SGAFR/CAFR FROM THE GROUND UP

113

SGAFR/CAFR FROM THE GROUND UP Linda Dufresne, CPA Dufresne & Associates, CPA, PA KBLD LLC GNP Services, CPA, PA

description

SGAFR/CAFR FROM THE GROUND UP. Linda Dufresne, CPA Dufresne & Associates, CPA, PA KBLD LLC GNP Services, CPA, PA. Objectives. Introduction to the Certificate of Conformance Program Award for Small Governments Reasons to prepare a CAFR - PowerPoint PPT Presentation

Transcript of SGAFR/CAFR FROM THE GROUND UP

SGAFR/CAFR FROM THE GROUND UP

Linda Dufresne, CPADufresne & Associates, CPA, PAKBLD LLCGNP Services, CPA, PA

Objectives Introduction to the Certificate of Conformance

Program Award for Small Governments Reasons to prepare a CAFR Components of the CAFR and the order in which

they should be presented Common CAFR inadequacies How to make application for the GFOA Certificate of

Conformance Program Award or Certificate of Excellence in Financial Reporting

Certificate of Conformance Program (COCP)

Established by GFOA in late 2012 Recognizes small governments Modified Cash Basis of Accounting Eligible to earn the new Certificate of

Conformance Program award

Certificate of Conformance Program

If GAAP financials not practical option Little guidance or consistency Certificate of Conformance Program

award will help these small governments improve quality of financial reports

Creates nationally recognized guidelines Participants benefit from increased

training and professionalism resulting from producing high-quality financial reports

Purpose for Certificate of Conformance Program

Strives to recognize quality and consistency in three ways Provides guidelines to help standardize the

format and content of financial reports presented on a modified cash basis

Seeks to encourage governments to follow those guidelines by publicly recognizing entities that choose to follow those guidelines

Aims to improve quality and consistency by assisting governments in implementing guidelines by providing technical materials and training

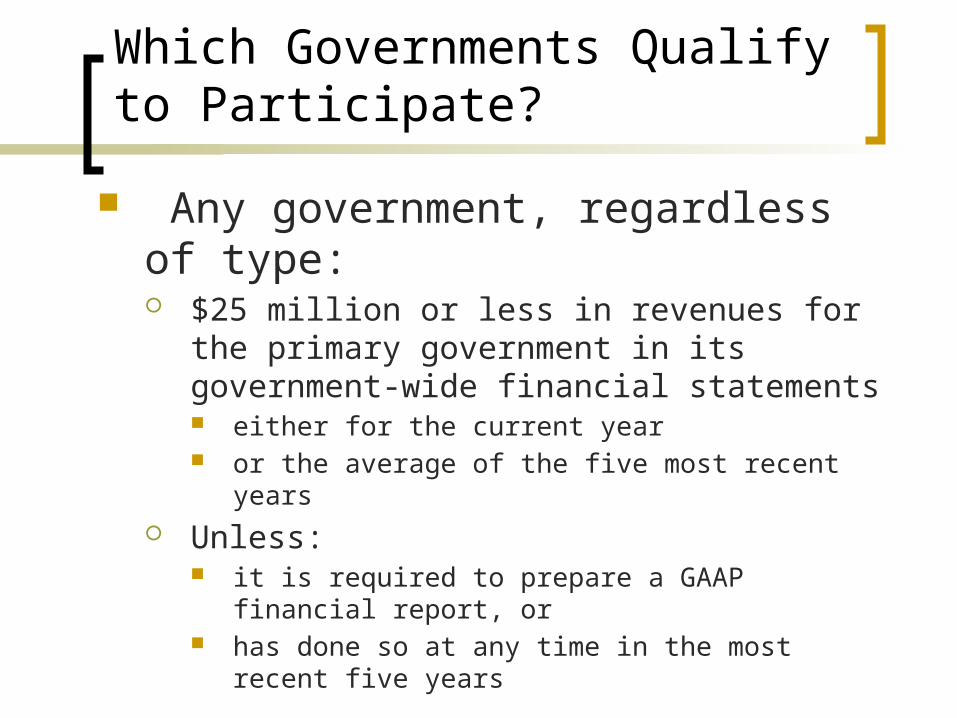

Which Governments Qualify to Participate?

Any government, regardless of type: $25 million or less in revenues for the primary

government in its government-wide financial statements either for the current year or the average of the five most recent years

Unless: it is required to prepare a GAAP financial report, or has done so at any time in the most recent five years

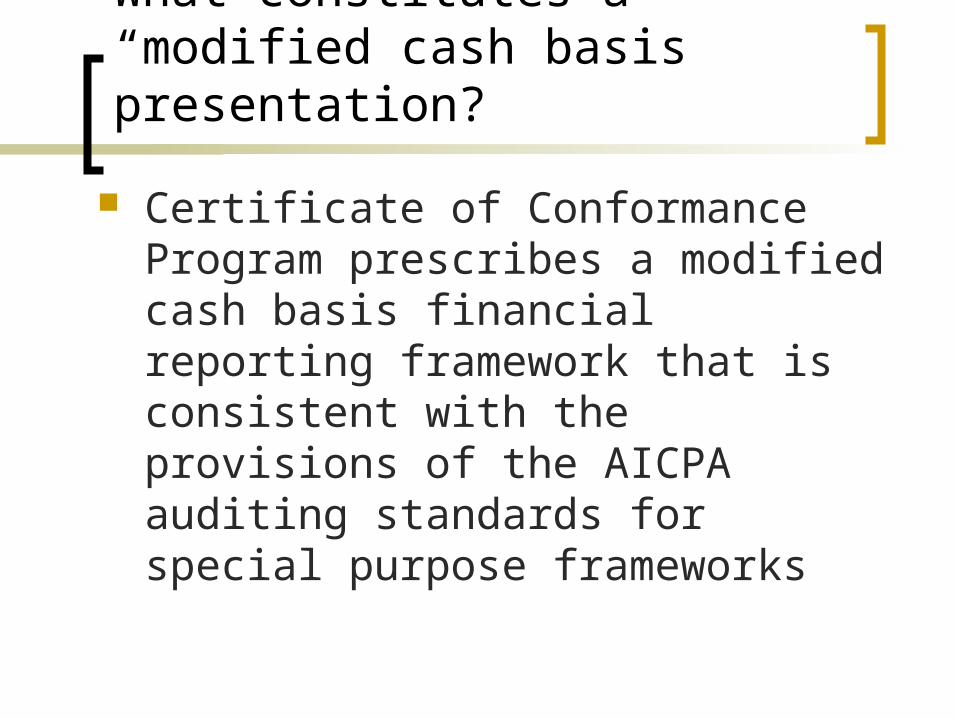

What constitutes a “modified cash basis” presentation?

Certificate of Conformance Program prescribes a modified cash basis financial reporting framework that is consistent with the provisions of the AICPA auditing standards for special purpose frameworks

What constitutes a “modified cash basis” presentation?

For purposes of the Certificate of Conformance Program, a “modified cash basis” presentation must meet all of the following criteria Comply, in substance, with the basic requirements of

GAAP for financial statement presentation, but applied in a manner consistent with a modified cash basis, for example, a small general purpose government would need to present a

combination of government-wide and fund financial statements (i.e., compliance, in substance, with the basic requirements of GAAP), but

would use the same modified cash basis for presenting data in both (i.e., applied in a manner consistent with a modified cash basis)

What constitutes a “modified cash basis” presentation?

Only cash (and cash equivalents) and items that involve the receipt or disbursement of cash (or cash equivalents) during the period should be recognized, except as follows: Interfund receivables and payables that arise from transactions and events involving cash or cash

equivalents must be recognized; Assets that normally convert to cash or cash equivalents (e.g., certificates of deposit, marketable

investments, and receivables resulting from loans) that arise from transactions and events involving cash or cash equivalents must be recognized;

Liabilities for cash (or cash equivalents) held on behalf of others, held in escrow, or received in advance of being earned or meeting eligibility requirements must be recognized

Note disclosures similar to those required by GAAP must be made if they are relevant to any of the items listed above

Other note disclosures related to matters not presented on the face of the financial statements should be provided, as considered necessary

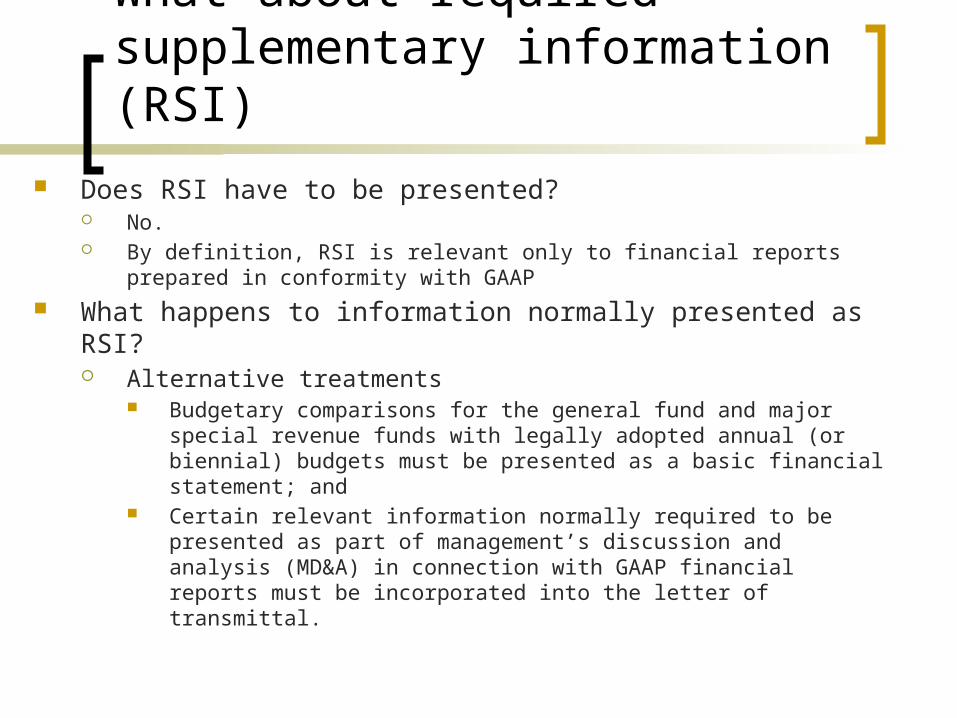

What about required supplementary information (RSI)

Does RSI have to be presented? No. By definition, RSI is relevant only to financial reports prepared in conformity with

GAAP What happens to information normally presented as RSI?

Alternative treatments Budgetary comparisons for the general fund and major special revenue

funds with legally adopted annual (or biennial) budgets must be presented as a basic financial statement; and

Certain relevant information normally required to be presented as part of management’s discussion and analysis (MD&A) in connection with GAAP financial reports must be incorporated into the letter of transmittal.

Does COCP require a CAFR? Does a CAFR have to be prepared?

No. COCP requires that the basic financial statements and certain other information

be presented as part of a small government annual financial report (SGAFR) rather than as part of a comprehensive annual financial report (CAFR)

A SGAFR, like a CAFR, must include both an introductory section and a financial section.

Conversely, unlike a CAFR, a SGAFR does not have to include a statistical section

What does Scarlett eat when she arrives at Tara after their escape from Atlanta?

Turnip Peanuts Radish Egg

Trivia question

Scarlett vowing in a barren field: "I'll never be hungry again!”

Answer

Radish

69% of players have answered correctly

This is the only food she finds at Tara since the Yankees has destroyed all the plantations and killed or taken all of the livestock.

What specific information must be included in the SGAFR?

Financial section, like a CAFR, must present: Combining and individual fund financial statements and schedules,

including budgetary comparisons presented at the legal level of budgetary control for all individual governmental funds with legally adopted annual or biennial budgets.

In addition, the financial section needs to provide the following schedules of five-year trend data, as applicable: Net position – government-wide financial statements – modified cash basis, Changes in net position – government-wide financial statements – modified

cash basis, Fund balances – governmental funds – modified cash basis, Revenues, expenditures, and changes in fund balances – governmental

funds – modified cash basis, and Outstanding debt by type

What are the application deadlines?

How will the reports be judged? Combination of volunteer reviewers and GFOA professional staff Same process as the Certificate of Achievement for Excellence in

Financial Reporting Program

What does it cost? The fee for participating in the Certificate of Conformance Program

is based on the total amount of revenues reported in the government-wide financial statements (excluding discretely presented component units), as follows:Total Revenues GFOA Member Fee Nonmember Fee Under $1 million $290 $580 $1-10 million $370 $740 Over $10 million $435 $870

BONUS!! Nonmembers that submit for the first time receive a GFOA membership that allows them to submit at the member rate.

What are the benefits? All governments that participate in the Certificate of Conformance

Program will receive: a grade assigned to each of section of their report, and a list of specific comments and suggestions for improvement

The Certificate of Conformance Program normally will provide results within six months of receiving a submission, which should give the government adequate time to implement comments and suggestions in its next report

If the report meets the program’s criteria, the participating government also will receive A plaque and a press release A complete list of all award-winning reports will be maintained on the

GFOA’s website First-time winners of the award will be announced in the GFOA

Newsletter

How can I obtain more information?

http://www.gfoa.org/index.php?option=com_content&task=view&id=2586 Details on how to become a participant or reviewer Download a COCP FAQ sheet Access letter from GFOA’s Executive Director/CEO Download a COCP award application Download COCP checklists All you need to know is easily found at the above link

Trivia question

Which secret do the Tarleton twins share with Scarlett?

That they have been expelled from University That Ashley Wilkes will be marrying his cousin Melanie Hamilton That her father is jumping his horse again That they wish the war would start.

Answer

That Ashley Wilkes will be marrying his cousin Melanie Hamilton.

77% of players have answered correctly

Scarlett O'Hara, the main female character in the movie (and in the book as well), was always in love with Ashley Wilkes and dreamed of marrying him and becoming his wife. Scarlett was portrayed by Vivien Leigh.

Certificate of Conformance GFOA Training

http://www.gfoa.org/index.php?option=com_content&task=view&id=2586 GFOA’s complimentary one-hour Internet

training seminar, The GFOA’s New Program for Small Governments that Prepare Modified Cash Basis Financial Reports

Interactive training will offer guidance on the practical application of the modified cash basis for financial reporting as well as the format and contents of a SGAFR

July 11, 2013 and September 18, 2013

Certificate of Conformance Questions??

On to the CAFR!!

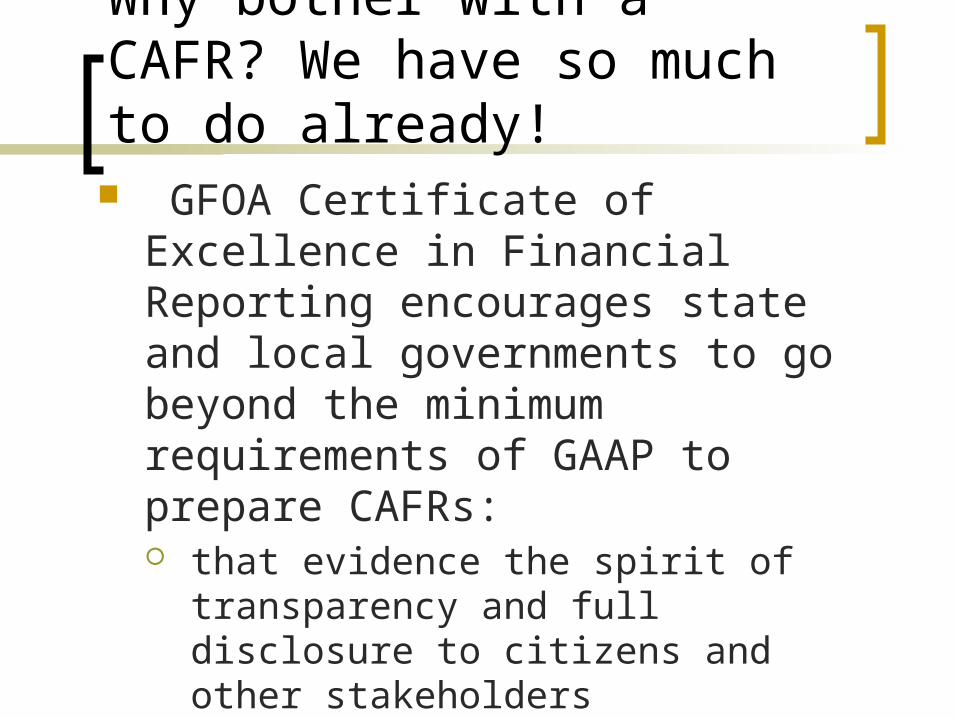

Why bother with a CAFR? We have so much to do already! GFOA Certificate of Excellence in

Financial Reporting encourages state and local governments to go beyond the minimum requirements of GAAP to prepare CAFRs: that evidence the spirit of transparency

and full disclosure to citizens and other stakeholders

recognize individual governments that succeed in achieving that goal.

Why bother? Reports submitted to the CAFR program are

reviewed by selected members of the GFOA professional staff and the GFOA Special Review Committee (SRC)

Individuals with expertise in public-sector financial reporting perform the review - Financial statement preparers, independent auditors, academics, and other finance professionals.

Reviewers provide constructive feedback for improvement

Why bother? Credit rating agencies and other interested

parties may view the award as a positive factor in decisions about your government

Accounting and financial reporting standards evolve; participation helps to ensure that your financial report fully implements those standards

GFOA has formally recognized that the CAFR format meets the SEC Rule 15c2-12 (financial statement disclosure to investors)

Plenty of resources!

Blue book – GAAFR (Governmental Accounting, Auditing and Financial Reporting)

Auditors – “Yellow book” In-house staff GFOA reviewer’s checklist

http://www.gfoa.org/downloads/GENERALPURPOSECHECKLIST.pdf

Web-based software applications Third party vendors

CAFRComprehensive Annual Financial Report

3 Major Sections

Introductory

Financial

Statistical

And

And

Order of presentation

I. Table of ContentsII. Introductory Section

A. Letter of TransmittalB. Organizational ChartC. GFOA’s Certificate of Achievement

Cover Page-Specific Requirements

Comprehensive Annual Financial Report (not “Annual Report”)

Name of primary government State where government is located Fiscal period covered Not a requirement, but common

practice to use art work highlighting the attributes of the entity

Cover page exampleState where government located

CAFR

Name of primary government

Fiscal period coveredComprehensive Annual Financial Report

For the Fiscal Year Ended September 30, 2012

City of Tara, Georgia

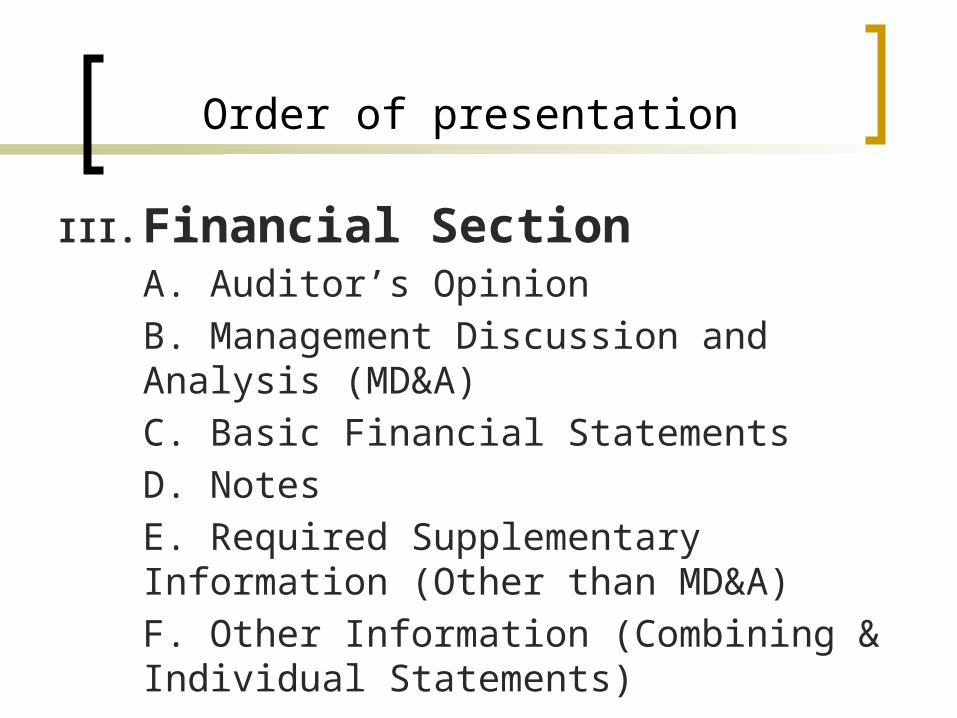

III. Financial SectionA. Auditor’s OpinionB. Management Discussion and Analysis (MD&A)C. Basic Financial StatementsD. NotesE. Required Supplementary Information (Other than MD&A)F. Other Information (Combining & Individual Statements)

Order of presentation

IV. Statistical SectionV. Optional Sections

Order of presentation

Two Pines Twelve Oaks Nine Wattles Five Alpines

Trivia question

What is the Wilkes's plantation called?

This is where a barbeque is held and where Scarlett tells Ashley Wilkes that she loves him for the first time, with disastrous consequences. This is also where Scarlett first meets Rhett Butler.

95% of players have answered correctly.

Answer

Title Page-Specific Requirements

Comprehensive Annual Financial Report (not “Annual Report”)

Name of primary government State where government is located Fiscal period covered Department responsible for preparing

the report

Title page exampleState where government located

CAFR

Name of primary government

Fiscal period covered

Department responsible

Comprehensive Annual Financial Report

For the Fiscal Year Ended September 30, 2012

City of Tara, Georgia

Prepared by the Finance Department

Introductory Section-Purpose?

Provides background and context of CAFRNOT included in scope of audit

Introductory Section-Contents

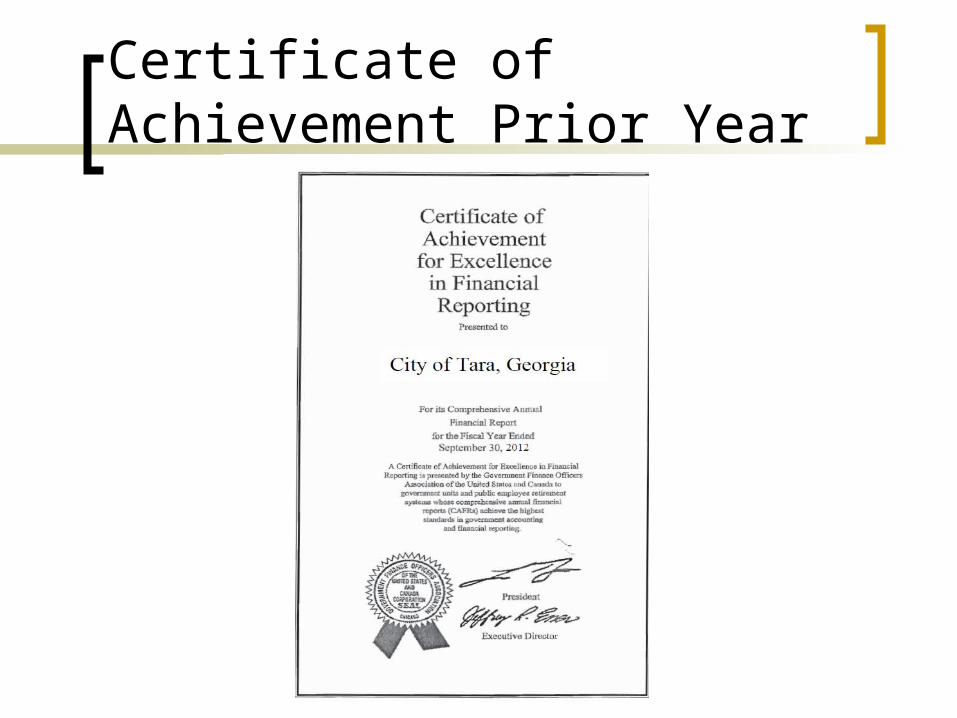

1. Certificate of Achievement for Excellence in Financial Reporting-Prior Year

2. List of Principal Officials3. Letter of Transmittal4. Organizational Chart

Certificate of Achievement Prior Year

City OfficialsPrincipal City Officials

Elected Officials

Rhett Butler - Mayor India Wilkes - Vice Mayor Aunt Pittypat - Councilor

Mammy - Councilor Will Benteen - Councilor

Appointed Officials

Scarlett O’Hara - City Manager Ashley Wilkes - City Attorney Emmie Slattery – City Clerk

Belle Watling - Director of Public Services Big Sam - Director of Public Safety

Jonas Wilkerson - Director of Finance

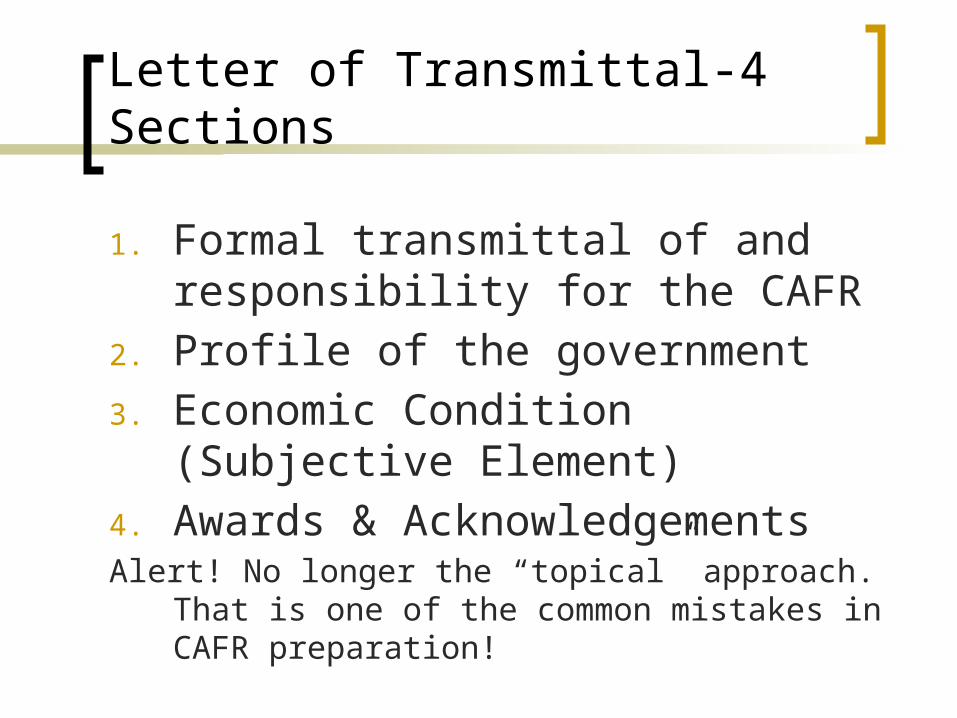

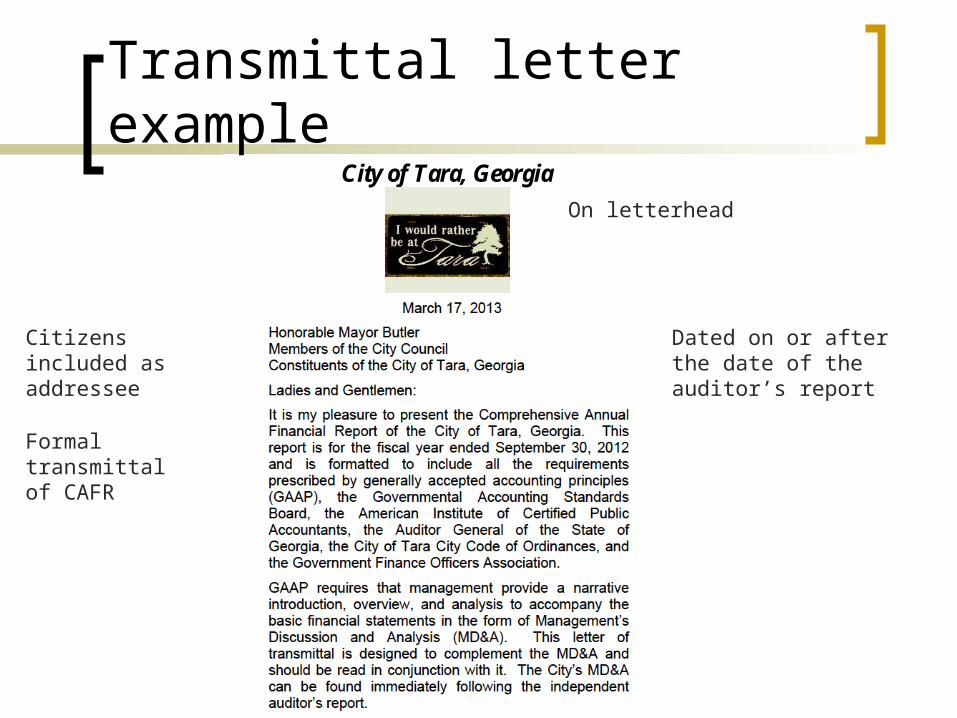

Letter of Transmittal-4 Sections

1. Formal transmittal of and responsibility for the CAFR

2. Profile of the government3. Economic Condition (Subjective

Element)4. Awards & AcknowledgementsAlert! No longer the “topical” approach. That is one of

the common mistakes in CAFR preparation!

Letter of Transmittal

Minimum-Signed by CFO Dated on the date the CAFR is first

made available to the public (no earlier than the auditor’s report)

On letterhead stationery of the entity Citizens included as addressee

Letter of Transmittal

States that management is responsible for the contents of the report

Directs readers to the MD&A Refrains from duplicating information

contained in the MD&A or notes to the financial statements

Formal Transmittal Streamline discussion without altering basic contents

Profile of the Government No discussion of the budget calendar and budgetary responsibilities Simple discussion of the legal level of budgetary control

Information useful in Assessing Economic Condition

Discussion of the local economy to encompass financial trends during the past five to 10 years Discussion of long-term planning to explain how it may shed light on current and future financial position

Discussion of relevant financial policies

Letter of Transmittal Helpful Hints

Information useful in Assessing Economic Condition

Discussion of major initiatives from the budget document

Eliminate separate topical discussions of cash management, risk financing, pensions, and other postemployment benefits

Letter of Transmittal Helpful Hints

Transmittal letter example

Dated on or after the date of the auditor’s report

On letterhead

Citizens included as addressee

Formal transmittal of CAFR

City of Tara, Georgia

Transmittal letter example

Signed by CFO

Required section headings tobe completed with concisecharts and graphs

Organizational Chart Example

What color is the dress that Scarlett wears to Ashley's birthday party?

Trivia question

Black with white polka dotsGray Violet Red

Answer Red

Answer

65% of players have answered correctly

Financial Section-Purpose?

Provides critical information regarding the financial condition of the government through the presentation of financial

statements and schedules, note disclosures and narratives (MD&A)

Financial Section – When the audit is done, this part is

done! Whew!

1. Independent Auditor’s Report2. Management Discussion and Analysis

(MD&A)3. Basic Financial Statements4. Required Supplementary Information

(Other than MD&A)5. Combining and Individual Fund

Presentations & Supplementary Info

Provides assurance that the financial statements are reliable Opines on opinion units

Governmental activities Business-type activities Major governmental funds Major enterprise funds All other funds/discretely presented component units

In-relation-to Opinions No opinion: introductory and statistical sections

Independent Auditors’ Report

Provide users with a narrative introduction, overview and analysis of the basic financial statements

The concept of MD&A originated in the private sector, the SEC required MD&A in connection with the financial reports of publicly traded companies

GAAP indentifies specific topics that should be addressed in MD&A; additional topics not on this list should not be addressed in MD&A

MD&A

Discussion of basic financial

statements

Condensed comparative

data

Overall analysis

Fund analysis

Budget variances in the

general fund

Capital asset and long-term debt activity

MD&A

Basic Financial Statements

Core of CAFR’s financial section and has three components: Government-wide financial statements

Presented using the economic resources measurement focus and accrual basis of accounting

Fund financial statements Presented using the current financial resources

measurement focus and modified accrual basis of accounting (governmental funds only)

Notes to the financial statements

Financial Section

RSI (other than MD&A) Budgetary comparisons Trend data on infrastructure condition and

maintenance (only if modified approach is used to account for infrastructure)

Trend data on the funding of pension and other postemployment benefits (OPEB)

Revenue and claims development trend data for public-entity risk pools

Financial Section

Combining and individual fund presentation and other supplementary information CAFR should include a combining

statement to support each column in the basic financial statements that aggregates data from more than one fund

Statistical Section

Financial Trends

• Information to help users understand and assess how financial position has changed over time

Revenue Capacity

• Information to help users understand and assess an entity’s ability to generate own-source revenues

Debt Capacity

• Information to help users understand and assess an entity’s debt burden and its ability to issue additional debt

Statistical Section

Demographic and Economic Information

• Information to help users understand the socioeconomic environment and to facilitate comparisons over time and among governments

Operating Information

• Information to help users understand operations and resources and to provide context for understanding and assessing its economic condition

Where is Scarlett seen which fires up gossip?

Trivia question

In a carriage with a man other than her husband A charity bazaar A cemetery A hospital

After Charles dies of measles while enlisted in the army, Scarlett is sent to Atlanta by her mother

to cheer her up.However, Scarlett is supposed to be in

mourning and therefore should not be seen in

public; this is what fires up the gossip among the

townsfolk, especially after Rhett Butler bids on her for a dance and she

accepts.

Answer

66% of players have answered correctly

Order of Presentation

1. Government-wide Financial Statements

2. Fund Financial Statements3. Required Supplementary Information4. Combining and Individual Fund

Statements and Schedules

Government-wide Statements

Statement of Net AssetsStatement of Activities

All financial statements should refer to Notes!

Gov’t Wide Statements-Major Points View the primary governmental entity

using the economic resources measurement focus and full accrual basis of accounting as a whole unit rather than a group of separately operated funds.

Essentially, a government-wide perspective somewhat conforms a governmental entity's financial reports to those used in the private sector.

Gov’t Wide Statement of Activities-Major Points

Purpose is to show the extent of how each governmental function supports itself, before general tax dollars kick in

Order of Presentation:1. Expenses2. Program Revenues3. Net (Expense) Revenue4. General Revenues

Gov’t Wide Statement of Activities-Net Expenses

What you would expect, in theory…

Governmental activities carry net expenses and depend on tax revenues

Business-type activities either break even or carry net revenues

Fund Financial Statements

GOVERNMENTAL FUNDS(Current Resources/Modified)

1. Balance Sheet2. Statement of Revenues,

Expenditures and Changes in Fund Balance

3. Reconciliation to Government-wide Statements

PROPRIETARY FUNDS(Economic Resources/Full Accrual)

1. Statement of Net Assets2. Statement of Revenues,

Expenses and Changes in Fund Net Assets

3. Statement of Cash Flows

FIDUCIARY FUNDS(Economic Resources/Full Accrual)

4. Statement of Fiduciary Net Assets

5. Statement of Changes in Fiduciary Net Assets

Governmental Fund Financial Statements-Major Points

Separates funds – Major vs. Nonmajor Includes reconciliation back to

governmental activities for both financial statements

All financial statements should refer to Notes!

Financial Section - Notes

Summary of Significant Accounting Policies

Budgetary Information Cash Deposits w/

Financial Institutions Investments Derivatives Contingent Liabilities Encumbrances

Subsequent Events Defined benefit

pensions and post employment benefit plans

Capital Assets and Long-term Liabilities

Significant Commitments

Financial Section – Notes Cont.

Fund Balances Interfund Activity Component Units Endowments Risk Financing Fiscal Year

Inconsistencies Landfill Closure &

Post closure

Property Taxes Segment

Information Related Party

Transactions Joint Ventures Fund Balances Prior Period

Adjustments

RSI-Other than MD&A

1. Budgetary Comparisons if schedule rather than financial statement (General Fund & Major Special Revenue Funds)

2. Trend data on infrastructure condition and maintenance (Modified Approach Only)

3. Trend data on the funding of Pension/Other Post Employment Benefits

4. Revenue & Claims Development Trend Data (Public Entity Risk Pools)

Combining fund financial statements

CAFR should include a combining statement to support each column in the basic financial statements that aggregates data from more than one fund

How many Academy Awards did the film earn?

Trivia question

2 8 5 7

Answer

Best Supporting Actress Hattie McDaniel (“Gone with the Wind”) and presenter Fay Bainter pose with an Oscar statuette.

8 Academy Awards were earned by Gone with the Wind including “Best Picture,” Vivian Leigh for “Best Actress in a Leading Role,” and various others

Statistical Section

Governments present historical information—typically for the past 10 years—about their finances and operations and about their constituents and economy.

GASB Statement No. 44, Economic Condition Reporting: The Statistical Section

Added new information to capture the changes that have taken place in government finance

Made previously reported information more useful Reorganized the statistical section’s required information

and clarifies the objectives of that information Captured the “new” information governments are now

reporting after implementation of Statement 34 Did not change the status of the statistical section as

unaudited supplementary information Any statistical section that accompanies a government’s

financial statements, regardless of whether they are in a CAFR or not, should conform to Statement 44

Statistical SectionGASB 44 – 10 Yr Trending

Financial Trends Revenue Capacity Debt Capacity Demographics and Economy Operating Information

Optional Sections to the CAFRCommon Examples

Investment Section (Pension Plans or Investment Pools)

Actuarial Section (Pension Plans) Single Audit (Federal Awards)

Other Reviewer Considerations

Were comments from prior year CAFR resolved?

Is the report free of inconsistencies?

Do we qualify to apply for the award? Any state or local government, including, in

certain circumstances, funds and departments of governments, may participate in the Certificate Program.

The report must have an unqualified audit opinion (a “clean opinion”) from an independent auditor.

Ordinarily, the CAFR should be published within six months of the government’s fiscal year end.

How to apply

Once the comprehensive annual financial report (CAFR) is prepared, submit it along with a completed application obtained at http://www.gfoa.org/downloads/CERTAPP.pdf

Application form requires information about your government, audit firm and report

Submission and fee calculation instructions Questions regarding disclosure of material

items Authorization of official requesting the review

The normal submission deadline is six months following the government’s fiscal year end

Requests for a one-month extension beyond the deadline may be made as a result of various factors (e.g., employee turnover, implementation of major pronouncements, audit issues, etc.) by e-mailing [email protected]

Reasons resulting from extraordinary events such as hurricane closures are sometimes approved.

How to apply

Awards programs information

Visit www.gfoa.org and click on “Awards Programs” to learn more about:• Awards for Excellence in Government

Finance• Distinguished Budget Presentation Award• Popular Annual Financial Reporting Award

What year was Gone with the Wind released?

Trivia question

1939 1945 1934 1949

Answer

1939

Other films released in 1939 include: “The Wizard of Oz,” “Mr. Smith Goes to Washington,” “Stagecoach,” and “Goodbye, Mr. Chips”

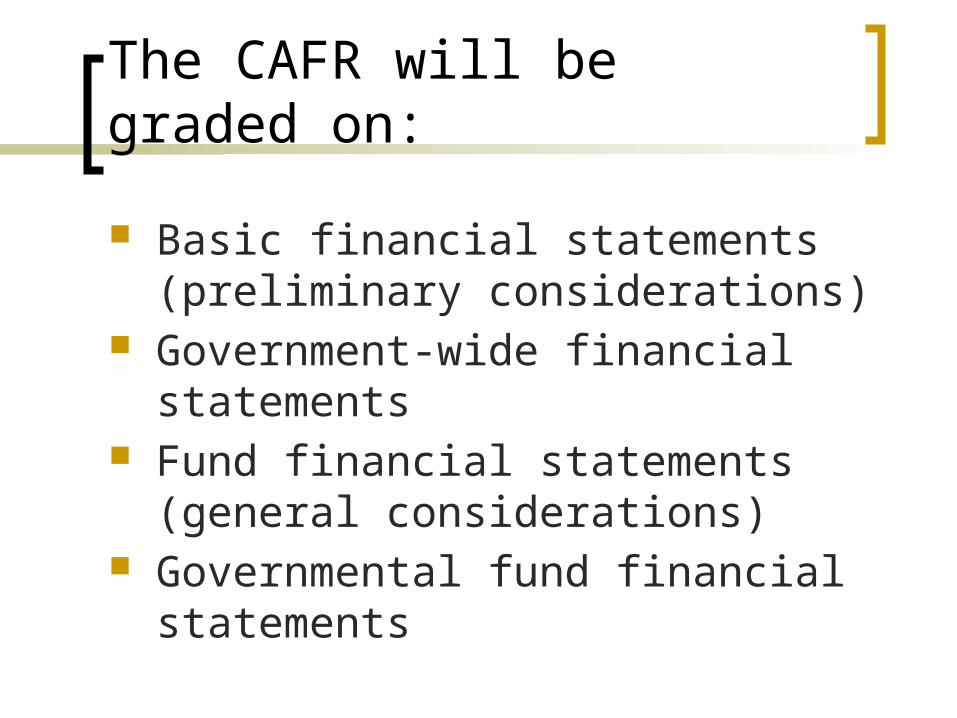

The CAFR will be graded on:

Cover, table of contents, and formatting

Introductory section Report of the independent auditor Management’s discussion and

analysis (MD&A)

The CAFR will be graded on:

Basic financial statements (preliminary considerations)

Government-wide financial statements Fund financial statements (general

considerations) Governmental fund financial

statements

The CAFR will be graded on:

Proprietary fund financial statements Fiduciary fund financial statements Summary of significant accounting

policies (SSAP) Note disclosure (other than the SSAP

and pension-related disclosures) Pension and other postemployment

benefit related note disclosures

The CAFR will be graded on:

Required supplementary information (RSI)

Combining and individual fund information and other supplementary information

Statistical section Other considerations

Then what? After review results are combined and a final vote is

determined, an award decision letter is mailed to the submitting government which includes: grading for various sections of the CAFR, a list of comments and suggestions that detail

how the government can improve its financial reporting, and

a press release. Normally results are sent within six months after

receiving a submission, giving the government time to implement comments and suggestions for its next report.

For more information, please e-mail [email protected]

The Basic Inconsistencies Ending balances on change statements do not agree to

balance sheet/statement of net assets Totals from combining schedules do not agree to the

combined amount in the basic financial statements Amounts in MD&A tables and condensed schedules do

not agree to the basic financial statements or notes Amounts that can be reconciled within the financial

statements and/or between the statements and notes do not reconcile

Amounts in statistical section or other supplemental information do not agree or cannot be reconciled with the financial statements and schedules

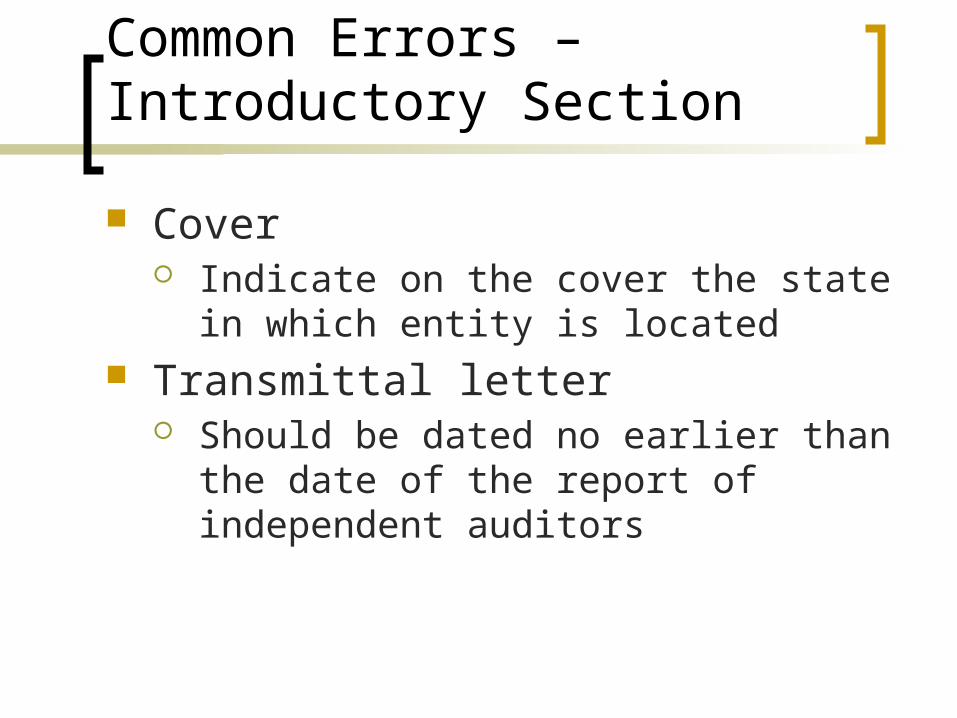

Common Errors – Introductory Section

Cover Indicate on the cover the state in which

entity is located Transmittal letter

Should be dated no earlier than the date of the report of independent auditors

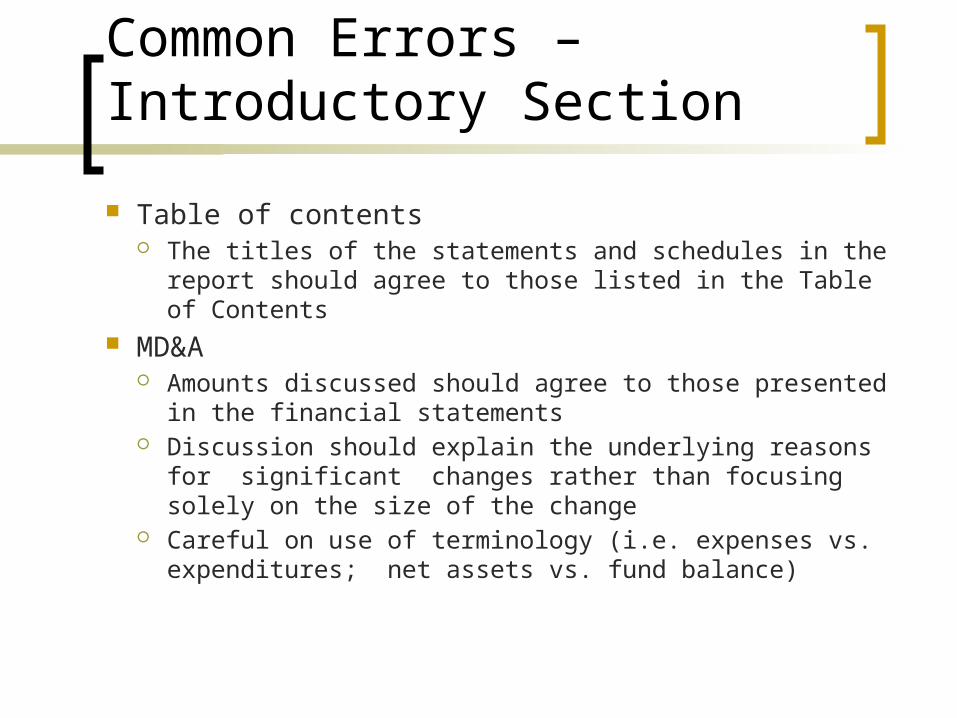

Common Errors – Introductory Section

Table of contents The titles of the statements and schedules in the report

should agree to those listed in the Table of Contents MD&A

Amounts discussed should agree to those presented in the financial statements

Discussion should explain the underlying reasons for significant changes rather than focusing solely on the size of the change

Careful on use of terminology (i.e. expenses vs. expenditures; net assets vs. fund balance)

Common Errors – Basic Financial Statements

All basic financial statements Each of the statements should include a reference to the notes Nonmajor governmental funds should be used rather than other

governmental funds Statement of activities

Except for interest and unallocated depreciation, expenses related to governmental activities should be classified by function rather than by object of expenditure

Expenditures associated with the issuance of debt should not be included

Capital assets should be disclosed by major asset class (i.e. capital leases)

Common Errors – Basic Financial Statements

Statement of net assets Unearned revenue NOT deferred revenue

Governmental balance sheet and statement of revenues, expenditures, and changes in fund balance Governmental funds that report more than 10% of the

total governmental funds assets, liabilities, revenues, or expenditures and more than 5% of the combined total of governmental and enterprise funds for the same element, have to be reported as a major fund

Common Errors – Basic Financial Statements

Proprietary fund financial statements If no debt related to capital assets, use the

caption: Net Assets, Invested in Capital Assets

Common Errors – Basic Financial Statements

Notes to the financial statements Narrative explanations of combining and individual

fund statements and schedules describing the nature and purpose of the funds should be included

Additions to long-term debt disclosed in the notes should agree to the Proceeds from the Issuance of Debt presented in the fund financial statements

Depreciation expense charged by function should agree to current year increases to accumulated depreciation

Common Errors – Basic Financial Statements

Notes to the financial statements Specify action to establish, modify, or rescind

fund balance commitments; disclose body or official authorized to assign fund balance (GASBS No. 54)

Disclose increases and decreases to compensated absences rather than the net change; also, disclose amount due within one year (even if an estimate must be made)

Common Errors – Other Supplementary Info.

Schedule of delinquent taxes receivable Should agree to property tax receivable

per governmental funds balance sheet

Common Errors – Statistical Section

Principal taxpayers, principal employers, demographic and economic information If the information for the period nine or ten year prior

to the current period is not available, then include data from the earliest year from which information is available and disclose the reason for the exception

Property tax levies and collections Total tax collections as a percentage of the annual

levy should not exceed 100%

Trivia question

Why did Scarlett not flee when Atlanta was under attack from the Yankees? She was too scared There was no transportation She was committed to work at the local hospital to care for the

wounded soldiers She promised Ashley she would take care of Melanie

Answer

She promised Ashley she would

take care of Melanie, played by Olivia

deHavilland

Volunteer and LearnWith the Certificate Program

The Government Finance Officers Association invites you to join the Special Review Committee (SRC),

The contribution of these members is invaluable to the Certificate of Achievement for Excellence in Financial Reporting Program (Certificate Program).

What are the benefits?

In exchange for your service to the Certificate Program, you will receive valuable professional development benefits, including:• Being at the forefront of the most recent changes in accounting and financial reporting for state and local governments..

What are the benefits?

• Direct contact with a variety of report formats from around the country.• Each SRC member can elect to review only CAFRs of government types that are of particular interest to them. • See firsthand the current reporting techniques and trends for particular types of governments .

What are the benefits?

• Access to a practical way of providing training and development for junior staff without an incremental cost.• Insight into what it takes to achieve the Certificate of Achievement • Ideas to help you prepare for or improve a future CAFR submission.• Professional recognition for your service and time.

Do I qualify? An individual does not necessarily

have to be upper management or have significant experience with external financial reporting.

The GFOA encourages those with any experience in state and local government accounting and financial reporting to join in the review process.

Do I qualify? Should have had a role:

• in the preparation of a CAFR that received the Certificate of Achievement,• in the independent audit of a CAFR that received the Certificate of Achievement, or• relevant experience and a recommendation from a past or current SRC member.

How will I find the time? The application allows you to shape

your involvement to maximize the use of your time.

The contribution that you make to the SRC can be tailored around your availability and goals.

You are encouraged to use SRC service as a tool for professional development and educational purposes.

Questions?