Service tax

19

Module SERVICE TAX

-

date post

14-Sep-2014 -

Category

Education

-

view

5.203 -

download

2

description

Transcript of Service tax

Module

SERVICE TAX

Introduction

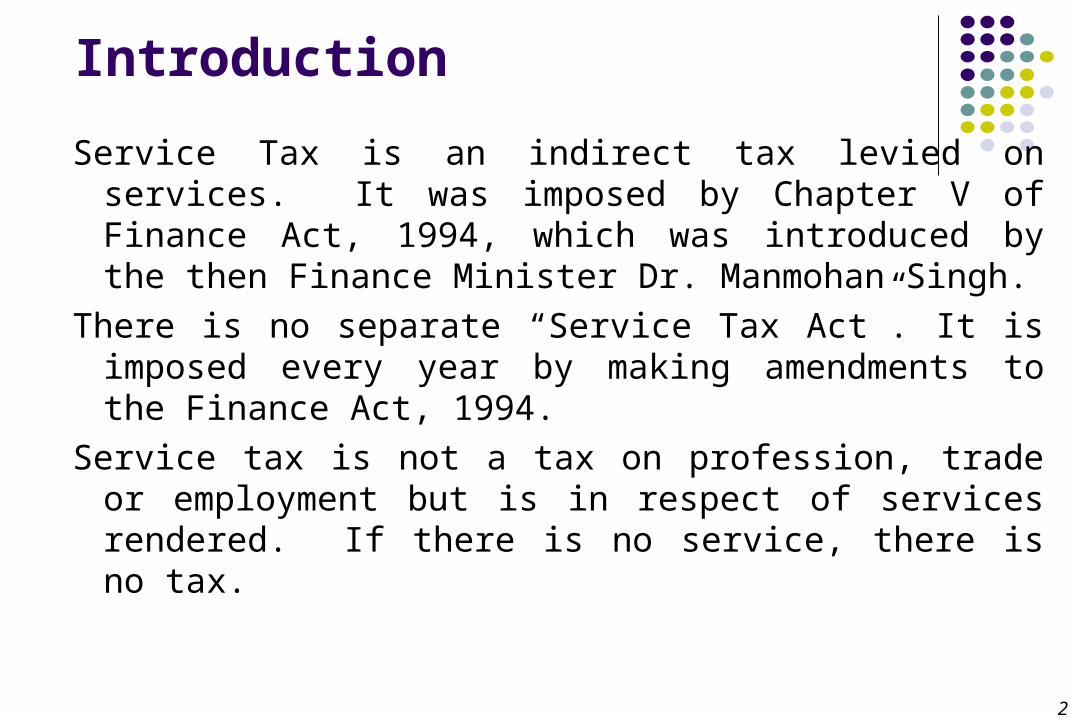

Service Tax is an indirect tax levied on services. It was imposed by Chapter V of Finance Act, 1994, which was introduced by the then Finance Minister Dr. Manmohan Singh.

There is no separate “Service Tax Act”. It is imposed every year by making amendments to the Finance Act, 1994.

Service tax is not a tax on profession, trade or employment but is in respect of services rendered. If there is no service, there is no tax.

2

Service Tax LawThere is no separate service tax statute and following are the various

legislatures to cover service tax: Service Tax Rules, 1994 Service Tax (Registration of Special Category of Persons) Rules, 2005 Export of Services Rules, 2005 Cenvat Credit Rules 2004 Service Tax (Advance Rulings) Rules, 2003 Taxation of Services (provided from outside India and Received in India) Rules, 2006 Service Tax (Determination of Value) Rules, 2006 Authority for Advance Rulings (Customs, Central Excise and Service Tax Procedure

Regulation, 2005 Central Excise (Appeals) Rules 2001 Customs, Excise and Service Tax Appellate Tribunal (Procedure) Rules, 1982 Service Tax Circulars, notifications and case laws.

- 3

Applicability of Service Tax Service Tax is applicable to the whole of India except Jammu and

Kashmir. If a service provider provides taxable services in Jammu and Kashmir,

then it is not liable to Service tax. However, if a service provider provides taxable services from Jammu and Kashmir to the client any where else in the country, he shall be liable to service tax.

Rate of TaxRate of Service tax is 12% for all services, plus Education Cess 2% and

Secondary and Higher Secondary Education Cess @ 1%, effectively the tax rate shall be 12.36%

- 4

Service liable to Service Tax All services are liable to service tax except –a) Activities specifically excluded in definition of service.b) Services covered under the negative listc) Services covered under Mega Exemption notification.d) Services provided outside the taxable territory.e) Services received by a unit located in SEZ (subject to conditions).

Negative List of ServicesThere are 17 categories of services which are not chargeable to service tax ––1. Services provided by Government or local authority. [Except (a) services by Dept of post by

way of speed post, express parcel post, life insurance, and agency services, (b) services in relation to an aircraft or a vessel, inside or outside the precincts of a port or an airport, (c) transport of goods or passengers, (d) support services]

2. Services provided by RBI

- 5

Service liable to Service Tax Negative List of Services Contd….3. Services provided by a Foreign diplomatic mission located in India4. Services relating to agriculture5. Trading of goods (commission agent or clearing agent)6. Any process amounting to manufacture or production of goods.7. Selling of space or time slots for advertisement other than advertisements broadcast by

radio or television.8. On payment of toll charges9. Betting, gambling or lottery10. Admission to entertainment events or access to amusement facilities.11. Transmission or distribution of electricity by an electricity transmission or distribution utility12. A few of services relating to education.13. Services by way of renting of residential dwelling for use as residence

- 6

Service liable to Service Tax Negative List of Services Contd….14. A few financial services like deposits, loans advance, foreign currency sale or purchase

by banks or authorised dealers etc)15. Service of transportation of passengers, with or without accompanied belongings.16. Services by way of transportation of goods17. Funeral services

Exemptions from Service Tax–Mega Notifications – Notification No. 12/2012-S.T.

1. Services provided to UNO2. Health care services3. Services by a veterinary clinic4. Services by charitable trust

- 7

Service liable to Service Tax Exemptions from Service Tax–Mega Notifications – Notification

No. 12/2012-S.T. Contd…5. Religious services6. Legal or arbitral service7. Technical testing of drugs etc.8. Coaching in recreational activities9. Educational institution10. Services provided to a recognized sports body11. Sponsorship of sporting events12. Construction service to Government13. Construction of road, bridge etc.14. Other construction service – airport, single residential units, low-cost houses up to a carpet

area of 60 sqmt etc.15. Copyright service

- 8

Service liable to Service Tax Exemptions from Service Tax–Mega Notifications –

Notification No. 12/2012-S.T. Contd…17. Services in folk or classical art forms18. Services of collecting or providing news19. Services of renting of a hotel etc for residence20. Services of providing food or beverages21. Services of transportation by rail or a vessel of specified goods – petroleum, relief

materials, defence equipment, postal mail, household effects, newspaper/magazines, railway equipment, agricultural produce, chemical fertilizers

22. Goods transport agency for fruits etc.23. Hiring motor vehicle for transport of more than 12 passengers24. Transport of passengers25. Vehicle parking to general public

- 9

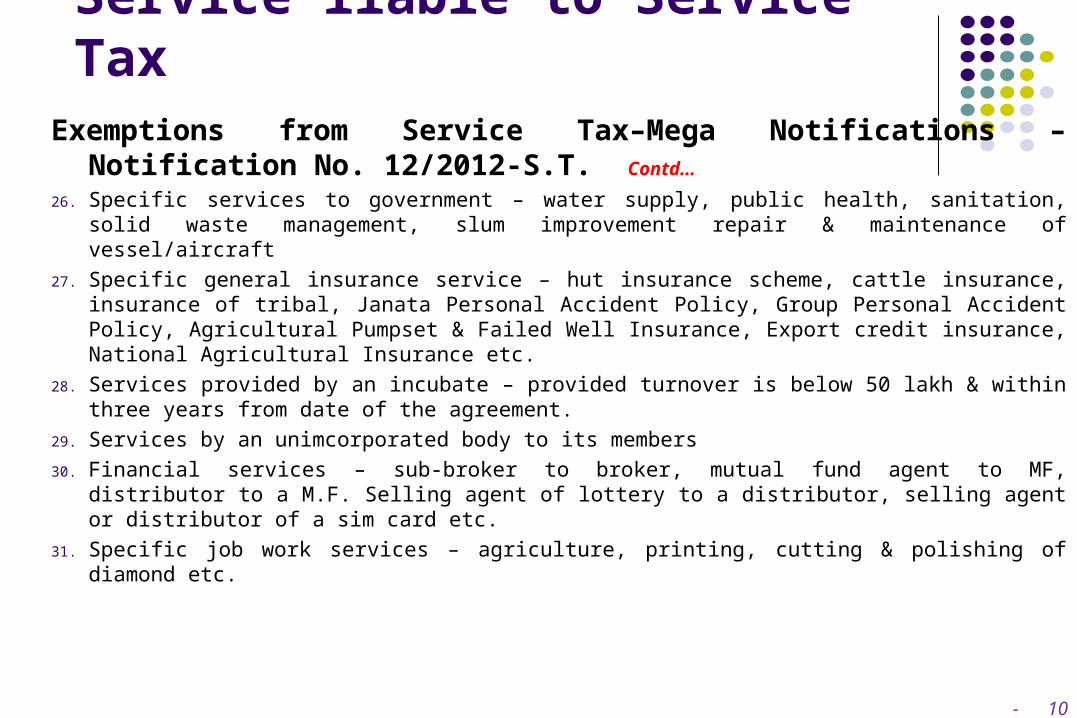

Service liable to Service Tax Exemptions from Service Tax–Mega Notifications –

Notification No. 12/2012-S.T. Contd…26. Specific services to government – water supply, public health, sanitation, solid waste

management, slum improvement repair & maintenance of vessel/aircraft27. Specific general insurance service – hut insurance scheme, cattle insurance, insurance of

tribal, Janata Personal Accident Policy, Group Personal Accident Policy, Agricultural Pumpset & Failed Well Insurance, Export credit insurance, National Agricultural Insurance etc.

28. Services provided by an incubate – provided turnover is below 50 lakh & within three years from date of the agreement.

29. Services by an unimcorporated body to its members30. Financial services – sub-broker to broker, mutual fund agent to MF, distributor to a M.F.

Selling agent of lottery to a distributor, selling agent or distributor of a sim card etc.31. Specific job work services – agriculture, printing, cutting & polishing of diamond etc.

- 10

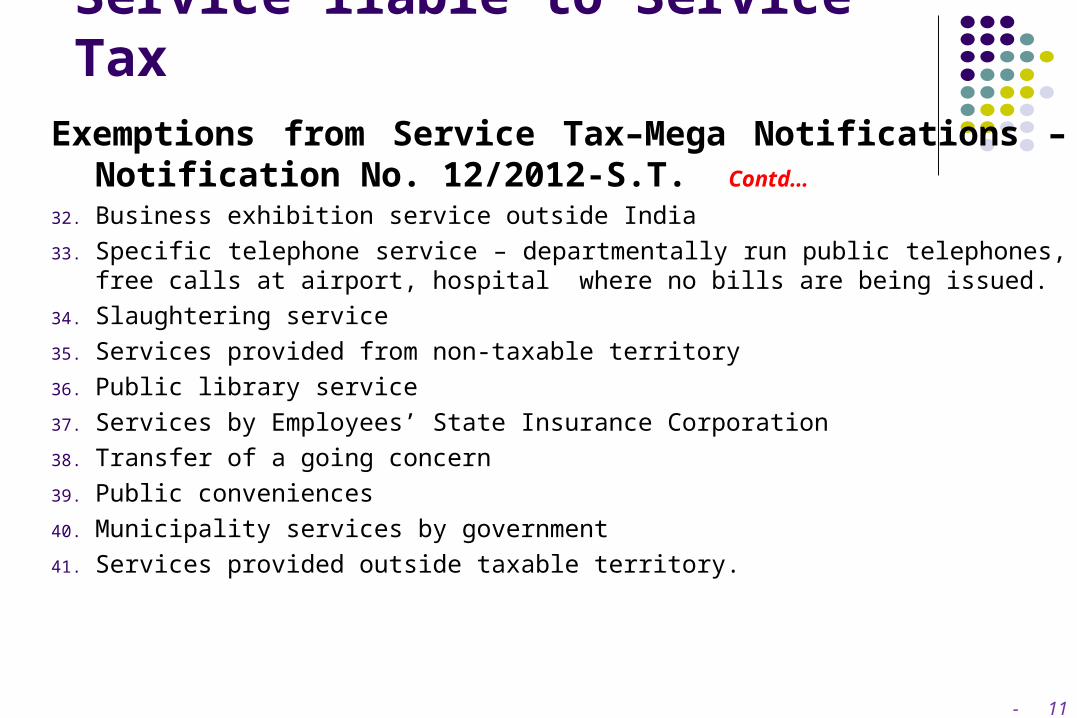

Service liable to Service Tax Exemptions from Service Tax–Mega Notifications –

Notification No. 12/2012-S.T. Contd…32. Business exhibition service outside India33. Specific telephone service – departmentally run public telephones, free calls at airport,

hospital where no bills are being issued.34. Slaughtering service35. Services provided from non-taxable territory36. Public library service37. Services by Employees’ State Insurance Corporation38. Transfer of a going concern39. Public conveniences40. Municipality services by government41. Services provided outside taxable territory.

- 11

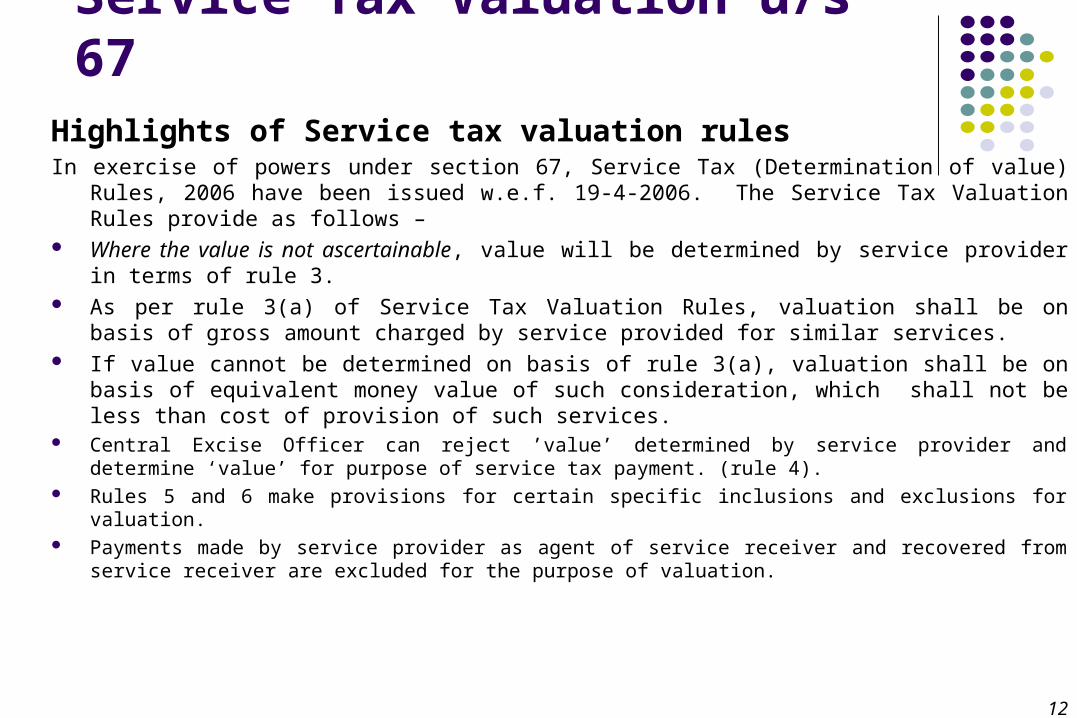

Service Tax Valuation u/s 67Highlights of Service tax valuation rulesIn exercise of powers under section 67, Service Tax (Determination of value) Rules, 2006 have

been issued w.e.f. 19-4-2006. The Service Tax Valuation Rules provide as follows – Where the value is not ascertainable, value will be determined by service provider in terms

of rule 3. As per rule 3(a) of Service Tax Valuation Rules, valuation shall be on basis of gross amount

charged by service provided for similar services. If value cannot be determined on basis of rule 3(a), valuation shall be on basis of equivalent

money value of such consideration, which shall not be less than cost of provision of such services.

Central Excise Officer can reject ’value’ determined by service provider and determine ‘value’ for purpose of service tax payment. (rule 4).

Rules 5 and 6 make provisions for certain specific inclusions and exclusions for valuation. Payments made by service provider as agent of service receiver and recovered from service receiver

are excluded for the purpose of valuation.

12

Service Tax Valuation u/s 67Highlights of Service tax valuation rulesIn exercise of powers under section 67, Service Tax (Determination of value) Rules, 2006 have

been issued w.e.f. 19-4-2006. The Service Tax Valuation Rules provide as follows – Where the value is not ascertainable, value will be determined by service provider in terms

of rule 3. As per rule 3(a) of Service Tax Valuation Rules, valuation shall be on basis of gross amount

charged by service provided for similar services. If value cannot be determined on basis of rule 3(a), valuation shall be on basis of equivalent

money value of such consideration, which shall not be less than cost of provision of such services.

Central Excise Officer can reject ’value’ determined by service provider and determine ‘value’ for purpose of service tax payment. (rule 4).

Rules 5 and 6 make provisions for certain specific inclusions and exclusions for valuation. Payments made by service provider as agent of service receiver and recovered from service receiver

are excluded for the purpose of valuation.

- 13

Service Tax Valuation u/s 67Valuation

- 14

Situation ValueWhere total consideration is monetary consideration

Taxable value = Gross Amount charged exclusive of Service Tax.

Where consideration is in kind (ie., non-monetary consideration)

• Wholly in kind

•Partly in Kind

Taxable value = Monetary Equivalent of “non-monetary consideration”.

Rule 3 of Service Tax Valuation Rules 2006Method -1 Taxable Value = GAC by service provider for similar service provided to third party.

Method-2: Taxable Value = [Monetary consideration + Mkt Value of Non-monetary consideration]{but it shall not be less than the cost of provisioning of service.

Where consideration is “not- quantifiable”

Taxable Value = Value determined in prescribed manner. Nor manner is prescribed so far – but is practically best judgment assessment.

Service Tax Provisions Relating to ––– ADVERTISEMENTService tax is payable only on advertisements on radio or Television.Advertisement means – any form of presentation for promotion of or bringing awareness

about any event, idea, immovable property, person, service, goods or actionable claim through newspaper, television, radio or any other means but does not include any presentation made in person.

Sale of space in print media, bill boards, public places, buildings, conveyances, cell phones, ATM, internet is not taxable.

Advertisement Agents, Designers are subject to Service Tax – The exemption is only to advertisement and not to other services like designs, advertisement agents etc.

Advertising Agency is liable to pay service tax on its commission, and other services like designing, preparation of advertisement material, advertisement films etc.

Service Tax – Prof. Ajaz Ahmed Khan– 2013 - 15

Service Tax Provisions Relating to ––– CONSULTING ENGINEERING SERVICESThis service is taxable under service tax. If Research and Development Cess is paid, service tax

exemption is available to the extent of R&D Cess paid.

SOFTWARE RELATED SERVICESDevelopment, design, programming, customisation, adaptation, upgradation, enchance,

implementation of information technology software is a ‘declared service’under section 66E(d) of Finance Act, 1994.

Ïnformation technology software”means any represenation of instruction, data, sound or image, including source code and object code, recorded in a machine readable form, and capable of being manipulated or providing interactivity to a user, by means of a computer or an automatic data processing machine or any other device or equipment –

The provision has been specifically included as “declared service”, since really software is goods and whether and when service tax can be imposed is a matter of argument and even litigation.

Service Tax – Prof. Ajaz Ahmed Khan– 2013 - 16

Service Tax Provisions Relating to ––– TRANSPORT OF GOODS BY AIRTransport of goods by air from a place outside India upto the customs station of

clearance in India is in Negative List of Services.Service tax is payable incase of transport of goods by air within India.

SERVICES OF AIR TRAVEL AGENTAir Travel Agents are subject to service tax only on the commission and not on entire

air ticket. Simple method for calculation of service tax payable by Air Travel Agents –

Service Tax @ 0.60% of basic fare incase of domestic booking and @ 1.20% of the basic fare in case of international bookings, of passage for travel by air, instead of the rate as prescribed in section 66.

- 17

Highlight the service tax valuation rules. (12)

Discuss the provisions relating to the service tax in the following cases : Air Travel agents services Consulting engineers Practicing Chartered Accountants. (12)

Discuss the service tax provisions relating to information technology software service. (10)

Briefly discuss the provisions of the Finance Act 1994 as amended, relating to service tax with respect to the following taxable services :

Consulting Engineer Practicing Chartered Accountant. (10)

- 18

19

To be Continued in next To be Continued in next sessionsession

2013 Prof. Ajaz Ahmed Khan

THANK YOUTHANK YOU