Session 47 PD, Accelerated Underwriting and … 47 PD, Accelerated Underwriting and Simplified Issue...

46

Session 47 PD, Accelerated Underwriting and Simplified Issue/New Underwriting Moderator: Richard J. Tucker, FSA, MAAA Presenters: Gregory A. Brandner, FSA, MAAA Michael David Hoyer, FSA, MAAA Mark Andrew Sayre, ASA, CERA, MAAA

Transcript of Session 47 PD, Accelerated Underwriting and … 47 PD, Accelerated Underwriting and Simplified Issue...

Session 47 PD, Accelerated Underwriting and Simplified Issue/New Underwriting

Moderator:

Richard J. Tucker, FSA, MAAA

Presenters: Gregory A. Brandner, FSA, MAAA Michael David Hoyer, FSA, MAAA

Mark Andrew Sayre, ASA, CERA, MAAA

Accelerated Underwriting - Where we started- Where we are today- Where we’re going

Society of Actuaries Life & Annuity Symposium - May, 2016

Gregory Brandner, FSA, MAAAAssistant Vice President & Actuary

A Few Broad Observations

The market is evolving, and the pace of change is accelerating

We continue to move closer to fully underwritten mortality (progress, not perfection)

Use of BIG DATA may be a game-changer

2

How do we measure progress?

Customer experience (UW requirements, processing time, premium rates, . . .)

Target market

Issue Ages

Face Amounts

Preferred Classes

Automation

Products

Mortality

3

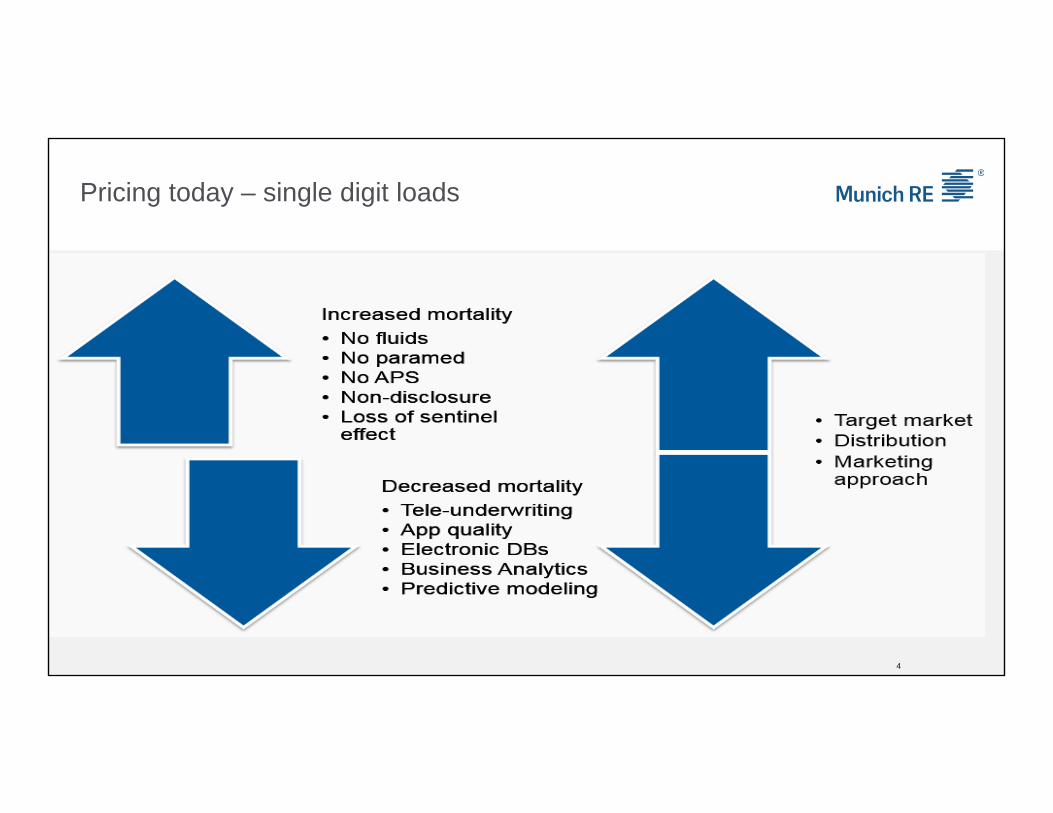

Pricing today – single digit loads

4

Current Medical Underwriting

5

Distribution by risk class

Super Preferred 30.0%Preferred 40.0%Standard 20.0%

Substandard 7.0%Decline 3.0%Overall 100.0%

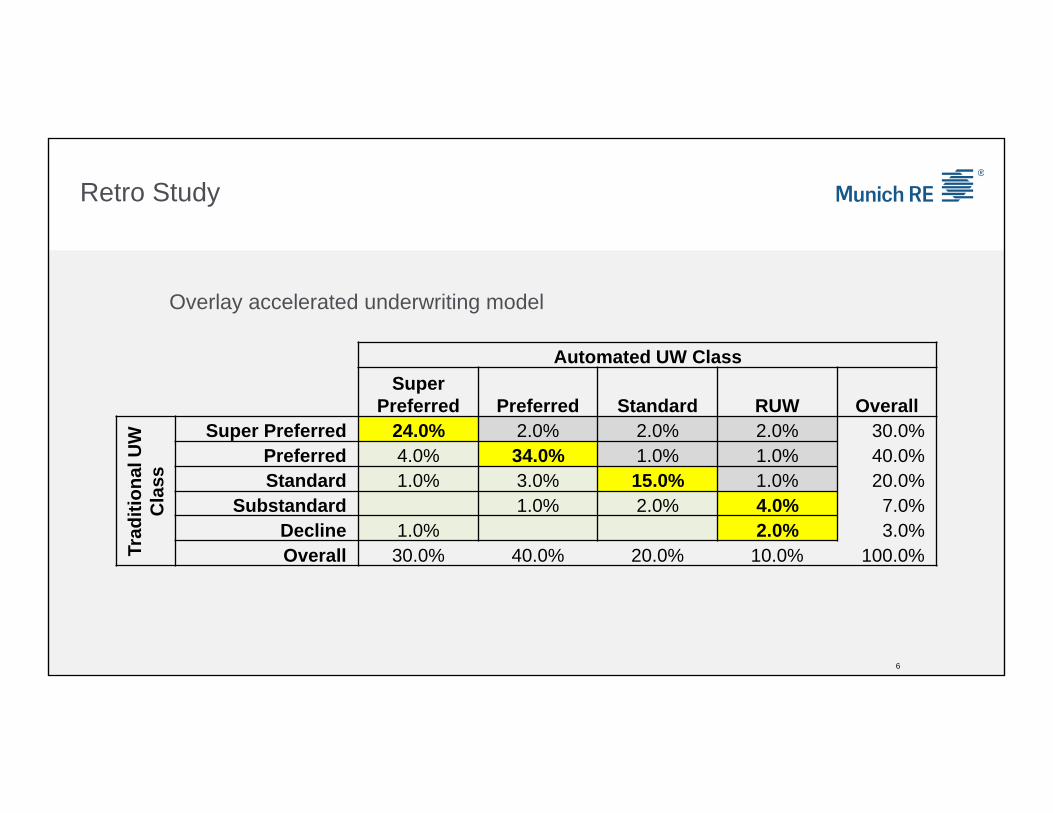

Retro Study

6

Overlay accelerated underwriting model

Automated UW ClassSuper

Preferred Preferred Standard RUW Overall

Trad

ition

al U

W

Cla

ss

Super Preferred 24.0% 2.0% 2.0% 2.0% 30.0%Preferred 4.0% 34.0% 1.0% 1.0% 40.0%Standard 1.0% 3.0% 15.0% 1.0% 20.0%

Substandard 1.0% 2.0% 4.0% 7.0%Decline 1.0% 2.0% 3.0%Overall 30.0% 40.0% 20.0% 10.0% 100.0%

Retro Study

7

Normalized to exclude “defectors”

Automated UW ClassSuper

Preferred Preferred Standard RUW Overall

Trad

ition

al U

W

Cla

ss

Super Preferred 26.4% 26.4%Preferred 4.4% 37.4% 41.8%Standard 1.1% 3.3% 16.5% 20.9%

Substandard 1.1% 2.2% 4.4% 7.7%Decline 1.1% 2.2% 3.3%Overall 33.0% 41.8% 18.7% 6.6% 100.0%

Retro Study

8

Relative Mortality

Automated UW ClassSuper

Preferred Preferred Standard RUW Overall

Trad

ition

al U

W

Cla

ss

Super Preferred 100.0% 80.0%Preferred 115.0% 100.0% 92.0%Standard 150.0% 130.4% 100.0% 120.0%

Substandard 218.8% 190.2% 145.8% 100.0% 175.0%Decline 1000.0% 100.0% 800.0%Overall 133.7% 104.8% 105.4% 100.0% 114.1%

Automated UW ClassSuper

Preferred Preferred Standard RUW Overall

Trad

ition

al U

W

Cla

ss

Super Preferred 100.0% 80.0%Preferred 115.0% 100.0% 92.0%Standard 150.0% 130.4% 100.0% 120.0%

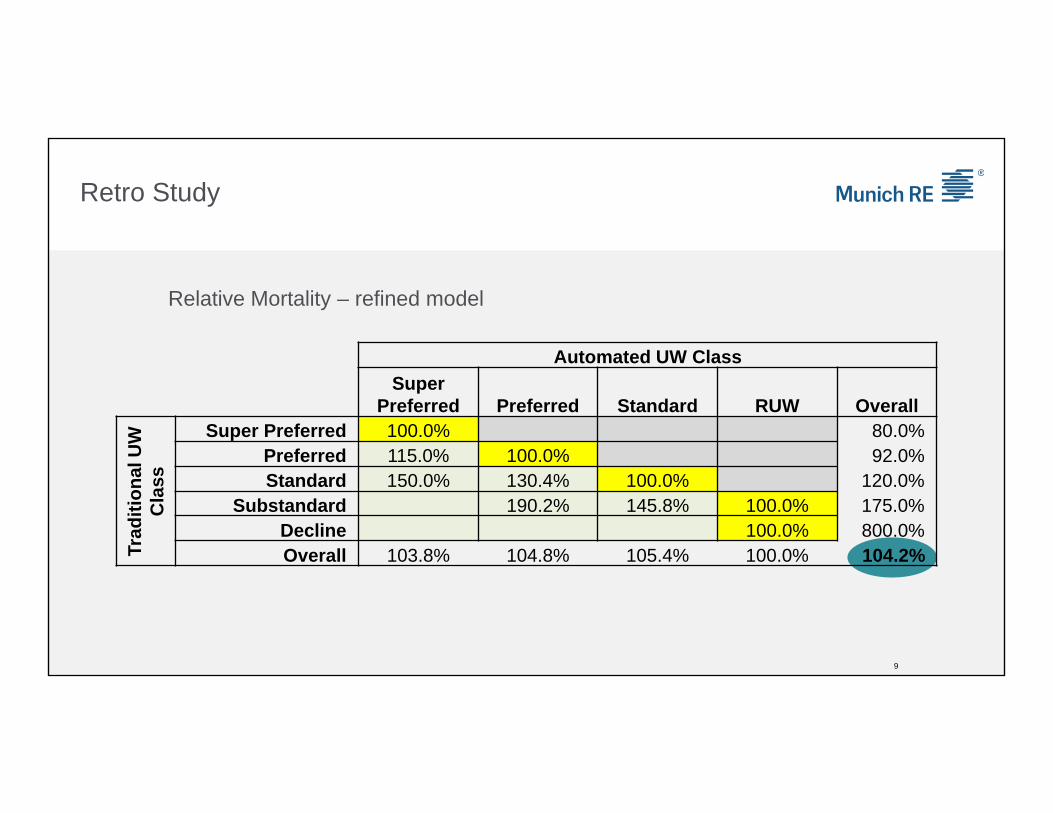

Substandard 190.2% 145.8% 100.0% 175.0%Decline 100.0% 800.0%Overall 103.8% 104.8% 105.4% 100.0% 104.2%

Retro Study

9

Relative Mortality – refined model

Self-reporting Full disclosure

Height and weight

Cryptic smokers

Avocations

Family history

Medical history

10

“Survey Shows Many Americans Fine with Lying to the IRS, or Their Insurer”

One-in-five people surveyed said it is acceptable to lie about the number of miles driven each year to receive lower auto insurance rates

16 percent of Americans believe it’s acceptable to lie about smoking marijuana to receive lower life insurance rates

Eleven percent of respondents say it is acceptable to lie about tobacco smoking habits to receive lower life insurance rates

P.S. 24 percent of people are OK with withholding information about extra income from the IRS

11

February 2016 survey conducted by NerdWallet

Smoking Prevalence - Nondisclosure

2013 study published in the Journal of Insurance Medicine:19.3% of life insurance applicants who tested positive for cotinine self-reported as non-tobacco users

Impact on Mortality (example)

Fully Underwritten program: 80% non-tobacco; 20% tobacco

Accelerated Underwriting program:

• 1 out of 5 tobacco users does not disclose their tobacco use

• 84% “non-tobacco”; 16% tobacco

• Assume tobacco mortality is 200% of non-tobacco

“Non-Tobacco” mortality will increase by 4.8% due to nondisclosure

12

And… questions everywhere

What’s the value of labs? What’s the impact of Rx, MVR, and MIB? Is there value in a tele-interview? How do I blend requirements to achieve pricing metrics and the desired customer experience? What’s the protective value of a new data source?

I’m being approached by a startup telling me that shoe size and choice of footwear predicts mortality. How do I assess?

Can I use it this new data source in making an underwriting decision?

How far can I go in using data in my target marketing?

How do I quantify the impact of a predictive model? Will Electronic Health Records solve all my problems?

13

The future of accelerated underwriting:A few thoughts, observations, and predictions

Easy to hypothesize on how it should be done; not nearly so easy to do

New data sources will help

• Wearable devices

• The Internet of Things

• Electronic Health Records

Predictive modeling

Effective use of Business Analytics is essential

Some distribution channels work better than others

Be prepared to make adjustments – you won’t get it right the first time

14

The future of accelerated underwriting:A few thoughts, observations, and predictions

Predictions:

As an industry we will get to fully underwritten pricing using accelerated underwriting

If we don’t figure it out, somebody else will

(i.e. watch out for Google and Amazon)

15

Thank you for your attention

1

Proprietary and Confidential.

Prescription for Success in Accelerated Underwriting

SOA Life & Annuity Symposium Session 47May 17, 2016

Mike Hoyer, FSA, MAAA

2

Proprietary and Confidential.

Agenda

How does Rx work

Mortality implications

Rx rules engines and predictive models

Assessing protective value

3

Proprietary and Confidential.

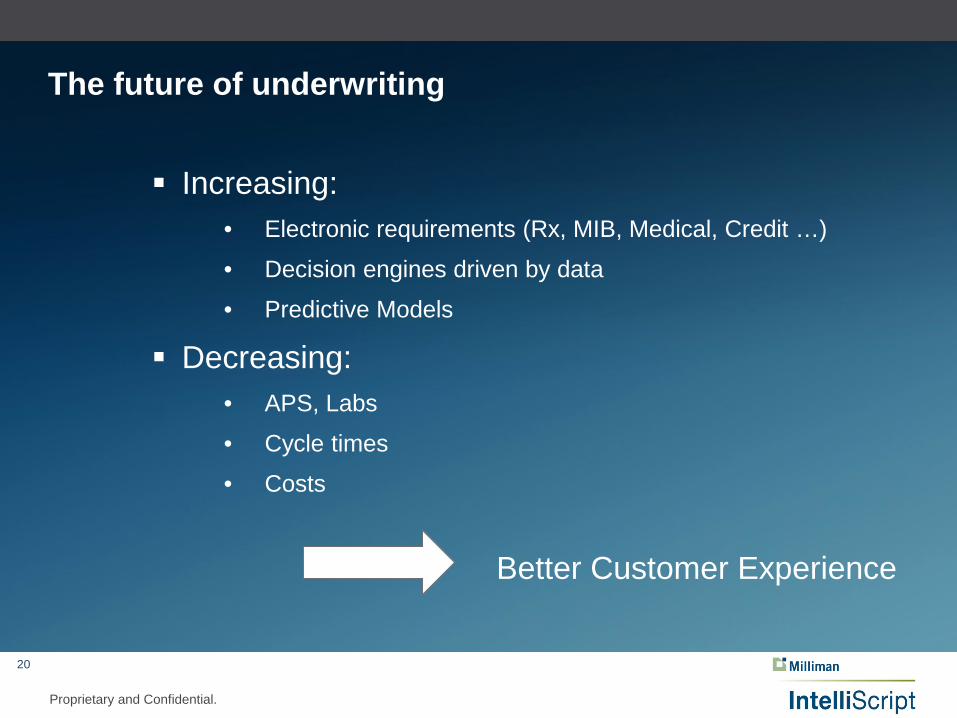

The future of underwriting

Increasing:• Electronic requirements (Rx, MIB, Medical, Credit …)

• Decision engines driven by data

• Predictive Models

Decreasing:• APS, Labs

• Cycle times

• Costs

Better Customer Experience

4

Proprietary and Confidential.

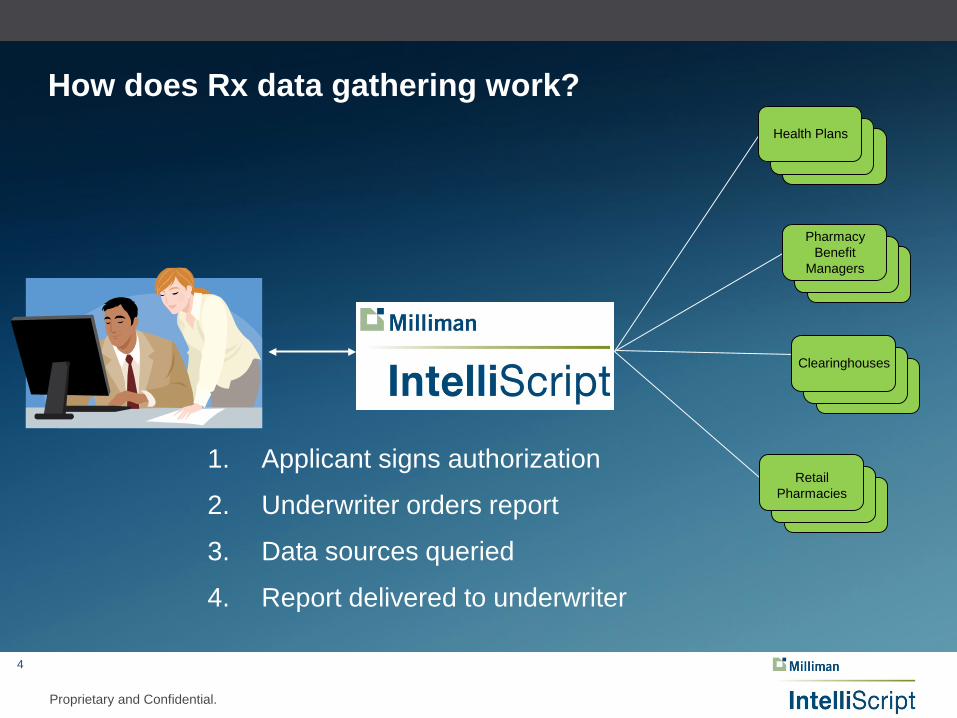

How does Rx data gathering work?

Pharmacy Benefit

Managers

Clearinghouses

Retail Pharmacies

Health Plans

1. Applicant signs authorization

2. Underwriter orders report

3. Data sources queried

4. Report delivered to underwriter

5

Proprietary and Confidential.

Rx history query information Prescription

• Brand and generic name• Dosage and quantity• Date of fill

Physician• Specialty• Contact information

Pharmacy• Contact information

Dates of eligibility

With or without prescriptions

Underwriting significance indicator (risk score)

6

Proprietary and Confidential.

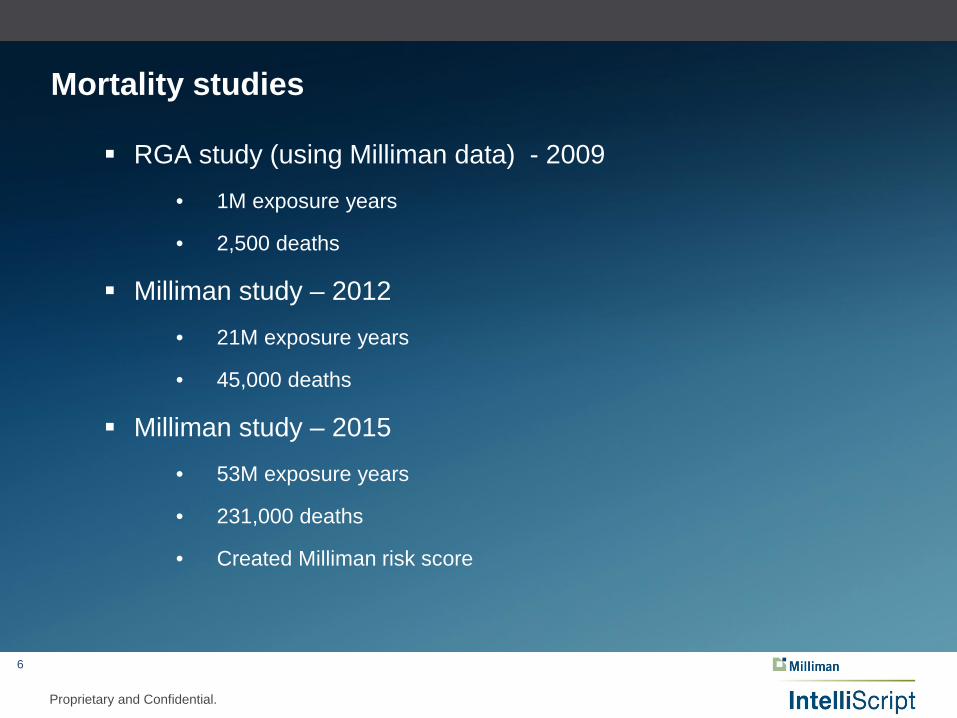

Mortality studies

RGA study (using Milliman data) - 2009

• 1M exposure years

• 2,500 deaths

Milliman study – 2012

• 21M exposure years

• 45,000 deaths

Milliman study – 2015

• 53M exposure years

• 231,000 deaths

• Created Milliman risk score

7

Proprietary and Confidential.

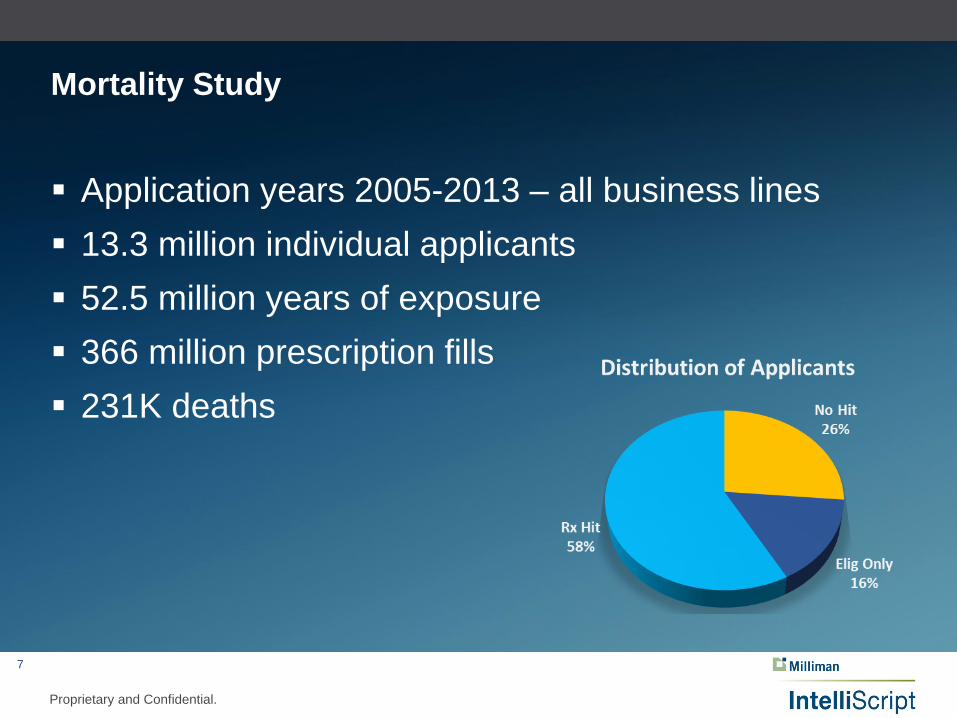

Mortality Study

Application years 2005-2013 – all business lines 13.3 million individual applicants 52.5 million years of exposure 366 million prescription fills 231K deaths

8

Proprietary and Confidential.

Relative mortality - hit status

9

Proprietary and Confidential.

Relative mortality – hit status by age

10

Proprietary and Confidential.

Relative mortality by red fill count

11

Proprietary and Confidential.

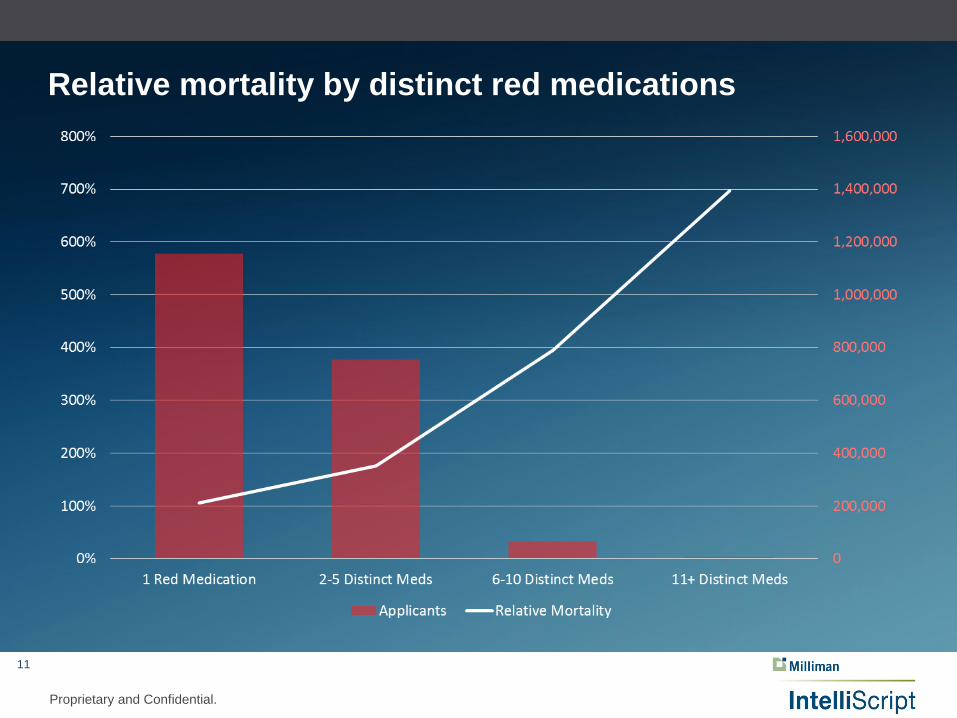

Relative mortality by distinct red medications

12

Proprietary and Confidential.

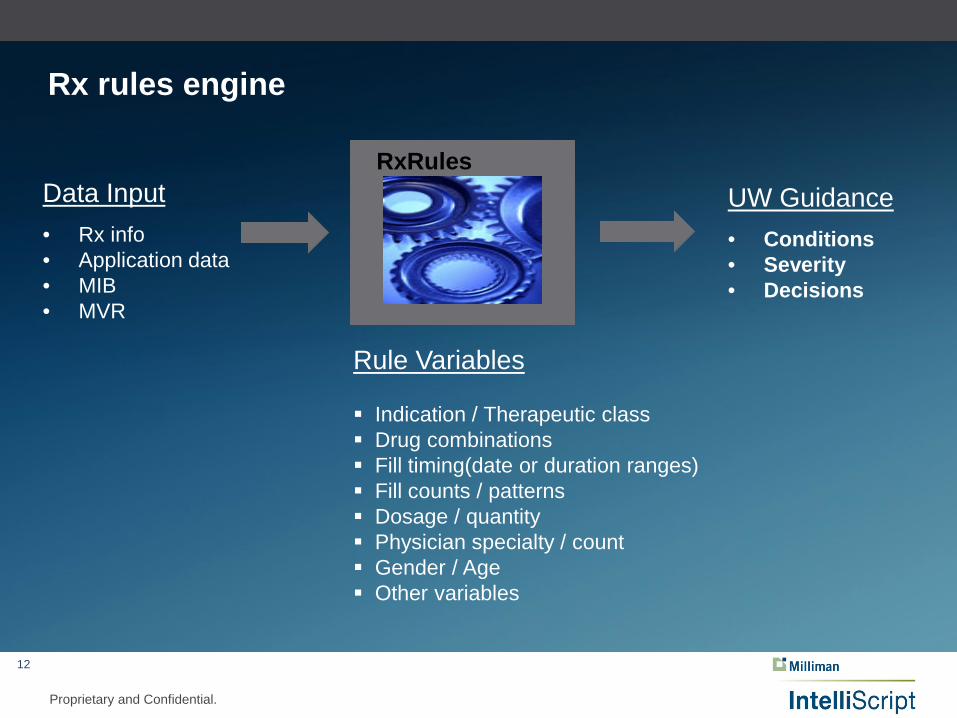

Rx rules engine

UW Guidance• Conditions• Severity• Decisions

Data Input• Rx info• Application data• MIB • MVR

RxRules

Rule Variables

Indication / Therapeutic class Drug combinations Fill timing(date or duration ranges) Fill counts / patterns Dosage / quantity Physician specialty / count Gender / Age Other variables

13

Proprietary and Confidential.

Benefits of Rx rules engine

Consistency

Efficiency

Decisions

Evidence

14

Proprietary and Confidential.

RxRules – timing and duration matters.

Corticosteroids105% relative mortality

Low frequency/duration99%

High frequency/duration201%

Corticosteroids are very common among insurance applicants

15

Proprietary and Confidential.

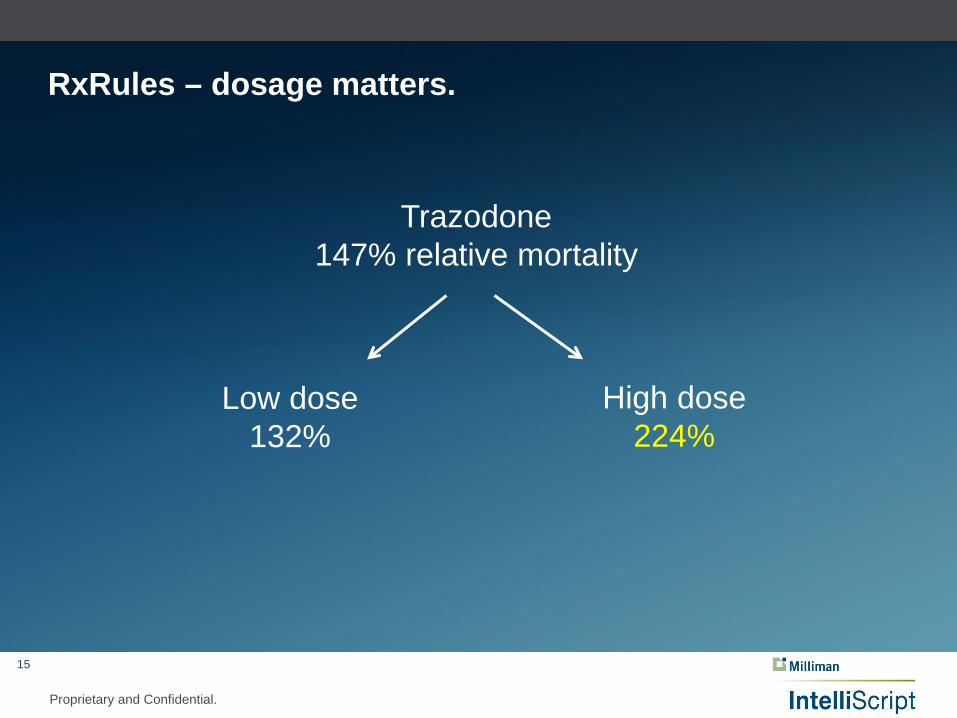

RxRules – dosage matters.

Trazodone147% relative mortality

Low dose132%

High dose224%

16

Proprietary and Confidential.

RxRules – drug combinations matter.

Spironolactone 209% relative mortality

With 2 out of 3 of:

Thiazide Diuretics (102%)Ace / Angio II (ARBS) (116%)Beta Blocker (122%)

328%

Without 2 out of 3 of:

Thiazide Diuretics (102%)Ace / Angio II (ARBS) (116%)Beta Blocker (122%)

166%

17

Proprietary and Confidential.

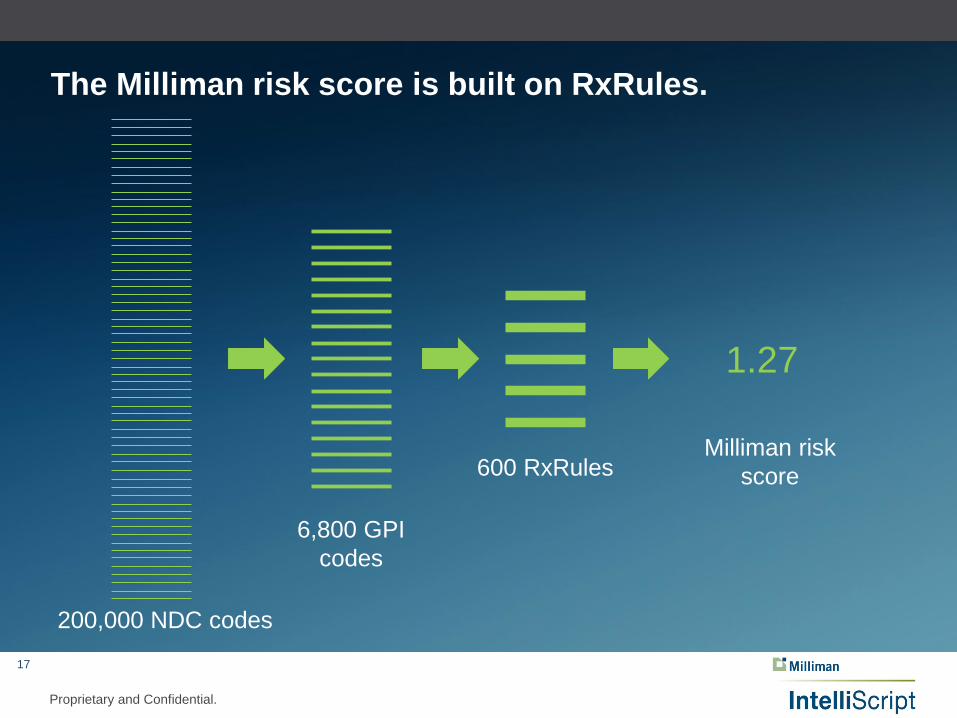

The Milliman risk score is built on RxRules.

Milliman risk score

200,000 NDC codes

6,800 GPI codes

600 RxRules

1.27

18

Proprietary and Confidential.

Milliman’s risk score predicts mortality.

19

Proprietary and Confidential.

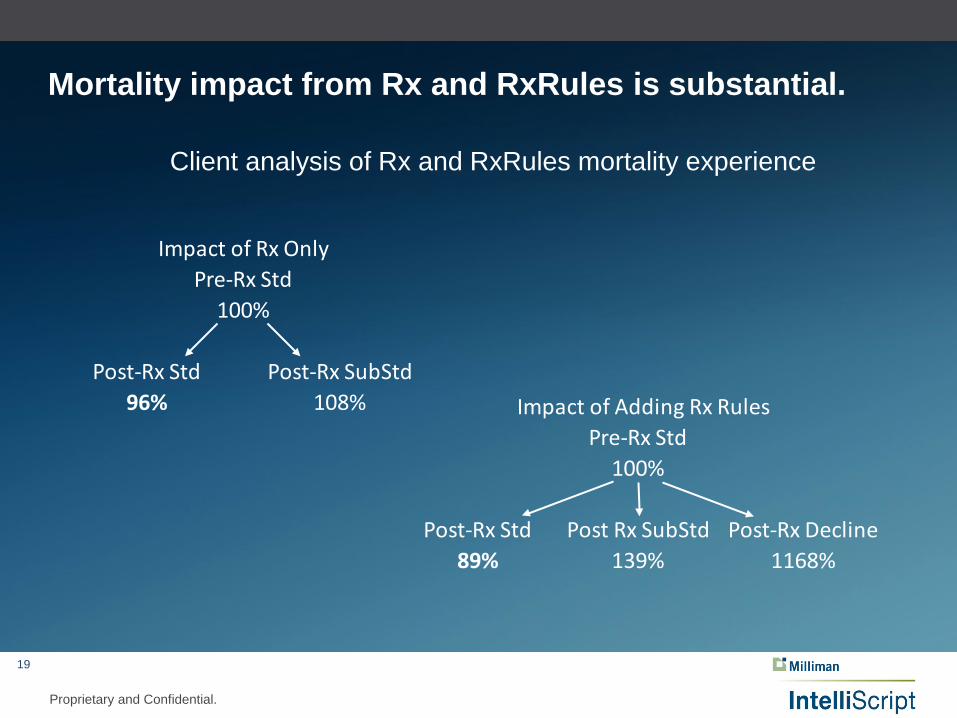

Mortality impact from Rx and RxRules is substantial.

Client analysis of Rx and RxRules mortality experience

Pre-Rx Std100%

Post-Rx Std Post-Rx SubStd96% 108%

Impact of Rx Only

Pre-Rx Std100%

Post-Rx Std Post Rx SubStd Post-Rx Decline89% 139% 1168%

Impact of Adding Rx Rules

20

Proprietary and Confidential.

The future of underwriting

Increasing:• Electronic requirements (Rx, MIB, Medical, Credit …)

• Decision engines driven by data

• Predictive Models

Decreasing:• APS, Labs

• Cycle times

• Costs

Better Customer Experience

21

Proprietary and Confidential.

Contact Info

Mike Hoyer, FSA, MAAA Life [email protected] (262) 923-3636

PROPRIETARY & CONFIDENTIAL

Accelerated Underwriting

SOA Life & Annuity Symposium - May 17, 2016Nashville, TNMark A. Sayre, FSA, CERA, MAAA

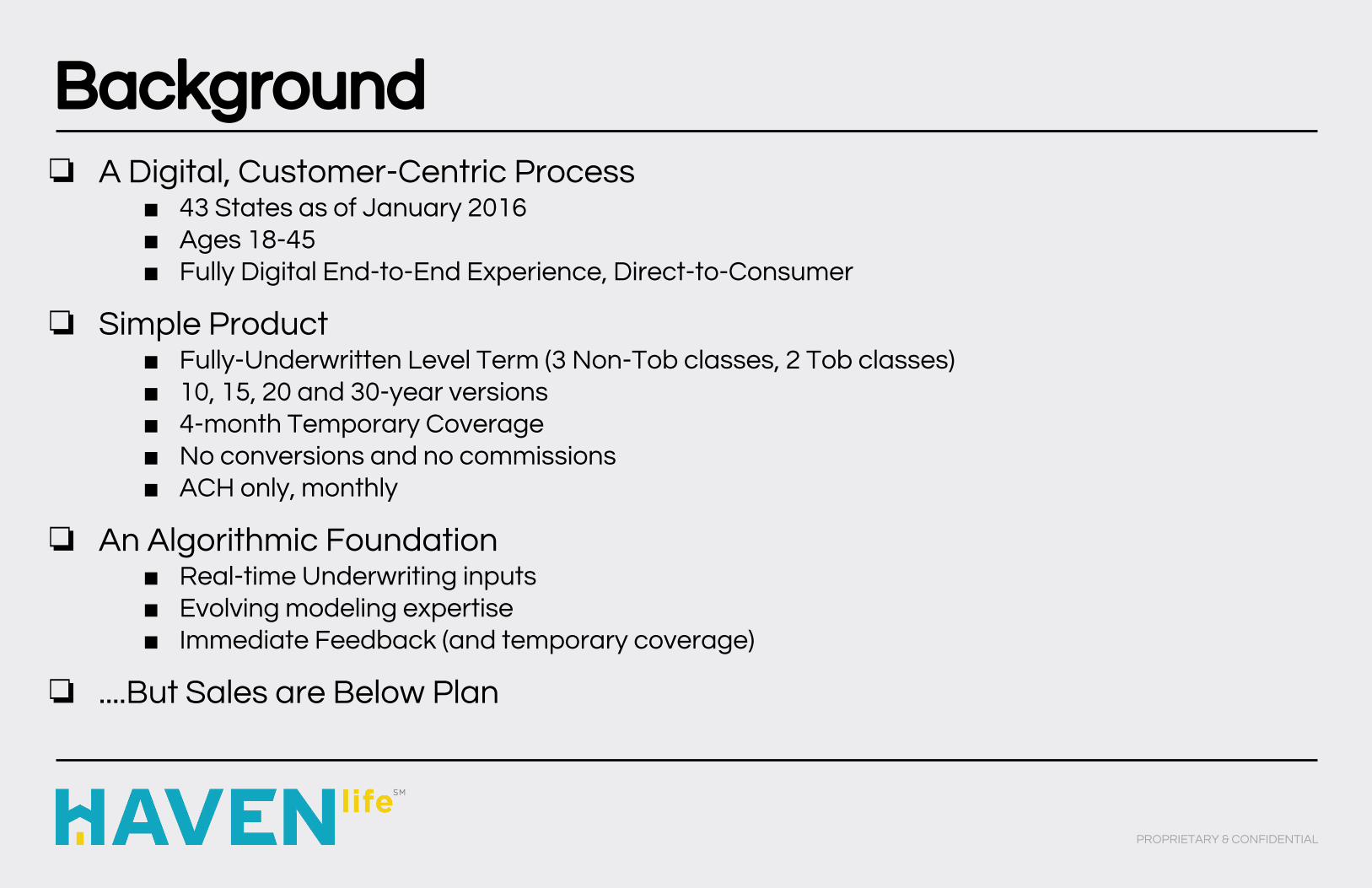

❏ A Digital, Customer-Centric Process■ 43 States as of January 2016■ Ages 18-45■ Fully Digital End-to-End Experience, Direct-to-Consumer

❏ Simple Product■ Fully-Underwritten Level Term (3 Non-Tob classes, 2 Tob classes)■ 10, 15, 20 and 30-year versions■ 4-month Temporary Coverage■ No conversions and no commissions■ ACH only, monthly

❏ An Algorithmic Foundation■ Real-time Underwriting inputs■ Evolving modeling expertise■ Immediate Feedback (and temporary coverage)

❏ ....But Sales are Below Plan

Background

PROPRIETARY & CONFIDENTIAL

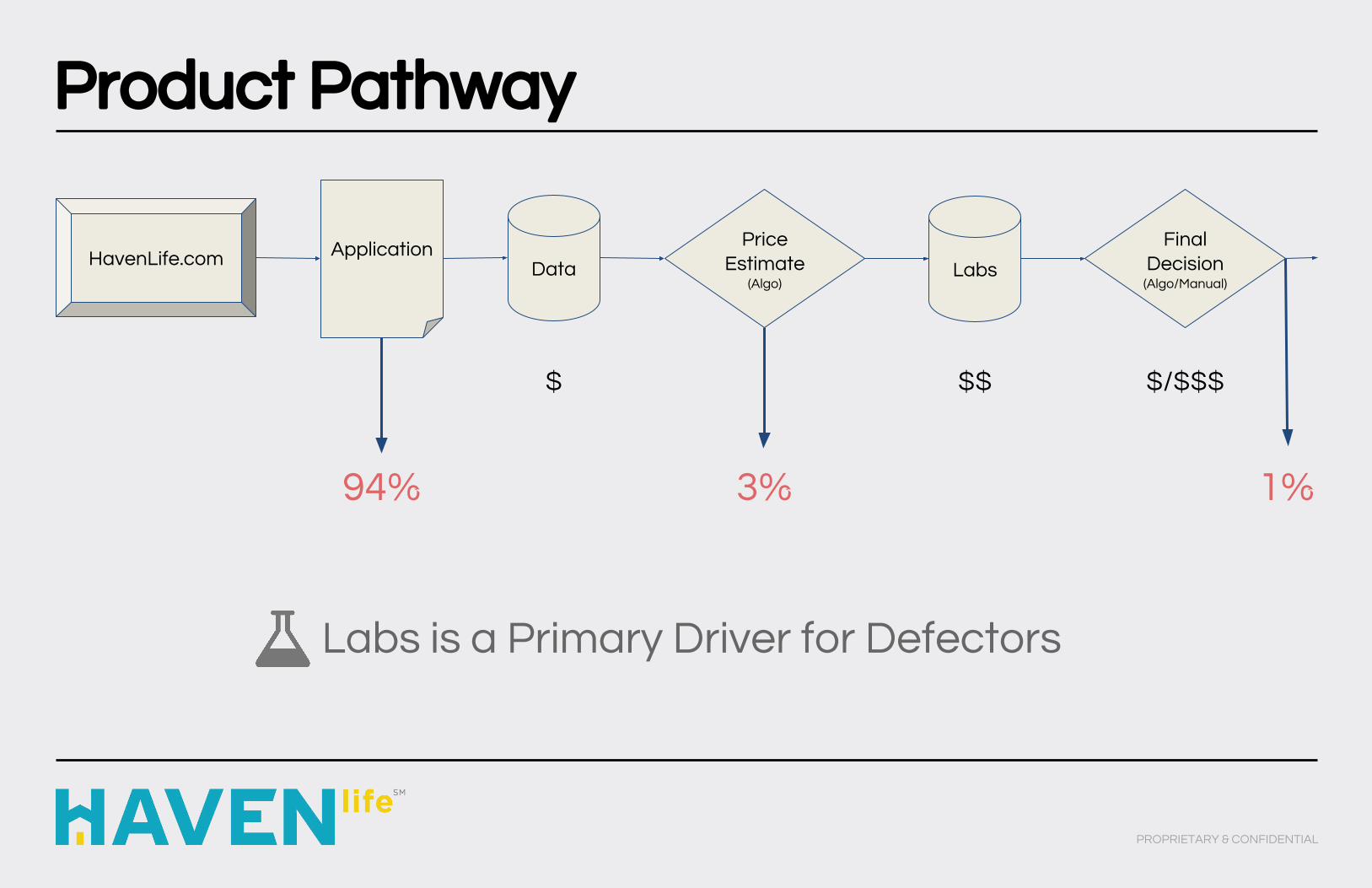

Product Pathway

PROPRIETARY & CONFIDENTIAL

HavenLife.com Application Price Estimate

(Algo)LabsData

Final Decision

(Algo/Manual)

$ $$ $/$$$

94% 3% 1%

Labs is a Primary Driver for Defectors

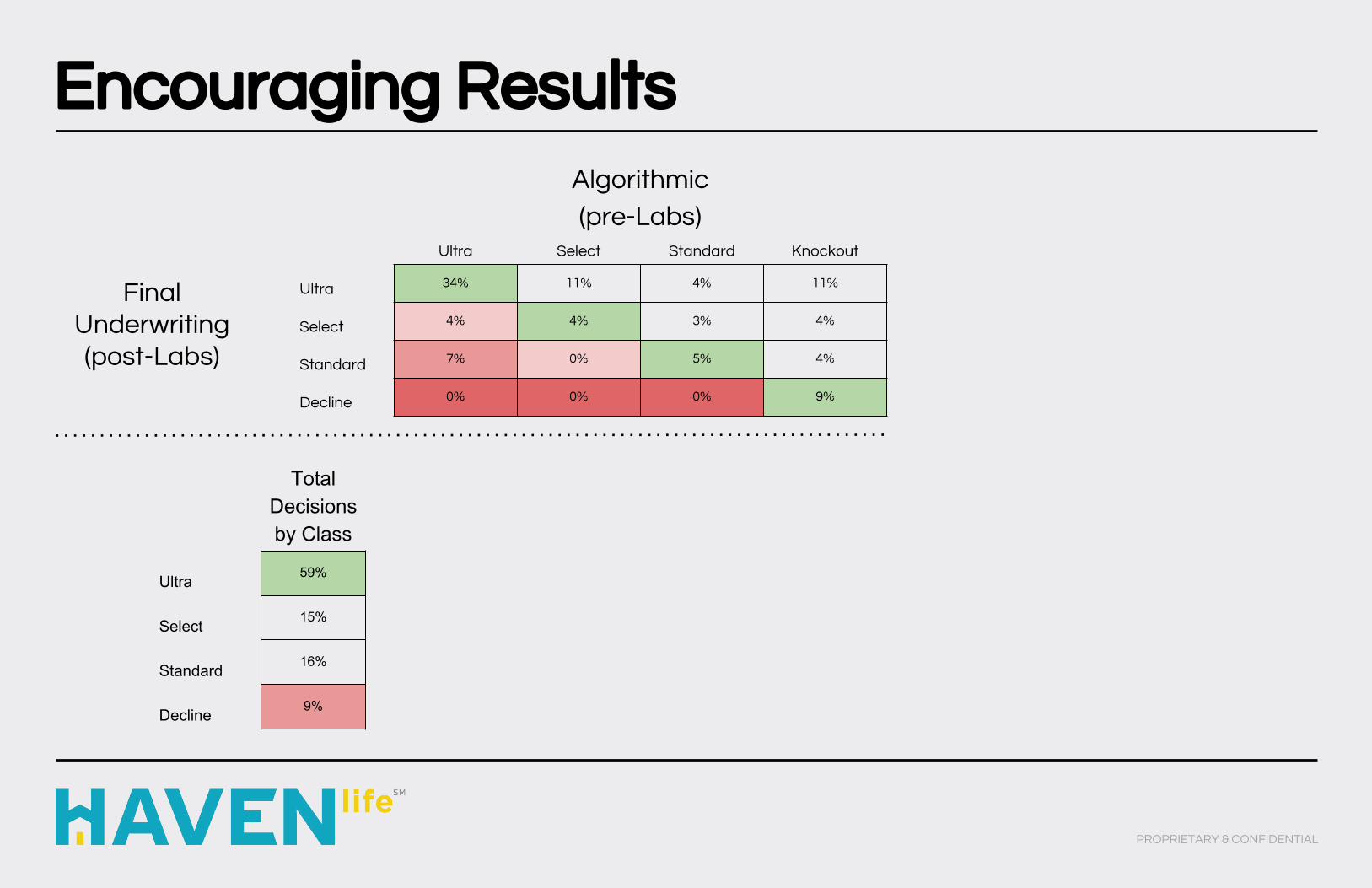

Encouraging Results

PROPRIETARY & CONFIDENTIAL

Algorithmic

(pre-Labs)Ultra Select Standard Knockout

Ultra 34% 11% 4% 11%

Select 4% 4% 3% 4%

Standard 7% 0% 5% 4%

Decline 0% 0% 0% 9%

Final Underwriting (post-Labs)

Total Decisions by Class

Ultra 59%

Select 15%

Standard 16%

Decline 9%

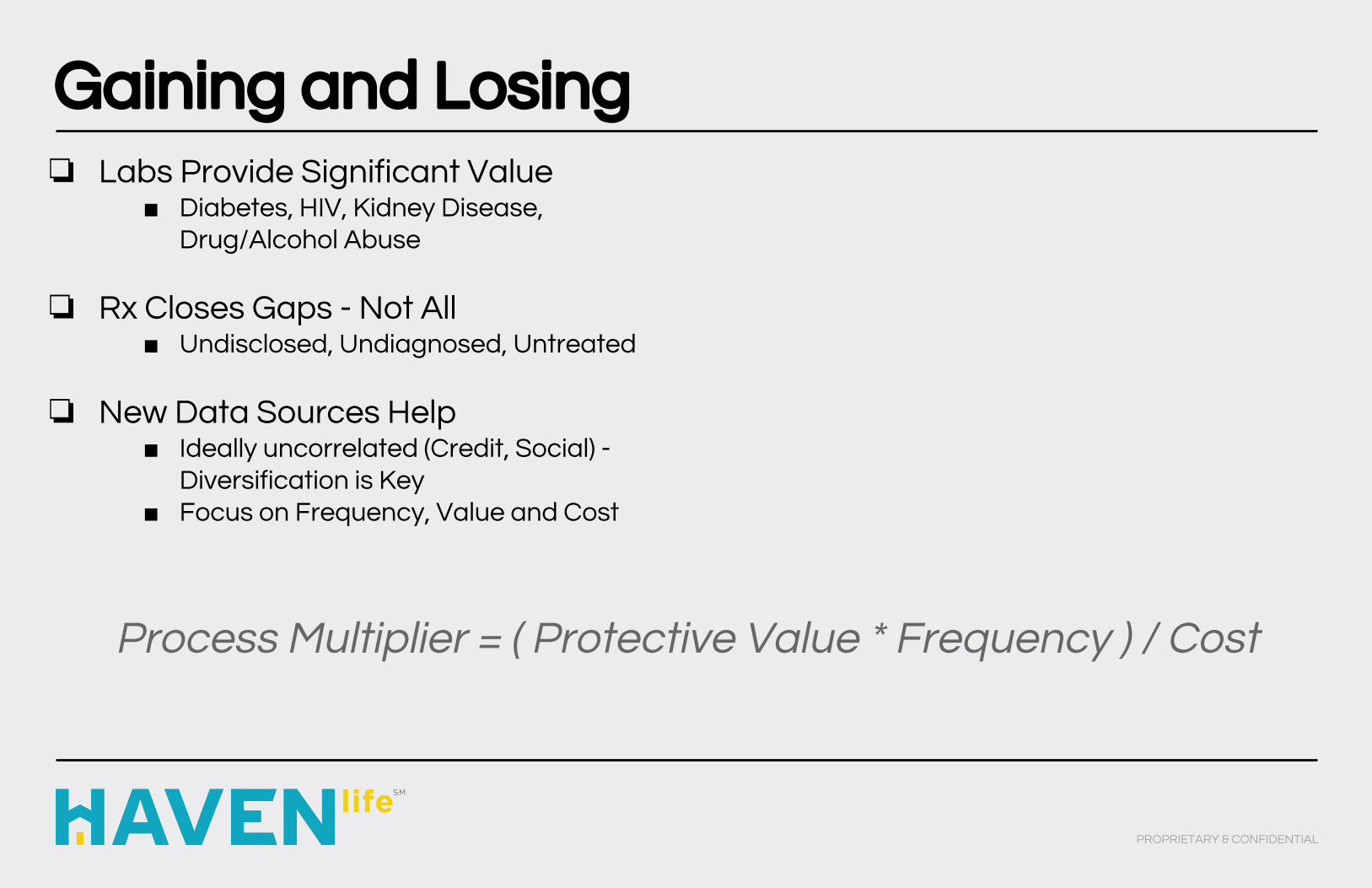

Gaining and Losing

PROPRIETARY & CONFIDENTIAL

❏ Labs Provide Significant Value■ Diabetes, HIV, Kidney Disease,

Drug/Alcohol Abuse

❏ Rx Closes Gaps - Not All■ Undisclosed, Undiagnosed, Untreated

❏ New Data Sources Help■ Ideally uncorrelated (Credit, Social) -

Diversification is Key■ Focus on Frequency, Value and Cost

Process Multiplier = ( Protective Value * Frequency ) / Cost

A New Approach

PROPRIETARY & CONFIDENTIAL

Algorithmic Underwriting

❏ Reflexive Application❏ Identity Verification❏ Driving History❏ Prescription History❏ Rx Interpretation

Accelerated Underwriting

❏ Reflexive Application❏ Identity Verification❏ Driving History❏ Prescription History❏ Rx Interpretation✓ Credit Data✓ Inspection Reports✓ Credit/MVR Scoring

What Comes Next

PROPRIETARY & CONFIDENTIAL

❏ Lifestyle Risk ■ Foreign Travel■ Avocation (Skydiving, Scuba Diving)■ Thrill-Seeking■ Binge-Drinking / Party Drugs

❏ Real-Time Medical Information■ Historical Labs■ Diagnoses and Treatments■ Clarity and Context for Rx

❏ Advanced Algorithms■ Dimensionality Reduction■ Clustering■ Complex Rules

Thank You!

PROPRIETARY & CONFIDENTIAL