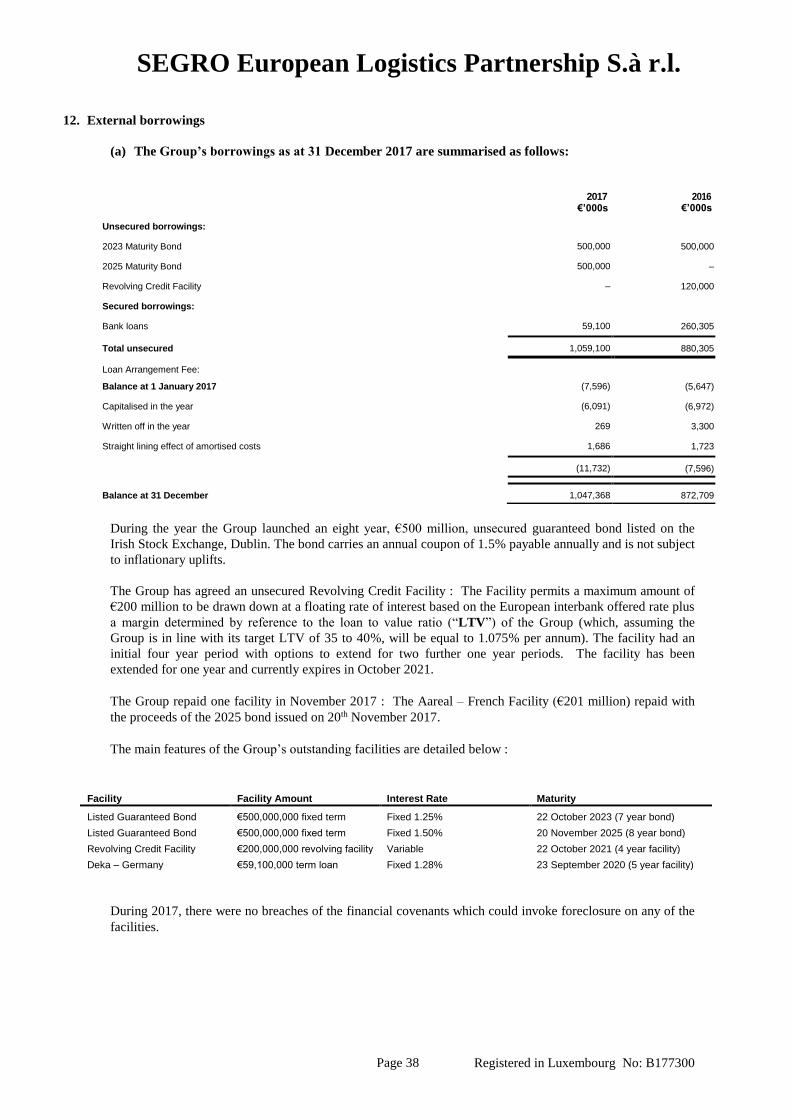

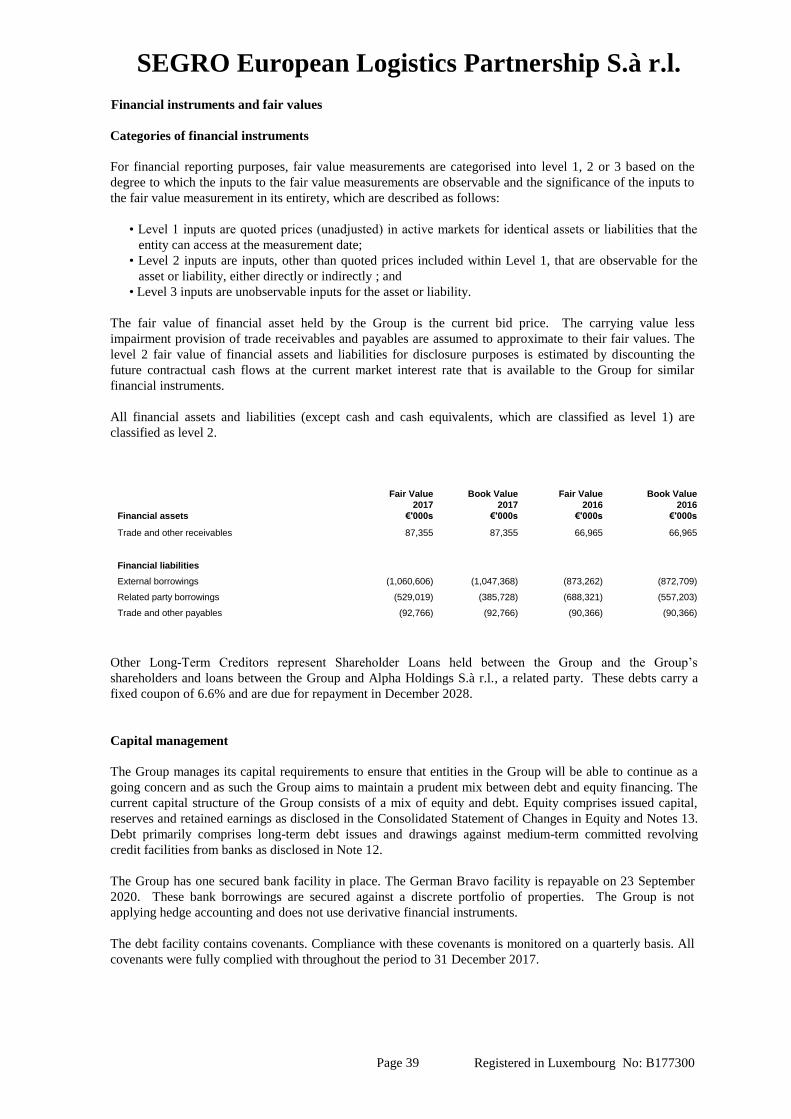

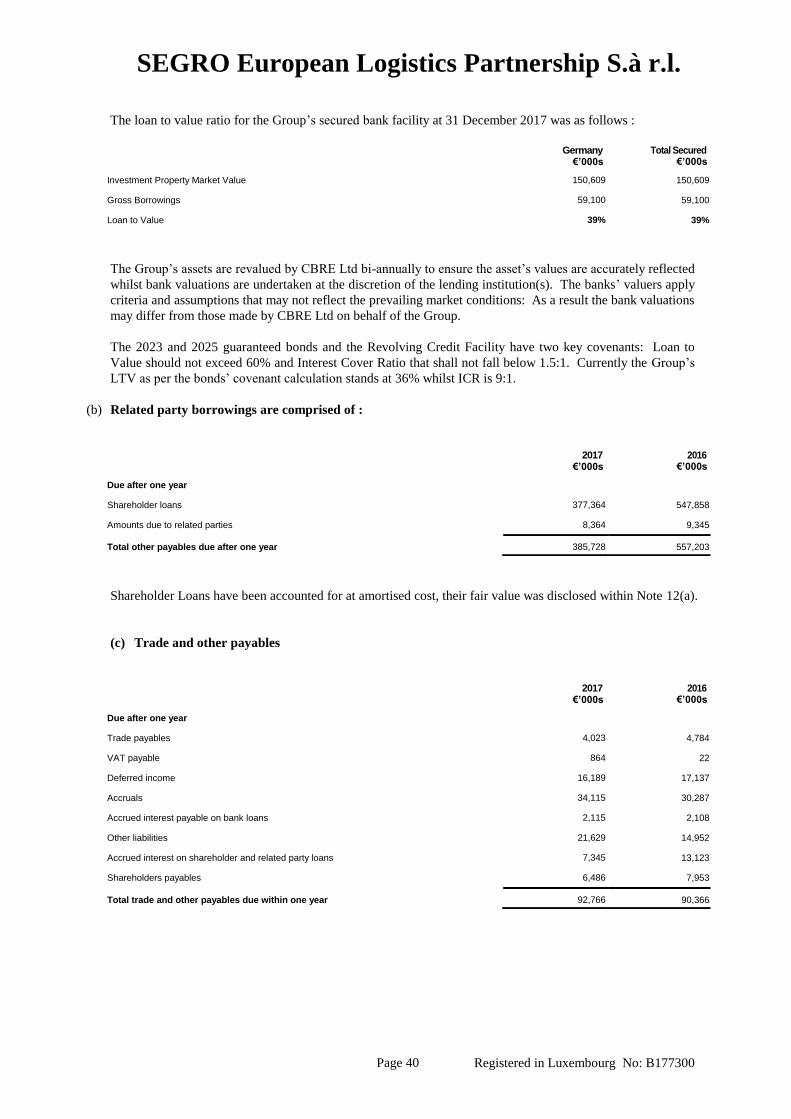

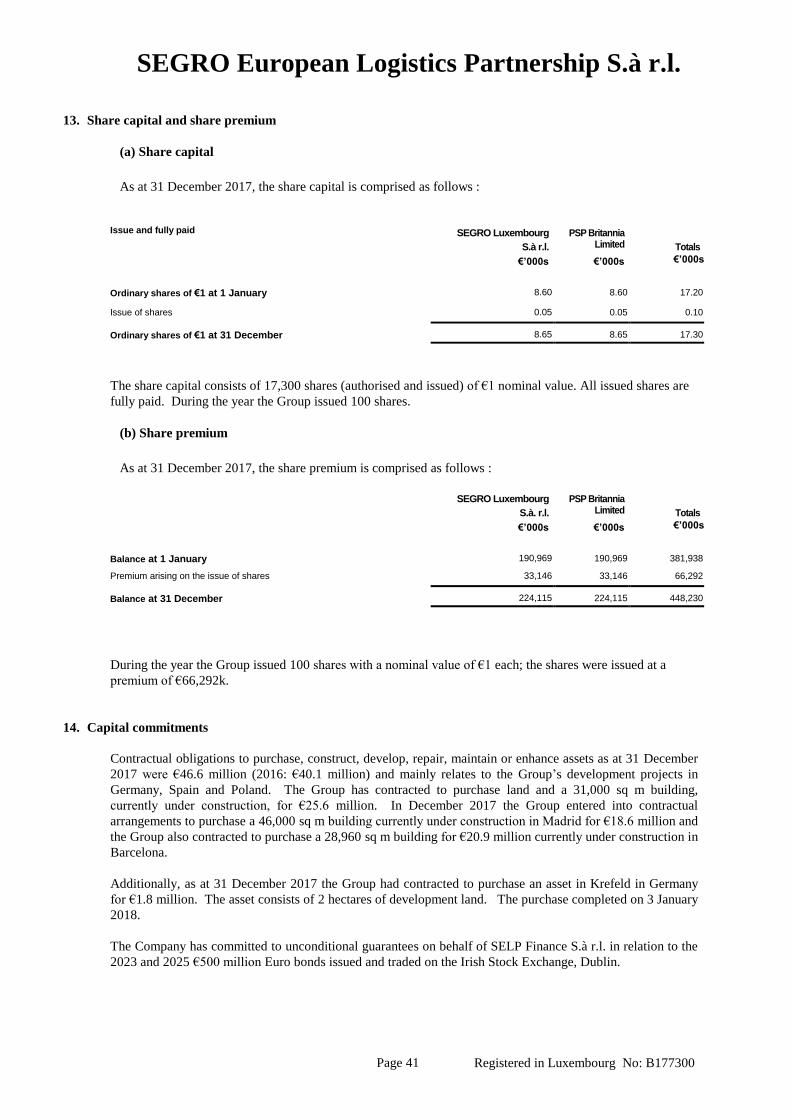

SEGRO European Logistics Partnership S.à...

49

Transcript of SEGRO European Logistics Partnership S.à...

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 1

SEGRO European Logistics Partnership

Société à responsabilité limitée

Registered in Luxembourg No: B177300 Subscribed Share Capital: EUR 17,300

CONSOLIDATED FINANCIAL STATEMENTS AND REPORT OF THE

RÉVISEUR D´ENTREPRISES AGRÉÉ

AS AT AND FOR THE YEAR ENDED

31 DECEMBER 2017

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 2

CONTENTS

Shareholders, advisers and other information

3

Managers’ report

4

Corporate governance statement 9

Managers’ responsibilities statement

12

Report of the reviseur d’entreprises agrée

13

Consolidated income statement

Consolidated statement of comprehensive income

17

18

Consolidated statement of financial position

19

Consolidated statement of changes in equity

20

Consolidated statement of cash flows

21

Notes to the consolidated financial statements

22

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 3

SHAREHOLDERS, ADVISERS AND

OTHER INFORMATION

Shareholders

SEGRO Luxembourg S.à r.l.

35-37 avenue de la Liberté

L-1931 Luxembourg

LUXEMBOURG

PSP Britannia Limited

10 Bressenden Place

8th Floor

London

SW1E 5DH

United Kingdom

Venture Adviser

SELP Management Limited

Cunard House

15 Regent Street

London SW1Y 4LR

United Kingdom

Registered place of business

35-37 avenue de la Liberté

L-1931 Luxembourg

LUXEMBOURG

Registered under number B177300

Managers

Mr. Desmond Mitchell

Mr. Neil Ross

Mr. Philip Anthony Redding

Mr. Stéphane Jalbert

Auditor

PwC Société coopérative

2, rue Gerhard Mercator

B.P. 1443

L-1014 Luxembourg

LUXEMBOURG

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 4

MANAGERS’

REPORT

The Managers have pleasure in presenting their report on the operations of the Group for the year ended 31 December 2017

(“the period”) together with the consolidated financial statements.

CONSTITUTION

SEGRO European Logistics Partnership S.à r.l. (“the Company”) was incorporated on 8 May 2013.

It owns directly or indirectly the companies shown within Note 22, the whole being the “The Group”:

The Group is owned by SEGRO plc Group (“the SEGRO Group”) through its subsidiary SEGRO Luxembourg S.à r.l.

and PSP Investment Group through its subsidiary PSP Britannia Limited.

PRINCIPAL ACTIVITIES

The principal activity of the Group is to invest in prime Logistics investment properties and development sites located

in Continental Europe. The investment portfolio comprises Logistics properties together with undeveloped sites held

for development.

MARKET OUTLOOK

European commercial property markets have continued to perform well throughout 2017 with prime yields continuing

to tighten in the Group’s key markets. Competition for well-located assets in core markets continues despite

historically low investment yields. Capital allocations towards commercial real estate remains strong with reports of

record levels of capital allocated to but not yet invested in real estate. The year has seen a number of platform deals

completed, where operational platforms as well as logistics investment portfolios have been traded and this reflects the

desire of some investors to acquire both operational skills and logistics portfolios in a market where scale is becoming

increasingly important.

Occupier demand remains strong across Europe, although rental value growth remains muted where supply is keeping

pace, and is expected to remain so into 2018. The Group’s key markets have enjoyed continued low vacancy rates

throughout 2017.

Development of new stock is becoming an increasingly important element of many logistics investors’ portfolios, with

strong demand for pre-let and build-to-suit warehouses, and a number of speculative development schemes letting up

during construction.

In this context the outlook for European logistics assets remains stable.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 5

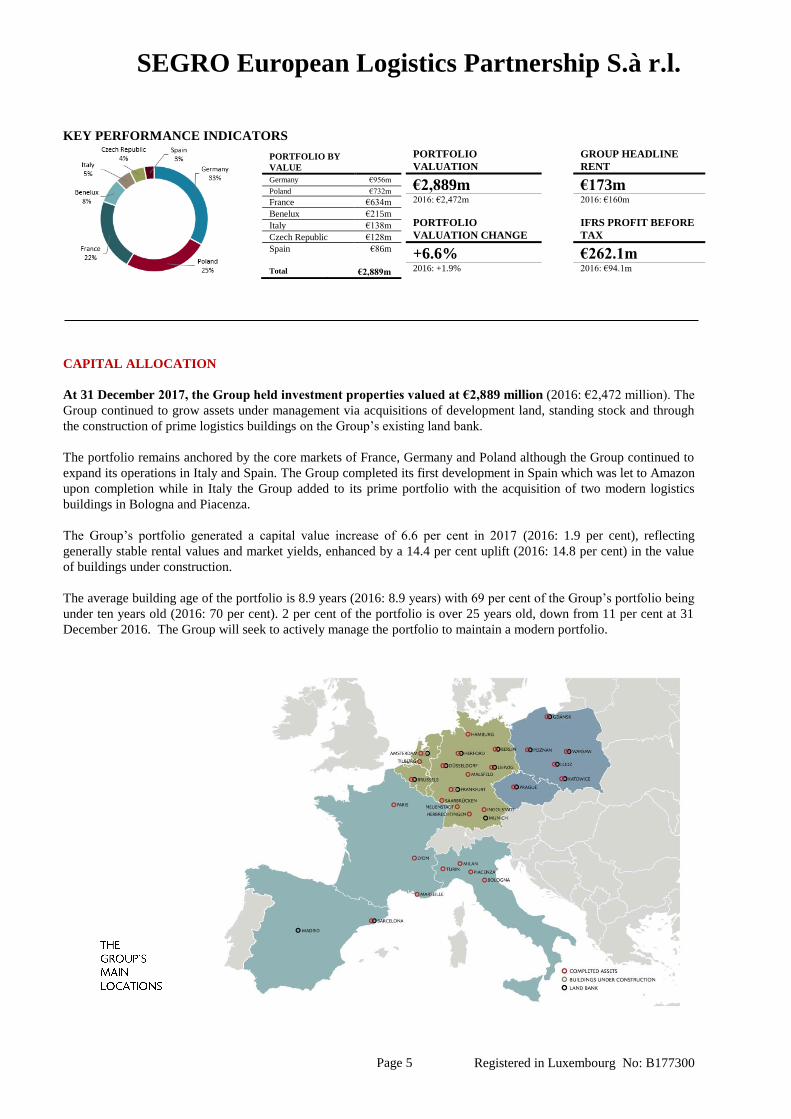

KEY PERFORMANCE INDICATORS

CAPITAL ALLOCATION

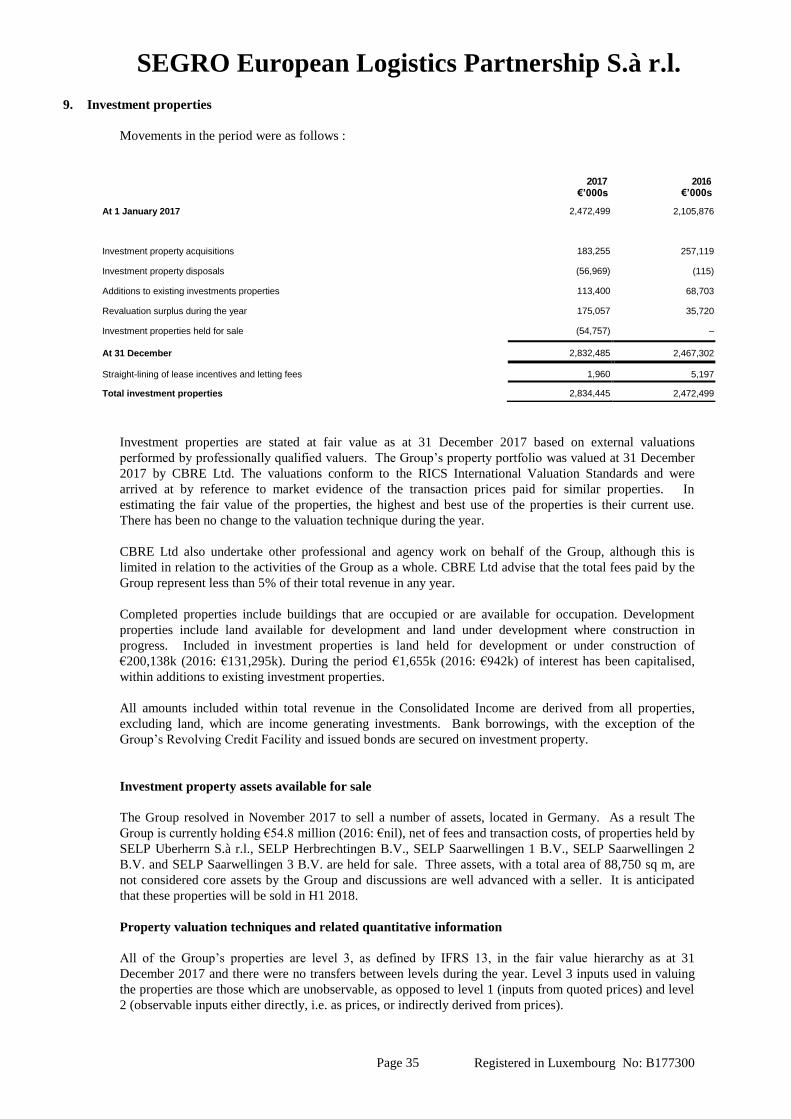

At 31 December 2017, the Group held investment properties valued at €2,889 million (2016: €2,472 million). The

Group continued to grow assets under management via acquisitions of development land, standing stock and through

the construction of prime logistics buildings on the Group’s existing land bank.

The portfolio remains anchored by the core markets of France, Germany and Poland although the Group continued to

expand its operations in Italy and Spain. The Group completed its first development in Spain which was let to Amazon

upon completion while in Italy the Group added to its prime portfolio with the acquisition of two modern logistics

buildings in Bologna and Piacenza.

The Group’s portfolio generated a capital value increase of 6.6 per cent in 2017 (2016: 1.9 per cent), reflecting

generally stable rental values and market yields, enhanced by a 14.4 per cent uplift (2016: 14.8 per cent) in the value

of buildings under construction.

The average building age of the portfolio is 8.9 years (2016: 8.9 years) with 69 per cent of the Group’s portfolio being

under ten years old (2016: 70 per cent). 2 per cent of the portfolio is over 25 years old, down from 11 per cent at 31

December 2016. The Group will seek to actively manage the portfolio to maintain a modern portfolio.

PORTFOLIO BY

VALUE

Germany €956m

Poland €732m

France €634m

Benelux €215m

Italy €138m

Czech Republic €128m

Spain €86m

Total €2,889m

PORTFOLIO

VALUATION GROUP HEADLINE

RENT

€2,889m €173m 2016: €2,472m

2016: €160m

PORTFOLIO

VALUATION CHANGE

IFRS PROFIT BEFORE

TAX

+6.6% €262.1m 2016: +1.9% 2016: €94.1m

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 6

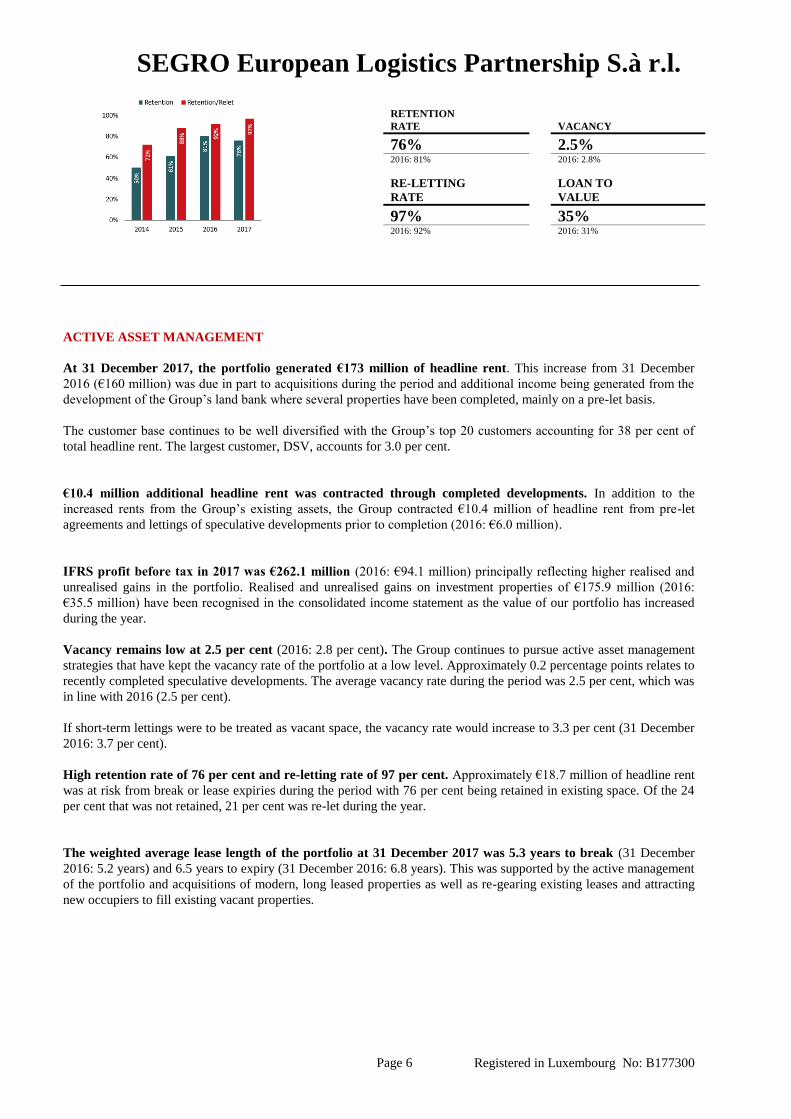

ACTIVE ASSET MANAGEMENT

At 31 December 2017, the portfolio generated €173 million of headline rent. This increase from 31 December

2016 (€160 million) was due in part to acquisitions during the period and additional income being generated from the

development of the Group’s land bank where several properties have been completed, mainly on a pre-let basis.

The customer base continues to be well diversified with the Group’s top 20 customers accounting for 38 per cent of

total headline rent. The largest customer, DSV, accounts for 3.0 per cent.

€10.4 million additional headline rent was contracted through completed developments. In addition to the

increased rents from the Group’s existing assets, the Group contracted €10.4 million of headline rent from pre-let

agreements and lettings of speculative developments prior to completion (2016: €6.0 million).

IFRS profit before tax in 2017 was €262.1 million (2016: €94.1 million) principally reflecting higher realised and

unrealised gains in the portfolio. Realised and unrealised gains on investment properties of €175.9 million (2016:

€35.5 million) have been recognised in the consolidated income statement as the value of our portfolio has increased

during the year.

Vacancy remains low at 2.5 per cent (2016: 2.8 per cent). The Group continues to pursue active asset management

strategies that have kept the vacancy rate of the portfolio at a low level. Approximately 0.2 percentage points relates to

recently completed speculative developments. The average vacancy rate during the period was 2.5 per cent, which was

in line with 2016 (2.5 per cent).

If short-term lettings were to be treated as vacant space, the vacancy rate would increase to 3.3 per cent (31 December

2016: 3.7 per cent).

High retention rate of 76 per cent and re-letting rate of 97 per cent. Approximately €18.7 million of headline rent

was at risk from break or lease expiries during the period with 76 per cent being retained in existing space. Of the 24

per cent that was not retained, 21 per cent was re-let during the year.

The weighted average lease length of the portfolio at 31 December 2017 was 5.3 years to break (31 December

2016: 5.2 years) and 6.5 years to expiry (31 December 2016: 6.8 years). This was supported by the active management

of the portfolio and acquisitions of modern, long leased properties as well as re-gearing existing leases and attracting

new occupiers to fill existing vacant properties.

RETENTION

RATE

VACANCY

76% 2.5% 2016: 81%

2016: 2.8%

RE-LETTING

RATE

LOAN TO

VALUE

97% 35% 2016: 92% 2016: 31%

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 7

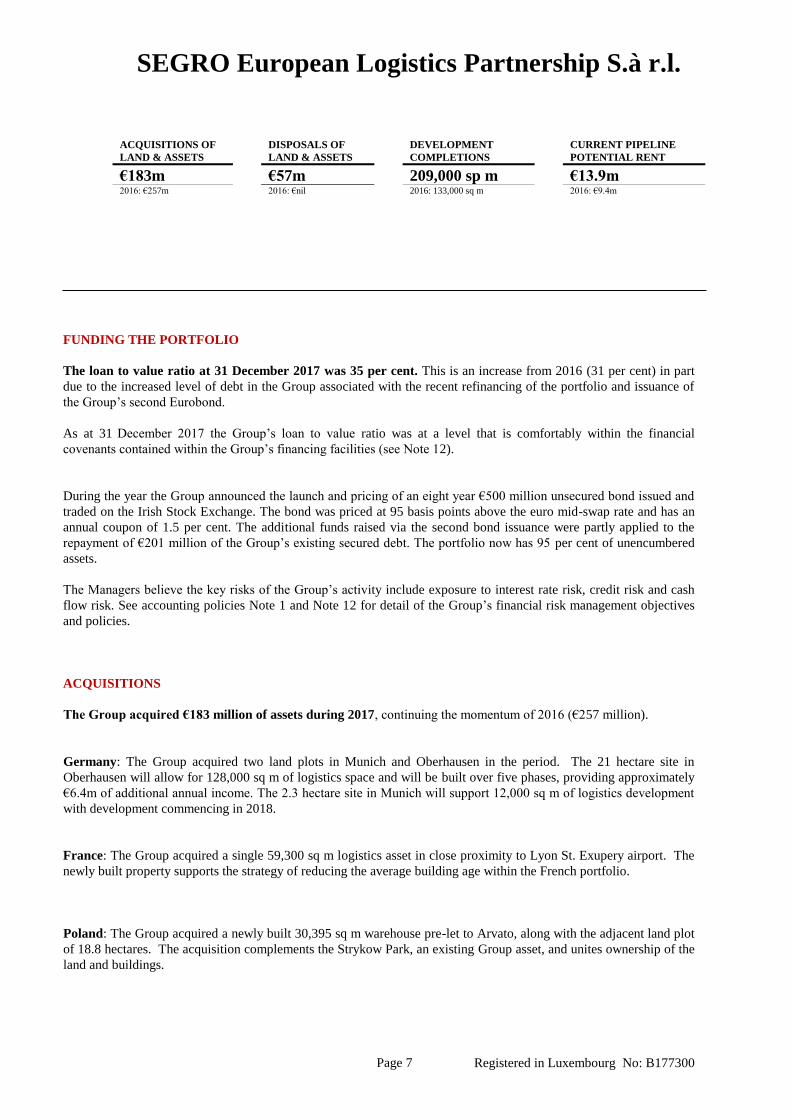

FUNDING THE PORTFOLIO

The loan to value ratio at 31 December 2017 was 35 per cent. This is an increase from 2016 (31 per cent) in part

due to the increased level of debt in the Group associated with the recent refinancing of the portfolio and issuance of

the Group’s second Eurobond.

As at 31 December 2017 the Group’s loan to value ratio was at a level that is comfortably within the financial

covenants contained within the Group’s financing facilities (see Note 12).

During the year the Group announced the launch and pricing of an eight year €500 million unsecured bond issued and

traded on the Irish Stock Exchange. The bond was priced at 95 basis points above the euro mid-swap rate and has an

annual coupon of 1.5 per cent. The additional funds raised via the second bond issuance were partly applied to the

repayment of €201 million of the Group’s existing secured debt. The portfolio now has 95 per cent of unencumbered

assets.

The Managers believe the key risks of the Group’s activity include exposure to interest rate risk, credit risk and cash

flow risk. See accounting policies Note 1 and Note 12 for detail of the Group’s financial risk management objectives

and policies.

ACQUISITIONS

The Group acquired €183 million of assets during 2017, continuing the momentum of 2016 (€257 million).

Germany: The Group acquired two land plots in Munich and Oberhausen in the period. The 21 hectare site in

Oberhausen will allow for 128,000 sq m of logistics space and will be built over five phases, providing approximately

€6.4m of additional annual income. The 2.3 hectare site in Munich will support 12,000 sq m of logistics development

with development commencing in 2018.

France: The Group acquired a single 59,300 sq m logistics asset in close proximity to Lyon St. Exupery airport. The

newly built property supports the strategy of reducing the average building age within the French portfolio.

Poland: The Group acquired a newly built 30,395 sq m warehouse pre-let to Arvato, along with the adjacent land plot

of 18.8 hectares. The acquisition complements the Strykow Park, an existing Group asset, and unites ownership of the

land and buildings.

ACQUISITIONS OF

LAND & ASSETS

DISPOSALS OF

LAND & ASSETS

DEVELOPMENT

COMPLETIONS CURRENT PIPELINE

POTENTIAL RENT

€183m €57m 209,000 sp m €13.9m 2016: €257m

2016: €nil

2016: 133,000 sq m

2016: €9.4m

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 8

ACQUISITIONS (CONTINUED)

Czech Republic: Two small buildings along with an adjacent 29.5 hectares of development land were acquired in

Hostiwice. The acquisition unites ownership of the Hostiwice Park and the acquired land will support 99,000 sq m of

future logistics buildings.

Netherlands: The Group acquired a 1.7 hectare land plot adjacent to the LC1 development site during the period. The

site benefits from the pre-performed infrastructure works, and will support construction of an 11,296 sq m logistics

terrace building.

Spain: The Group acquired four plots of land in Gavilanes, Sant Esteve, San Fernando de Henares and Martorelles.

These locations strengthen the Group’s positions in Barcelona. Two of the sites are already under construction and are

expected to complete in 2018, with all four sites expected to add 147,000 sq m of modern logistics buildings.

Italy: In April 2017 the Group acquired two buildings in Bologna and Piacenza. Both buildings are newly completed

logistics warehouses let on long leases and provide a total of 32,400 sq m of logistics space.

DISPOSALS

Four older, short-let assets were sold in France during 2017. The proceeds will be used to support the Group’s

investment activities in both acquisitions and development.

The Group has agreed terms to dispose a further three assets in Germany in 2018.

DEVELOPMENT ACTIVITY: COMPLETED, CURRENT AND FUTURE

The Group completed 209,000 sq m of new space during 2017, 57 per cent more than in 2016 (133,000 sq m).

These projects were 75 per cent pre-let prior to the start of construction and 96 per cent let as at the end of December

2017, generating €10.4 million of headline rent, with a potential further €0.4 million once the remaining space is let.

As at 31 December 2017, the Group had a current development pipeline of 250,000 sq m that will generate €13.9

million of headline rent. These projects were 44 per cent pre-let as at 31 December 2017.

The portfolio holds a land bank of 240 hectares identified for future development as at 31 December 2017,

equating to €166 million, or around 6 per cent of the Group’s portfolio. The Group invested €98 million in acquiring

new land during the year associated with developments expected to start in the near term.

The Group plans to grow the portfolio size in the next years, both through acquisition of standing assets and through

development of existing and newly acquired development land.

Mitry Mory, France, development provides 57,000 sq m of space 30,395 sq m asset acquired in Poland pre-let to Arvato

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 9

CORPORATE GOVERNANCE

STATEMENT

Governance is an important element of the Group’s culture and affects its decisions and actions, being central to all

areas of the business and designed to create an environment where matters can be considered and decisions made at the

appropriate level in the organisation.

The Luxembourg Corporate Governance Code 2009 is the standard against which the Company measures its

compliance with governance and a link to it can be found at:

https://www.luxembourgforfinance.com/sites/luxembourgforfinance/files/code-bourse-eng.pdf

The Company is governed by its articles of association and the private Shareholders’ Agreement made between (1)

PSP Britannia Limited, (2) SEGRO Luxembourg S.à r.l., (3) the Company, (4) SELP Investments S.à r.l., and (5)

SELP Finance S.à r.l..

THE BOARD

The Board is responsible for creating and delivering sustainable shareholder value. Each Manager acts in a way he

believes, best promotes the long-term success of the Group for the benefit of Shareholders, stakeholders and the wider

community.

Composition

The Company has four Managers who have the power to represent the Company, details of which are set out on page 3.

Each Shareholder is responsible for the appointment of two Managers in accordance with the Shareholders’

Agreement, and each Manager has agreed contractual terms with the appropriate Shareholder appointing him. The

Managers were appointed at a general meeting of the Shareholders for an unlimited period of time, although the

Shareholder appointing them can remove the relevant manager at any time in accordance with the provisions of the

Shareholders’ Agreement. The Managers are remunerated by the appointing Shareholder.

Although the Company does not have a Diversity Policy, the Shareholders did not discriminate on the grounds of

gender or age (or any other factor) when selecting the Managers. Each Manager was appointed because of his

qualification, experience and suitability as a Manager and because he was the best person for the role.

There have been no changes in the Management Board during the year and the respective members of the Board have

experience in the real estate industry as well as experience as Managers within similar enterprises.

Board Committees

The Managers meet regularly at the Group’s registered address in order to consider matters that are of significance to

the Company, to allow it to achieve the objectives of the Company and the Group. The objectives of the Company and

Group are detailed on page 26.

The Board of Managers has decided not to delegate any of its responsibilities to Board committees and therefore does

not have an audit, investment or risk management committee. Instead, the Board meets most months, to attend to all

relevant affairs of the Company, including those related to investment (acting on the advice of the Group’s appointed

investment adviser), risk management and ensuring the robustness of internal controls and the soundness for the

process for preparing the Group’s audited financial statements. The Board is satisfied that it has the relevant

knowledge, experience and time to retain control over all of these matters and makes use of the available resource and

experience of SELP Management Limited to allow it to effectively discharge its duties. With regards to the

preparation of the audited financial statements, the auditor attends the relevant Board meeting when the financial

statements are being considered and is also available outside of the meeting to discuss any matter with the Managers

should they so wish.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 10

PROVISION OF SERVICES AND EMPLOYEES

The Group employs a number of external service providers in relation to the management of the Group’s assets.

Principally, the Group contracts SELP Management Limited, a related party, to provide services in relation to

investment decisions, development project management, property and asset management as well as administrative

services.

The Group has also contracted three members of staff within its head office in Luxembourg. The recruitment of the

Group’s employees was carried out by SELP Management Limited as part of its role of providing administration

services to the Group. As part of this role, SELP Management also provides HR services to the employees applying its

policies on equal opportunities and human rights to ensure that the best people are attracted and retained.

INVESTMENT ADVISER TO THE GROUP

As set out on page 3, SELP Management Limited is appointed to act as investment adviser to the Group.

AUDITOR OF THE GROUP

PricewaterhouseCoopers Société cooperative was the auditor of the Group for the year ended 31 December 2017.

POLICIES AND CODES

The purpose of the Group’s key policies and procedures is to protect the integrity of the Company and the Group and

its decision making process. The Group operates policies that are ethical and the key policies are listed below:

Health and Safety

Standards of health and safety are important to the Group. As a result of SEGRO’s role as development project

manager, property manager and asset manager, the Board decided to adopt SEGRO’s health and safety policy in 2013.

This can be found at www.SEGRO.com. The policy is designed to ensure that health and safety is embedded into the

Group’s culture with risks being managed through tight controls, training and raising awareness.

Sustainability

In 2015, the Group, on the recommendation of SELP Management Limited, adopted SEGRO’s sustainability strategy,

‘SEGRO 2020’, for itself and its subsidiaries. SEGRO 2020 focuses on ensuring that building design, new buildings

and refurbishments use resources efficiently, most notably energy and water, and obtain recognised building

certifications such as BREEAM and LEED.

Related Parties

The Group enacts contracts and arrangements with related parties in line with best market practice on an arms-length

basis and discloses such arrangements in the notes to the Consolidated Financial Statements.

Conflicts of Interest

Managers and officers strive to avoid any conflict of interest between the interests of the Company and the Group on

the one hand, and personal, professional, and business interests on the other. This includes avoiding actual conflicts of

interest as well as the perception of conflicts of interest.

Conflicts of interest are monitored and recorded. Managers, employees, officers of the Group and the adviser to the

Group are required to declare Conflicts of Interest.

Code of Ethics including the Policy on Anti Bribery and Corruption

The Company seeks to maintain high ethical standards in its business activities. The Group is committed to conducting

business in accordance with applicable laws and regulations that are designed to maintain and enhance the Group’s

reputation. The Group strives to behave in a professional, honest and responsible manner and avoids any conduct

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 11

which may be considered to be corrupt or contrary to good corporate ethics. Any activity that seeks to bribe, corrupt or

otherwise improperly influence a public official or third party in any country, is strictly prohibited by the Group.

CAPITAL MANAGEMENT

The Group’s capital management policies are included within the notes to the Consolidated Financial Statements.

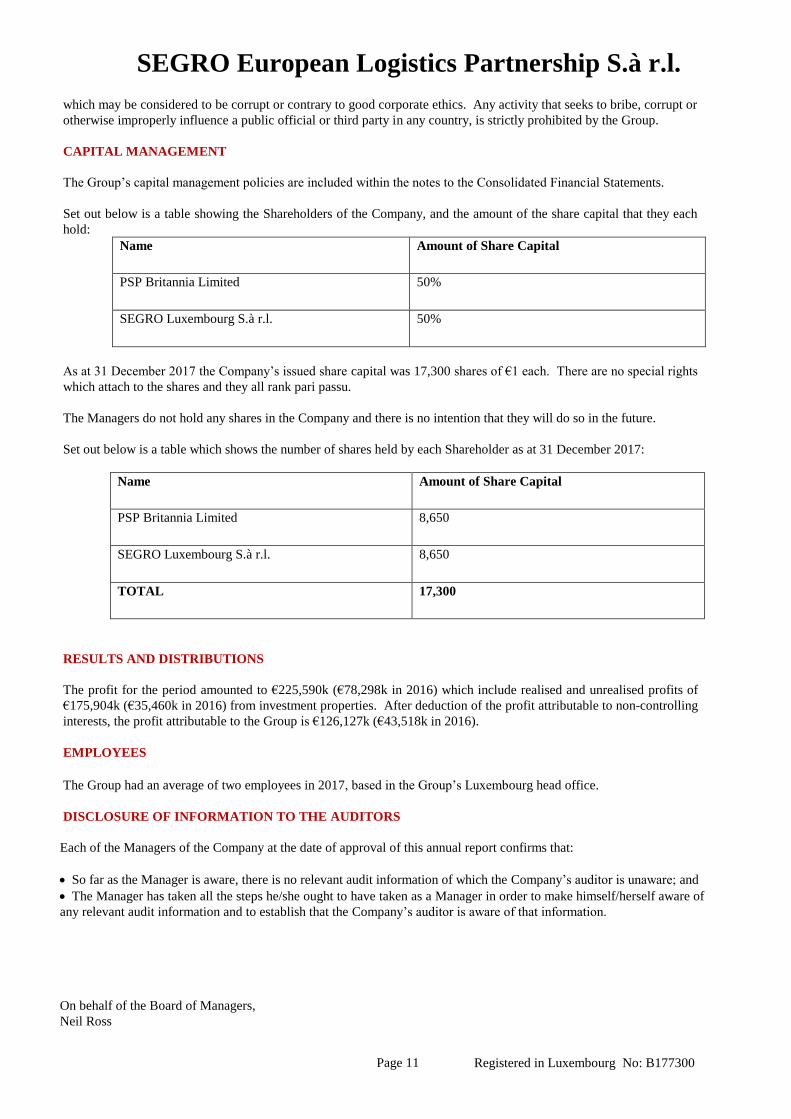

Set out below is a table showing the Shareholders of the Company, and the amount of the share capital that they each

hold:

Name Amount of Share Capital

PSP Britannia Limited 50%

SEGRO Luxembourg S.à r.l. 50%

As at 31 December 2017 the Company’s issued share capital was 17,300 shares of €1 each. There are no special rights

which attach to the shares and they all rank pari passu.

The Managers do not hold any shares in the Company and there is no intention that they will do so in the future.

Set out below is a table which shows the number of shares held by each Shareholder as at 31 December 2017:

Name Amount of Share Capital

PSP Britannia Limited 8,650

SEGRO Luxembourg S.à r.l. 8,650

TOTAL 17,300

RESULTS AND DISTRIBUTIONS

The profit for the period amounted to €225,590k (€78,298k in 2016) which include realised and unrealised profits of

€175,904k (€35,460k in 2016) from investment properties. After deduction of the profit attributable to non-controlling

interests, the profit attributable to the Group is €126,127k (€43,518k in 2016).

EMPLOYEES

The Group had an average of two employees in 2017, based in the Group’s Luxembourg head office.

DISCLOSURE OF INFORMATION TO THE AUDITORS

Each of the Managers of the Company at the date of approval of this annual report confirms that:

So far as the Manager is aware, there is no relevant audit information of which the Company’s auditor is unaware; and

The Manager has taken all the steps he/she ought to have taken as a Manager in order to make himself/herself aware of

any relevant audit information and to establish that the Company’s auditor is aware of that information.

On behalf of the Board of Managers,

Neil Ross

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 12

MANAGERS’ RESPONSIBILITIES

STATEMENT

The Managers are responsible for preparing the Consolidated Financial Statements in accordance with applicable law

and regulations.

Company law requires the Managers to prepare consolidated financial statements for each financial year. Under that

law the Managers have elected to prepare the Consolidated Financial Statements in accordance with International

Financial Reporting Standards (IFRS) as adopted by the European Union. Under company law the Managers must not

approve the accounts unless they are satisfied that they give a true and fair view of the state of affairs of the company

and of the profit or loss of the company for that period. In preparing these Consolidated Financial Statements, the

Managers are required to :

properly select and apply accounting policies ;

present information, including accounting policies, in the manner that provides relevant, reliable, comparable

and understandable information ;

provide additional disclosures when compliance with the specific requirements in IFRS are insufficient to

enable users to understand the impact of particular transactions, other events and conditions on the entity’s

financial position and financial performance ; and

make an assessment of the company’s ability to continue as a going concern.

The Managers are responsible for keeping adequate accounting records that are sufficient to show and explain the

company’s transactions and disclose with reasonable accuracy at any time the financial position of the company. They

are also responsible for safeguarding the assets of the company and hence for taking reasonable steps for the prevention

and detection of fraud and other irregularities.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 17

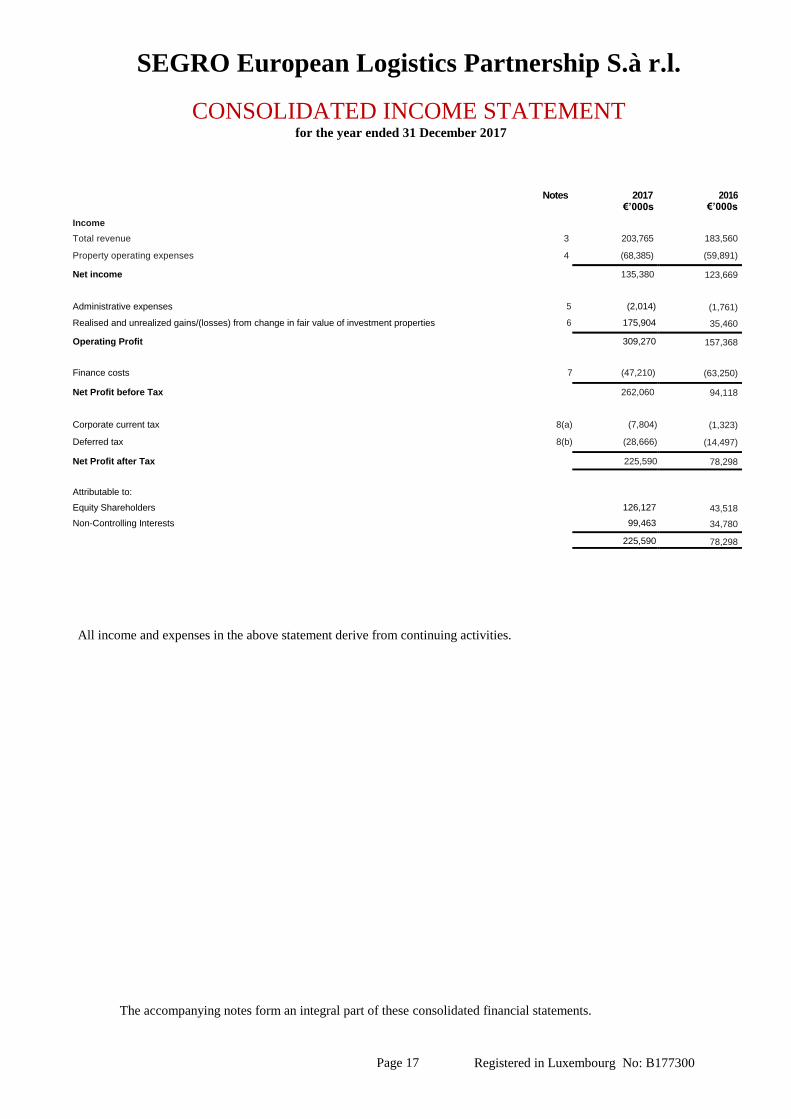

CONSOLIDATED INCOME STATEMENT for the year ended 31 December 2017

Notes 2017 €’000s

2016 €’000s

Income

Total revenue 3 203,765 183,560

Property operating expenses 4 (68,385) (59,891)

Net income 135,380 123,669

Administrative expenses 5 (2,014) (1,761)

Realised and unrealized gains/(losses) from change in fair value of investment properties 6 175,904 35,460

Operating Profit 309,270 157,368

Finance costs 7 (47,210) (63,250)

Net Profit before Tax 262,060 94,118

Corporate current tax 8(a) (7,804) (1,323)

Deferred tax 8(b) (28,666) (14,497)

Net Profit after Tax 225,590 78,298

Attributable to:

Equity Shareholders 126,127 43,518

Non-Controlling Interests 99,463 34,780

225,590 78,298

All income and expenses in the above statement derive from continuing activities.

The accompanying notes form an integral part of these consolidated financial statements.

SEGRO European Logistics Partnership S.à r.l.

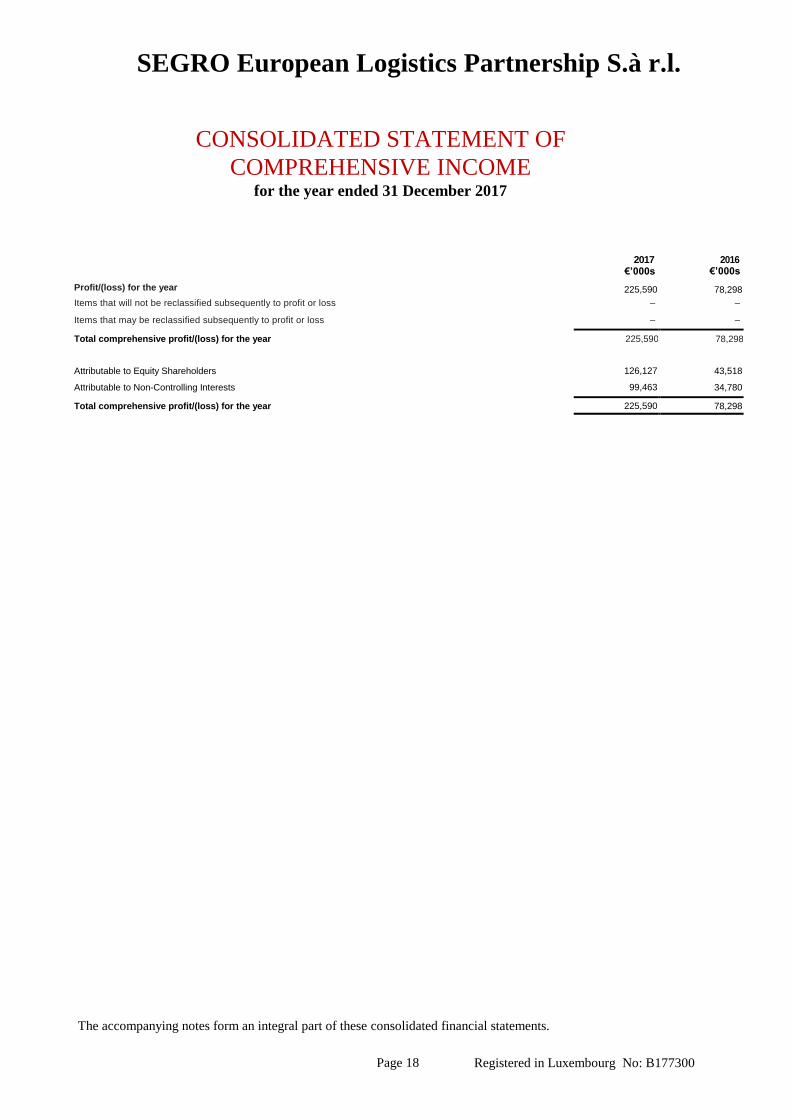

Registered in Luxembourg No: B177300 Page 18

CONSOLIDATED STATEMENT OF

COMPREHENSIVE INCOME for the year ended 31 December 2017

The accompanying notes form an integral part of these consolidated financial statements.

2017 €’000s

2016 €’000s

Profit/(loss) for the year

225,590 78,298

Items that will not be reclassified subsequently to profit or loss – –

Items that may be reclassified subsequently to profit or loss – –

Total comprehensive profit/(loss) for the year 225,590 78,298

Attributable to Equity Shareholders 126,127 43,518

Attributable to Non-Controlling Interests 99,463 34,780

Total comprehensive profit/(loss) for the year 225,590 78,298

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 19

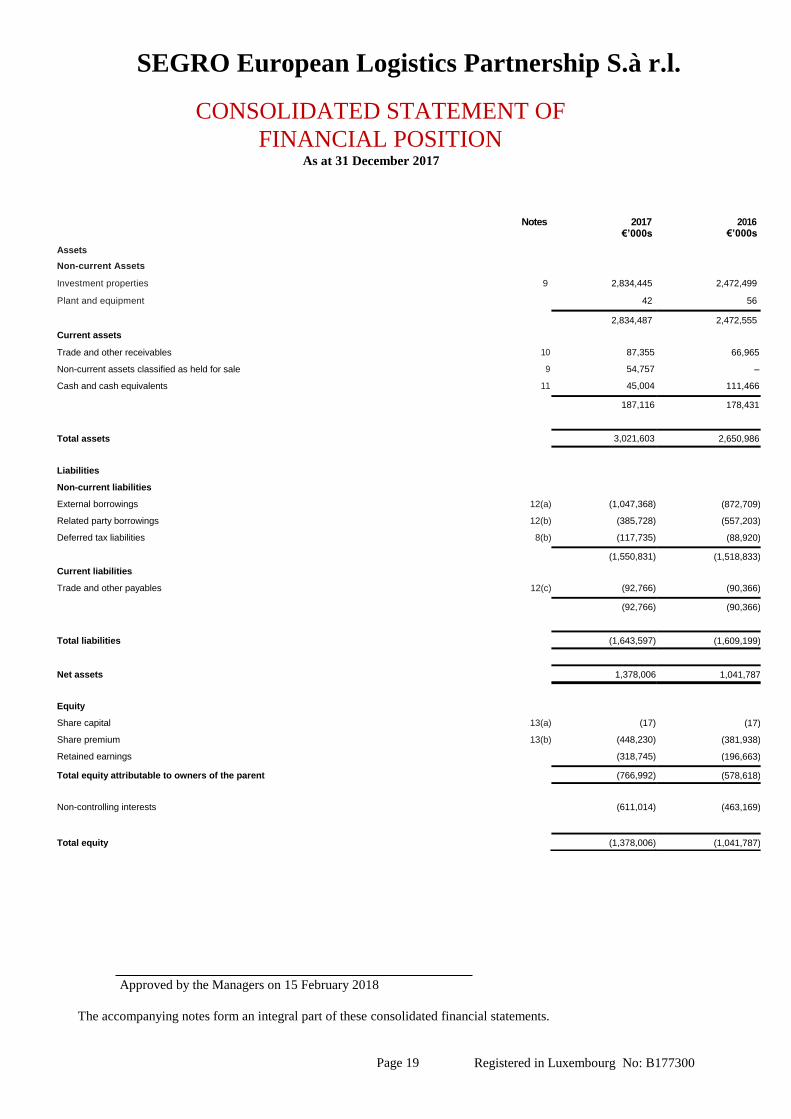

CONSOLIDATED STATEMENT OF

FINANCIAL POSITION As at 31 December 2017

Approved by the Managers on 15 February 2018

The accompanying notes form an integral part of these consolidated financial statements.

Notes 2017 €’000s

2016 €’000s

Assets

Non-current Assets

Investment properties 9 2,834,445 2,472,499

Plant and equipment 42 56

2,834,487 2,472,555

Current assets

Trade and other receivables 10 87,355 66,965

Non-current assets classified as held for sale 9 54,757 –

Cash and cash equivalents 11 45,004 111,466

187,116 178,431

Total assets 3,021,603 2,650,986

Liabilities

Non-current liabilities

External borrowings 12(a) (1,047,368) (872,709)

Related party borrowings 12(b) (385,728) (557,203)

Deferred tax liabilities 8(b) (117,735) (88,920)

(1,550,831) (1,518,833)

Current liabilities

Trade and other payables 12(c) (92,766) (90,366)

(92,766) (90,366)

Total liabilities (1,643,597) (1,609,199)

Net assets 1,378,006 1,041,787

Equity

Share capital 13(a) (17) (17)

Share premium 13(b) (448,230) (381,938)

Retained earnings (318,745) (196,663)

Total equity attributable to owners of the parent (766,992) (578,618)

Non-controlling interests (611,014) (463,169)

Total equity (1,378,006) (1,041,787)

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 20

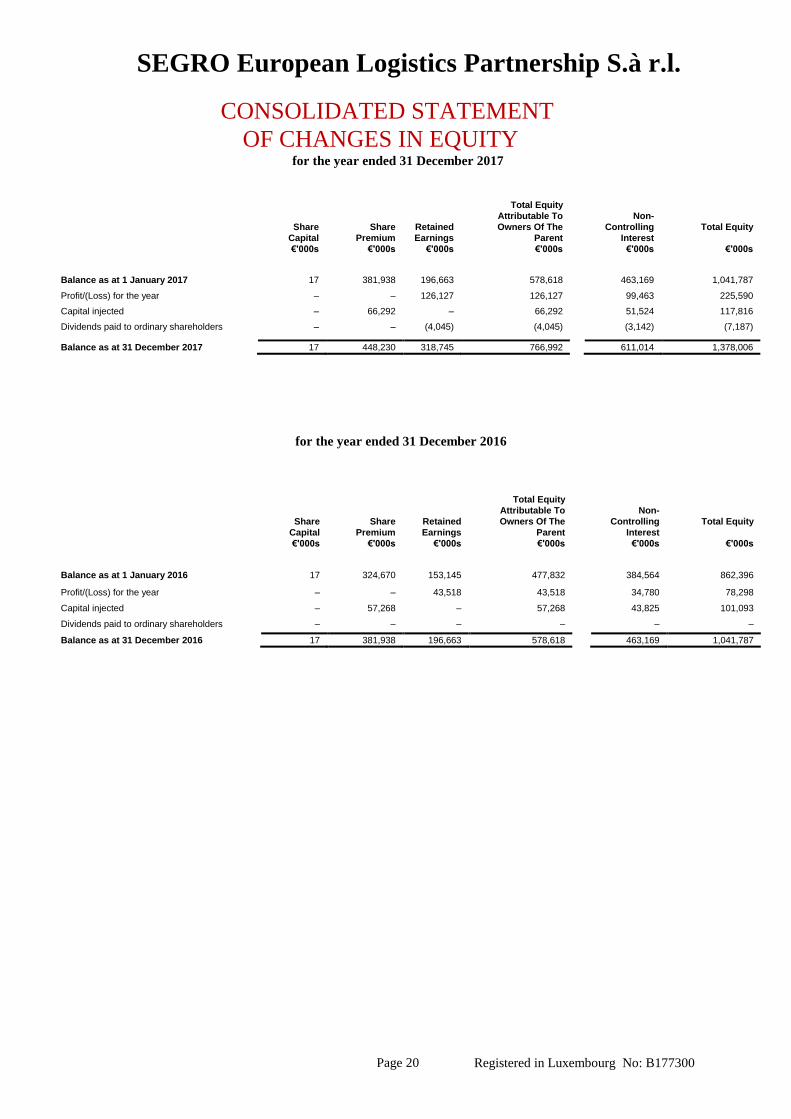

CONSOLIDATED STATEMENT

OF CHANGES IN EQUITY for the year ended 31 December 2017

Share

Capital

Share

Premium

Retained

Earnings

Total Equity

Attributable To

Owners Of The

Parent

Non-

Controlling

Interest

Total Equity

€'000s €'000s €'000s €'000s €'000s €'000s

Balance as at 1 January 2017 17 381,938 196,663 578,618 463,169 1,041,787

Profit/(Loss) for the year – – 126,127 126,127 99,463 225,590

Capital injected – 66,292 – 66,292 51,524 117,816

Dividends paid to ordinary shareholders – – (4,045) (4,045) (3,142) (7,187)

Balance as at 31 December 2017 17 448,230 318,745 766,992 611,014 1,378,006

for the year ended 31 December 2016

Share

Capital

Share

Premium

Retained

Earnings

Total Equity

Attributable To

Owners Of The

Parent

Non-

Controlling

Interest

Total Equity

€'000s €'000s €'000s €'000s €'000s €'000s

Balance as at 1 January 2016 17 324,670 153,145 477,832 384,564 862,396

Profit/(Loss) for the year – – 43,518 43,518 34,780 78,298

Capital injected – 57,268 – 57,268 43,825 101,093

Dividends paid to ordinary shareholders – – – – – –

Balance as at 31 December 2016 17 381,938 196,663 578,618 463,169 1,041,787

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 21

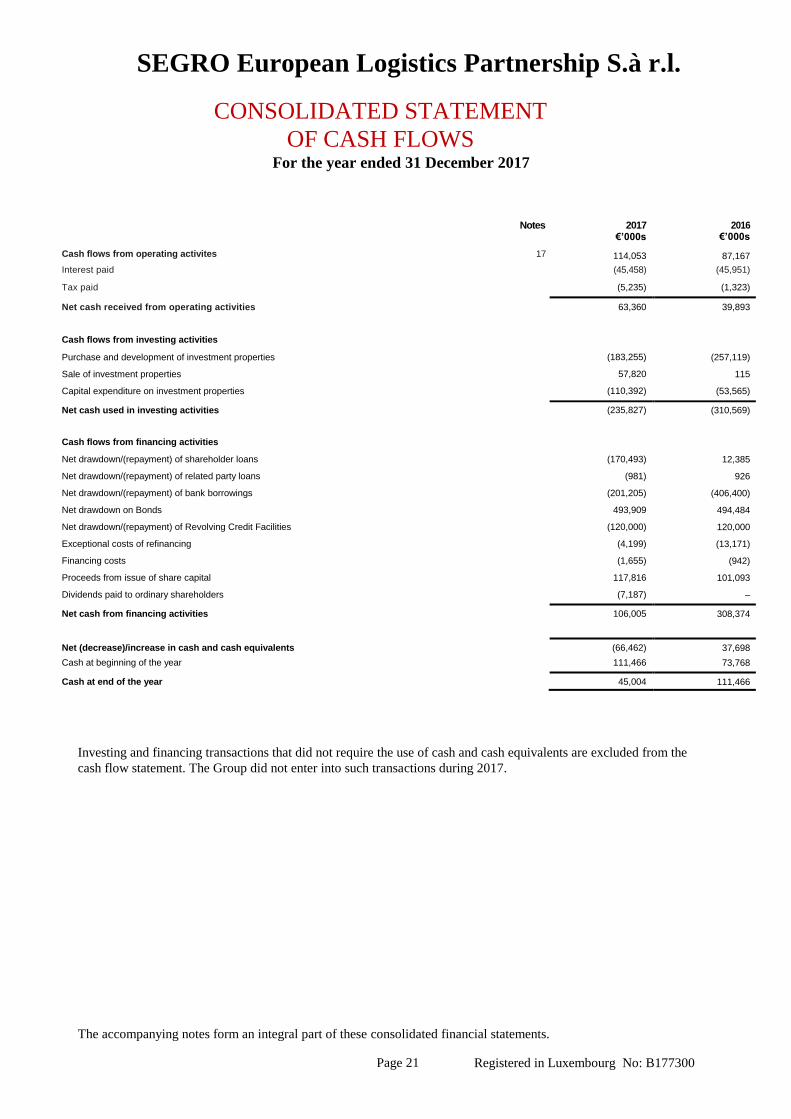

CONSOLIDATED STATEMENT

OF CASH FLOWS

For the year ended 31 December 2017

Investing and financing transactions that did not require the use of cash and cash equivalents are excluded from the

cash flow statement. The Group did not enter into such transactions during 2017.

The accompanying notes form an integral part of these consolidated financial statements.

Notes 2017 €’000s

2016 €’000s

Cash flows from operating activites

17 114,053 87,167

Interest paid (45,458) (45,951)

Tax paid (5,235) (1,323)

Net cash received from operating activities 63,360 39,893

Cash flows from investing activities

Purchase and development of investment properties (183,255) (257,119)

Sale of investment properties 57,820 115

Capital expenditure on investment properties (110,392) (53,565)

Net cash used in investing activities (235,827) (310,569)

Cash flows from financing activities

Net drawdown/(repayment) of shareholder loans (170,493) 12,385

Net drawdown/(repayment) of related party loans (981) 926

Net drawdown/(repayment) of bank borrowings (201,205) (406,400)

Net drawdown on Bonds 493,909 494,484

Net drawdown/(repayment) of Revolving Credit Facilities (120,000) 120,000

Exceptional costs of refinancing (4,199) (13,171)

Financing costs (1,655) (942)

Proceeds from issue of share capital 117,816 101,093

Dividends paid to ordinary shareholders (7,187) –

Net cash from financing activities 106,005 308,374

Net (decrease)/increase in cash and cash equivalents (66,462) 37,698

Cash at beginning of the year 111,466 73,768

Cash at end of the year 45,004 111,466

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 22

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

for the year ended 31 December 2017

1. General information

SEGRO European Logistics Partnership S.à r.l (“the Company”) was incorporated on 8 May 2013 under the

law of 10 August 1915 (as amended) as a “société à responsabilité limitée” for an unlimited duration. The

registered office of the Company is established in Luxembourg City at 35-37 av. de la Liberté, L-1931,

Luxembourg and is registered at the Trade and Companies register in Luxembourg under the number B 177

300.

The Company’s financial year begins on 1 January and ends on the 31 December of each year. The

Company and its subsidiaries (“the Group”), had an average of two employees based in the registered office

of the Company.

These Consolidated Financial Statements have been approved for issue by the Board of Managers on 15

February 2018. The shareholders have the power to amend the Consolidated Financial Statements after

issue.

The purpose of the Group is:

To act as an investment holding company and to co-ordinate the business of any corporate bodies in which

the Group is for the time being directly or indirectly interested, and to acquire (whether by original

subscription, tender, purchase, exchange or otherwise) the whole of or any part of the stock, shares,

debentures, debenture stocks, bonds and other securities issued or guaranteed by any person and any other

asset of any kind and to hold the same as investments, and to sell, exchange and dispose of the same ;

To carry on any trade or business whatsoever and to acquire, undertake and carry on the whole or any part

of the business, property and/or liabilities of any person carrying on any business;

To invest and deal with the Group's money and funds in any way the Board of Managers thinks fit and to

lend money and give credit in each case to any person with or without security;

To borrow, raise and secure the payment of money in any way the Board of Managers thinks fit, including

by the issue (to the extent permitted by Luxembourg Law) of debentures and other securities or instruments,

perpetual or otherwise, convertible or not, whether or not charged on all or any of the Group's property

(present and future) or its uncalled capital, and to purchase, redeem, convert and pay off those securities;

To acquire an interest in, amalgamate, merge, consolidate with and enter into partnership or any

arrangement for the sharing of profits, union of interests, co-operation, joint venture, reciprocal concession

or otherwise with any person, including any employees of the Group;

To enter into any guarantee or contract of indemnity or suretyship, and to provide security for the

performance of the obligations of and/or the payment of any money by any person (including any corporate

body in which the Group has a direct or indirect interest or any person (a "Holding Entity") which is for the

time being a member of or otherwise has a direct or indirect interest in the Group or anybody corporate in

which a Holding Entity has a direct or indirect interest and any person who is associated with the Group in

any business or venture, with or without the Group receiving any consideration or advantage (whether direct

or indirect), and whether by personal covenant or mortgage, charge or lien over all or part of the Group's

undertaking, property or assets (present and future) or by other means; for the purposes of this Article 3.6

"guarantee" includes any obligation, however described, to pay, satisfy, provide funds for the payment or

satisfaction of, indemnify and keep indemnified against the consequences of default in the payment of, or

otherwise be responsible for, any indebtedness or financial obligations of any other person;

To purchase, take on lease, exchange, hire and otherwise acquire any real or personal property and any right

or privilege over or in respect of it;

To sell, lease, exchange, let on hire and dispose of any real or personal property and/or the whole or any

part of the undertaking of the Group, for such consideration as the Board of Managers thinks fit, including

for shares, debentures or other securities, whether fully or partly paid up, of any person, whether or not

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 23

having objects (altogether or in part) similar to those of the Group ; to hold any shares, debentures and other

securities so acquired; to improve, manage, develop, sell, exchange, lease, mortgage, dispose of, grant

options over, turn to account and otherwise deal with all or any part of the property and rights of the

Company;

To do all or any of the activities provided above (a) in any part of the world; (b) as principal, agent,

contractor, trustee or otherwise; (c) by or through trustees, agents, sub-contractors or otherwise; and (d)

alone or with another person or persons; and

to do all activities (including entering into, performing and delivering contracts, deeds, agreements and

arrangements with or in favour of any person) that are in the opinion of the Board of Managers incidental or

conducive to the attainment of all or any of the Group's objects, or the exercise of all or any of its powers.

These Consolidated Financial Statements are presented in Euros because that is the currency of the primary

economic environment in which the Group operates.

2. Significant accounting policies

Basis of preparation

The Consolidated Financial Statements have also been prepared in accordance with IFRS adopted by the

European Union. The Group’s Consolidated Financial Statements also comply with Article 4 of the EU IAS

Regulations.

The Consolidated Financial Statements have been prepared on a going concern basis, applying a historical

cost convention, except for the measurement of investment property, financial assets classified as available-

for-sale and derivative financial instruments that have been measured at fair value.

In the current year, the Group has applied a number of amendments to IFRSs and a new Interpretation

issued by the International Accounting Standards Board (IASB) that are mandatorily effective for an

accounting period that begins on or after 1 January 2017.

Recognition of deferred tax assets for unrealised losses – Amendments to IAS 12, and

Disclosure initiative – amendments to IAS 7.

The adoption of these amendments did not have any impact on the Consolidated Financial Statements of the

Group or the Company for the current period or any prior period and is not likely to affect future periods.

The amendments to IAS 7 require disclosure of changes in liabilities arising from financing activities, see

Note 17.

A number of new standards and amendments to standards and interpretations are effective for annual

periods beginning after 1 January 2017, and have not been applied in preparing these consolidated financial

statements:

IFRS 9 ‘Financial instruments’

IFRS 15 ‘Revenue from contracts with customers’

IFRS 16 ‘Leases’

Amendment to IAS 40, ‘Investment property’ relating to transfers of investment property

Annual improvements 2014–2016

IFRIC 22 ‘Foreign currency transactions and advance consideration’

None of these standards not yet effective are expected to have a significant effect on the Consolidated

Financial Statements of the Group. Certain Standards which might have an impact are discussed below.

Title of standard IFRS 9 Financial Instruments

Nature of change IFRS 9 addresses the classification, measurement and derecognition of financial

assets and financial liabilities, introduces new rules for hedge accounting and a new

impairment model for financial assets.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 24

Impact

The group has reviewed its financial assets and liabilities and is expecting the

following impact from the adoption of the new standard on 1 January 2018:

i. Classification – Financial assets and liabilities

IFRS 9 contains three principal classification categories for financial assets:

measured at amortised cost, FVOCI and FVTPL. The standard eliminates the

existing IAS 39 categories of held to maturity, loans and receivables and available

for sale.

Based on its assessment, the Group does not believe that the new classification

requirements will have a material impact on its accounting for investments in

equity securities that are managed on a fair value basis. At 31 December 2017, the

Group had no equity investments classified as available-for-sale.

There will be no impact on the Group’s accounting for financial liabilities, as the

new requirements only affect the accounting for financial liabilities that are

designated at fair value through the Consolidated Statement of Comprehensive

Income and the group does not have any such liabilities. The derecognition rules

have been transferred from IAS 39 Financial Instruments: Recognition and

Measurement and have not been changed.

ii. Impairment – Financial assets and contract assets

The new impairment model requires the recognition of impairment provisions

based on expected credit losses (ECL) rather than only incurred credit losses as is

the case under IAS 39. It applies to financial assets classified at amortised cost,

debt instruments measured at FVOCI, contract assets under IFRS 15 Revenue from

Contracts with Customers, lease receivables, loan commitments and certain

financial guarantee contracts.

The significant financial assets held by the Group that will be impacted by the

impairment losses recognised under IFRS 9 are trade receivables. Gross trade

receivables held at 31 December 2017 were €29,139k with an impairment

provision, recognised under IAS 39, of an immaterial amount as shown in Note 10.

Based on the reasons set out in the Financial risk factors section (Note 1), the credit

risk associated with unpaid rent is deemed to be low. Management have performed

an assessment of the impact of impairment losses recognised for trade receivables

under IFRS 9 at 31 December 2017 through estimating the ECLs based on actual

credit loss experienced over the past three years. Based on this assessment the

impact and volatility on impairment losses recognised under IFRS 9 is immaterial.

iii. Hedge accounting

As a general rule, more hedge relationships might be eligible for hedge accounting,

as the standard introduces a more principles-based approach. The Group has no

current hedge relationships for foreign exchange contracts or cross currency swap

contracts designated as net investment hedges which would qualify as continuing

hedges upon the adoption of IFRS 9.

The Group does not intend to designate other derivative instruments which may be

used as part of its risk management strategy as hedging relationships under IFRS 9.

iv. Disclosures

The new standard also introduces expanded disclosure requirements and changes in

presentation. These are not expected to change the nature and extent of the Group’s

disclosures.

Date of adoption

by group

Must be applied for financial years commencing on or after 1 January 2018. The

Group will apply the new rules retrospectively from 1 January 2018, with the

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 25

practical expedients permitted under the standard. Comparatives for 2017 do not

require restatement.

Title of standard IFRS 15 Revenue from Contracts with Customers

Nature of change The IASB has issued a new standard for the recognition of revenue. This will

replace IAS 18 which covers contracts for goods and services. The new standard is

based on the principle that revenue is recognised when control of a good or service

transfers to a customer. The standard permits either a full retrospective or a

modified retrospective approach for the adoption.

Impact

Management has assessed the effects of applying the new standard on the Group’s

financial statements.

Revenue recognition – IFRS 15 does not apply to rental income which

makes up over 76% of total revenue of the Group, but does apply to other

non-core revenue streams; service charge income, management and

performance fees and trading property disposals. At present the Group

does not expect IFRS 15 to have a significance difference in the timing of

the recognition of revenue for the non-core income streams that falls

under the scope and an immaterial impact on the Group’s Consolidated

Statement of Comprehensive Income.

Disclosures – The new standard also introduces expanded disclosure

requirements. These will change the nature and extent of the Group’s

revenue disclosures.

Date of adoption

by group

Mandatory for financial years commencing on or after 1 January 2018. The Group

intends to adopt the standard using the modified retrospective approach which

means that the cumulative impact of the adoption will be recognised in retained

earnings as of 1 January 2018 and that comparatives will not be restated.

Title of standard IFRS 16 Leases

Nature of change IFRS 16 was issued in January 2016. It will result in almost all leases being

recognised on the balance sheet for a lessee, as the distinction between operating

and finance leases is removed. Under the new standard, an asset (the right to use

the leased item) and a financial liability to pay rentals are recognised. The only

exceptions are short-term and low-value leases. The accounting for lessors will not

significantly change.

Impact

At present, as a lessee the Group holds one operating lease, with the non-

cancellable future lease payments at 31 December 2017 of €96k. Management

have performed an assessment of the impact of bringing operating leases on

balance sheet and IFRS 16 is expected to be immaterial to the Group.

Date of adoption

by group

Mandatory for financial years commencing on or after 1 January 2019. At this

stage, the Group does not intend to adopt the standard before its effective date. The

Group intends to apply the simplified transition approach and will not restate

comparative amounts for the year prior to first adoption.

There are no other IFRSs or IFRS IC interpretations that are not yet effective that would be expected to have

a material impact on the Group.

Basis of consolidation

The Consolidated Financial Statements comprise the financial statements of the Company and its

subsidiaries (“the Group”).

The controlling share in the Group’s subsidiaries is held by SEGRO European Logistics Partnership S.à r.l.

via its holding in SELP Investments S.à r.l. which, in turn holds a majority of shares in SELP Finance S.à

r.l. The Group’s remaining subsidiaries are held by SELP Finance S.à r.l.

The share of shareholder interests and profit or loss attributable to non-Group shareholders is attributed to

Non-Controlling Interests. Non-Controlling Interests are held directly or indirectly by SEGRO Luxembourg

S.à r.l. and PSP Britannia Ltd which each own 50% shareholding in Segro European Logistics Partnership

S.à r.l. Inter-company transactions, balances and unrealised gains or losses on transactions between Group

companies are eliminated.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 26

Subsidiaries are all entities (including structured entities) over which the Group has control. The Group

controls an entity when the Group is exposed to, or has rights to, variable returns from its involvement with

the entity and has the ability to affect those returns through its power over the entity. Subsidiaries are fully

consolidated from the date on which control is transferred to the Group. They are deconsolidated from the

date that control ceases.

Business combinations

The acquisition of subsidiaries is accounted for using the acquisition method. The cost of the acquisition is

measured at the aggregate of the fair values of assets given, liabilities incurred or assumed, and equity

instruments issued by the Group in exchange for control of the acquiree. Acquisition related costs are

recognised in the Income Statement as incurred. The acquiree’s identifiable assets, liabilities and contingent

liabilities that meet the conditions for recognition under IFRS 3 are recognised at their fair value at the

acquisition date, except for non-current assets (or disposal groups) that are classified as held for sale in

accordance with IFRS 5 Non-Current Assets Held for Sale and Discontinued Operations, which are

recognised and measured at fair value less costs to sell.

Goodwill arising on acquisition is recognised as an asset measured at cost, being the excess of the cost of

the business combination over the Group’s interest in the net fair value of the identifiable assets, liabilities

and contingent liabilities recognised. If, after reassessment, the Group’s interest in the net fair value of the

acquiree’s identifiable assets, liabilities and contingent liabilities exceeds the cost of the business

combination, the excess is recognised immediately in the Income Statement.

The interest of non-controlling interest shareholders in the acquiree is initially measured at their proportion

of the net fair value of the assets, liabilities and contingent liabilities recognised.

When the consideration transferred by the Group in a business combination includes a contingent

consideration arrangement, the contingent consideration is measured as its acquisition-date fair value.

Changes in fair value of the contingent consideration that qualify as measurement period adjustments are

adjusted retrospectively, with corresponding adjustments against goodwill. Measurement period adjustments

are adjustments that arise from additional information obtained during the ‘measurement period’ (which

cannot exceed one year from the acquisition date) about facts and circumstances that existed at the

acquisition date.

Contingent consideration that is classified as an asset or a liability is re-measured at subsequent reporting

dates in accordance with IAS 39, as appropriate, with the corresponding gain or loss being recognised in the

Group Income Statement.

Accounting for asset acquisitions

For acquisitions of a subsidiary not meeting the definition of a business, the Group allocates the cost

between the individual identifiable assets and liabilities in the Group based on their relative fair values at

the date of acquisition. Such transactions or events do not give rise to goodwill.

Going concern

Note 1 to the Consolidated Financial Statements includes the Group’s risk factors, along with its policies

and processes for managing such risks.

The Group considers that positive net operating cash flows at €114,053k (€87,167k in 2016) together with

its short term net assets and access to funding via the Group’s Revolving Credit Facility will allow the

Group to meet its short-term commitments. As a consequence, Management believes that the Group has

adequate resources to continue in operation for the foreseeable future and, accordingly, continues to adopt

the going concern basis of accounting in preparing the annual Consolidated Financial Statements.

Cash Flow Statement

The Group reports cash flows from operating activities using the indirect method. Interest received is

presented within investing cash flows; interest paid is presented within operating cash flows. The

acquisitions of investment properties are disclosed as cash flows from investing activities because this most

appropriately reflects the Group's business activities.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 27

Foreign currency transactions

Foreign currency transactions are translated into the functional currency at the exchange rates ruling on the

transaction date. Foreign exchange gains and losses resulting from settling these, or from retranslating

monetary assets and liabilities held in foreign currencies, are booked in the Consolidated Income Statement.

Consolidation of foreign entities

The Consolidated Financial Statements are presented in Euro which is the Company’s functional currency

and the Group’s presentational currency. The Group is domiciled within the Euro-zone and its operations

are predominately located within the Euro-zone, hence, the Group’s functional currency is the Euro.

Entities located outside the Euro-zone are mainly using Euro as the main operating currency, as a majority

of transactions and balances held in Euro and therefore the Group considers that the functional currency of

these entities is the Euro. Thus no currency translation adjustment (CTA) is recognised in the consolidated

statement of other comprehensive income.

The main exchange rates used to translate foreign currency denominated amounts in 2017 are:

Consolidated Statement of Financial Position: €1 = PLN4.159 (2016: 4.402) and €1 = CZK25.58 (2016:

27.09)

Consolidated Statement of Comprehensive Income: €1 = PLN4.31 (2016: 4.36) and €1 = CZK26.59 (2016:

27.03)

Investment properties are valued by the Group’s independent valuers in Euro.

Investment properties

These properties include completed properties that are generating rent or are available for rent, and

development properties that are under development or land this is available for development. Investment

properties comprise freehold and leasehold properties and are first measured at cost (including transaction

costs), then revalued to market value at each reporting date by independent professional valuers. Leasehold

properties are shown gross of the leasehold payables (which are accounted for as finance lease obligations).

Valuation gains and losses in a period are recognised in the Consolidated Income Statement. As the Group

uses the fair value model, as per IAS 40 Investment Properties, no depreciation is provided. An asset will be

classified as held for sale in line with IFRS 5 Non-Current Assets Held for Sale and Discontinued

Operations, where there is Board approval at the year-end date and the asset is expected to be disposed of

within 12 months after the date of the Consolidated Statement of Financial Position.

Property acquisitions and disposals

Properties are treated as acquired at the point when the Group assumes the significant risks and rewards of

ownership and as disposed of when these risks or rewards are transferred to the buyer. Generally, this would

occur on completion of contract. Any gains or losses arising on de-recognition of the property (calculated as

the difference between the net disposal proceeds and the carrying amount of the asset) is included in profit

or loss in the period in which the property is de-recognised.

Leases

Leases where substantially all of the risks and rewards of ownership are transferred to the lessee are

classified as finance leases. All others are deemed operating leases. Under operating leases, properties

leased to tenants are accounted for as investment properties. In cases where only the built part of a property

lease qualifies as a finance lease, the land is shown as an investment property.

Revenue

Revenue includes gross rental income, joint venture management fee income, income from service charges

and proceeds from the sale of trading properties.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 28

Rental income

Rental income from properties let as operating leases is recognised on a straight-line basis over the lease

term. Lease incentives and initial costs to arrange leases are capitalised, then amortised on a straight-line

basis over the lease term (‘rent averaging’). For properties let as finance leases, ‘minimum lease receipts’

are apportioned between finance income and principal repayment, but receipts that were not fixed at lease

inception (e.g. rent review rises) are recognised as income when earned. Surrender premiums received in the

period are included in rental income.

Service charges and other recoveries from tenants

These include income in relation to service charges, directly recoverable expenditure and management fees.

Revenue from services is recognised by reference to the state of completion of the relevant services

provided at the reporting date. Service charge income and expenditure is recognised within the

Consolidated Income Statement.

Sale of trading properties

Proceeds from the sale of trading properties are recognised when the risks and rewards of ownership have

been transferred to the purchaser. This generally occurs on completion of the contract.

Operating Segments

The Group considers its operating segments to be based on the geographical location of the Group’s assets

and this is reported in a manner consistent with the internal reporting provided to the board of Managers.

The chief operating decision maker is the board of Managers. The board of managers considers the

operating segments to be Northern Europe (principally Germany and Benelux), Central Europe (principally

Poland and Czech Republic), and Southern Europe (principally France, Italy and Spain).

Financial instruments

Borrowings

Borrowings are recognised initially at fair value less attributable transaction costs. Subsequent to initial

recognition, borrowings are stated at amortised cost with any difference between the amount initially

recognised and the redemption value being recognised in the Consolidated Income Statement over the

period of the borrowings, using the effective interest rate method.

Gross borrowing costs relating to direct expenditure on properties under development or undergoing major

refurbishment are capitalised. The interest capitalised is calculated using the Group’s weighted average cost

of borrowing for the relevant currency. Interest is capitalised as from the commencement of the

development work until the date of practical completion. The capitalisation of finance costs is suspended if

there are prolonged periods when development activity is interrupted.

Borrowings are classified as current liabilities unless the Group has an unconditional right to defer

settlement of the liability for at least 12 months after the date of the Consolidated Statement of Financial

Position.

Interest payable and finance costs

Interest payable is charged to the Consolidated Income Statement as accrued. Costs incurred directly in

connection with the issue of debt are deducted from the proceeds and the net amount included in liabilities.

Such costs, together with any premium or discount on issue, are credited or charged, as appropriate, to the

Consolidated Income Statement over the term of the debt at a constant rate on the carrying amount of the

liability.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 29

Trade and other receivables and payables

Trade and other receivables are initially booked at fair value net of transaction costs and subsequently

measured at amortised cost less provisions for impairment. An impairment provision is created where there

is objective evidence that the Group will not be able to collect in full.

Trade and other payables are recognised initially at fair value and subsequently measured at amortised cost

using the effective interest method.

The Group requires that tenants provide deposits or guarantees. Where a guarantee is in place the Group

does not provide for impairment of monies receivable. Receivables and payables are classified as current

unless the Group has an unconditional right to defer settlement of the receivables or payables for at least 12

months after the date of the Consolidated Statement of Financial Position.

Cash and cash equivalents

Cash and cash equivalents includes cash in hand, deposits held at call with banks, other short-term highly

liquid investments with original maturities of three months or less, and bank overdrafts.

Share capital and legal reserves

Share capital is recognised when issued. Reserves are recognised in line with the local legal requirements

and to the extent that legal reserves are required, not distributed. Share capital and reserves are recognised

at original cost and are held at the cost of issue.

Current and deferred income tax

The tax expense for the period comprises current and deferred tax. Tax is recognised in the Consolidated

Income Statement, except to the extent that it relates to items recognised directly in other comprehensive

income or equity - in which case, the tax is also recognised in other comprehensive income or equity.

The current income tax charge is calculated on the basis of the tax laws enacted or substantively enacted at

the date of the Consolidated Statement of Financial Position in the countries where the Group operates.

Management periodically evaluates positions taken in tax returns with respect to situations in which

applicable tax regulation is subject to interpretation, and establishes provisions where appropriate on the

basis of amounts expected to be paid to the tax authorities.

Deferred income tax is provided in full, using the liability method, on temporary differences arising between

the tax bases of assets and liabilities and their carrying amounts in the Consolidated Financial Statements.

However, deferred income tax is not accounted for if it arises from initial recognition of an asset or liability

in a transaction other than a business combination that at the time of the transaction affects neither

accounting nor taxable profit or loss. Deferred income tax is determined using tax rates (and laws) that have

been enacted or substantially enacted by the date of the Consolidated Statement of Financial Position and

are expected to apply when the related deferred income tax asset is realised or the deferred income tax

liability is settled.

Deferred income tax assets are recognised to the extent that it is probable that future taxable profit will be

available against which the temporary differences can be utilised.

The carrying value of the Group’s investment property is assumed to be realised by sale at the end of use.

The capital gains tax rate applied is that which would apply on a direct sale of the property recorded in the

Consolidated Statement of Financial Position regardless of whether the Group would structure the sale via

the disposal of the subsidiary holding the asset, to which a different tax rate may apply. The deferred tax is

then calculated based on the respective temporary differences and tax consequences arising from recovery

through sale.

Deferred income tax is provided on temporary differences arising on investments in subsidiaries, except

where the timing of the reversal of the temporary difference is controlled by the Group and it is probable

that the temporary difference will not reverse in the foreseeable future.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 30

Deferred income tax assets and liabilities are offset when there is a legally enforceable right to offset current

tax assets against current tax liabilities and when the deferred income tax assets and liabilities relate to

income taxes levied by the same taxation authority on either the same taxable entity or different taxable

entities where there is an intention to settle the balances on a net basis.

Critical accounting judgements and key sources of estimation uncertainty

In the application of the Group’s accounting policies and IFRS, the Managers are required to make

judgements, estimates and assumptions about the carrying amount of assets and liabilities that are not

readily apparent from other sources. The estimates and associated assumptions are based on historical

experience and other factors that are considered to be relevant. Actual results may differ from these

estimates. The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to

accounting estimates are recognised in the period in which the estimate is revised if the revision affects only

that period, or in the period of the revisions and future periods if the revision affects both current and future

periods.

Significant areas of estimation uncertainty:

Property valuations

Valuation of property is a central component of the business. In estimating the fair value, the Group engages

third party qualified valuers to perform the valuation. Information about the valuation techniques and inputs

used in determining the fair value of the property portfolio is disclosed in Note 9 property valuation

techniques and related quantitative information.

Financial instruments and fair value measurements

In estimating the fair value of an asset or a liability, the Group uses market-observable data to the extent it is

available. Information about the valuation techniques and inputs used in determining the fair value of

various assets and liabilities is disclosed in Note 12.

Significant areas of judgements in applying the group’s accounting policies:

Accounting for significant acquisitions, disposals and investments

Property transactions are complex in nature. Management considers each material transaction separately

with an assessment carried out to determine the most appropriate accounting treatment and judgements

applied, including whether the transaction represents an asset acquisition or business combination. Where

the Group has acquired property assets by way of acquiring the share capital of the entity that owns the

physical property assets, where this acquisition was not accounted for as a Business Combination and as

neither accounting profit nor taxable profit were affected at the time of the transaction, the initial

recognition exemption in IAS 12, ‘Income Taxes’ has been applied and the Group does not recognise

deferred tax that would otherwise have arisen on temporary differences associated with the acquired assets

and liabilities at initial recognition.

Revenue recognition

In making its judgement over revenue recognition for cut-off for property transactions, management

considered the detailed criteria for the recognition of revenue set out in IAS 18 Revenue and, in particular,

whether the Group had transferred to the buyer the significant risks and rewards of ownership of the assets

disposed. Management also considers the appropriate accounting treatment of tenant lease incentives.

Financial and operational risk management

Financial risks factors

The risk management function within the Group is carried out in respect of financial risks. Financial risks

are risks arising from financial instruments to which the Group is exposed during or at the end of the

reporting period. Financial risk comprises market risk (including currency risk, interest rate risk and other

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 31

price risk), credit risk and liquidity risk. The primary objectives of the financial risk management function is

to establish risk limits, and then ensure that exposure to risks remains within these limits.

Risk management is overseen by the Managers with advice from the Venture Advisor. The Venture

Advisor cooperates closely with all of the Group’s operating units and third party advisors.

a. Market risk

Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because

of changes in market prices. The Group’s market risks may arise from open positions in foreign currencies

and interest-bearing assets and liabilities, to the extent that these are exposed to general and specific market

movements.

The Group seeks to manage Market risk, principally, by seeking to fix future interest payments in advance.

During the period ending 31 December 2017, the Group has minimal exposure to interest rate risks and an

analysis of this risk is disclosed in Note 2.

The Group’s main currency exposures are Polish Zlotys and Czech Crowns. The Group’s balance sheet

translation exposure is as follows:

Gross currency assets: €14,715k

Gross currency liabilities: €334k

Net exposure: €14,381k

The blended sensitivity of the net assets of the Group to a 5% change in the value of the Euro against the

relevant currencies is €757k.

b. Credit risk

Credit risk refers to the risk that a counterparty will default on its contractual obligations resulting in

financial loss to the Group. Potential customers are evaluated for creditworthiness and where necessary

collateral is secured. There is no concentration of credit risk within the lease portfolio to either business

sector or individual company as the Group has a diverse customer base with no one customer accounting for

more than 5% of rental income. Trade receivables (which include unpaid rent and amounts receivable in

respect of property disposals) were approximately 1% of total assets at 31 December 2017. The Managers

are of the opinion that the credit risk associated with unpaid rent is low. In excess of 80% of rent due is

generally collected within 21 days of the due date. Trade receivables are actively monitored and collection

pursued to ensure that the Group has minimal exposure to credit risk.

An analysis of the Group’s trade receivables can be found in Note 10.

Investment in financial instruments is restricted to banks and short-term liquidity funds with a good credit

rating.

The Group’s exposure and the credit ratings of its counterparties are continuously monitored and the

aggregate value of transactions concluded is spread among approved counterparties.

c. Liquidity risk

Ultimate responsibility for liquidity risk management rests with the Managers, who have built an

appropriate liquidity risk management framework for the management of the Group’s short, medium and

long-term funding and liquidity management requirements. The Group manages liquidity risk by having a

policy that requires that adequate cash and committed bank facilities remain available to cover and match

all debt maturities, development spend, trade related and corporate cash flows forward over a rolling 18-

month period. This is achieved by continuously monitoring forecast and actual cash flows and matching the

maturity profiles of financial assets and liabilities. Details on current financing facilities are provided in

Note 12.

Current assets and liabilities are deemed receivable / payable within one year and are, therefore, carried at a

value equal to their nominal value including accrued interest.

Bank covenants are monitored on a regular basis and reviewed by the Managers. Long-term liquidity risks

are monitored and reviewed annually by the Managers whilst financing and the Group’s financial strategy is

reviewed and updated annually in conjunction with the Group’s long-term business model.

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 32

Details of the maturity of long-term payables is shown within Note 12.

Cash flows and fair value interest rate risk

Interest from bank loans and bonds within the Group are fixed and known in advance with the exception of

the Revolving Credit Facility which carries a variable coupon rate as of 31 December 2017, if interest rates

had been 200 basis points higher, with all other variables held constant, post-tax profit for the year would

have been €1,850k lower. If interest rates had been 200 basis points lower, with all other variables held

constant, post-tax profit for the year would have increased by €581k.

Operational risks

The Group is mainly exposed to Operational risk through the fair value movements in property values

which are classified in the Consolidated Statement of Financial Position at fair value through consolidated

income statement. To manage this risk, arising from investments in property, the Group diversifies its

portfolio, seeks to maintain financially sound tenants on long leases and maintains a prime portfolio in areas

and functions of high demand. Diversification of the portfolio is maintained in accordance with the limits

set out in the Shareholders Agreement. The Group targets a geographically diverse portfolio with a 20-40%

allocation to Germany, France and Poland, a 5-15% allocation to Benelux, a 0-10% allocation to Czech

Republic, Spain and Italy.

3. Total revenue

Total revenue is comprised of:

4. Property operating expenses

Property operating expenses are comprised of:

5.

2017 €’000s

2016 €’000s

Rental income from investment properties 155,222 140,230

Surrender premiums 580 –

Gross rental income 155,802 140,230

Property management fees 2,670 2,729

Service charge income 45,293 40,601

Total revenue 203,765 183,560

2017 €’000s

2016 €’000s

Vacant property costs (1,490) (1,580)

Service charge (42,781) (38,512)

Venture and asset management fees (14,255) (12,456)

Letting, marketing, legal and professional fees (2,455) (2,194)

Bad debt expense (488) (521)

Other expenses (6,833) (4,529)

Property management expenses (68,302) (59,792)

Property administration expenses (83) (99)

Total property operating expenses (68,385) (59,891)

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 33

5. Administration expenses

Administration expenses are comprised of :

Auditor’s remuneration includes non audit services for an amount of €75k. During the period the Group

employed an average of two employees (2016: two).

6. Realised and unrealised property gains/(losses) from changes in fair value of investment properties

Gains and losses from changes in the fair value of investment properties are comprised of :

7. Finance costs

Finance costs are comprised of :

Refinancing costs relate to the repayment of the financing facilities detailed in Note 12 and is, therefore,

considered to be a one-off cost.

2017 €’000s

2016 €’000s

Administration expenses

(2,014) (1,761)

Administration expenses include:

Auditor’s remuneration (455) (281)

Staff costs (110) (112)

2017 €’000s

2016 €’000s

Profit/(loss) on sale of investment properties

847 (260)

Unrealised gain/(losses) on investment properties

175,057 35,720

Total realised and unrealised property gain/(losses) 175,904 35,460

2017 €’000s

2016 €’000s

Finance costs

Interest on loans

(14,186) (20,622)

Interest on shareholder and related party loans (30,897) (29,253)

Exchange gain/(loss) 417 (1,098)

Refinancing costs (4,199) (13,219)

Total borrowing costs (48,865) (64,192)

Less amounts capitalised on the development of properties 1,655 942

Net finance costs (47,210) (63,250)

SEGRO European Logistics Partnership S.à r.l.

Registered in Luxembourg No: B177300 Page 34

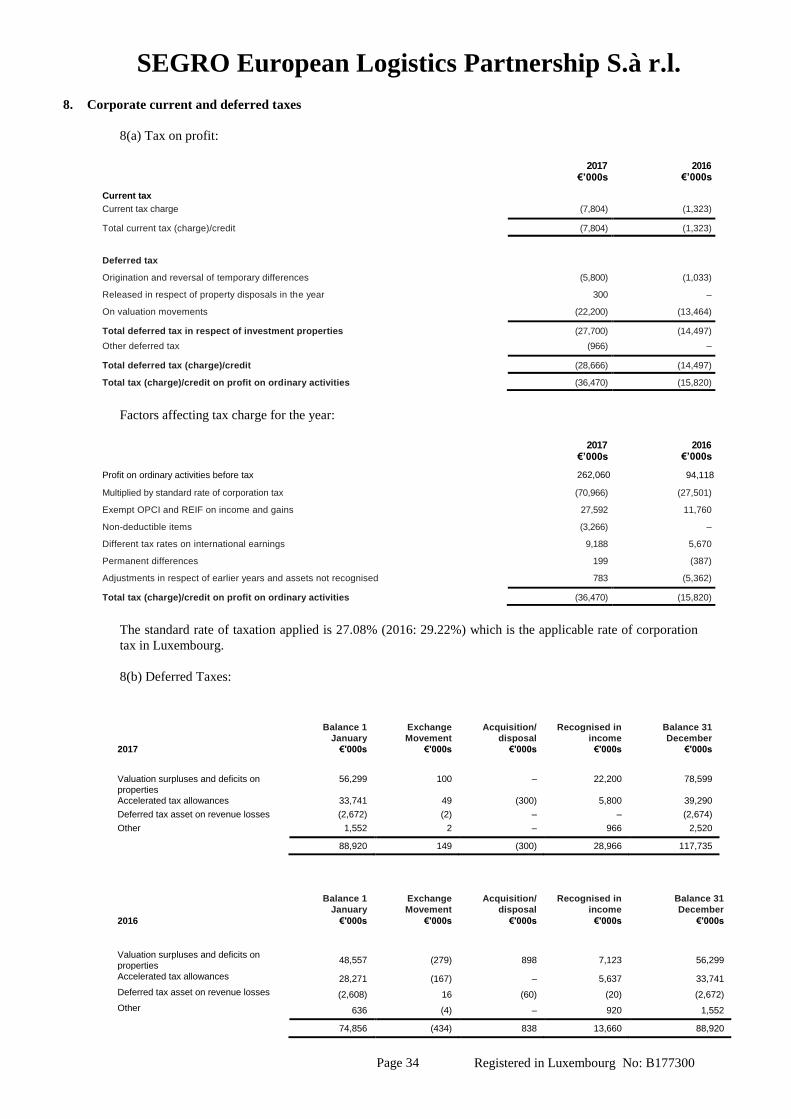

8. Corporate current and deferred taxes

8(a) Tax on profit:

Factors affecting tax charge for the year:

The standard rate of taxation applied is 27.08% (2016: 29.22%) which is the applicable rate of corporation

tax in Luxembourg.

8(b) Deferred Taxes:

Balance 1

January

Exchange

Movement

Acquisition/

disposal

Recognised in

income

Balance 31

December

2017 €'000s €'000s €'000s €'000s €'000s

Valuation surpluses and deficits on properties

56,299 100 – 22,200 78,599

Accelerated tax allowances 33,741 49 (300) 5,800 39,290

Deferred tax asset on revenue losses (2,672) (2) – – (2,674)