Session 127 Panel Discussion: USA vs. World – … · Michelle M. Haines, ASA, MAAA . Stephen...

50

Session 127PD, USA Vs World – Supplemental Health Products Presenters: Michelle M. Haines, ASA, MAAA Stephen Rook, FSA, MAAA Anil Sanwal SOA Antitrust Disclaimer SOA Presentation Disclaimer

Transcript of Session 127 Panel Discussion: USA vs. World – … · Michelle M. Haines, ASA, MAAA . Stephen...

Session 127PD, USA Vs World – Supplemental Health Products

Presenters: Michelle M. Haines, ASA, MAAA

Stephen Rook, FSA, MAAA Anil Sanwal

SOA Antitrust Disclaimer SOA Presentation Disclaimer

2018 SOA Health MeetingPresenters

STEPHEN ROOK, FSA, Vice President, Aflac Group Insurance

ANIL SANWAL, Vice President, RGA International Corporation

MICHELLE HAINES, ASA, Associate Actuary, RGA US Group Reinsurance

Session Coordinator

KAMRAN MALIK, ASA, Consulting Actuary, Wakely Actuarial

Session 127, USA vs World – Supplemental Health Products

June 27, 2018

SOCIETY OF ACTUARIESAntitrust Compliance Guidelines

Active participation in the Society of Actuaries is an important aspect of membership. While the positive contributions of professional societies and associations are well-recognized and encouraged, association activities are vulnerable to close antitrust scrutiny. By their very nature, associations bring together industry competitors and other market participants.

The United States antitrust laws aim to protect consumers by preserving the free economy and prohibiting anti-competitive business practices; they promote competition. There are both state and federal antitrust laws, although state antitrust laws closely follow federal law. The Sherman Act, is the primary U.S. antitrust law pertaining to association activities. The Sherman Act prohibits every contract, combination or conspiracy that places an unreasonable restraint on trade. There are, however, some activities that are illegal under all circumstances, such as price fixing, market allocation and collusive bidding.

There is no safe harbor under the antitrust law for professional association activities. Therefore, association meeting participants should refrain from discussing any activity that could potentially be construed as having an anti-competitive effect. Discussions relating to product or service pricing, market allocations, membership restrictions, product standardization or other conditions on trade could arguably be perceived as a restraint on trade and may expose the SOA and its members to antitrust enforcement procedures.

While participating in all SOA in person meetings, webinars, teleconferences or side discussions, you should avoid discussing competitively sensitive information with competitors and follow these guidelines:

• Do not discuss prices for services or products or anything else that might affect prices

• Do not discuss what you or other entities plan to do in a particular geographic or product markets or with particular customers.

• Do not speak on behalf of the SOA or any of its committees unless specifically authorized to do so.

• Do leave a meeting where any anticompetitive pricing or market allocation discussion occurs.

• Do alert SOA staff and/or legal counsel to any concerning discussions

• Do consult with legal counsel before raising any matter or making a statement that may involve competitively sensitive information.

Adherence to these guidelines involves not only avoidance of antitrust violations, but avoidance of behavior which might be so construed. These guidelines only provide an overview of prohibited activities. SOA legal counsel reviews meeting agenda and materials as deemed appropriate and any discussion that departs from the formal agenda should be scrutinized carefully. Antitrust compliance is everyone’s responsibility; however, please seek legal counsel if you have any questions or concerns.

2

Presentation Disclaimer

Presentations are intended for educational purposes only and do not replace independent professional judgment. Statements of fact and opinions expressed are those of the participants individually and, unless expressly stated to the contrary, are not the opinion or position of the Society of Actuaries, its cosponsors or its committees. The Society of Actuaries does not endorse or approve, and assumes no responsibility for, the content, accuracy or completeness of the information presented. Attendees should note that the sessions are audio-recorded and may be published in various media, including print, audio and video formats without further notice.

3

To Participate, look for Polls in the SOA Event App or visit health.cnf.io in your browser

4

Type health.cnf.io In Your Browser

or

Find The Polls Feature Under MoreIn The Event App

Choose your

session

Setting the Stage

Supplemental Health Products

•Supplemental Health = in addition to other coverage

•Session Focus•Critical Illness, Accident, Hospital Indemnity

• Group chassis, optionally renewable• Sold at the workplace

6

1

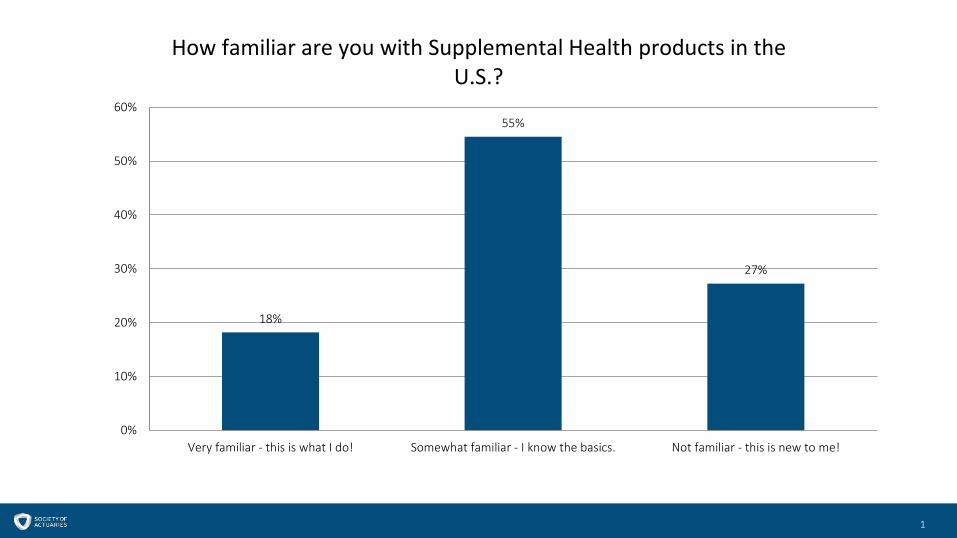

18%

55%

27%

0%

10%

20%

30%

40%

50%

60%

Very familiar - this is what I do! Somewhat familiar - I know the basics. Not familiar - this is new to me!

How familiar are you with Supplemental Health products in the U.S.?

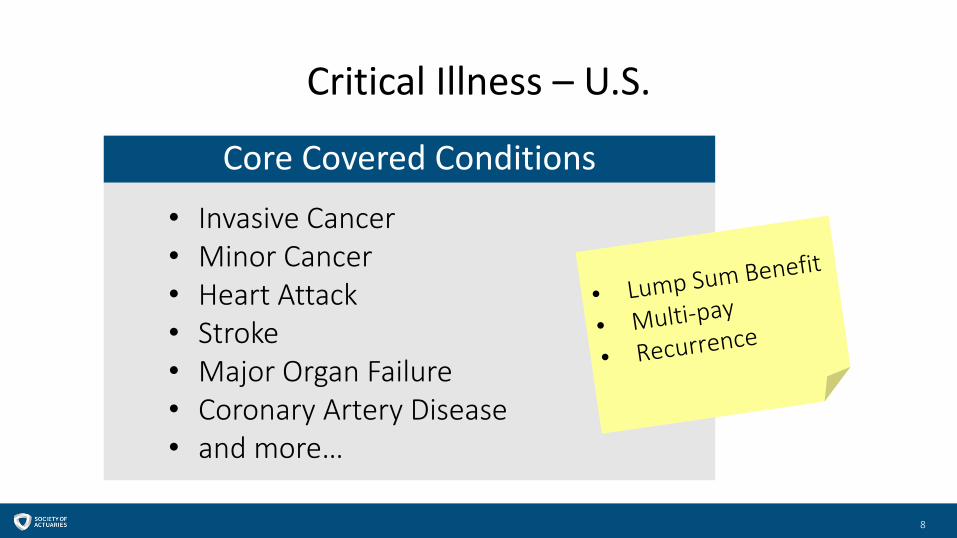

Critical Illness – U.S.

8

Core Covered Conditions

• Invasive Cancer• Minor Cancer• Heart Attack• Stroke• Major Organ Failure• Coronary Artery Disease• and more…

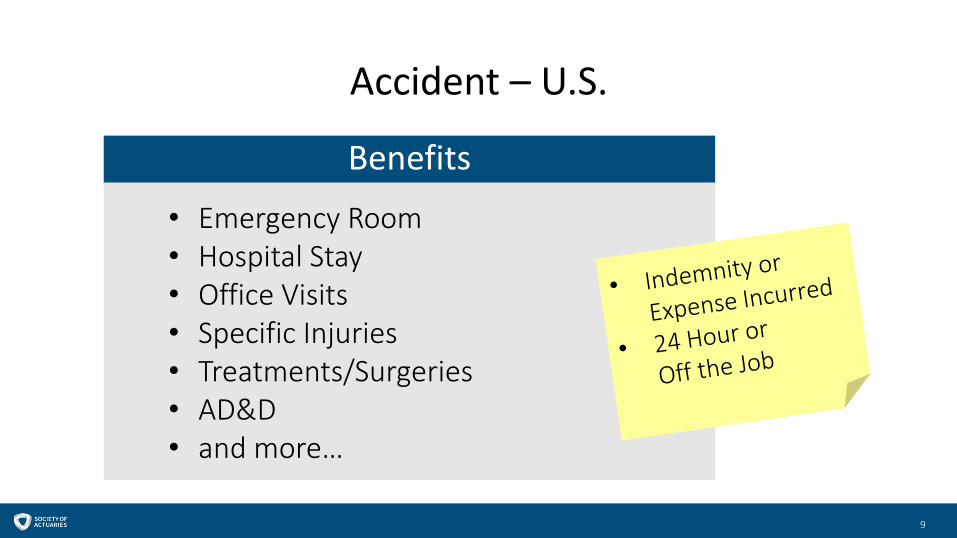

Accident – U.S.

9

Benefits

• Emergency Room• Hospital Stay• Office Visits• Specific Injuries• Treatments/Surgeries• AD&D• and more…

Hospital Indemnity – U.S.

10

Benefits

Standard (HSA Compatible)• Hospital Admission• Hospital ConfinementExtras• Emergency Room• Office Visits• Treatments/Surgeries• and more…

2017 U.S. Workplace Sales

11

$0

$200

$400

$600

$800

$1,000

$1,200

Premium (millions)

Critical Illness Accident Hospital Indemnity

Source: LIMRAU.S. Workplace Supplemental Health Insurance2017 Fourth Quarter Review

18%

9%1%

0%

5%

10%

15%

20%

% Change from 2016

Critical Illness Accident Hospital Indemnity

CI Inforce Premium & Growth – Canada, India, UK

12

Country Inforce Premium (millions)

AnnualGrowth

Canada ~CAD 300 (USD 230) 10-15%1

India ~INR 750 (USD 10) 7-10%2

UK ~£ 85 (USD 110) 10-15%3

South Africa small but growing

1 Fraser Group2 IRDA3 Swiss Re Group Watch

Marketing & Distribution

Marketing

USA vs World

• Gap Filler

• Network Expansion

• Unexpected Costs

• Gap Filler

• Mortgage Protection

• Complement to LTD

14

Distribution

USA vs World

• Employer Groups

• Associations and Affinity Groups

• Employer Groups in Canada, Potential in Other Markets

• Associations and Affinity Groups

• Bank Distribution

15

Market Penetration

USA vs World1Product Ownership:• Accident: 16%• Critical Illness: 7%• Hospital Indemnity: 7%

CI as % of Total Group Premium• UK: 5%• Canada: 8-10%• India: <5%• South Africa: <5%

16

1Eastbridge Consulting, Delving Deeper into Employee Demographics (March 2018)

Critical Illness

Critical Illness Covered Conditions

USA vs World

• Long list of conditions

• Partial benefits for less “critical” conditions

• Childhood illnesses

• Long list of conditions

• Staged CI

• Juvenile CI

18

2

30%

60%

0% 0%

10%

0%

10%

20%

30%

40%

50%

60%

70%

More than 5 More than 10 More than 15 More than 20 Other

How many conditions is too many?

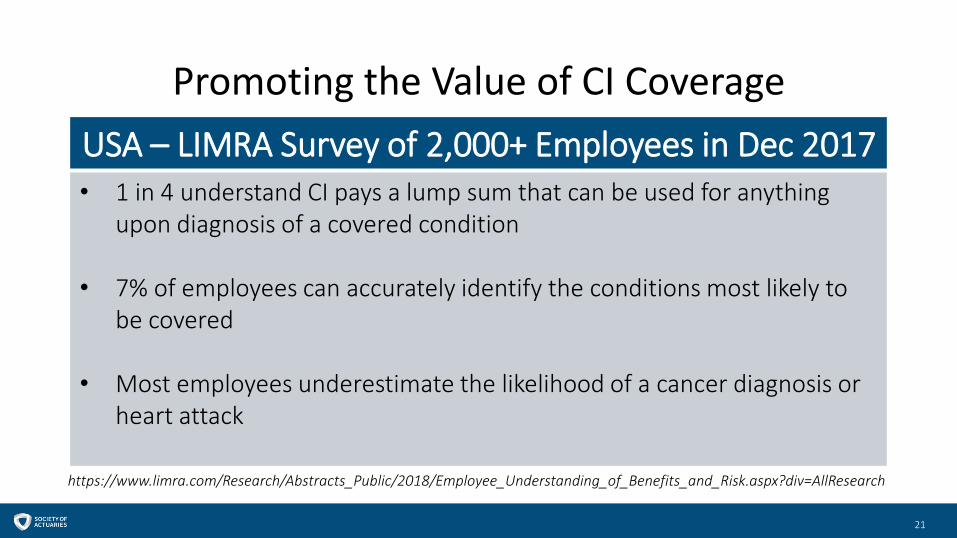

Promoting the Value of CI Coverage

USA – LIMRA Survey of 2,000+ Employees in Dec 2017• 1 in 4 understand CI pays a lump sum that can be used for anything

upon diagnosis of a covered condition

• 7% of employees can accurately identify the conditions most likely to be covered

• Most employees underestimate the likelihood of a cancer diagnosis or heart attack

21

https://www.limra.com/Research/Abstracts_Public/2018/Employee_Understanding_of_Benefits_and_Risk.aspx?div=AllResearch

Promoting the Value of CI Coverage

vs World – RGA Canada CI Focus Group

General:• 75% did not have a health concern• 65% would have no problem handling the extra expense

Those who purchased CI:• Upon recommendation of an advisor & made sense based on their age• 3-5 covered conditions was adequate

Those who did not purchase CI:• Felt already covered through existing insurance• No clear consensus on amount of CI that was appropriate

22

Critical Illness Plan Design Features

USA vs World

• Spouse and Child Coverage

• No Survival Period

• Multi-pay• Recurrence

• Survival Period but reducing (14-30 days)

• Recurrence• Partial payments

• Administration• Customer Confusion

23

Critical Illness Plan Design Features

USA vs World

• Age-Banded Rates• Issue Age vs Attained Age• Requests for Composite Rates

• Portable• Interaction and

Complementarity with Short Term Medical

• Portable• Fit with Medical and LTD

24

3

60%

30%

10%

0%

10%

20%

30%

40%

50%

60%

70%

Yes No I don't know

Do you see Short Term Medical + CI as a promising option in its price competitiveness?

4

70%

0%

30%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Yes No I don't know

Do you see STD/LTD and CI as a good complementary fit?

Critical Illness Underwriting

USA vs World

• Actively at Work• Primarily Guaranteed Issue• Pre-ex• Participation Requirements• Open Enrollments• Industry

• FCL Approach• Response to Low (Minimum)

Participation• Primarily Simplified Issue

• Selective use of Pre-ex• Move away from

Participation Requirements

27

RGA 2017 U.S. Group CI Underwriting Survey

29

Snapshot of Trends• Liberalization of Plan Designs

• No lifetime maximum• Higher spouse benefits• Increase in recurrence benefit levels

• Liberalization of Underwriting Practices• More requests to remove pre-ex• ‘Perpetual’ GI• Longer rate guarantees

Pre-ex and T-Rex…both extinct?

Source: RGA 2017 U.S. Group CI Underwriting Survey

Recurrence Benefits on the Rise

Source: RGA 2017 U.S. Group CI Underwriting SurveyQuestion not asked on 2015 survey

Rate Guarantees

2 years remains standard – but carriers will offer 3 years when needed

Source: RGA 2017 U.S. Group CI Underwriting Survey

Critical Illness Emerging Trends

USA vs World

• Testing and stage at diagnosis• CancerSEEK• Genome sequencing

• Continued lack of consumer awareness

• Growth in markets with nationalized healthcare

• Growth in workplace distribution

• Rise in covered conditions• Continued lack of

consumer awareness

34

Accident

Accident Benefits

USA

• Indemnity or Expense Incurred

• Include Accidental Death or not

• Treatment provided within stated timeline

• Diagnosis requirements

37

Accident Plan Design Features

USA

• Spouse and Child Coverage

• Portable

• Price Point Sensitivity

38

Accident Underwriting

USA

• Actively at Work

• Guaranteed Issue

• Participation Requirements

• Open Enrollments

• Industry

39

RGA 2017 U.S. Voluntary/Worksite Accident Survey

Top Concerns When Underwriting Accident Insurance

40

Participation Pricing

Industry Competition

Hospital Indemnity

Hospital Indemnity Benefits

USA

• Hospital Admission• How much is too much?• Optimal ratio of Hospital Admission to Daily Hospital Confinement?

• HSA Compatible Benefits• Hospital Admission, Daily Hospital, Accident

43

Hospital Indemnity Plan Design Features

USA

• Spouse and Child Coverage

• Portable

• Benefit Considerations• Maternity, Substance Abuse, Mental Nervous Disorders

44

Hospital Indemnity Underwriting

USA

• Actively at Work• Push toward Guaranteed Issue• Pre-ex• Participation Requirements• Open Enrollments• Industry

45

Regulatory Environment

Regulation

USA vs World

• 50 State Filing• State Variations• Excepted Benefit• HSA Compatibility• Minimum Loss Ratio

Requirements

• Standard Definitions- UK & Canada

47

General Trends

General Trends

USA vs World

• Combination Products• One product filing or product

bundling

• Growth in Employer Paid• Longer Rate Guarantees• Gig Economy• Innovating for Persistency

• Growth in Employee Paid

49