Session 5 - Cost of Capital

49

Cost of Capital Spring / Summer 2007 BA 6323 Jeffrey Allen, Ph.D.

-

Upload

muhammad-hanafi -

Category

Documents

-

view

220 -

download

0

Transcript of Session 5 - Cost of Capital

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 1/49

Cost of Capital

Spring / Summer 2007

BA 6323

Jeffrey Allen, Ph.D.

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 2/49

Topics in this Section

Capital Market History

Measuring Risk in a Portfolio

Types of Risk Diversification & Portfolio Theory

Risk and Return Relationships

Measuring the Cost of Equity Capital Asset Pricing Model (CAPM) & Beta

Company-Specific Costs of Capital

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 3/49

A $1 Investment in 1900

$1

$10

$100

$1,000

$10,000

$100,000

1 9 0 0

1 9 1 0

1 9 2 0

1 9 3 0

1 9 4 0

1 9 5 0

1 9 6 0

1 9 7 0

1 9 8 0

1 9 9 0

2 0 0 0

D o l l a r s

Common Stock

US Govt Bonds

T-Bills

15,578

147

61

2 0 0 4

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 4/49

A $1 Investment in 1900

$1

$10

$100

$1,000

1 9 0 0

1 9 1 0

1 9 2 0

1 9 3 0

1 9 4 0

1 9 5 0

1 9 6 0

1 9 7 0

1 9 8 0

1 9 9 0

2 0 0 0

D o l l a r s

Equities

Bonds

Bills

719

6.81

2.80

2 0 0 4

Real Returns

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 5/49

Average Market Risk Premia

4.3 4.7 5.1 5.3 5.8 5.9 5.9 6.3 6.4 6.67.6 8.1 8.2 8.6

9.310

10.7

0

1

2

3

4

56

7

8

9

10

11

D e n m a r k

B e l g i u m

S w i t z e r l a n

d

S p a i n

C a n a d a

I r e l a n d

G e r m a n

y

U K

A v e r a g

e

N e t h e r l a n d

s

U S A

S w e d e n

S o u t h A f r i c

a

A u s t r a l i

a

F r a n c

e

J a p a n

I t a l

y

Risk premium, %

Country

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 6/49

Rates of Return 1900-2003

Source: Ibbotson Associates

-60%

-40%

-20%

0%

20%

40%

60%

80%

1900 1920 1940 1960 1980 2000

Year

P e r c e n t a g e R e t u r n

Stock Market Index Returns

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 7/49

Market Performance

1 1

4

1012

19

15

24

13

32

0

4

8

12

16

20

24

- 5 0 %

t o - 4 0 %

- 4 0 %

t o - 3 0 %

- 3 0 %

t o - 2 0 %

- 2 0 %

t o - 1 0 %

- 1 0 %

t o 0 %

0 %

t o 1 0 %

1 0 %

t o 2 0 %

2 0 %

t o 3 0 %

3 0 %

t o 4 0 %

4 0 %

t o 5 0 %

5 0 %

t o 6 0 % Return %

# of Years Histogram of Annual Stock Market Returns

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 8/49

Types of risk

Unique Risk (also called “diversifiable risk”):

Unique risk associated with the assets owned by the company

Industry risks, e.g. competition, innovation, R&D dependence, etc.

Risk related to outstanding debt (financial leverage)

Age, size and stability of the organization

Market Risk (also called “systematic risk”):

Economic volatility

Inflation

Political or other events that impact stability or the value of assets

Changes in interest rates

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 9/49

Measuring Risk

Investors must be compensated for volatility (likelihood of incurring a loss) due to any of the risk factors on the previousslide

Total risk is measured by variance or standard deviation instock returns.

Unique risk, however, can be nearly completely eliminated

in a diversified portfolio

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 10/49

Portfolio Theory

Price changes vs. Normal distribution

Coca Cola - Daily % change 1987-2004

0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

-9 -7 -5 -3 -1 0 2 4 6 7

P r o p o r t i o n o f D

a y s

% daily change

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 11/49

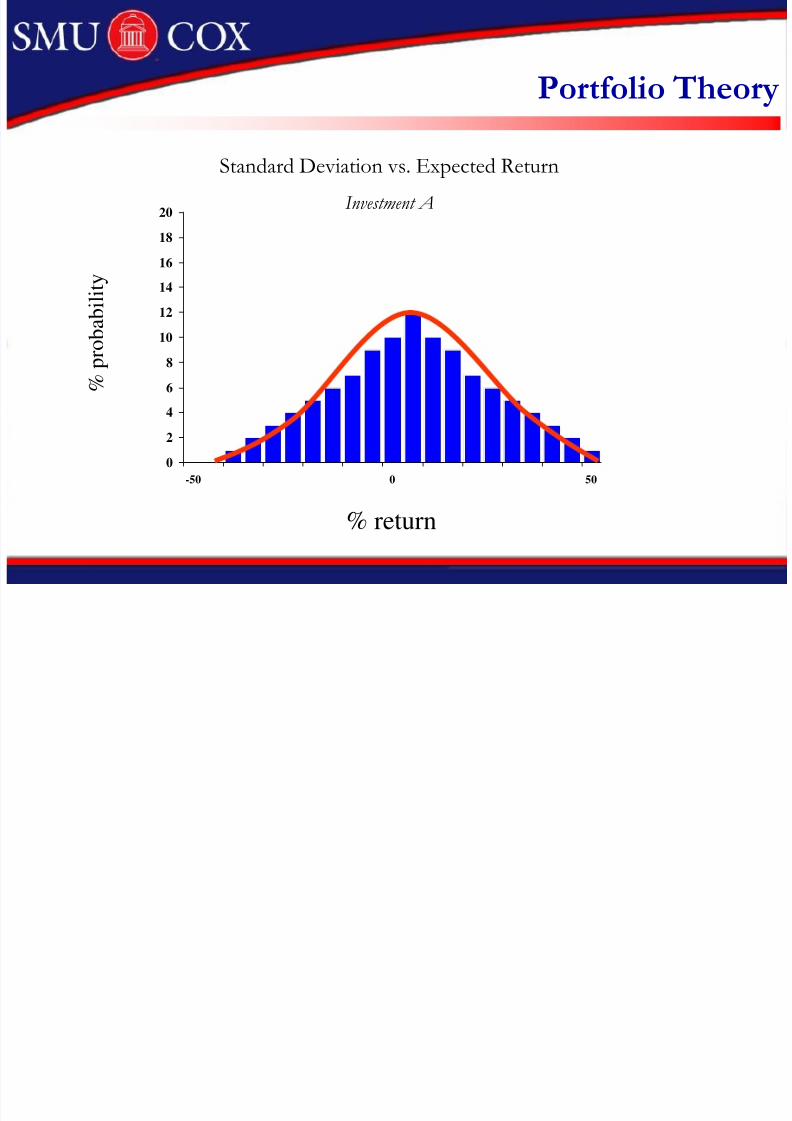

Portfolio Theory

Standard Deviation vs. Expected Return

Investment A

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

% p

r o b a b i l i t y

% return

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 12/49

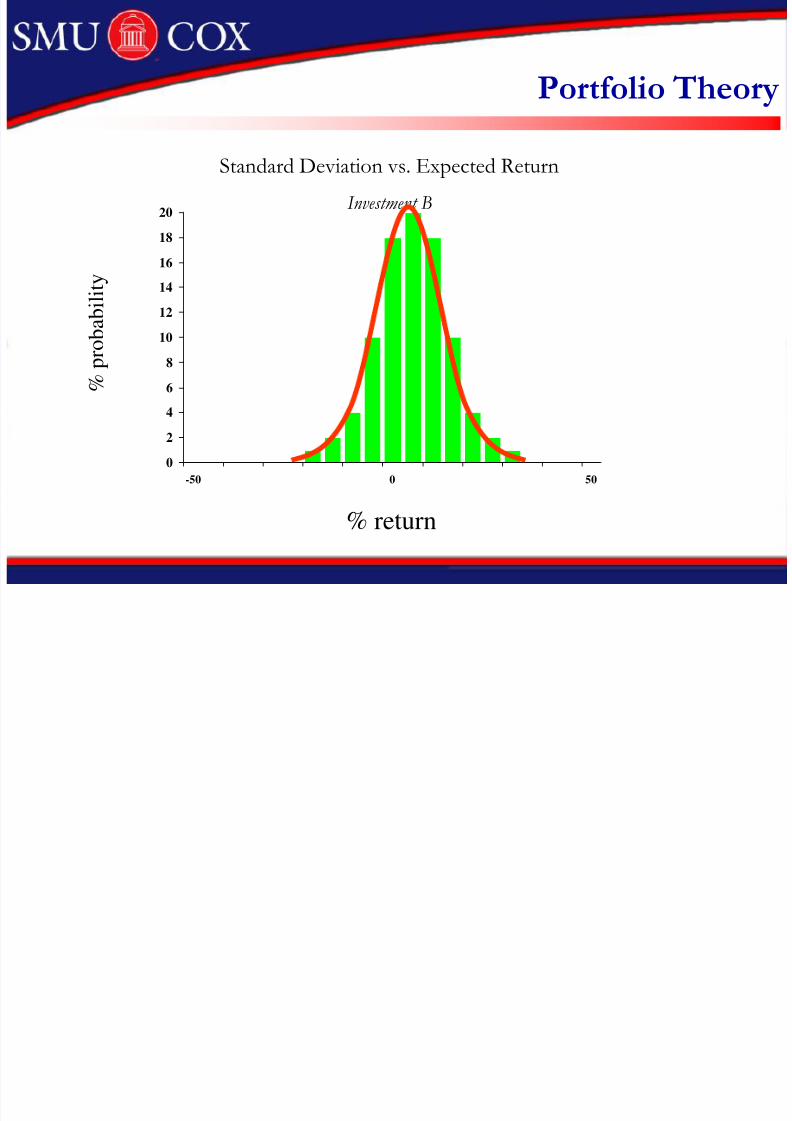

Portfolio Theory

Standard Deviation vs. Expected Return

Investment B

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

% p

r o b a b i l i t y

% return

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 13/49

Portfolio Theory

Standard Deviation vs. Expected Return

Investment C

0

2

4

6

8

10

12

14

16

18

20

-50 0 50

% p

r o b a b i l i t y

% return

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 14/49

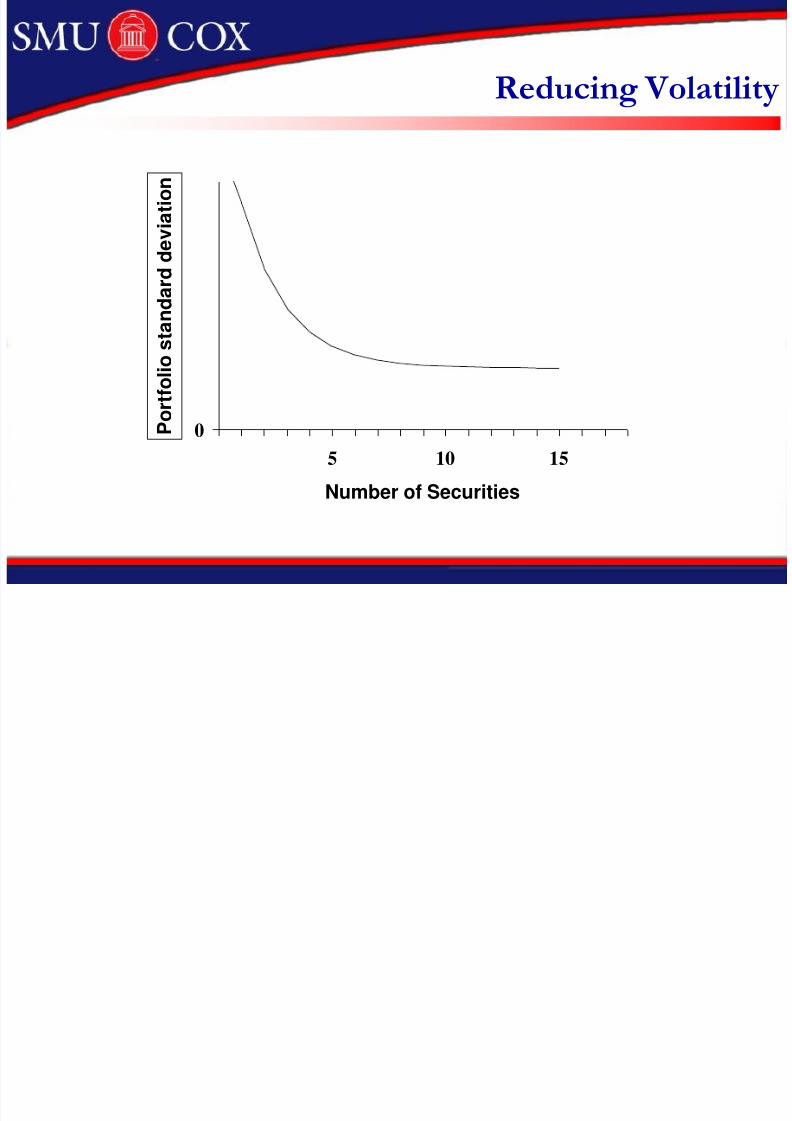

Portfolio Theory

Combining stocks into portfolios reduces the portfoliostandard deviation below the weighted average of theindividual stocks.

Covariance (also measured by correlation coefficient)between assets makes this possible.

The various weighted combinations of stocks that create

this standard deviations constitute the set of “efficientportfolios” or efficient frontier.

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 15/49

Expected Return on a Portfolio

22

11

rasset,secondon

returnof ratex

wasset,secondin

portfolioof fraction+

rasset,firston

returnof ratex

wasset,firstin

portfolioof fraction=

returnof

rate Portfolio

((

(

()) ))

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 16/49

Measuring Risk

Calculating variance and standard deviation

Excel formulas: = var(…), =stdev(…)

21.2%=450=varianceof rootsquare=deviationStandard

450=1800/4=deviationssquaredof average=Variance

90030-20-

0010+

0010+

90030+40+

DeviationSquaredMeanfromDeviationReturnof tePercent Ra

(3)(2)(1)

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 17/49

Reducing Volatility

0

5 10 15

Number of Securities

P o r t f o l i o

s t a n d a r d

d e v i a t i o n

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 18/49

Diversification

0

5 10 15

P o

r t f o l i o

s t a n d a r d

d e v i a t i o n

Market risk

Unique

risk

Number of Securities

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 19/49

Portfolio Risk

2

2

2

2211221

1221

211221

12212

1

2

1

σwσσρww

σww2Stock

σσρww

σwwσw1Stock

2Stock 1Stock

The total variance of a two stock portfolio is the sum of

these four boxes

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 20/49

Portfolio Risk

)rw()r(wReturnPortfolioExpected 2211

)σσρww(2σwσwVariancePortfolio211221

2

2

2

2

2

1

2

1

Weighted average of expected returns

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 21/49

Portfolio Risk Example

Example

Suppose you invest 40% of your portfolio in

Exxon Mobil and 60% in Coca Cola. The

expected return on your Exxon Mobil stock is 15%

and 10% on Coca Cola. Your portfolio expected

return is:

%0.12)10.60(.)15.40(.ReturnExpected

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 22/49

Portfolio Risk

222

2

2

2

211221

211221222

1

2

1

)167(.)60(.σw167.224.6.

60.40.σσρwwCola-Coca

167.224.6.x

60.40.σσρww)224(.)40(.σwMobil-Exxon

KOXOM

Example

Suppose you invest 40% of your portfolio in Exxon Mobil (XOM) and 60% in

Coca Cola (KO). The expected return on XOM is 15% and 10% on KO. The

historical standard deviation of their annualized daily returns are 22.4%

and 16.7%, respectively. Assume a correlation coefficient of 0.6 and

calculate the portfolio variance (see XL solution).

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 23/49

Efficient Frontier

Return

Risk

Low Risk

High Return

High Risk

High Return

Low Risk

Low Return

High Risk

Low Return

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 24/49

Efficient Frontier

Standard Deviation

Expected Return (%)

•Each half egg shell represents the possible weighted combinations for twostocks.

•The composite of all stock sets constitutes the efficient frontier

Efficient Frontier

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 25/49

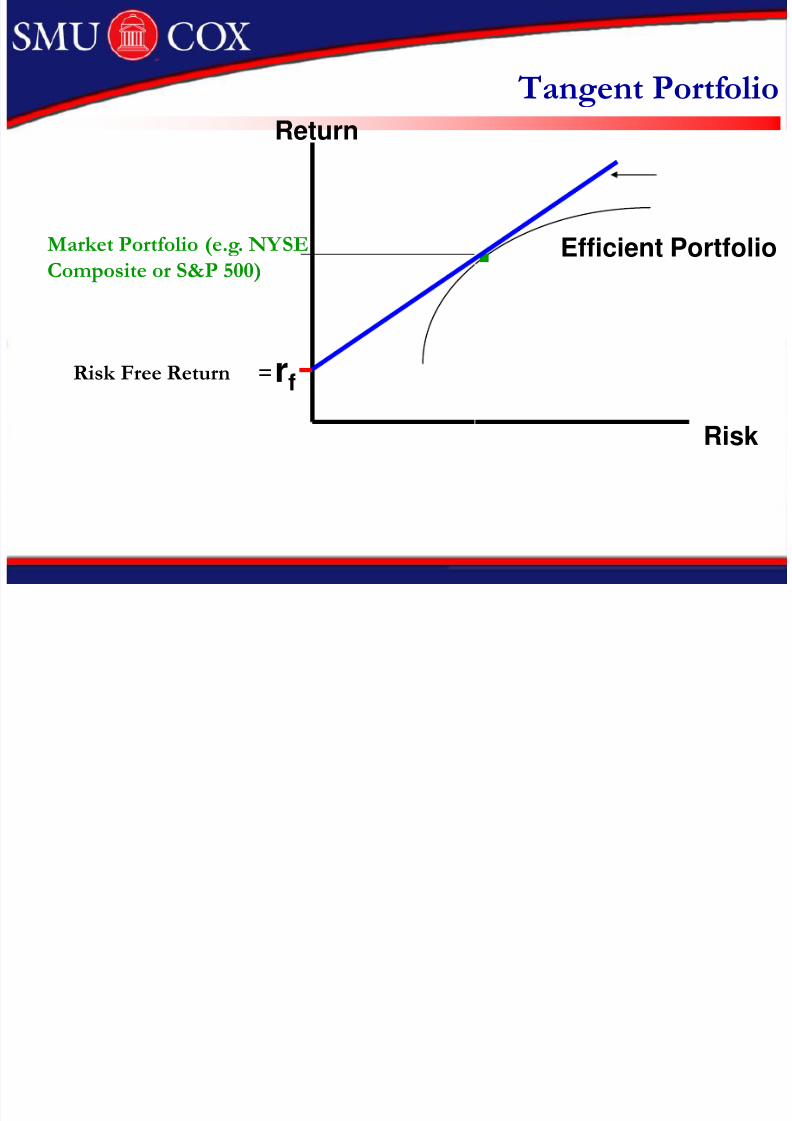

Tangent Portfolio

Return

Risk

.

rfRisk Free Return =

Efficient PortfolioMarket Portfolio (e.g. NYSE

Composite or S&P 500)

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 26/49

New Efficient Frontier

Standard Deviation

Expected Return (%)

Lending or Borrowing at the risk free rate (rf ) allows us to exist outside the

efficient frontier.

rf

T

T = tangent point to the market portfolio

“New” Efficient Frontier (SML)

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 27/49

Lending vs. Borrowing

The optimal investment (highest risk / reward ratio) lieson the security market line – a combination of the risk-

free asset and the market portfolio.

An investor can invest more than 100 percent of his or her wealth by borrowing (margin) and increasing both risk andexpected return.

An investor wanting less risk would split his or herinvestments between risk-free assets and the marketportfolio (lending portion of SML).

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 28/49

Security Market LineReturn

BETA

rf

1.0 = market

SML

SML Equation = rf + B ( rm - rf )

Slope = Beta

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 29/49

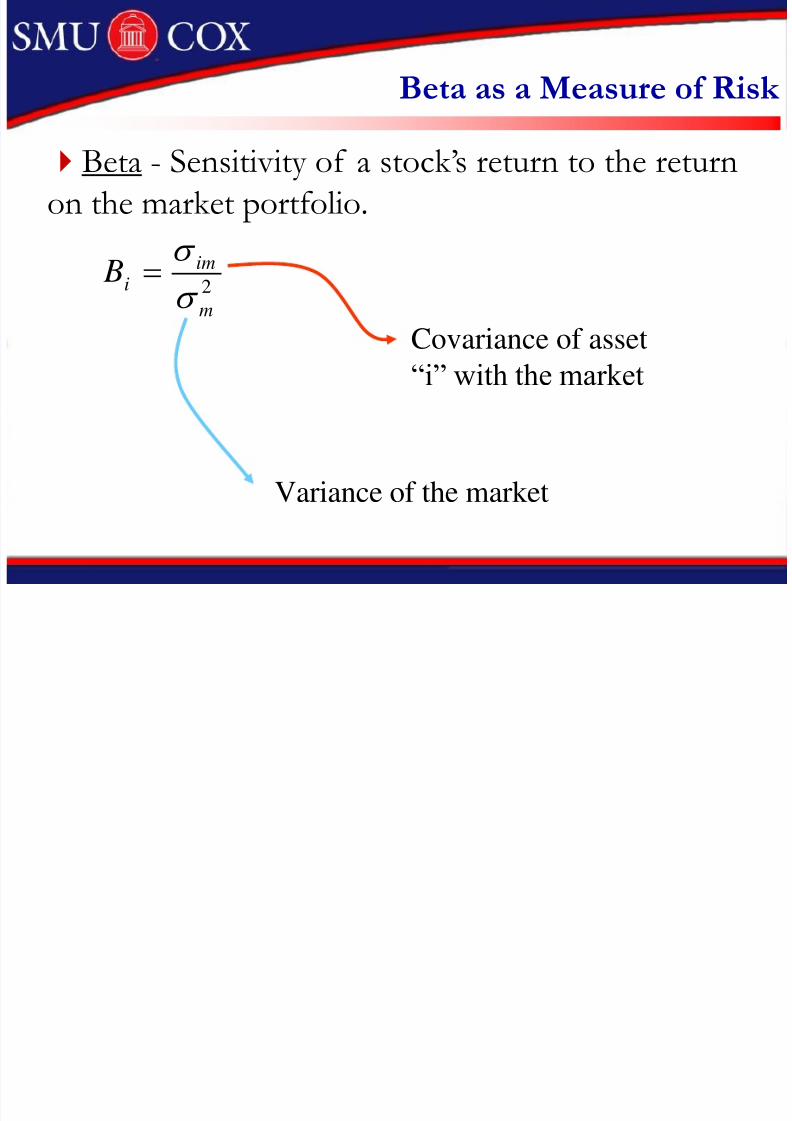

Beta as a Measure of Risk

2

m

im

i B

Covariance of asset

“i” with the market

Variance of the market

Beta - Sensitivity of a stock’s return to the return

on the market portfolio.

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 30/49

Measuring Beta

Dell Computer

Slope determined from plotting the

line of best fit.

Price data: May 91- Nov 97

Market return (%)

D e l l r e t u

r n ( % ) R2 = .10

B = 1.87

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 31/49

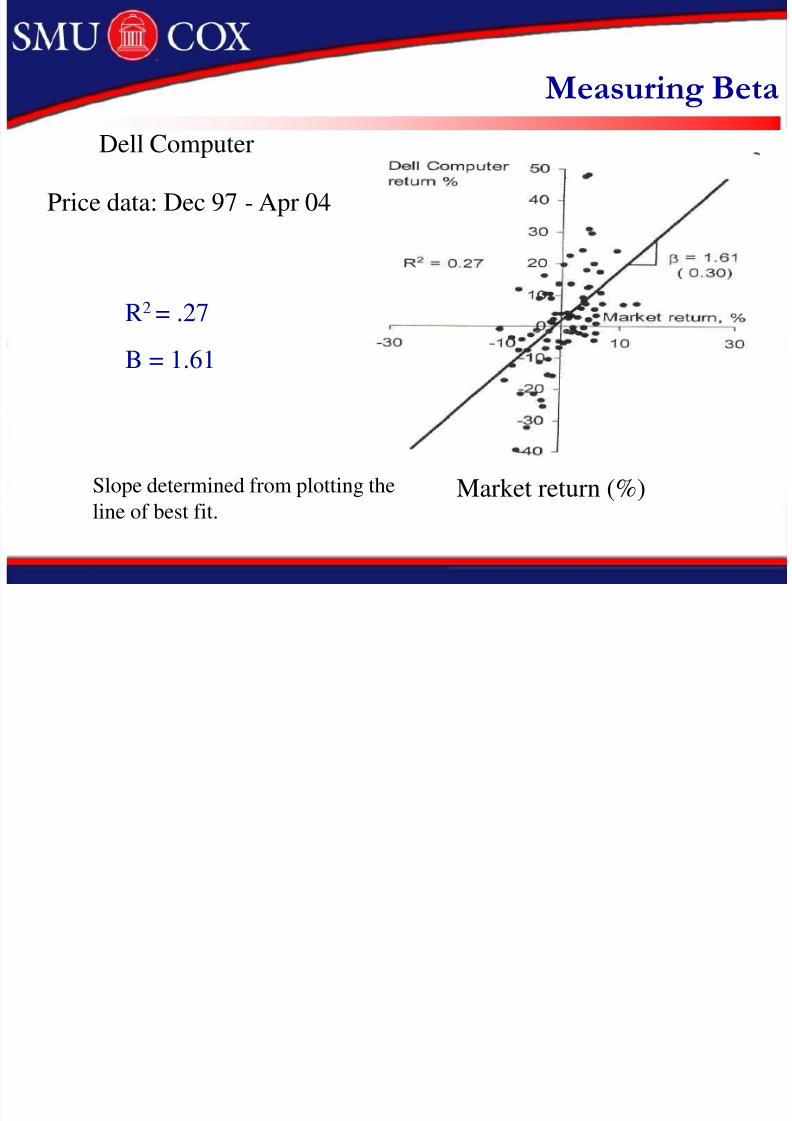

Measuring Beta

Dell Computer

Slope determined from plotting the

line of best fit.

Price data: Dec 97 - Apr 04

Market return (%)

D e l l r e t u

r n ( % ) R2 = .27

B = 1.61

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 32/49

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 33/49

Measuring Beta

General Motors

Slope determined from plotting the

line of best fit.Market return (%)

GM r e t u

r n ( % ) R2 = .29

B = 1.21

Price data: Dec 97 - Apr 04

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 34/49

Measuring Beta

Exxon Mobil

Slope determined from plotting the

line of best fit.Market return (%)

E xx onM

o b i l r e t ur n ( % )

R2 = .23

B = 0.57

Price data: May 91- Nov 97

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 35/49

Measuring Beta

Exxon Mobil

Slope determined from plotting the

line of best fit.Market return (%)

E xx onM

o b i l r e t ur n ( % )

R2 = .18

B = 0.51

Price data: Dec 97 - Apr 04

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 36/49

Security Market LineReturn

BETA

rf

1.0 = market

SML

SML Equation = rf + B ( rm - rf )

Slope = Beta

rm

“Market Risk Premium”

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 37/49

Capital Asset Pricing Model

R = rf + B ( rm - rf )

Capital Asset Pricing Model

(CAPM)

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 38/49

Market Risk Premium

The market risk premium is the expected return on themarket portfolio less the expected risk-free rate (rm – rf ).

The expected premium at this point in time (Jeff Allen’s

number..) is 6.0 percent.

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 39/49

Testing the CAPM

Avg Risk Premium1931-2002

Portfolio Beta1.0

SML30

20

10

rf

Investor

returns

MarketPortfolio

beta vs. average risk premium

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 40/49

Testing the CAPM

Avg Risk Premium1931-65

Portfolio Beta1.0

SML

30

20

10

rf

Investor

Returns

Market

Portfolio

beta vs. average risk premium

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 41/49

Testing the CAPM

Avg Risk Premium1966-2002

Portfolio Beta1.0

SML

30

20

10

rf

Investorreturns

Market

Portfolio

beta vs. average risk premium

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 42/49

CAPM and Cost of Capital

Let’s first assume that the company is financed solely with

equity.

A firm’s value can be stated as the sum of the value of its

various assets

etc.PV(B),PV(A)PV(AB)valueFirm

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 43/49

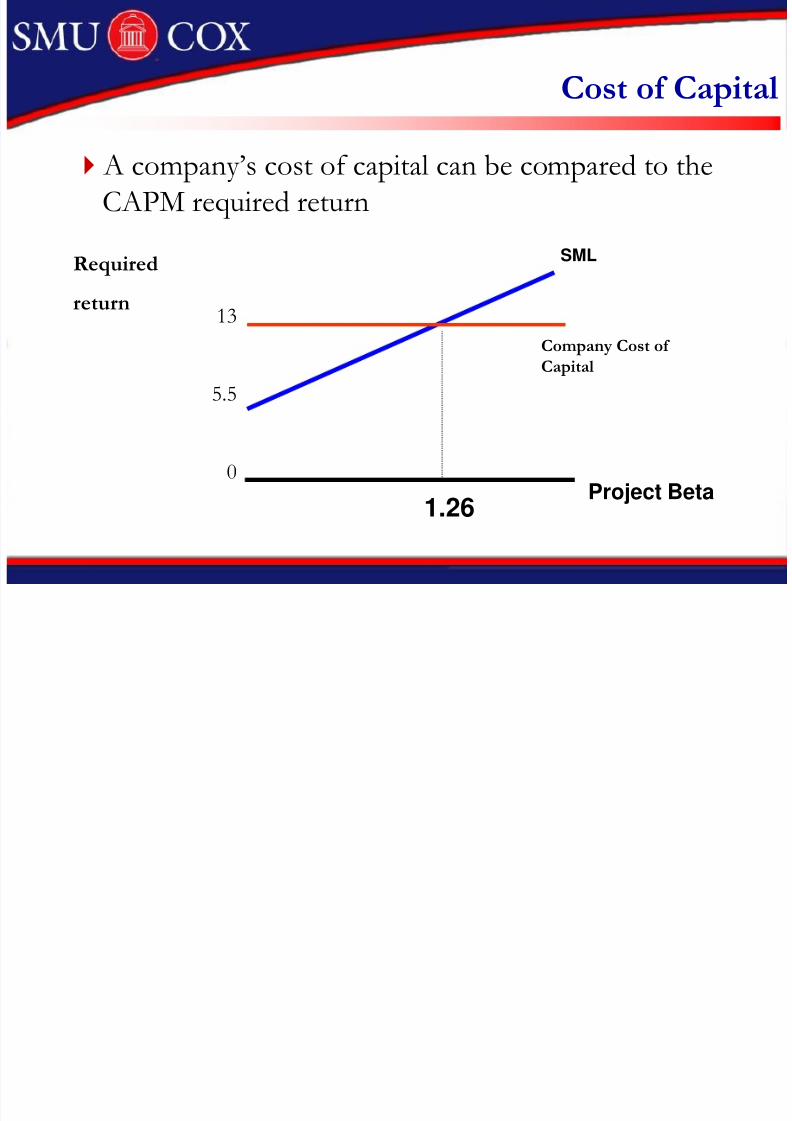

Cost of Capital

A company’s cost of capital can be compared to the

CAPM required return

Required

return

Project Beta1.26

Company Cost of

Capital

13

5.5

0

SML

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 44/49

Cost of Capital

10%ytechnologknownt,improvemenCost

COC)(Company12.5%businessexistingof Expansion

20%productsNew

30%VentureseSpeculativ

RateDiscountEst.Category

Adjustments to the required return areoften ad hoc…we can do better

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 45/49

Calculating the cost of capital

Cost of Debt: After-tax yield of outstanding debt

rdebt = avg. yield to maturity

Cost of Equity: Risk-free rate + risk premium

requity = risk-free rate + beta (market risk premium)

WACC: rdebt (1-t)(D/V) + requity (E/V) where V = D (total value of debt) + E (market value of equity)

(we use market values for the weights if available)

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 46/49

Cost of capital (example)

Suppose a firm has $3M debt outstanding yielding 8.5percent. The stock price is $35 and the firm has 200,000shares outstanding. The equity beta of the firm is 1.25,

the current risk-free rate is 5 percent. Assume the risk premium for holding the market portfolio is expected tobe 6 percent. At a tax rate of 34 percent, what is thecost of capital?

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 47/49

T. Medical Cost of Capital

Example: Technol Medical has 1M shares of stock outstanding which currently trade at $12 per share. Thecompany also has 100,000 shares of preferred stock

outstanding which pay a $3 dividend and currently trade at$21.38 per share. The firm has publicly traded bonds with10 years remaining to maturity, 10% coupon payments, atotal face value of $5M which currently trade at $985 per

bond. The equity beta is estimated at 1.2, the risk-free rateis seven percent, t = 34%, and the market risk premium issix percent. What is the WACC for T.Medical?

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 48/49

Nike, Inc. : Cost of Capital Case

Read through Exhibits 1-5 in the case

In groups of two, calculate the WACC for Nikeindependently of the analysis by Ms. Cohen

Note any improvements you would make to Ms. Cohen’sanalysis

8/4/2019 Session 5 - Cost of Capital

http://slidepdf.com/reader/full/session-5-cost-of-capital 49/49

PepsiCo Inc.: Cost of Capital

How has the company performed over the past 10 years?

How have the segments performed?

What is your estimate of the cost of capital for eachdivision of the company (soft drinks, restaurants & snack foods)