Seeing Beyond the Complexity: Making the Case for ...

16

Collateralized loan obligations are robust, opportunity-rich debt instruments that offer the potential for above- average returns versus other fixed income strategies. Here, we explore how these instruments work and the potential benefits they offer insurance investors. Seeing Beyond the Complexity: Making the Case for Collateralized Loan Obligations for US Insurers November 2018

Transcript of Seeing Beyond the Complexity: Making the Case for ...

Collateralized loan obligations are robust, opportunity-rich debt instruments that offer the potential for above-average returns versus other fixed income strategies. Here, we explore how these instruments work and the potential benefits they offer insurance investors.

Seeing Beyond the Complexity: Making the Case for Collateralized Loan Obligations for US Insurers

November 2018

2 | PineBridge Investments

Authors:

Steven Oh, CFAGlobal Head of Credit and Fixed Income

Laila Kollmorgen, CFACLO Tranche Portfolio Manager

Jeannine Heal, CFAInsurance Client Advisor

Collateralized loan obligations (CLOs) are robust, opportunity-rich debt instruments that have been around for more than 20 years. US insurers have more than doubled their exposure to this asset class since year-end 2009, with approximately $51.5 billion allocated to CLOs at the end of 2017.1

It’s no surprise why CLOs are gaining wider prominence in markets: They offer a compelling combination of above-average yield and potential appreciation. They are especially attractive to insurers because they are capital efficient with relatively low interest rate durations and high spreads. For many insurers, CLOs can provide a compelling return on risk-based capital.

And yet, in many ways, CLOs have yet to be widely embraced by the industry, and many insurers are still underallocated to this asset class, in our view.

Why are many insurance companies shying away from CLOs? CLOs have long intimidated a wide range of investors due to their complexity, and some misconceptions have also become associated with them. Beyond the complexity, insurers in particular might be concerned about liquidity and costs. And while some insurers have the resources and specialization in-house to allocate to CLOs, others do not.

Despite these common reservations, we believe many insurers, particularly smaller and midsize companies, should consider adding CLOs to their portfolios. While CLOs are structurally complicated, they are that way for investors’ benefit, and they offer levels of yield that we believe are more than commensurate with their levels of risk. Insurance companies without in-house CLO expertise, or those that are looking to invest in CLO tranches that require a higher degree of specialization (i.e., tranches rated below AA/A), may want to consider hiring a third-party manager.

Here, we take a closer look at CLOs and what they can offer insurance investors – and clear up some misconceptions along the way.

What is a CLO?Put simply, a collateralized loan obligation is a portfolio of leveraged loans that is securitized and managed as a fund. Each CLO is structured as a series of tranches that are interest-paying bonds, along with a small portion of equity.

CLOs originated in the late 1980s, similar to other types of securitizations, as both a financing tool and a way for banks to package leveraged loans together to provide investors with an investment vehicle with varied degrees of risk and return to best suit their investment objectives. The first vintage of “modern” CLOs – which focused on generating income via cash flows – was issued starting in the mid-to-late 1990s. Commonly known as “CLO 1.0,” they included some high yield bonds, as well as loans, and were the standard CLO structure until the financial crisis struck in 2008.

The next vintage, CLO 2.0, began in 2010 and changed in response to the crisis by strengthening credit support and shortening the period in which loan interest and proceeds could be reinvested into additional loans.

The current vintage, CLO 3.0, began in 2014 and further reduced risk by eliminating high yield bonds and adhering to the Volcker Rule and other new regulations.

Making the Case for Collateralized Loan Obligations for US Insurers | 3

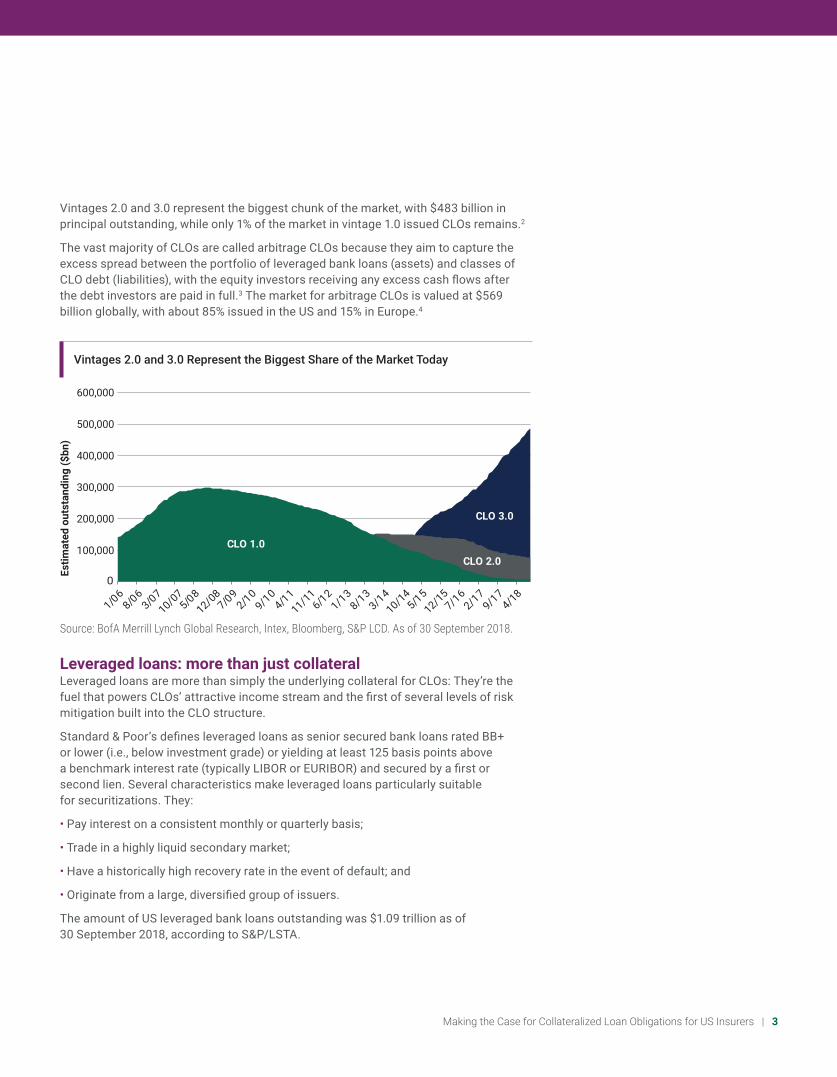

Vintages 2.0 and 3.0 represent the biggest chunk of the market, with $483 billion in principal outstanding, while only 1% of the market in vintage 1.0 issued CLOs remains.2

The vast majority of CLOs are called arbitrage CLOs because they aim to capture the excess spread between the portfolio of leveraged bank loans (assets) and classes of CLO debt (liabilities), with the equity investors receiving any excess cash flows after the debt investors are paid in full.3 The market for arbitrage CLOs is valued at $569 billion globally, with about 85% issued in the US and 15% in Europe.4

Source: BofA Merrill Lynch Global Research, Intex, Bloomberg, S&P LCD. As of 30 September 2018.

Vintages 2.0 and 3.0 Represent the Biggest Share of the Market Today

0

100,000

200,000

300,000

400,000

500,000

600,000

1/06

8/06

3/0710/0

75/0

812/0

87/0

92/1

09/1

04/1

111/1

16/1

21/1

38/1

33/1

410/1

45/1

512/1

57/1

62/1

79/1

7

4/18

CLO 2.0

CLO 3.0

CLO 1.0

Estim

ated

out

stan

ding

($bn

)

4/18

Leveraged loans: more than just collateralLeveraged loans are more than simply the underlying collateral for CLOs: They’re the fuel that powers CLOs’ attractive income stream and the first of several levels of risk mitigation built into the CLO structure.

Standard & Poor’s defines leveraged loans as senior secured bank loans rated BB+ or lower (i.e., below investment grade) or yielding at least 125 basis points above a benchmark interest rate (typically LIBOR or EURIBOR) and secured by a first or second lien. Several characteristics make leveraged loans particularly suitable for securitizations. They:

• Pay interest on a consistent monthly or quarterly basis;

• Trade in a highly liquid secondary market;

• Have a historically high recovery rate in the event of default; and

• Originate from a large, diversified group of issuers.

The amount of US leveraged bank loans outstanding was $1.09 trillion as of 30 September 2018, according to S&P/LSTA.

4 | PineBridge Investments

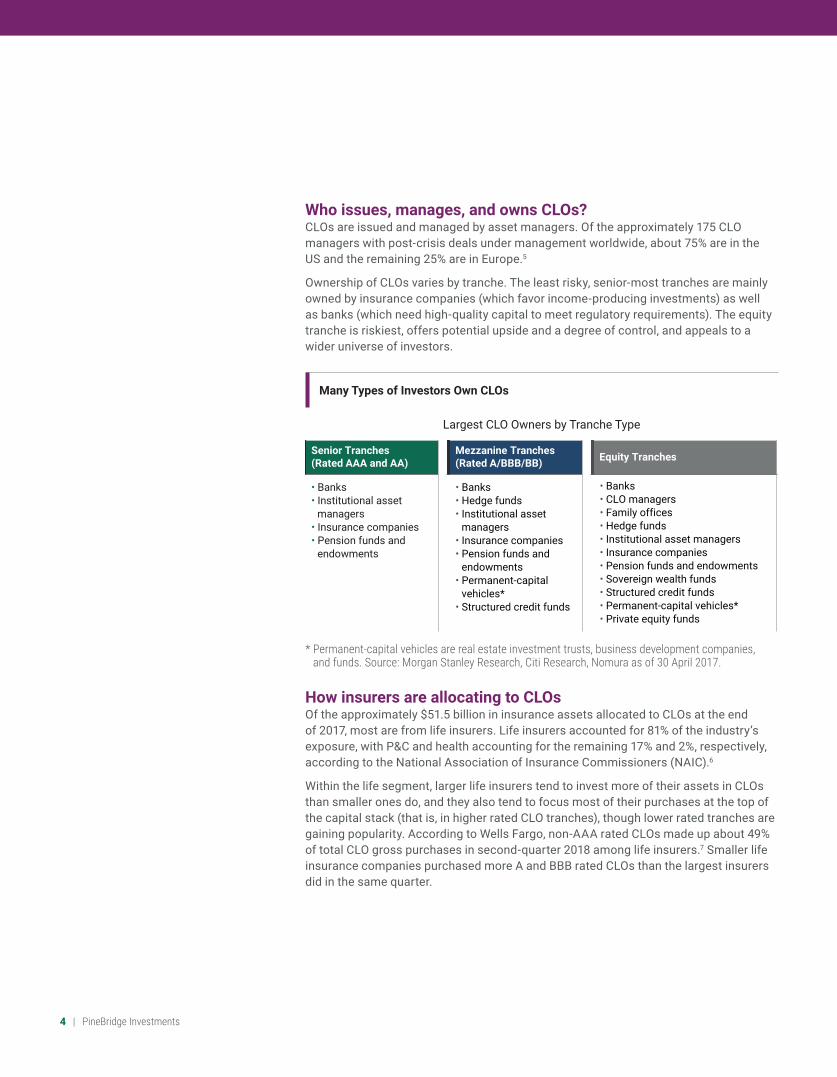

Who issues, manages, and owns CLOs?CLOs are issued and managed by asset managers. Of the approximately 175 CLO managers with post-crisis deals under management worldwide, about 75% are in the US and the remaining 25% are in Europe.5

Ownership of CLOs varies by tranche. The least risky, senior-most tranches are mainly owned by insurance companies (which favor income-producing investments) as well as banks (which need high-quality capital to meet regulatory requirements). The equity tranche is riskiest, offers potential upside and a degree of control, and appeals to a wider universe of investors.

* Permanent-capital vehicles are real estate investment trusts, business development companies, and funds. Source: Morgan Stanley Research, Citi Research, Nomura as of 30 April 2017.

Many Types of Investors Own CLOs

Senior Tranches(Rated AAA and AA)

Mezzanine Tranches(Rated A/BBB/BB) Equity Tranches

• Banks• Institutional asset managers• Insurance companies• Pension funds and endowments

• Banks• Hedge funds• Institutional asset managers• Insurance companies• Pension funds and endowments• Permanent-capital vehicles*• Structured credit funds

• Banks• CLO managers• Family offices• Hedge funds• Institutional asset managers• Insurance companies• Pension funds and endowments• Sovereign wealth funds• Structured credit funds• Permanent-capital vehicles*• Private equity funds

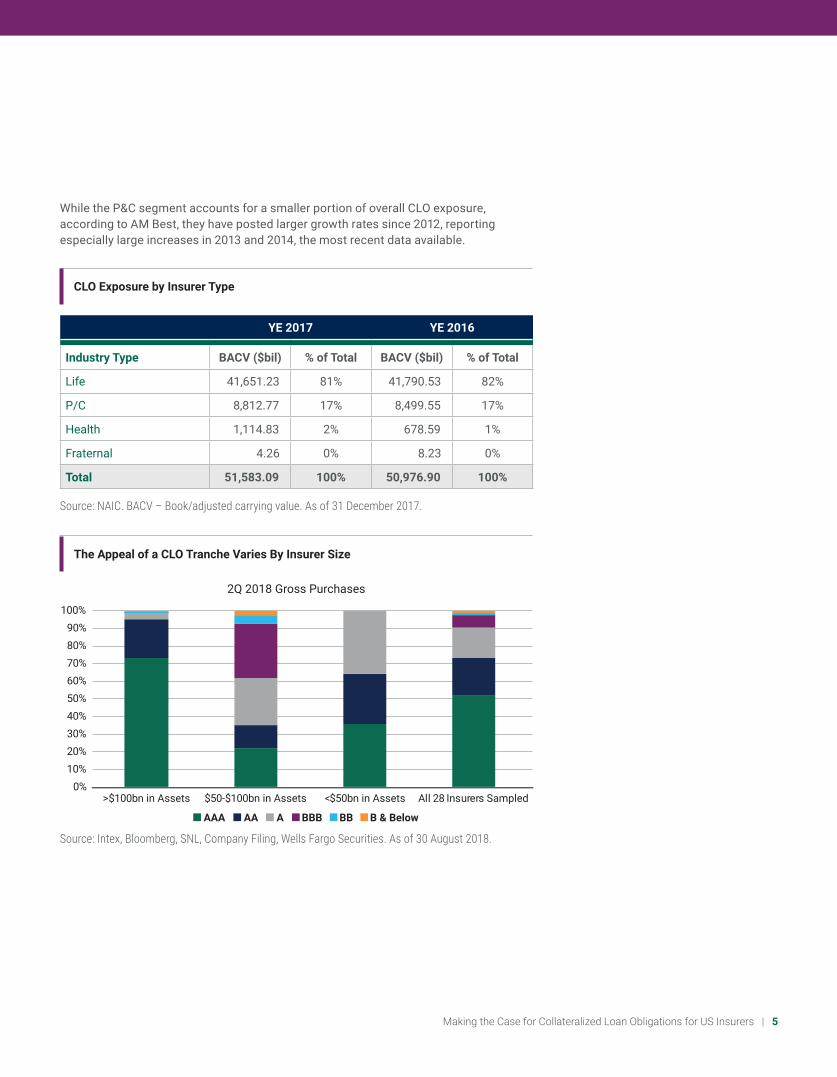

How insurers are allocating to CLOsOf the approximately $51.5 billion in insurance assets allocated to CLOs at the end of 2017, most are from life insurers. Life insurers accounted for 81% of the industry’s exposure, with P&C and health accounting for the remaining 17% and 2%, respectively, according to the National Association of Insurance Commissioners (NAIC).6

Within the life segment, larger life insurers tend to invest more of their assets in CLOs than smaller ones do, and they also tend to focus most of their purchases at the top of the capital stack (that is, in higher rated CLO tranches), though lower rated tranches are gaining popularity. According to Wells Fargo, non-AAA rated CLOs made up about 49% of total CLO gross purchases in second-quarter 2018 among life insurers.7 Smaller life insurance companies purchased more A and BBB rated CLOs than the largest insurers did in the same quarter.

Largest CLO Owners by Tranche Type

Making the Case for Collateralized Loan Obligations for US Insurers | 5

Source: NAIC. BACV – Book/adjusted carrying value. As of 31 December 2017.

CLO Exposure by Insurer Type

While the P&C segment accounts for a smaller portion of overall CLO exposure, according to AM Best, they have posted larger growth rates since 2012, reporting especially large increases in 2013 and 2014, the most recent data available.

YE 2017 YE 2016

Industry Type BACV ($bil) % of Total BACV ($bil) % of Total

Life 41,651.23 81% 41,790.53 82%

P/C 8,812.77 17% 8,499.55 17%

Health 1,114.83 2% 678.59 1%

Fraternal 4.26 0% 8.23 0%

Total 51,583.09 100% 50,976.90 100%

Source: Intex, Bloomberg, SNL, Company Filing, Wells Fargo Securities. As of 30 August 2018.

The Appeal of a CLO Tranche Varies By Insurer Size

0%10%20%30%40%50%60%70%80%90%

100%

>$100bn in Assets $50-$100bn in Assets <$50bn in Assets All 28 Insurers Sampled

AAA AA A BBB BB B & Below

2Q 2018 Gross Purchases

6 | PineBridge Investments

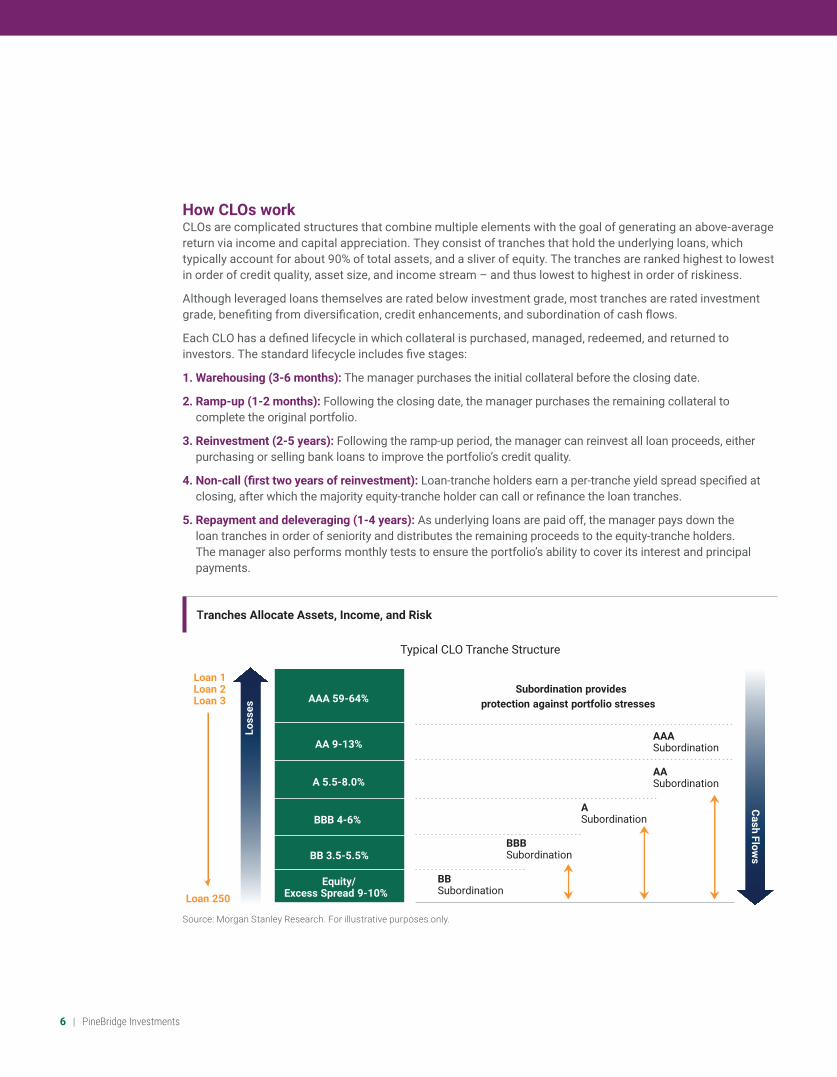

How CLOs workCLOs are complicated structures that combine multiple elements with the goal of generating an above-average return via income and capital appreciation. They consist of tranches that hold the underlying loans, which typically account for about 90% of total assets, and a sliver of equity. The tranches are ranked highest to lowest in order of credit quality, asset size, and income stream – and thus lowest to highest in order of riskiness.

Although leveraged loans themselves are rated below investment grade, most tranches are rated investment grade, benefiting from diversification, credit enhancements, and subordination of cash flows.

Each CLO has a defined lifecycle in which collateral is purchased, managed, redeemed, and returned to investors. The standard lifecycle includes five stages:

1. Warehousing (3-6 months): The manager purchases the initial collateral before the closing date.

2. Ramp-up (1-2 months): Following the closing date, the manager purchases the remaining collateral to complete the original portfolio.

3. Reinvestment (2-5 years): Following the ramp-up period, the manager can reinvest all loan proceeds, either purchasing or selling bank loans to improve the portfolio’s credit quality.

4. Non-call (first two years of reinvestment): Loan-tranche holders earn a per-tranche yield spread specified at closing, after which the majority equity-tranche holder can call or refinance the loan tranches.

5. Repayment and deleveraging (1-4 years): As underlying loans are paid off, the manager pays down the loan tranches in order of seniority and distributes the remaining proceeds to the equity-tranche holders. The manager also performs monthly tests to ensure the portfolio’s ability to cover its interest and principal payments.

Source: Morgan Stanley Research. For illustrative purposes only.

Tranches Allocate Assets, Income, and Risk

Loan 1Loan 2Loan 3

Loan 250

Loss

es

Subordination provides protection against portfolio stresses

AAA Subordination

AASubordination

BB Subordination

BBBSubordination

ASubordination

Cash Flows

AAA 59-64%

AA 9-13%

A 5.5-8.0%

BBB 4-6%

BB 3.5-5.5%

Equity/Excess Spread 9-10%

Typical CLO Tranche Structure

Making the Case for Collateralized Loan Obligations for US Insurers | 7

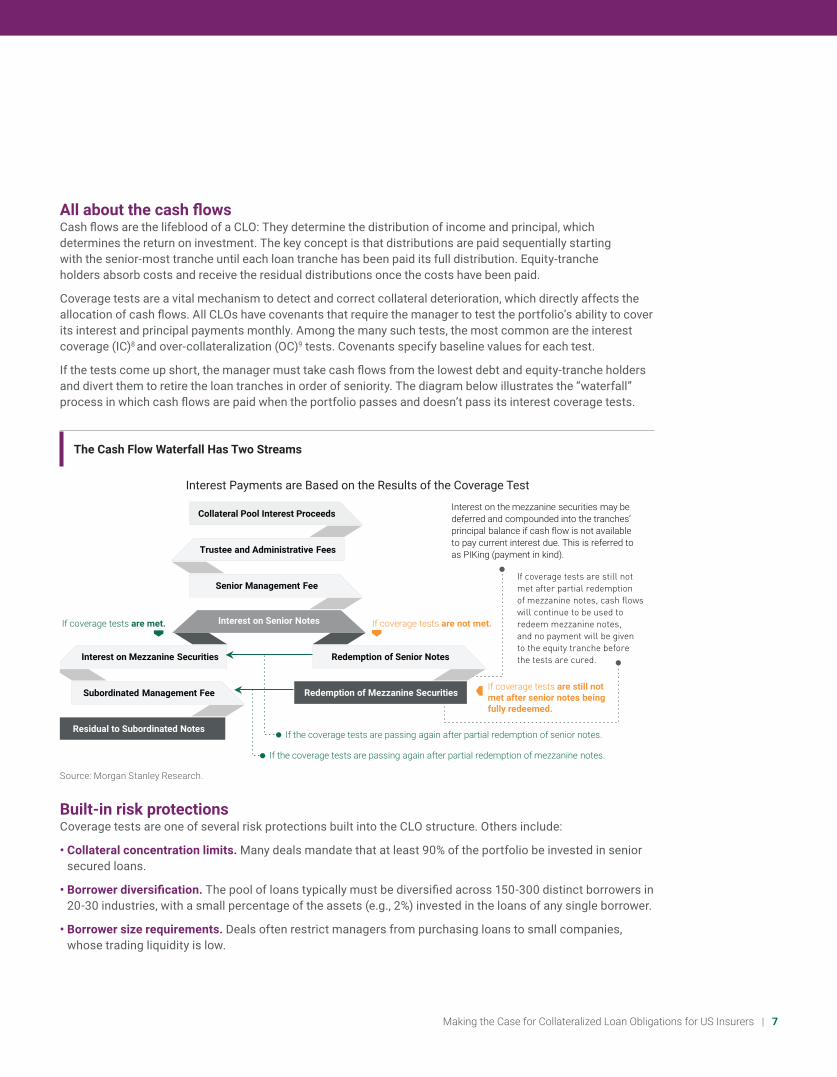

All about the cash flowsCash flows are the lifeblood of a CLO: They determine the distribution of income and principal, which determines the return on investment. The key concept is that distributions are paid sequentially starting with the senior-most tranche until each loan tranche has been paid its full distribution. Equity-tranche holders absorb costs and receive the residual distributions once the costs have been paid.

Coverage tests are a vital mechanism to detect and correct collateral deterioration, which directly affects the allocation of cash flows. All CLOs have covenants that require the manager to test the portfolio’s ability to cover its interest and principal payments monthly. Among the many such tests, the most common are the interest coverage (IC)8 and over-collateralization (OC)9 tests. Covenants specify baseline values for each test.

If the tests come up short, the manager must take cash flows from the lowest debt and equity-tranche holders and divert them to retire the loan tranches in order of seniority. The diagram below illustrates the “waterfall” process in which cash flows are paid when the portfolio passes and doesn’t pass its interest coverage tests.

Source: Morgan Stanley Research.

The Cash Flow Waterfall Has Two Streams

If the coverage tests are passing again after partial redemption of senior notes.

If the coverage tests are passing again after partial redemption of mezzanine notes.

Redemption of Mezzanine Securities

Collateral Pool Interest Proceeds

Trustee and Administrative Fees

Senior Management Fee

Redemption of Senior Notes

Interest on Senior Notes

Interest on Mezzanine Securities

Subordinated Management Fee

Residual to Subordinated Notes

If coverage tests are met. If coverage tests are not met.

Interest on the mezzanine securities may bedeferred and compounded into the tranches’ principal balance if cash flow is not available to pay current interest due. This is referred to as PIKing (payment in kind).

If coverage tests are still not met after senior notes being fully redeemed.

If coverage tests are still notmet after partial redemptionof mezzanine notes, cash flowswill continue to be used toredeem mezzanine notes, and no payment will be given to the equity tranche before the tests are cured.

Interest Payments are Based on the Results of the Coverage Test

Built-in risk protectionsCoverage tests are one of several risk protections built into the CLO structure. Others include:

• Collateral concentration limits. Many deals mandate that at least 90% of the portfolio be invested in senior secured loans.

• Borrower diversification. The pool of loans typically must be diversified across 150-300 distinct borrowers in 20-30 industries, with a small percentage of the assets (e.g., 2%) invested in the loans of any single borrower.

• Borrower size requirements. Deals often restrict managers from purchasing loans to small companies, whose trading liquidity is low.

8 | PineBridge Investments

The equity tranche: highest risk could mean highest returnThe equity tranche occupies a unique place in the CLO structure. It’s essentially a highly leveraged play on the strength of the underlying collateral. Because the equity tranche’s success depends on the success of the loan tranches – it’s last in line to receive cash flows and first to realize loan losses – its owners take the most risk of any CLO investors. Their goal, then, is to maximize the value of the equity.

As compensation for assuming a higher share of risk, the majority equity-tranche holder is given potential control over the entire CLO in the form of options to call or refinance the CLO after the non-call period (usually the first two years of a transaction) expires.

• The call typically is exercised if the equity-tranche holders consider the underlying loans at or near the top of their market value – which is when the equity is most valuable. Exercising the call in this scenario results in the liquidation of the entire portfolio and, in the process, the equity-tranche holders reap the fullest possible benefit of the equity’s leverage.

• Refinancing can happen if CLO tranche spreads fall enough so the CLO capital stack can be replaced at lower spreads, which reduces equity-tranche holders’ cost of leverage and thus increases their return. The portfolio can be refinanced either partially or in full.

A wealth of benefits…CLOs offer insurance investors multiple benefits, both on their own and versus other fixed income sectors.

Higher returns. Over the long term, CLO tranches have significantly outperformed other corporate debt categories, including bank loans, high yield bonds, and investment grade bonds.

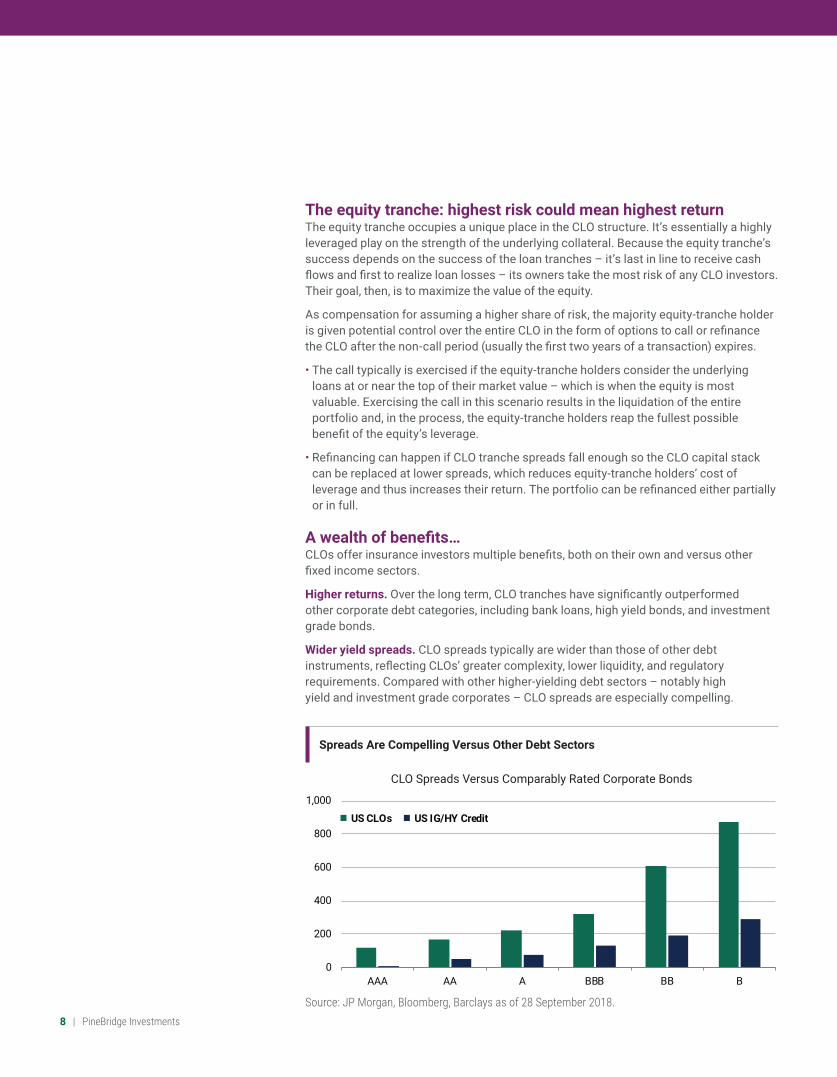

Wider yield spreads. CLO spreads typically are wider than those of other debt instruments, reflecting CLOs’ greater complexity, lower liquidity, and regulatory requirements. Compared with other higher-yielding debt sectors – notably high yield and investment grade corporates – CLO spreads are especially compelling.

Spreads Are Compelling Versus Other Debt Sectors

Source: JP Morgan, Bloomberg, Barclays as of 28 September 2018.

0

200

400

600

800

1,000

AAA AA A BBB BB B

US CLOs US IG/HY Credit

CLO Spreads Versus Comparably Rated Corporate Bonds

Making the Case for Collateralized Loan Obligations for US Insurers | 9

Low interest-rate sensitivity. Leveraged loans and their CLO tranches are floating-rate instruments, priced at a spread above a benchmark rate such as LIBOR or EURIBOR. As interest rates rise or fall, CLO yields will move accordingly and their prices will move less than those of fixed-rate instruments. These characteristics can be advantageous to investors in diversified fixed income portfolios.

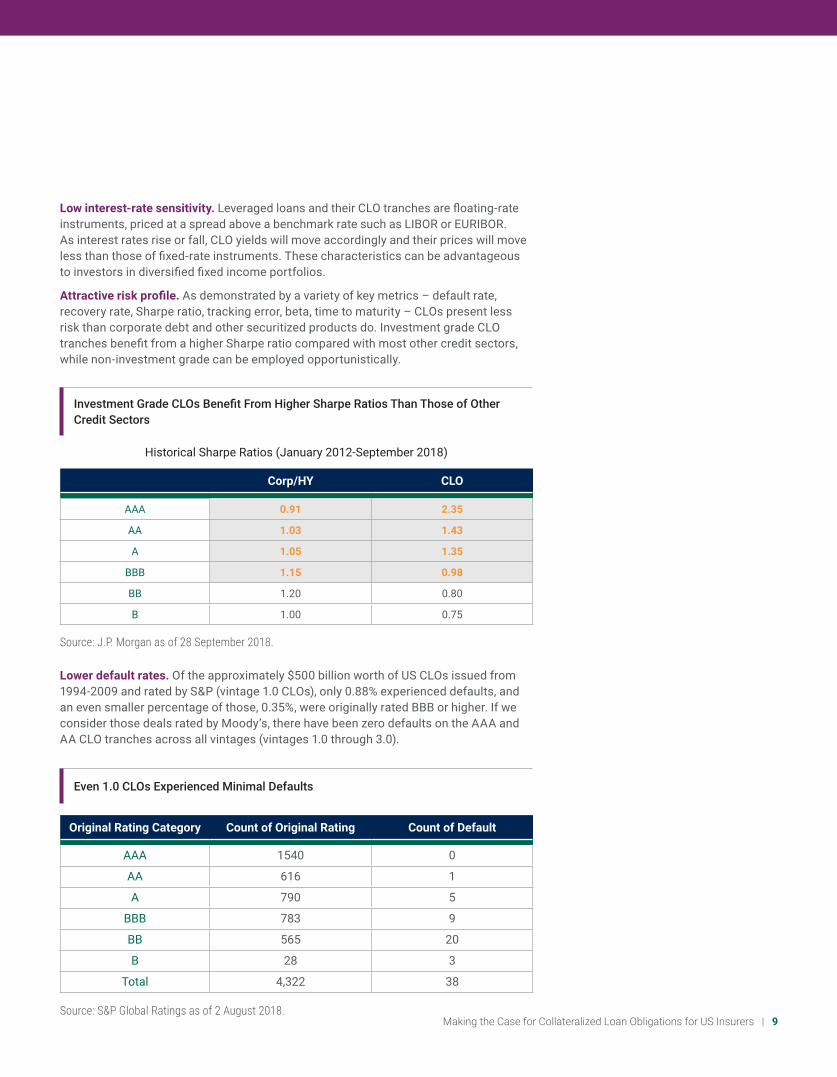

Attractive risk profile. As demonstrated by a variety of key metrics – default rate, recovery rate, Sharpe ratio, tracking error, beta, time to maturity – CLOs present less risk than corporate debt and other securitized products do. Investment grade CLO tranches benefit from a higher Sharpe ratio compared with most other credit sectors, while non-investment grade can be employed opportunistically.

Investment Grade CLOs Benefit From Higher Sharpe Ratios Than Those of Other Credit Sectors

Corp/HY CLO

AAA 0.91 2.35

AA 1.03 1.43

A 1.05 1.35

BBB 1.15 0.98

BB 1.20 0.80

B 1.00 0.75

Source: J.P. Morgan as of 28 September 2018.

Lower default rates. Of the approximately $500 billion worth of US CLOs issued from 1994-2009 and rated by S&P (vintage 1.0 CLOs), only 0.88% experienced defaults, and an even smaller percentage of those, 0.35%, were originally rated BBB or higher. If we consider those deals rated by Moody’s, there have been zero defaults on the AAA and AA CLO tranches across all vintages (vintages 1.0 through 3.0).

Source: S&P Global Ratings as of 2 August 2018.

Even 1.0 CLOs Experienced Minimal Defaults

Original Rating Category Count of Original Rating Count of Default

AAA 1540 0

AA 616 1

A 790 5

BBB 783 9

BB 565 20

B 28 3

Total 4,322 38

Historical Sharpe Ratios (January 2012-September 2018)

10 | PineBridge Investments

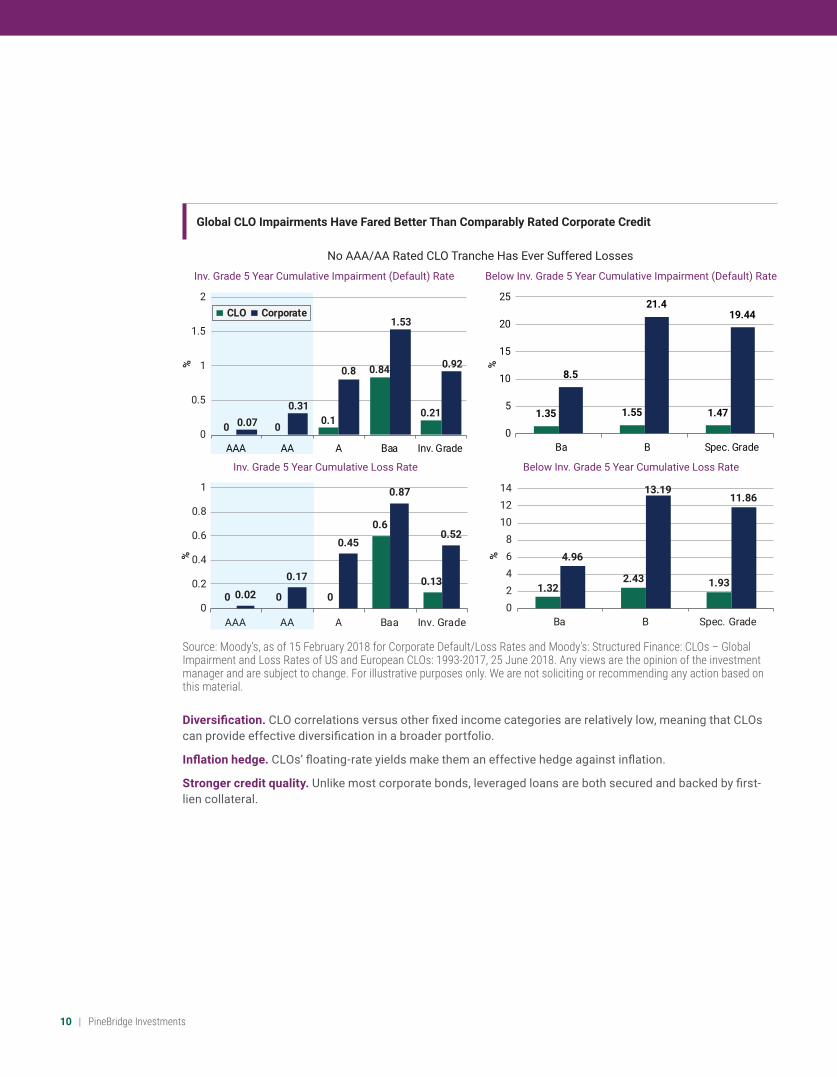

Diversification. CLO correlations versus other fixed income categories are relatively low, meaning that CLOs can provide effective diversification in a broader portfolio.

Inflation hedge. CLOs’ floating-rate yields make them an effective hedge against inflation.

Stronger credit quality. Unlike most corporate bonds, leveraged loans are both secured and backed by first-lien collateral.

Global CLO Impairments Have Fared Better Than Comparably Rated Corporate Credit

No AAA/AA Rated CLO Tranche Has Ever Suffered Losses

0 0 0.1

0.84

0.210.07

0.31

0.8

1.53

0.92

0

0.5

1

1.5

2

AAA AA A Baa Inv. Grade

%

Inv. Grade 5 Year Cumulative Impairment (Default) Rate

Inv. Grade 5 Year Cumulative Loss Rate

Below Inv. Grade 5 Year Cumulative Impairment (Default) Rate

Below Inv. Grade 5 Year Cumulative Loss Rate

1.35 1.55 1.47

8.5

21.419.44

0

5

10

15

20

25

Ba B Spec. Grade

%

0 0 0

0.6

0.130.02

0.17

0.45

0.87

0.52

0

0.2

0.4

0.6

0.8

1

AAA AA A Baa Inv. Grade

% %

1.322.43 1.93

4.96

13.1911.86

02468

101214

Ba B Spec. Grade

CLO Corporate

Source: Moody’s, as of 15 February 2018 for Corporate Default/Loss Rates and Moody’s: Structured Finance: CLOs – Global Impairment and Loss Rates of US and European CLOs: 1993-2017, 25 June 2018. Any views are the opinion of the investment manager and are subject to change. For illustrative purposes only. We are not soliciting or recommending any action based on this material.

Making the Case for Collateralized Loan Obligations for US Insurers | 11

…and important risks to considerThe complexity of CLOs comes with a number of risks that investors should consider carefully.

Credit strength. While CLOs enjoy strong credit quality due to the senior secured status of leveraged loans, it’s important to keep in mind that leveraged loans carry inherent credit risk: They’re issued to below-investment-grade companies whose fortunes are sensitive to fluctuations in the economic cycle.

Collateral deterioration. If a CLO’s loans experience losses, cash flows are allocated to tranches in order of seniority. Depending on the severity of the losses, the value of the equity tranche could be wiped out and junior loan tranches could lose principal.

Nonrecourse and not guaranteed. Leveraged loans are senior obligations and, as such, have full recourse to the borrower and its assets in the event of default. A CLO, however, has recourse only to the principal and interest payments of the loans in the portfolio.

Loan prepayments. Leveraged loan borrowers may choose to prepay their loans in pieces or completely. While experienced CLO managers may anticipate prepayments, they’re nonetheless unpredictable. The size, timing, and frequency of prepayments could potentially disrupt cash flows and challenge managers’ ability to maximize portfolio value.

Trading liquidity. CLOs generally enjoy healthy trading liquidity – but that could change very quickly if market conditions turn. A prime example is the financial crisis, when trading activity for even the most liquid debt instruments slowed to a trickle.

Timing of issuance. While market conditions could be strong when a CLO is issued, they might not be during its reinvestment period. That’s what happened to the 2003 vintages, whose reinvestment period coincided with the onset of the financial crisis and its resulting drop-off in trading volume.

Manager selection. Historical performance of CLO managers encompasses a wide spectrum of returns, underscoring the importance of choosing seasoned managers with solid long-term track records.

Spread duration. While interest rate duration is low due to the floating-rate nature of CLO tranches (indexed off three-month LIBOR), spread duration is a consideration that should be taken into account. Due to a typical reinvestment period of four to five years, spread duration is usually between 3.5 and seven years. The higher up the capital stack, the lower the spread duration as each CLO is redeemed sequentially, making the lower rated tranches longer in spread duration.

12 | PineBridge Investments

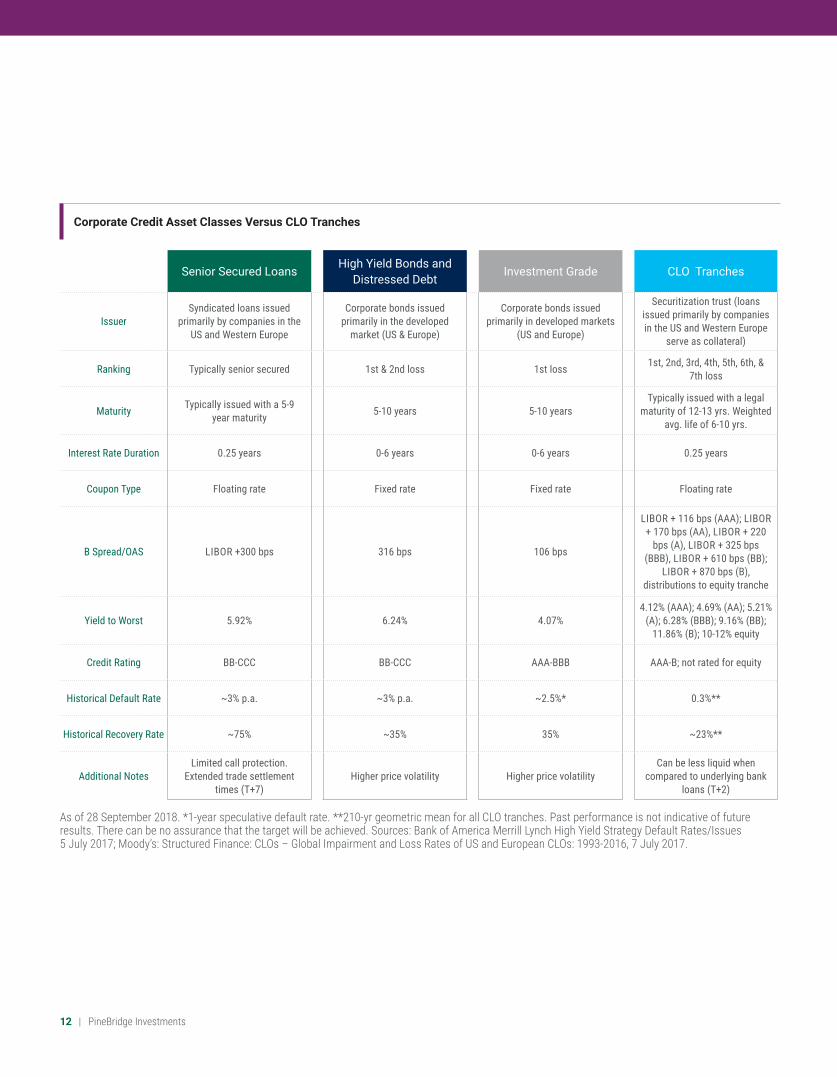

Senior Secured LoansHigh Yield Bonds and

Distressed DebtInvestment Grade CLO Tranches

IssuerSyndicated loans issued

primarily by companies in the US and Western Europe

Corporate bonds issued primarily in the developed

market (US & Europe)

Corporate bonds issued primarily in developed markets

(US and Europe)

Securitization trust (loans issued primarily by companies in the US and Western Europe

serve as collateral)

Ranking Typically senior secured 1st & 2nd loss 1st loss 1st, 2nd, 3rd, 4th, 5th, 6th, & 7th loss

Maturity Typically issued with a 5-9 year maturity 5-10 years 5-10 years

Typically issued with a legal maturity of 12-13 yrs. Weighted

avg. life of 6-10 yrs.

Interest Rate Duration 0.25 years 0-6 years 0-6 years 0.25 years

Coupon Type Floating rate Fixed rate Fixed rate Floating rate

B Spread/OAS LIBOR +300 bps 316 bps 106 bps

LIBOR + 116 bps (AAA); LIBOR + 170 bps (AA), LIBOR + 220

bps (A), LIBOR + 325 bps (BBB), LIBOR + 610 bps (BB);

LIBOR + 870 bps (B), distributions to equity tranche

Yield to Worst 5.92% 6.24% 4.07%4.12% (AAA); 4.69% (AA); 5.21%

(A); 6.28% (BBB); 9.16% (BB); 11.86% (B); 10-12% equity

Credit Rating BB-CCC BB-CCC AAA-BBB AAA-B; not rated for equity

Historical Default Rate ~3% p.a. ~3% p.a. ~2.5%* 0.3%**

Historical Recovery Rate ~75% ~35% 35% ~23%**

Additional NotesLimited call protection.

Extended trade settlement times (T+7)

Higher price volatility Higher price volatilityCan be less liquid when

compared to underlying bank loans (T+2)

Corporate Credit Asset Classes Versus CLO Tranches

As of 28 September 2018. *1-year speculative default rate. **210-yr geometric mean for all CLO tranches. Past performance is not indicative of future results. There can be no assurance that the target will be achieved. Sources: Bank of America Merrill Lynch High Yield Strategy Default Rates/Issues 5 July 2017; Moody’s: Structured Finance: CLOs – Global Impairment and Loss Rates of US and European CLOs: 1993-2016, 7 July 2017.

Making the Case for Collateralized Loan Obligations for US Insurers | 13

More regulation means less risk – and greater appeal to insurance investors In the wake of securitized investments’ difficulties during the financial crisis, US and European regulators took steps to mitigate CLOs’ structural risks – and made CLOs more attractive for investors.

Risk retention, commonly known as “skin in the game,” is a requirement in Europe. It holds that CLO managers must retain 5% of the original value of the assets in their CLOs to align their interests more closely with those of investors. The US required CLOs to be risk-retention compliant from December 2016 to May 2018. A court case brought by the LSTA reversed the decision, as it was deemed that CLO managers do not “originate” the loans, rather, they buy them. As a result, risk retention is no longer required for US CLO issuers.

A prominent US regulatory development was the implementation of the Volcker Rule, which became effective in 2014. To be in compliance, most vintage 2.0 CLOs issued starting in 2014 are collateralized with loans only, and many 1.0 CLOs have been “Volckerized” to eliminate nonloan collateral (where previously, CLOs had 5%-10% exposure to bonds).

European regulation is concentrated in several rules governing the capital requirements for banks and insurance companies. European risk retention was implemented in 2010.

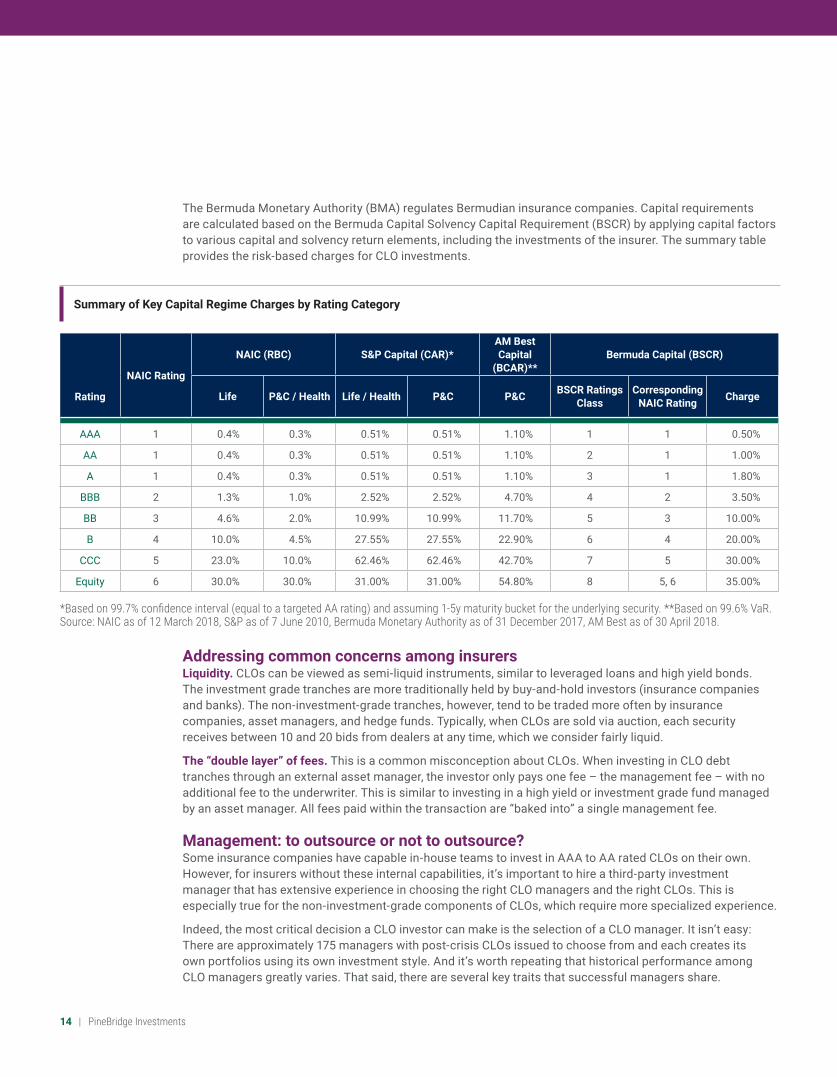

Insurance capital considerationsCapital is a key consideration when making any new investment decision and can play an important role in an insurer’s asset allocation decision. Here, we describe and provide the primary capital regimes relevant for a US- or Bermuda-domiciled insurer investing in CLOs.

The National Association of Insurance Commissioners’ (NAIC) Risk Based Capital (RBC) framework measures the minimum amount of capital required to support overall business operations. The capital charge for CLOs is decided by a combination of rating and carry value/amortized cost. The price at which the insurance company holds the bond influences the NAIC rating and hence the associated capital charge. The summary table shows the rating-based charges for CLOs.

The S&P Capital Adequacy Model seeks to capture the value of expected economic losses to a degree of certainty that is commensurate with the targeted rating category of the insurer. Confidence levels are established based on rating categories of AAA-BBB. The summary table shows CLO capital charges for a target rating of AA. These charges will differ based on different target ratings.

AM Best’s Capital Adequacy Ratio (BCAR) depicts the quantitative relationship between a rating unit’s balance sheet strength and key financial risks that could impact such strength. Net required capital, the capital needed to support such financial risks, is computed for different confidence intervals (VAR levels), resulting in BCAR scores for each of these levels. The capital charges applied to determine required capital will vary based on a number of factors, including credit risk and maturity of the underlying investments as well as the size of the insurer’s ratings exposures. The summary table shows a sample P&C rating unit’s investment risk charges.

14 | PineBridge Investments

Addressing common concerns among insurersLiquidity. CLOs can be viewed as semi-liquid instruments, similar to leveraged loans and high yield bonds. The investment grade tranches are more traditionally held by buy-and-hold investors (insurance companies and banks). The non-investment-grade tranches, however, tend to be traded more often by insurance companies, asset managers, and hedge funds. Typically, when CLOs are sold via auction, each security receives between 10 and 20 bids from dealers at any time, which we consider fairly liquid.

The “double layer” of fees. This is a common misconception about CLOs. When investing in CLO debt tranches through an external asset manager, the investor only pays one fee – the management fee – with no additional fee to the underwriter. This is similar to investing in a high yield or investment grade fund managed by an asset manager. All fees paid within the transaction are “baked into” a single management fee.

Management: to outsource or not to outsource?Some insurance companies have capable in-house teams to invest in AAA to AA rated CLOs on their own. However, for insurers without these internal capabilities, it’s important to hire a third-party investment manager that has extensive experience in choosing the right CLO managers and the right CLOs. This is especially true for the non-investment-grade components of CLOs, which require more specialized experience.

Indeed, the most critical decision a CLO investor can make is the selection of a CLO manager. It isn’t easy: There are approximately 175 managers with post-crisis CLOs issued to choose from and each creates its own portfolios using its own investment style. And it’s worth repeating that historical performance among CLO managers greatly varies. That said, there are several key traits that successful managers share.

NAIC Rating

NAIC (RBC) S&P Capital (CAR)*AM Best Capital

(BCAR)**Bermuda Capital (BSCR)

Rating Life P&C / Health Life / Health P&C P&C BSCR Ratings Class

Corresponding NAIC Rating Charge

AAA 1 0.4% 0.3% 0.51% 0.51% 1.10% 1 1 0.50%

AA 1 0.4% 0.3% 0.51% 0.51% 1.10% 2 1 1.00%

A 1 0.4% 0.3% 0.51% 0.51% 1.10% 3 1 1.80%

BBB 2 1.3% 1.0% 2.52% 2.52% 4.70% 4 2 3.50%

BB 3 4.6% 2.0% 10.99% 10.99% 11.70% 5 3 10.00%

B 4 10.0% 4.5% 27.55% 27.55% 22.90% 6 4 20.00%

CCC 5 23.0% 10.0% 62.46% 62.46% 42.70% 7 5 30.00%

Equity 6 30.0% 30.0% 31.00% 31.00% 54.80% 8 5, 6 35.00%

Summary of Key Capital Regime Charges by Rating Category

*Based on 99.7% confidence interval (equal to a targeted AA rating) and assuming 1-5y maturity bucket for the underlying security. **Based on 99.6% VaR. Source: NAIC as of 12 March 2018, S&P as of 7 June 2010, Bermuda Monetary Authority as of 31 December 2017, AM Best as of 30 April 2018.

The Bermuda Monetary Authority (BMA) regulates Bermudian insurance companies. Capital requirements are calculated based on the Bermuda Capital Solvency Capital Requirement (BSCR) by applying capital factors to various capital and solvency return elements, including the investments of the insurer. The summary table provides the risk-based charges for CLO investments.

Everything flows from experience

There’s no substitute for deep CLO management experience, which provides the combination of skills, practice, tactical, and strategic savvy, adjustment-making, and chronological perspective needed to generate strong returns in such a complicated asset class.

Chronological perspective may be the most important aspect of experience in the CLO world, as the benefit of having managed portfolios before, during, and after the financial crisis is incalculable.

Excellence of execution

Managers must excel in the vital competencies that collectively define best-practice portfolio management. These begin with loan selection, as creating a strong collateral base lays the foundation for potential success. Trading skill enables the manager to know when to take gains, avoid losses, and adjust the portfolio as market conditions evolve. Effective management of deteriorating credits affects not just the specific credits involved, but also the entire CLO due to the way cash flows are distributed through the tranche structure. And the reinvestment of principal proceeds in new collateral can make the difference between good and great performance.

A knack for handling risk

Sound risk management is both a cause and effect of these best practices: It informs everything the manager does and is reflected in the results. In addition to oversight of the portfolio, it includes skillful execution of coverage tests; the ability to understand the nuances and idiosyncrasies of CLO documentation, which is nonstandard and complex; and a talent for balancing the numerous portfolio metrics by optimizing as many as possible while taking a hit on as few as possible.

Insurers may also want to consider an investment manager that has an in-house bank loan team available to perform collateral analysis and other research and due diligence on the underlying loans.

Notes1 Source: National Association of Insurance Commissioners (NAIC) Capital Markets Bureau,

“U.S. Insurance Industry Exposure to Collateralized Loan Obligations Update as of Year-End 2017,” 27 September 2018

2 Source: Bank of America Merrill Lynch, “US CLO September Chartbook,” 4 October 2018 3 Source: NAIC Capital Markets Bureau, Collateralized Loan Obligations (CLOs) Primer4 Source: Wells Fargo Research 2 October 20185 Source: Bank of America Merrill Lynch, “An introduction to the US CLO Market,” 9 August 20186 Source: NAIC report 27 September 20187 Source: Wells Fargo Structured Products Research Asset Allocator Q2 Update, 30 August 20188 The income generated by underlying pool of loans must be greater than the interest due on the

outstanding debt in the CLO.9 The principal amount of underlying pool of loans must be greater than the principal amount of

outstanding CLO tranches.

PineBridge has a long history in CLOsPineBridge Investments has extensive experience in leveraged finance not only as a manager, but also as an issuer: Starting in 1999, we’ve issued over 35 CLOs in the US and Europe, with a par value of more than $13 billion. Our team of professionals includes senior leadership that has been in place for nearly 20 years, as well as credit analysts, most of whom have been with us for at least 10 years. We are differentiated by an experienced team that has been serving the insurance industry across a variety of niche fixed income asset classes.

In fixed income, our multi-billion dollar portfolio is invested across the spectrum of developed and emerging markets, investment grade debt, leveraged finance, and multi-sector strategies. Our investment process is informed by rigorous, proprietary credit analysis across sectors and regions.

Investing involves risk, including possible loss of principal. This information represents a general assessment of the markets at a specific time and is not a guarantee of future performance results or market movement. This material does not constitute investment, financial, legal, tax, or other advice; investment research or a product of any research department; an offer to sell, or the solicitation of an offer to purchase any security or interest in a fund; or a recommendation for any investment product or strategy. PineBridge Investments is not soliciting or recommending any action based on information in this document. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author, may differ from the views or opinions expressed by other areas of PineBridge Investments, and are only for general informational purposes as of the date indicated. Views may be based on third-party data that has not been independently verified. PineBridge Investments does not approve of or endorse any republication of this material.

Disclosure Statement PineBridge Investments is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. PineBridge Investments is a registered trademark proprietary to PineBridge Investments IP Holding Company Limited.

For purposes of complying with the Global Investment Performance Standards (GIPS®), the firm is defined as PineBridge Investments Global. Under the firm definition for the purposes of GIPS, PineBridge Investments Global excludes some alternative asset groups and regional legal entities that may be represented in this presentation, such as the assets of PineBridge Investments.

Readership: This document is intended solely for the addressee(s) and may not be redistributed without the prior permission of PineBridge Investments. Its content may be confidential, proprietary, and/or trade secret information. PineBridge Investments and its subsidiaries are not responsible for any unlawful distribution of this document to any third parties, in whole or in part.

Opinions: Any opinions expressed in this document represent the views of the manager, are valid only as of the date indicated, and are subject to change without notice. There can be no guarantee that any of the opinions expressed in this document or any underlying position will be maintained at the time of this presentation or thereafter. We are not soliciting or recommending any action based on this material.

Risk Warning: All investments involve risk, including possible loss of principal. Past performance is not indicative of future results. If applicable, the offering document should be read for further details including the risk factors. Our investment management services relate to a variety of investments, each of which can fluctuate in value. The investment risks vary between different types of instruments. For example, for investments involving exposure to a currency other than that in which the portfolio is denominated, changes in the rate of exchange may cause the value of investments, and consequently the value of the portfolio, to go up or down. In the case of a higher volatility portfolio, the loss on realization or cancellation may be very high (including total loss

of investment), as the value of such an investment may fall suddenly and substantially. In making an investment decision, prospective investors must rely on their own examination of the merits and risks involved.

Performance Notes: Past performance is not indicative of future results. There can be no assurance that any investment objective will be met. PineBridge Investments often uses benchmarks for the purpose of comparison of results. Benchmarks are used for illustrative purposes only, and any such references should not be understood to mean there would necessarily be a correlation between investment returns of any investment and any benchmark. Any referenced benchmark does not reflect fees and expenses associated with the active management of an investment. PineBridge Investments may, from time to time, show the efficacy of its strategies or communicate general industry views via modeling. Such methods are intended to show only an expected range of possible investment outcomes, and should not be viewed as a guide to future performance. There is no assurance that any returns can be achieved, that the strategy will be successful or profitable for any investor, or that any industry views will come to pass. Actual investors may experience different results.

Information is unaudited unless otherwise indicated, and any information from third-party sources is believed to be reliable, but PineBridge Investments cannot guarantee its accuracy or completeness.

PineBridge Investments Europe Limited is authorised and regulated by the Financial Conduct Authority (FCA). In the UK this communication is a financial promotion solely intended for professional clients as defined in the FCA Handbook and has been approved by PineBridge Investments Europe Limited. Should you like to request a different classification, please contact your PineBridge representative.

Approved by PineBridge Investments Ireland Limited. This entity is authorised and regulated by the Central Bank of Ireland.

In Australia, PineBridge Investments LLC is exempt from the requirement to hold an Australian financial services license under the Corporations Act 2001 (Cth) in respect of the financial services it provides to wholesale clients, and is not licensed to provide financial services to individual investors or retail clients. Nothing herein constitutes an offer or solicitation to anyone in or outside Australia where such offer or solicitation is not authorised or to whom it is unlawful. This information is not directed to any person to whom its publication or availability is restricted.

In Hong Kong, the issuer of this document is PineBridge Investments Asia Limited, licensed and regulated by the Securities and Futures Commission (SFC). This document has not been reviewed by the SFC.

In Dubai, PineBridge Investments Europe Limited is regulated by the Dubai Financial Services Authority as a Representative Office.

PineBridge Investments Singapore Limited is licensed and regulated by the Monetary Authority of Singapore (MAS). In Singapore, this material may not be suitable to a retail investor and is not reviewed or endorsed by the MAS.

Last updated 6 March 2017.

PineBridge Investments is a private, global asset manager focused on active, high-conviction investing. We draw on the collective power of our experts in each discipline, market, and region of the world through an open culture of collaboration designed to identify the best ideas. Our mission is to exceed clients’ expectations on every level, every day. As of 30 September 2018, the firm managed US$91.4 billion across global asset classes for sophisticated investors around the world.

MULTI-ASSET | FIXED INCOME | EQUITIES | ALTERNATIVES

About PineBridge

Investments

pinebridge.com