Self-Employed Borrower Schedule Analysis Method …...Schedule Analysis Method Part II, Business...

111

Genworth Mortgage Insurance Corporation ©2018 Genworth Financial, Inc. All rights reserved. Self-Employed Borrower Schedule Analysis Method or SAM Part II: Business Tax Returns November 2018

Transcript of Self-Employed Borrower Schedule Analysis Method …...Schedule Analysis Method Part II, Business...

Genworth Mortgage Insurance Corporation ©2018 Genworth Financial, Inc. All rights reserved.

Self-Employed Borrower

Schedule Analysis Method or SAMPart II: Business Tax Returns

November 2018

2Schedule Analysis Method Part II, Business Return Review

Objective

-Learn to use SAM Form to calculate supportable income for self

employed borrowers, using K-1s and business tax returns

– Partnership income and expenses, IRS Form 1065 and associated K-1s

– S-Corp income and expenses, from IRS Form 1120S and associated K-1s

Fannie Mae policy is different from Freddie Mac

– We will review both in today’s session

Does Borrower Own 25% or More of a

Business?

3Schedule Analysis Method Part II, Business Return Review 3

Can checking the Self-Employed Indicator to yes -

increase the risk of loans when evaluated by DU®?

Loan Product Advisor®?

YesNo

Self-Employment Fannie Mae

4Schedule Analysis Method Part II, Business Return Review

Self-Employment Fannie Mae

5Schedule Analysis Method Part II, Business Return Review

Written Analysis of Income-Fannie Mae

Fannie Mae 2016 Selling Guide B3-3.2-01, Underwriting Factors and

Documentation for a Self-Employed Borrower (06/28/2016)

6Schedule Analysis Method Part II, Business Return Review

Written Analysis of Income-Fannie Mae

7Schedule Analysis Method Part II, Business Return Review

Fannie Mae 2016 Selling Guide B3-3.2-01, Underwriting Factors and

Documentation for a Self-Employed Borrower (06/28/2016)

11

Implementation Of Income Requirements

Freddie Mac Documentation Matrix

Documentation Matrix

– Assists in underwriting and

documenting loans for Freddie Mac

– Lenders may have overlays

– Check specific program

requirements

– Updated September 2018

12

http://freddiemac.com/learn

Freddie Mac Seller/Servicer Guide

13

When Do We Have To Tell Loan Product Advisor Our Borrower Is Self-

Employed?

Updated and Effective September 19,2018

14Schedule Analysis Method Part II, Business Return Review

Freddie Mac Self-Employed Documentation

15Schedule Analysis Method Part II, Business Return Review

Freddie Mac Self-Employed Documentation

16Schedule Analysis Method Part II, Business Return Review

Freddie Mac Self-Employed Documentation

17Schedule Analysis Method Part II, Business Return Review

Chapter 5304

18Schedule Analysis Method Part II, Business Return Review

Chapter 5304

19Schedule Analysis Method Part II, Business Return Review

5304 Income NOT On the Personal Returns

21Schedule Analysis Method Part II, Business Return Review

In Case Study Part I, We

Completed Sections 1-8

Personal Tax Return Review

You Will Need

22Schedule Analysis Method Part II, Business Return Review

:You will be working with John and Mary Homeowner who

– Own 33.33% of an LLC called Street Art Design Company (John)

• Reported on a Partnership Return 1065

• John receives a K-1

– Own 100% of an S Corporation called Modern Dwelling Enterprises, Inc. (Mary)

• Mary receives a K-1

• 1120S business tax return

• Mary & John receives a W-2 Wage Statements from the business

The Case Study

23Schedule Analysis Method Part II, Business Return Review

Training Tools and Information

24Schedule Analysis Method Part II, Business Return Review

Training Tools and Information

25Schedule Analysis Method Part II, Business Return Review 25

26Schedule Analysis Method Part II, Business Return Review

Access SAM Reference Guide - Page 2

27Schedule Analysis Method Part II, Business Return Review

Analyzing IRS Form K-1

28Schedule Analysis Method Part II, Business Return Review

Analyzing Partnership Returns

29Schedule Analysis Method Part II, Business Return Review

30Schedule Analysis Method Part II, Business Return Review

Freddie Mac Seller/Servicer Guide

5304.1 Stable Monthly Income

31Schedule Analysis Method Part II, Business Return Review

Freddie Mac Seller/Servicer Guide5304.1 Stable Monthly Income

32

1065 Partnership

Line 22 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

$_________

Schedule E page 2

Part II1040

Line 17 Net Income/Loss Sch.E

$_________

Taxed at a personal rate

Schedule Analysis Method Part II, Business Return Review

Check for trends or changes

– Gross receipts

– Cost of Goods Sold

– Gross Profit

– Bottom line “Ordinary Income”

:Note

– Guaranteed Payments can be

found on Line 10

– This is compensation paid to the

owners and has nothing to do

with distributions

Partnership 1065

Schedule Analysis Method Part II, Business Return Review 33

Page 22

1065 Partnership

Line 22 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

$_________

Schedule E page 2

Part II

1040

Line 17 Net Income/Loss Sch.E

$_________

Taxed at a personal rate

34Schedule Analysis Method Part II, Business Return Review

Partnership K-1

Schedule Analysis Method Part II, Business Return Review35

Page 20

35

Rental Income - Partnership or S Corp

36

No Example

Schedule Analysis Method Part II, Business Return Review

Partnership K-1

Schedule Analysis Method Part II, Business Return Review37

Page 20

37

1065 Partnership

Line 22 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

$_________

Schedule E page 2

Part II

1040

Line 17 Net Income/Loss Sch.E

$_________

Taxed at a personal rate

38Schedule Analysis Method Part II, Business Return Review

Schedule E

39Schedule Analysis Method Part II, Business Return Review

Page 12

1065 Partnership

Line 22 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

$_________

Schedule E page 2

Part II

1040

Line 17 Net Income/Loss Sch.E

$_________

Taxed at a personal rate

40Schedule Analysis Method Part II, Business Return Review

1040

41Schedule Analysis Method Part II, Business Return Review

Page 3

Remember - We Must Confirm Liquidity

…There was not a distribution so

43Schedule Analysis Method Part II, Business Return Review

Fannie Mae 2017 Selling Guide B3-3.2.2-01, Analyzing Partnership

Returns for a Partnership or LLC (6/28/2016)

44Schedule Analysis Method Part II, Business Return Review

Freddie Mac Seller/Servicer Guide

5304.1 Stable Monthly Income

K-1 Less than 25% Ownership

45Schedule Analysis Method Part II, Business Return Review

Training Tools and Information

46Schedule Analysis Method Part II, Business Return Review

Liquidity

47

Generally Accepted Accounting Principles

Schedule Analysis Method Part II, Business Return Review

Generally Accepted Accounting Principles

Liquidity - Current Ratio

48Schedule Analysis Method Part II, Business Return Review

Balance Sheet

49Schedule Analysis Method Part II, Business Return Review

Page 26

Balance Sheet

50Schedule Analysis Method Part II, Business Return Review

(Cash #1 + Acct Receivable #2 + #4+ #5 +Other Current Assets #6)

(Acct Pay. #15 + MNB #16 + Other Current Liabilities #17)

Quick Ratio or Acid Test

Current Assets :

Current Liabilities:

Current Assets:

Current Liabilities: .201 - Solvency

$765 + 0 + 0 +0+0 = $765

$0 + $0+ $3,800 = $3,800

Page 26

Generally Accepted Accounting Principles

Liquidity

51Schedule Analysis Method Part II, Business Return Review

Follow The Guidelines For The Investor You Are Underwriting To And

Provide Justification For Decisioning

Quick Reference Guide Partnership K-1

52Schedule Analysis Method Part II, Business Return Review

Genworth Calculator Is A Tool. Lenders/Underwriters Review Each Loan

File And Determine Compliance With Fannie Mae Or Investor Guidelines.

Partnership K-1

53Schedule Analysis Method Part II, Business Return Review

Can We Use Ordinary Income/Rental Income From the K-1?

Was There A Distribution? Was Liquidity Verified?

Page 20

Quick Reference Guide Partnership K-1

54Schedule Analysis Method Part II, Business Return Review

Genworth Calculator Is A Tool. Lenders/Underwriters Review Each Loan

File And Determine Compliance With Fannie Mae Or Investor Guidelines.

Partnership K-1

55

Page 20

Schedule Analysis Method Part II, Business Return Review

Before You Give Credit For The Guarantee Payments, Does This Business Appear to

Be Capable Of Paying It In The Future? Could We Look At The Balance Sheet Again?

Balance Sheet

56Schedule Analysis Method Part II, Business Return Review

Page 26

Could We Verify What Is Included On Line 17? Our Borrower Indicated The

Business Loan Listed Has Been Paid Off And Provided Evidence When Advised

That The Business Did Not Appear Solvent

Liquidity Test Without The Loan

57Schedule Analysis Method Part II, Business Return Review

Do You Feel More Comfortable Using The Guaranteed Payment Now?

Quick Reference Guide Partnership K-1

58Schedule Analysis Method Part II, Business Return Review

Guaranteed Payments Can Be Used; Follow Investor Guidelines

SAM Form Section XI, IRS Form 1065

59Schedule Analysis Method Part II, Business Return Review

Page 22

Partnership Form 1065

60Schedule Analysis Method Part II, Business Return Review

Page 22

S Corporation Form 1120S

61Schedule Analysis Method Part II, Business Return Review

Partnership Form 1065

62Schedule Analysis Method Part II, Business Return Review

Page 22

Review The Statement

The statement must be reviewed to determine if “other deductions” includes

amortization and/or casualty losses. None have been identified in this return.

Schedule Analysis Method Part II, Business Return Review 63

Page 28

Partnership Form 1065

64Schedule Analysis Method Part II, Business Return Review

Page 26

Partnership Form 1065

65Schedule Analysis Method Part II, Business Return Review

Page 26

Partnership K-1

66Schedule Analysis Method Part II, Business Return Review

Page 20

SAM Form Section X, IRS Form 1065

67Schedule Analysis Method Part II, Business Return Review

68Schedule Analysis Method Part II, Business Return Review

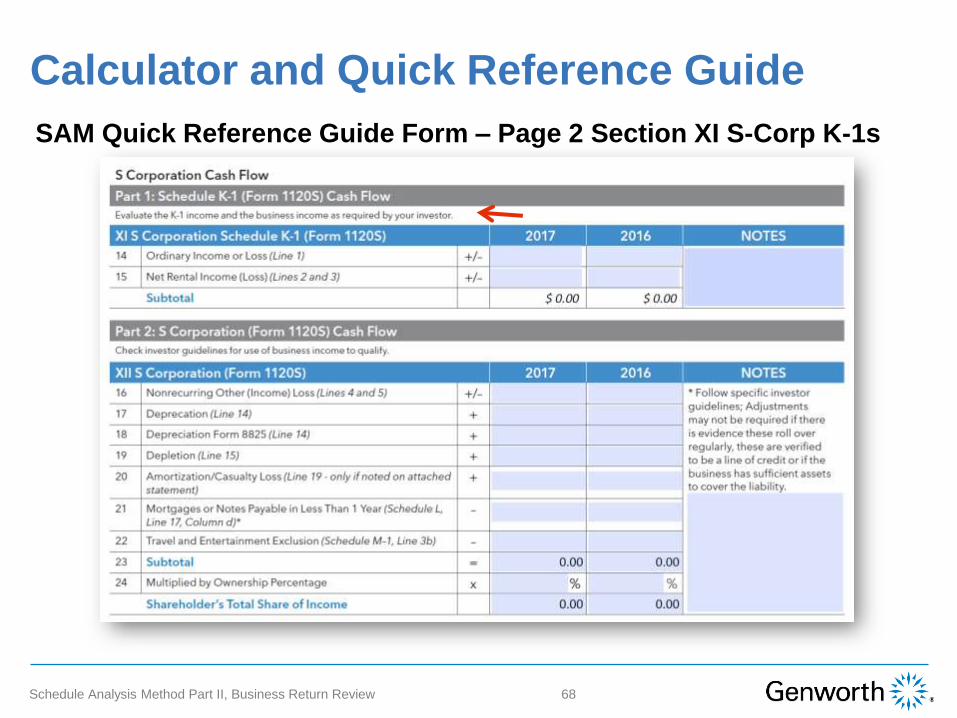

Calculator and Quick Reference Guide

SAM Quick Reference Guide Form – Page 2 Section XI S-Corp K-1s

S Corporation Income - Fannie Mae

69Schedule Analysis Method Part II, Business Return Review

70Schedule Analysis Method Part II, Business Return Review

Freddie Mac Seller/Servicer Guide

5304.1 Stable Monthly Income

1120S Corporation

Line 21 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

Schedule E page 2

Part II

Net Income/Loss $_______

1040

Line 17 Net Income Sch.E

*$_________

*Taxed at a personal rate

72Schedule Analysis Method Part II, Business Return Review

Check for Trends or Changes

– Gross receipts

– Cost of goods sold

– Gross profit

– Bottom line “Ordinary Income”

– W-2 wages

• Were these paid to borrower?

S Corps

73Schedule Analysis Method Part II, Business Return Review

Page 33

S Corps

74Schedule Analysis Method Part II, Business Return Review

Page 38

Compensation of Owners And/Or Officers From Line 7; Did We Give Credit

For Mary’s W-2 Already?

75Schedule Analysis Method Part II, Business Return Review

1120S Corporation

Line 21 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

$_________

Schedule E page 2

Part II

1040

Line 17 Net Income Sch.E

*$_________

*Taxed at a personal rate

76Schedule Analysis Method Part II, Business Return Review

S Corp K-1

Did Mary get a distribution?

77Schedule Analysis Method Part II, Business Return Review

Page 31

Page 2 of K-1 and Page 3 of Form 1120S

78Schedule Analysis Method Part II, Business Return Review

Page 32

1120S Corporation

Line 21 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

$_________

Schedule E page 2

Part II

1040

Line 17 Net Income Sch.E

*$_________

*Taxed at a personal rate

80Schedule Analysis Method Part II, Business Return Review

Schedule E Partnerships and S Corps

81Schedule Analysis Method Part II, Business Return Review

Page 12

1120S Corporation

Line 21 Ordinary Income/Loss

$_________

K-1

%

Line 1 Ordinary Income/Loss

$_________

Schedule E page 2

Part II1040

Line 17 Net Income Sch.E

*$_________

*Taxed at a personal rate

82Schedule Analysis Method Part II, Business Return Review

83Schedule Analysis Method Part II, Business Return Review

Page 3

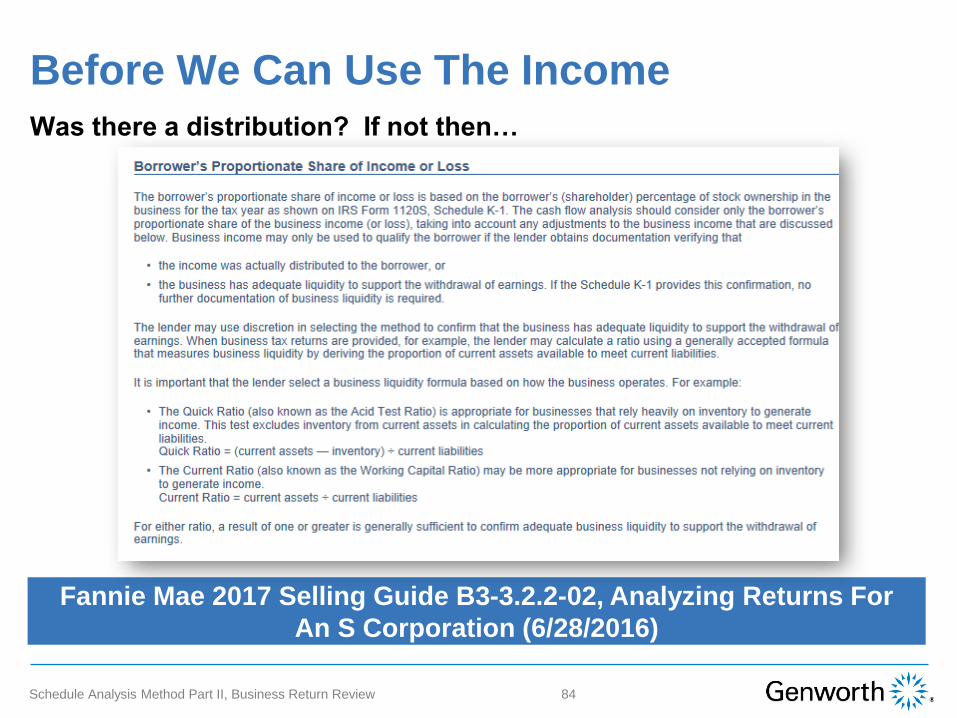

Before We Can Use The Income

…Was there a distribution? If not then

84Schedule Analysis Method Part II, Business Return Review

Fannie Mae 2017 Selling Guide B3-3.2.2-02, Analyzing Returns For

An S Corporation (6/28/2016)

85Schedule Analysis Method Part II, Business Return Review

Chapter 5304

86Schedule Analysis Method Part II, Business Return Review

Liquidity

Generally Accepted Accounting Principles

Balance Sheet

87Schedule Analysis Method Part II, Business Return Review

Page 36

Balance Sheet

Quick Ratio or Acid Test

Current Assets :

Current Liabilities:

88Schedule Analysis Method Part II, Business Return Review

(Cash #1 + Acct Receivable #2 + #4+ #5 +Other Current Assets #6)

(Acct Pay. #16 + MNB #17 + Other Current Liabilities #18)

Current Assets:

Current Liabilities: .045 - Solvency

$6,530 + 0 + 0 +0+ $5,578 = $12,108

$146,222 + $0+ $124,347 = $270,569

Page 36

Liquidity

89

Generally Accepted Accounting Principles

Schedule Analysis Method Part II, Business Return Review

Review for W-2 Paid from Business

– Did we give credit for this income already?

AS A REMINDER…..

90Schedule Analysis Method Part II, Business Return Review

Page 1

1120S K1 Review

91Schedule Analysis Method Part II, Business Return Review

S Corp K-1

Did Mary get a distribution?

92Schedule Analysis Method Part II, Business Return Review

Page 31

S Corp K-1

93Schedule Analysis Method Part II, Business Return Review

Page 31

Let’s put numbers on our tool

S Corp K-1 Review

– Was there a distribution?

S Corp K-1

94Schedule Analysis Method Part II, Business Return Review

Page 31

S Corporation Form 1120S

95Schedule Analysis Method Part II, Business Return Review

Page 33

S Corporation Form 1120S

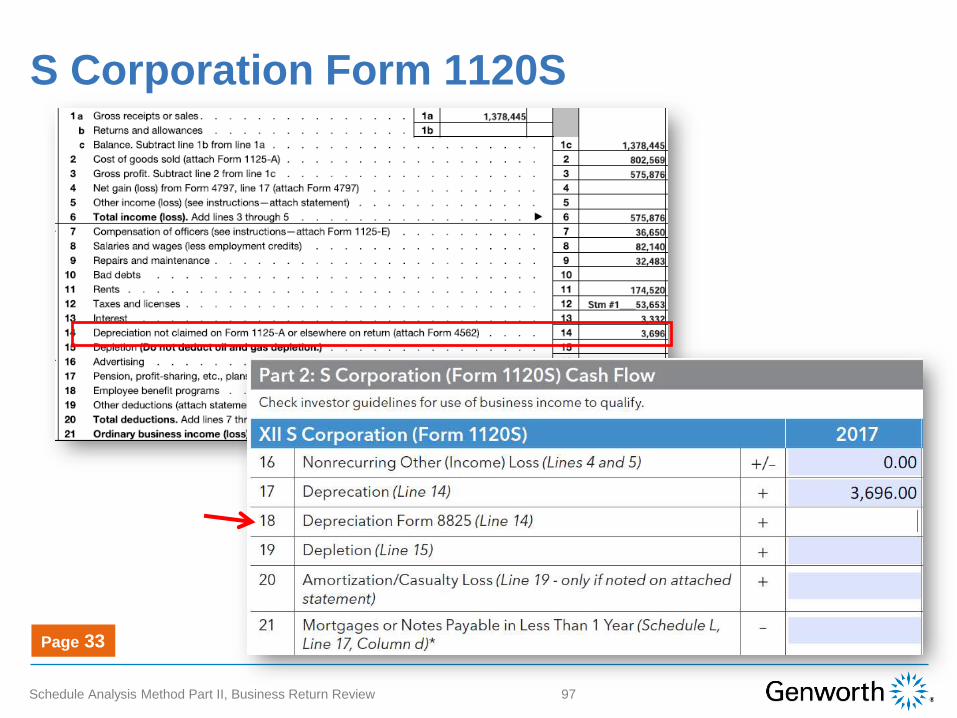

96Schedule Analysis Method Part II, Business Return Review

Page 33

S Corporation Form 1120S

97Schedule Analysis Method Part II, Business Return Review

Page 33

S Corporation Form 1120S

98Schedule Analysis Method Part II, Business Return Review

Page 33

S Corporation Form 1120S

99Schedule Analysis Method Part II, Business Return Review

Page 33

S Corporation Form 1120S

100Schedule Analysis Method Part II, Business Return Review

Page 33

S Corporation Form 1120S

101Schedule Analysis Method Part II, Business Return Review

Page 42

S Corporation Form 1120S

102Schedule Analysis Method Part II, Business Return Review

Page 36

S Corporation Form 1120S

103Schedule Analysis Method Part II, Business Return Review

Page 36

S Corporation Form 1120S

104Schedule Analysis Method Part II, Business Return Review

Page 36

S Corporation Form 1120S

105Schedule Analysis Method Part II, Business Return Review

Page 37

S Corporation Form 1120S

106Schedule Analysis Method Part II, Business Return Review

S Corp K-1

?How much does Mary own

107Schedule Analysis Method Part II, Business Return Review

Page 31

S Corporation Form 1120S

108Schedule Analysis Method Part II, Business Return Review

Do you feel comfortable using the W2 income to qualify?

Do Not Use Any W-2 Income For John Or Mary From Modern Dwelling

And You Are NOT Required To For Modern Dwelling Enterprises Losses;

Try to Qualify Using the Partnership Income and Schedule C Income

Fannie Mae

109Schedule Analysis Method Part II, Business Return Review

Freddie Mac

110Schedule Analysis Method Part II, Business Return Review

Requires Sellers To Account For Business Losses If It Is Their Primary

Source Of Income; Other Option Would Be To Take Mary Off The Loan,

BUT Still Not Use John’s W-2 Wages From The Business

Genworth Underwriting Guidelines

111Schedule Analysis Method Part II, Business Return Review

Genworth Rate Express®

Schedule Analysis Method Part II, Business Return Review 112

LOS Connections

Schedule Analysis Method Part II, Business Return Review113

Training Tools and Information

114Schedule Analysis Method Part II, Business Return Review

Training Tools and Information

Schedule Analysis Method Part II, Business Return Review 115

Additional MI Site Information

116Schedule Analysis Method Part II, Business Return Review

117Schedule Analysis Method Part II, Business Return Review

➢ ActionCenter®: 800 444.5664

➢ Your Local Genworth

Regional Underwriter

➢ Your Genworth Sales

Representative

Your Genworth Resources

118Schedule Analysis Method Part II, Business Return Review

Legal Disclaimer Genworth Mortgage Insurance is happy to provide you with these training materials. While we strive for

accuracy, we also know that any discussion of laws and their application to particular facts is subject to

individual interpretation, change, and other uncertainties. Our training is not intended as legal advice, and is

not a substitute for advice of counsel. You should always check with your own legal advisors for

interpretations of legal and compliance principles applicable to your business.

,GENWORTH EXPRESSLY DISCLAIMS ANY AND ALL WARRANTIES, EXPRESS OR IMPLIED

INCLUDING WITHOUT LIMITATION WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A

PARTICULAR PURPOSE, WITH RESPECT TO THESE MATERIALS AND THE RELATED TRAINING. IN

NO EVENT SHALL GENWORTH BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, PUNITIVE, OR

CONSEQUENTIAL DAMAGES OF ANY KIND WHATSOEVER WITH RESPECT TO THE TRAINING AND

THE MATERIALS.

Genworth Mortgage Insurance Offers A Comprehensive Suite Of Training

Opportunities To Boost Your Know-How, Benefit Your Bottom Line, And Serve Your

Borrowers Better. Visit mi.genworth.com To Learn More.

Collateral Underwriter®, Home Ready ® and Desktop Underwriter® or DU® are registered trademarks of Fannie Mae

Loan Product Advisor®, Home Possible®, Home Possible Advantage®, Loan Collateral Advisor® and Home Value Explorer® (HVE®) are registered trademarks of

Freddie Mac

ActionCenter®, Homebuyer Privileges® and Rate Express® are registered trademarks of Genworth Mortgage Insurance

Simply UnderwriteSM is a registered service mark of Genworth Mortgage Insurance