An Affordable Broadband Seismometer : The Capacitive Geophone Aaron Barzilai 1 , Tom VanZandt 2 ,

Main structure

(Sessions 1–6)

(Firms’ decisions& equilibrium)

Firms are price-takers(Perfect competition)

Firms have market power(Imperfect competition)

(Sessions 7–11)

Firms’decisions

(Sessions 12–15)

Equilibrium

In each case: fixed firms in the market, then entry/exit

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 1

Key ideas on imperfect competition

Imperfect competition

Fixed firmsin market

MC = MR⇓

P, Q

Firms’decisions

Nash eqm.

Equili-brium

Entry& exit

VΠ > FC?

Firms’decisions

Each active firm haseconomic profit ≥ 0 .

No potential entrant could makeeconomic profit > 0 by entering.

Equilibrium

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 2

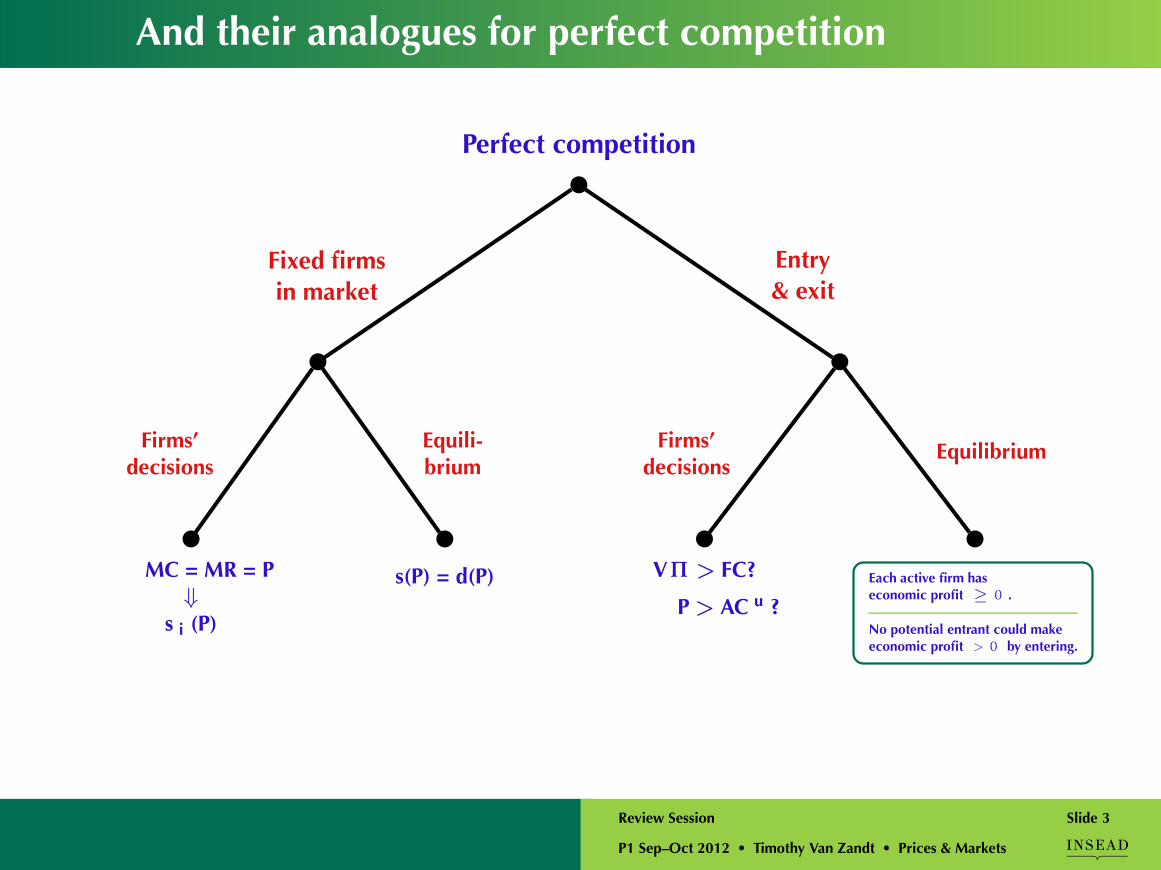

And their analogues for perfect competition

Perfect competition

Fixed firmsin market

MC = MR = P⇓

s i (P)

Firms’decisions

s(P) = d(P)

Equili-brium

Entry& exit

VΠ > FC?

P > AC u ?

Firms’decisions

Each active firm haseconomic profit ≥ 0 .

No potential entrant could makeeconomic profit > 0 by entering.

Equilibrium

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 3

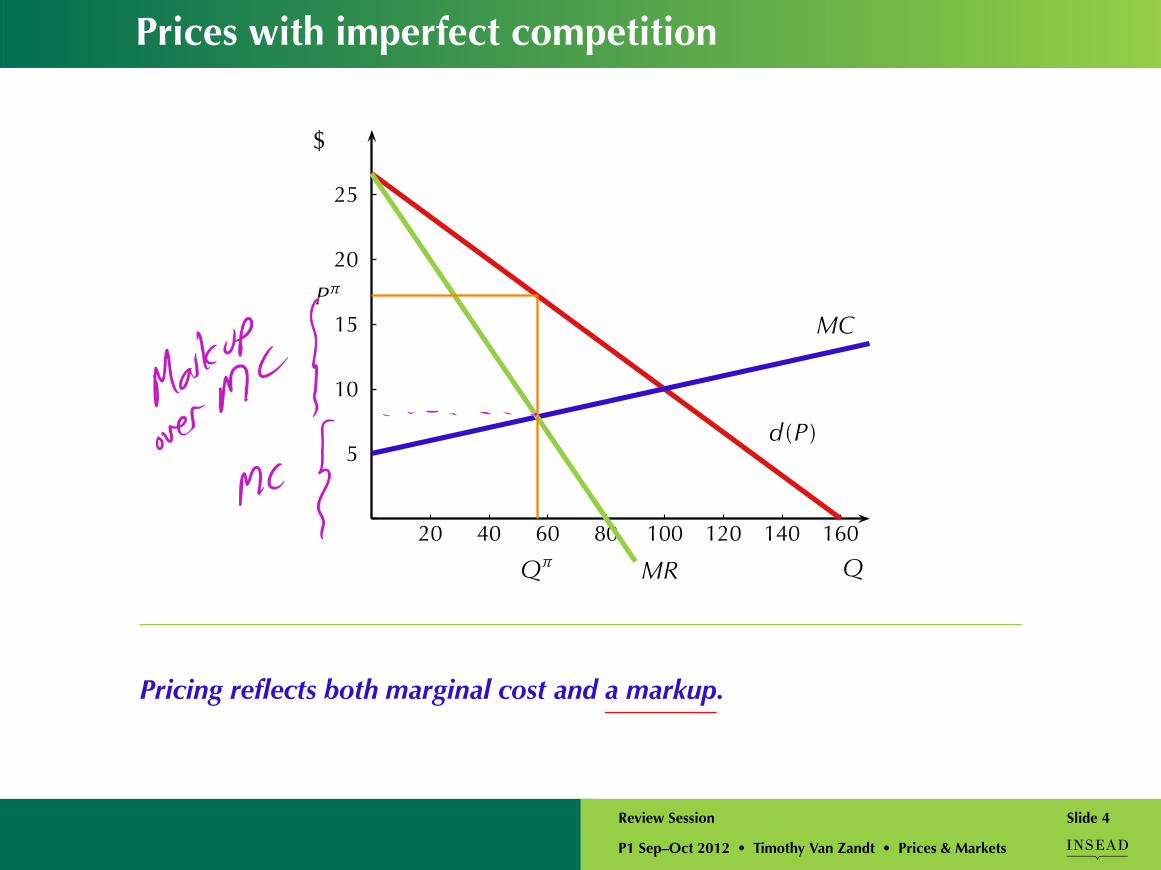

Prices with imperfect competition

5

10

15

20

25

20 40 60 80 100 120 140 160

Q

$

d (P )

MCPπ

Qπ MR

Pricing reflects both marginal cost and a markup.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 4

Advantage of the model of perfect competition?

There are no mark-ups, so we can isolate the effects of cost on prices.

… with a remarkably simple 2-dimensional picture: supply=demand.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 5

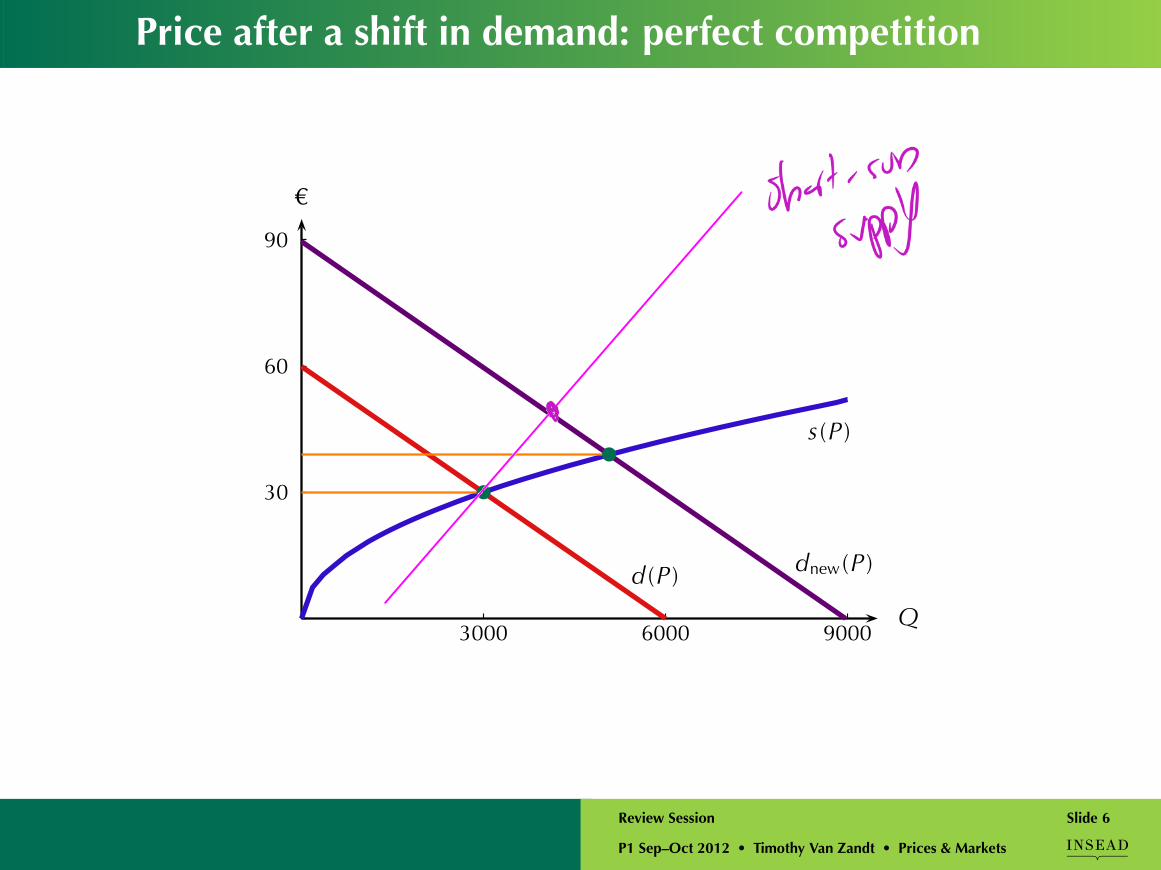

Price after a shift in demand: perfect competition

30

60

90

3000 6000 9000

€

Q

d (P )

s(P )

�

�

dnew(P )

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 6

Reasons for the upward sloping supply curve?

1. Increasing marginal cost of firms in the market.

• Particularly pronounced in the short-run, hence the lower elasticityof short-run supply and the greater short-run volatility of prices.

2. Increasing minimum average cost of subsequent entrants(entry by heterogeneous firms).

3. Increasing cost of key inputs(example: cranberry bogs)

$

Q

Producersurplus

Total cost

P∗

Q∗

d (P )

s(P )

10

20

30

40

50

60

100 200 300 400 500 600 700 800 900

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 7

Price after a shift in demand: perfect competition

30

60

90

3000 6000 9000

€

Q

d (P )

s(P )

�

�

dnew(P )

Change in price is due entirely to increasing marginal costs(of existing firms, of new entrants, or of scarce inputs).

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 8

Session 8: Pricing with Market Power

1. The firm’s “pricing” problem: MC = MR .

2. Profit-maximization versus social efficiency.

3. Exit and entry.

4. Social efficiency with a LR fixed cost.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 9

Once upon a time, on some exam …

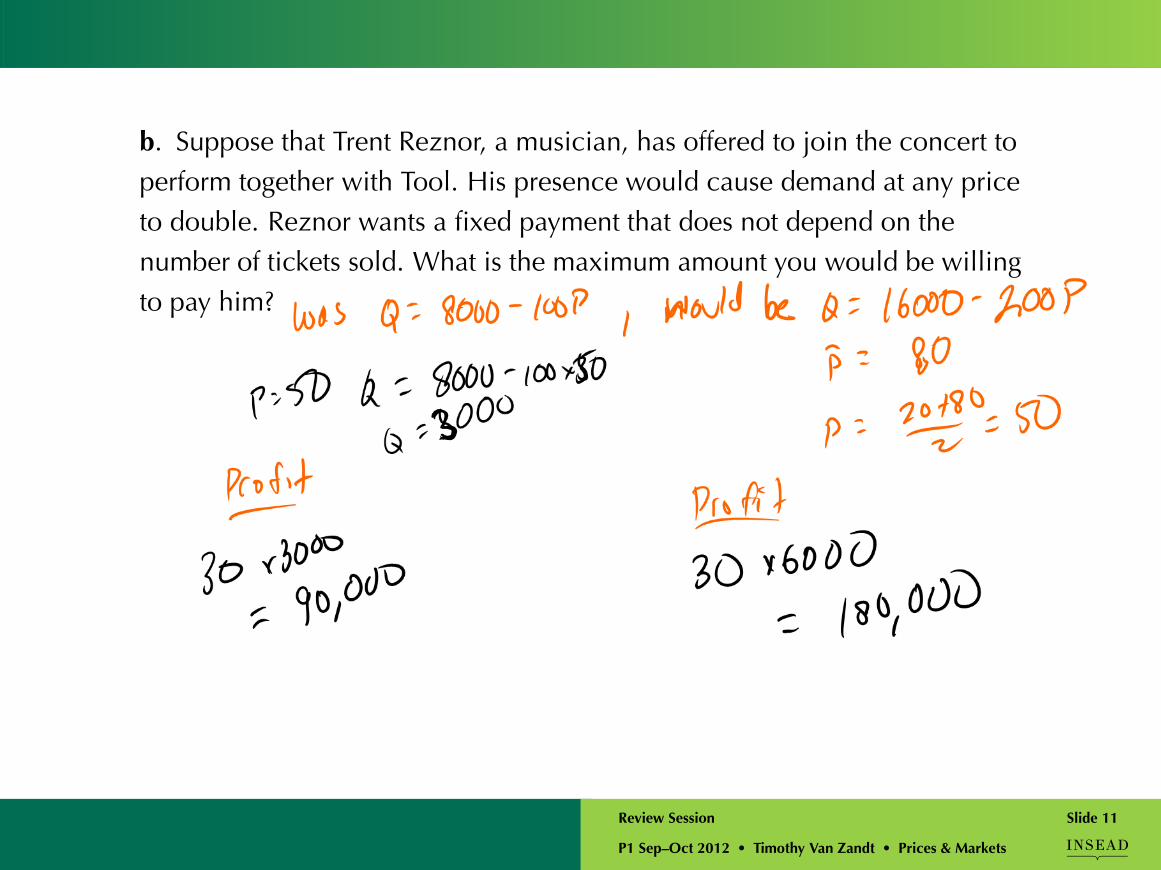

You manage the Zenith, a venue for concerts in Paris. You have signed acontract with a band called “Tool” for a concert on December 10. Thecontract specifies that the band receives €60,000 plus €12 per ticket sold.Assume that you have additional (constant) marginal costs of €8 per ticketsold and that you are not capacity constrained. The demand curve for theconcert is Q = 8,000 − 100P .

a. What price should you charge?

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 10

b. Suppose that Trent Reznor, a musician, has offered to join the concert toperform together with Tool. His presence would cause demand at any priceto double. Reznor wants a fixed payment that does not depend on thenumber of tickets sold. What is the maximum amount you would be willingto pay him?

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 11

Session 9: How pricing depends on demand

1. Useful formula:

MR = P(

1 − 1E

)

2. Price-sensitivity effect: (Assuming constant marginal cost …)

If demand becomes less price sensitive, then the firm shouldraise its price.

3. Volume effect: (Keeping price-sensitivity constant …)

If a firm has increasing marginal cost and the volume of demandgoes up, then the firm should raise its price.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 12

Session 10: Explicit price discrimination

Bottom line:

• Equate MR across market segments.

• Charge higher price to segment with less elastic demand.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 13

Once upon a time, on some exam …

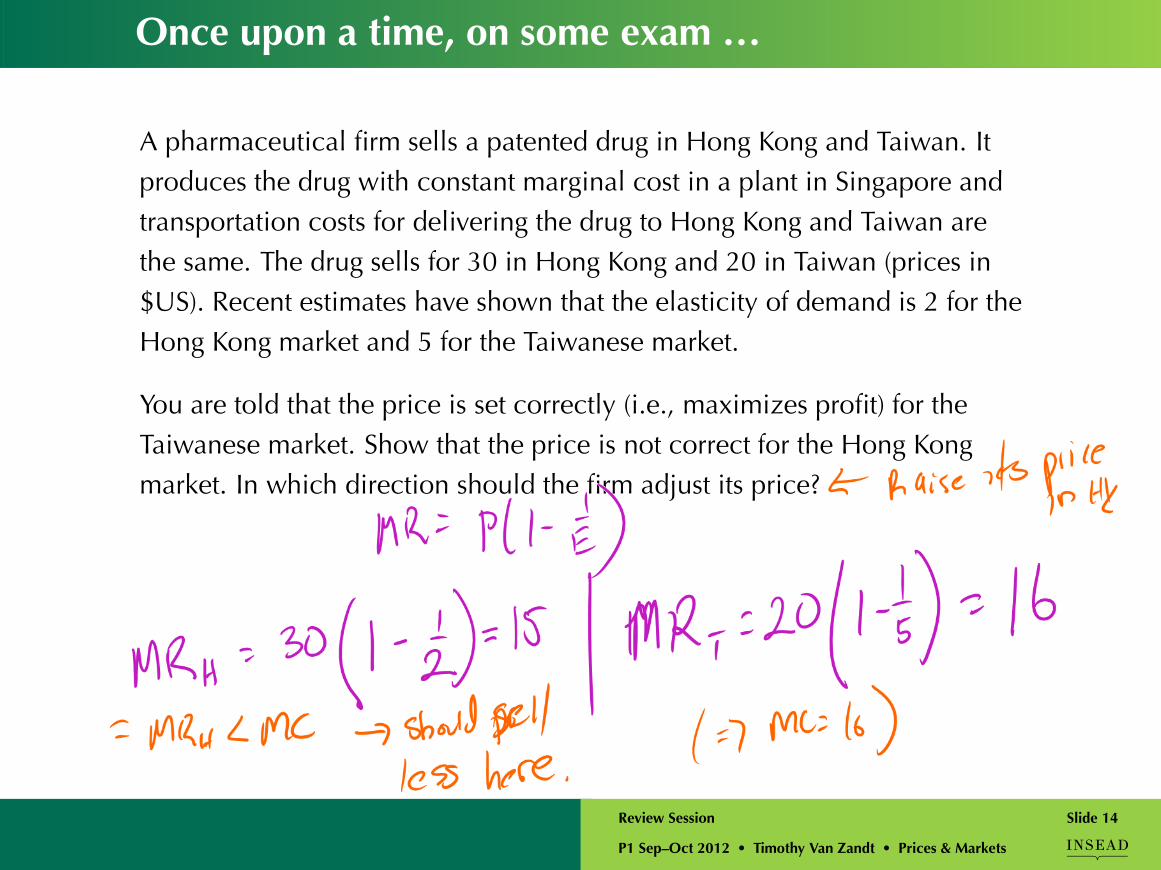

A pharmaceutical firm sells a patented drug in Hong Kong and Taiwan. Itproduces the drug with constant marginal cost in a plant in Singapore andtransportation costs for delivering the drug to Hong Kong and Taiwan arethe same. The drug sells for 30 in Hong Kong and 20 in Taiwan (prices in$US). Recent estimates have shown that the elasticity of demand is 2 for theHong Kong market and 5 for the Taiwanese market.

You are told that the price is set correctly (i.e., maximizes profit) for theTaiwanese market. Show that the price is not correct for the Hong Kongmarket. In which direction should the firm adjust its price?

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 14

Session 11: Implicit price discrimination (Screening)

1. Perfect price discrimination (benchmark)

2. Screening via differentiated products

3. Bundling

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 15

FPM Ex. 11.8

Zahra sells a good with unit demand. She has constant MC = 5 .

Zahra has perfect information about her customers’ valuations. But she is initially prohibitedby law from price discrimination. She chooses to charge $10, which results in sales to 10,000customers. She calculates that these customers obtain a total of $50,000 in consumer surplus.

Then the regulation is lifted and she engages in perfect price discrimination.Based on this limited information, what can you say about …

(a) how many customers she will sell to? >10,000

(all her old customers plus more)

(b) what range of prices she will charge? 5 and up

(down to her MC)

(c) how much her profit will go up by? >50,000

(prior consumer surplus + deadweight loss)

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 16

Sample Exam 3, Problem 17 (Bundling)

You are a monopolist selling two different types of concert tickets. You have zero

marginal cost and hence your objective is to maximize revenue. You face three

groups of potential customers, with an equal number of customers in each group.

The following table summarizes the valuation of each group for each concert. (Each

customer’s valuation of going to both concerts is just the sum of his individual

valuations.)

Valuation

Type Rock World

A 5 60

B 35 65

C 40 70

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 17

Sample Exam 3, Problem 17 (Bundling) (Continued)

Valuation

Type Rock World Bundle

A 5 60 65

B 35 65 100

C 40 70 110

(a) Pure bundling: What is the optimal price for the bundle of both tickets? Whatis your profit?

See valuations of bundle above. Possible price points are 65,100, and 110, yielding revenue (profit) 195, 200, and 110. Sooptimal bundle price is 100 for a profit of 200.

(b) Mixed bundling: Find one mixed bundle pricing strategy that gives you higherprofit than your answer with pure bundling.

Offer World ticket alone for 60; sell this to A. Offer bundlefor 95; sell this to B and C. (Price has to leave surplus of atleast 5 for type B and 10 for type C, so that they do notprefer the single ticket. Total profit is 60 + 2 × 95 = 240 .

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 18

With 4 sessions on game theory

… Tools/concepts that go beyond our applications to pricing and competition

Session 12: Static Games and NE

Basic and universal tools.

Session 13: Imperfect Competition

Price and quantity competition: static games.Core session

vis-à-vis the framework.

Session 14: Explicit and Implicit Cooperation

How—and why—to explicitly or implicitly cooperate.

Session 15: Strategic Commitment

How timing and commitment matter.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 19

Session 12: Static Games and Nash Equilibrium

1. Players, actions, payoffs.

2. Best responses.

3. Dominant strategies.

4. Nash equilibrium.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 20

Session 13: Price competition with fixed firms

1. Each firm’s decision is same as pricing with market power: Topics 8&9

2. Goods are substitutes ⇒ prices are strategic complements(Always with linear demand; almost always in real life.)

3. Interaction captured by Nash equilibriumEach firm’s price maximizes its own profit given price of the other firm.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 21

Scenario

Product category: Passenger jets.

Dominated by two firms: Airbus (A) and Boeing (B).

(For simplicity, imagine that each firm produces one kind of jet, and thesetwo jets make up the entire product category.)

Hypothetical demand functions:

QA = 60 − 3PA + 2PB

QB = 60 − 3PB + 2PA

Constant marginal cost, same for both firms: MCA = MCB = 12 .

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 22

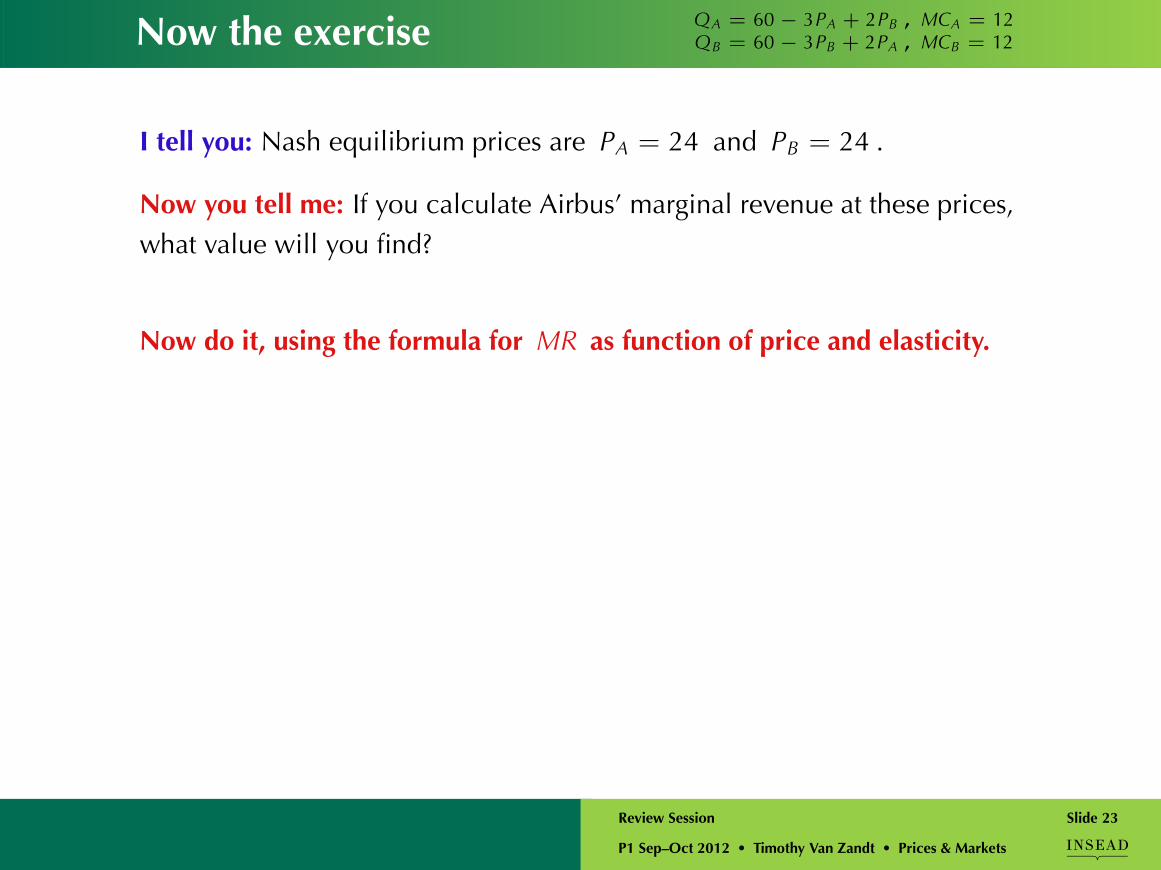

Now the exercise QA = 60 − 3PA + 2PB , MCA = 12QB = 60 − 3PB + 2PA , MCB = 12

I tell you: Nash equilibrium prices are PA = 24 and PB = 24 .

Now you tell me: If you calculate Airbus’ marginal revenue at these prices,what value will you find?

Now do it, using the formula for MR as function of price and elasticity.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 23

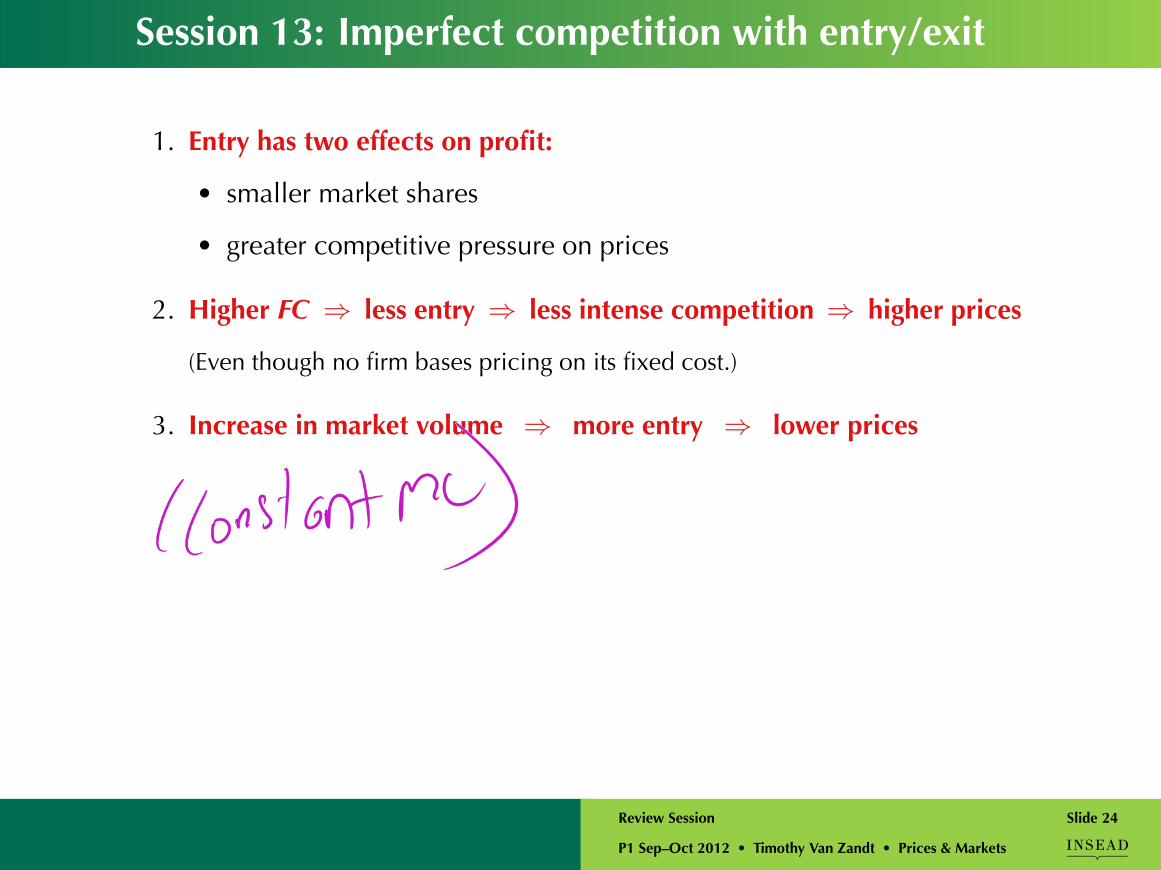

Session 13: Imperfect competition with entry/exit

1. Entry has two effects on profit:

• smaller market shares

• greater competitive pressure on prices

2. Higher FC ⇒ less entry ⇒ less intense competition ⇒ higher prices

(Even though no firm bases pricing on its fixed cost.)

3. Increase in market volume ⇒ more entry ⇒ lower prices

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 24

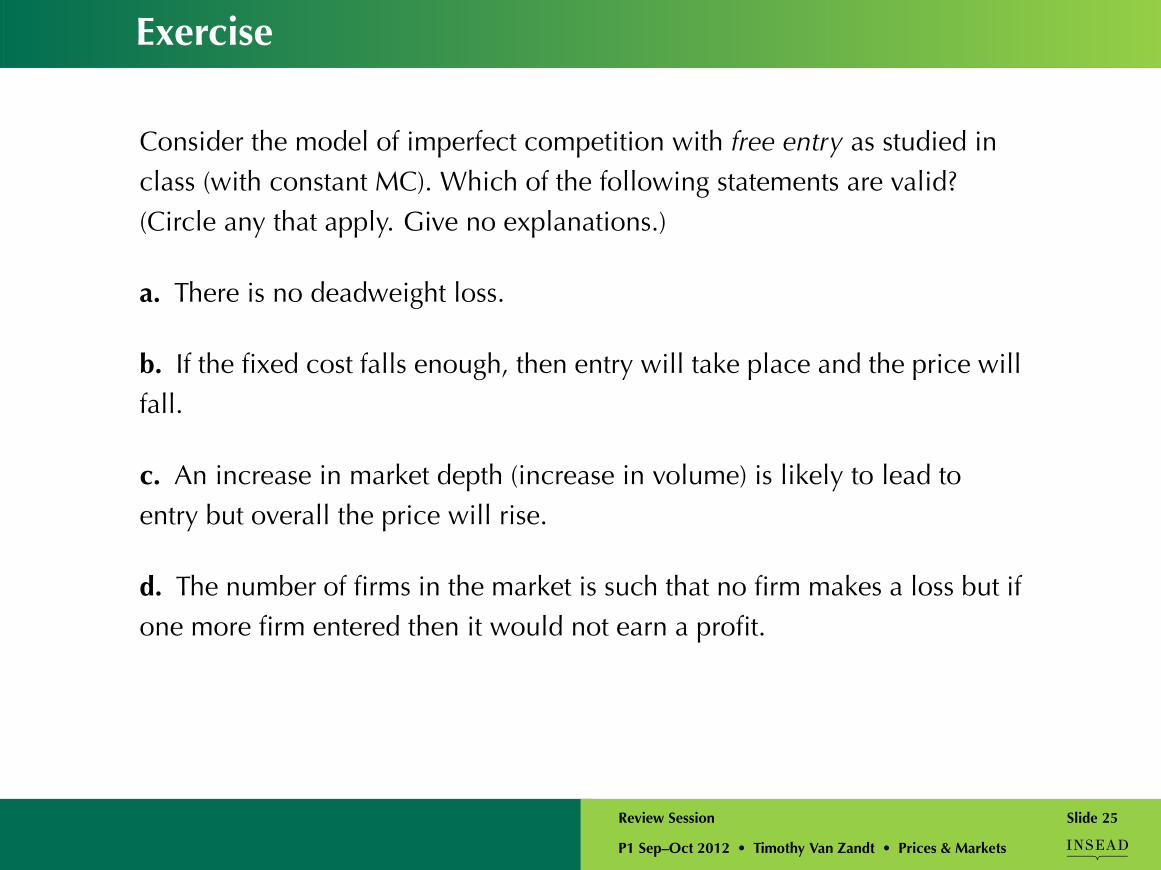

Exercise

Consider the model of imperfect competition with free entry as studied inclass (with constant MC). Which of the following statements are valid?(Circle any that apply. Give no explanations.)

a. There is no deadweight loss.

b. If the fixed cost falls enough, then entry will take place and the price willfall.

c. An increase in market depth (increase in volume) is likely to lead toentry but overall the price will rise.

d. The number of firms in the market is such that no firm makes a loss but ifone more firm entered then it would not earn a profit.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 25

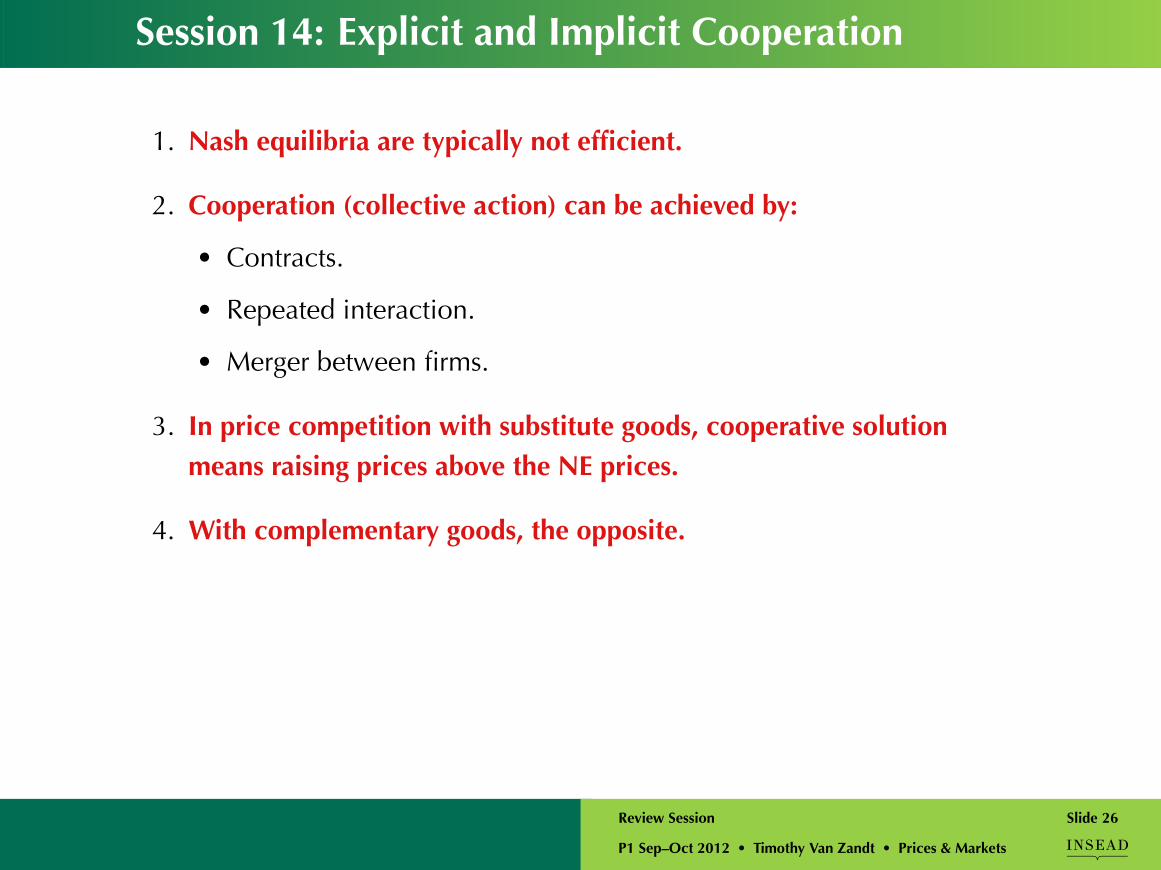

Session 14: Explicit and Implicit Cooperation

1. Nash equilibria are typically not efficient.

2. Cooperation (collective action) can be achieved by:

• Contracts.

• Repeated interaction.

• Merger between firms.

3. In price competition with substitute goods, cooperative solutionmeans raising prices above the NE prices.

4. With complementary goods, the opposite.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 26

Go back to our Airbus-Boeing example

Firms’ demand functions: QA = 60 − 3PA + 2PB

QB = 60 − 3PB + 2PA

Demand of merged firm:

Use hint that prices should be the same: Common value P .

Total demand Q = QA + QB as a function of P : Q = 120 − 2P .

Elasticity of demand at the NE prices?

What does this illustrate?

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 27

Session 15: Strategic Commitment

1. Sequential games and backward induction.

Life must be understood backward, but … it must be livedforward.

– Soren Kierkegaard

2. When you have the chance to commit, think about:

• In what way you want to influence the other players’ actions.

• How you can achieve this.

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 28

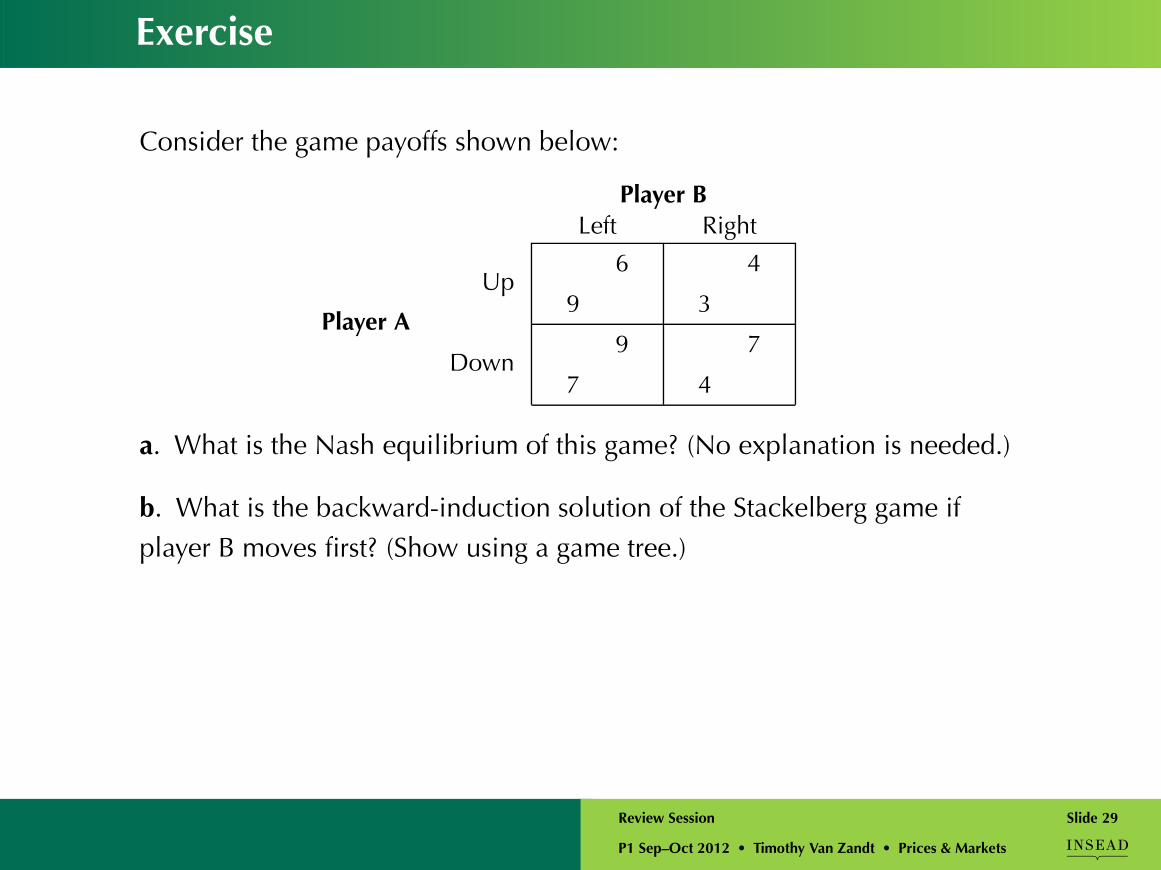

Exercise

Consider the game payoffs shown below:

Player BLeft Right

Up6

9

4

3Player A

Down9

7

7

4

a. What is the Nash equilibrium of this game? (No explanation is needed.)

b. What is the backward-induction solution of the Stackelberg game ifplayer B moves first? (Show using a game tree.)

P1 Sep–Oct 2012 • Timothy Van Zandt • Prices & Markets

Review Session Slide 29