SECURITIES AND EXCHANGE COMMISSION · P I O N E E R C O R M A D I S O N S T R E E T S , M A ......

93

G L O B E T E L E C O M , I N C . 5 / F G L O B E T E L E C O M P L A Z A P I O N E E R C O R M A D I S O N S T R E E T S , M A N D A L U Y O N G C I T Y 1 2 3 1 1 7 Q 0 4 1 2 Dept. Requiring this Doc. Total No. Of Stockholders Remarks = pls. Use black ink for scanning purposes Document I.D. Cashie S T A M P S 730-2742 To be accomplished by SEC Personnel concerned LC File Amended Articles Number/Section Total Amount of Borrowings Domesti Foreig Fiscal Year Annual Meeting Secondary License Type, if Applicable Month Day Day Month FORM (Business Address: No. Street City / Town / Province) Contact Person Company Telephone Number COVER SHEET (Company's Full Name) ALBERTO M. DE LARRAZABAL P W 0 0 0 0 1 1 7 7

Transcript of SECURITIES AND EXCHANGE COMMISSION · P I O N E E R C O R M A D I S O N S T R E E T S , M A ......

G L

MA. CARIDAD D. GONZALES

O B E T E L E C O M , I N C .

5 / F G L O B E T E L E C O M P L A Z A

P I O N E E R C O R M A D I S O N S T R E E T S ,

M A N D A L U Y O N G C I T Y

1 2 3 1 1 7 Q 0 4 1 2

Dept. Requiring this Doc.

Total No. Of Stockholders

Remarks = pls. Use black ink for scanning purposes

Document I.D. Cashie

S T A M P S

730-2742

To be accomplished by SEC Personnel concerned

LCFile

Amended Articles Number/Section

Total Amount of Borrowings

Domesti Foreig

Fiscal Year Annual Meeting

Secondary License Type, if Applicable

Month Day DayMonth FORM

(Business Address: No. Street City / Town / Province)

Contact Person Company Telephone Number

COVER SHEET

(Company's Full Name)

ALBERTO M. DE LARRAZABAL

P W 0 0 0 0 1 1 7 7

SEC Number 1177 File Number ____

GLOBE TELECOM, INC. (Company’s Full Name)

5th Floor Globe Telecom Plaza (Pioneer Highlands) Pioneer corner Madison Streets, 1552 Mandaluyong City

(Company’s Address)

(632) 730-2000 (Telephone Numbers)

31 March 2011 (Quarter Ending)

SEC FORM 17-Q (Form Type)

SECURITIES AND EXCHANGE COMMISSION

SEC FORM 17-Q

QUARTERLY REPORT PURSUANT TO SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17(2)(b) THEREUNDER

1. For the three months ended 31 March 2011 2. Commission identification number: 1177 3. BIR Tax Identification No. 000-768-480-000 4. Exact name of registrant as specified in its charter: GLOBE TELECOM, INC. 5. Province, country or other jurisdiction of incorporation or organization: PHILIPPINES 6. Industry Classification Code: (SEC Use Only) 7. Address of registrant’s principal office: 5th Floor, Globe Telecom Plaza (Pioneer Highlands) Pioneer corner Madison Streets 1552 Mandaluyong City 8. Registrant’s telephone number, including area code: (632) 730-2000 9. Former name, former address and former fiscal year, if changed since last report: N / A 10. Securities registered pursuant to Sections in Securities Regulation Code Number of shares of stock Title of each class outstanding Common Stock, P50.00 par value 132,348,473 Preferred Stock, P5.00 par value 158,515,021 11. Are any or all of the Securities listed on the Philippine Stock Exchange? Yes 12. Indicate whether the registrant:

a) Has filed all reports required to be filed by Section 17 of the Code and SRC Rule 17 thereunder or Sections 11 of the SRC and SRC Rule 11(a)-1 thereunder, and Sections 26 and 141 of the Corporation Code of the Philippines, during the preceding 12 months (or for such shorter period the registrant was required to file such reports). Yes

b) Has been subject to such filing requirements for the past 90 days. Yes

SEC Form 17Q – 1Q 2011 2

SEC Form 17Q – 1Q 2011 3

GLOBE TELECOM, INC. AND SUBSIDIARIES

MANAGEMENT’S DISCUSSION AND ANALYSIS

OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

FOR THE THREE MONTHS ENDED

31 MARCH 2011

SEC Form 17Q – 1Q 2011 4

PART I FINANCIAL INFORMATION ITEM 1. FINANCIAL STATEMENTS Our unaudited condensed consolidated financial statements include the accounts of Globe Telecom, Inc. and its wholly owned subsidiaries, Innove Communications, Inc.(Innove), G-Xchange, Inc. (GXI), Entertainment Gateway Group (EGG Group) and GTI Business Holdings, Inc. (GTI BH), collectively referred to as the “Globe Group” in this report. The unaudited condensed consolidated financial statements for the three months ended 31 March 2011 (filed as Annex 1 of this report) have been prepared in accordance with Philippine Accounting Standard 34, Interim Financial Reporting, hence, do not include all of the information required in the December 31, 2011 annual audited financial statements. ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS (MD&A) OF FINANCIAL

CONDITION AND RESULTS OF OPERATIONS The following is a discussion and analysis of Globe Group’s financial performance for the three months ended 31 March 2011. The prime objective of this MD&A is to help the readers understand the dynamics of the Company’s business and the key factors underlying its financial results. Hence, Globe’s MD&A is comprised of a discussion of its core business, and analysis of the results of operations for each business segment. This section also focuses on key statistics from the audited consolidated financial statements and pertains to known risks and uncertainties relating to the telecommunications industry in the Philippines where we operate up to the stated reporting period. However, Globe’s MD&A should not be considered all inclusive, as it excludes unknown risks, uncertainties and changes that may occur in the general economic, political and environmental condition after the stated reporting period. The Globe Group has adopted an expanded corporate governance approach in managing its business risks. An Enterprise Risk Management Policy was developed to systematically view the risks and to manage these risks in the context of the normal business processes such as strategic planning, business planning, operational and support processes. The Company’s MD&A should be read in conjunction with its unaudited consolidated financial statements and the accompanying notes. All financial information is reported in Philippine Pesos (Php) unless otherwise stated. Any references in this MD&A to “we”, “us”, “our”, “Company” means the Globe Group and references to “Globe” mean Globe Telecom, Inc., not including its wholly-owned subsidiaries. Additional information about the Company, including annual and quarterly reports, can be found on our corporate website www.globe.com.ph.

SEC Form 17Q – 1Q 2011 5

The following is a summary of the key sections of this MD&A:

OVERVIEW OF OUR BUSINESS_________________________________________ 6

FINANCIAL AND OPERATIONAL RESULTS _____________________________ 14 GROUP FINANCIAL SUMMARY ___________________________________________ 14 GROUP OPERATING REVENUES __________________________________________ 16 GROUP OPERATING EXPENSES ___________________________________________ 29 LIQUIDITY AND CAPITAL RESOURCES____________________________________ 32 FINANCIAL RISK MANAGEMENT _________________________________________ 36

LEGAL, REGULATORY AND CORPORATE DEVELOPMENTS______________ 40

SEC Form 17Q – 1Q 2011 6

OVERVIEW OF OUR BUSINESS Globe Telecom, Inc. is a major provider of telecommunications services in the Philippines, supported by over 5,700 employees and over 760,000 retailers, distributors, suppliers, and business partners nationwide. The Company operates one of the largest and most technologically-advanced mobile, fixed line and broadband networks in the country, providing reliable, superior communications services to individual customers, small and medium-sized businesses, and corporate and enterprise clients. Globe currently has over 27 million mobile subscribers, over 1,180,000 broadband customers, and over 600,000 landline subscribers. Globe is also one of the largest and most profitable companies in the country, and has been consistently recognized both locally and internationally for its corporate governance practices. It is listed on the Philippine Stock Exchange under the ticker symbol GLO and had a market capitalization of US$2.7 billion as of the end of March 2011. The Company’s principal shareholders are Ayala Corporation and Singapore Telecom, both industry leaders in their respective countries. Aside from providing financial support, this partnership has created various synergies and has enabled the sharing of best practices in the areas of purchasing, technical operations, and marketing, among others. Globe is committed to being a responsible corporate citizen. Globe BridgeCom, the company’s umbrella corporate social responsibility program, leads and supports various initiatives that (1) promote education and raise the level of computer literacy in the country, (2) support entrepreneurship and micro-enterprise development particularly in the countryside, and (3) ensures sustainable development through protection of the environment and excellence in operations. Since its inception in 2003, Globe BridgeCom has made a positive impact on the lives of thousands of public elementary and high school students, teachers, community leaders, and micro-entrepreneurs throughout the country. For its efforts, Globe BridgeCom has been recognized and conferred several awards and citations by various Philippine and international organizations.

SEC Form 17Q – 1Q 2011 7

The Globe Group is composed of the following companies:

• Globe Telecom, Inc. (Globe) provides mobile telecommunications services;

• Innove Communications Inc. (Innove), a wholly-owned subsidiary, provides fixed line telecommunications and broadband services, high-speed internet and private data networks for enterprise clients, services for internal applications, internet protocol-based solutions and multimedia content delivery;

• G-Xchange, Inc. (GXI), a wholly-owned subsidiary, provides mobile commerce

services under the GCash brand;

• Entertainment Gateway Group Corp. and EGGstreme (Hong Kong) Limited (EHL) (collectively referred here as EGG Group), provide digital media content and applications; and

• GTI Business Holdings, Inc. (GTI), a wholly-owned subsidiary, is an investment

company with authority to provide VOIP services. The Company is a grantee of various authorizations and licenses from the National Telecommunications Commission (NTC) as follows: (1) license to offer and operate facsimile, other traditional voice and data services and domestic line service using Very Small Aperture Terminal (VSAT) technology; (2) license for inter-exchange services; and (3) Certificate of Public Convenience and Necessity (CPCN) for: (a) international digital gateway facility (IGF) in Metro Manila, (b) nationwide digital cellular mobile telephone system under the GSM standard (CMTS-GSM), (c) nationwide local exchange carrier (LEC) services after being granted a provisional authority in June 2005, and (d) international cable landing stations located in Nasugbu, Batangas and Ballesteros, Cagayan. Business Segments Mobile Business Globe provides digital mobile communication services nationwide using a fully digital network based on the Global System for Mobile Communication (GSM) technology. It provides voice, data and value-added services to its mobile subscribers through three major brands: Globe Postpaid, Globe Prepaid and TM. Globe Postpaid includes all postpaid plans such as regular G-Plans, consumable G-Flex Plans, Load Allowance Plans, Load Tipid, Apple TM iPhone 3G plans and high-end Platinum Plans. In 2010, the Company further expanded its postpaid offerings to include MY SUPERPLAN and MY FULLY LOADED PLAN which allow subscribers to personalize their plans, choose and combine various unlimited call, text and web browsing service options. , In addition to these personalized plans, Globe has made available a various add-on roaming and mobile browsing plans to cater to the needs of its subscribers. Globe Prepaid and TM are the prepaid brands of Globe. Globe Prepaid is targeted towards the adult, mainstream market. Its unique brand proposition revolves around its innovative product

SEC Form 17Q – 1Q 2011 8

and service offerings, superior customer service, and Globe’s “worldwidest” services and global network reach. TM, on the other hand, caters to the value-conscious segment of the market. In addition to digital wireless communications, Globe also offers mobile payments and remittance services under the GCash brand. GCash is an internationally acclaimed micro payment service that transforms a mobile phone into a virtual wallet, enabling secure, fast, and convenient money transfers at the speed and cost of a text message. Since the launch of GCash, wholly-owned subsidiary GXI has established a wide network of local and international partners that includes government agencies, utility companies, cooperatives, insurance companies, remittance companies, universities, and commercial establishments which have agreed to accept GCash as a means of payment for products and services. Globe offers various top-up or reloading options and facilities for prepaid subscribers including prepaid call and text cards, bank channels such as ATMs, credit cards, and through internet banking. Subscribers can also top-up at over 760,000 AutoLoad Max retailers nationwide, all at affordable denominations and increments. A consumer-to-consumer top-up facility, Share-A-Load, is also available to enable subscribers to share prepaid load credits via SMS. Globe’s AutoLoad Max and Share-A-Load services are also available in selected OFW hubs all over the world. In 2010, the Company launched a loyalty and rewards program called My Rewards, My Globe for Globe Prepaid subscribers and TM Astig Rewards for TM subscribers. Under the program, and based on a defined scoring system, prepaid subscribers earn points based on tenure and reload. Subscribers can use their points to redeem rewards including Globe and TM products, travel mileage, and gift certificates from leading retail establishments. Globe Postpaid subscribers outside the lock-up period can also earn points based on their monthly billed amounts and length of stay with Globe. Rewards also include Globe products, as well as bill rebates, gadgets, gift certificates, and travel mileage. Subscribers have the option to redeem rewards instantly, or accumulate points to avail of higher-value rewards. Redeemed points in a form of telecom services is netted out against revenues whereas points redeemed in a form of non-telco services such as gift certificates and other products are reflected as marketing expense. At the end of each period, Globe estimates and records the amount of probable future liability for unredeemed points.

1. Mobile Voice

Globe’s voice services include local, national and international long distance call services. It has one of the most extensive local calling options designed for multiple calling profiles. In addition to its standard, pay-per-use rates, subscribers can choose from bulk and unlimited voice offerings for all-day or off-peak use, and in several denominations to suit different budgets.

Globe pioneered international roaming in 1995 and now has one of the widest networks with over 600 roaming partners in more than 200 calling destinations worldwide. Globe also offers roaming coverage on-board selected shipping lines, airlines and via satellite. Through its Globe Kababayan program, Globe provides an extensive range of international call and text services to allow OFWs (Overseas Filipino Workers) to stay connected with their friends and families in the Philippines. This includes prepaid and

SEC Form 17Q – 1Q 2011 9

reloadable call cards and electronic PINs available in popular OFW destinations worldwide.

2. Mobile Data and Value-Added Services

Globe’s data services include local and international SMS offerings, mobile browsing and content downloads. Globe also offers various bucket and unlimited SMS packages to cater to the different needs and lifestyles of its postpaid and prepaid subscribers. Additionally, Globe subscribers can send and receive Multimedia Messaging Service (MMS) pictures and video, or do local and international 3G video calling. Globe’s mobile browsing services allow subscribers to access the internet using their internet-capable handsets or laptops with USB modems. Data access can be made using various technologies including HSPA, 3G with HSDPA, EDGE and GPRS. Browsing subscribers also have multiple charging options available with Globe’s Flexible Mobile Internet Browsing rates which allow subscribers to choose between time or usage-based rates. They can also choose between daily or monthly browsing plans. The Company offers a full range of downloadable content covering multiple topics including news, information, and entertainment through its web portal. Subscribers can purchase or download music, movie pictures and wallpapers, games, mobile advertising, applications or watch clips of popular TV shows and documentaries as well as participate in interactive TV, mobile chat and play games, among others. Through Globe’s partnership with major banks and remittance companies, and using Globe’s pioneering GCash platform, subscribers can perform mobile banking and mobile commerce transactions. Globe subscribers can complete international and domestic remittance transactions, pay fees, utility bills and income taxes, avail of micro-finance transactions, donate to charitable institutions, and buy Globe prepaid load credits using its GCash-activated SIM.

Fixed Line and Broadband Business

Globe offers a full range of fixed line communications services, wired and wireless broadband access, and end-to-end connectivity solutions customized for consumers, SMEs (Small & Medium Enterprises), large corporations and businesses. To better serve the various needs of its customers, Globe organized dedicated customer facing units (CFUs) within the Company to focus on the integrated mobile and fixed line needs of specific market segments. The Company has a Consumer Business unit with dedicated marketing and sales groups to address the needs of retail customers, and a Business CFU (Globe Business) focused on the needs of big and small businesses. Globe Business provides end-to-end mobile and fixed line solutions and is equipped with its own technical and customer relationship teams to serve the requirements of its client base.

SEC Form 17Q – 1Q 2011 10

1. Fixed Line Voice

Globe’s fixed line voice services include local, national and international long distance calling services in postpaid and prepaid packages through its Globelines brand. Subscribers get to enjoy toll-free rates for national long distance calls with other Globelines subscribers nationwide. Additionally, postpaid fixed line voice consumers enjoy free unlimited dial-up internet from their Globelines subscriptions. Low-MSF (monthly service fee) and fixed lines bundled with internet plans are available nationwide and can be customized with value-added services including multi-calling, call waiting and forwarding, special numbers and voice mail. For corporate and enterprise customers, Globe offers voice solutions that include regular and premium conferencing, enhanced voice mail, IP-PBX solutions and domestic or international toll free services.

2. Fixed Line Data

Fixed line data services include end-to-end data solutions customized according to the needs of businesses. Globe’s product offerings include international and domestic data services, wholesale and corporate internet access, data center services and segment-specific solutions tailored to the needs of specific industries. Globe’s international data services provide its corporate and enterprise customers with the most diverse international connectivity solutions. Globe’s extensive data network allow customers to manage their own virtual private networks (VPN), subscribe to wholesale internet access via managed international private leased lines (IPL), run various applications, and access other networks with integrated voice services over high-speed, redundant and reliable connections. In addition to bandwidth access from multiple international submarine cable operators, Globe also has two international cable landing stations situated in different locales to ensure redundancy and network resiliency.

The Company’s domestic data services include data center solutions such as business continuity and data recovery services, 24x7 monitoring and management, dedicated server hosting, maintenance for application-hosting, managed space and carrier-class facilities for co-location requirements and dedicated hardware from leading partner vendors for off-site deployment. Other fixed line data services include access services that deliver premium-grade access solutions combining voice, broadband and video offerings designed to address specific connectivity requirements. These include Broadband Internet Zones (BIZ) for broadband-to-room internet access for hotels, and Internet Exchange (GiX) services for bandwidth-on-demand access packages based on average usage.

3. Broadband

Globe offers wired, fixed wireless, and fully mobile internet-on-the-go services across various technologies and connectivity speeds for its residential and business customers. Wired or DSL broadband packages bundled with voice, or broadband data-only services are available at download speeds ranging from 256 kbps up to 3 mbps. In selected areas where DSL is not yet available, Globe offers a fixed wireless broadband service using its WiMAX network. Meanwhile, for consumers who require a fully mobile, internet-on-the-go broadband connection, Globe Broadband Tattoo allows subscribers to access the

SEC Form 17Q – 1Q 2011 11

internet at speeds of up to 2 mbps using 3G with HSDPA, EDGE, GPRS or Wi-Fi at various hotspots nationwide using a plug-and-play USB modem. This service is available in both postpaid and prepaid packages. In addition, consumers in selected urban areas who require faster connections have the option to subscribe to Globe’s Hyper Speed broadband plans using leading edge GPON (Gigabit Passive Optical Network) technology with speeds of up to 100 mbps.

SEC Form 17Q – 1Q 2011 12

KEY PERFORMANCE INDICATORS Globe is committed to enhancing shareholder value and to efficiently manage the Company’s resources. The Company regularly reviews its performance against its operating and financial plans and strategies, and use key performance indicators to monitor its progress. Some of its key performance indicators are set out below. Except for Net Income, these key performance indicators are not measurements in accordance with Philippine Financial Reporting Standards (PFRS) and should not be considered as an alternative to net income or any other measure of performance which are in accordance with PFRS. GROSS AVERAGE REVENUE PER UNIT (GROSS ARPU) Gross ARPU measures the average monthly gross revenue generated for each subscriber. This is computed by dividing recurring gross service revenues for a business segment for the period by the average number of the segment’s subscribers and then dividing the quotient by the number of months in the period. NET AVERAGE REVENUE PER UNIT (NET ARPU) Net ARPU measures the average monthly net revenue generated for each subscriber. This is computed by dividing recurring net service revenues of the segment for the period (net of discounts and interconnection charges to external carriers and content provider revenue share) by the average number of the segment’s subscribers and then dividing the quotient by the number of months in the period. SUBSCRIBER ACQUISITION COST (SAC) SAC is computed by totaling marketing costs (including commissions and handset/SIM subsidies1 ) related to the acquisition programs for the segment for the period divided by the gross incremental subscribers. AVERAGE MONTHLY CHURN RATE The average monthly churn rate is computed by dividing total disconnections (net of reconnections) for the segment by the average number of the segment’s subscribers, and then divided by the number of months in the period. This is a measure of the average number of customers who leave/switch/change to another type of service or to another service provider and is usually stated as a percentage. EBITDA EBITDA (Earnings before Interest, Taxes, Depreciation and Amortization) is calculated as service revenues less subsidy1, operating expenses and other income and expenses2. This measure provides useful information regarding a company’s ability to generate cash flows, incur and service debt, finance capital expenditures and working capital changes. As the Company’s method of calculating EBITDA may differ from other companies, it may not be comparable to similarly titled measures presented by other companies.

1 Computed as non-service revenues less cost of sales, mostly on sale of handsets/SIM packs, accessories & gadgets 2 Operating expenses do not include any property and equipment-related gains and losses and financing costs

SEC Form 17Q – 1Q 2011 13

EBITDA MARGIN EBITDA margin is calculated as EBITDA divided by total service revenues. Total service revenue is equal to total net operating revenue less non-service revenue. This is useful in measuring the extent to which subsidies and operating expenses (excluding property and equipment-related gains and losses and financing costs), use up revenue. EBIT and EBIT MARGIN EBIT is defined as earnings before interest, property and equipment-related gains and losses and income taxes. This measure is calculated by deducting depreciation and amortization from EBITDA. Globe Group’s method of calculating EBIT may differ from other companies, hence, may not be comparable to similar measures presented by other companies. EBIT margin is calculated as EBIT divided by total service revenues. NET INCOME As presented in the unaudited condensed consolidated financial statements for applicable periods, net income provides an indication of how well the Company performed after all costs of the business have been factored in.

SEC Form 17Q – 1Q 2011 14

FINANCIAL AND OPERATIONAL RESULTS GROUP FINANCIAL SUMMARY

Globe Group

Quarter on Quarter Year on Year 1Q 4Q* QoQ 1Q 1Q YoY

Change Change Results of Operations (Php Mn)

2011 2010 (%)

2011 2010 (%)

Net Operating Revenues ………………. 17,469 17,106 2% 17,469 15,841 10% Service Revenues...……………........ 16,452 16,214 1% 16,452 15,231 8% Non-Service Revenues……………... 1,017 892 14% 1,017 610 67%

Costs and Expenses ……………………. 8,378 8,882 -6% 8,378 7,190 17% Cost of Sales……………………….. 1,460 1,291 13% 1,460 869 68% Operating Expenses ……………….. 6,918 7,591 -9% 6,918 6,321 9%

EBITDA………………………………… 9,091 8,224 11% 9,091 8,651 5% EBITDA Margin……………………….. 55% 51% 55% 57%

Depreciation and Amortization…...... 4,347 4,836 -10% 4,347 4,238 3% EBIT……………………………………... 4,744 3,388 40% 4,744 4,413 8% EBIT Margin…………………………… 29% 21% 29% 29% Non-Operating Charges……………….. (463) (578) -20% (463) (220) 110% Net Income After Tax (NIAT)………… 2,991 2,297 30% 2,991 2,947 1% Core Net Income ** ……………………. 2,961 1,944 52% 2,961 2,795 6%

* 4Q 2010 service revenues, EBITDA and EBIT have been normalized to exclude the impact of a one-time upward adjustment, recorded in the same period, amounting to P526 million representing prepaid load credits that have either expired or have already been used up. ** Core net income excludes all foreign exchange and mark-to-market gains and losses, as well as all non-recurring items such as the P526 million adjustment discussed above. • Consolidated service revenues in the first quarter grew 8% from P15.2 billion last year to

P16.5 billion. On a normalized basis, excluding last quarter’s P526 million upward adjustment from prepaid load credits, this quarter’s revenues represent an all-time high for the Company. Mobile revenues were up 4% despite intense competition and dilutive effect of lower yield unlimited and bucket promo offerings. The fixed line and broadband business, on the other hand, registered 26% revenue growth anchored on the 40% expansion of the broadband subscriber base and sustained strong demand for data services from the corporate sector.

• Against the last quarter, consolidated service revenues were P238 million or 1% higher than

normalized 4Q 2010 numbers. Revenues from the fixed line data and broadband segments grew 7% and 9%, respectively, and supported the steady performance of the mobile business which was boosted by the strong take-up of new and affordable postpaid plans as well as increased revenues from the prepaid segment.

• Operating expenses and subsidy increased by 12% from P6.6 billion a year ago to P7.4 billion

mainly on higher marketing and subsidy costs, and increased outsourced services and utilities. Network-related costs such as electricity, fuel, licenses and contracted services grew as a result of an expanded 2G, 3G and broadband networks, and to support the increased

SEC Form 17Q – 1Q 2011 15

growth in voice and data traffic. Similarly, subsidy and marketing expenses increased by 48% against last year following an aggressive promotional campaign across all business segments. As a percentage of total service revenues, subsidy and marketing costs were at 9% this period against 6% last year. Compared to the previous quarter, however, operating expenses and subsidy declined by 8% with reductions in subsidy & marketing, as well as network-related expenses.

• Consolidated EBITDA rose 5% from P8.7 billion a year ago to P9.1 billion this period as

revenue growth outpaced the increase in operating expenses. Consolidated EBITDA margin was at 55% from 57% last year. EBITDA growth helped offset the 3% year-on-year increase in depreciation charges which were driven by continued investments in the broadband and mobile networks. As a result, EBIT rose 8% from P4.4 billion last year to P4.7 billion this quarter, while EBIT margin remained at 29%. Compared to the previous quarter, the growth in service revenues complemented by an 8% decline in operating expenses and subsidy raised consolidated EBITDA this period by 11% from the normalized EBITDA in 4Q 2010. As a result, consolidated EBITDA margin improved from 51% to 55%.

• At the end of the first period, consolidated net income after tax of P3.0 billion was about P44

million or 1% better than last year’s level. Excluding foreign exchange and mark-to-market gains and losses as well non-recurring items, core net income after tax stood at P3.0 billion, 6% higher than last year’s P2.8 billion. Compared to last quarter, net income and core net income was higher by 30% and 52% respectively, driven by higher EBITDA, lower depreciation, and lower non-operating charges.

• Total capital expenditures as of the first quarter amounted to P5.5 billion (or about US$125

million) driven by the continued upgrade and expansion of the Company’s broadband and mobile networks. This amount is in line with last year’s spending of about P5.6 billion. The Company recently announced a major expansion of its current 4G footprint by becoming the country’s first carrier to commercially roll out its 4G mobile technology, which Globe has deployed in various part of Metro Manila including Marikina, Quezon City, Makati, Pasay, Las Pinas, Taguig, and Manila. As of end-March, Globe has a total of 11,733 base stations and 6,755 cell sites to support its 2G, 3G and WiMAX services.

SEC Form 17Q – 1Q 2011 16

GROUP OPERATING REVENUES

Globe Group Quarter on Quarter Year on Year

1Q 4Q QoQ 1Q 1Q YoY Change Change

Operating Revenues By Businesses (Php Mn)

2011 2010 (%)

2011 2010 (%)

Mobile 13,868 13,652 2% 13,868 13,047 6% Service Revenues *…………………. 13,060 13,006 - 13,060 12,530 4% Non-Service Revenues……………… 808 646 25% 808 517 56% Fixed Line and Broadband 3,601 3,454 4% 3,601 2,794 29% Service Revenues…………………… 3,392 3,208 6% 3,392 2,701 26% Non-Service Revenues…………….... 209 246 -15% 209 93 125% Total Net Operating Revenues………. 17,469 17,106 2% 17,469 15,841 10%

* 4Q 2010 service revenues have been normalized to exclude the impact of a one-time upward adjustment, recorded in the same period, amounting to P526 million representing prepaid load credits that have either expired or have already been used up.

The Globe Group closed the first quarter with total net operating revenues of P17.5 billion, 10% higher than last year and 2% above previous quarter’s level. The mobile business, which comprised 79% of consolidated service revenues at the end of the first quarter, closed the period with revenues of P13.1 billion, 4% above last year’s P12.5 billion. The mobile industry remained highly competitive, characterized by slowing revenue growth, high penetration levels, continued multi-SIM usage, aggressive pricing, and declining yields resulting from the prevalence of value offers. However, the programs initiated by the Company from earlier periods have gained traction which consequently translated to revenue improvement. Even when compared against seasonally strong 4Q 2010 revenues, revenues from the mobile business were steady with revenues supported by above average daily top-ups from the prepaid brands and the continued strong showing from the postpaid segment. The fixed line and broadband business accounted for 21% of consolidated service revenues, up from 18% a year ago. Revenues from this segment surpassed last year’s level by 26% from P2.7 billion to P3.4 billion lifted by the robust performance of the broadband and fixed line data segments. In relation to the previous quarter, the fixed line and broadband business sustained its growth momentum as well with a 6% increase in revenues. Demand for internet connectivity, being an effective means of communication coupled with the popularity of social networking sites and the introduction of new technology which enables faster browsing speeds, continued to drive the growth of the retail business. Meanwhile, for the corporate sector, the sustained expansion of the country’s offshoring and outsourcing industry contributed to the growth of the fixed line data business. Mobile non-service revenues meanwhile increased by 56% against last year driven largely by handset sales mostly for the postpaid segment. The same trend was observed against last quarter with non-service revenues growing by 25%. For the fixed line and broadband business, on the other hand, non-service revenues were more than double last year’s level of P93 million resulting from the higher dongle prices of Globe Broadband Tattoo. Against last quarter, however, fixed line and broadband non-service revenues declined by 15% to P209 million.

SEC Form 17Q – 1Q 2011 17

MOBILE BUSINESS

Quarter on Quarter Year on Year 1Q 4Q** QoQ 1Q 1Q** YoY

Change Change Mobile Net Service Revenues (Php Mn)

2011 2010 (%)

2011 2010 (%)

Service Voice 1 ….………………………………. 6,112 6,304 -3% 6,112 6,024 1% Data 2..…………………………………... 6,948 6,702 4% 6,948 6,506 7%

Mobile Net Service Revenues *………...... 13,060 13,006 - 13,060 12,530 4% * 4Q 2010 service revenues have been normalized to exclude the impact of a one-time upward adjustment, recorded in the same period, amounting to P526 million representing prepaid load credits that have either expired or have already been used up. ** 2010 revenue split between mobile voice and data has been restated for better comparability. 1 Mobile voice net service revenues include the following:

a) Prorated monthly service fees on consumable minutes of postpaid plans; b) Subscription fees on unlimited and bucket voice promotions including the expiration of the unused value of

denomination loaded; c) Charges for intra-network and outbound calls in excess of the consumable minutes for various Globe Postpaid

plans, including currency exchange rate adjustments (CERA) net of loyalty discounts credited to subscriber billings; and

d) Airtime fees for intra network and outbound calls recognized upon the earlier of actual usage of the airtime value or expiration of the unused value of the prepaid load credit denomination (for Globe Prepaid and TM SIMs) which occurs between 3 and 120 days after activation depending on the prepaid value reloaded by the subscriber, net of (i) bonus credits and (ii) prepaid load credit discounts; and revenues generated from inbound international and national long distance calls and international roaming calls.

Revenues from (a) to (d) are reduced by any interconnection or settlement payouts to international and local carriers and content providers.

2 Mobile data net service revenues consist of prorated monthly service fees on free text allocation of postpaid plans,

revenues from value-added services such as inbound and outbound SMS and MMS, content downloading, mobile data browsing and infotext, international VAS and related services, subscription fees on unlimited and bucket prepaid SMS and add-on VAS services, net of any interconnection or settlement payouts to international and local carriers and content providers.

Mobile Voice Mobile voice revenues accounted for 47% of total mobile service revenues in the first quarter to close at P6.1 billion, up 1% from last year. Revenues from unlimited and bulk voice subscriptions as well as roaming services increased from last year. Growth, however, was partly offset by the year-on-year decline in regular voice and IDD services. Globe sustained its suite of innovative and affordable mobile voice offers during the period. This includes its pioneering per-second charging offer, Super Sakto Calls, as well as its bulk voice services such as Tawag 236 for 20-minutes of intra-network calls for only P20, and its P10 for 3-minute calls to Globe Postpaid and Globe Prepaid subscribers. It also maintained its unlimited and hybrid voice packages such as SuperUnli which provides unlimited calls and texts within the Globe and TM networks, as well as its breakthrough 2-in-1 mobile and landline service, SuperDuo.

SEC Form 17Q – 1Q 2011 18

Similarly for TM, the Company sustained its per-second charging offer, Sulit Segundo Calls, and its bulk voice call promotions such as TodoTawag P15 for 15-minute intra-network calls, AstigTawag20 for consumable 15-minute calls to all networks, and TM SuliTawag for 3-minute intra-network calls. For value-seekers, meanwhile, the Company sustained its low-denomination bulk voice service TM DAGDAGCALL, an add-on service to TM’s text promotions which provides 3 consumable minutes of voice calls to any Globe or TM subscriber for only P5. TM UNLICOMBO, on the other hand, provides unlimited intra-network calls from 10 PM to 5 PM the following day coupled with unlimited SMS for 24 hours. For Filipinos who wish to stay connected with their loved ones abroad, Globe continued to offer its pioneering IDD Sakto Calls and Super Sulit Tipid IDD services. Globe similarly expanded its all-you-can offerings to include international voice calls with SuperIDD which supports unlimited IDD service to US and Canada from 11:00 PM to 5:59 AM (Philippine Time) for only P99 a day. Globe also introduced IDD Tingi, a bucket IDD service to popular and selected overseas destinations, while continuing to offer its TipIDD card at various Globe distribution channels. Mobile Data Mobile data revenues accounted for 53% of total mobile service revenues, and increased by 7% from P6.5 billion last year to P6.9 billion this period. Revenues from mobile browsing were significantly higher than last year driven by the popularity of social networking sites, affordable data plans, and pervasiveness of mobile phones and access devices. These were supported as well by the growth in regular and bucket SMS revenues. In the first quarter, Globe continued to offer its unlimited text services such as UnliTxt and SuperTxt, alongside TM’s AstigTxt10. Globe also maintained its bucket SMS services such as SuliTxt, EverybodyTxt, and SuperAll Txt together with TM’s AstigTxtAll and SuliTxt. The Company also sustained its bundled voice and text services such as (a) Globe’s Super One for unlimited calls and text messages to a frequently called Globe or TM number, (b) TM’s ASTIGCOMBO10 which provides 50 text messages to all networks plus 10 consumable voice minutes to other Globe and TM subscribers, and (c) ASTIGCOMBO20 for 24 hours of unlimited SMS plus 100 consumable voice minutes within the Globe and TM networks. Globe similarly continued to offer SUPERCOMBO20 which is primarily an unlimited text service which comes with 50 minutes worth of voice calls to any Globe or TM subscriber. With the prevalence of smartphones and the increasing demand for mobile internet service driven by the popularity of social networking sites, Globe continued to provide an affordable add-on data plan, Super Surf, which allows unlimited chatting, downloading, emailing and browsing for its Globe Postpaid and Globe Prepaid subscribers. Globe similarly sustained its Power Surf offering to allow Globe Prepaid subscribers to purchase mobile internet hours by bulk in either of the two denominations: 3 hours for P30 valid for a day, or 5 hours for P50 valid for 3 days. For BlackBerry® users, on the other hand, Globe sustained its attractive and affordable data services such as the following: unlimited BlackBerry® service for Globe Prepaid subscribers, Super Surf for BlackBerry® for unlimited BlackBerry® services using the BlackBerry® APN and Super Surf for BlackBerry® Max for unlimited BlackBerry® services using both mobile internet service and BlackBerry® APN for its Globe Postpaid subscribers. Globe likewise maintained its two add-on data plans to its Globe Postpaid and Globe Prepaid subscribers: BlackBerry® Messaging and BlackBerry® Social.

SEC Form 17Q – 1Q 2011 19

The key drivers for the mobile business are as follows:

Quarter on Quarter Year on Year 1Q 4Q QoQ 1Q 1Q YoY

Change Change 2011 2010

(%) 2011 2010

(%)

Cumulative Subscribers (or SIMs) – Net 27,319,553 26,470,859 3% 27,319,553 23,889,706 14% Globe Postpaid 1………………………………. 1,146,738 1,066,137 8% 1,146,738 880,491 30% Prepaid .…………………………………… 26,172,815 25,404,722 3% 26,172,815 23,009,215 14% Globe Prepaid …………………………… 14,211,548 13,834,716 3% 14,211,548 13,041,308 9% TM .………………………………………… 11,961,267 11,570,006 3% 11,961,267 9,967,907 20% Net Subscriber (or SIM) Additions 848,694 1,067,857 -21% 848,694 644,700 32% Globe Postpaid ..…………………………...…. 80,601 83,259 -3% 80,601 29,123 177% Prepaid .…………………………………… 768,093 984,598 -22% 768,093 615,577 25% Globe Prepaid …………………………… 376,832 483,473 -22% 376,832 (7,553) 5089% TM .………………………………………… 391,261 501,125 -22% 391,261 623,130 -37% Average Revenue Per Subscriber (ARPU) Gross ARPU Globe Postpaid………………………………... 1,402 1,580 -11% 1,402 1,723 -19% Prepaid 2 Globe Prepaid ………………………….... 199 207 -4% 199 219 -9% TM ………………………………………… 115 121 -5% 115 120 -4% Net ARPU Globe Postpaid..………………………………. 1,090 1,176 -7% 1,090 1,268 -14% Prepaid 2 Globe Prepaid ……………………………. 152 155 -2% 152 167 -9% TM .………………………………………… 86 92 -7% 86 92 -7% Subscriber Acquisition Cost (SAC) Globe Postpaid………………………………... 4,238 3,959 7% 4,238 3,837 10% Prepaid Globe Prepaid ……………………………. 22 28 -21% 22 10 120% TM .………………………………………… 24 27 -11% 24 32 -25% Average Monthly Churn Rate (%) Globe Postpaid ....…………………………….. 1.41% 1.32% 1.41% 2.07% Prepaid Globe Prepaid ……………………………. 5.52% 5.65% 5.52% 6.71% TM .……………………………………….... 6.47% 6.41% 6.47% 6.76%

1 As of 1Q 2011, Globe had a total of 1.44 million wireless postpaid subscribers which includes 1.15 million mobile telephony and 0.29 million wireless broadband customers. This is higher compared to the 1.33 million wireless postpaid subscribers as of 4Q 2010 which is comprised of 1.07 million mobile telephony subscribers and 0.26 million wireless broadband customers. Mobile telephony revenues are reflected under “Mobile Service Revenues” while wireless broadband revenues are included under “Broadband.” 2 4Q 2010 ARPUs have been normalized to exclude the impact of a one-time upward adjustment, recorded in the same period, amounting to P526 million representing prepaid load credits that have either expired or have already been used up.

SEC Form 17Q – 1Q 2011 20

At the end of the first quarter, Globe had a total subscriber base of 27.3 million, 14% and 3% above last year and previous quarter, respectively. Strong subscriber acquisitions were sustained with 5.5 million SIM additions in the first quarter, 4% higher than last year’s 5.3 million. With churn rate significantly improving from last year’s 6.56% to this period’s 5.77%, net additions as of end-March increased from last year’s 644,700 to 848,694 SIMs. Compared to the previous quarter, gross additions were about 84,000 SIMs below the 5.6 million recorded earlier. With churn rate almost at par with prior quarter’s 5.81%, net additions declined by 21% from 1,067,857 recorded in fourth quarter of 2010. The succeeding sections cover the key brands of the mobile business – Globe Postpaid, Globe Prepaid and TM. Globe Postpaid The postpaid segment comprises 4% of Globe’s total mobile subscriber base. The Company’s successful launch of its personalized subscription plans drew great response from new and old customers alike bringing this quarter’s gross acquisitions to a record-high of nearly 121,000 from only about 80,000 in the same period last year. With churn rate significantly improving from 2.07% to 1.41% year-on-year, net additions increased from 29,123 to 80,601. Against previous quarter, however, net additions were slightly below the 83,259 recorded earlier. As a result, postpaid subscribers stood at 1,146,738 as of the first quarter, 30% higher than year ago level of 880,491 subscribers, and 8% higher than last quarter’s 1,066,137 subscribers Anchoring on the recent success of its My Super Plan and My Fully Loaded Plan offerings, Globe further intensified its efforts in customizing and personalizing subscriber plans with the launch of the ALL NEW My Super Plan. Under the new plans, subscribers are given the flexibility to determine the monthly service fee suited to their budget by choosing between an All-Unlimited Plan and an All-Consumable Plan. Subscribers then pick a monthly add-on unlimited service such as calls, texts, or mobile surfing to boost their plans. On top of these, subscribers select freebies such as bulk voice, bucket text and mobile surfing hours to complete the services available to their chosen subscription plan. Finally, with the ALL NEW My Super Plan, customers also pick a handset or a device bundle that comes with their plan either for free or at a discount. When subscribed to the ALL NEW My Super Plan, postpaid subscribers are also allowed to change their add-on service and freebies as often as monthly. Alternatively, Globe launched MY SUPERTXT ALL, the first-ever unlimited text offer to all networks for mobile postpaid subscribers. This latest service from Globe is available to postpaid subscribers for a fixed monthly fee of P599, or effectively for as low as P20 a day. Recognizing the demand for mobile internet service, Globe likewise launched exciting promotional gadget deals during the period. Globe brought in a number of smartphones and tablet devices from Samsung, Huawei, and HTC to come with its new postpaid subscription plans. To complement this, the Company held a one-day sale in February for its BlackBerry® handsets which allowed subscribers to purchase a pair of BlackBerry® units for a monthly fee of as low as P2,098. Postpaid gross and net ARPUs of P1,402 and P1,090 were lower than last year’s P1,723 and P1,268, respectively, given the strong subscriber take-up of more affordable postpaid subscription plans. Growth in mobile browsing, domestic voice and local SMS revenues were offset by lower

SEC Form 17Q – 1Q 2011 21

revenues from international services. Postpaid subscriber acquisition costs (SAC) increased by 10% from previous year’s P3,837 to P4,238 due largely to advertising and promotion charges related to the launch of new postpaid plans. Costs, however, remained recoverable within the 24-month contract period for postpaid subscribers. Prepaid Globe’s prepaid segment, which includes the Globe Prepaid and TM brands, comprises 96% of its total subscriber base. As of end-March 2011, cumulative prepaid subscribers of 26.2 million were 14% above last year’s 23.0 million, and 3% higher than last quarter’s 25.4 million. A prepaid subscriber is recognized upon the activation and use of a new SIM card. The subscriber is provided with 60 days (first expiry) to utilize the preloaded SMS value. If the subscriber does not reload prepaid credits within the first expiry period, the subscriber retains the use of the mobile number but is only entitled to receive incoming voice calls and text messages for another 120 days (second expiry). The second expiry is 120 days from the date of the first expiry. However, if the subscriber does not reload prepaid credits within the second expiry period, the account is permanently disconnected and considered part of churn. The first expiry periods of reloads vary depending on the denominations, ranging from 1 day for P10 to 60 days for P300 to P500 reloads. The first expiry is reset based on the longest expiry period among current and previous reloads. Under this policy, subscribers are included in the subscriber count until churned. In 2009, the National Telecommunications Commission (NTC) published Memorandum Circular 03-07-2009 which promulgates the extension of the validity periods of prepaid reloads effective July 19, 2009. Under the new pronouncement, the first expiry periods now range from 3 days for P10 or below to 120 days for reloads amounting to P300 and above. The second expiry remains at 120 days from the date of the new first expiry periods. The succeeding sections discuss the performance of the Globe Prepaid and TM brands in more detail.

Globe Prepaid Globe Prepaid accounts for 52% of the total mobile subscriber base. Gross additions in the first quarter rose by 3% from last year’s 2.6 million to 2.7 million. Churn rate similarly improved from last year’s 6.71% to 5.52% resulting to subscriber net additions of 376,832 against last year’s net reduction of 7,553. Against the previous quarter, however, gross additions slightly declined from about 2.8 million to 2.7 million SIMs this period. Churn rate, likewise, declined from 5.65% to 5.52%, bringing net additions down by 22% quarter-on-quarter. Cumulative Globe Prepaid subscribers stood at 14.2 million, 9% higher than last year’s 13.0 million and 3% above previous quarter’s 13.8 million. In the first quarter, Globe enhanced its bucket text service SuperAll Txt 20 which now provides 250 all-network text messages, up from just 200 messages from the time of its inception in the third quarter of 2010. The service remains affordable for the same fee of P20 for 1 day subscription. Meanwhile, in an effort to stimulate usage and encourage retention among its subscribers, Globe had a soft launch of its first-ever all-in-one offer, SuperLahat20, to Globe

SEC Form 17Q – 1Q 2011 22

Prepaid subscribers in Davao. The promo provides unlimited intra-network text messages and 100 intra-network consumable call minutes, 60 consumable minutes of mobile internet surfing, and 5 international text messages to 190 destinations. Globe Prepaid subscribers in Davao can avail of the promo for only P20 for a day’s use. Capitalizing on its strong partnership with Puregold, Globe launched a special promotional offer for shoppers who top-up their prepaid load credits at any check-out lane of Puregold branches nationwide. For every P50 purchase of prepaid load credits, the subscriber gets an additional P5 load. The promo was offered daily from March 11 to April 10, 2011, and was made available during weekends beginning April 15 up to June 30, 2011. During the period, Globe also enhanced its mobile data offerings to its Globe Prepaid subscribers. The Company launched Super Facebook, which allows subscribers to surf on Facebook on their mobile phones for 5 straight hours for only P10. Alternatively, users who browse the internet from time to time can subscribe to PowerSurf15 for 1 hour consumable mobile internet access for just P15 and valid for 1 day. Finally, for prepaid subscribers with BlackBerry® units, Globe launched Super Surf for BlackBerry® Max Prepaid which provides unlimited chatting, downloading, emailing via push email service and video streaming using both the internet and the BlackBerry® APN. The service, which used to be offered only to postpaid subscribers, is available in three variants: P60 for 24 hours, P300 for 5 days, and P1,500 for 30 days access. Despite an overall increase in voice and SMS traffic, Globe Prepaid gross and net ARPUs declined by 9% from last year. Subscribers’ continued preference for lower yield unlimited and bucket promos was the key driver behind the decline. Revenue growth from mobile browsing, domestic voice and SMS was offset by lower revenues from international services. Subscriber acquisition costs, on the other hand, grew more than twice last year’s P10 to P22 mainly on higher advertising and promo expenses. SAC, however, remained recoverable within a month’s net ARPU. TM TM comprises 44% of the total mobile subscriber base. Gross additions in the first quarter stood at about 2.7 million, slightly above last year’s level of 2.6 million, while churn rate improved year-on-year from 6.76% to 6.47%. Net additions for the period, however, declined by 37% from 623,130 last year to 391,261. As a result, cumulative TM subscribers closed at nearly 12.0 million at the end of the first quarter, 20% above last year’s level of about 10.0 million SIMs. Compared to last quarter, TM subscribers were 3% higher. During the period, the Company further enhanced TM’s service offerings with ASTIGCOMBOALL for TM subscribers in Davao. For only P10 a day, subscribers are entitled to 100 texts to all networks and 100 consumable call minutes to any Globe or TM number. Similar to Globe Prepaid and as a way of thanking Puregold shoppers for staying Globe-connected, TM subscribers who purchase prepaid load credits at any of Puregold’s point-of-sale and check-out counters nationwide are also entitled to get an additional P5 load for every P50 load top-up. The Super Reload Deal complemented the earlier campaign by Globe and Puregold that rewarded loyal customers with the Aling Puring Super Suki SIM, a special multi-function SIM card which allows Puregold to text blast announcements and reminders to “Aling Puring”

SEC Form 17Q – 1Q 2011 23

members in an easy, reliable and personal way. Globe provided Aling Puring Super Suki SIM card holders with discounted call and text rates to any Globe or TM subscribers. Similar to the trends in Globe Prepaid, TM gross and net ARPUs declined from last year by 4% and 7%, respectively. Subscriber acquisition costs (SAC), likewise, declined by 25% year-on-year on lower advertising and promotion charges and handset subsidy. TM SAC remained recoverable within a month’s net ARPU.

SEC Form 17Q – 1Q 2011 24

GCash GCash continues to establish its presence in the mobile commerce industry. GCash’s initial thrust towards money-transfers, purchase of goods and services from retail outlets, and sending and receiving domestic and international remittances has spurred alliances in the field of mobile commerce. Today, GCash allows Globe and TM subscribers to pay or transact for the following using their mobile phone:

• domestic and international remittances • utility bills • interest and amortization of loans • insurance premiums • donations to various institutions and organizations • sales commissions and payroll disbursements • school tuition fees • micro tax payments and business registration • electronic loads and pins • online purchases • airline tickets

In addition to the above transactions, GCash is also used as a wholesale payment facility. On October 9, 2009, the Company announced that the Bangko Sentral ng Pilipinas (BSP) has approved the sale and transfer by Bank of the Philippine Islands (BPI) of its shares of stock in Pilipinas Savings Bank, Inc. (PSBI) that will result in the ownership of PSBI as follows: 40 % each for BPI and Globe Telecom and 20 % for Ayala Corporation (AC). BPI, Globe and AC plan to transform PSBI into the country’s first mobile microfinance bank. On October 23, 2009 the official name of PSBI was changed to BPI GLOBE BANKO, INC. after getting the approval of both the BSP and the Securities and Exchange Commission (SEC). BPI Globe BanKo Inc. opened its first branch last February 2010, and added 5 more branches as of 31 March 2011 in Dipolog, Dumaguete, Lucena, Naga and Tacloban. While the bank’s initial focus is on wholesale lending to other microfinance institutions, it is now expanding into retail banking products and services to include micro-savings, micro-lending, and insurance. Globe also launched its GCash Remit Service, providing mobile subscribers a quick, affordable and convenient way to send and receive domestic and international remittances. With BSP’s recent approval to use its sub-distributors as cash-in and cash-out outlets, GCash now has the largest remittance network in the country with its 18,000 GCash outlets. On October 14, 2010, Globe also achieved a milestone with the launch of the GCash Card, the country’s first customizable ATM card linked to a mobile wallet. This gives subscribers 24/7 access to GCash and allows them to withdraw funds in their GCash via any of the 9,000 Bancnet, Megalink, ExpressNet or Encash Automated Teller Machines (ATMs) nationwide. In addition, the GCash Card is the only customizable ATM Card in the country where subscribers can make their own personalized ATM card design or choose from a variety of design templates.

SEC Form 17Q – 1Q 2011 25

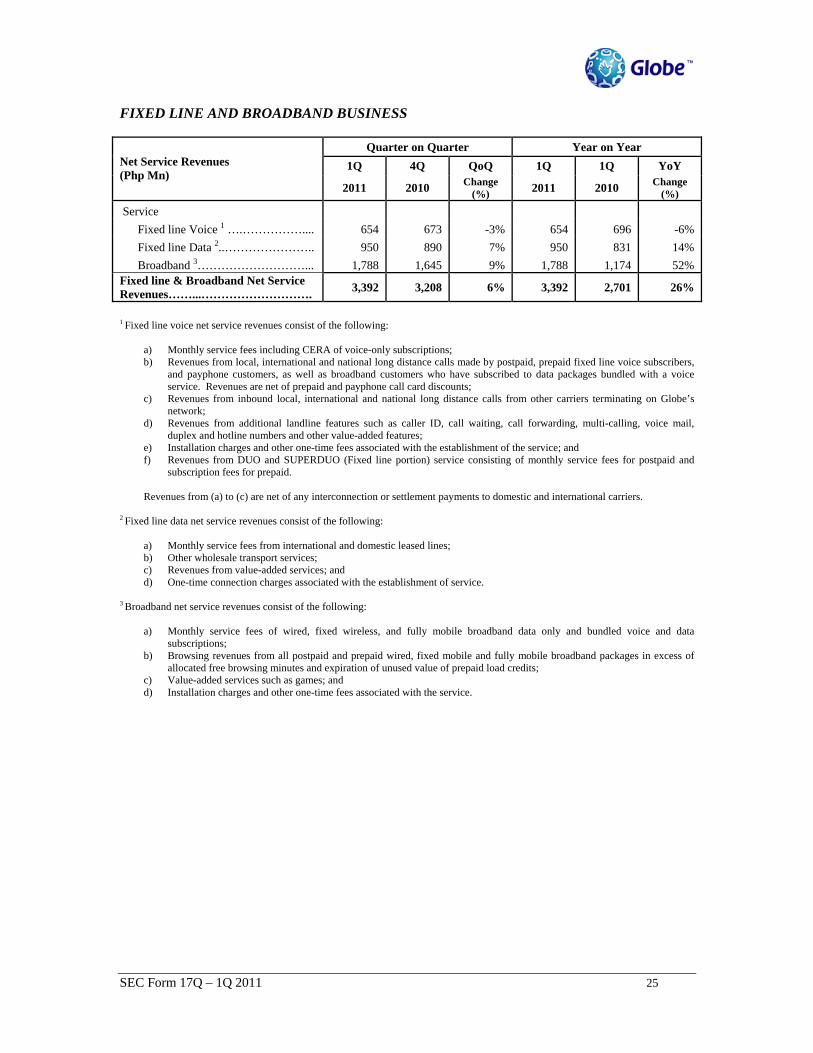

FIXED LINE AND BROADBAND BUSINESS

Quarter on Quarter Year on Year 1Q 4Q QoQ 1Q 1Q YoY Net Service Revenues

(Php Mn) 2011 2010 Change

(%) 2011 2010 Change (%)

Service Fixed line Voice 1 ….…………….... 654 673 -3% 654 696 -6% Fixed line Data 2..………………….. 950 890 7% 950 831 14% Broadband 3………………………... 1,788 1,645 9% 1,788 1,174 52% Fixed line & Broadband Net Service Revenues……...………………………. 3,392 3,208 6% 3,392 2,701 26% 1 Fixed line voice net service revenues consist of the following:

a) Monthly service fees including CERA of voice-only subscriptions; b) Revenues from local, international and national long distance calls made by postpaid, prepaid fixed line voice subscribers,

and payphone customers, as well as broadband customers who have subscribed to data packages bundled with a voice service. Revenues are net of prepaid and payphone call card discounts;

c) Revenues from inbound local, international and national long distance calls from other carriers terminating on Globe’s network;

d) Revenues from additional landline features such as caller ID, call waiting, call forwarding, multi-calling, voice mail, duplex and hotline numbers and other value-added features;

e) Installation charges and other one-time fees associated with the establishment of the service; and f) Revenues from DUO and SUPERDUO (Fixed line portion) service consisting of monthly service fees for postpaid and

subscription fees for prepaid. Revenues from (a) to (c) are net of any interconnection or settlement payments to domestic and international carriers.

2 Fixed line data net service revenues consist of the following:

a) Monthly service fees from international and domestic leased lines; b) Other wholesale transport services; c) Revenues from value-added services; and d) One-time connection charges associated with the establishment of service.

3 Broadband net service revenues consist of the following:

a) Monthly service fees of wired, fixed wireless, and fully mobile broadband data only and bundled voice and data subscriptions;

b) Browsing revenues from all postpaid and prepaid wired, fixed mobile and fully mobile broadband packages in excess of allocated free browsing minutes and expiration of unused value of prepaid load credits;

c) Value-added services such as games; and d) Installation charges and other one-time fees associated with the service.

SEC Form 17Q – 1Q 2011 26

Fixed line Voice

Quarter on Quarter Year on Year 1Q 4Q QoQ 1Q 1Q YoY

2011 2010 Change (%) 2011 2010 Change

(%) Cumulative Voice Subscribers -

Net (End of period)1…………............................ 631,200 618,606

2% 631,200 583,149 8% Average Revenue Per Subscriber (ARPU) ...... Gross ARPU………………………………… 417 437 -5% 417 480 -13% Net ARPU…………………………………… 349 369 -5% 349 402 -13% Average Monthly Churn Rate ..…………….... 2.92% 2.68% 2.92% 5.93%

1 Includes DUO and SuperDUO subscribers Total fixed line voice revenues decreased by 6% to P654 million from P696 million last year mainly due to the continued shift in traffic from fixed line voice to mobile services and the resulting weaker demand for voice-only, fixed line products. This decline was partially offset by the continued strong performance of Globe’s DUO and SUPERDUO service, which led to the growth in cumulative fixed line voice subscribers of 8% year-on-year to over 631,000. On a sequential basis, cumulative voice subscribers increased by 2% due to the increase in both postpaid and prepaid subscriptions to the DUO and SUPERDUO service. Fixed line Data

Quarter on Quarter Year on Year 1Q 4Q QoQ 1Q 1Q YoY Net Service Revenues (Php Mn)

2011 20102 Change (%) 2011 20102 Change

(%) Fixed line Data International …..………………………... 257 258 - 257 243 6% Domestic….… …………………............. 422 395 7% 422 379 11% Others 1 ………………………………… 271 237 14% 271 209 30% Total Fixed line Data Service Revenues….. 950 890 7% 950 831 14% 1 Includes revenues from value-added services such as internet, data centers and bundled services. 2 2010 revenues have been restated for comparability The fixed line data segment sustained its strong growth and ended the first quarter of 2011 with P950 million in revenues, an increase of 14% over the same period last year following gains across all product segments. Growth has continued to be fueled by the Company’s expansion of its network of high-speed data nodes, transmission links, and international bandwidth capacity to serve the requirements of business and enterprise clients, including those in the financial services, retail, offshoring and outsourcing industries.

SEC Form 17Q – 1Q 2011 27

Broadband

Quarter on Quarter Year on Year 1Q 4Q QoQ 1Q 1Q YoY

2011 2010 Change (%) 2011 2010 Change

(%) Cumulative Broadband Subscribers Wireless 1 ……………………………… 915,148 819,276 12% 915,148 606,344 51% Wired………………………………….. 265,251 255,077 4% 265,251 234,253 13% Total (end of period)…………………….. 1,180,399 1,074,353 10% 1,180,399 840,597 40% 1 Includes fixed wireless and fully mobile broadband subscribers. Globe’s broadband business ended the first quarter of the year with over 1,180,000 subscribers, 40% higher than the prior year’s level of 841,000. This was driven by the significant subscriber gains in Globe Broadband Tattoo, the Company’s nomadic broadband service, and in Globe WiMAX, Globe’s fixed wireless service for at-home use. Wireless broadband subscribers now account for 78% of total broadband customers, up from 72% last year. The robust subscriber pick-up translated to sustained revenue gains, with broadband service revenues up 52% to close the quarter at P1.8 billion compared to P1.2 billion in the same period in 2010. The broadband business now comprises 11% of consolidated service revenues compared to 8% last year. In an effort to sustain the strong growth in the segment, Globe launched the all-new Tattoo Broadband: No Limits campaign, with an edgier and more vibrant look and feel. Along with this, Globe also launched the new barkada-friendly Buy 3, Get 1 Free promo that offers a free Tattoo stick for every three sticks purchased. For only P3,735, the promotion offers 4 Tattoo sticks at an effective price of P933.75 per stick versus the regular price of P1,245, providing savings of up to 25%. Globe also introduced Tattoo SURFTXT 60, the first-ever surf and text combo offer available to prepaid broadband dongles. The combined promotion provides Globe Tattoo Prepaid Broadband subscribers access to an entire day of surfing and texting for only P60. In the last quarter of 2010, Globe launched the Tattoo SuperStick, Globe Tattoo’s most powerful mobile broadband, capable of speeds of up to 3 mbps, and with sharable Globe-powered WIFI connection for only P1,299 per month. In the first quarter of 2011, Globe also announced the expansion of its 4G footprint by becoming the first carrier in the Philippines to commercially roll-out its 4G mobile technology, complementing the company’s existing 4G WiMAX network. Globe’s 4G mobile network (HSPA+ technology or Evolved High-Speed Packet Access, a 4G wireless, mobile and high speed broadband technology) has been deployed in different cities across Metro Manila, providing customers with an improvement in their call and text services as well as an enhancement in their data experience, providing consistent browsing speeds of 4-6 Mbps with even faster peak speeds.

SEC Form 17Q – 1Q 2011 28

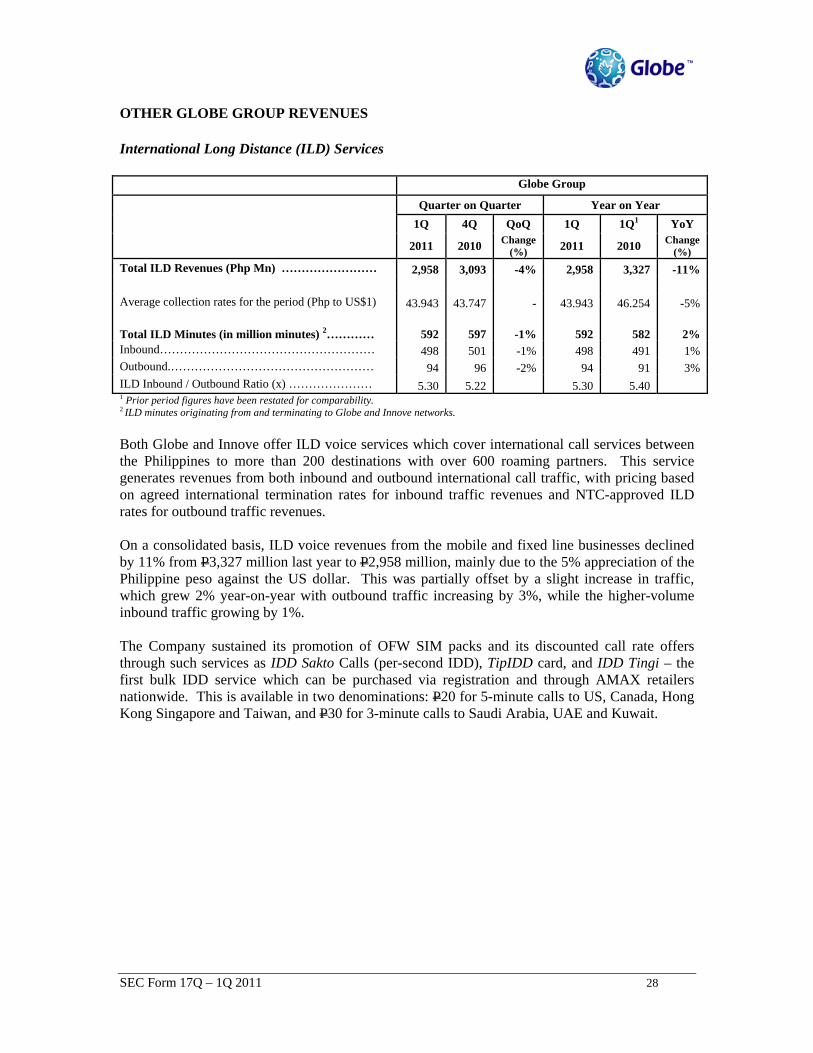

OTHER GLOBE GROUP REVENUES

International Long Distance (ILD) Services

Globe Group

Quarter on Quarter Year on Year 1Q 4Q QoQ 1Q 1Q1 YoY

2011 2010 Change (%) 2011 2010 Change

(%) Total ILD Revenues (Php Mn) …………………… 2,958 3,093 -4% 2,958 3,327 -11% Average collection rates for the period (Php to US$1) 43.943 43.747 - 43.943 46.254 -5% Total ILD Minutes (in million minutes) 2………… 592 597 -1% 592 582 2% Inbound……………………………………………… 498 501 -1% 498 491 1% Outbound.…………………………………………… 94 96 -2% 94 91 3% ILD Inbound / Outbound Ratio (x) ………………… 5.30 5.22 5.30 5.40 1 Prior period figures have been restated for comparability. 2 ILD minutes originating from and terminating to Globe and Innove networks. Both Globe and Innove offer ILD voice services which cover international call services between the Philippines to more than 200 destinations with over 600 roaming partners. This service generates revenues from both inbound and outbound international call traffic, with pricing based on agreed international termination rates for inbound traffic revenues and NTC-approved ILD rates for outbound traffic revenues. On a consolidated basis, ILD voice revenues from the mobile and fixed line businesses declined by 11% from P3,327 million last year to P2,958 million, mainly due to the 5% appreciation of the Philippine peso against the US dollar. This was partially offset by a slight increase in traffic, which grew 2% year-on-year with outbound traffic increasing by 3%, while the higher-volume inbound traffic growing by 1%. The Company sustained its promotion of OFW SIM packs and its discounted call rate offers through such services as IDD Sakto Calls (per-second IDD), TipIDD card, and IDD Tingi – the first bulk IDD service which can be purchased via registration and through AMAX retailers nationwide. This is available in two denominations: P20 for 5-minute calls to US, Canada, Hong Kong Singapore and Taiwan, and P30 for 3-minute calls to Saudi Arabia, UAE and Kuwait.

SEC Form 17Q – 1Q 2011 29

GROUP OPERATING EXPENSES For the first three months of the year, the Globe Group’s total costs and expenses, including depreciation, grew by 8% to P=11,708 million from P=10,818 million in the same period in 2010, mainly driven by higher marketing and subsidy spend and service costs. Compared to last quarter, total costs and expenses, including depreciation, were lower by 9%.

Globe Group Quarter on Quarter Year on Year

1Q 4Q QoQ 1Q 1Q YoY (Php Mn)

2011 2010 Change (%) 2011 2010 Change

(%) Cost of sales…………………………………………. 1,460 1,291 13% 1,460 869 68% Less: Non-service revenues………………………….. 1,017 892 14% 1,017 610 67% Subsidy………………………………………………. 443 399 11% 443 259 71% Selling, Advertising and Promotions ………………. 1,001 1,268 -21% 1,001 715 40% Staff Costs …………………………………………… 1,412 1,281 10% 1,412 1,337 6% Utilities, Supplies & Other Administrative Expenses... 866 924 -6% 866 725 19% Rent…………………………………………………… 628 762 -18% 628 715 -12% Repairs and Maintenance…………………………….. 721 913 -21% 721 742 -3% Provisions ………………… ……………………………. 370 350 6% 370 364 2% Services and Others…………………………………... 1,920 2,093 -8% 1,920 1,723 11% Operating Expenses…………………………………. 6,918 7,591 -9% 6,918 6,321 9% Depreciation and Amortization ……………….…… 4,347 4,836 -10% 4,347 4,238 3% Costs and Expenses…………………………………. 11,708 12,826 -9% 11,708 10,818 8% Subsidy and Marketing Total subsidy and selling, advertising and promotions was higher at P1,444 million against last year’s P974 million. Against the prior quarter, subsidy and selling, advertising and promotions expenses were lower by 13% mainly due to the seasonally high marketing spend in the previous quarter. Total subsidies increased 71% or by P184 million mainly from higher gross acquisitions in the mobile business partially offset by the decrease in subsidies in broadband following the price increase of Globe Broadband Tattoo Prepaid kits in May 2010. Selling, advertising and promotion, which comprised 14% of total subsidy and operating expenses, were higher by P286 million or 40%. Against last quarter, first quarter spend was P267 million or 21% lower. As a percentage of total service revenues, total marketing expenses and subsidy increased to 9% from last year’s 6%. Staff Costs Staff costs, which accounted for 19% of total subsidy and operating expenses, increased by 6% to end the period at P1,412 million from P1,337 million last year mainly due to the higher headcount

SEC Form 17Q – 1Q 2011 30

for the period, coupled with increases in other incentives. Total headcount increased 5% compared to last year, from 5,433 to 5,710. On a quarter on quarter basis, staff costs increased 10% due to higher variable pay during the period. Utilities, Supplies and Other Administrative Expenses Utilities, Supplies and Other Administrative expenses accounted for 12% of total subsidy and operating expenses. Costs rose by 19% year on year due mainly to higher electricity, fuel expenses coming from the continued expansion of Globe’s cellular and broadband network. Rent Rent expenses, which accounted for 9% of total subsidy and operating expenses, decreased by P87 million or 12% year on year due mainly to lower leases on international cable facilities. On a quarter on quarter basis, rental expenses decreased 18% or P134 million. Provisions This account includes provisions related to trade, non-trade and traffic receivables and inventory. Overall, provisions posted a net increase of P6 million or 2% from P364 million to P370 million this year driven by higher traffic and inventory provisions. As a percentage of service revenues, provisions remained within the 2% level. Repairs and Maintenance Repairs and Maintenance expenses, which include fees for technical and service providers as well as maintenance costs for hardware, software and network facilities, accounted for 10% of total subsidy and operating expenses and decreased by P21 million or 3% from last year. Services and Others Services and Others, which accounted for 26% of total subsidy and operating expenses, increased by P197 million or 11% from P1,723 million to P1,920 million. This increase is mainly attributable to higher charges related to various outsourced functions such as call centers, technical helpdesk, and subscriber line installation charges for broadband and fixed line voice services, coupled with higher professional and consulting fees. These were partially offset by lower security costs for the period. Depreciation and Amortization Depreciation and amortization expenses increased by 3% year on year to P4,347 million from P4,238 million due to additional investments resulting from the continued expansion of the Company’s networks. Compared to last quarter, depreciation expense was lower by P489 million or 10%. Depreciation is computed using the straight line method over the estimated useful life (EUL) of the assets, where the weighted EUL of all depreciable assets as of March 31, 2011 is 10.11 years.

SEC Form 17Q – 1Q 2011 31

Other income statement items

Other income statement items include net financing costs, net foreign exchange gain (loss), interest income and net property and equipment related income (charges) as shown below:

Globe Group

Quarter on Quarter Year on Year

1Q 4Q QoQ 1Q 1Q YoY (Php Mn)

2011 2010 Change (%) 2011 2010 Change

(%)

Financing Costs – net

Interest Expense…………………………... (522) (534) -2% (522) (458) 14% (Loss) on derivative instruments – net……. 10 (4) -350% 10 (9) -211% Swap costs and other financing costs……... (51) (25) 104% (51) (12) 325% Foreign Exchange (loss) / gain - net.…..…. 32 (13) -346% 32 224 -86% (531) (576) -8% (531) (255) 108% Interest Income ……………………………... 85 57 49% 85 54 57% Others – net…………………………………. (17) (59) -71% (17) (19) -11% Total Other (Expenses) Income……………. (463) (578) -20% (463) (220) 110% As of the end of March 2011, the Globe Group’s non-operating charges posted a year on year increase of 110% or P243 million to close at P463 million. With the Philippine peso registering only a slight 1% appreciation from January to March 2011, the Company recorded lower foreign exchange gains of P32 million in contrast to the P224 million gains booked in the same period last year, when the currency had appreciated by 2% (See related discussion on derivative instruments and swap costs in the Foreign Exchange and Interest Rate Exposure section). Meanwhile, interest expense increased by 14% from P458 million last year to P522 million due to increased borrowings this period despite the decline in average local and foreign interest rates. On the other hand, interest income increased by P31 million or 57% against last year.

SEC Form 17Q – 1Q 2011 32

LIQUIDITY AND CAPITAL RESOURCES

Globe Group

31 Mar 2011

31 Mar 2010

YoY change (%)

Balance Sheet Data (Php Mn) Total Assets …………………………………………………… 133,682 127,491 5% Total Debt …………………………………………………….. 50,524 47,991 5% Total Stockholders’ Equity …………………………………… 45,953 45,427 1% Financial Ratios (x) Total Debt to EBITDA ………………………………………... 1.39 1.39 Debt Service Coverage………………………………………… 2.24 2.33 Interest Cover (Gross) ………………………………………… 13.04 11.80 Debt to Equity (Gross) ………………………………………... 1.10 1.06 Debt to Equity (Net) 1…………………………………………. 0.94 0.97 Total Debt to Total Capitalization (Book) ……………………. 0.52 0.51 Total Debt to Total Capitalization (Market) ...………………... 0.30 0.27

1 Net debt is calculated by subtracting cash, cash equivalents and short term investments from total debt. Globe’s balance sheet and cash flows remain strong with ample liquidity and gearing within optimum level. Globe Group’s consolidated assets as of 31 March 2011 amounted to P=133,682 million compared to P=127,491 million for the same period in 2010. Consolidated cash, cash equivalents and short term investments (including investments in assets available for sale and held to maturity investments) was at P=7,279 million at the end of the period compared to last year’s P3,944 million. The Company’s gearing levels have been increasingly optimized over the past few years with the raised dividend payouts and higher proportion of debt to total capitalization. Globe ended the quarter with gross debt to equity ratio of 1.1:1 on a consolidated basis which is well within the 2:1 debt to equity limit dictated by its debt covenants. Meanwhile, net debt to equity ratio was at 0.94:1 compared to 0.97:1 for the same period last year. The financial tests under Globe’s loan agreements include compliance with the following ratios:

• Total debt to equity not exceeding 2:1; • Total debt to EBITDA not exceeding 3:1; • Debt service coverage 1 exceeding 1.3 times; and • Secured debt ratio 2 not exceeding 0.2 times.

As of 31 March 2011, Globe is well within the ratios prescribed under its loan agreements. 1 Debt service coverage ratio is defined as the ratio of EBITDA to required debt service, where debt service includes subordinated debt but excludes shareholder loans.

2 Secured debt ratio is defined as the ratio of the total amount for the period of all present consolidated obligations for payment, whether actual or contingent which are secured by Permitted Security Interest as defined in the loan agreement to the total amount of consolidated debt. Globe has no secured debt as of 31 March 2011.

SEC Form 17Q – 1Q 2011 33

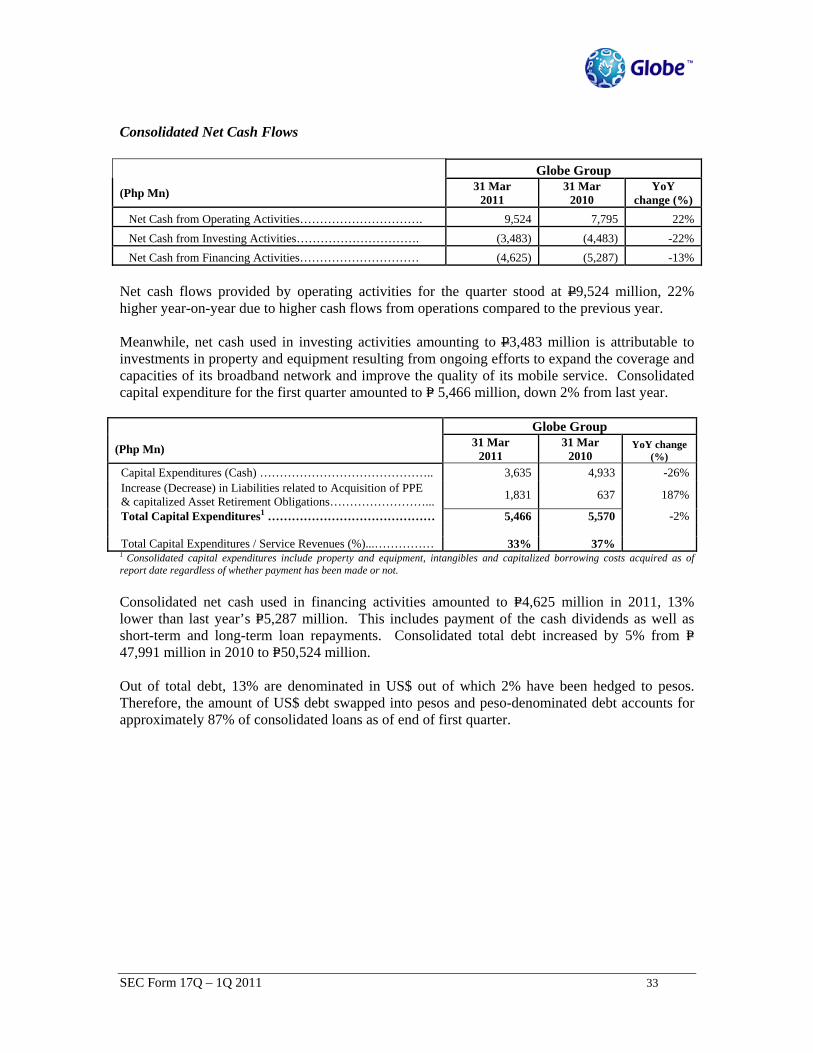

Consolidated Net Cash Flows

Globe Group

(Php Mn) 31 Mar 2011

31 Mar 2010

YoY change (%)

Net Cash from Operating Activities…………………………. 9,524 7,795 22% Net Cash from Investing Activities…………………………. (3,483) (4,483) -22% Net Cash from Financing Activities………………………… (4,625) (5,287) -13% Net cash flows provided by operating activities for the quarter stood at P9,524 million, 22% higher year-on-year due to higher cash flows from operations compared to the previous year. Meanwhile, net cash used in investing activities amounting to P3,483 million is attributable to investments in property and equipment resulting from ongoing efforts to expand the coverage and capacities of its broadband network and improve the quality of its mobile service. Consolidated capital expenditure for the first quarter amounted to P= 5,466 million, down 2% from last year.

Globe Group

(Php Mn) 31 Mar 2011

31 Mar 2010

YoY change (%)

Capital Expenditures (Cash) …………………………………….. 3,635 4,933 -26% Increase (Decrease) in Liabilities related to Acquisition of PPE & capitalized Asset Retirement Obligations……………………... 1,831 637 187%

Total Capital Expenditures1 …………………………………… 5,466 5,570 -2% Total Capital Expenditures / Service Revenues (%)...…………… 33% 37%

1 Consolidated capital expenditures include property and equipment, intangibles and capitalized borrowing costs acquired as of report date regardless of whether payment has been made or not.

Consolidated net cash used in financing activities amounted to P=4,625 million in 2011, 13% lower than last year’s P=5,287 million. This includes payment of the cash dividends as well as short-term and long-term loan repayments. Consolidated total debt increased by 5% from P=47,991 million in 2010 to P=50,524 million. Out of total debt, 13% are denominated in US$ out of which 2% have been hedged to pesos. Therefore, the amount of US$ debt swapped into pesos and peso-denominated debt accounts for approximately 87% of consolidated loans as of end of first quarter.

SEC Form 17Q – 1Q 2011 34

Below is the schedule of debt maturities for Globe for the years stated below based on total outstanding debt as of 31 March 2011: Year Due Principal *