Welcome to Back to School Night! Janney Elementary We are the Dynamic Ducks!

F O O D & B E V E R A G E

MERG E R S & A CQU I S I T I O N S A D V I S O R Y • P U B L I C O F F E R I N G S

P R I V A T E P L A C EM EN T S • F A I R N E S S O P I N I O N S

F O O D & B E V E R A G EQ2 2013 QUARTERLY NEWSLETTER

S E L E C T E D C O N S U M E R & R E TA I L T R A N S A C T I O N S

$667,000,000$37,575,000

Common StockInitial Public Offering

has been acquired by

CMPO / PIPE

a division of

has been acquired by

HRSH Acquisitions LLC

$9,849,900 $58,173,000

Co-ManagerMarch 2013

$38,295,000

Advisor to SellerApril 2013

Sole Book Running ManagerJuly 2013

Advisor to SellerJune 2013

Common StockPIPE

Lead Financial Advisor Advisor to Seller

has been acquired by

Advisor to Seller

has sold certain assets to

Common StockFollow-on Offering

Lead Book Running ManagerOctober 2012

$702,190,000 $ 165,000,000$175,000,000$205,000,000

November 2011Advisor to Seller

September 2012

Lead Book Running ManagerFebruary 2013

Common StockFollow-on Offering

Co-ManagerMay 2011

Green Mountain Coffee Roasters, Inc.

Advisor to BuyerApril 2011

has acquired certain assets, including

Advisor to SellerMay 2011

has been acquired by

Advisor to SellerSeptember 2011

has been acquired by

Q 2 2 0 1 3 : I N S I D E T H I S I S S U E

Select Headlines 1

Public Company Universe Snapshot 2

Macro Story 3

View from the Street: Q2 Earnings 4

Equity Offering Activity 7

Debt Offering Activity 8

M&A Activity 10y

Financial Sponsor Activity 12

Financial Sponsor Sector Snapshot: Fresh Baked Goods 12

Select Commodity Trends 13

Public Company Universe Details 14

This material is a publication of Janney Montgomery Scott LLC’s Investment Banking Department and for informational Purpose only and shallin no event be construed as an offer to sell or a solicitation of an offer to buy any securities. The views expressed in this publication may differfrom those expressed by other areas of the Firm including the Firm’s Research Department. To view the firm’s current research on the Consumer& Retail sector please go to www.janney.com. Janney Montgomery Scott LLC’s Investment Banking Department is independent of the Firm’sResearch Department.

The factual information described herein is taken from sources which we believe to be reliable, but the accuracy and completeness of suchinformation is not guaranteed by us. The opinions expressed herein may be given only such weight as opinions warrant. Opinions expressed aresubject to change without notice and do not take into account the particular investment objectives, financial situations or needs of individualinvestors. This Firm, its officers, directors, employees, or members of their families may have positions in the securities mentioned and maymake purchases or sales of such securities from time to time in the open market or otherwise and may sell to or buy from customers suchsecurities on a principal basis. Supporting information related to the recommendation, if any, made in this material is available upon request.

Janney Montgomery Scott LLC is a registered broker-dealer member of FINRA, NYSE, and SIPC.

B. JOHN LINDEMANManaging Director

215.665.6302jlindeman@janney com

JOHN W. DAMIANDirector

215.665.4451jdamian@janney [email protected] [email protected]

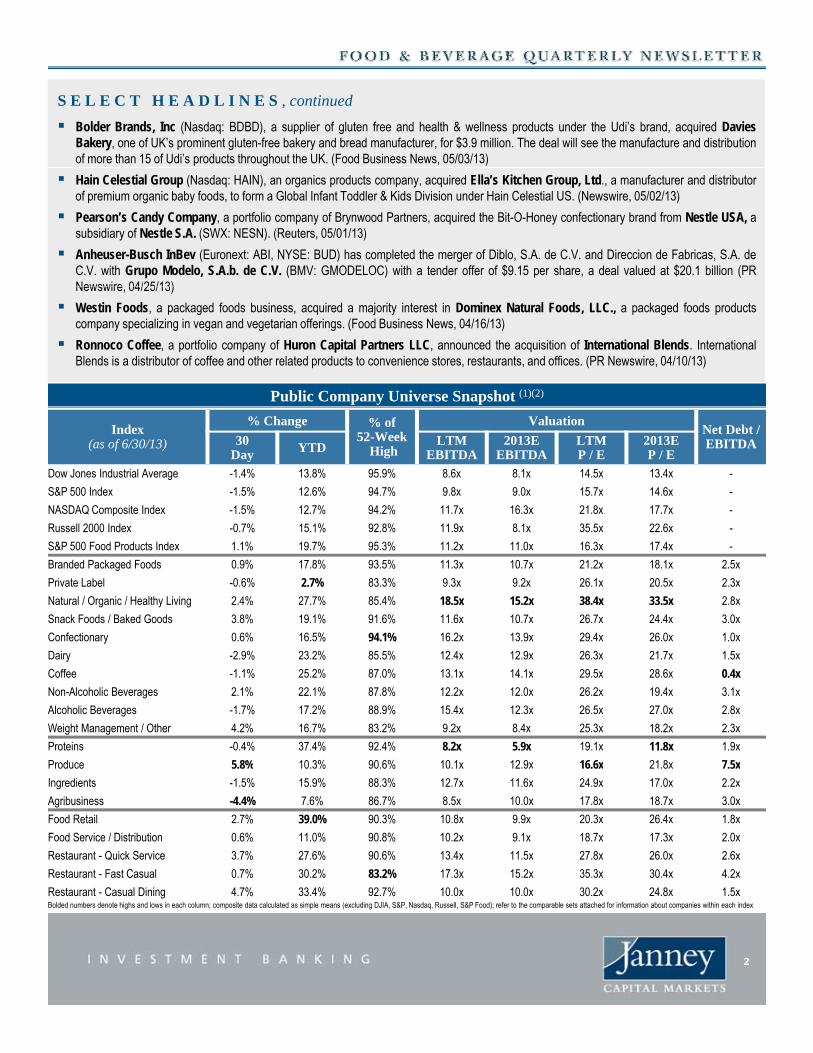

S E L E C T H E A D L I N E S

Sprouts Farmers Market priced its initial public offering of 18.5 million shares of common stock at $18 per share, above its previouslypredicted range, for about $333 million in proceeds. (Associated Press, 08/01/13)

Roark Capital Group announced that it had acquired Miller's Ale House, a 65 unit casual dining restaurant chain. (PRNewswire, 07/22/13)

Kroger, the nation’s second-largest retailer, announced that it would buy Harris Teeter, an upscale grocer known for fresh foods andproduce, in a deal valued at $2.5 billion. (New York Times Dealbook, 07/09/13)

Arbor Investments, a Chicago-based private equity firm focusing on the food and beverage industry, has acquired The New French Bakery,a full line bread company. (PEHub, 06/25/13)

Smashburger, a private hamburger chain, has closed on a $35 million round of financing with Golub Capital, a middle-market focused PEfund. Smashburger intends to use the capital to finance ongoing growth plans. (MarketWatch, 06/25/13)

Johnny Rockets a hamburger chain was sold by RedZone Capital to an affiliate of Sun Capital Partners Johnny Rockets operates and Johnny Rockets, a hamburger chain, was sold by RedZone Capital to an affiliate of Sun Capital Partners. Johnny Rockets operates andfranchises about 300 restaurants in 30 states and 16 countries. (PEHub, 06/18/13)

Campbell Soup Company (NYSE: CPB) acquired Plum Organics. “Plum” is the No. 2 brand of organic baby food in the U.S. and iscurrently the No. 4 baby food brand overall, generating $93 million in gross sales in 2012. (Food Business News, 06/14/13)

Sobeys, Inc, a subsidiary of Empire Company, Ltd. (TSX: EMP.A), has agreed to acquire Safeway, Ltd, a grocery and pharmacy chain, forapproximately $5.7 billion. (Food Business News, 06/13/13)

B&G Foods, Inc. (NYSE: BGS) announced the acquisition of Robert’s American Gourmet Food, LLC dba Pirate Brands, a leader in the, ( ) q , ,all-natural snack foods category, for approximately $195 million in cash. (Business Wire, 06/10/13)

DC Brands International (OTC: HRDN) acquired a minority interest in Village Tea Company Distribution, Inc, a distributor and owner ofVillage Tea Company, from Total Apparel Group (OTC Pink: TLAG). (PR Newswire, 06/06/13)

Russian Standard Corporation completed its acquisition of Central European Distribution Corporation, a producer and distributor ofvodka and other alcoholic beverages, creating the second-largest vodka producing corporation in the world. (PR Newswire, 06/05/13)

Tyson Foods, LLC, (NYSE: TSN), a meat and poultry manufacturer and distributor, acquired Circle Foods, LLC, a producer of frozen andrefrigerated handheld Mexican foods uncooked tortillas and Indian flatbreads from Claridge Inc (MarketWatch 06/03/13)refrigerated handheld Mexican foods, uncooked tortillas and Indian flatbreads from Claridge Inc. (MarketWatch, 06/03/13)

Inventure Foods, Inc. (Nasdaq: SNAK), a maker of healthy snack food products, has acquired Willamette Valley Fruit Company, a localfruit growing and processing company, for approximately $9.5 million. (Food Business News, 06/03/13)

Coregistics, a supply chain services company, acquired the assets of Cano Packaging Corporation, a Chicago-area company thatspecializes in primary contract packaging services for food and confectionary manufactures. (PR Newswire, 05/30/13)

Shuanghui, China’s biggest pork producer has agreed to buy Smithfield Foods, the 87-year-old Virginia-based meat giant with brands likeArmour and Farmland, for $4.7 billion in cash. This transaction values Smithfield at approximately $7.1 billion. (New York Times, 05/29/13), $ pp y $ ( , )

NutraBev Holdings International, Inc. acquired Silverbow Honey Co., a honey producer and retailer that packs annually over 5 millionpounds of honey for sales to retail, bakery, food service, specialty and industrial businesses. (Wall Street Journal, 05/22/13)

Tate & Lyle, PLC, a provider of specialty food ingredients and solutions, acquired Biovelop, a manufacturer of oat beta glucan for use in thefood, beverage and supplement markets, as well as the cosmetics industry. (Food Business News, 05/21/13)

Goosecross Cellars, a luxury winery located in Yountville, Ca, was sold to Golden Equity Investments for an undisclosed amount. (PRNewswire, 05/16/13)

Bellisio Foods, Inc. agreed to acquire Overhill Farms, Inc. (AMEX: OFI), a frozen foods supplier, for about $81 million in cash. (Wall StreetJournal, 05/15/13)

Lifeway Foods, Inc, (Nasdaq: LWAY), a supplier of cultured dairy products, acquired the Golden Guernsey dairy plant for $7.4 million inorder to provide more manufacturing capability. (PR Newswire, 05/15/13)

Post Holdings, Inc. (NYSE: POST), a manufacturer and distributor of cereals, agreed to acquire the cereal, granola, and snack business ofHearthside Food Solutions for $158 million in cash at closing. (PR Newswire, 05/09/13)

B&G Foods Inc (NYSE: BGS) acquired the TrueNorth nut cluster brand from DeMet’s Candy Company a portfolio company of Brynwood B&G Foods, Inc. (NYSE: BGS) acquired the TrueNorth nut cluster brand from DeMet s Candy Company,. a portfolio company of BrynwoodPartners. DeMet's, best known for their signature TURTLES candies, acquired TrueNorth from Frito-Lay in 2010. (Business Wire, 05/07/13)

11

S E L E C T H E A D L I N E S , continued

Bolder Brands, Inc (Nasdaq: BDBD), a supplier of gluten free and health & wellness products under the Udi’s brand, acquired DaviesBakery, one of UK’s prominent gluten-free bakery and bread manufacturer, for $3.9 million. The deal will see the manufacture and distributionof more than 15 of Udi’s products throughout the UK. (Food Business News, 05/03/13)

Hain Celestial Group (Nasdaq: HAIN), an organics products company, acquired Ella’s Kitchen Group, Ltd., a manufacturer and distributorof premium organic baby foods, to form a Global Infant Toddler & Kids Division under Hain Celestial US. (Newswire, 05/02/13)

Pearson’s Candy Company, a portfolio company of Brynwood Partners, acquired the Bit-O-Honey confectionary brand from Nestle USA, asubsidiary of Nestle S.A. (SWX: NESN). (Reuters, 05/01/13)

Anheuser-Busch InBev (Euronext: ABI, NYSE: BUD) has completed the merger of Diblo, S.A. de C.V. and Direccion de Fabricas, S.A. deC.V. with Grupo Modelo, S.A.b. de C.V. (BMV: GMODELOC) with a tender offer of $9.15 per share, a deal valued at $20.1 billion (PRNewswire 04/25/13)

Public Company Universe Snapshot (1)(2)

Newswire, 04/25/13)

Westin Foods, a packaged foods business, acquired a majority interest in Dominex Natural Foods, LLC., a packaged foods productscompany specializing in vegan and vegetarian offerings. (Food Business News, 04/16/13)

Ronnoco Coffee, a portfolio company of Huron Capital Partners LLC, announced the acquisition of International Blends. InternationalBlends is a distributor of coffee and other related products to convenience stores, restaurants, and offices. (PR Newswire, 04/10/13)

Index(as of 6/30/13)

% Change % of 52-Week

High

ValuationNet Debt /EBITDA30

Day YTD LTM EBITDA

2013EEBITDA

LTM P / E

2013E P / E

Dow Jones Industrial Average -1.4% 13.8% 95.9% 8.6x 8.1x 14.5x 13.4x -

S&P 500 Index -1.5% 12.6% 94.7% 9.8x 9.0x 15.7x 14.6x -

NASDAQ Composite Index -1.5% 12.7% 94.2% 11.7x 16.3x 21.8x 17.7x -

Russell 2000 Index 0 7% 15 1% 92 8% 11 9x 8 1x 35 5x 22 6xRussell 2000 Index -0.7% 15.1% 92.8% 11.9x 8.1x 35.5x 22.6x -

S&P 500 Food Products Index 1.1% 19.7% 95.3% 11.2x 11.0x 16.3x 17.4x -

Branded Packaged Foods 0.9% 17.8% 93.5% 11.3x 10.7x 21.2x 18.1x 2.5x

Private Label -0.6% 2.7% 83.3% 9.3x 9.2x 26.1x 20.5x 2.3x

Natural / Organic / Healthy Living 2.4% 27.7% 85.4% 18.5x 15.2x 38.4x 33.5x 2.8x

Snack Foods / Baked Goods 3.8% 19.1% 91.6% 11.6x 10.7x 26.7x 24.4x 3.0x

Confectionary 0.6% 16.5% 94.1% 16.2x 13.9x 29.4x 26.0x 1.0x

Dairy -2.9% 23.2% 85.5% 12.4x 12.9x 26.3x 21.7x 1.5x

Coffee -1.1% 25.2% 87.0% 13.1x 14.1x 29.5x 28.6x 0.4x

Non-Alcoholic Beverages 2.1% 22.1% 87.8% 12.2x 12.0x 26.2x 19.4x 3.1x

Alcoholic Beverages -1.7% 17.2% 88.9% 15.4x 12.3x 26.5x 27.0x 2.8x

Weight Management / Other 4.2% 16.7% 83.2% 9.2x 8.4x 25.3x 18.2x 2.3x

Proteins -0.4% 37.4% 92.4% 8.2x 5.9x 19.1x 11.8x 1.9x

Produce 5 8% 10 3% 90 6% 10 1x 12 9x 16 6x 21 8x 7 5xProduce 5.8% 10.3% 90.6% 10.1x 12.9x 16.6x 21.8x 7.5x

Ingredients -1.5% 15.9% 88.3% 12.7x 11.6x 24.9x 17.0x 2.2x

Agribusiness -4.4% 7.6% 86.7% 8.5x 10.0x 17.8x 18.7x 3.0x

Food Retail 2.7% 39.0% 90.3% 10.8x 9.9x 20.3x 26.4x 1.8x

Food Service / Distribution 0.6% 11.0% 90.8% 10.2x 9.1x 18.7x 17.3x 2.0x

Restaurant - Quick Service 3.7% 27.6% 90.6% 13.4x 11.5x 27.8x 26.0x 2.6x

Restaurant - Fast Casual 0.7% 30.2% 83.2% 17.3x 15.2x 35.3x 30.4x 4.2x

Restaurant - Casual Dining 4.7% 33.4% 92.7% 10.0x 10.0x 30.2x 24.8x 1.5x

2

Bolded numbers denote highs and lows in each column; composite data calculated as simple means (excluding DJIA, S&P, Nasdaq, Russell, S&P Food); refer to the comparable sets attached for information about companies within each index

2

M A C R O S T O R Y

The Conference Board Consumer Confidence Index®, which had improved in June, pulled back slightly in July. The Index now stands at 80.3,up from 74.3 in May and 68.1 in January. Consumers’ assessment of current conditions continues to gain ground and expectations remain inexpansionary territory despite the July retreat. Overall, indications are that the economy is strengthening and may even gain some momentumin the months ahead.

The U.S. Department of Labor reported that the unemployment rate remained unchanged at 7.6 percent in June as the 195,000 increase intotal nonfarm payrolls was offset by increased labor force participation. Employment continued to trend up over the month in food servicesand drinking places and in wholesale trade.

The combined percentage of loans in foreclosure or at least one payment past due was 10.3 percent on a non-seasonally adjusted basis, a 95basis point decrease from last quarter and a 103 basis point decrease from the same quarter one year ago.

Personal saving was $387 6 billion in May compared with $359 2 billion in April The personal savings rate which refers to personal saving

12%

Unemployment Rate (4)

Personal saving was $387.6 billion in May, compared with $359.2 billion in April. The personal savings rate, which refers to personal savingas a percentage of disposable personal income, was 3.2 percent in May, compared with 3.0 percent in April.

Enrollment in the Supplemental Nutrition Assistance Program (SNAP) declined in April, falling to 47.6 participants. Improvement in the jobmarket, particularly the low wage sector, has led to a decrease in the number of people dependent on the SNAP program.

Consumer Confidence (3)

SourceRelease

DateActual

% Chg MoM

% Chg YoY

Estimate SourceRelease

DateActual

% Chg MoM

% Chg YoY

80

100

120

140

160

5%

6%

7%

8%

9%

10%

11%Conference Board 7/30/2013 80.3 -1.4% 22.8% 81.3

Reuters / U. of Michigan

6/28/2013 84.1 -0.5% 14.9% 81.0

US Dept. of Labor 7/5/2013 7.6 -0.0% -7.3%

0

20

40

60

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 20130%

1%

2%

3%

4%

1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013

Credit Card Delinquency & Personal Saving (6)(7)Mortgage Delinquencies & Foreclosures (5)

12%

15%

7%

8%

9%

Credit Card Delinquency

Personal Savings

Credit Card Delinquency & Personal Saving (6)(7)Mortgage Delinquencies & Foreclosures (5)

SourceRelease

DateActual

% Chg QoQ

% Chg YoY

Federal Reserve 5/19/13 2.65% -2.6% -13.7%

US Dept. of Commerce 6/27/13 3.2% 23.1% -17.9%

SourceRelease

DateActual

% Chg QoQ

% ChgYoY

Foreclosure – Mortgage Bankers Association 5/9/13 3.6% -5.1% -19.1%

Delinquent – Mortgage Bankers Association 5/9/13 6.8% -4.8% -8.8%

0%

3%

6%

9%

0%

1%

2%

3%

4%

5%

6%

0%1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

0%1991 1992 1994 1995 1997 1998 2000 2001 2003 2004 2006 2007 2009 2010 2012

3

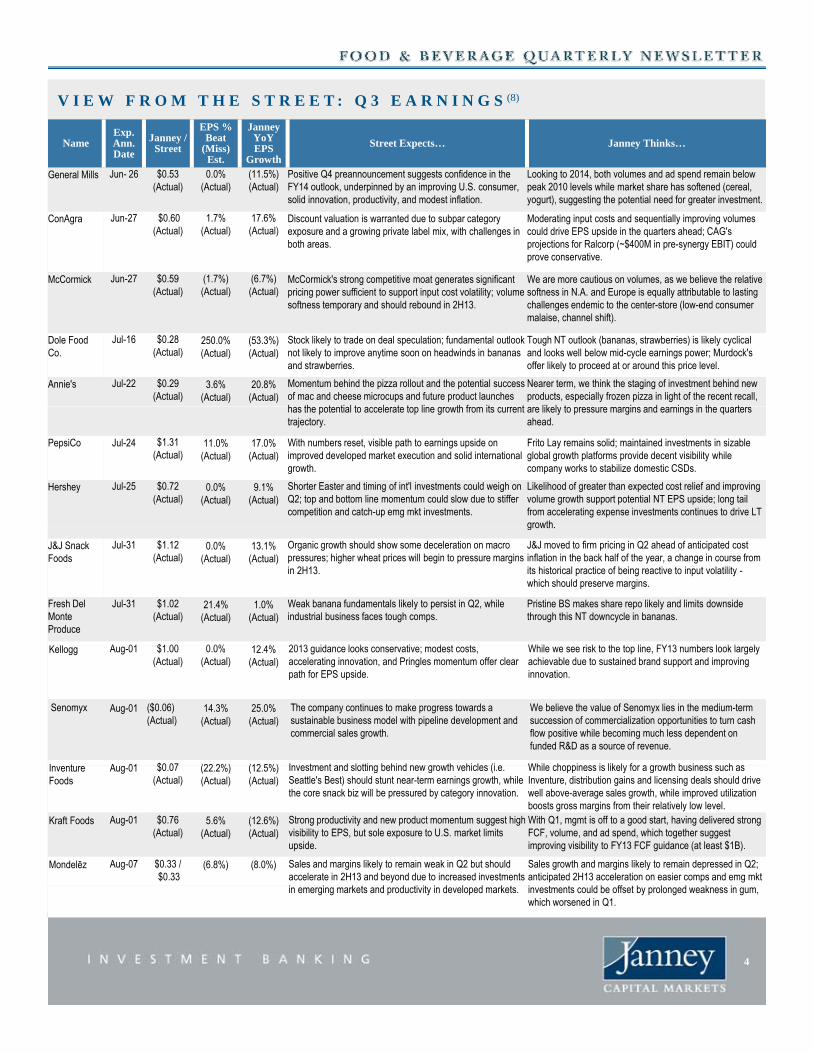

V I E W F R O M T H E S T R E E T : Q 3 E A R N I N G S (8)

NameExp.Ann. Date

Janney /Street

EPS %Beat

(Miss) Est.

Janney YoY EPS

Growth

Street Expects… Janney Thinks…

General Mills Jun- 26 $0.53(Actual)

0.0%(Actual)

(11.5%)(Actual)

Positive Q4 preannouncement suggests confidence in the FY14 outlook, underpinned by an improving U.S. consumer, solid innovation, productivity, and modest inflation.

Looking to 2014, both volumes and ad spend remain below peak 2010 levels while market share has softened (cereal, yogurt), suggesting the potential need for greater investment.

ConAgra Jun-27 $0.60(Actual)

1.7%(Actual)

17.6%(Actual)

Discount valuation is warranted due to subpar category exposure and a growing private label mix, with challenges in both areas.

Moderating input costs and sequentially improving volumes could drive EPS upside in the quarters ahead; CAG's projections for Ralcorp (~$400M in pre-synergy EBIT) could prove conservative.

McCormick Jun-27 $0.59 (1.7%) (6.7%) McCormick's strong competitive moat generates significant We are more cautious on volumes, as we believe the relative (Actual) (Actual) (Actual) pricing power sufficient to support input cost volatility; volume

softness temporary and should rebound in 2H13.softness in N.A. and Europe is equally attributable to lasting challenges endemic to the center-store (low-end consumer malaise, channel shift).

Dole Food Co.

Jul-16 $0.28(Actual)

250.0%(Actual)

(53.3%)(Actual)

Stock likely to trade on deal speculation; fundamental outlook not likely to improve anytime soon on headwinds in bananas and strawberries.

Tough NT outlook (bananas, strawberries) is likely cyclical and looks well below mid-cycle earnings power; Murdock's offer likely to proceed at or around this price level.

Annie's Jul-22 $0.29(Actual)

3.6%(Actual)

20.8%(Actual)

Momentum behind the pizza rollout and the potential success of mac and cheese microcups and future product launches h th t ti l t l t t li th f it t

Nearer term, we think the staging of investment behind new products, especially frozen pizza in light of the recent recall,

lik l t i d i i th t has the potential to accelerate top line growth from its current trajectory.

are likely to pressure margins and earnings in the quarters ahead.

PepsiCo Jul-24 $1.31(Actual)

11.0%(Actual)

17.0%(Actual)

With numbers reset, visible path to earnings upside on improved developed market execution and solid international growth.

Frito Lay remains solid; maintained investments in sizable global growth platforms provide decent visibility while company works to stabilize domestic CSDs.

Hershey Jul-25 $0.72(Actual)

0.0%(Actual)

9.1%(Actual)

Shorter Easter and timing of int'l investments could weigh on Q2; top and bottom line momentum could slow due to stiffer competition and catch-up emg mkt investments.

Likelihood of greater than expected cost relief and improving volume growth support potential NT EPS upside; long tail from accelerating expense investments continues to drive LT growthgrowth.

J&J Snack Foods

Jul-31 $1.12(Actual)

0.0%(Actual)

13.1%(Actual)

Organic growth should show some deceleration on macro pressures; higher wheat prices will begin to pressure margins in 2H13.

J&J moved to firm pricing in Q2 ahead of anticipated cost inflation in the back half of the year, a change in course from its historical practice of being reactive to input volatility -which should preserve margins.

Fresh DelMonteProduce

Jul-31 $1.02(Actual)

21.4%(Actual)

1.0%(Actual)

Weak banana fundamentals likely to persist in Q2, while industrial business faces tough comps.

Pristine BS makes share repo likely and limits downside through this NT downcycle in bananas.

K ll A 01 $1 00 0 0% 12 4% 2013 id l k ti d t t Whil i k t th t li FY13 b l k l l Kellogg Aug-01 $1.00 (Actual)

0.0%(Actual)

12.4% (Actual)

2013 guidance looks conservative; modest costs, accelerating innovation, and Pringles momentum offer clear path for EPS upside.

While we see risk to the top line, FY13 numbers look largely achievable due to sustained brand support and improvinginnovation.

Senomyx Aug-01 ($0.06) (Actual)

14.3% (Actual)

25.0% (Actual)

The company continues to make progress towards a sustainable business model with pipeline development and commercial sales growth.

We believe the value of Senomyx lies in the medium-term succession of commercialization opportunities to turn cash flow positive while becoming much less dependent on funded R&D as a source of revenue.

I t A 01 $0 07 (22 2%) (12 5%) Investment and slotting behind new growth vehicles (i e While choppiness is likely for a growth business such as InventureFoods

Aug-01 $0.07 (Actual)

(22.2%) (Actual)

(12.5%) (Actual)

Investment and slotting behind new growth vehicles (i.e. Seattle's Best) should stunt near-term earnings growth, while the core snack biz will be pressured by category innovation.

While choppiness is likely for a growth business such as Inventure, distribution gains and licensing deals should drive well above-average sales growth, while improved utilization boosts gross margins from their relatively low level.

Kraft Foods Aug-01 $0.76(Actual)

5.6% (Actual)

(12.6%) (Actual)

Strong productivity and new product momentum suggest high visibility to EPS, but sole exposure to U.S. market limits upside.

With Q1, mgmt is off to a good start, having delivered strong FCF, volume, and ad spend, which together suggest improving visibility to FY13 FCF guidance (at least $1B).

Mondelēz Aug-07 $0.33 /$0.33

(6.8%) (8.0%) Sales and margins likely to remain weak in Q2 but should accelerate in 2H13 and beyond due to increased investments

Sales growth and margins likely to remain depressed in Q2; anticipated 2H13 acceleration on easier comps and emg mkt

ffin emerging markets and productivity in developed markets. investments could be offset by prolonged weakness in gum, which worsened in Q1.

4

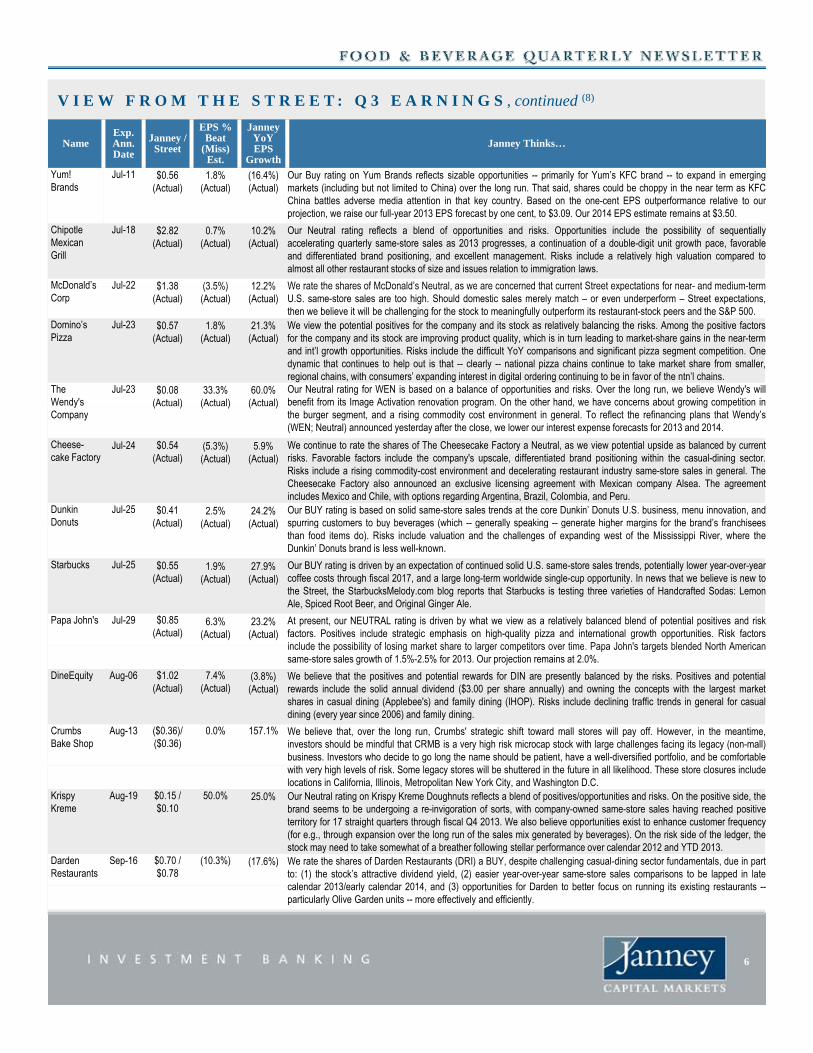

V I E W F R O M T H E S T R E E T : Q 3 E A R N I N G S , continued (8)

NameExp.Ann. Date

Janney /Street

EPS %Beat

(Miss) Est.

Janney YoY EPS

Growth

Street Expects… Janney Thinks…

GreenMountainCoffeeRoasters

Aug-07 $0.78 /$0.72

2.5% 49.3% Near-term outlook solid given continued strong takeaway for brewers and K-Cups and easing headwinds (green coffee prices, capacity utilization); Starbucks re-up removes key intermediate risk; channel, line, and international expansion suggest meaningful long-term opportunity.

We anticipate sustained top line momentum and near-term margin improvement, though quality Green Mountain-produced K-Cups at the low end of the pricing scale (i.e. Kirkland) has potential implications for the retail price/mix and profit efficiency.

Dean Foods Aug-07 $0.15 /$0.16

8.5% (58.0%) While Dean is likely to benefit from productivity improvements, anticipated milk volume declines resulting from a key contract loss and general category weakness, will drive operational deleveraging above those benefits.

While we expect 2Q13 operating margin per gallon to rise modestly in the face of a potentially significant volume decline (-7%), we believe that both mixshift and plant-level cost savings will help offset production inefficiencies.

Snyder's-Lance

Aug-08 $0.29 /$0.28

5.5% 35.6% Looking for top line trends to stabilize as focus narrows to core brands; 10% EBIT margin in 2-3 years on improved scale efficiency, portfolio optimization.

While the long-suffering non-branded sgmt appears to be closer to right-sized, with improved profitability, and core four brands are gaining market share, a ramp in mktingspend to support those and catch up invmt in Pretzel Crisps in subsequent Q at least temporarily stunt margin growth.

Chiquita Aug-08 $0.52 /$0.41

25.8% 91.6% Weak banana fundamentals unlikely to turn around anytime soon; euro volatility, financial leverage make for lowvisibility.

Soft NT banana outlook remains a drag on 2013 but should be offset by good progress on restructuring initiatives and new product wins; suggests improved visibility to midcycleconditions.

TreeHouse Aug-08 $0.61 /$0.63

(2.7%) 3.0% Industry headwinds appear to be abating, but visibility remains choppy from one quarter to the next; talk on M&A yet to materialize.

Gross margin upside should continue on moderating input costs and improving consumption trends; expect fundamentals and deals to pick up in the year ahead on moderating costs and normal margins.

FlowersFoods

Aug-13 $0.37 /$0.35

3.9% 69.3% Upside to current forecasts on anticipated top line andmargin accretion while Hostess dark; longer-term, theacquisition of select Hostess assets and brands will likely improve the industry's profit pool significantly.

The recent step-function improvement from the Hostess liquidation makes for a strong near-term outlook, but bread is historically a low return business and remained so during a pre-Hostess period of dramatic consolidation.

Pinnacle Aug 14 $0 28 / 86 7% 60 3% High probability of upside to FY guidance driven by Should see improved margin flexibility throughout the year Pinnacle Foods

Aug-14 $0.28 / $0.15

86.7% 60.3% High probability of upside to FY guidance driven by favorable mix and tepid cost inflation.

Should see improved margin flexibility throughout the year on modest cost inflation, leading share positions, and mix-positive innovations.

J.M. Smucker

Aug-16 $1.20 /$1.20

0.0% 2.2% Deceleration in K-Cups, both in volume and pricing as increased competition at the low end enters the fray in ever-increasing numbers, brings into question the outlook for Smucker's fastest growth segment.

We view concerns over lower pricing and Kcup deceleration as overblown–especially given that we believe its a 25% margin business driving upwards of $75M in FCF during thisperiod of green coffee cost deflation, which in part drives oursuspicion that guidance for FY14 FCF of $600M appearsconservative.

H i $0 62 / % % R f i U S t li th i t C t i i d it tili ti d t HainCelestial

Aug-21 $0.62 /$0.62

0.0% 31.3% Runway for organic U.S. top line growth remains strong. There is meaningful scale leverage available in Europe on the heels of recent deals (Daniels Group, Premier).

Customer wins, improved capacity utilization, and apparent cost and mfg synergies, figures to drive LDD margins in the UK over the next 18 months, which is largely built into our model, and combined with the limited potential for accretive N-T acquisitions, implies minimal upside.

Hormel Aug-22 $0.42 /$0.47

(11.9%) 0.9% Negative preannouncement offers buying opportunity; likely to regain EPS momentum on better results in pork, strong portfolio, and solid balance sheet.

The quickness of the neg. preannouncement after Q2 update implies low NT visibility; prolonged headwinds in pork and mean reversion in turkey margins should continue to pressure earnings in the quarters ahead.

Campbell Aug-30 $0.40 /$0.42

(5.5%) (3.0%) EPS momentum likely to slow on tough weather comps and continued pressures in beverages and foodservice.

Despite solid new product innovations and a strong soup season, we think ad spend will eventually need to increase, especially as CPB consciously diversifies away from its dominant soup business.

CalavoGrowers

Sep-05 $0.39 /$0.40

(3.0%) 0.7% Lumpy investment in avocado market share likely to be only a NT impact; LT growth outlook remains solid on favorable avocado industry trends and momentum in RFG.

Top line outlook remains stellar but aggressive discounting to grow share of Mexican imports has pressured per box profits; since this is a new direction for the company, we will wait and see if profitability can return to historical levels.

Limoneira Sep-05 $0.47 / 7.4% 7.1% Encouraging NT outlook for development of East Area I & II; Good momentum in Agribusiness ops (lemons, avocados),

5

o e a Sep 05 $0 /$0.44

7.4% cou ag g out oo o de e op e t o ast ea & ;FY guidance for volume growth in lemons (+25%) and avocados (+50%) looks conservative.

Good o e tu g bus ess ops ( e o s, a ocados),but that's a tertiary consideration to the outlook for dev. of East Area I & II, which appears to be accelerating.

V I E W F R O M T H E S T R E E T : Q 3 E A R N I N G S , continued (8)

NameExp.Ann. Date

Janney /Street

EPS %Beat

(Miss) Est.

Janney YoY EPS

Growth

Janney Thinks…

Yum! Brands

Jul-11 $0.56 (Actual)

1.8%(Actual)

(16.4%)(Actual)

Our Buy rating on Yum Brands reflects sizable opportunities -- primarily for Yum’s KFC brand -- to expand in emergingmarkets (including but not limited to China) over the long run. That said, shares could be choppy in the near term as KFCChina battles adverse media attention in that key country. Based on the one-cent EPS outperformance relative to ourprojection, we raise our full-year 2013 EPS forecast by one cent, to $3.09. Our 2014 EPS estimate remains at $3.50.

Chipotle Mexican Grill

Jul-18 $2.82 (Actual)

0.7% (Actual)

10.2% (Actual)

Our Neutral rating reflects a blend of opportunities and risks. Opportunities include the possibility of sequentiallyaccelerating quarterly same-store sales as 2013 progresses, a continuation of a double-digit unit growth pace, favorableand differentiated brand positioning, and excellent management. Risks include a relatively high valuation compared toalmost all other restaurant stocks of size and issues relation to immigration laws.

McDonald’s Jul-22 $1 38 (3 5%) 12 2% We rate the shares of McDonald’s Neutral as we are concerned that current Street expectations for near- and medium-termMcDonald s Corp

Jul 22 $1.38 (Actual)

(3.5%)(Actual)

12.2% (Actual)

We rate the shares of McDonald s Neutral, as we are concerned that current Street expectations for near- and medium-termU.S. same-store sales are too high. Should domestic sales merely match – or even underperform – Street expectations,then we believe it will be challenging for the stock to meaningfully outperform its restaurant-stock peers and the S&P 500.

Domino’s Pizza

Jul-23 $0.57 (Actual)

1.8% (Actual)

21.3% (Actual)

We view the potential positives for the company and its stock as relatively balancing the risks. Among the positive factorsfor the company and its stock are improving product quality, which is in turn leading to market-share gains in the near-termand int’l growth opportunities. Risks include the difficult YoY comparisons and significant pizza segment competition. Onedynamic that continues to help out is that -- clearly -- national pizza chains continue to take market share from smaller,regional chains, with consumers’ expanding interest in digital ordering continuing to be in favor of the ntn’l chains.

The Wendy's

Jul-23 $0.08 (Actual)

33.3%(Actual)

60.0%(Actual)

Our Neutral rating for WEN is based on a balance of opportunities and risks. Over the long run, we believe Wendy's willbenefit from its Image Activation renovation program. On the other hand, we have concerns about growing competition iny

Company ( ) ( ) ( ) g p g , g g p

the burger segment, and a rising commodity cost environment in general. To reflect the refinancing plans that Wendy’s(WEN; Neutral) announced yesterday after the close, we lower our interest expense forecasts for 2013 and 2014.

Cheese-cake Factory

Jul-24 $0.54(Actual)

(5.3%)(Actual)

5.9%(Actual)

We continue to rate the shares of The Cheesecake Factory a Neutral, as we view potential upside as balanced by currentrisks. Favorable factors include the company's upscale, differentiated brand positioning within the casual-dining sector.Risks include a rising commodity-cost environment and decelerating restaurant industry same-store sales in general. TheCheesecake Factory also announced an exclusive licensing agreement with Mexican company Alsea. The agreementincludes Mexico and Chile, with options regarding Argentina, Brazil, Colombia, and Peru.

Dunkin Donuts

Jul-25 $0.41(Actual)

2.5%(Actual)

24.2%(Actual)

Our BUY rating is based on solid same-store sales trends at the core Dunkin’ Donuts U.S. business, menu innovation, andspurring customers to buy beverages (which -- generally speaking -- generate higher margins for the brand’s franchisees(Actual) (Actual) (Actual) spu g custo e s to buy be e ages ( c ge e a y spea g ge e ate g e a g s o t e b a d s a c seesthan food items do). Risks include valuation and the challenges of expanding west of the Mississippi River, where theDunkin’ Donuts brand is less well-known.

Starbucks Jul-25 $0.55(Actual)

1.9%(Actual)

27.9%(Actual)

Our BUY rating is driven by an expectation of continued solid U.S. same-store sales trends, potentially lower year-over-yearcoffee costs through fiscal 2017, and a large long-term worldwide single-cup opportunity. In news that we believe is new tothe Street, the StarbucksMelody.com blog reports that Starbucks is testing three varieties of Handcrafted Sodas: LemonAle, Spiced Root Beer, and Original Ginger Ale.

Papa John's Jul-29 $0.85(Actual)

6.3%(Actual)

23.2%(Actual)

At present, our NEUTRAL rating is driven by what we view as a relatively balanced blend of potential positives and riskfactors. Positives include strategic emphasis on high-quality pizza and international growth opportunities. Risk factorsinclude the possibility of losing market share to larger competitors over time Papa John's targets blended North Americaninclude the possibility of losing market share to larger competitors over time. Papa John s targets blended North Americansame-store sales growth of 1.5%-2.5% for 2013. Our projection remains at 2.0%.

DineEquity Aug-06 $1.02 (Actual)

7.4% (Actual)

(3.8%) (Actual)

We believe that the positives and potential rewards for DIN are presently balanced by the risks. Positives and potentialrewards include the solid annual dividend ($3.00 per share annually) and owning the concepts with the largest marketshares in casual dining (Applebee's) and family dining (IHOP). Risks include declining traffic trends in general for casualdining (every year since 2006) and family dining.

Crumbs Bake Shop

Aug-13 ($0.36)/ ($0.36)

0.0% 157.1% We believe that, over the long run, Crumbs' strategic shift toward mall stores will pay off. However, in the meantime,investors should be mindful that CRMB is a very high risk microcap stock with large challenges facing its legacy (non-mall)business. Investors who decide to go long the name should be patient, have a well-diversified portfolio, and be comfortable

i h hi h l l f i k S l ill b h d i h f i ll lik lih d Th l i l dwith very high levels of risk. Some legacy stores will be shuttered in the future in all likelihood. These store closures includelocations in California, Illinois, Metropolitan New York City, and Washington D.C.

KrispyKreme

Aug-19 $0.15 / $0.10

50.0% 25.0% Our Neutral rating on Krispy Kreme Doughnuts reflects a blend of positives/opportunities and risks. On the positive side, thebrand seems to be undergoing a re-invigoration of sorts, with company-owned same-store sales having reached positiveterritory for 17 straight quarters through fiscal Q4 2013. We also believe opportunities exist to enhance customer frequency(for e.g., through expansion over the long run of the sales mix generated by beverages). On the risk side of the ledger, thestock may need to take somewhat of a breather following stellar performance over calendar 2012 and YTD 2013.

Darden Restaurants

Sep-16 $0.70 / $0.78

(10.3%) (17.6%) We rate the shares of Darden Restaurants (DRI) a BUY, despite challenging casual-dining sector fundamentals, due in partto: (1) the stock’s attractive dividend yield, (2) easier year-over-year same-store sales comparisons to be lapped in latecalendar 2013/early calendar 2014 and (3) opportunities for Darden to better focus on running its existing restaurantscalendar 2013/early calendar 2014, and (3) opportunities for Darden to better focus on running its existing restaurants --particularly Olive Garden units -- more effectively and efficiently.

6

$10,00060IPO

Annual Equity Offering Activity (9)Quarterly Equity Offering Activity (9)

While Q1 2013 was the most active quarter for equityofferings since 2009, Q2 2013 offering activity fell…

… however, post deal performances have generallybeen strong (Noodles IPO up 104%).

8

10

12

14

16

r of O

fferin

gs

IPO

FO

CVT

Series4

32

11

2

1

$

$5,000

$6,000

$7,000

$8,000

$9,000

30

40

50

Deal Value ($ be

r of O

fferin

gs

IPOFOCVTAgg Deal Value

5

32

4

1

1

1

2

13

8

5

1

3

12

4

12

1 12

3

6

1

1

1

14

1

2 21

4 2

1

1

0

2

4

6

Num

ber

3 2 2 2

18 20

63

9 712

11

23

10 9 7 72

6 86

63 9

2

$0

$1,000

$2,000

$3,000

$4,000

0

10

20

2003 2005 2007 2009 2011 2013 YTD

MM

)

Num

b

YTD

Select Recent Equity Offering Activity (9)

PricingDate Issuer Business Description Deal Sub Type Amt

($MM)% Ch. 1-day

% Ch. 1-month

06/27/13 Noodles & Co. Fast casual restaurants IPO – Common Shares $96.4 104.2% N/A

05/22/13 Bloomin Brands Casual dining restaurants FO – Common Shares $408.5 2.9% 16.4%

03/27/13 Pinnacle Foods Inc. Manufactures branded food products IPO – Common Shares $667.0 11.1% 18.0% 03/ / 3 ac e oods c a u actu es b a ded ood p oducts O Co o S a es $66 0 % 18.0%

03/21/13 Fiesta Restaurant Group, Inc. Casual dining restaurants FO – Common Shares $70.3 7.1% 0.9%

03/12/13 Annie’s, Inc. Natural food products FO – Common Shares $140.0 0.1% -5.9%

03/07/13 Del Frisco’s Restaurant Group, Inc. Full-service restaurants FO – Common Shares $80.8 0.0% -4.5%

02/13/13 Limoneira Company Agribusiness FO – Common Shares $38.3 0.5% 0.5%

01/24/13 Chuy’s Holdings, Inc. Casual dining restaurants FO – Common Shares $129.4 13.1% 11.9%

01/07/13 ConAgra Foods, Inc. Packaged food FO – Common Shares $275.0 1.3% 11.9%g g

12/04/12 Carrols Restaurant Group Quick-service and quick-casual restaurants FO – Common Shares $23.7 7.2% 6.6%

10/25/12 The WhiteWave Foods Co. Consumer food and beverage IPO – Common Shares $391.0 -1.5% -1.5%

10/09/12 Amira Nature Foods Ltd. Packaged specialty rice and snacks IPO – Common Shares $90.0 -18.3% -4.2%

10/02/12 B&G Foods, Inc. Packaged food and meats FO – Common Shares $126.2 -3.1% 0.1%

08/09/12 Dunkin’ Brands Group, Inc. Serves coffee, baked goods FO – Common Shares $661.3 -0.3% -2.7%

08/07/12 Bloomin Brands Casual dining restaurants IPO – Common Shares $202.3 12.8% 31.3%

07/31/12 Annie's Natural food products FO – Common Shares $143.3 1.6% 5.9%

07/26/12 Del Frisco's Steakhouse restaurants IPO – Common Shares $75.4 0.0% -2.1%

07/24/12 Natural Grocers Natural grocery store IPO – Common Shares $107.1 19.1% 30.5%

07/23/12 Chuy's Holdings Casual dining restaurants IPO – Common Shares $87.2 15.9% 38.8%

06/12/12 The Fresh Market Gourmet supermarket FO – Common Shares $506.7 0.0% 9.8%

05/10/12 Ignite Restaurant Group Casual dining restaurants IPO – Common Shares $92.9 22.4% 28.9%

03/30/12 Dunkin’ Brands Group, Inc. Serves coffee, baked goods FO – Common Shares $895.6 2.0% 10.3%All data shown above for Food, Beverage & Restaurant industry only, most recent transactions to 6/30/13

7

35

40

45

50

60

70

80

90

s V

Number of Loans

Volume of Loans ($ in MM)

20

25

35

40

45

s

Number of Bonds

$ of Bonds

Quarterly Bond Volume (2) Quarterly Loan Volume (2)

0

5

10

15

20

25

30

35

0

10

20

30

40

50

60

Num

ber o

f Loa

ns

Volumes ($ BN

)

0

5

10

15

0

5

10

15

20

25

30

Volumes ($ BN

)

Num

ber o

f Bon

ds

Interest Rate Forecasts (%) (2) Credit Spreads (2)

Security 6/30/13Forecast

3Q13

4Q13

1Q14

2Q14

1200 bps

1400 bps

1600 bpsAaa

Aa

A

BaaFed Funds Target 0.25 0.25 0.25 0.25 0.25

3-Month LIBOR 0.27 0.30 0.31 0.33 0.36

2-Year T-Note 0.36 0.37 0.45 0.54 0.65

10-Year T-Note 2.52 2.50 2.62 2.78 2.90

30-Year T-Note 3.52 3.58 3.67 3.81 3.93

+386bps

+221bps+132 bps200 bps

400 bps

600 bps

800 bps

1000 bps

1200 bps Baa

Ba/B

Sign. Date

Borrower Description Type Size

($ MM)Maturity Rating Use of Proceeds

06/28/13 CTI Foods Holding Co LLC Food & Beverage TERM 140.0 06/28/21 CCC+ / Caa1 LBO06/28/13 CTI Foods Holding Co LLC Food & Beverage TERM 345 0 06/28/20 B / B2 LBO

Select Recent Debt Offerings (2)

+73 bps+98 bps

p

00 bps

200 bps

01/06 07/06 01/07 07/07 01/08 07/08 01/09 07/09 01/10 07/10 01/11 07/11 01/12 07/12 01/13 07/13

06/28/13 CTI Foods Holding Co LLC Food & Beverage TERM 345.0 06/28/20 B / B2 LBO06/26/13 CHS Inc Retail Staples REV 2,500.0 06/26/18 NR / NR Refinance Debt06/21/13 Rite Aid Corp Retail Staples TERM 500.0 06/21/21 B- / B3 Refinance Debt06/19/13 Glazers Inc Food & Beverage REV 600.0 06/19/18 NR / NR General Corporate Purposes06/19/13 Orchard Supply Hardware LLC Retail Staples DIP REV 140.0 12/14/13 NR / NR General Corporate Purposes06/18/13 Rite Aid Corp Retail Staples 6.75 Cpn Bond 810.0 6/15/21 CCC / Caa2 Repay/Refinance Debt06/18/13 Rite Aid Corp Retail Staples 6.75 Cpn Bond 810.0 6/15/21 CCC / Caa2 Repay/Refinance Debt06/17/13 Casey‘s General Stores Inc Retail Staples 3.67 Cpn Bond 150.0 06/15/28 NR / NR N/A06/10/13 PepsiCo Inc Food & Beverage REV 2,875.0 06/10/18 NR / NR General Corporate Purposes06/10/13 PepsiCo Inc Food & Beverage REV 2,875.0 06/09/14 NR / NR General Corporate Purposes06/07/13 HJ Heinz Co Food & Beverage TERM 6,550.0 06/05/20 BB / Ba2 LBO06/07/13 HJ Heinz Co Food & Beverage TERM 2,950.0 06/07/19 BB / Ba2 LBO06/07/13 HJ Heinz Co Food & Beverage REV 1,000.0 06/07/18 BB / Ba2 LBO06/07/13 HJ Heinz Co Food & Beverage REV 375.0 06/07/18 NR / NR LBO06/07/13 HJ Heinz Co Food & Beverage REV 625.0 06/07/18 NR / NR LBO06/07/13 US Foods Inc Retail Staples TERM 2,100.0 03/31/19 B- / B2 Refinance Debt06/04/13 Nestle Holdings Inc Food & Beverage 2 Cpn Bond 500.0 12/11/19 NR / Aa2 N/A6/3/2013 Beam Inc Food & Beverage 1.75 Cpn Bond 250.0 06/15/18 BBB- / Baa2 Repay/Refinance Debt6/3/ 0 3 ea c ood & e e age 5 Cp o d 50 0 06/ 5/ 8 / aa epay/ e a ce eb6/3/2013 Beam Inc Food & Beverage 3.25 Cpn Bond 250.0 06/15/23 BBB- / Baa2 Repay/Refinance Debt

8

All data shown above for Food, Beverage & Restaurant industry only from 4/1/2013 to 6/30/13; ratings by S&P / Moody’s; date represents signing data for loans and announcement date for bonds

Select Recent Debt Offerings, continued (2)

Sign. Date

Borrower Description Type Size

($ MM)Maturity Rating Use of Proceeds

6/1/2013 Wal-Mart Stores Inc Retail Staples 5.403 Cpn Bond 500.0 6/1/2014 AA / Aa2 General Working Capital05/31/13 JR Simplot Co Food & Beverage REV 110.0 09/15/18 NR / NR Refinance Debt05/29/13 Smart & Final Inc Supermarkets TERM 578.7 11/15/19 NR / NR Refinance Debt5/29/2013 Ingles Markets Inc Supermarkets 5.75 Cpn Bond 700.0 06/15/23 BB- / B1 Capital Expenditures5/29/2013 Ingles Markets Inc Supermarkets 5.75 Cpn Bond 700.0 06/15/23 BB- / B1 Capital Expenditures05/20/13 B&G Foods Inc Food & Beverage 4.625 Cpn Bond 700.0 06/01/21 B+ / B1 Repay/Refinance Debt05/16/13 SUPERVALU Inc Supermarkets TERM 1,500.0 03/21/19 B+ / B1 Refinance Debt05/16/13 Wendy's International Inc Restaurants TERM 769.4 05/15/19 BB- / B1 Refinance Debt05/16/13 Wendy's International Inc Restaurants TERM 350.0 05/15/18 BB- / B1 Refinance Debt05/16/13 Supervalu Inc Supermarkets 6.75 Cpn Bond 400.0 06/01/21 B- / Caa1 Loan Payment05/16/13 Supervalu Inc Supermarkets 6 75 Cpn Bond 400 0 06/01/21 B- / Caa1 General Corporate Purpose05/16/13 Supervalu Inc Supermarkets 6.75 Cpn Bond 400.0 06/01/21 B / Caa1 General Corporate Purpose05/15/13 Pinnacle Operating Corp Retail Staples TERM 348.3 11/13/18 B / B2 Refinance Debt05/15/13 Mcdonald'S Corp Restaurants 2 Cpn Bond 350.0 06/01/23 A / A2 Loan Payment05/14/13 Dave & Buster's Inc Restaurants TERM 145.9 06/01/16 NR / NR Refinance Debt05/14/13 Hershey Co/The Food & Beverage 2.625 Cpn Bond 250.0 05/01/23 A / A2 /*+ General Corporate Purpose05/13/13 Cedc Finance Corp International Food & Beverage 10 Cpn Bond 200.0 04/30/18 NR / NR N/A05/13/13 Cedc Finance Corp International Food & Beverage 8 Cpn Bond 465.0 04/30/18 NR / NR N/A05/09/13 Albertsons LLC Supermarkets TERM 700.0 05/09/19 BB- / NR Refinance Debt05/09/13 Albertsons LLC Supermarkets TERM 450.0 03/21/16 NR / NR Refinance Debt05/08/13 B i k I t ti l I R t t 3 875 C B d 300 0 05/15/23 BBB / B 2 Sh B b k05/08/13 Brinker International Inc Restaurants 3.875 Cpn Bond 300.0 05/15/23 BBB- / Ba2 Share Buyback05/08/13 Brinker International Inc Restaurants 2.6 Cpn Bond 250.0 05/15/18 BBB- / Ba2 Repay/Refinance Debt05/08/13 Tops Holding Ii Corp Retail Staples 8.75 Cpn Bond 150.0 06/15/18 CCC+ / Caa2 Loan Payment05/08/13 Tops Holding Ii Corp Retail Staples 8.75 Cpn Bond 150.0 06/15/18 CCC+ / Caa2 General Corporate Purpose05/06/13 Fresh Mark Inc Food & Beverage REV 125.0 05/06/18 NR / NR General Corporate Purposes05/03/13 Fairway Group Acquisition Co Supermarkets TERM 274.3 08/17/18 NR / NR Refinance Debt05/01/13 Landry'S Inc Restaurants 9.375 Cpn Bond 235.0 05/01/20 CCC+ / B3 Repay/Refinance Debt04/30/13 FOCUS Brands Inc Restaurants TERM 358.0 02/22/18 NR / B1 Refinance Debt04/30/13 Constellation Brands Inc Food & Beverage 4.25 Cpn Bond 1,050.0 05/01/23 BB+ / Ba1 Acquisition Financing04/30/13 Constellation Brands Inc Food & Beverage 3.75 Cpn Bond 500.0 05/01/21 BB+ / Ba1 Loan Payment04/29/13 Pinnacle Foods Finance LLC Retail Staples TERM 1,630.0 04/29/20 BB / Ba3 Refinance Debt04/29/13 Coca-Cola Enterprises Inc Food & Beverage 2.375 Cpn Bond 350.0 05/07/25 BBB / A3 General Corporate Purpose04/29/13 McDonald’s Corp Restaurants 3.625 Cpn Bond 500.0 5/1/243 A / A2 General Corporate Purpose04/25/13 Cst Brands Inc Retail Staples 5 Cpn Bond 550.0 05/01/23 BB- / Ba3 N/A04/25/13 Cst Brands Inc Retail Staples 5 Cpn Bond 550.0 05/01/23 BB- / Ba3 N/A04/24/13 Denny's Inc Restaurants REV 190.0 04/24/18 NR / NR Refinance Debt04/24/13 Pantry Inc/The Retail Staples 8.375 Cpn Bond 250.0 08/01/20 B+ / Caa1 General Corporate Purpose04/15/13 Pinnacle Foods Finance Llc Food & Beverage 4 875 Cpn Bond 350 0 05/01/21 B- / B3 Repay/Refinance Debt04/15/13 Pinnacle Foods Finance Llc Food & Beverage 4.875 Cpn Bond 350.0 05/01/21 B- / B3 Repay/Refinance Debt04/15/13 Pinnacle Foods Finance Llc Food & Beverage 4.875 Cpn Bond 350.0 05/01/21 B- / B3 General Corporate Purpose04/11/13 Dollar General Corp Retail Staples TERM 1,000.0 04/11/18 BBB- / NR Refinance Debt04/11/13 Dollar General Corp Retail Staples REV 850.0 04/11/18 BBB- / NR Refinance Debt04/10/13 OSI Restaurant Partners LLC Restaurants TERM 975.0 10/26/19 BB / B1 Refinance Debt04/09/13 Ignite Restaurant Group Inc Restaurants REV 100.0 04/08/18 NR / NR Acquisition04/08/13 Dollar General Corp Retail Staples 3.25 Cpn Bond 900.0 04/15/23 BB+ *+ / Baa3 Loan Payment04/08/13 Dollar General Corp Retail Staples 1.875 Cpn Bond 400.0 04/15/18 BB+ *+ / Baa3 General Corporate Purpose04/05/13 Flowers Foods Inc Food & Beverage DELAY-DRAW TERM 300.0 04/05/18 NR / NR Acquisition04/05/13 Us Foods Inc Retail Staples 8.5 Cpn Bond 1,323.8 06/30/19 CCC+ / Caa2 General Corporate Purpose04/04/13 Wal-Mart Stores Inc Retail Staples 2.55 Cpn Bond 1,750.0 04/11/23 AA / Aa2 General Corporate Purpose04/04/13 Wal-Mart Stores Inc Retail Staples 1.125 Cpn Bond 1,250.0 04/11/18 AA / Aa2 General Corporate Purpose04/04/13 Wal-Mart Stores Inc Retail Staples 4 Cpn Bond 1,000.0 04/11/43 AA / Aa2 General Corporate Purpose04/04/13 Wal-Mart Stores Inc Retail Staples 0.6 Cpn Bond 1,000.0 04/11/16 AA / Aa2 General Corporate Purpose04/03/13 Ruby Tuesday Inc Restaurants 7.625 Cpn Bond 234.9 05/15/20 B- / B3 Bond Exchange04/01/13 Dole Food Co Inc Food & Beverage TERM 675.0 04/01/20 B+ / Ba3 Refinance Debt04/01/13 Dole Food Co Inc Food & Beverage DELAY-DRAW TERM 125.0 04/01/20 NR / WR Refinance Debt04/01/13 Reddy Ice Corp Food & Beverage TERM 120.0 10/01/19 NR / NR Refinance Debt

9

y p g04/01/13 Reddy Ice Corp Food & Beverage TERM 225.0 04/01/19 B / B1 Refinance Debt

All data shown above for Food, Beverage & Restaurant industry only from 4/1/2013 to 6/30/13; ratings by S&P / Moody’s; date represents signing data for loans and announcement date for bonds

$120,000600 Food Retail180Food Retail

Annual M&A Activity (1)Quarterly M&A Activity (1)

M&A activity in the Food & Beverage sectorsincreased over Q1 2013...

… and aggregate deal values increased as a result ofseveral large transactions (including Heinz acquisition)

28230976 66

117

131

105

124

118129 142

50 51

79

85

67

60

89 73 78

$60,000

$80,000

$100,000

300

400

500

Deal Value ($ r o

f Tra

nsac

tions

Restaurant

Food & Beverage

28 2932 32 36

42

31

23

2750

42

43 36

22

1119

2027

23

2217 16

21

22

14

10

2022

26

1220

80

100

120

140

160

er o

f Tra

nsac

tions

Restaurants

Food & Beverage

174

221 227258

198

249 261236

100

47

79

44

32

$0

$20,000

$40,000

0

100

200

2003 2005 2007 2009 2011 2013 YTD

MM

)

Num

ber

55

43 42 4136

5147

53 56 57 5462

49

6355

67

50

64

4852

2621 23

32

29 30 2420

231110 11

0

20

40

60

Num

be

Ann.Date

Target Business Description Acquirer EVEV/

Rev. EBITDA06/27/13 Tulocay & Company, Certain Brands Produce food products Robert Rothschild Farm, LLC - - -

06/26/13 Snapfinger Platform for online and mobile food ordering EMN8, Inc. - - -

06/25/13 The New French Bakery Inc. Manufactures and sells breads and rolls Arbor Private Investment Company - - -

06/25/13 Raley Bros And Tubbs Rice And Grain Produces and markets agricultural products Agspring LLC

YTD

Select Recent M&A Activity (1)(8)

06/25/13 Raley Bros And Tubbs Rice And Grain Produces and markets agricultural products Agspring, LLC - - -

06/24/13 Cains Foods, L.P. Food products for retail and food service customers Treehouse Foods, Inc. (NYSE:THS) $35.0 0.44x -

06/21/13 IGA Portage Lakes SuperCenter Owns and operates a supermarket in Ohio Buehler Food Markets, Inc. - - -

06/21/13 Stacy's Greenhouses, Inc. Operates a nursery in South Carolina Metrolina Greenhouses, Inc. $17.0 - -

06/20/13 Primera Foods Corporation Provides egg and specialty products M.G. Waldbaum Company $35.7 - -

06/20/13 Value Foods Company Owns 13 franchised Wendy's restaurants NPC Quality Burgers, Inc. $11.0 0.70x -

06/19/13 Austin Packaging Company Engages in contract manufacturing and packaging Bellisio Foods, Inc. $6.4 - -

06/19/13 FITT Highway Products Manufacture distribution and sale of energy drinks F I T T Energy Products Inc06/19/13 FITT Highway Products Manufacture, distribution, and sale of energy drinks F.I.T.T. Energy Products, Inc. - - -

06/18/13 The Johnny Rockets Group, Inc. Owns and operates a chain of restaurants Sun Capital Partners, Inc. - - -

06/13/13 Long Grove Confectionery Co. Produces and sells chocolates Baldi Candy Company - - -

06/13/13 RMH Foods, LLC Produces food products Sandridge Food Corporation - - -

06/13/13 24 Wendy's Restaurants Owns 24 Wendy's Restaurants in Kansas City NPC International, Inc. $9.3 - -

06/12/13 Canada Safeway Limited Owns and operates food stores Sobeys Inc. $5,690.1 0.87x 10.7x06/12/13 Three Krispy Kreme shops in Dallas Owns three Krispy Kreme shops in Dallas Sun Holdings, LLC - - -

06/11/13 Ott ' Chi k T d LLC O d t f t f d t t P t F d LLC06/11/13 Otter's Chicken Tenders, LLC Owns and operates a fast food restaurant Peterson Foods, LLC - - -

06/11/13 American Restaurant, reverse merger Quick service, fast casual & casual restaurants American Restaurant (OTCPK:FEII.D) - - -

06/10/13 Robert's American Gourmet Food, LLC Produces snack food products B&G Foods North America, Inc. $195.0 - -

06/08/13 Skyfall Vineyard Owns a vineyard of approximately 174 acres Precept Wine - - -

06/07/13 Gerland Corporation Owns and operates supermarkets in Houston The Grocers Supply Co., Inc. - - -

06/07/13 VPS Convenience Store, SE Division Owns 263 convenience stores GPM Investments, LLC. - - -

06/05/13 H&J Trading Corporation Markets food products Atalanta Corporation - - -

06/04/13 Mastro's Restaurants, LLC Owns and operates steakhouse/seafood restaurants Landry's, Inc. - - -

10

All data shown above for Food, Beverage & Restaurant industry only from 4/1/2013 to 6/30/13

Select Recent M&A Activity, continued (1)(7)

Ann.Date

Target Business Description Acquiror EVEV/

Rev. EBITDA06/03/13 Pryority Food Marketing, Inc. Operates as a food brokerage company Advantage Sales and Marketing LLC - - -

06/03/13 Thompsons Limited Supplies and offers food products The Andersons, Inc. (Nasdaq:ANDE) $145.0 - -

06/03/13 Farmland in Marion County Owns a farm to cultivate blueberries Gladstone Land (Nasdaq:LAND) $3.1 - -

06/03/13 Circle Foods, LLC Produces and sells specialty food products Tyson Foods, Inc. (NYSE:TSN) - - -

06/03/13 43 Church Operates as a restaurant and offers dining services J. Turner Seafoods Inc. $1.5 - -

05/29/13 Smithfield Foods, Inc. (NYSE:SFD) Produces Fresh meat and packaged meat Henan Shineway Industry Group Co., Ltd. $6,965.6 0.53x 9.17x05/28/13 Delhaize America, Supermarket stores Owns 165 supermarket stores BI-LO, LLC $265.0 0.15x -

05/28/13 Jack in the Box,18 Restaurants in TX Owns 18 Restaurants in Beaumont, Texas TLIG Restaurants, LLC - - -

05/24/13 248-Acre Vineyard Sonoma Coast Owns a 248-Acre Vineyard Guarachi Family Wines05/24/13 248 Acre Vineyard, Sonoma Coast Owns a 248 Acre Vineyard Guarachi Family Wines - - -

05/23/13 Plum Organics, Inc. Production of organic baby food products Campbell Soup Company (NYSE:CPB) - - -

05/22/13 Silverbow Honey Co., Inc. Processing, packaging, and sale of honey NutraBev Holdings International, Inc. - - -

05/21/13 Gregory Farmers Elevator Company Provides grain storage and distribution services Interstate Commodities, Inc. $0.6 - -

05/21/13 Empire Wineries, LLC Produces wines, vodka and spirits Panache Distillery, LLC $4.4 - -

05/16/13 Goosecross Cellars Operates a winery Golden Equity Investments - - -

05/15/13 Panther Creek Cellars LLC Produces wines Bacchus Capital Management - - -

05/15/13 Adi N t iti I P d ti A t P id i f bi ti d t Li i E i I (OTCPK LVVV)05/15/13 Adia Nutrition, Inc., Production Assets Provides services of probiotics products Livewire Ergogenics, Inc. (OTCPK:LVVV) $1.0 - -

05/15/13 Overhill Farms, Inc. (AMEX:OFI) Manufactures prepared frozen food products Bellisio Foods, Inc. $84.6 0.44x 13.1x05/14/13 Golden Guernsey Dairy, LLC Manufactures, bottles, and distributes dairy products Lifeway Foods Inc. (Nasdaq:LWAY) $7.4 - -

05/14/13 David's Steak & Spirits Operates as a restaurant Solanbridge Group, Inc. (OTCPK:SLNX) - - -

05/13/13 Nurture, Inc. Produces baby and toddler meals Danone (ENXTPA:BN) - - -

05/10/13 Florida Chemical Company, Inc. Manufactures and supplies citrus oils Flotek Industries Inc. (NYSE:FTK) $102.2 1.00x 10.3x05/10/13 Burger Bar 419 Owns and operates a restaurant in Ohio Star Bar & Grille - - -

05/09/13 CTI Foods, Inc. Provides food solutions for foodservice industry Thomas H. Lee Partners; Goldman Sachs - - -

05/09/13 Hearthside Food, Cereal & Snacks Branded and private label cereal, granola & snacks Attune Foods, Inc. $158.0 - -

05/09/13 Gracious Gifts, Inc. Produces and sells gourmet confectionary snacks Consolidated Investment Group, LLC - - -

05/08/13 Canadian Nutrition Super Stores Owns and operates a chain of discount retail stores Creative Edge Nutrition (OTCPK:FITX) $0.4 - -

05/07/13 DeMet's Candy Company, TrueNorth Owns a roasted nut brand B&G Foods Inc. (NYSE:BGS) - - -

05/06/13 Matilija Pure Water, Bottled Water Owns a bottled water and coffee delivery business DS Waters of America, Inc. - - -

05/06/13 Tru Meals-Diet Gourmet Produces and offers prepared meals Snap Kitchen LLC - - -p p p

05/01/13 Nestlé USA, Inc., Bit-O-Honey Owns Bit-O-Honey candy brand Pearson's Candy Company - - -

04/30/13 Flat Out Crazy, LLC Full-service Asian-style restaurants in the Midwest HillStreet Capital Inc. $2.3 - -

04/26/13 Healthy & Tasty Ventures, LLC Fast food and casual restaurant franchise GRILLiT, Inc. (OTCPK:GRLT) - - -

04/25/13 Willamette Valley, Berry Processing Provides berry processing services Inventure Foods, Inc. (Nasdaq:SNAK) $12.5 0.83x -

04/25/13 Mekonza Corp. Fresh and frozen seafood products Latteno Food Corp. (OTCPK:LATF) - - -

04/23/13 Blue Smoke, Inc. Provides food products National Fruit Product Company, Inc. - - -

04/17/13 Maria's Santa Fe Inc Operates a bar and restaurant in New Mexico Santa Fe Dining Inc - - -04/17/13 Maria s Santa Fe, Inc. Operates a bar and restaurant in New Mexico Santa Fe Dining Inc. - - -

04/16/13 Coca-Cola Bottling Operations in Denver Provides beverage bottling services Swire Coca-Cola, USA - - -

04/16/13 Six Quick Service Restaurants in TX Owns six restaurants in Texas. Indigo Group LLC, Investment Arm - - -

04/15/13 Weathervane Restaurant Property Owns a restaurant offering seafood Turf Hotels, Inc. - - -

04/12/13 Caviness Beef Packers San Angelo, Ltd. Operates a meat processing plant Caviness Beef Packers, LTD. - - -

04/09/13 Eppa Wine Company Produces Eppa SupraFruta Sangria Deutsch Family Wine & Spirits - - -

04/08/13 CB Mart Inc., 46 Stores in South Carolina Owns 46 brand convenience store locations 7-Eleven, Inc. - - -

11

All data shown above for Food, Beverage & Restaurant industry only from 4/1/2013 to 6/30/13

04/05/13 Newark Diner Operates as a restaurant in New York Larkin Enterprises, Inc. - - -

Ann.Date Target Acquiror Seller

06/26/13 BAI Brands Strand Equity Partners -

Th N F h A b P i t I t t

Financial Sponsor Activity (1)Select Recent Financial Sponsor Activity (1)

69

75InvestmentsExits

06/25/13 The New French Bakery

Arbor Private Investment Company

-

06/18/13 The Johnny Rockets Group

Sun Capital Partners Red Zone Capital Management

06/10/13 Robert's American Gourmet Food

B&G Foods North America

VMG Partners

06/05/13 Brad's Raw Foods Ben Franklin Technology Partners of SEPA

- 4648

59

5045

60

Tran

sact

ions

06/03/13 Circle Foods Tyson Foods (NYSE:TSN)

Claridge

05/29/13 NextFoods Maveron; Emil Capital Partners

-

05/23/13 Plum Organics Campbell Soup Company (NYSE:CPB)

Catterton Partners; Catamount Ventures;

05/15/13 Overhill Farms (AMEX:OFI)

Bellisio Foods (Centre Partners)

Public

38

27

22

15

21

14

25

20

26

20

37

2931

15

30

Num

ber o

f T

05/01/13 Philz Coffee Summit Partners -

05/01/13 Tokyo Inc. Gridiron Capital -

04/30/13 Flat Out Crazy HillStreet Capital -

Select Financial Sponsor Sector Snapshot: Fresh Baked Goods

02005 2006 2007 2008 2009 2010 2011 2012 2013

YTD

Select Financial Sponsor Sector Snapshot: Fresh Baked Goods

Financial Sponsor Portfolio Holding Yr. Invested Est. $ Sales (in MMs)(10)

% Sales Growth(10)

% Volume Growth(10)

Plaza Belmont Labriola Baking 2013 2.7 8.8% 5.4%

Arbor Investments New French Bakery 2013 12.0 -11.0% -14.4%

Metropoulos & Co. and Apollo Group Hostess Brands 2013 NMF NMF NMF

Goode Partners Dave’s Killer Bread 2012 44.1 64.0% 66.6%

Frontenac Company Wenner Bread Products 2011 2 8 12 4% 16 9%Frontenac Company Wenner Bread Products 2011 2.8 -12.4% -16.9%

Wind Point Partners Nonni’s Biscotti 2011 - - -

Blue Point Capital JTM Foods 2011 27.9 19.0% 14.3%

Stonebridge Partners Specialty Bakers 2010 36.8 -4.1% -4.5%

Glencoe Capital Pattco 2010 50.7 13.3% 12.1%

Quad-C Management Cloverhill Bakery 2009 106.7 8.8% 5.0%

Ancor Capital Partners Tom Cat Bakery Inc 2008 0.8 -10.6% -8.6%

Arbor Private Investment Gold Standard Baking 2008 - - -

OMERS Give and Go Prepared Foods 2007 91.9 14.5% 11.3%

Swander Pace Pineridge Bakery 2007 - - -

Sherbrooke Capital Immaculate Baking 2006 - - -

Charterhouse Group Charter Baking Company 2005 26.1 34.8% 24.4%

GESD Capital Partners Dobake Bakeries 2002 1.2 -72.1% -76.1%

GESD Capital Partners Gold Coast Baking 2002 3 3 -11 7% -13 4%

12

All data shown above for Food and Beverage and Restaurant sector only; select recent activity list may include non-North American businesses

GESD Capital Partners Gold Coast Baking 2002 3.3 11.7% 13.4%

120

140

160

el)

200

250

Commodity Price Index

Commodity Food & Beverage Price Index

Crude Oil (2)Food & Beverage CPI (2)

0

20

40

60

80

100

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Nea

r Fut

ure

( $ p

er b

arre

0

50

100

150

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

15

20

25

Cen

ts p

er b

ushe

l)

400

500

600

700

800

900

ure

(Cen

ts p

er B

ushe

l)

Wheat (2)Corn (2)

0

5

10

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Whe

aat (

C

0

100

200

300

400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Cor

n -N

ear F

utu

Soybeans (2)Chicken (2)

100

150

200

250

300

Chi

cken

Bre

ast (

cent

s pe

r Lb.

)

600

800

1,000

1,200

1,400

1,600

1,800

2,000

bean

-ne

ar fu

ture

(cen

ts p

er b

ushe

l)

2.5

0

50

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 20130

200

400

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Soy

35

40

World Sugar (2)Cheddar Cheese (2)

0.5

1.0

1.5

2.0

Che

ddar

Che

ese

($ p

er L

b.)

5

10

15

20

25

30

Suga

r -N

ear F

utur

e (C

ents

per

Pou

nd)

0.02001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

02001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

13

14

Inst

.

Mul

tiple

Ow

ners

hip

Div

iden

d

E20

14E

(% o

f Tot

al)

Yie

ld (%

)

x16

.0x

27.1

%3.

3%

x17

.3x

70.4

%2.

6%

x17

.4x

73.0

%3.

5%

x16

.0x

71.6

%2.

9%

x15

.7x

81.0

%2.

7%

x13

.6x

70.8

%2.

7%

x15

.7x

42.7

%2.

5%

x16

.9x

73.8

%2.

1%

x17

.4x

33.6

%1.

6%

x20

.1x

78.5

%1.

9%

x14

.6x

80.2

%2.

8%

x16

.5x

79.2

%1.

4%

x16

.4x

65.2

%2.

5%

x16

.2x

72.3

%2.

7%

x19

.1x

NM

0.0%

x19

.8x

42.6

%2.

1%

x14

.3x

92.2

%0.

0%

x12

.0x

58.4

%2.

8%

AN

/A62

.8%

0.0%

AN

/A41

.8%

0.0%

x16

.3x

59.5

%0.

8%

x16

.7x

58.4

%0.

0%

x28

.3x

84.3

%0.

7%

x20

.7x

92.1

%0.

0%

x19

.5x

23.7

%0.

0%

x19

.9x

96.0

%0.

0%

x26

.3x

85.6

%0.

0%

x38

.5x

NM

0.0%

x27

.0x

88.5

%0.

0%

x45

.7x

41.6

%0.

0%

x14

.5x

65.9

%0.

0%

x34

.4x

17.0

%0.

4%

M33

.3x

5.8%

0.0%

x28

.0x

60.0

%0.

1%

x27

.0x

75.1

%0.

0%

Val

uatio

n B

ench

mar

ks

EV/

Rev

.EV

/ EB

ITD

AP

E

LTM

LTM

2013

E20

14E

2013

2.28

x12

.2x

11.8

x11

.0x

17.4

x

2.24

x11

.9x

11.5

x10

.8x

18.7

x

2.29

x10

.7x

11.9

x10

.9x

19.1

x

2.24

x11

.4x

11.2

x10

.5x

17.5

x

2.10

x14

.3x

11.7

x11

.2x

17.0

x

1.57

x11

.8x

10.4

x9.

4x15

.6x

2.14

x10

.4x

10.4

x10

.1x

16.6

x

2.15

x10

.5x

10.3

x9.

7x18

.2x

1.21

x12

.1x

10.7

x10

.0x

19.0

x

2.60

x15

.5x

14.6

x13

.4x

22.2

x

2.14

x12

.3x

11.9

x11

.5x

15.8

x

0.32

x2.

8x2.

7x2.

4x20

.1x

1.94

x11

.3x

10.7

x10

.1x

18.1

x

2.15

x11

.9x

11.3

x10

.7x

17.9

x

1.43

x10

.5x

9.8x

9.2x

21.2

x

1.52

x14

.0x

11.9

x10

.8x

23.1

x

0.33

x5.

5x8.

5x8.

0x18

.9x

0.60

x6.

6x6.

6x5.

9x18

.7x

0.43

x6.

5xN

/AN

/AN

/A

0.43

x12

.8x

N/A

N/A

N/A

0.79

x9.

3x9.

2x8.

5x20

.5x

0.52

x8.

5x9.

1x8.

6x20

.1x

1.41

x15

.0x

14.3

x12

.0x

33.6

x

2.28

x17

.4x

14.3

x12

.5x

23.9

x

1.52

x13

.2x

12.5

x11

.1x

23.0

x

0.49

x13

.1x

11.7

x10

.0x

23.0

x

1.75

x15

.6x

13.7

x11

.4x

31.7

x

4.26

x34

.4x

24.6

x20

.9x

45.9

x

2.21

x16

.3x

12.6

x10

.4x

39.1

x

1.85

x27

.0x

20.9

x16

.6x

59.9

x

0.65

x11

.2x

9.5x

7.9x

18.2

x

3.29

x21

.7x

18.4

x15

.9x

36.5

x

2.17

xN

MN

/AN

/AN

M

1.99

x18

.5x

15.2

x12

.9x

33.5

x

1.85

x16

.0x

14.0

x11

.7x

32.7

x

Net

Deb

t /N

ext 5

Yr

EPS

LTM

EPS

Gro

w

3E20

14E

EBIT

DA

Rat

e

76$4

.08

1.0x

7.3%

374.

731.

7x8.

7%

923.

222.

2x7.

3%

773.

042.

1x7.

8%

784.

093.

4x7.

6%

242.

564.

6x10

.4%

702.

852.

2x6.

4%

676.

091.

5x8.

9%

042.

21N

M11

.0%

173.

491.

8x8.

9%

531.

665.

8x10

.6%

642.

011.

1x4.

0%

053.

342.

5x8.

2%

843.

132.

1x8.

3%

09$3

.42

2.6x

10.1

%

231.

443.

0x13

.0%

530.

702.

6x12

.0%

420.

652.

7x14

.1%

/A N

/A2.

6xN

/A

/A N

/A0.

6xN

/A

321.

552.

3x12

.3%

881.

072.

6x12

.5%

53$1

.82

NM

18.6

%

723.

152.

9x17

.4%

710.

832.

8x18

.0%

342.

720.

8x15

.0%

571.

890.

0x21

.3%

931.

110.

1x22

.5%

310.

454.

0x20

.0%

520.

680.

2x26

.5%

420.

523.

1x30

.0%

480.

510.

0x13

.0%

010.

1513

.8x

35.0

%

051.

262.

8x21

.6%

710.

831.

8x20

.0%

ics

LTM

EBIT

DA

EBIT

DA

LTM

2013

EM

argi

n20

13

$18,

916

$19,

529

18.8

%$3

.

12,4

1812

,899

18.8

%4.

3,94

53,

518

21.5

%2.

3,47

73,

554

19.6

%2.

2,18

22,

654

14.7

%3.

2,05

42,

343

13.3

%2.

1,72

01,

722

20.5

%2.

1,21

21,

231

20.5

%5.

843

954

10.0

%2.

678

723

16.7

%3.

430

447

17.4

%1.

478

497

11.7

%1.

4,02

94,

172

16.9

%3.

1,88

72,

032

18.1

%2.

$299

$320

13.6

%$3

.

179

210

10.9

%1.

683

446

6.0%

0.

196

196

9.0%

0.

85N

/A6.

7% N

6N

/A3.

3% N

241

293

8.2%

1.

187

265

7.9%

0.

$1,2

12$1

,268

9.4%

$1.

212

258

13.1

%2.

270

285

11.5

%0.

216

241

3.7%

2.

154

175

11.2

%1.

2129

12.4

%0.

5875

13.5

%0.

2633

6.8%

0.

6476

5.7%

0.

1315

15.1

%0.

0N

/A1.

4%0.

204

246

9.4%

1.

6412

511

.2%

0.

Ope

ratin

g M

etri

arke

tEn

terp

rise

LT

M

Cap

.V

alue

Rev

enue

08,7

96$2

30,1

75$1

00,8

41

26,4

8114

7,95

865

,994

33,2

1342

,019

18,3

81

31,1

0139

,752

17,7

74

23,6

2231

,187

14,8

58

14,6

5424

,263

15,4

91

14,0

2617

,890

8,37

6

10,9

3212

,693

5,89

8

10,2

1810

,213

8,44

7

9,28

710

,539

4,06

0

2,83

25,

305

2,47

5

786

1,31

94,

077

40,4

9647

,776

22,2

23

14,3

4021

,076

11,6

53

$2,3

75$3

,140

$2,1

98

1,96

52,

498

1,64

4

1,87

13,

771

11,4

71

744

1,29

32,

170

330

555

1,27

7

7983

194

1,22

71,

890

3,15

9

1,30

71,

895

1,90

7

19,0

94$1

8,13

2$1

2,85

2

3,07

23,

694

1,62

2

2,81

23,

561

2,34

6

2,66

32,

825

5,76

6

2,40

12,

405

1,37

1

721

724

170

717

953

432

694

699

379

502

720

1,11

5

284

284

86

6369

32

3,00

23,

097

2,37

9

721

953

1,11

5

% o

f

% C

hang

e52

Wee

kM

a

0 D

ayY

TD

Hig

hC

-1.0

%0.

6%88

.5%

$20

1.3%

19.5

%96

.5%

12

1.3%

22.9

%96

.6%

3

3.1%

20.1

%95

.2%

3

3.5%

15.0

%96

.1%

2

3.7%

18.4

%96

.2%

1

4.6%

28.4

%91

.7%

1

2.2%

19.6

%98

.1%

1

-3.1

%23

.6%

89.4

%1

1.9%

10.8

%93

.5%

-1.7

%N

/A91

.2%

-4.5

%17

.6%

88.7

%

0.9%

17.8

%93

.5%

4

1.6%

19.5

%94

.4%

1

0.1%

25.7

%97

.1%

$

9.6%

17.8

%99

.3%

-4.5

%-3

9.3%

47.6

%

-5.0

%-3

.1%

71.8

%

-4.0

%0.

9%85

.1%

0.0%

14.3

%99

.0%

-0.6

%2.

7%83

.3%

-2.0

%7.

6%91

.1%

-0.7

%12

.9%

96.0

%$ 1

-2.4

%19

.9%

88.2

%

-6.8

%4.

6%83

.0%

2.0%

0.7%

88.1

%

0.4%

N/A

75.7

%

9.8%

27.8

%87

.5%

14.9

%N

/A86

.1%

9.3%

62.4

%90

.3%

-3.7

%34

.4%

93.6

%

-0.9

%98

.6%

94.5

%

4.2%

-12.

0%56

.7%

2.4%

27.7

%85

.4%

0.4%

19.9

%88

.1%

Mar

ket S

tatis

tics

Sto

ck

Pri

ce30

$65.

46

81.7

9

c.55

.87

48.5

3

64.2

3

34.9

3

pany

44.7

9

ompa

ny10

3.15

atio

n38

.58

any

70.3

6

24.1

5

pany

33.0

8

Mea

n

Med

ian

$65.

54

28.4

1

y10

.02

7.80

30.6

8

4.95

Mea

n

Med

ian

HY

LIVI

NG

Inc.

$51.

48

oup,

Inc.

65.0

1

s C

ompa

ny16

.25

Inc.

53.9

9

.49

.72

42.7

4

12.0

5

tam

in C

otta

ge, I

nc.

31.0

0

7.57

17.3

6

5.00

Mea

n

Med

ian

As

of J

une

30, 2

013

($ in

milli

ons,

exc

ept p

er s

hare

dat

a)

Tic

ker

Com

pany

BR

AND

ED P

ACK

AGED

FO

OD

SN

ES

NN

estlé

S.A

.

PE

PP

epsi

co, I

nc.

KR

FTK

raft

Food

s G

roup

, In c

GIS

Gen

eral

Mills

, Inc

.

KK

ello

gg C

ompa

ny

CA

GC

onA

gra

Food

s, In

c.

CP

BC

ampb