999, and include sreductions in statutory marginal tax rates ,marriage penalty relief, a doubling of theper child tax credit and other changes tothe credit, among other provisions, for atotal five year tax cut of $483 billion an da tax cut in 2006 estimated to be $162 .16

billion .The McCain plan includes a widen-

ing of the 15 percent tax bracket, dou-bling the per child tax credit, an increasein the standard deduction for couples ,and other tax cuts, and a lengthy list oftax increases, primarily though not exclu-

Both the Bush andMcCain plans wouldincrease the share oftaxes levied on marriedtaxpayers with incomesabove $200,000.

sively on businesses . The net tax cu tunder the McCain plan over five years is$85 .6 billion and the net tax cut in 200 6is estimated to be $30 .31 billion. l®

Tax Data on the Bush and McCain Tax Plan s

Calendar Year 2006

AdjustedGrossIncome

Numberof Filer s

(Thousands)

Share of

Share ofTaxes Paid

Taxes Pai dunder

underCurrent Law

Bush Plan

Share ofTaxes Pai d

underMcCain Plan

Net Ta xRelief fromBush Pla n($billions)

Net Ta xRelief fro m

McCain Plan($billions )

$1 Under $20,000 31,421 2 .5%Single Filer s

2 .5% 2 .9% $4 .60 - $3 .93 *$20,000 under $30,000 7,517 2 .0% 2 .0% 2.2% $2 .67 - $1 .97 *$30,000 under $40,000 5,146 2 .1 % 2 .0% 2 .1 % $3 .72 $0 .86$40,000 under $50,000 2,654 1 .7% 1 .7% 1 .6% $2 .95 $2 .1 4$50,000 under $75,000 2,576 2 .7% 2 .7% 2.7% $3 .63 $0 .9 8$75,000 under $100,000 938 1 .5% 1 .5% 1 .5% $2 .02 $0.0 3$100,000 under $200,000 861 2 .4% 2 .5% 2 .5% $2 .79 - $1 .16 *$200,000 under $500,000 226 1 .8% 1 .9% 1 .9% $1 .03 - $1 .95*$500,000 under $1,000,000 51 1 .0% 1 .1% 1 .1% $0 .89 - $1 .43 *$1,000,000 and over 36 2 .8% 3.0% 3.2% $2 .13 - $4 .95 *

$1 Under $20,000 9,176 0 .6%Married Filers

0 .6% 0.6% $1 .28 - $0.06 *$20,000 under $30,000 6,405 0 .9% 0.6% 0.8% $4 .66 $1 .6 6$30,000 under $40,000 7,504 1 .6% 1 .1% 1 .4% $8 .46 $3.7 8$40,000 under $50,000 7,621 2 .4% 1 .9% 2.2% $9 .84 $4.1 0$50,000 under $75,000 15,567 8 .7% 7 .6% 7.5% $27.52 $18.0 6$75,000 under $100,000 8,640 8 .7% 8.2% 6 .6% $19 .48 $30.2 4$100,000 under $200,000 8,070 16 .2% 16 .5% 15 .5% $22 .30 $13 .2 9$200,000 under $500,000 2,078 13 .1% 14 .3% 13 .6% $7 .55 - $2 .66*$500,000 under $1,000,000 413 7 .1 % 7 .3% 7 .6% $9 .44 - $3 .52*$1,000,000 and over 232 15 .6% 16 .6% 17 .8% $14 .23 - $24 .49*

*Negative numbers in the "Tax Relief" column mean that a tax hike results for this income range .Note: Shares and totals do not sum to one because taxpayers with no adjusted gross income and heads of households, and married taxpayers filin gseparately are omitted from the data .Source : All figures are Tax Foundation estimates .

10

Inland Waterways Tax Hurts Economy andEnvironment, According to New Study

The inland waterways tax is eco-nomically and environmentally destruc-tive, according to a new Tax FoundationBackground Paper titled The Unin-tended Consequences of the InlandWaterways Excise Tax .

The study's author is John Dunham ,Manager of Fiscal Issues for Philip Mor-ris Management Corp ., whose recentstudies include "The Creation of Impos-sible Markets," published in BusinessEconomics and "The Effects of SmokingLaws on Seating Allocations of Restau-rants and Bars," published in EconomicInquiry.

What Is the Inland Waterway?The inland waterways system in th e

United States is made up of over 25,000miles of lakes, rivers, and canals as wel las the infrastructure needed for ships totraverse them . The system reaches from

The inland waterwaysexcise tax either reducesinterstate trade andcommerce, or moves thattrade to truck and railmodes, resulting in morepollution and a morehazardous transportationsystem.

the ocean into 35 states, to points as fa rinland as Oklahoma .

In 1997, the last year for whichcomprehensive data are available, ove r2 .2 billion tons of cargo were carrie don barges over the nation's inland wa-terways . Also, thousands of passenger swere carried on river cruise vessels, andcountless individuals used the water-way system for recreational pursuits .

According to the Army Corps ofEngineers, water transportation is themost efficient and cost effective way to

transport large amounts of goods fromone place to another. For example, on estandard 1,500-ton barge can transpor tas much wheat as 15 rail cars or 5 8tractor trailer trucks . Barges are muc hmore energy efficient than these othe rmeans of transportation and create les sair pollution per ton mile carried .

How Is the Waterway Taxed ?In 1978, Congress passed the firs t

excise tax on users of the nation's in-land waterway system—a fuel tax thattook effect in October 1980 . The ratewas 4 cents per gallon then but hasrisen steadily and now exceeds 2 4cents per gallon . In FY 1997, the taxgenerated $108 million which the fed-eral government earmarked toward th eInland Waterways Trust Fund .

Though governments find excis etaxes easier to impose than other taxes ,that doesn't mean they're part of a wiseeconomic policy. In fact, the impositio nof an excise tax has a number of unex-pected, unwelcome implications for th eeconomy. Excise taxes can introduc einefficiencies into the economic mar-ketplace, reducing net consumer ben-efits . In addition, these taxes may influ-ence consumer and business decisions ,often discouraging them from pursuin gtheir best options .

Is the Inland Waterway Tax aProper Excise Tax?

Some proponents of excise taxesview the inland waterways tax as a use rfee; but the justifications most ofte ncited for user fees do not apply to theinland waterways tax .

There are no "negative externali-ties" to account for; that is, the moneycollected does not redress some nega-tive side effect of transporting cargo o nthe waterway. Also, the market is no tdominated by a monopoly supplier o rmonopsony buyer, and the tax is col-lected from only certain users of thesystem. Therefore, the imposition ofthe inland waterways tax simply re-duces interstate trade and commerce,

Publication Summary

General : Background Paper No . 33 ;ISSN 1527-0408 ; 12pp . ; $25 or $60/yr.for 6 issues on varied fiscal topic s

Title : The Unintended Consequences o fthe Inland Waterways Excise Tax

Author: John Dunha mDate : February 2000Subject : Clarifies misconceptions abou tuser fees in general, and in particularhow a user fee is unjustified in the cas eof the inland waterways system . Arguesthat the tax has only succeeded i ntransferring cargo from barges to rai land trucks, with a host of negative con -sequences including environmenta ldegradation, higher energy use an dmore traffic accidents .

or moves that trade to truck and rai lmodes . There appear to be no offset-ting benefits .

Empirical analysis finds that for anominal increase of one cent in the taxrate there would be a 15,000 ton dro pin cargo volumes . This leads to unin-tended consequences such as increase dair pollution, higher energy use, andmore traffic accidents . e

Other Papers in the Ta xFoundation's Excise Tax

Research Progra m

♦The Telephone Excise and the E-Rat eAdd-on Tax

♦Flow Excise Tax Differentials AffectCross-Border Sales of Beer in the UnitedState s

♦Federal Excise Taxes and the Distributio nof Taxes Under Tax Reform

♦How Excise Tax Differentials Affec tInterstate Smuggling and Cross-Borde rSales of Cigarettes in the United States

♦Burning Issues in the Tobacco Settle-ment: An Economic Perspectiv e

♦How the McCain Bill Would Ai let tSmokers'Wallets and the IndergroundCigarette Marke t

♦My Favorite Tax Hike by G .O.Party♦The Regressivity of Sin Tax : The hifetime

Tax Burden of Taxes on Alcohol andCigarette s

♦The Use and Abuse of Excise Taxes♦Excise Taxes and Sound Tax Policy

1 1

Humility As TradePolicy

The United States government ha sadopted a public attitude towards theeconomic policies of our largest tradin gpartners that is simultaneously obnox-ious and contrary to the best interest sof our own economy.

At the recently concluded Worl dEconomic Forum in Davos, Switzerland ,U .S . representatives once again toldeverybody else what to do to get theireconomies moving smartly. The rest o fthe world is surely tired of this by now,since the U .S . government has taken tolecturing at almost every opportunity .

To be sure, we have reason to crow.We are breaking records for economicgrowth, inflation is negligible, and pro-jected budget surpluses run into th etrillions of dollars . And for their part ,the Europeans and Japanese shouldthink back to the 1970s and 1980s be-fore they complain about our high-toned lectures . They didn't hesitatethen to lecture us about our budge tdeficits and high inflation, or abouttheir own economic wisdom and short-lived "miracles "

Even so, public admonitions andproddings by the Yankees are not appre-ciated. As Bundesbank President ErnstWelteke is quoted in the Wall StreetJournal,"In Europe, we discuss theproblem of disequilibrium in the U .S . ,but we don't tell the U .S . what to doabout it ." The disequilibrium he wa sreferring to is the huge U.S . trade deficit .It's small wonder the Europeans keeptheir opinions to themselves on thi sscore, since fixing our trade defici tmight require breaking down tradebarriers into, say, Europe, or cuttingimports from, say, Europe, which wouldcertainly not help the German economy .

Nevertheless, there are four goodreasons the U .S . should tone down itsrhetoric . First, it's arrogant . It's surelygalling for the rest of the world towatch American popular culture be-come their own, as their children eatMcDonald's Happy Meals, watch Ameri -

can moviesand speakAmericanslang . It'sirksome toour allie sthat they relyon the U .S .military toput out Euro -pean firesand providestability in Asia . And it's bad enough fo rthem to have their economies struggl ewithout watching the United States pos ta 5.8 percent growth rate in the fourt hquarter. Humility has never been a nAmerican forté, but now would be agood time to try.

A second reason the United Statesshould be more circumspect in its opin-ions is that we cannot be sure that wha tworks here will work as well abroad.Deregulation, relatively low marginal ta xrates, and stiff competition work in theUnited States . It should work equallywell in Western Europe and Japan, bu twho can say for sure? We thought i twould work equally well in Russia, andeventually it will, but we found ou rinitial prescriptions to be naive .

Economic policy is about choices .Many Europeans place a high premiu mon social justice while fearing the roughand tumble of American-like markets .Most Europeans want far more vacatio nthan Americans would typically take ,and they want to work far fewer hoursthan Americans with no loss in pay. TheJapanese, for their part, want a morerigid society than Americans wouldtolerate . These are not unreasonabl echoices, but they come with a cost . Weshould not lecture others for makin greasonable choices unless those choicesimpose costs on Americans .

Finally, why should we cajole ou rtrading partners into adopting morepro-growth policies when it's probablynot in our best interest economically ?

The classic answer is that if ourtrading partners grow more rapidly ,their demand for our products andservices will grow, and our exports will

surge. Given the size of our trade defi-cit, this seems reasonable, but it misse sthe point . The goal of trade policy isn' tjust to raise exports, but to increasewhat we can buy abroad for a give namount of what we can sell abroad .No one works just for wages . We workso that we can buy goods and services .If the other guy is willing to give u smore for our wages, why should wecomplain ?

In the old days, some would say thatthe trade deficit depresses domesti cemployment . Domestic employment isnow so strong that the unemploymen trate has dropped to levels unimaginablein the old days, and the economy is s ostrong the Federal Reserve is sure toraise interest rates to knock it down apeg. Encouraging stronger economie sabroad to increase our exports to ex-pand domestic employment doesn' tseem a very pressing issue .

While some of the recent U .S .growth is due to increases in employ-ment, much of it is due to rapid an dsustained increases in labor productivitycommonly attributed to new technolo-gies and the rapid pace of U .S . capitalformation . If labor productivity growt hin the United States continues to out -strip that of our trading partners, theneventually the underlying terms of tradebetween the United States and the res tof the world must shift in our favor. U .S .workers will be able to buy more goods ,both domestic and foreign, per hour ofwork, which is as good a definition asany of greater prosperity.

The United States certainly shouldnot inhibit better economic policie samong our trading partners . But weshould not forget that the pre-eminen tgoal of U .S . policy should be to enhanc ethe lives of U .S . citizens . One way to dothis is to encourage policies that allo wAmericans to buy more for less . There' san old saying that goes, if someone in-sists on being a fool, make sure there'sonly one. If our trading partners insis ton maintaining anti-growth economicpolicies, we should just make sure w edon't follow suit . 4

J. D . Foster, Ph .D .Executive Director &

Chief EconomistTax Foundation

12TAX FEATURES© Tax Foundation Schedule of Events and ResearchTax Features© (ISSN 1069 -711X) is published 10 time sa year by the Tax Foundation,an independent 501(c)(3)organization chartered in theDistrict of Columbia . Annualsubscriptions to th enewsletter are $15 .

Co-Chairman, Policy CouncilDominic A. Tarantino

Co-Chairman, Policy CouncilJames C . Miller III, Ph .D .

Chairman, Program Committe eJoseph 0 . Luby, Jr.

Vice Chairman, ProgramCommitte e

Michael P. Boyle

Executive Director and ChiefEconomist

J.D . Foster, Ph .D.

Senior Director, Developmentand Operation s

Renee A . Nowland

Edito rBill Ahern

Contributing economists:Patrick Fleenor, Claire M . Hintz,Scott Moody

Tax Foundation(202) 783-2760 Tel(202) 783-6868 Faxwww.taxfoundation.orgtf@taxfoundation .org

February•

18-26 Latin American International Ta xConferenc e

• Background Paper on the Inland Waterways Tax• Special Report on the President's FY 2001 Budget• Special Report on State Tax Rates and Collection s

March• 9th Tax Policy Conference co-sponsored with

PricewaterhouseCoopers LLP and Baker& Hostetler, LLP (see article below)

• Special Report on Government Spending in th e20th Centur y

• Background Paper on Telephone Excise s• Background Paper on the Smuggling and Cross -

Border Sales of Cigarettes in New York Cit y

April• 14th Tax Freedom Day Announcement• Publication of Facts & Figures on Governmen t

Finance, 34th Editio n

May• European International Tax Conferenc e• Publication of Taxpayer's Guide to Federal Spend-

ing, FY 200 1• Annual Report

On March 9, 2000, the Tax Foundation will co-host the eleventh annual Tax and Budge tPolicy Seminar with Baker & Hostetler LLPand PricewaterhouseCoopers LLP A sophisti-cated analysis of the regulatory, budgetary, andlegislative forces that will shape federal taxand budget policy in the coming years, th eseminar will once again take place at theHyatt Regency Capitol Hill, 400 New Jersey

June• Excise Tax Conferenc e

July• Special Report on Federal Tax Burdens and Spend-

ing by State• Background Paper on the Economic Costs o f

Smoking

August• Background Paper on the Economic Cost of Beer

September• Special Report on the Price of Civilized Societ y

October• Special Report on State and Local Property Tax

Collection s

November• 16th Annual Dinner and National Conferenc e• Special Report on the Distribution of the Federal

Individual Income Tax

Research in the works• Individual Tax Complianc e• Corporate Tax Complianc e• The Estate Ta x• The Regressivity of the Tax on Capita l• The Taxation of Human Capita l

Avenue, NW, Washington, DC (202-737-1234) .The program will run from 8 :00 a.m. to 4 :00p.m., and the cost including continental break-fast and lunch is $285 .

To register or get more information, pleas econtact Sarah McKittrick at (202) 861-1747, o rprint the registration form located on the webat www.taxfoundation.org/bhformfax.htm land fax it to Ms . McKittrick at 202/861-1783 .

Tax Foundation Co-Hosts Tax Policy Conferenc eWith Baker & Hostetler and PricewaterhouseCooper s

6ZZS'9N lfwJadJQ `uol&urgsF

Qldda rlsod SflSSFID ISJhLI

8068-9000 00 `uolbuNseM

ocz el!ns MN 'l88J1S H O9z l

NOIl~/aN1

LE6 taouig