Seminar V - Protact · PDF fileSeminar V Inbound Investments ... North America 429 146 242.3...

8

Seminar V Inbound Investments In India & Outbound Investments From India – Post BEPS Planning and Challenges (For GAAR, PoEm/CFC & Transfer Pricing) 18 th June, 2016

Transcript of Seminar V - Protact · PDF fileSeminar V Inbound Investments ... North America 429 146 242.3...

Seminar V Inbound Investments In India & Outbound

Investments From India – Post BEPS

Planning and Challenges (For GAAR, PoEm/CFC & Transfer Pricing)

18th June, 2016

1

IFA INDIA WRC-CONFERENCE

Chairman

Panellists

Kuntal Dave – Nanubhai Desai & Co.

Ms. Geeta Jani – EY, India

Mr. Vishal Gada – Dhruva Advisors LLP

2

IFA INDIA WRC-CONFERENCE

Investment flows

Particulars 2015 – 16 2015 – 14 2014 – 13

Foreign Direct Investment to India 44.79 36.55 31.66

Overseas Direct Investment by

India 8.83 1.68 7.89

Source : Reserve Bank of India

(US$ in Billions)

3

IFA INDIA WRC-CONFERENCE

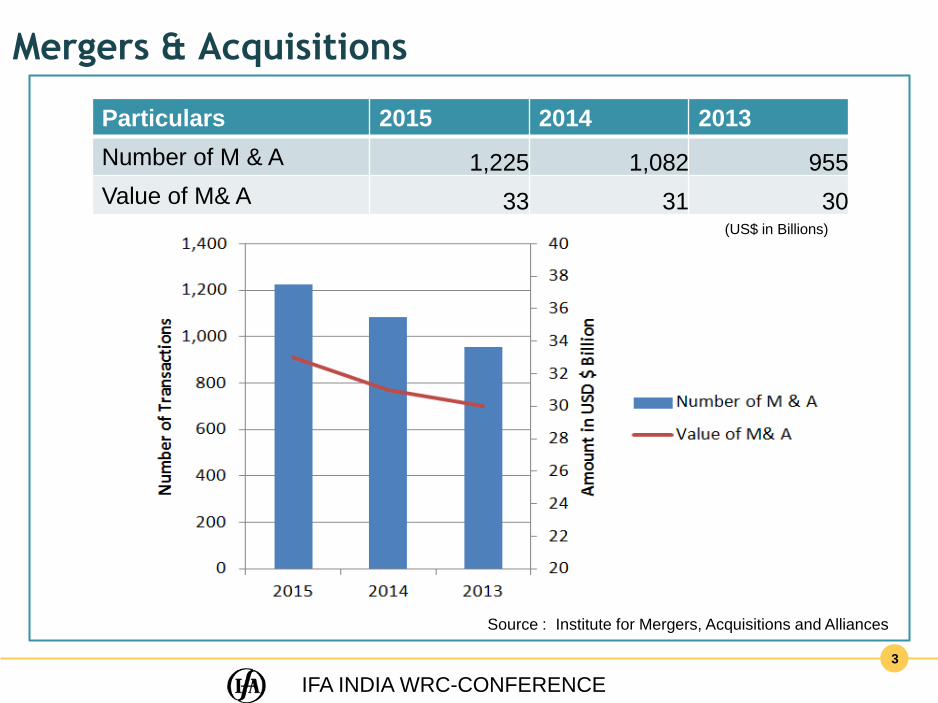

Mergers & Acquisitions

(US$ in Billions)

Particulars 2015 2014 2013

Number of M & A 1,225 1,082 955

Value of M& A 33 31 30

Source : Institute for Mergers, Acquisitions and Alliances

(US$ in Billions)

4

IFA INDIA WRC-CONFERENCE

FDI Inflows, Cross-border M&As, by Region and Major Economy

(US$ in Billions)

Source : United Nation Conference on Trade and Development

Region / Economy FDI Inflows

Cross - Border M &

As

2015 2014 2015 2014

World 1,699 1,245 643.7 398.9

Developed Economies 936 493 566.8 274.5

Europe Union 426 254 269.2 160.6

North America 429 146 242.3 44.1

Developing Economies 741 703 67.6 120.1

Africa 38 55 20.4 5.1

Latin Africa and the

Caribbean 151 170 10.1 25.5

Developing Aisa 548 475 35.3 89.3

Transition Economies 22 49 9.3 4.2

5

IFA INDIA WRC-CONFERENCE

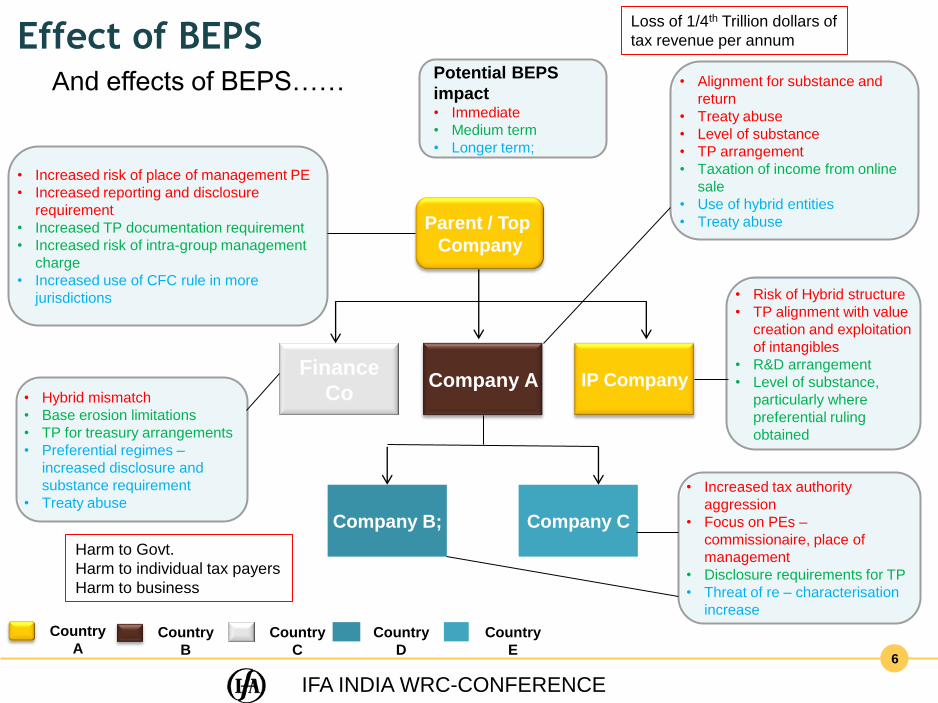

Business Model of a Typical MNC Structure

Parent / Top

Company

Company A

Management

Fee

IP Company Finance

Co

Royalty

License Interest

Loan

Company B Company C

Cost plus payment for

manufacturing of

goods

Cost plus payment for

distribution of goods Country

A Country

B Country

C

Country

D

Country

E

A “brilliant” tax structure in a

pre-BEPS World……

6

IFA INDIA WRC-CONFERENCE

Effect of BEPS

Country

A Country

B

Country

C

Country

D

Country

E

• Increased risk of place of management PE

• Increased reporting and disclosure

requirement

• Increased TP documentation requirement

• Increased risk of intra-group management

charge

• Increased use of CFC rule in more

jurisdictions

Potential BEPS

impact • Immediate

• Medium term

• Longer term;

• Risk of Hybrid structure

• TP alignment with value

creation and exploitation

of intangibles

• R&D arrangement

• Level of substance,

particularly where

preferential ruling

obtained

• Hybrid mismatch

• Base erosion limitations

• TP for treasury arrangements

• Preferential regimes –

increased disclosure and

substance requirement

• Treaty abuse

• Alignment for substance and

return

• Treaty abuse

• Level of substance

• TP arrangement

• Taxation of income from online

sale

• Use of hybrid entities

• Treaty abuse

• Increased tax authority

aggression

• Focus on PEs –

commissionaire, place of

management

• Disclosure requirements for TP

• Threat of re – characterisation

increase

Parent / Top

Company

Company A IP Company Finance

Co

Company B; Company C

And effects of BEPS……

Harm to Govt.

Harm to individual tax payers

Harm to business

Loss of 1/4th Trillion dollars of

tax revenue per annum

7

IFA INDIA WRC-CONFERENCE

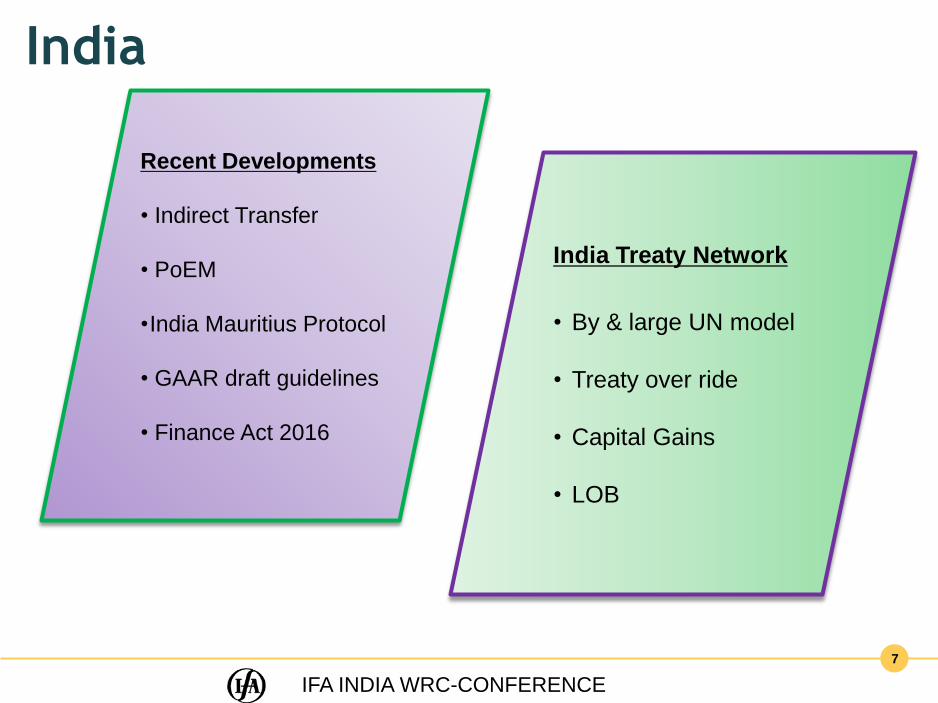

India

Recent Developments

• Indirect Transfer

• PoEM

•India Mauritius Protocol

• GAAR draft guidelines

• Finance Act 2016

India Treaty Network

• By & large UN model

• Treaty over ride

• Capital Gains

• LOB

![Sir, · PDF fileSeminar(Present the seminar report for external evaluation and viva. Seminar should not be project based. ... Insulators, Conductors, Semiconductors [2]](https://static.fdocuments.us/doc/165x107/5ab3b5877f8b9a7e1d8e7cf1/sir-present-the-seminar-report-for-external-evaluation-and-viva-seminar-should.jpg)