September 2011 Acc Docket Due Diligence & Your M&A Success Story Fletcher Gottfried

13

INSIDE: Canadian Briefings September 2011 Due Diligence and M&A / IP in Joint Ventures / Importer Loopholes / Legal Cost Containment In-house Defendants / Wastewater Violations / Legal Hold Workflow CONTRACT, COPYRIGHT AND TRADEMARK LAW

-

Upload

frank-fletcher -

Category

Economy & Finance

-

view

512 -

download

5

description

Tips on executing a successful M&A due diligence plan

Transcript of September 2011 Acc Docket Due Diligence & Your M&A Success Story Fletcher Gottfried

INSIDE:Canadian Briefings

September 2011

Due Diligence and M&A / IP in Joint Ventures / Importer Loopholes / Legal Cost ContainmentIn-house Defendants / Wastewater Violations / Legal Hold Workflow

CONTRACT, COPYRIGHT AND TRADEMARK LAW

ACC Docket 35 September 2011

&BY FRANK FLETCHER AND KEITH E. GOTTFRIED

You are in-house counsel at MidSize Software

Corporation, a leading publicly-held developer

and marketer of computer software based in

California’s Silicon Valley. MidSize has a market

capitalization of approximately $300 million.

Over the preceding fiscal year, MidSize had

almost an equivalent amount of revenue, which

means the stock market is valuing MidSize at

approximately one times its most recent fiscal

year revenue. There is a consensus among

management that MidSize’s stock price does not

reflect its intrinsic value or its growth prospects.

Your CEO has decided that MidSize needs to

grow by acquisition. She envisions a “roll-up”

strategy where MidSize would acquire relatively

small privately-held software companies that

can be acquired and integrated quickly, thus

expanding MidSize’s annual revenue.

Due Diligence

Your M&A Success Story

ACC Docket 36 September 2011

paid a flat royalty equivalent to 20 percent of

the purchase price for each unit of software

sold by TargetCo. Next, you receive a letter

from an investment banking firm that had

been retained by TargetCo in connection

with its efforts to find a buyer but was

subsequently terminated three months later

and replaced by another investment banking

firm. Attached to the letter is an agreement

that requires TargetCo to pay the investment

banking firm 3 percent of the aggregate

consideration paid for TargetCo in the event

that it was sold during the 12 months follow-

ing the termination of the agreement, which

did in fact occur. You also begin to receive

notices from collection agencies seeking

payment on behalf of the target’s vendors

for invoices that were not paid. That amount

quickly aggregates into millions of dollars

and explains why TargetCo has as much

cash as it does on its balance sheet. Unfor-

tunately, none of these invoices had been

recorded as accounts payable, and much

of TargetCo’s cash will be needed to pay

these invoices. As you begin to consolidate

TargetCo’s trademark portfolio, you discover

that although TargetCo’s trademarks are

indicated as registered on the software pack-

aging, none of the trademarks have been

registered in the United States, but rather

they are registered only in a few foreign

countries. Further, one of TargetCo’s prod-

ucts, a virus protection program promoted

as the best in the business, is discovered to

have had a programming flaw that prevents

it from detecting computer viruses. While a

patch is quickly developed and made avail-

able to all customers, it is too late for some

customers — a virus has already corrupted

their computer network. As a result of the

virus, tens of millions of dollars in damages

are incurred by affected customers. The product liability

lawsuits are filed in rapid succession across the country.

Next, a US Government agency indicates that it believes

TargetCo had been overcharging it for custom software de-

velopment work, and has filed a debarment action against

TargetCo to prevent it from doing business with any agency

or instrumentality of the US government, one of the largest

customers of both TargetCo and MidSize. You also now

start to hear rumors of some overseas payments, made to

facilitate the completion of contracts with several inter-

national governmental organizations, and your outside

The first target, TargetCo, is a small

privately-held venture-backed start-up with

products that are complementary to Mid-

Size’s offerings. While TargetCo is not cheap,

your CEO believes that as long as TargetCo

brings to MidSize the revenue it forecast, or

even an amount relatively close to that num-

ber, and given the synergies and earnings

accretion that are expected to be generated

from the acquisition of TargetCo, the acquisi-

tion should be a “home run” even if MidSize

pays a “full price” for TargetCo. Your CEO,

however, adds as a caveat that she is assum-

ing no “landmines” will be uncovered post-

acquisition. TargetCo has told MidSize that

other companies are lining up to make offers

so MidSize believes that it needs to move

quickly. Your CEO makes an offer which is

accepted by TargetCo.

Your CEO takes you aside and instructs

you to get this deal closed as soon as possible

so that MidSize can announce the deal and

demonstrate to its investors its commitment

to growth by acquisition. You are told to

get M&A counsel engaged yesterday and to

focus your efforts on negotiating the acqui-

sition agreement. You ask the CEO about

forming a due diligence team and adding

consultants, accountants and other industry

experts, and the CEO tells you that there is

“no time to waste needlessly kicking tires

and overlawyering the transaction.” You

easily meet the CEO’s accelerated schedule

for negotiating the acquisition agreement.

Following the approval of the acquisition

agreement by MidSize’s board, it is executed

by MidSize and TargetCo. The transaction

is structured as a simultaneous signing and

closing so it is consummated upon signing.

Your CEO congratulates you on completing

the acquisition of TargetCo. You are celebrat-

ed throughout the company as its “superstar M&A lawyer”

and as the “can do” lawyer who “gets deals done.” When

you are in ear shot, the CEO often comments loudly, “there

goes my favorite lawyer!”

Unfortunately, these halcyon days are short-lived, as

your “stock” is about to crash. Fast-forward 60 days follow-

ing the acquisition of TargetCo by MidSize. You receive

a letter from one of the major patent troll firms politely

asking you to enter into a patent license since allegedly

TargetCo’s software infringes on a few of their patents. In

connection with the license, the patent troll is seeking to be

FRANK FLETCHER is the general counsel of Nero AG, a developer of

platform-neutral software technology for editing and

managing video, music, photos and other multimedia, which is headquartered in Karlsbad,

Germany with subsidiaries in Hangzhou, China; Yokohama,

Japan; and Glendale, California. Fletcher is responsible for all

aspects of the company’s worldwide legal function, including mergers and acquisitions, software

licensing, patents, trademarks, antipiracy and litigation. Prior to

joining Nero, he was a member of the products and technologies law group at Sun Microsystems where he served as chief counsel for the

CPU manufacturing, integrated circuit testing and validation and

global business services groups. He is available at [email protected].

KEITH E. GOTTFRIED is a partner in the Washington, DC office of

Blank Rome LLP. He concentrates his practice primarily on mergers

and acquisitions, corporate governance, shareholder activism,

securities regulation, NYSE and Nasdaq compliance and general

corporate matters. Over the course of his career, Gottfried has worked on a number of high-profile mergers

and acquisitions across a broad range of industries and sectors. Prior to rejoining Blank Rome, he

was the general counsel of the US Department of Housing and Urban Development, a position to which

he was appointed by President George W. Bush and unanimously

confirmed by the US Senate. Previous to that, Gottfried was the

general counsel of Borland Software Corporation in Cupertino,

California. He is available at [email protected].

!"#$%&!'!("()#*+,-+#(..&'/%0+1#/%#2("1$!"3#-&/2$+''#.2(-(./+-'4

!"#$%&'(%")*#%(+,&% ,#+),%-"),,#$+#.% /$% 0"#%1)&'(%20)0#3% &'(%$##4%

,)5.%5"'%7$'5%0"#%8'(/./)$)%,#+),%.&.0#93%0"#%:,)/$0/;;.%<)63%)$4%

"'5%8'(/./)$)%=(6/#.%0"/$7>%?.%0"#%-):/0),%)6#)@.%,)6+#.0%,)5%;/693%5#%

")*#%0"#%4#:0"%)$4%6#.'(6-#.%0'%4#;#$4%&'(6%/$0#6#.0.3%6#+)64,#..%';%

0"#%($/A(#$#..3%-'9:,#B/0&%'6%./C#%';%0"#%),,/+)0'6%&'(@6#%56#.0,/$+>

!"#$%&'$()%'*%$+,$-".+*+),)$-'/)($0'1'("23',%*4$2(')*'$1+*+%$(".+*+),)()56("/78"3

D%EFGG%H#)$%I/,,#6%88J

ACC Docket 38 September 2011

counsel gives you a quick tutorial on the Foreign Corrupt

Practices Act. Finally, after an extensive review of Tar-

getCo’s schedule for launching new software products or

releasing updates to existing products, it is discovered that

the software development teams are at least six months

behind schedule, and there will be nothing for TargetCo to

release for at least the next two fiscal quarters. Numerous

HR-related issues begin to percolate at TargetCo, including

severance obligations that were not uncovered during the

course of the due diligence process. At the same time, you

learn that assignment of invention agreements cannot be

located for many of TargetCo’s top inventors.

As more bad news on the acquisition of TargetCo

becomes public knowledge, the financial and trade press

show no mercy and label the transaction as an ill-timed,

poorly executed fiasco. The MidSize board is furious over

not seeing the promised benefits from the acquisition and

now questions the strategy of growth by acquisition. The

board believes that it was not adequately briefed about the

risks of acquiring TargetCo. The investors of MidSize are

also angry, and several shareholder suits are filed claiming

that the board breached its fiduciary duties in not properly

evaluating the acquisition of TargetCo. After an initial pe-

riod of denial, your CEO now agrees that the acquisition of

TargetCo is an unequivocal disaster and demands to know

how you could have allowed her and the board to be so

“blindsided.” She makes it clear to you that she is no longer

a member of your “fan club” and glares coldly at you when

you pass by her in the hallway.

This scenario may seem familiar to many of you. After

all, it is well known that many mergers fail or turn out to

be great disappointments. While there are many reasons

to account for an M&A transaction not meeting expecta-

tions, a poorly planned and executed due diligence process

is often responsible. There are few aspects of the M&A

process that are more important — and often not carefully

planned and appropriately executed — than the due dili-

gence process. The due diligence process of any acquisition

is a critical, if not the most important, phase of any M&A

transaction. While different buyers may have different

goals for what they hope to achieve from the due diligence

phase, generally, this is the time to develop an understand-

ing of what you are buying, justify the proposed purchase

price and the transaction, determine whether there are

any unusual or unanticipated risks to the acquisition, and

determine whether there are any actual or contingent li-

abilities that may be assumed in the acquisition. To put it

succinctly, the due diligence phase is the time to identify

any “landmines” and to prevent the acquisition from result-

ing in disaster. This is also the time to identify issues relat-

ing to how the transaction will be structured, identify what

additional provisions will be needed to be included in the

1. Accumulate bargaining chips for the

negotiation of the acquisition agreement.

2. Assess possible synergies and cost-

saving opportunities with other

businesses of the acquirer.

3. Help management decide whether

to acquire the target.

4. Confirm the strategic rationale

for the transaction.

5. Justify the proposed purchase price.

6. Mitigate risk and avoid “landmines.”

7. Determine what legal hurdles exist to

acquiring the target or operating the

business (e.g., existence of a non-

competition agreement, restrictions on use

of IP, agreements with regulators, etc.).

8. Determine how to structure the transaction.

9. Determine how to document the transaction.

10. Plan the post-closing operation

and integration of the target.

The Big Ten Purposes of M&A Due Diligence

1. Company representatives (e.g., legal,

corporate development, finance, accounting,

marketing, product management, tax,

human resources, risk management, etc.)

2. Outside M&A counsel

3. Other legal counsel (e.g., antitrust,

labor/employee benefits, intellectual

property, tax, environmental, government

contracts, litigation, etc.)

4. Local/state law counsel (e.g., real

estate, zoning, state licensing, etc.)

5. Foreign counsel

6. Accountants (independent auditors,

an accounting firm’s transaction

advisory group, tax advisors, etc.)

7. Consultants

8. Investment bankers

9. Lender’s counsel

10. Private investigative firm

Assembling the M&A Due Diligence Team

FTI TECHNOLOGY | Be Ready. Be Right.© 2010 FTI Consulting, Inc. FTI Technology LLC is a business of FTI Consulting, Inc.

Incomplete e-discovery

could leave you all wet.When it’s raining down risk, many e-discovery

providers leave you exposed. FTI delivers a

comprehensive e-discovery solution that protects

you from the complexity of global litigations and

investigations—and pricing that won’t soak you

with surprises.

Be Ready. Be Right.

ftitechnology.com

ACC Docket 40 September 2011

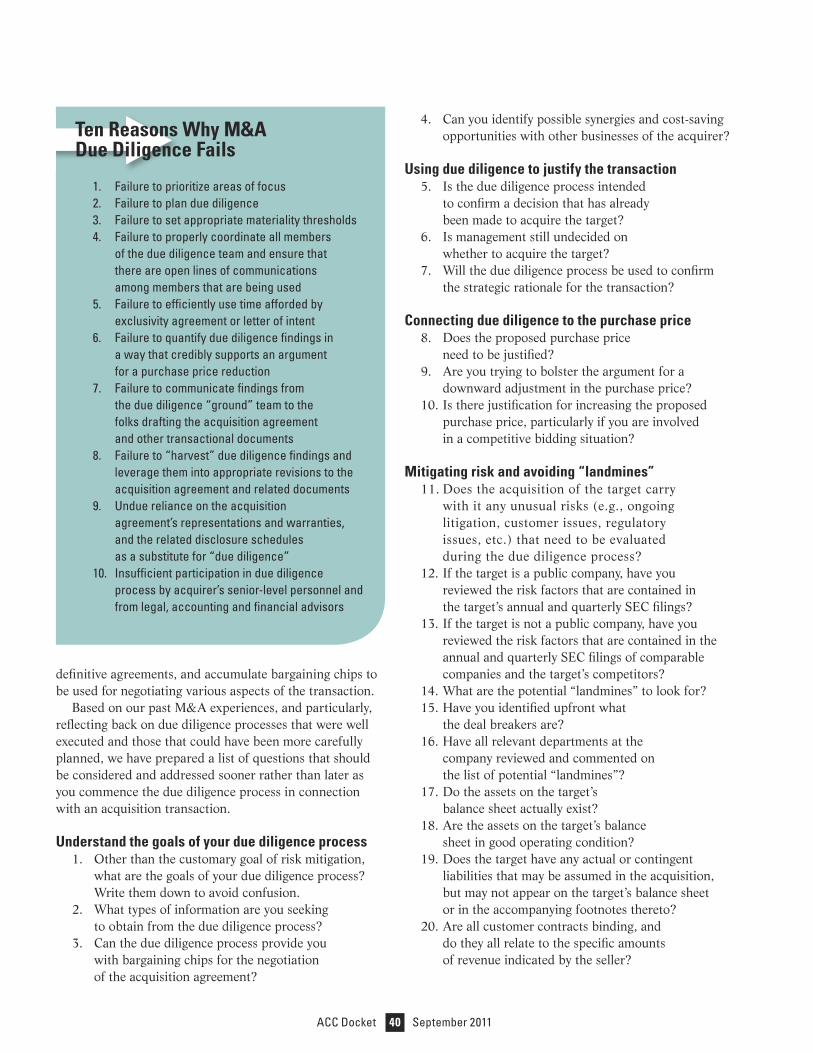

4. Can you identify possible synergies and cost-saving

opportunities with other businesses of the acquirer?

Using due diligence to justify the transaction 5. Is the due diligence process intended

to confirm a decision that has already

been made to acquire the target?

6. Is management still undecided on

whether to acquire the target?

7. Will the due diligence process be used to confirm

the strategic rationale for the transaction?

Connecting due diligence to the purchase price8. Does the proposed purchase price

need to be justified?

9. Are you trying to bolster the argument for a

downward adjustment in the purchase price?

10. Is there justification for increasing the proposed

purchase price, particularly if you are involved

in a competitive bidding situation?

Mitigating risk and avoiding “landmines” 11. Does the acquisition of the target carry

with it any unusual risks (e.g., ongoing

litigation, customer issues, regulatory

issues, etc.) that need to be evaluated

during the due diligence process?

12. If the target is a public company, have you

reviewed the risk factors that are contained in

the target’s annual and quarterly SEC filings?

13. If the target is not a public company, have you

reviewed the risk factors that are contained in the

annual and quarterly SEC filings of comparable

companies and the target’s competitors?

14. What are the potential “landmines” to look for?

15. Have you identified upfront what

the deal breakers are?

16. Have all relevant departments at the

company reviewed and commented on

the list of potential “landmines”?

17. Do the assets on the target’s

balance sheet actually exist?

18. Are the assets on the target’s balance

sheet in good operating condition?

19. Does the target have any actual or contingent

liabilities that may be assumed in the acquisition,

but may not appear on the target’s balance sheet

or in the accompanying footnotes thereto?

20. Are all customer contracts binding, and

do they all relate to the specific amounts

of revenue indicated by the seller?

definitive agreements, and accumulate bargaining chips to

be used for negotiating various aspects of the transaction.

Based on our past M&A experiences, and particularly,

reflecting back on due diligence processes that were well

executed and those that could have been more carefully

planned, we have prepared a list of questions that should

be considered and addressed sooner rather than later as

you commence the due diligence process in connection

with an acquisition transaction.

Understand the goals of your due diligence process1. Other than the customary goal of risk mitigation,

what are the goals of your due diligence process?

Write them down to avoid confusion.

2. What types of information are you seeking

to obtain from the due diligence process?

3. Can the due diligence process provide you

with bargaining chips for the negotiation

of the acquisition agreement?

1. Failure to prioritize areas of focus

2. Failure to plan due diligence

3. Failure to set appropriate materiality thresholds

4. Failure to properly coordinate all members

of the due diligence team and ensure that

there are open lines of communications

among members that are being used

5. Failure to efficiently use time afforded by

exclusivity agreement or letter of intent

6. Failure to quantify due diligence findings in

a way that credibly supports an argument

for a purchase price reduction

7. Failure to communicate findings from

the due diligence “ground” team to the

folks drafting the acquisition agreement

and other transactional documents

8. Failure to “harvest” due diligence findings and

leverage them into appropriate revisions to the

acquisition agreement and related documents

9. Undue reliance on the acquisition

agreement’s representations and warranties,

and the related disclosure schedules

as a substitute for “due diligence”

10. Insufficient participation in due diligence

process by acquirer’s senior-level personnel and

from legal, accounting and financial advisors

Ten Reasons Why M&A Due Diligence Fails

The right technology

for the wrong market?

Innovation in itself is no guarantee of success. You need a market that’s prepared to accept that

innovation. At Foley Hoag, we can help you fit your technology to its proper market. We offer more

than clear and sound legal advice. We offer strategic thinking that helps you realize every advantage.

Learn more at foleyhoag.com.

www.foleyhoag.comAttorney advertising. Prior results do not guarantee a similar outcome.

ACC Docket 42 September 2011

26. What corporate approvals are required

to consummate acquisition (e.g.,

board, shareholder, etc.)?

27. What third-party consents are needed to

consummate acquisition (e.g., customers,

lenders, bondholders, licensors, etc.)?

28. What permits, licenses and other

governmental authorizations are needed to

operate the business going forward?

Determining how best to structure the transaction 29. What is the optimal corporate structure

for the acquisition (e.g., asset purchase,

stock purchase, merger, etc.)?

30. What tax-planning opportunities exist for the

transaction, such as a 338(h)(10) election?

Planning the post-closing operation of the target 21. What information is needed to be gathered

from the due diligence process to plan the

post-closing integration of the target?

22. What additional investment is required post-closing?

23. How much working capital will be required

to operate the business post-closing?

24. Which employees will you retain post-closing?

Determining what legal hurdles exist to acquiring the target or operating the business

25. What legal hurdles need to be met to acquire

the target or operate the business (e.g.,

existence of a non-competition agreement,

restrictions on use of IP, agreements with

regulators, governmental approvals, etc.)?

1. Agreements with professional services providers

(e.g., investment banking firms, law firms,

accounting firms, consulting firms, etc.)

2. Agreements restricting the target’s right to compete

3. Agreements restricting the target’s

right to solicit employees

4. Agreements that are triggered upon the sale

or other change in control of the target

5. Agreements that are not yet executed

6. Correspondence alleging breaches of agreements

7. Correspondence threatening a lawsuit

8. Lawyers’ response letters to auditors

9. Agreements in connection with previous M&A

transactions, whether completed, aborted or

still in progress (e.g., letters of intent, exclusivity

agreements, merger agreements, stock purchase

agreements, asset purchase agreements and

other business combination agreements)

10. Agreements with respect to ongoing earn-outs

in connection with past M&A transactions

11. Agreements to indemnify third parties, including

those in connection with previous M&A transactions

12. Agreements providing for indemnification

obligations of the target in connection with

past M&A transactions that may be deemed to

continue past any specified durational limits, and

in excess of any specified indemnity cap, due to

certain specified carve-outs, such as claims for

intentional misrepresentation, fraud and taxes

13. Settlement agreements, including those related to

litigation, governmental investigations and other past

disputes, and particularly those that provide for the

target to have any ongoing obligations or restrictions

14. Offer letters and other employment, compensation,

option and incentive agreements that the target is a

party to or, if not yet executed, that exist in draft form

15. Proprietary rights and confidentiality

agreements with employees

16. Consulting and independent contractor agreements

17. Severance agreements with former employees

18. Written communications between

the target and its stockholders

19. Samples of all packaging for its products

that contain legal notices and/or reference

to any protected intellectual property,

whether registered or unregistered

20. Presentations given by any employee of the target,

whether to customers, employees, investors, analysts,

trade, and professional associations or other groups

21. Press releases issued by the target over

the past three years

22. Certified copies of the target’s corporate

charter (long-form)

23. The corporation statute of the

target’s state of incorporation

24. Analyst reports on the target

25. Market research studies that reference the target,

whether commissioned by the target or another party

Twenty-Five Items to Enhance the Customary Due Diligence Request List

ACC Docket 44 September 2011

Using due diligence as part of your commitment to best practices in corporate governance

39. How will you demonstrate that the board of

directors took reasonable steps to inform itself, to

the extent of satisfying its fiduciary duties, of the

potential risks associated with the transaction?

40. What additional data points are needed

to convince the board of directors of why

they should approve the transaction?

41. Have either you or your CEO asked the

board of directors whether there are specific

areas of the due diligence process that

they are particularly concerned with?

42. Have either you or your CEO asked the board

of directors how they would like the due

diligence findings communicated to them?

Paying attention to the clock43. How much time do you think the due

diligence process will take?

44. Have you planned your due diligence

using a realistic time table?

45. Does the team negotiating the definitive

transaction agreement understand that, from

a timing perspective, they need to remain

in sync with the due diligence team?

Determining how best to document the transaction 31. What ancillary agreements will be needed,

such as escrow, transitional services, non-

compete, employment, consulting, etc.?

32. What specific representations and

warranties will be required to be included

in the acquisition agreement?

33. What special covenants should be contained

in the definitive acquisition agreement

(e.g., cooperation, tax, treatment of stock

options and restricted stock, etc.)?

34. Which particular closing documents

(e.g., officer certificates, legal opinions,

releases, etc.) will be required?

Using due diligence to support broadening the seller’s indemnification obligations

35. Should the seller’s indemnification

obligations be broadened?

36. Should a portion of the purchase price

be placed in escrow as security for the

seller’s indemnification obligations?

37. What types of special indemnification provisions

should be included in the acquisition agreement?

38. What should be the appropriate cap amount on

seller’s indemnification obligations, and how long

should such indemnification obligations last?

ACC Docket

• Outsource Resource: Outsourcing Challenges

During a Merger and Acquisition (Nov. 2009).

www.acc.com/docket/outsource_nov09

Presentations• Technology Issues in Mergers and Acquisitions

(Oct. 2010). www.acc.com/tech-m&a_oct10

• Avoiding Surprises in M&A Transactions (March

2009). www.acc.com/surprise-m&a_mar09

Forms & Policies• Intellectual Property Due Diligence Request List

(Oct. 2010). www.acc.com/forms/ip-dd_oct10

• IP Due Diligence Issues in M&A Transactions Checklist

(Feb. 2010). www.acc.com/quickref/ip-m&a_feb10

• Preliminary Due Diligence Checklist (July 2009).

www.acc.com/quickref/pre-dd_jul09

• Goals of Due Diligence (July 2009).

www.acc.com/quickref/duedil_jul09

Article• Mergers and Acquisitions (Fraser Milner Casgrain

LLP) (June 2010). www.acc.com/m&a-fraser_jun10

Education• Dealing with M&A transactions abroad? Join us at ACC’s

2011 Annual Meeting, October 23-26 in Denver, Colo.,

and attend session 204 – Hot Issues in International

M&A. This session will discuss the critical issues

associated with international M&A, including anti-

trust law, privacy, and environmental liability. Learn

more and register today at http://am.acc.com.

ACC has more material on this subject on our website.

Visit www.acc.com, where you can browse our resources

by practice area or search by keyword.

ACC Extras on… M&A Due Diligence

ACC Docket 45 September 2011

51. Are there unique issues of local or state law (e.g.,

real estate, zoning, state licensing, etc.) involved

in the acquisition that would suggest that local

counsel be represented on the due diligence team?

52. Are these assets and/or operations located

overseas and require that foreign counsel be

represented on the due diligence team?

53. Have you verified that your outside counsel

is appropriately staffing the due diligence

team and not just assigning you relatively

junior lawyers? Have you received a list of the

attorneys that have been assigned to the due

diligence team? Have you read their bios?

54. Will the company’s auditors be represented

on the due diligence team?

55. In addition to the company’s auditors, will

any other accounting firms be retained in

connection the due diligence process (e.g., an

accounting firm’s transaction advisory group)?

56. Are there any anticipated tax issues (e.g.,

open tax audits, NOL carryovers, etc.) with

respect to the target that would suggest

that tax advisors be retained in connection

with the due diligence process?

Deciding who should participate as part of your team46. Who from the company will be part of the

due diligence team (e.g., legal, corporate

development, finance, accounting,

marketing, product management, tax, human

resources, risk management, etc.)?

47. Who from your outside law firm will be part of the

due diligence team (e.g., M&A counsel, securities

counsel — if target is a public company — etc.)?

48. What legal specialties should be represented on

the due diligence team (e.g., antitrust, labor/

employee benefits, intellectual property, tax,

environmental, government contracts, etc.)?

49. Is your M&A law firm the right law firm to

coordinate due diligence, or does the nature

of the target’s business require a law firm

with very specific industry experience to

coordinate the due diligence process?

50. In addition to your M&A counsel’s law

firm, will other law firms be retained in

connection with the due diligence process?

Corporate Finance

Mergers and Acquisitions

Product Liability Defense

Energy and Agribusiness

Life Sciences

Financial Institutions

Bankruptcy

Commercial Litigation

Insurance Recovery

Securities Litigation

Real Estate

Employment and Bene" ts

Intellectual Property

Minneapolis ! Denver ! www.lindquist.com

ACC Docket 46 September 2011

Reporting due diligence findings69. How should each member of the due diligence

team memorialize their due diligence findings?

70. Should you provide each member of the

due diligence team with a template to use

to capture their due diligence findings?

71. What is the most appropriate and optimal method

to memorialize the aggregate due diligence

findings (e.g., memo, report, chart, etc.)?

72. Should you prepare a separate due diligence

summary or report that focuses only on issues that

have a quantitative impact on valuation of the

target and may affect ultimate purchase price?

73. Should you hold regular status update

meetings? How will they be organized? Who

will attend? How will results be presented?

Preparing and submitting the due diligence request list

74. Have you prepared and submitted to the target

a comprehensive due diligence request list that

has been appropriately tailored to the target

and the transaction you are pursuing? Is the

due diligence list appropriately tailored to the

target’s industry and regulatory environment?

75. Should each of the “legal specialists,” regulatory

counsel, employee benefits counsel, foreign

counsel, etc., prepare separate due diligence

request lists focused on their respective areas?

Haste makes wasteWhile the due diligence process may not be the most ex-

citing phase of an M&A transaction, there are many more

opportunities for the in-house counsel to be the “hero” in

that phase than the phase where definitive agreements are

executed. The M&A world is littered with deals that have

gone bad because folks unduly rushed a signing without

knowing what they were buying, and would be owning and

operating. We hope the questions that we list above will

provide in-house counsel with a useful roadmap for issues

that need to be clarified early in planning and conducting

the due diligence phase of any acquisition. By organizing

an efficient and effective due diligence plan up front, at

the end of the process, you will be the “hero” and remain

prudent in protecting the your company’s interests.∑

Have a comment on this article? Visit ACC’s blog

at www.inhouseaccess.com/articles/acc-docket.

57. Will any consultants be retained for the due

diligence? Who will engage these consultants?

Should they be retained by your law firm so as to

preserve the attorney-client privilege reasons or

should they be retained directly to save costs?

58. Will the company’s investment bankers be

represented on the due diligence team?

59. Who will conduct the customer/partner due

diligence, and when will that due diligence be done?

60. Will any of the parties providing financing

for the acquisition of the target be

represented on the due diligence team?

61. Is there any need to retain a private investigative

firm to conduct background checks on the

target’s management team, particularly where

the target holds various security clearances;

the loss of which would have a material

adverse effect on the target’s business?

62. Have you prepared an appropriate form

of confidentiality agreement up front to be

executed by each professional service firm

involved in the due diligence process?

63. Have you reviewed, and as appropriate, had

your outside counsel review and comment

on the engagement letters and/or retention

agreements for each professional service firm

involved in the due diligence process?

64. Should any of the non-legal service providers

participating in the due diligence process be

retained by your outside counsel so as to attempt

to preserve the attorney-client privilege?

Establishing appropriate reporting channels and lines of communication

65. Have you established appropriate reporting

channels, intervals and deadlines for the due

diligence team to forward their findings?

66. Have you established and communicated materiality

thresholds and what your company, as the acquirer,

would view as possible “deal breakers”?

67. Have you scheduled weekly conference calls with

due diligence team members to review findings and

update all on timing and progress of transaction?

68. Do you need to establish a virtual deal room for

transaction participants to provide updates?