September 2017 - Servelec Group · September 2017. Servelec Group Overview Servelec HSC Comprising:...

20

H1 17 Results Presentation Alan Stubbs, Chief Executive Officer Mike Cane, Chief Financial Officer September 2017

Transcript of September 2017 - Servelec Group · September 2017. Servelec Group Overview Servelec HSC Comprising:...

H1 17 Results PresentationAlan Stubbs, Chief Executive Officer

Mike Cane, Chief Financial Officer

September 2017

Servelec Group Overview

Servelec HSC

Comprising:

Healthcare, Synergy, Corelogic, Abacus

Software Systems, Support & Hosting

• Mental, Community & Child Health

• Acute Healthcare

• Social Care

• Children’s Services

• Finance

306 employees

Servelec Automation

Hardware, Software & Control Systems

Servelec Controls:

• Oil & Gas

• Power & Infrastructure

Servelec Technologies:

• Utilities

• Broadcast

• Rail

257 employees

Servelec Group

56 employees

619 total employeesat H1 17

Servelec is a UK-headquartered technology Group,with significant intellectual property, providingsoftware, hardware and services to the healthcare,social care and education, oil and gas, energy andutilities sectors.

1

% of Group Revenue % of Group Profit

Servelec HSC 56% 59%

Servelec Controls 18% 11%

Servelec Technologies 26% 30%

Servelec Group at H1 17

Return to growth - Underlying operating profit up 44%

Cash conversion returns to normal levels

Servelec HSC main driver for return to growth due to strong performance in Healthcare and Children’s Services

Servelec Automation delivering strong result in Servelec Controls Oil & Gas but market challenges persist for Servelec Technologies

Reduction in anticipated growth for the full year

2

30,006

28,377

31,513

H1 2015

H1 2016

H1 2017

Revenue (£'000)

6,261

4,506

6,504

H1 2015

H1 2016

H1 2017

Underlying Operating Profit* ** (£'000)

44,095

37,437

34,746

H1 2015

H1 2016

H1 2017

Order Entry (£'000)

76,551

73,184

77,404

H1 2015

H1 2016

H1 2017

Order Bank (£'000)

168%

39%

96%

H1 2015

H1 2016

H1 2017

Cash Conversion

Results Summary

• Return to growth

• Group revenue up 11%

• Organic revenue up 2%

• Organic operating profit growth of 20%

• Adjusted EPS up 45%

• Cash conversion at 96%

• Order bank increased £4.2m

• Increased interim dividend 2.00p (H1 2016: 1.65p)

96%

£31.5m

*Underlying operating profit excludes share basedpayments, non-recurring items and amortisation fromacquired intangibles

3

£34.7m

£6.5m

£77.4m

Servelec HSC

Performance and Market Opportunities

Servelec HSC

• Healthcare and Synergy performing well but Corelogic flat

• Profit growth a combination of acquisitions and the business improvements made in 2016

• Slight increase in recurring revenue at 66% compared to 64% in FY16

• Invested in sales team and account management

• Closed our Indian development centre in Q3

• Positive on converting opportunities particularly mobile apps and portals

£'000s H1 2017 H1 2016 % Change

Segment Revenue 17,503 14,951 17%

Cost of Sales (8,999) (8,490) 6%

Adjusted Gross Profit 8,504 6,461 32%

Gross Margin % 49% 43%

Overheads (2,496) (2,290) 9%

Underlying Operating Profit 6,008 4,171 43%

Net margin % 34% 29%

4

14%

5 Servelec HSC: H1 17 Update Across our Markets

Non-Acute Acute Social Care Education

NHS Local Government

• University Hospitals Birmingham live with Oceano – Reference site

• Royal Cornwall Hospitals in delivery phase – to go live in early 2018

• Encouraging bidding activity

• Delivering steady performance

• Market opportunities growing

• Focusing on account management of installed base

• Investing in portal and mobile product extensions

• Active market

• Sales behind expectations

• Revitalising go-to-market strategy

• Action taken to strengthen team

• Account management of installed base

• Portal product extensions

• Synergy continues to perform well

• Contributor to growth

• Continues to outperform competitors (CACI & Capita)

• Market testing every five years

• High win rate

Oceano: £500m Flow: £70m PICS £50m

£50m

Cumulative value of potential new contracts coming to market in next five years:

Increasing links between our products as markets converge

£100m £50m

Servelec HSC: Mobile Apps6Product Enhancements through Mobile Apps

• Signed two deals to secure best of breed mobile product extensions

• Role-based apps to deliver product enhancements in line with customer demand and market trends towards staff mobilisation

• First app = RiO District Nursing app

• Clinical testing complete to ensure robust product

• Competitive landscape

• Total Mobile, EMIS, ACS

• Currently in Healthcare, moving into Social Care & Technologies

Market Opportunity

• ‘Every nurse an e-nurse’ – endorsement of apps from NHS Digital

• Anticipated market share increase YoY over next three years

• Swift rate of adoption anticipated

Business Model

• Minimal cost of development

• Pay per User per Month recurring revenue model

• Revenue share with third party developers

• High margins

Outlook / Next Steps

• Launch date – available now

Servelec HSC: Portals for channel shift in Social Care Care

7

Market Opportunity

• Finestra already in Social Care market place

• Upgrading existing customers and account management sell to Mosaic installed base

Citizens & Professionals Portal

• Empowering the customer’s clients

Market place

• Citizens purchase care services online

Reverse auction

• Providers bid for services required

Extranet

• Providers manage invoicing online

Saving customers money, improving their efficiencies, empowering end users

End to end solution of portal technology

Business Model

• Nil cost uplift for new product development

• Finestra development by third party, CHIPS & Extranet in-house IP

• Recurring licence revenue model

Outlook / Next Steps

• Launch date – available now

Servelec Automation

Performance and Market Opportunities

Servelec Controls

• Oil & Gas segment delivering stronger than anticipated performance

• Power & Infrastructure under pressure due to hiatus in nuclear market

• Consolidated business under one Managing Director

• Common engineering team across specialist routes to market

• Turkey CHP Plant– decision to be taken at year-end

£'000s H1 2017 H1 2016 % Change

Segment Revenue 5,721 5,397 6%

Cost of Sales (4,081) (3,988) 2%

Adjusted Gross Profit 1,640 1,409 16%

Gross Margin % 29% 26%

Overheads (1,095) (1,002) 9%

Underlying Operating Profit 545 407 34%

Net margin % 10% 8%

8Many points now covered on next slide so need to refine

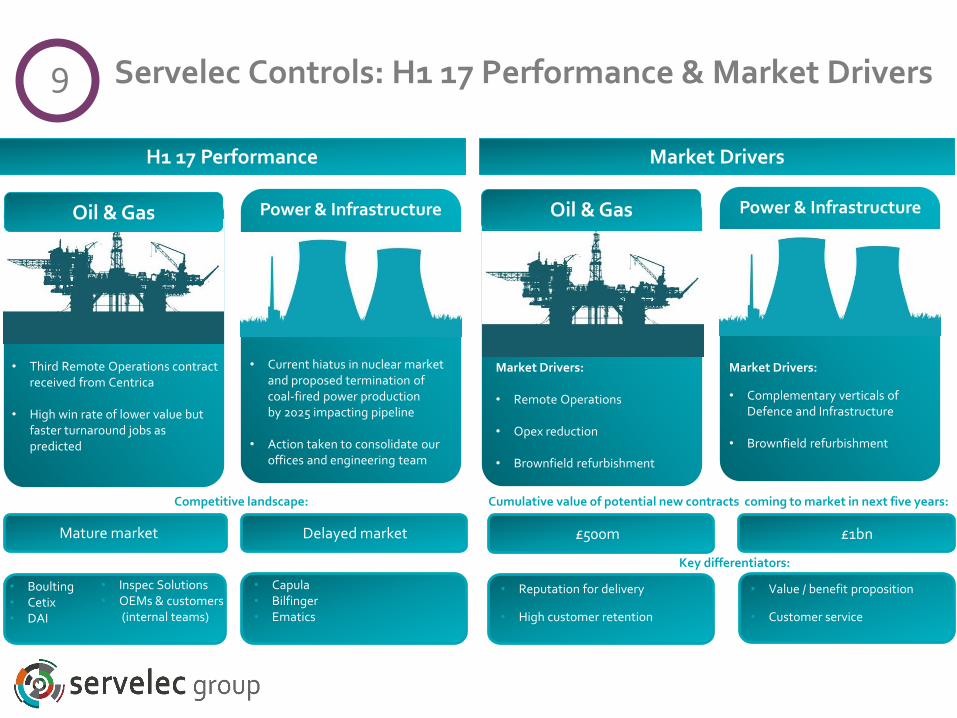

H1 17 Performance

Oil & Gas

Market Drivers

Servelec Controls: H1 17 Performance & Market Drivers

Mature market Delayed market

• Capula• Bilfinger• Ematics

£500m £1bn

• Boulting• Cetix• DAI

Cumulative value of potential new contracts coming to market in next five years:

Key differentiators:

• Reputation for delivery

• High customer retention

• Value / benefit proposition

• Customer service

Competitive landscape:

• Inspec Solutions• OEMs & customers

(internal teams)

9

• Third Remote Operations contract received from Centrica

• High win rate of lower value but faster turnaround jobs as predicted

• Current hiatus in nuclear market and proposed termination of coal-fired power production by 2025 impacting pipeline

• Action taken to consolidate our offices and engineering team

Power & Infrastructure Oil & Gas

Market Drivers:

• Remote Operations

• Opex reduction

• Brownfield refurbishment

Market Drivers:

• Complementary verticals of Defence and Infrastructure

• Brownfield refurbishment

Power & Infrastructure

Servelec Technologies

• Revenue broadly flat with small increase in profit

• Strong margins maintained

• Reduced order entry due to deferment of AMP6 orders for SCADA / Telemetry projects and RTUs

• Overhead increase predominantly due to currency changes post EU Referendum result

£'000s H1 2017 H1 2016 % Change

Segment Revenue 8,289 8,029 3%

Cost of Sales (3,914) (4,172) (6)%

Adjusted Gross Profit 4,375 3,857 13%

Gross Margin % 53% 48%

Overheads (3,023) (2,586) 17%

Underlying Operating Profit 1,352 1,271 6%

Net margin % 16% 16%

10

£10.9m

The only UK-based end-to-end data acquisition,control and optimisation product suite

Software

Servelec Technologies: H1 17 Performance & Market Opportunities

Key differentiator:

• Uptick in growth

• UK water companies are investing in opex reduction and control and monitoring

• Expanding customer base

• Entry into new markets(UK & Global)

11

H1 17 Performance Market Opportunity

£5bn*

UK RTU sales in AMP6 are still behind expectations

• Awarded Severn Trent Water Framework

Global RTU sales steady

• Changing underperforming partners, improving our approach.

• Sales gaining traction in focus regions

RTUs Software

SCADA / Telemetry:• Reduction in large projects in

remainder of 2017• Focusing on account

management

Business Optimisation:• Expanding customer base• UK water companies investing

and continued success through global supply chain

UK:• Disruption from ‘Open Water’

continuing for longer than anticipated

• Weak Sterling affecting water company budgets due to rising water treatment costs

• Orders expected to start to build from 2018

Global:• Focusing on optimising channel

partner network in China, Middle East and USA.

RTUs

Cumulative value of potential new contracts coming to market in next five years*:

UK:£34m (RTUs)

£30m(loggers)

Global:£5bn

Optimisation£70m (UK)

Creating the market globally

SCOPE:£80m (UK)

£1bn (Global)

* Based on Management review of available market

Group Financial Slides, Strategy & Outlook

Income Statement

H1 2017 H1 2016H1 2016

Adjusted*

£'000 £'000 £’000

Group Revenue 31,513 28,377

Gross Profit 14,519 11,727

46% 41%

Underlying Operating Profit 6,504 4,505 4,755

21% 16% 17%

Non-recurring items - (943) Share based payments (285) (346)

EBITA 6,219 3,216

Amortisation (1,778) (1,388)

Operating Profit from Continuing Operations 4,441 1,828

Net Finance (Expense)/Income (158) (97)

Profit Before Tax 4,284 1,731

Tax (825) (346)

19% 20%

Profit After Tax from continuing operations 3,459 1,385

Diluted EPS 4.8p 1.9p

Adjusted EPS 7.1p 4.9p

• Return to growth in revenue, profit and gross margins in H1

• Underlying operating profit growth is 37% (organic: 12%) compared to adjusted 2016*

• Amortisation has increased following acquisitions in 2016

• Net finance expense includes debt used to fund the acquisition of Synergy in April 2016

* Includes an allocation of the full year Research and Development Credit (RDEC) which related to the full year but was booked in H2 2016

12

Group Cash Flow

H1 2017 H1 2016£'000 £'000

EBITDA (inc. non recurring items) 7,159 4,140 Working Capital Movements (297) (2,562) Movement in provisions 7 6Operating Cash Flow 6,869 1,584 Cash conversion 96% 38%Net Interest paid (93) (79)Tax Paid (919) (752)

Net Operating Cash Flow 5,857 753 Capex (inc Intangibles) (355) (873)Acquisition of Subsidiaries - (20,879)

5,502 (21,000)

Movement in Loans - 15,113

Dividends Paid (2,790) (2,429)Other 848 574

Net Cash Movement (3,560) (7,742) Opening Cash 5,555 9,896Closing Cash 9,115 2,154

13

H1 2017 H1 2016

£'000 £'000

Fixed Assets & Intangibles 70,955 74,678

Inventories 1,743 1,682

Receivables 31,528 27,247

Cash 9,115 2,154

42,386 31,083

Payables (23,061) (22,385)

Short term loans (15,113) (15,113)

Corporation Tax (443) -

Provisions (208) (195)

Deferred Tax (2,963) (3,831)

(41,788) (41,524)

Net Assets 71,553 64,237

Group Balance Sheet

• Cash conversion back to expected levels at 96%

• Synergy cash collections are H1 weighted so still targeting 80% cash conversion for the full year

• Loan relates to acquisition of Synergy in H1 2016

• Strong balance sheet

• No R&D capitalised YTD

• Reduction in net debt to £6.0m from £9.6m at FY 2016

Drive organic growth

Continue to enhance our product capability

Develop our distribution channels to market

Acquire where beneficial to the business

Group Strategy and Performance in 2017

• Continued focus on customer satisfaction• Improving sales and broadening customer base and markets• Streamlining operations and reallocating resources

• Developing a truly mobile offering• Enhancement of portal technology to capitalise on channel shift• Continued enhancement of business optimisation products

• Broaden the product set being actively sold through distribution channels• Build new relationships with proactive channel partners

• Continue to pursue bolt-on acquisitions that enhance solutions capability to focus on businesses with strong intellectual property and recurring revenues

14

Outlook

• Servelec Group is in a robust financial position with a strong balance sheet.

• Cash generation on track to return to normalised level with net debt balance expected to reduce further by the year-end.

• Servelec HSC is underpinned by steady revenue streams from Healthcare and Education. Improving pipeline in Corelogic but remains Q4 weighted due to timing of licenses.

• Within Servelec Automation, we see a building pipeline of opportunities for Controls, particularly within Oil & Gas, but customer deferments in other areas will temporarily slow growth prospects.

• The Board remains positive about the longer term prospects for the Group.

15