Sick Pay Changes & Changing Pension Landscape Presentation to HMI HR Group November, 2013....

36

Sick Pay Changes & Changing Pension Landscape Presentation to HMI HR Group November, 2013. Cornmarket Group Financial Services Ltd. is regulated by the Central Bank of Ireland. A member of the Irish Life Group Ltd. Irish Life Assurance plc is regulated by the Central Bank of Ireland. Telephone calls may be recorded for quality control and training purposes.

-

Upload

suzanna-stafford -

Category

Documents

-

view

217 -

download

0

Transcript of Sick Pay Changes & Changing Pension Landscape Presentation to HMI HR Group November, 2013....

Sick Pay Changes &

Changing Pension Landscape

Presentation to HMI HR GroupNovember, 2013.

Cornmarket Group Financial Services Ltd. is regulated by the Central Bank of Ireland. A member of the Irish Life Group Ltd. Irish Life Assurance plc is regulated by the Central Bank of Ireland. Telephone calls may be recorded for quality control and training purposes.

• Founded in 1972 (40th Anniversary in 2012)

• One of Ireland’s largest brokers recognised as market leader in affinity schemes for Public Sector employees.

• Acquisition of Marsh VGS’s in January 2013

• We now deal with over 14 Public Sector unions and administer over 50 Schemes covering over 53,000 public sector employees

• Now a member of the GreatWest LifeCo group of companies.

Key topics of today’s presentation

Current proposals represent the biggest ever changes to sick pay for all

Public Sector employees.

Proposed changes to paid sick leave

Paid Sick leave

Self-certified sick leave reduced from 7 days in 1 year, to 7 days in a rolling 2 year period

From 1st January 2014 - 3 months full pay & 3 months half pay (in a rolling four year period)

Paid Sick leave for ‘Critical’* Illness - 6 months full pay, and 6 months half pay (in a rolling four year period)

*Not yet defined

Pension Rate of Pay re-branded ‘Temporary Rehabilitation Pay’

Already in place

Already in place

TemporaryRehabilitation Pay

€3,931

Early Retirement Pension

€5,678

State Illness Benefit

€9,776

State Invalidity Pension

€10,062

100%

75%

25%

50%

Up to 13 weeks

After 13 weeks

After 26 weeks

After 2 years

Half Pay

Full Pay

€45,000

€22,500

Could you survive on a fraction of your salary?

Proposed Sick Pay Arrangements

The example above is based on a permanent, full-time Public Servant, who is a member of the Superannuation Scheme, with 15 years’ service earning €45,000 p.a., paying PRSI at the ‘A’ rate, who is now unable to work due to a long-term illness or disability. Claim is not for a critical illness. Member had no previous illness before joining the Scheme.

Could you automatically go onto HALF PAY if you fall ill in 2014?

2010 2011 2012 2013 2014

HALF PAY

Example: In early 2011 Mary, a Public Sector employee, broke her leg and couldn’t work for 12 weeks. In 2012, she fell ill again and was out of work for a further 2 weeks. Since then Mary hasn’t been out sick. However, come January 2014, Mary needs to know that if she falls ill again and cannot work, her pay will automatically drop to HALF PAY; as she has already used up her 13 weeks full pay allowance.

12 WEEKS 2 WEEKS ?No sick leave

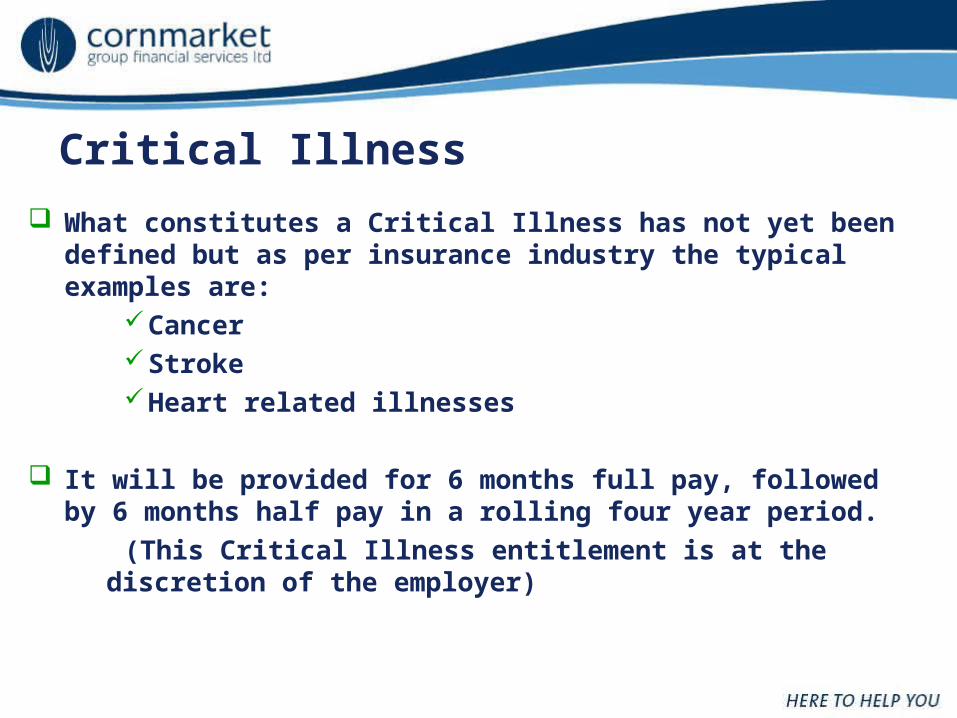

What constitutes a Critical Illness has not yet been defined but as per insurance industry the typical examples are:

CancerStrokeHeart related illnesses

It will be provided for 6 months full pay, followed by 6 months half pay in a rolling four year period.

(This Critical Illness entitlement is at the discretion of the employer)

Critical Illness

Previously known as ‘Pension Rate of Pay’ Payable for UP to 18 months after the 6 months

certified sick pay run out You must apply for Rehabilitation Pay before your

sick pay runs out – will be subject to periodical reviews (probably every 3 months)

Reviews will be carried out by an Occupational health consultant or by MedMark occupational healthcare.

Temporary Rehabilitation pay

What happens after 18 months?3 Options1. Early Retirement Pension – Use of Early Retirement

Pension table to calculate pension & gratuity Retiring on Ill Health means you cannot return to work

in the Public Sector

2. Option to go back to work3. You can opt to a maximum of 12 months of unpaid

leave After 12 months you must either:

I. Take Early Retirement Pension II. Go back to work orIII. Resign from your current position

Cornmarket can advise on all options

2 Options to Protect Your Salary

1 Union Salary Protection Group Schemes • INMO • SIPTU Schemes • Impact • PNA • IHCA

2 Private Salary Protection Plans• AVIVA • Friends First • New Ireland • Irish Life

SchemeBenefit

TemporaryRehabilitation

Pay€3,931

Early Retirement

Pension

€5,678

State Illness Benefit

€9,776

State InvalidityPension

€10,062

SchemeBenefit

€20,043

Scheme Benefit

€18,010

100%

75%

25%

50%

Up to 13 weeks

After 13 weeks

After 26 weeks

After 2 years

Half Pay

Salary Protection Schemes Post 1st January

2014

With Salary Protection you will receive up to 75% of your

salary*

Full Pay

€45,000

€22,500

€11,250

*Less any Temporary Rehabilitation Pay, Early Retirement Pension an/or State Illness Benefit to which you are entitled.The example above is based on a permanent, full-time Public Servant, who is a member of the Superannuation Scheme, with 15 years’ service earning €45,000 p.a., paying PRSI at the ‘A’ rate, who is now unable to work due to a long-term illness or disability. Claim is not for a critical illness. Member had no previous illness before joining the Scheme.

What does it mean for you?

Salary

€45,000

Service

15 years

After 26

weeks

€33,750

After 13

weeks

€33,750

After 2 yrs

onwards…

€33,750

Salary

€45,000

Service

15 years

After 26 weeks

€13,707

After 13 weeks

€22,500

After 2 yrs onwards…

€15,740

Example: WITH Salary Protection

Example: WITHOUT Salary Protection

Example above is based on a Public Servant, who is a member of the Superannuation Scheme, with 15 years’ service earning €45,000 p.a., paying PRSI at the ‘A’ rate, who is now unable to work due to a long-term illness or disability. Standard sick leave is assumed. Member had no previous illness before joining the Scheme. The example above assumes that Temporary Rehabilitation Pay and State Illness Benefit is paid for up to a maximum of 2 years and, thereafter, the member is granted an Early Retirement Pension and State Invalidity Pension.

The teams responsible for the smooth administration of Salary Protection schemes are:-

Phone Assistance One to one meetings in Office or Clients home

nationwide Assistance with arranging medicals Help with Appeals process with the Insurance

Company Help with FSO (Financial Services Ombudsman) if

required.

Tara CassidyAssistant Manager in charge of Claims

Claims Handling

Source: The Economist – 07.04.11

People living longer in retirement

• 1950: 7.2 people aged 20-64 for every 1 person over

65

• 1990: 5:1

• 2012: 3.5:1

• 2050: 1.8:1In other words, every couple will be supporting a pensioner

“Ireland’s numbers in retirement will double before 2040 to over 1m people with the biggest increase in the over 85s age group”*

*Source – Department of Health

Source: The Economist – 07.04.11

In the USA, if a married couple both retire at 65, there’s a 50% chance one will live to 90+

1. People Live Longer

greater need for private health care nursing homes

additional pressure on health care services

increased health costs

longevity

Source: The Economist – 07.04.11

3. Governments and companies cannot offer DB schemes

If pensions are underfunded or government does not have enough money to pay pensions, they can reduce cost or burden by:

– Raising taxes for existing workers– Current generation of workers fund more to Pension– Raise retirement age– Halt practice of early retirement – Auto-enrolment: compulsory for everyone to pay into a

Pension– Link retirement age to longevity.

Proposed Retirement Dates

How are Countries planning to deal with this?

Spending in RetirementIn retirement, people’s spending profile is U-Shaped

years

spen

ding

60s 70s 80s

Travel & spend

Still active

more time at home

spend less

accumulate

healthcare

spend more

Source: The Economist – 07.04.11

•OAP now moving from age 65 -> 68•Tax relief on pensions still available @ 41%*•Once-off option to withdraw up to (maximum) 30% of the value of your AVC Fund, subject to tax

Currently different Pension Schemes exist in the Public Sector:

Category 1. Pre 1995 Category 2. 1995 to 2004 Category 3. 2004 to 2009 / 2010 to 2012 Category 4. 1st January 2013

- Single New Pension Scheme

What are your options? …NSP, AVCs/PRSAs etc.

Salary Age Service Pension

€55,000 60 30 yrs €20,625

Pension Entitlements

Pre 2004 (inc Supp Pen for A Class PRSI)

€8,68630 yrs60€55,000

Cost Neutral Early Retirement

Post 2004

*subject to paying the higher rate of tax

Benefits payable from your Superannuation Scheme

Pension Lump SumSpouse & Children’s

Benefit

Taxed & Paid for Life

Tax-Free & Paid Once

Payable on Death

What’s important when working out my pension?

•Starting dates & re-entry dates •Service history•Final salary (except for 2013 Scheme)•Relevance of Social Welfare in your pension

• New Single Public Service Pension Scheme (Career average earnings)

• Retirement in line with State pension age (SPA): 66 to 68Minimum pension age of 66to 67 in 2021 and to 68 in 2028 Pensions being linked to life expectancy(from 65 to 66 in 2014)

• How will it work?• Referable amounts will accrue for each year service• Accrual rates of 0.58% on first €45k and 1.25% on balance• Lump-sum accrual rate of 3.75%• Annual increase in referable amounts in line with CPI.

New Pension Scheme for 2013

Enhancing your PensionEnhancing your Pension

Retirement planning is still a very tax efficient way to save

Contribution €100

Less tax relief

(assuming tax @41%) -41.00

NO PRSI rate (removed in Budget 2011)

Real cost to you for every €100

€59.00

1. Repurchase Superannuation credit for yrs spent in part-time/temporary service OR any Gratuity or Refunds

2. Buy Superannuation credit for missed years of service - Notional Service Purchase Scheme (NSP)

3. Fund additional benefits for your retirement

- Additional Voluntary Contribution Scheme (AVCs) or

- Personal Retirement Savings Account (PRSA).

Options Available

€00,000

€00,000

Top up tax free lump sum to its max

Mixture of other options

Pension (Annuity)€000 p.a.

Employer options

How an AVC can be usedHow an AVC can be used

ARF/AMRF€00,000

Last minute AVCs – (Dynamisation)

Issues to be aware of for Retirement Planning

1. Public Sector Pensions Act 2012 (Career Averaging)

2. Public Service Superannuation Act 2004

3. Cost Neutral Early Retirement

4. Personal tax rates – now & in retirement

5. Social Welfare entitlements

6. Tax Relief Scope & limits

7. Fee, Charges, Commissions on Advice, AVCs & PRSAs

8. Partner Pension Details (if applicable).

5 Modules to choose from

E-shot attachments for each module

Booklet & Booking form

Thank you for your attention

Questions?

Proud sponsors:

Cornmarket Group Financial Services Ltd. is regulated by the Central Bank of Ireland. A member of the Irish Life Group Ltd. Telephone calls may be recorded for quality control purposes.