Selling to the brain - Midwest Pension Conference › forms › 2012 › MWPC...-Think Twice:...

35

Selling to the brain: Understanding the mechanics of decision-making Name Title Legg Mason INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Transcript of Selling to the brain - Midwest Pension Conference › forms › 2012 › MWPC...-Think Twice:...

Selling to the brain:Understanding the mechanics of decision-making

NameTitleLegg Mason

INVESTMENT PRODUCTS: NOT FDIC INSURED • NO BANK GUARANTEE • MAY LOSE VALUE

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

1For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

About Michael Mauboussin

• Chief Investment Strategist, Legg Mason Capital Management

• Author- Think Twice: Harnessing the Power of

Counterintuition

- More Than You Know: Finding Financial Wisdom in Unconventional Places

• Co-author, with Alfred Rappaport, of Expectations Investing: Reading Stock Prices for Better Returns

• Adjunct professor of finance at Columbia Business School since 1993 and is on the faculty of the Heilbrunn Center for Graham and Dodd Investing

2For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Today’s Agenda

• Understanding the Decision-Making Framework

• The Mechanics of Decision-Making

- Hyperbolic Discounting

- Defaults

- Choice Architecture

• Action Steps

3For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Understanding the Decision-Making Framework

4For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Hyperbolic Discounting

5For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Hyperbolic Discountingthe tendency for people to prefer smaller payoffs now over larger payoffs later

6

Exponential Discounting: Time-consistent model –assumes a constant discount rate, with valuations falling by a constant factor per unit delay

Hyperbolic Discounting: Time-inconsistent model –assumes a varying discount rate, with valuations falling rapidly for small delay periods, but slowly for longer delay periods

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

7

Constant rate of decline Rapid rate of decline in short run

Slow rate of decline

in long run

Hyperbolic DiscountingExponential Discounting

Hyperbolic Discounting The perception of delayed rewards

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

8

Today Tomorrow

+

One yearOne year and one day

+

Source: Shane Frederick; George Loewenstein; Ted O'Donoghue, “Time Discounting and Time Preference: A Critical Review,” Journal of Economic Literature, Volume 40, No. 2. (June, 2002), 351-401.

Time discounting and time preference: 10% tomorrow vs. 10% in the future

“We want to be good in the future but are looking for the instant gratification today.”

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

9

Choose among 24 movie videos:• Some are low brow: e.g., The Hangover • Some are high brow: e.g., Schindler’s List

“Tonight, I want to have fun . . . next week I want things that are good for me.”

Source: Reed, Lowenstein, and Kalyanaraman, “Mixing Virtue and Vice: Combining the immediacy effect and the diversification heuristic, Journal of Behavioral Decision Making, 12, 257-273, November 1998, Published 1999.

Choosing for tonight Choosing for Next Wednesday Choosing for Second Wednesday

High brow

High brow High browLow brow Low brow

Mixing virtue and vice

Low browLow browLow brow

High browHigh browHigh brow

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

10

70%To eat today

To eat next week74%

Source: Read, D. and van Leeuwen, B., “Predicting Hunger: The effects of appetite and delay on choice,” Organizational behavior and human decision processes, 76, 189-205, 1998.

The healthy-unhealthy choice

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

U.S. Military Severance Packages

11

OfficersEnlisted

Annuity worth $83KLump Sum $46K

Lump sumAnnuity

Lump sum

Annuity worth $40K

Lump Sum $22K

Source: John T. Warner and Saul Pleeter, “The Personal Discount Rate: Evidence from military downsizing programs,” The American Economic Review, 91 (1), 33-53, March 2001.

Lump sum

Lump sumAnnuity

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Annuity

12

0.0

-0.05

0.05

ChooseSmaller

ImmediateReward

ChooseLarger

DelayedReward

EmotionalSystem

Frontalsystem

Bra

in A

ctiv

ity

Source: Samuel M. McClure, David I. Laibson, George Loewenstein, and Jonathan D. Cohen, “Separate Neural Systems Value Immediate and Delayed Monetary Rewards,” Science, Volume 306, October 15, 2004, 503-507.

Brain Activity: Frontal vs. Emotional Systems

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Hyperbolic Discounting & RetirementEffective dates of savings increases generally occur in the future

13

8.9% 9.4%

6.0%5.4% 5.8%

6.4% 6.2% 5.9%7.2%

6.5% 6.7%

15.7%

10.0%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

1 2 3 4 5 6 7 8 9 10 11 12 13+

*Source: Choice Architecture and Retirement Savings Plans, by Shlomo Benartzi, Ehud Peleg, Richard H. Thaler.

Participants’ Choices of the Delay Between Signing Up for the Program and the Effective Date of the Savings Increase

• 8.9% prefer the saving increase to be implemented within the same month they sign up

• 91.9% prefer to postpone

• 15.7% prefer that the first increase take place exactly one year after signing up

• 10% would like to wait longer than a year

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

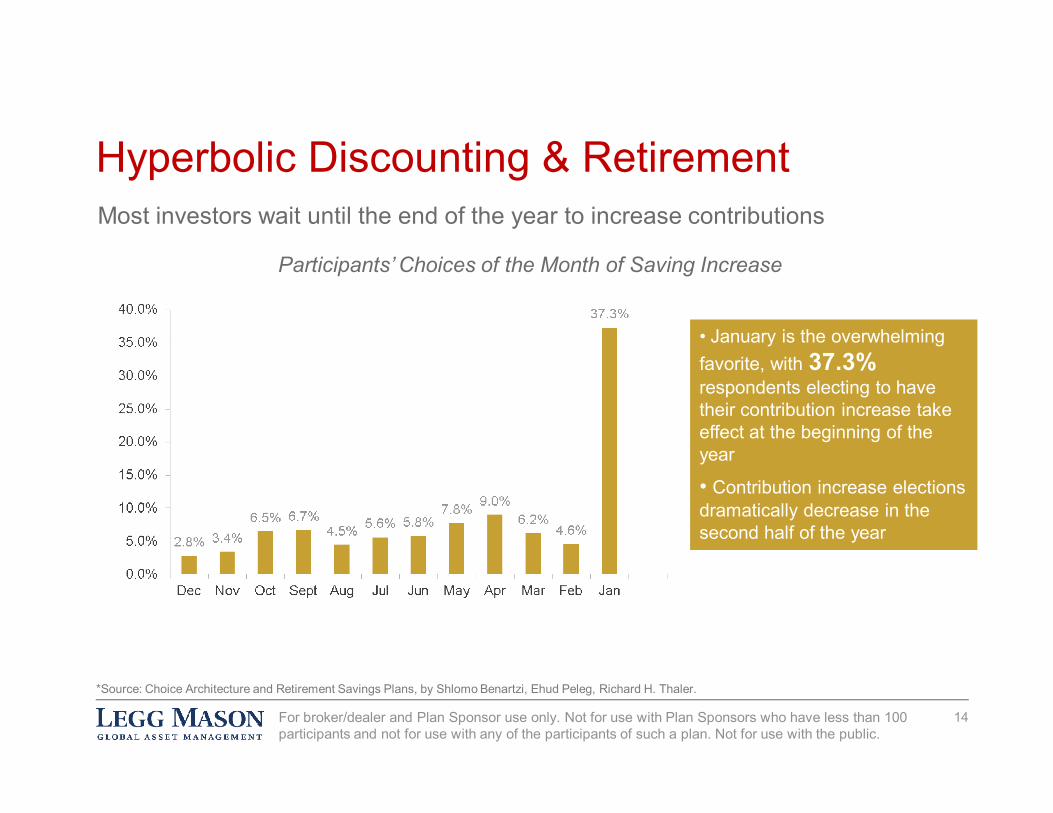

Hyperbolic Discounting & RetirementMost investors wait until the end of the year to increase contributions

14

*Source: Choice Architecture and Retirement Savings Plans, by Shlomo Benartzi, Ehud Peleg, Richard H. Thaler.

Participants’ Choices of the Month of Saving Increase

• January is the overwhelming favorite, with 37.3% respondents electing to have their contribution increase take effect at the beginning of the year

• Contribution increase elections dramatically decrease in the second half of the year

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

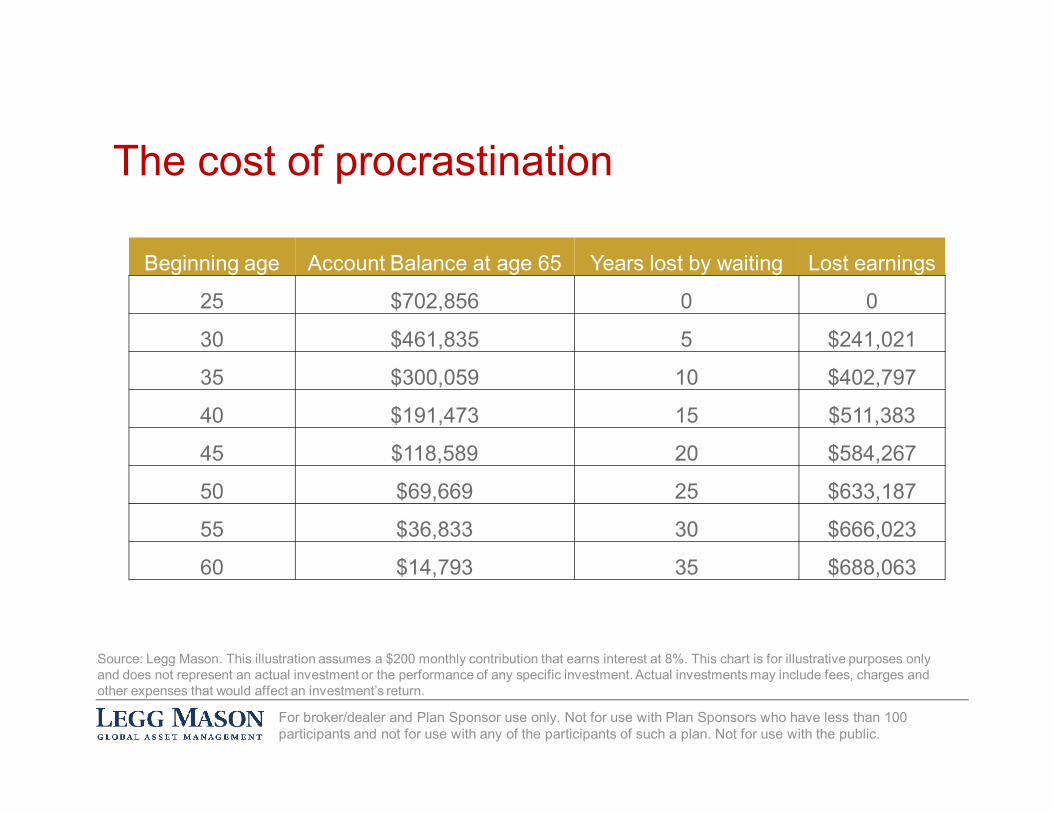

The cost of procrastination

Source: Legg Mason. This illustration assumes a $200 monthly contribution that earns interest at 8%. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. Actual investments may include fees, charges and other expenses that would affect an investment’s return.

Beginning age Account Balance at age 65 Years lost by waiting Lost earnings

25 $702,856 0 0

30 $461,835 5 $241,021

35 $300,059 10 $402,797

40 $191,473 15 $511,383

45 $118,589 20 $584,267

50 $69,669 25 $633,187

55 $36,833 30 $666,023

60 $14,793 35 $688,063

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Lesson Learned

16

There is a natural tendency to postpone the “right” decision• Provoke action by showing the high cost of procrastination

• Appeal to emotions by taking a role in helping others envision their retirement

• Encourage retirement savings plan participation

–Escalator programs

–Corporate matches

–Profit-sharing

“As predicted by hyperbolic discounting, the rewards provided by buying something today often outweigh the discounted pleasure of future payments.”–Joe Redden, Marketing Professor and founder of BehaviorLab.org

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Defaults

17For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

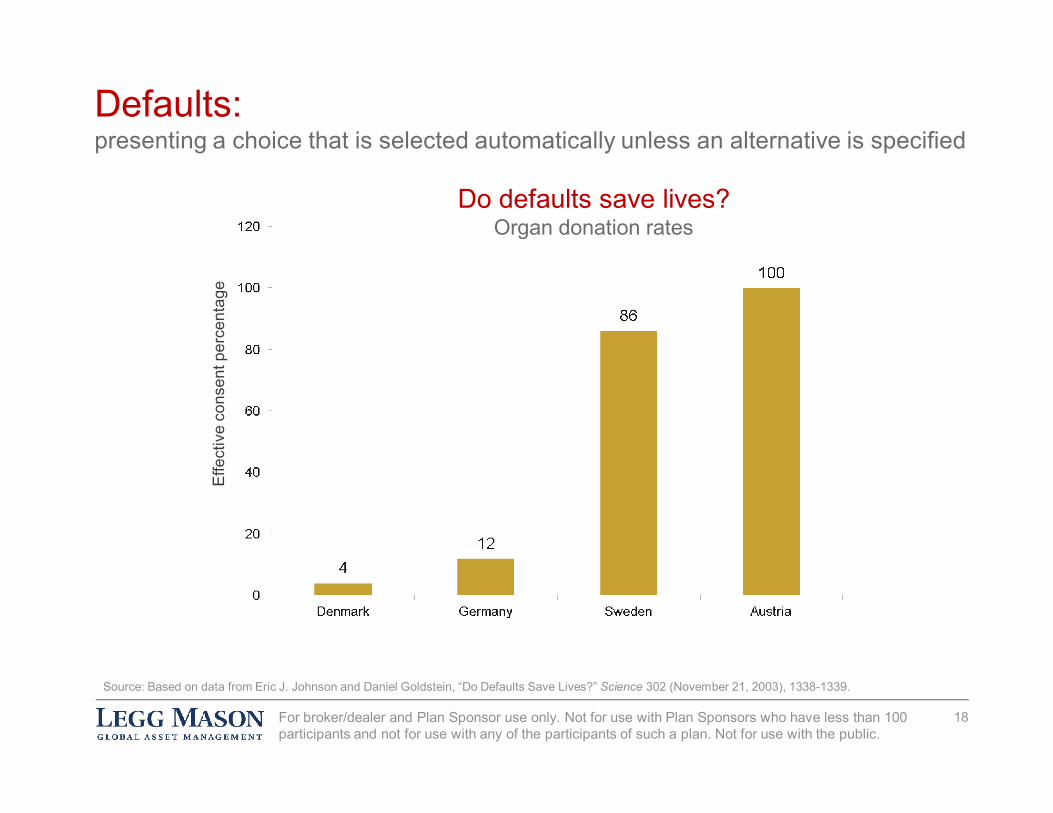

Defaults:presenting a choice that is selected automatically unless an alternative is specified

18

Source: Based on data from Eric J. Johnson and Daniel Goldstein, “Do Defaults Save Lives?” Science 302 (November 21, 2003), 1338-1339.

Do defaults save lives? Organ donation rates

Effe

ctiv

e co

nsen

t per

cent

age

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Auto insurance and default options

19

New Jersey

Pennsylvania

Default choice

Limited right to sue

Full right to sue

Limited right to sue

Full right to sue

Full right to sue

Limited right to

sue

State Preference

Source: Eric J. Johnson, Mary Steffel, and Daniel G. Goldstein, “Making Better Decisions: From Measuring to Constructing Preferences,” Health Psychology, 2005, Volume 24, No. 4 (Suppl.), S17-S22.

Full right to sue

Full right to sue

Limited right to sue

Limited right to

sue

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Defaults & Retirement

• Defaults exert tremendous influence on realized savings outcomes at every stage of the savings lifecycle:

– Savings plan participation

– Contributions

– Asset Allocation

– Rollovers

– Decumulation

• Defaults are not neutral – they can either facilitate or hinder better savings outcomes

20

Source: The Importance of Default Options for Retirement Savings Outcomes: Evidence from the United States, by John Beshears, James J. Choi, David Laibson, Brigitte C. Madrian, National Bureau of Economic Research, January 2006.

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Savings Plan Participation

21

Source: The Importance of Default Options for Retirement Savings Outcomes: Evidence from the United States, by John Beshears, James J. Choi, David Laibson, Brigitte C. Madrian, National Bureau of Economic Research, January 2006.

• Under automatic enrollment, participation jumps to approximately 95% of employees once it takes effect and increases only slightly thereafter• At low levels of tenure, the difference in participation rates under the standard enrollment and automatic enrollment scenarios is substantial – 35 percentage points at three months of tenure

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Contributions

22

Source: The Importance of Default Options for Retirement Savings Outcomes: Evidence from the United States, by John Beshears, James J. Choi, David Laibson, Brigitte C. Madrian, National Bureau of Economic Research, January 2006.

• Under the 3%default scenario, 28% of participants opted for the default

• Under the 6% default scenario, 49% of participants opted for the default

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

The Default Impact: A Tale of Two Investors

Source: Legg Mason. This illustration assumes an annual contribution of 3% ($2,250) and 6% ($4,500) on gross annual income of $75,000 that earns interest at 6% annually. This chart is for illustrative purposes only and does not represent an actual investment or the performance of any specific investment. Actual investments may include fees, charges and other expenses that would affect an investment’s return.

3% annual contribution ($2,250) vs. 6% annual contribution ($4,500) based on gross income of $75,000

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Lesson Learned

A high percentage of people go with defaultsü Increase retirement plan participation via automatic enrollment

ü Consider setting a pre-specified contribution rate with a pre-specified asset allocation

ü Set default contribution rates at higher levels to encourage increased contributions

ü Encourage maximizing of contributions as a way to reach retirement savings goals

24

“When you have to make a choice and don't make it, that is in itself a choice.”

–William James, American Psychologist and Professor

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Choice Architecture

25For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Predictably Irrational: Subscription Selection

26

16%

0%

84%

68%

32%

Students selecting option

Source: Dan Ariely, Predictably Irrational: The hidden forces that shape our decisions (New York: HarperCollins, 2010), 3-5.

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Choice Architecture:the conscious decision to arrange items to achieve a desired outcome

27For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

A Trip to the Supermarket

28For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Order in Product Customization Decisions

29

Source: Jonathan Levav, Mark Heitmann, Andreas Herrmann, Sheena S. Iyengar, “Order in Product Customization Decisions: Evidence from Field Experiments,” Journal of Political Economy, 2010, Volume 118, Number 2, 274-299.

Car Accessories

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Choice + Retirement = Major Challenge

• The central challenge in saving for retirement is striking the right balance between portfolio risk and longevity risk.

• Most people focus exclusively on portfolio risk, rather than longevity risk

• As a result, many people put themselves at a disadvantage by being too conservative in their asset allocation

• Investors have to consider all variables- How much they save- How the markets behave- What age they want to retire at- How much they plan on spending in

retirement- How long they will live in retirement

Simulation results of a more conservative retirement portfolio

with 40 years of savings

Source: Legg Mason Global Asset Allocation, LLC, as of December 2010. Past performance is not guarantee of future results.

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Lesson Learned

How you present an option affects how people choose• Provide perspective on what it means to invest for retirement

– Help strike the balance between portfolio risk and longevity risk

• Give close consideration to retirement plan design features– Carefully consider investment fund menu

– Pay attention to the number of funds in the investment menu

– Think about how risk-based and retirement/target date funds are presented on the investment menu

• Review investment election form design

31

“Choice architecture is particularly important in domains such as retirement savings where most of the decision-makers are unsophisticated.”– “Choice Architecture and Retirement Saving Plans,” By Shlomo Benartzi, Ehud Peleg, Richard Thaler

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

Key Takeaways

• Finding: Most people have a tendency to postpone making the “right’ decision

- Action: Provoke immediate action by showing the impact of the cost of waiting

• Finding: A high percentage of people go with defaults

- Action: Influence decision-making by setting default options to influence retirement plan participation and higher contribution rates

• Finding: How you present an option affects how people choose

- Action Step: Strike the balance between portfolio risk and longevity risk; Give careful consideration how your retirement plan is designed; consider every detail

32For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

33

Life is the sum of all your choices.

–Albert Camus

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.

34

34

About Legg MasonLegg Mason is a diversified group of world-class global asset management firms recognized for their proven long term investment expertise. Together, we’ve become a world leader in money management with $663 billion in assets under management as of June 30, 2011. With an unyielding commitment to investment excellence and service for more than 100 years, we’re privileged to offer financial advisors and their clients access to a depth and breadth of investment solutions.

For more information: www.leggmason.com

Follow us:www.twitter.com/leggmason

Legg Mason, Inc., its affiliates, and its employees are not in the business of providing tax or legal advice to taxpayers. These materials and any tax-related statements are not intended or written to be used, and cannot be used or relied upon, by any such taxpayer for the purpose of avoiding tax penalties. Tax-related statements, if any, may have been written in connection with the "promotion or marketing" of the transaction(s) or matters(s) addressed by these materials, to the extent allowed by applicable law. Any such taxpayer should seek advice based on the taxpayer's particular circumstances from an independent tax advisor.

All investments involve risks including loss of principal.© 2011 Legg Mason Investor Services, LLC, member FINRA/SIPC. Legg Mason Investor Services, LLC and Legg Mason Capital Management are subsidiaries of Legg Mason, Inc.

FN1111845

INVESTMENT PRODUCTS: NOT FDIC INSURED • NOT BANK GUARANTEE • MAY LOSE VALUE

For broker/dealer and Plan Sponsor use only. Not for use with Plan Sponsors who have less than 100 participants and not for use with any of the participants of such a plan. Not for use with the public.