Seminar Practice 7 Solutions (Latest).ppt

54

BU8101 SEMINAR PRACTICE 7 Yude Geraldine Jian Yang Hanis

-

Upload

feelingsofly -

Category

Documents

-

view

119 -

download

7

description

accounting

Transcript of Seminar Practice 7 Solutions (Latest).ppt

BU8101 SEMINAR PRACTICE 7YudeGeraldineJian YangHanis

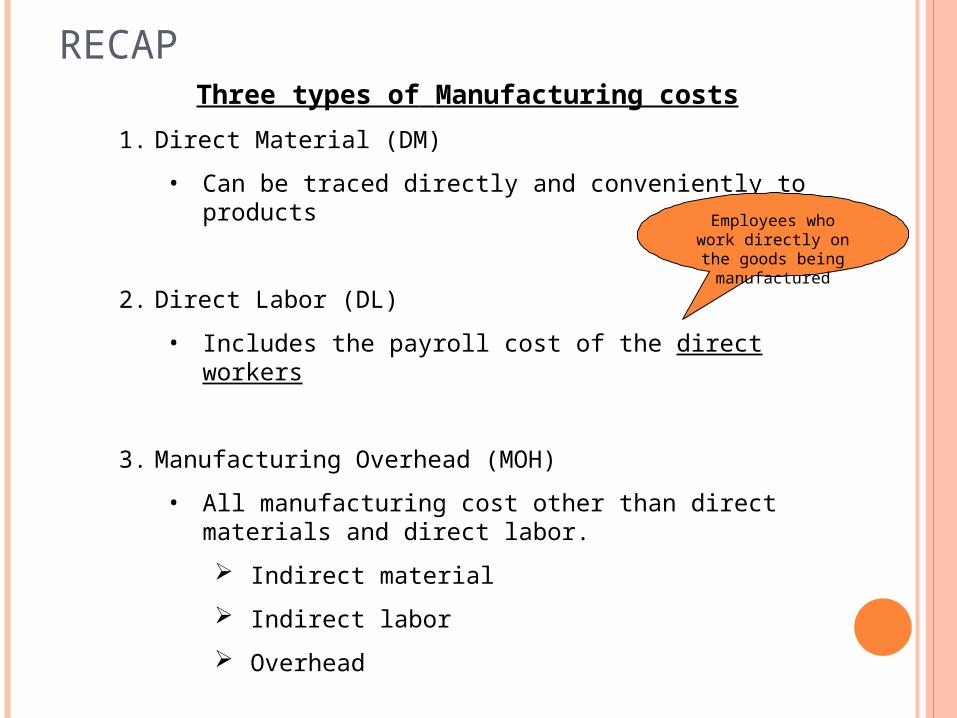

RECAPThree types of Manufacturing costs

1. Direct Material (DM)

• Can be traced directly and conveniently to products

2. Direct Labor (DL)

• Includes the payroll cost of the direct workers

3. Manufacturing Overhead (MOH)

• All manufacturing cost other than direct materials and direct labor.

Indirect material

Indirect labor

Overhead

Employees who work directly on the goods being manufactured

RECAPWhat are the three types of Inventories?

Raw material Inventory - Inventory on hand and

available for use

Work in process Inventory -Partially completed

goods

Finished goods Inventory- Completed goods

awaiting sale

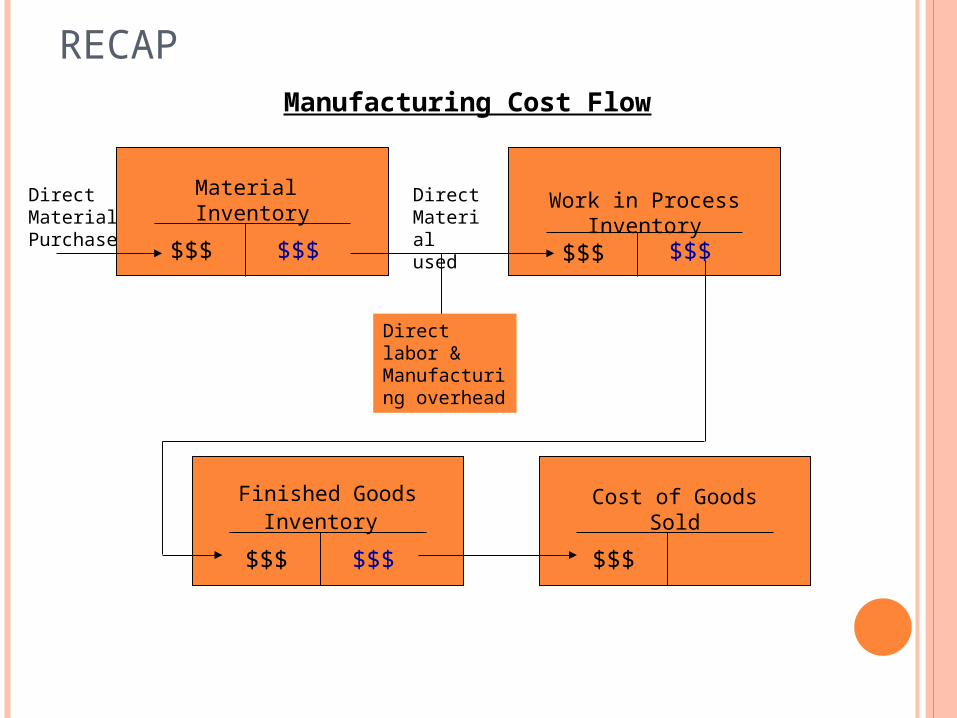

RECAPManufacturing Cost Flow

Material Inventory

Work in ProcessInventory

Finished GoodsInventory

$$$ $$$

Direct Material Purchase

$$$ $$$

Direct Material used

Direct labor & Manufacturing overhead

$$$ $$$

Cost of GoodsSold

$$$

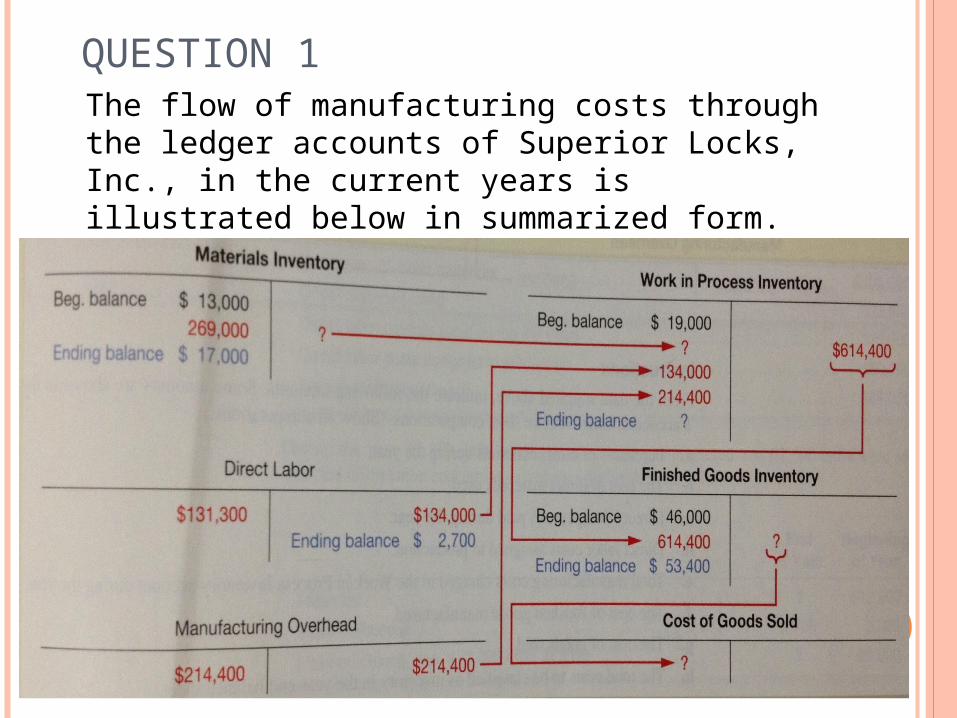

QUESTION 1The flow of manufacturing costs through the ledger accounts of Superior Locks, Inc., in the current years is illustrated below in summarized form.

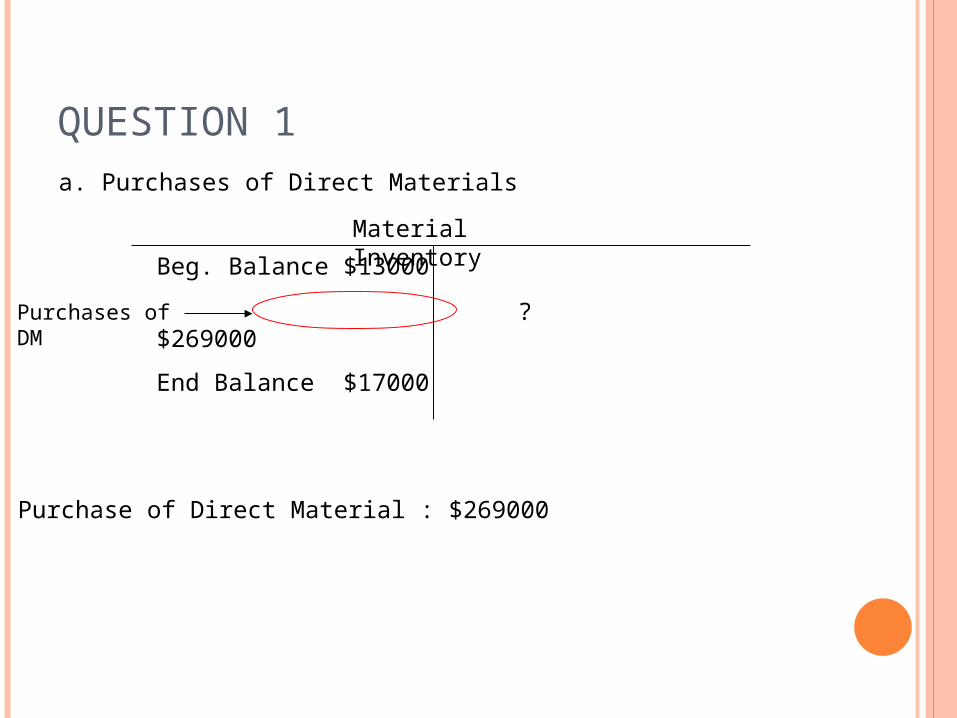

QUESTION 1a. Purchases of Direct Materials

Beg. Balance $13000

$269000

End Balance $17000

Material Inventory

Purchases of DM ?

Purchase of Direct Material : $269000

QUESTION 1b. Cost of Direct Materials used

B. Balance $13000

$269000

End Balance $17000

Material Inventory

Purchases of DM ?

End Balance = Beg. Balance + Purchases of DM - Cost of Direct Material used

Cost of Direct Material used = Beg. Balance + Purchase of DM – End Balance

= $13000 + $269000 - $17000

= $265000

Cost of Direct Material used

QUESTION 1c. Direct Labor costs assigned to production

Direct Labor

131300 134000

End Balance 2700

Direct Labor costs

Direct Labor costs assigned to production : $134000

QUESTION 1d. The year-end liability for direct wages payable

Direct Labor

131300 134000

End Balance 2700

Direct wages payable : $2700

End balance represent the amount owned to employee for work already performed. Therefore, its wages payable, a current liability

Direct Labor costs

QUESTION 1e. Total manufacturing costs charged to the Work in Process Inventory account during the current year.

Work in Process Inventory

$614400

Beg. Balance $19000

$265000

$134000

$214400

End Balance ?

Manufacturing costs = Direct Material costs + Direct Labor costs + Manufacturing Overhead costs

= $265000 + $134000 + $214400

= $613400

Direct MaterialBeg bal. 13000

269000

End bal. 17000

265000

Direct Labor

131300 134000

End bal. $2700

Manufacturing Overhead

214400 214400

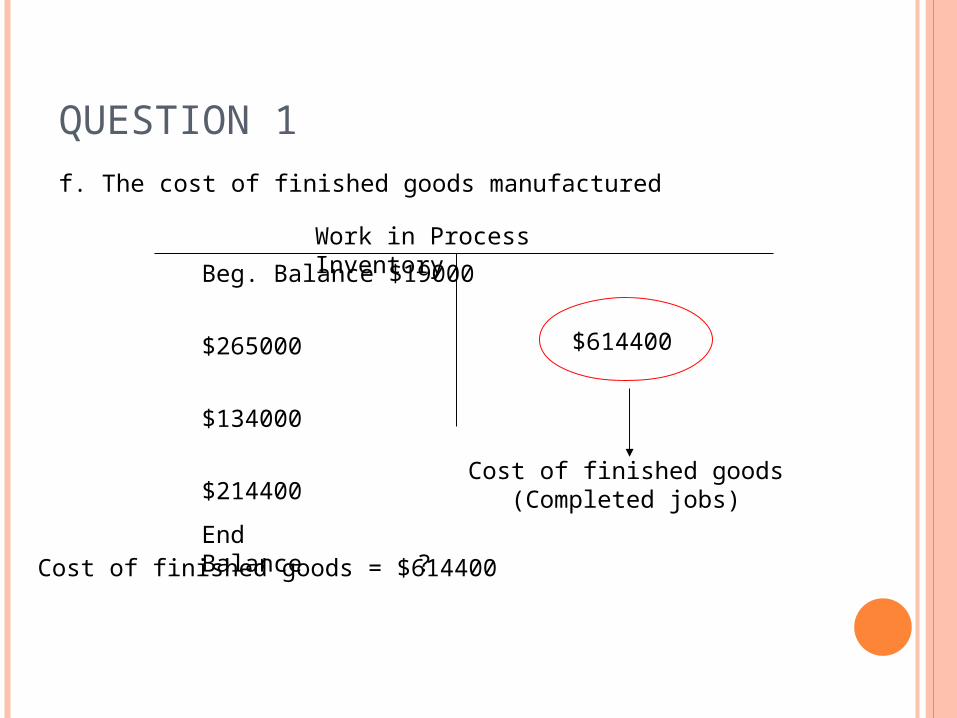

QUESTION 1f. The cost of finished goods manufactured

Work in Process Inventory

$614400

Beg. Balance $19000

$265000

$134000

$214400

End Balance ?

Cost of finished goods = $614400

Cost of finished goods (Completed jobs)

QUESTION 1g. The year-end balance in the Work in Process Inventory account

Work in Process Inventory

$614400

Beg. Balance $19000

$265000

$134000

$214400

End Balance ?

Work in Process End Balance = Beg. Bal. + Manufacturing Costs – Cost of finished goods

= $19000 + $613400 - $ 614400

= $18000

Cost of finished goods (Completed jobs)

Manufacturing Costs =

DM cost + DL cost + MOH cost

= 613400

QUESTION 1h. The cost of goods sold

Finished Goods Inventory

?Beg. Balance $46000

End Balance $53400

Cost of goods sold = Beg. Bal. + Cost of finished goods – End Bal.

= $46000 + $614400 - $53400

= $607000

Work in ProcessBeg bal. 19000

265000

134000

214400

End bal. 18000

614400Cost of finished goods $614400

Cost of Goods Sold

?

QUESTION 1i. The total amount of inventory listed in the year-end balance sheet

Material Inventory

Beg. Balance $13000

$269000

End Balance $17000

$265000

Work in Process Inventory

$614400

Beg. Balance $19000

$265000

$134000

$214400

End Balance $18000

Finished Goods InventoryBeg. Balance $46000

$614400

End Balance $53400

$607000

Total amount of Inventory = 17000 + 18000 + 53400

= $88400

QUESTION 1Overall flow of manufacturing costs

Material Inventory

Beg. Balance $13000

$269000

End Balance $17000

$265000

Work in Process Inventory

$614400

Beg. Balance $19000

$265000

$134000

$214400

End Balance $18000

Finished Goods InventoryBeg. Balance $46000

$614400

End Balance $53400

$607000

Direct Labor

Manufacturing Overhead

$131300 $134000

End bal. $2700

$214400 $214400 Cost of Goods Sold

$607000

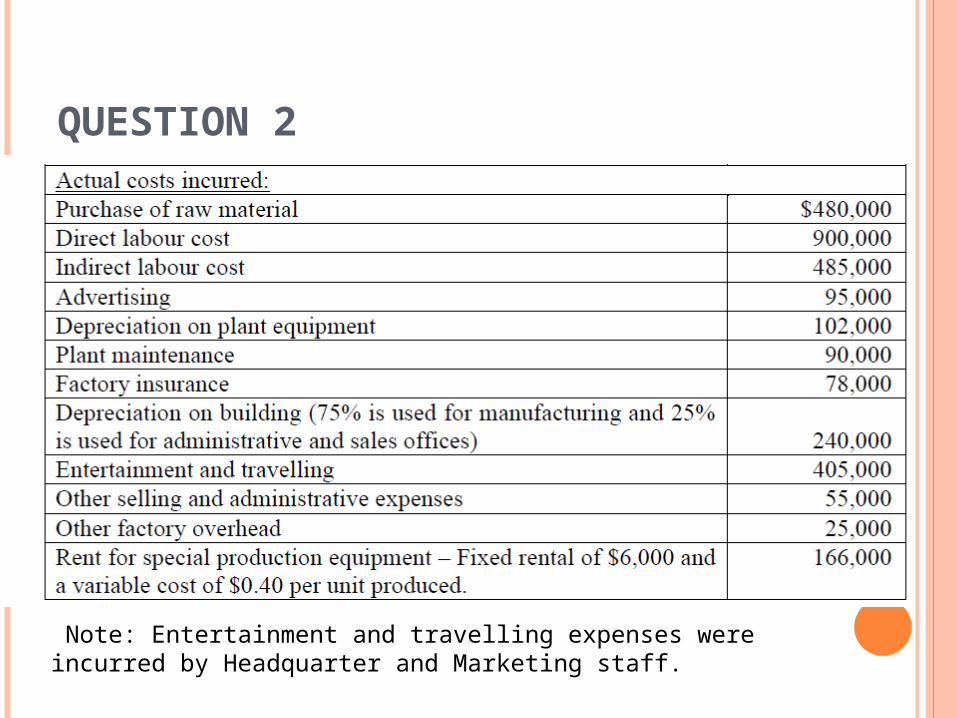

QUESTION 2

QUESTION 2

Note: Entertainment and travelling expenses were incurred by Headquarter and Marketing staff.

QUESTION 2

Part a: Calculate the over/under application of overheads.

Part b: Prepare a schedule of cost of goods manufactured for the year ended 31 December 2009.

A)CALCULATE THE OVER/UNDER APPLICATION OF OVERHEADS.

Three Step Process:

Calculate Predetermined Overhead Rate (POHR)

Apply overhead rate

Reconcile differences between actual and predetermined rate

A)CALCULATE THE OVER/UNDER APPLICATION OF OVERHEADS.

A)CALCULATE THE OVER/UNDER APPLICATION OF OVERHEADS.

Step 2:

Overhead Amount

Indirect labor cost 485,000

Depreciation on plant equipment

102,000

Plant Maintainance 90,000

Factory Insurance 78,000

Depreciation on building(75% for manufacturing)

0.75x240,000=180,000

Other factory overhead 25,000

Rent for special production equipment

166,000

Total $1.126 Million

A)CALCULATE THE OVER/UNDER APPLICATION OF OVERHEADS.

Step 3:

Actual Overhead:$1.126 Million

Applied Overhead: $1.08 Million

>

Overhead is under applied by: 1.126 Million – 1.08 Million = $46,000

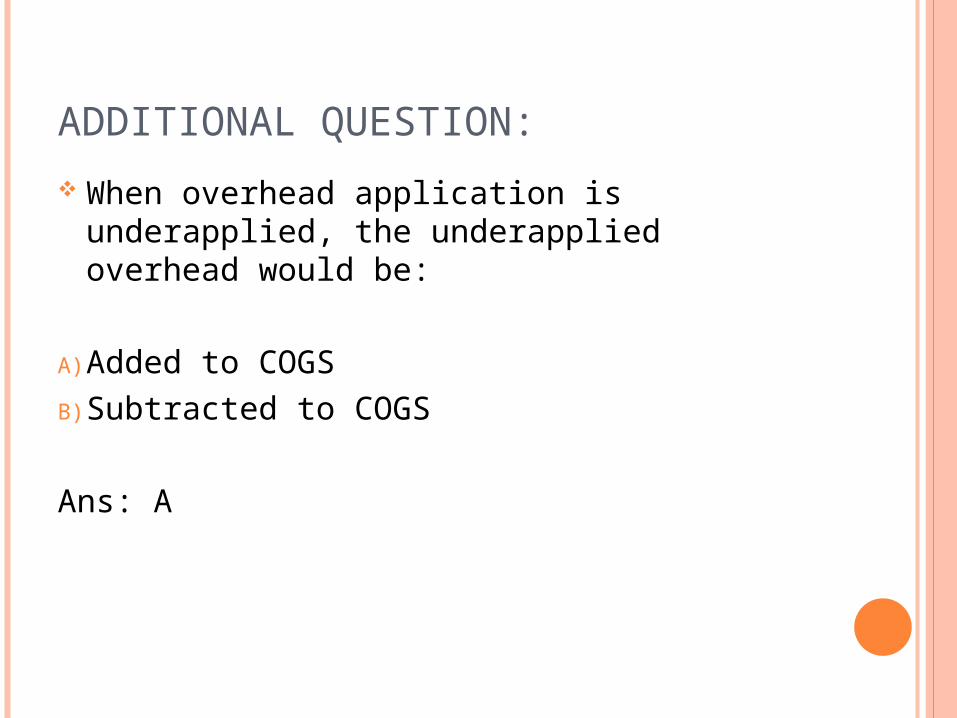

ADDITIONAL QUESTION:

When overhead application is underapplied, the underapplied overhead would be:

A) Added to COGSB) Subtracted to COGS

Ans: A

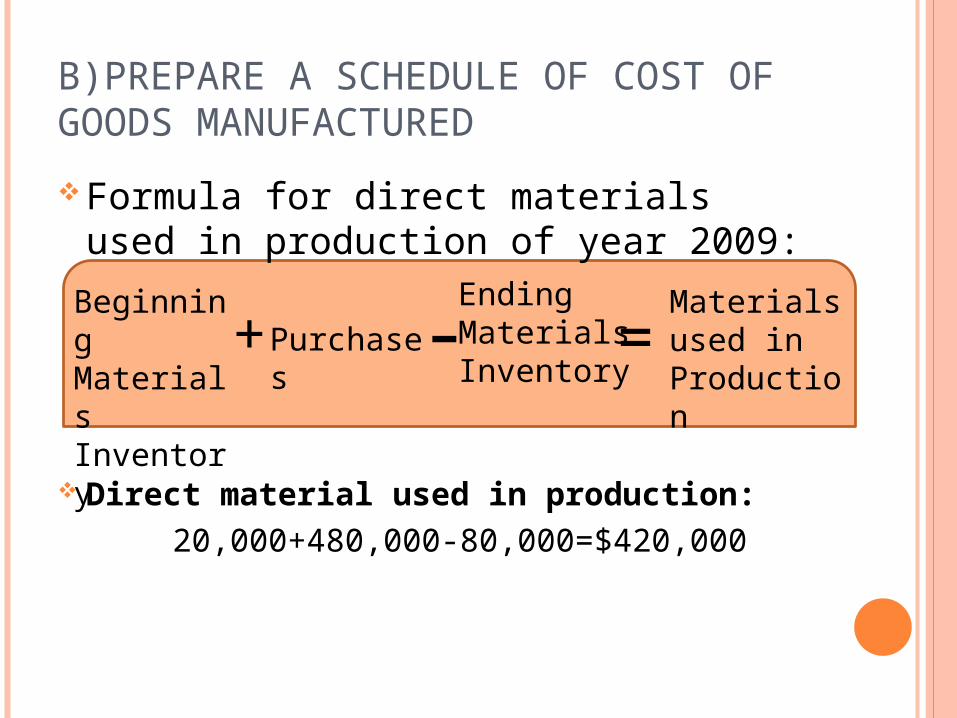

B)PREPARE A SCHEDULE OF COST OF GOODS MANUFACTURED

Formula for direct materials used in production of year 2009:

Direct material used in production: 20,000+480,000-80,000=$420,000

Beginning Materials Inventory

Purchases

Ending Materials Inventory

Materials used in Production

+ - =

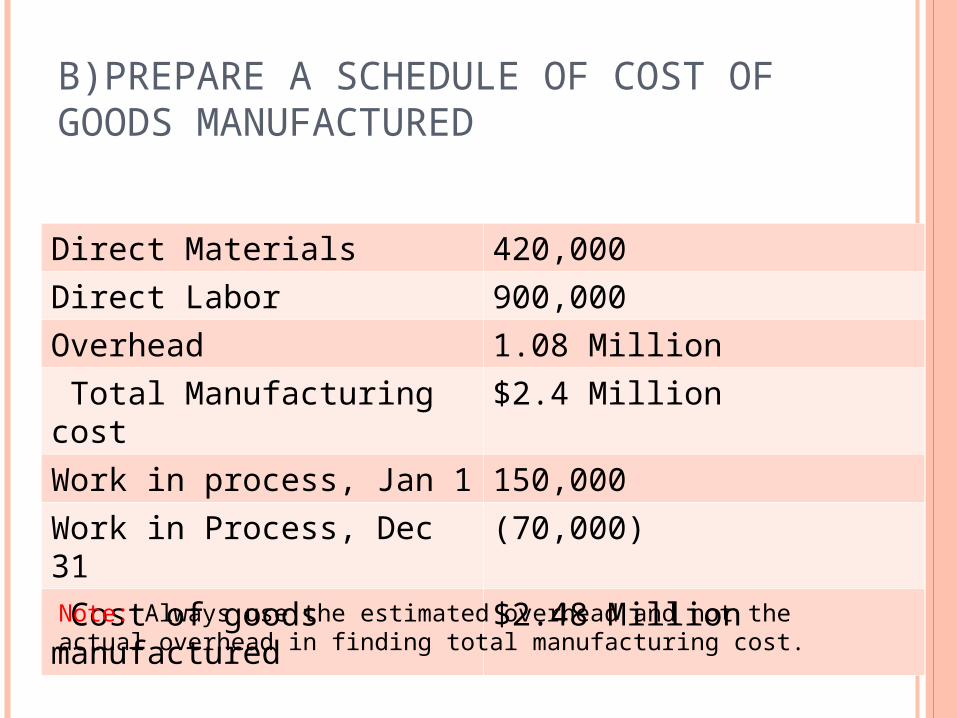

B)PREPARE A SCHEDULE OF COST OF GOODS MANUFACTURED

Direct Materials 420,000

Direct Labor 900,000

Overhead 1.08 Million

Total Manufacturing cost $2.4 Million

Work in process, Jan 1 150,000

Work in Process, Dec 31 (70,000)

Cost of goods manufactured

$2.48 Million

Note: Always use the estimated overhead and not the actual overhead in finding total manufacturing cost.

QUESTION 3

QUESTION 3

A. DETERMINE THE PRODUCTION COSTS ASSIGNED TO EACH JOB AT 30 APRIL, 2012 BY USING THE ABOVE TABLE FOR YOUR COMPUTATION.

Production Cost = Direct Material + Direct Labor + Manufacturing Overhead.

In this question, predetermined overhead rate is 50% of Direct Labor Cost.

A. DETERMINE THE PRODUCTION COSTS ASSIGNED TO EACH JOB AT 30 APRIL, 2012 BY USING THE ABOVE TABLE FOR YOUR COMPUTATION.

Applied Overhead for Job 306:$85,000 x 0.5= $42,500

Applied Overhead for Job 307:$150,000 x 0.5= $75,000

Applied Overhead for Job 308:$105,000 x 0.5= $52,500

A. DETERMINE THE PRODUCTION COSTS ASSIGNED TO EACH JOB AT 30 APRIL, 2012 BY USING THE ABOVE TABLE FOR YOUR COMPUTATION.

Job 306:Beginning Bal. of April$29,000 + $20,000 + $10,000= $59,000Cost During April $135,000+$85,000+$42,500=$262,500 Production Cost for Job 306 = $59,000+ $262,500

= $321,500

A. DETERMINE THE PRODUCTION COSTS ASSIGNED TO EACH JOB AT 30 APRIL, 2012 BY USING THE ABOVE TABLE FOR YOUR COMPUTATION.

Job 307:Beginning Bal. of April$35,000 + $18,000 + $9,000= $62,000Cost During April $220,000+$150,000+$75,000=$445,000Production Cost for Job 307 = $62,000+ $445,000

= $507,000

A. DETERMINE THE PRODUCTION COSTS ASSIGNED TO EACH JOB AT 30 APRIL, 2012 BY USING THE ABOVE TABLE FOR YOUR COMPUTATION.

Job 308:Cost During April$100,000+$105,000+$52,500=$257,500 Production Cost for Job 308 =$257,500

B. SHOW HOW INVENTORIES WOULD BE REPORTED IN THE BALANCE SHEET AT 30 APRIL, 2012.

According to this figure,

B. SHOW HOW INVENTORIES WOULD BE REPORTED IN THE BALANCE SHEET AT 30 APRIL, 2012.

Raw Material: Beginning Balance =$80,000 Purchases= $500,000 Indirect Material= $50,000 Used material for Job 306, 307, 308 during

April= $135,000 + $220,000 + $100,000 = $455,000

Left Over Material = $500,000 + $80,000 - $50,000 - $455,000= $75,000

B. SHOW HOW INVENTORIES WOULD BE REPORTED IN THE BALANCE SHEET AT 30 APRIL, 2012.

Work In Process (Job 308)=$100,000 + $105,000 + $52,500=$257,500

B. SHOW HOW INVENTORIES WOULD BE REPORTED IN THE BALANCE SHEET AT 30 APRIL, 2012.

Finished Goods:Beginning Balance of Job 307 = $35,000+ $18,000+ $9,000 = $62,000Cost for Job 307 during April =$220,000 + $150,000 + $75,000= $445,000

Finished Goods but unsold at the end of April=$62,000+$445,000= $507,000

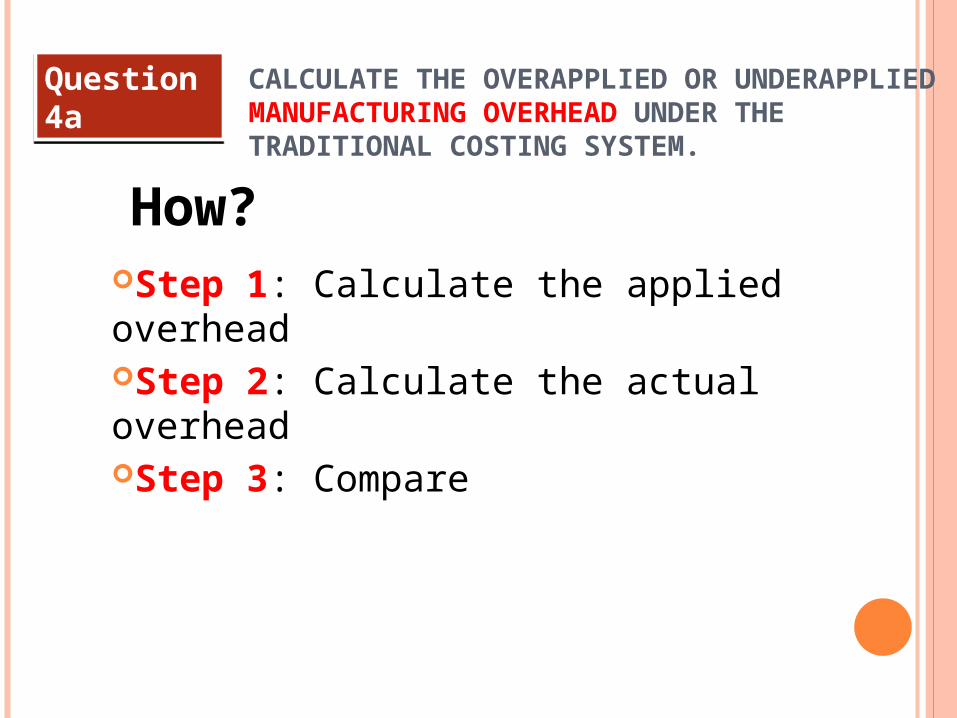

QUESTION 4

Watersport CompanyOverhead rate: $13 per DLHEstimated manufacturing overhead: $143,000Estimated DLH: 11,000 hours

Actual Operating Info 2010

For ABC

CALCULATE THE OVERAPPLIED OR UNDERAPPLIED MANUFACTURING OVERHEAD UNDER THE TRADITIONAL COSTING SYSTEM.

How?Step 1: Calculate the applied overheadStep 2: Calculate the actual overheadStep 3: Compare

Question 4aQuestion 4a

Manufacturing overhead(Recreation Canoe) = Overhead Rate × Actual Activity Level= $13 per DLH × (10 ×800) DLH = $104,000

Manufacturing overhead(Competition Canoe) = Overhead Rate × Actual Activity Level= $13 per DLH × (10 ×200) DLH = $26,000

Total Applied Manufacturing overhead = $104,000+$26,000= $130,000

Question 4aQuestion 4a

Step 1: Calculate the applied overhead

Recreation Canoe:

They take 10 hours per unit ($100 ÷ $10 per hour)

Competition Canoe:

They take 10 hours per unit ($100 ÷ $10 per hour)

20 hours

Actual Activity

Overapplied or Underapplied?

Question 4aQuestion 4a

Step 2: Calculate the actual overhead

Total Actual Manufacturing overhead = $25,000+$20,000+$15,000+$10,000+$10,000+$20,000+$30,000= $130,000 = $260,000 (Applied MOH)

Step 3: Compare

Neither Overapplied nor Underapplied

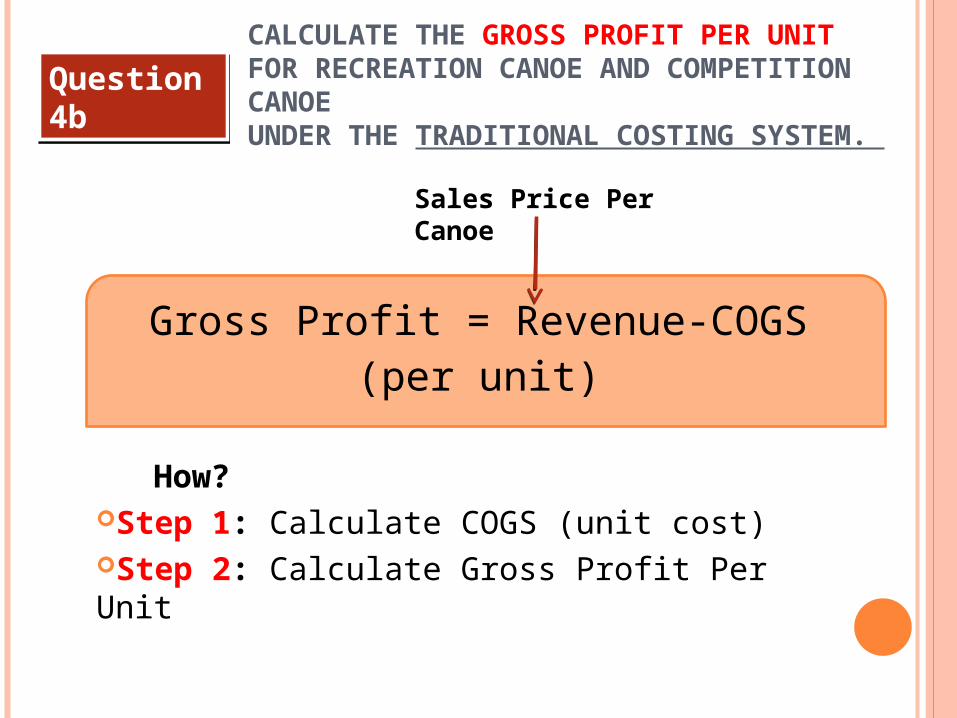

CALCULATE THE GROSS PROFIT PER UNIT FOR RECREATION CANOE AND COMPETITION CANOE UNDER THE TRADITIONAL COSTING SYSTEM.

Question 4bQuestion 4b

Gross Profit = Revenue-COGS(per unit)

Sales Price Per Canoe

How?Step 1: Calculate COGS (unit cost)Step 2: Calculate Gross Profit Per Unit

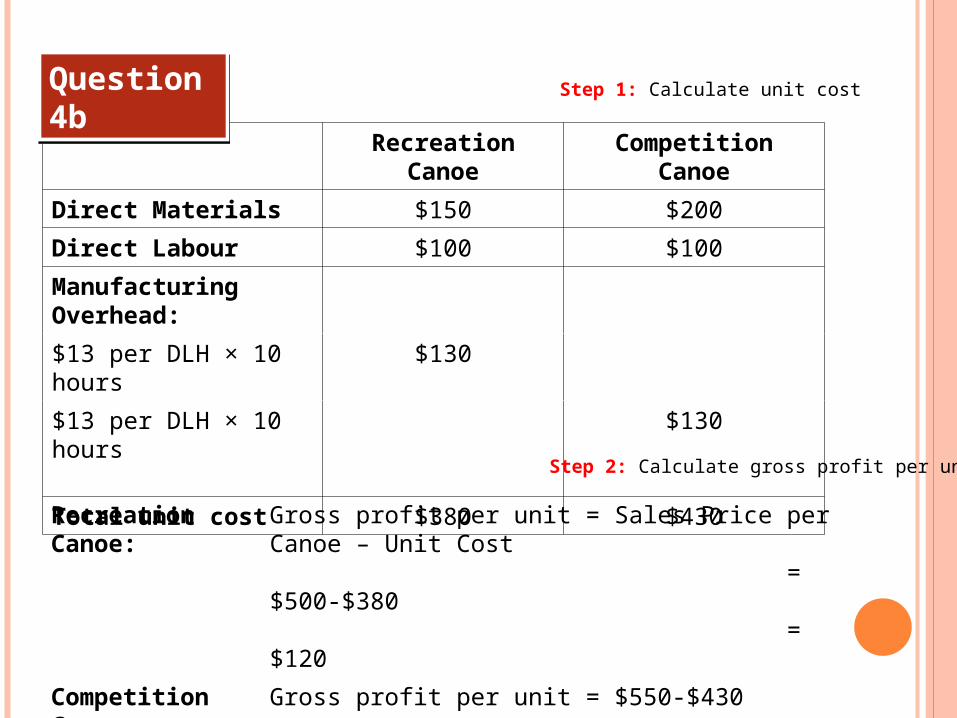

Recreation Canoe

Competition Canoe

Direct Materials $150 $200

Direct Labour $100 $100

Manufacturing Overhead:

$13 per DLH × 10 hours

$130

$13 per DLH × 10 hours

$130

Total unit cost $380 $430

Question 4bQuestion 4b

Step 1: Calculate unit cost

Step 2: Calculate gross profit per unit

Recreation Canoe:

Gross profit per unit = Sales Price per Canoe – Unit Cost = $500-$380 = $120

Competition Canoe:

Gross profit per unit = $550-$430 = $120

CALCULATE THE GROSS PROFIT PER UNIT FOR

RECREATION CANOE AND COMPETITION CANOE UNDER THE ACTIVITY-BASED COSTING SYSTEM.

Question 4cQuestion 4c

ABC:5-Step Computation

How?Similarly…Step 1: Calculate COGS (unit cost)

Step 2: Calculate Gross Profit Per Unit

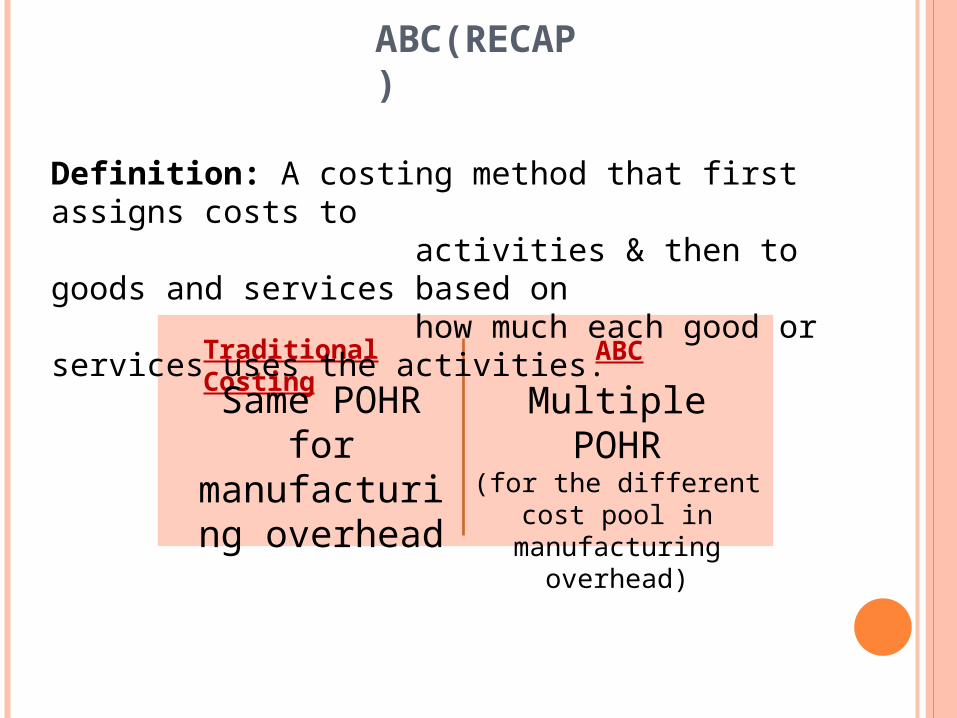

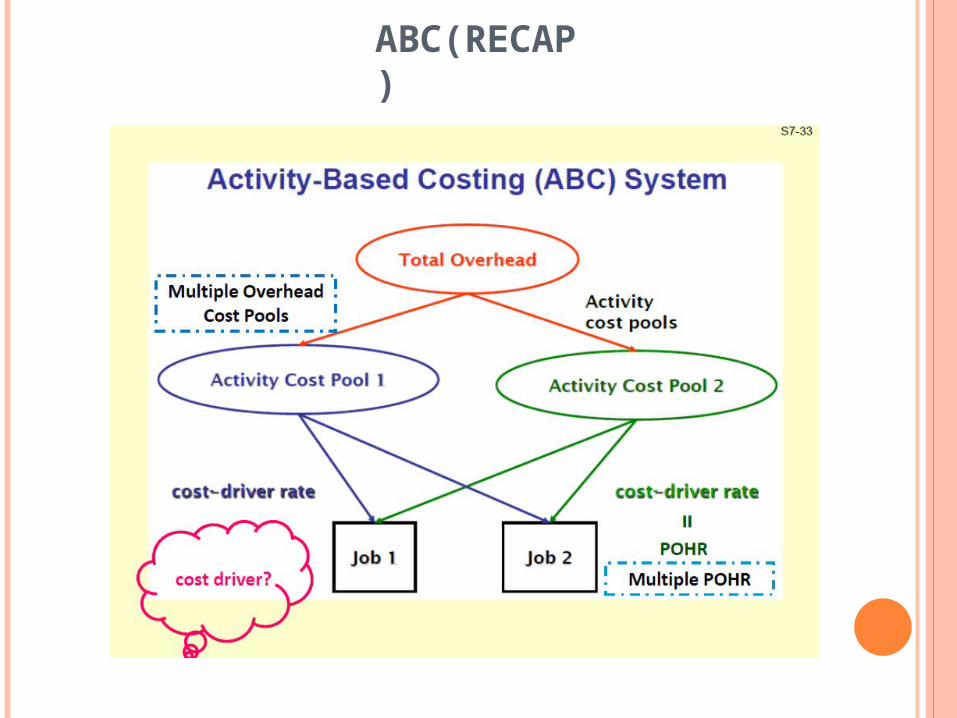

ABC(RECAP)

Traditional Costing

ABCSame POHR

for manufacturing overhead

Multiple POHR(for the different cost

pool in manufacturing

overhead)

Definition: A costing method that first assigns costs to activities & then to goods and services based on how much each good or services uses the activities.

ABC(RECAP)

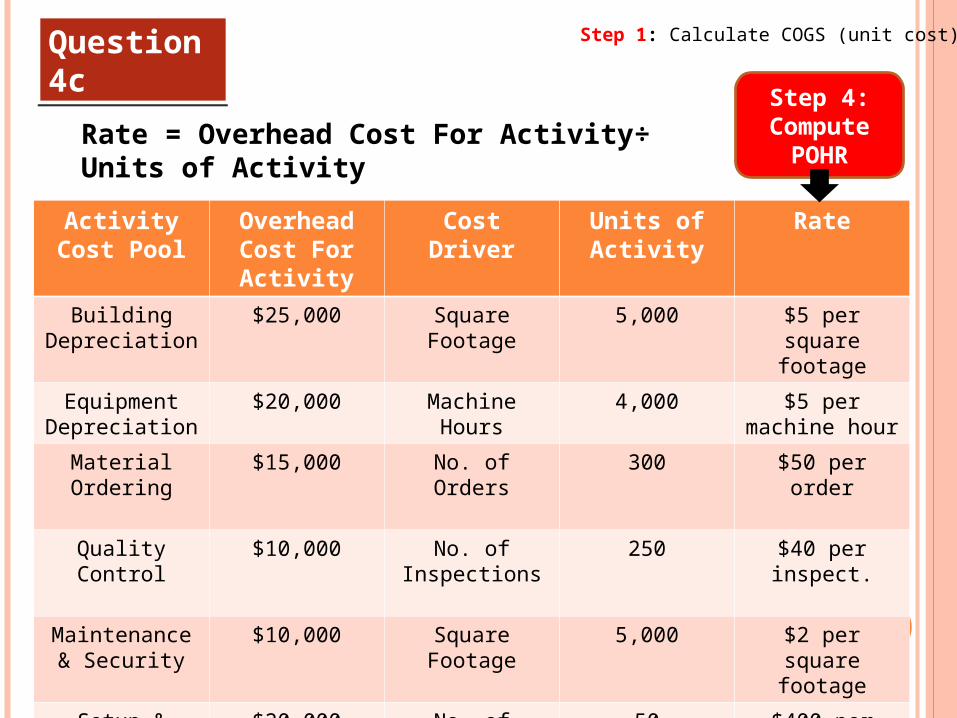

ActivityCost Pool

Overhead Cost For Activity

Cost Driver Units of Activity

Rate

Building Depreciation

$25,000 Square Footage

5,000 $5 per square footage

Equipment Depreciation

$20,000 Machine Hours

4,000 $5 per machine hour

Material Ordering

$15,000 No. of Orders 300 $50 per order

Quality Control

$10,000 No. of Inspections

250 $40 per inspect.

Maintenance & Security

$10,000 Square Footage

5,000 $2 per square footage

Setup & Drafting

$20,000 No. of Setups 50 $400 per setup

Supervision $30,000 Dir. Labour Costs

100% $3 per DLC

Question 4cQuestion 4c

Step 1: Identify

Activities

Step 3: Identify

Cost Driver

Step 2: Assign Cost to

Cost Pools

Step 1: Calculate COGS (unit cost)

ActivityCost Pool

Overhead Cost For Activity

Cost Driver Units of Activity

Rate

Building Depreciation

$25,000 Square Footage

5,000 $5 per square footage

Equipment Depreciation

$20,000 Machine Hours

4,000 $5 per machine hour

Material Ordering

$15,000 No. of Orders 300 $50 per order

Quality Control

$10,000 No. of Inspections

250 $40 per inspect.

Maintenance & Security

$10,000 Square Footage

5,000 $2 per square footage

Setup & Drafting

$20,000 No. of Setups 50 $400 per setup

Supervision $30,000 Dir. Labour Costs

100% $3 per DLC

Question 4cQuestion 4c Units of Activity =

Activity Level For Recreation Canoe + Activity Level For Competition Canoe

Step 1: Calculate COGS (unit cost)

ActivityCost Pool

Overhead Cost For Activity

Cost Driver Units of Activity

Rate

Building Depreciation

$25,000 Square Footage

5,000 $5 per square footage

Equipment Depreciation

$20,000 Machine Hours

4,000 $5 per machine hour

Material Ordering

$15,000 No. of Orders 300 $50 per order

Quality Control

$10,000 No. of Inspections

250 $40 per inspect.

Maintenance & Security

$10,000 Square Footage

5,000 $2 per square footage

Setup & Drafting

$20,000 No. of Setups 50 $400 per setup

Supervision $30,000 Dir. Labour Costs

100% $3 per DLC

Question 4cQuestion 4c

Step 4:Compute

POHRRate = Overhead Cost For Activity÷ Units of Activity

Step 1: Calculate COGS (unit cost)

ActivityCost Pool

Rate ACTUAL UNITS

OF ACTIVIT

Y

COST ALLOCATE

D TO PRODUCT

ACTUAL UNITS

OF ACTIVIT

Y

COST ALLOCATE

D TO PRODUCT

Building Depreciatio

n

$5 per square footage

4,000 $20,000 1,000 $5,000

Equipment Depreciatio

n

$5 per machine

hour

3,400 $17,000 600 $3,000

Material Ordering

$50 per order

200 $10,000 100 $5,000

Quality Control

$40 per inspection

160 $6,400 90 $3,600

Maintenance &

Security

$2 per square footage

4,000 $8,000 1,000 $2,000

Setup & Drafting

$400 per setup

20 $8,000 30 $12,000

Supervision $3 per DLC 90% $27,000 100% $3,000

Question 4cQuestion 4c

Step 1: Calculate COGS (unit cost)

Recreation Canoe Competition Canoe

Step 5:Allocate cost to Product

$96,400 $33,600Total Overhead

Cost Allocated to Product = Rate × Actual Units of

Activity

COST ALLOCATED TO PRODUCT

COST ALLOCATED TO PRODUCT

Total Overhead $96,400 $33,600

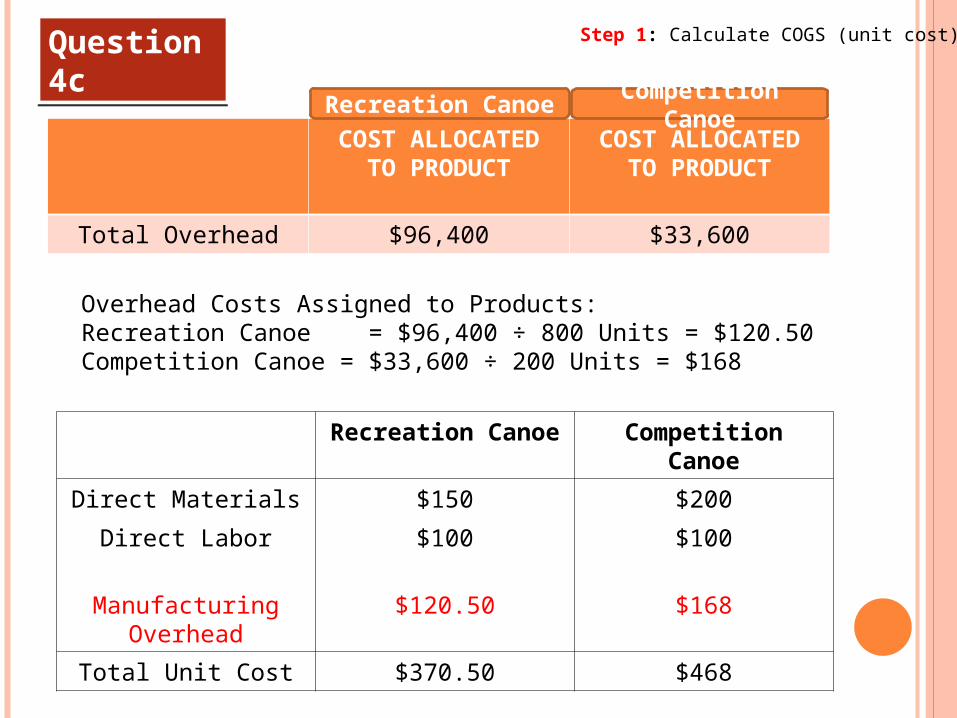

Step 1: Calculate COGS (unit cost)Question 4cQuestion 4c Recreation

CanoeCompetition

Canoe

Overhead Costs Assigned to Products:Recreation Canoe = $96,400 ÷ 800 Units = $120.50Competition Canoe = $33,600 ÷ 200 Units = $168

Recreation Canoe Competition Canoe

Direct Materials $150 $200

Direct Labor $100 $100

Manufacturing Overhead

$120.50 $168

Total Unit Cost $370.50 $468

Step 2: Calculate Gross Profit Per UnitQuestion 4cQuestion 4c

Recreation Canoe Competition Canoe

Direct Materials $150 $200

Direct Labor $100 $100

Manufacturing Overhead

$120.50 $168

Total Unit Cost $370.50 $468

For Recreation Canoe : Gross Profit per unit = $500 - $370.50 = $129.50

For Competition Canoe:Gross Profit per unit = $550 - $468 = $82

Question 4cQuestion 4c

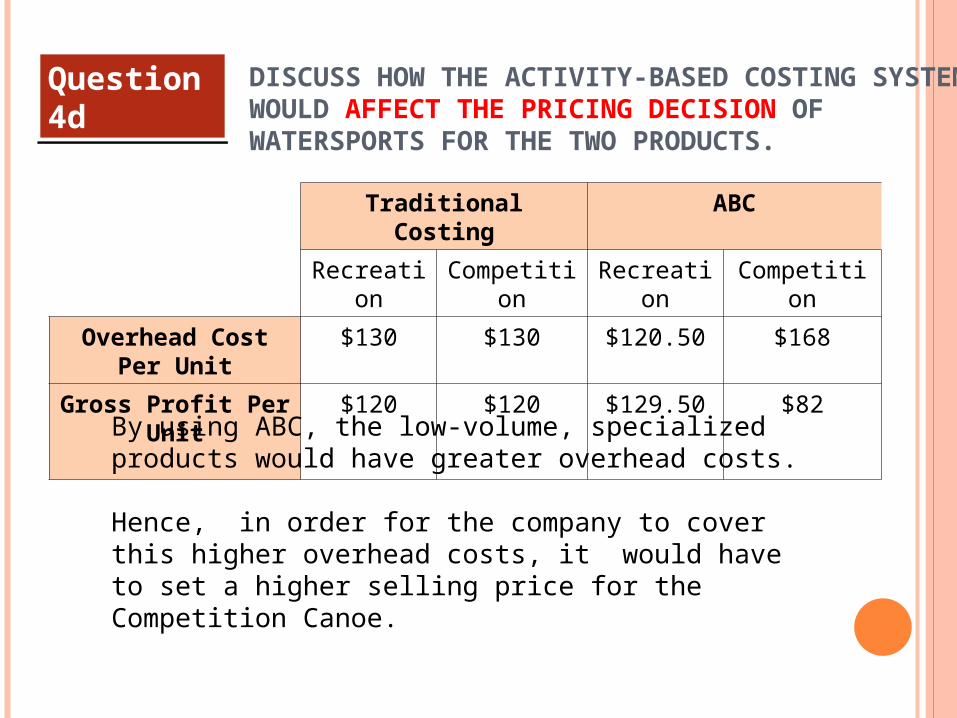

DISCUSS HOW THE ACTIVITY-BASED COSTING SYSTEM WOULD AFFECT THE PRICING DECISION OF WATERSPORTS FOR THE TWO PRODUCTS.

Traditional Costing ABC

Recreation

Competition

Recreation

Competition

Overhead Cost Per Unit

$130 $130 $120.50 $168

Gross Profit Per Unit

$120 $120 $129.50 $82

Question 4dQuestion 4d

By using ABC, the low-volume, specialized products would have greater overhead costs.

Hence, in order for the company to cover this higher overhead costs, it would have to set a higher selling price for the Competition Canoe.