Sector Report GPB Technology Predictions January 2011_final

13

c Important disclosures appear at the back of this report. GP Bullhound LLP is authorised and regulated by the Financial Services Authority in the United Kingdom Sector Update January 2011 Technology / Media / Telecoms GP BULLHOUND TECHNOLOGY PREDICTIONS 2011 Christian Lagerling [email protected] San Francisco: +1 415 986 0196 Per Roman [email protected] London: +44 (0) 207 101 7568 Julien Oussadon Justine Chan Florent Roulet Investors Ready to Open Pockets to Innovative Technologies In 2011 For the fourth year running, GP Bullhound is publishing its Technology Predictions for the upcoming year. As the global economy emerges from the financial crisis, we anticipate businesses and investors alike will capitalize their resources to invest in the next wave of innovation in 2011. Accordingly, many of our predictions seek to streamline the way we approach everyday tasks. In 2011, we anticipate consumers will take another step towards wireless by adopting shopping, dating, gambling, payments and even household management on mobile. The rise in augmented reality adoption will complement this, as we continue to merge the information on the web with our mobile lifestyles. Moreover, as mobile applications continue to proliferate we expect developer-friendly open platform benefits will extend Google’s Android lead over Apple’s iOS. In the wake of the explosion of mobile applications, we expect vendors to step up to provide real-time analysis and predictions of consumer behaviours. Additionally, we expect increasing mobility and pace of life will drive users to abridge communication messaging, favouring short messaging formats over blogs and long format emails. In another move towards increased mobility, we anticipate games will move into the cloud, reducing development and porting costs for developers and enabling gamers to access games and content real-time. As capital markets and investor appetite continues to grow, we also anticipate a comeback for solar thin films. Supported by increasing c-Si pricing and meaningful commercialization, we believe 2011 yields a turn of fortunes for the sector. All in all, as markets renew back to 2007 levels, we anticipate 2011 will yield a strong year of technological development. -------------------------------------------------- *Note that GP Bullhound acts or has acted as an advisor to some of the companies mentioned in this report. Please refer to disclaimer at the back for full disclosure INDEPENDENT TECHNOLOGY RESEARCH (1) 2011 PREDICTIONS: GOOGLE’S ANDROID DISTANCING APPLE’S IOS MOBILE PAYMENTS SET TO SURGE IN 2011 – GET READY FOR THE RACE SOCIAL SHOPPING, DATING AND GAMBLING WILL THRIVE ON MOBILE AUGMENTED REALITY APPLICATIONS TAKE-OFF, DRIVEN BY A LOCATION BASED SERVICES FOOTPRINT MOBILE AND SMART GRID APPLICATIONS OPEN THE DIGITAL HOME PRIVACY BECOMES A TOP PRIORITY FOR SOCIAL NETWORK USERS THIN FILM MAKES A COMEBACK AND VCS START TO EXIT TO STRATEGICS IN DROVES SHORT MESSAGING FORMAT WILL GAIN WIDER SUPPORT AND MOMENTUM GAMING MOVES INTO THE CLOUD A NEW GENERATION OF BUSINESS INTELLIGENCE AND DATA ANALYTICS CONSUMER APPS WILL EMERGE

-

Upload

romanpixell9199 -

Category

Documents

-

view

37 -

download

1

Transcript of Sector Report GPB Technology Predictions January 2011_final

c

Important disclosures appear at the back of this re port.

GP Bullhound LLP is authorised and regulated by the Financial Services Authority in the United Kingdom

Sector Update

January 2011

Technology / Media / Telecoms

GP BULLHOUND TECHNOLOGY PREDICTIONS 2011

Christian Lagerling [email protected]

San Francisco: +1 415 986 0196

Per Roman [email protected]

London: +44 (0) 207 101 7568

Julien Oussadon Justine Chan

Florent Roulet

Investors Ready to Open Pockets to Innovative Technologies In 2011

For the fourth year running, GP Bullhound is publishing its Technology

Predictions for the upcoming year.

As the global economy emerges from the financial crisis, we anticipate

businesses and investors alike will capitalize their resources to invest in the

next wave of innovation in 2011.

Accordingly, many of our predictions seek to streamline the way we approach

everyday tasks. In 2011, we anticipate consumers will take another step

towards wireless by adopting shopping, dating, gambling, payments and even

household management on mobile. The rise in augmented reality adoption will

complement this, as we continue to merge the information on the web with our

mobile lifestyles. Moreover, as mobile applications continue to proliferate we

expect developer-friendly open platform benefits will extend Google’s Android

lead over Apple’s iOS. In the wake of the explosion of mobile applications, we

expect vendors to step up to provide real-time analysis and predictions of

consumer behaviours. Additionally, we expect increasing mobility and pace of

life will drive users to abridge communication messaging, favouring short

messaging formats over blogs and long format emails.

In another move towards increased mobility, we anticipate games will move

into the cloud, reducing development and porting costs for developers and

enabling gamers to access games and content real-time.

As capital markets and investor appetite continues to grow, we also anticipate

a comeback for solar thin films. Supported by increasing c-Si pricing and

meaningful commercialization, we believe 2011 yields a turn of fortunes for the

sector.

All in all, as markets renew back to 2007 levels, we anticipate 2011 will yield a

strong year of technological development.

--------------------------------------------------

*Note that GP Bullhound acts or has acted as an advisor to some of the companies mentioned in this

report. Please refer to disclaimer at the back for full disclosure

INDEPENDENT TECHNOLOGY RESEARCH

(1)

2011 PREDICTIONS:

GOOGLE’S ANDROID DISTANCING APPLE’S IOS

MOBILE PAYMENTS SET TO SURGE IN 2011 – GET READY FOR THE RACE

SOCIAL SHOPPING, DATING AND GAMBLING WILL THRIVE ON MOBILE

AUGMENTED REALITY APPLICATIONS TAKE-OFF, DRIVEN BY A LOCATION BASED SERVICES FOOTPRINT

MOBILE AND SMART GRID APPLICATIONS OPEN THE DIGITAL HOME

PRIVACY BECOMES A TOP PRIORITY FOR SOCIAL NETWORK USERS

THIN FILM MAKES A COMEBACK AND VCS START TO EXIT TO STRATEGICS IN DROVES

SHORT MESSAGING FORMAT WILL GAIN WIDER SUPPORT AND MOMENTUM

GAMING MOVES INTO THE CLOUD

A NEW GENERATION OF BUSINESS INTELLIGENCE AND DATA ANALYTICS CONSUMER APPS WILL EMERGE

TMT PREDICTIONS 2011

2

GP Bullhound LLP January 2011

A RECAP OF GP BULLHOUND 2010 PREDICTIONS

Looking back at our “GP Bullhound Technology Predictions 2010” we are

pleased to note that several of our projections gained strong momentum

during the year, while a few showed early signs but still with some ways to

go.

Our first prediction that behavioural re-targeting will increasingly be

adopted by online retailers was confirmed with the market, reaching critical

mass in 2010 especially in the US. Several leading innovators received

more venture funding during the year (e.g. Criteo, MyThings, Cognitive

Match) while others were acquired by established Internet giants (e.g.

Dapper / Yahoo! or FetchBack / GSI Commerce).

Perhaps most obvious, the number of mobile applications exploded

during the year with Android gaining a significant market share and Apple’s

iPhone repeating its past successes with its 4th version. With the

confirmation of smartphones growing penetration in the consumer market,

augmented reality applications started to gain momentum. We noticed

particular opportunity for augmented reality in gaming applications due to

the high user interaction.

The tablet market did stage a comeback with the success of Apple’s iPad

leading the way. However, we will wait to see in 2011 if Apple and its

numerous followers using Google’s Android platform are able to capitalise

on this successful early adoption to reach the broader market. Ebook

applications will rely on tablets to explode in 2011. Even if several

channels and devices have adopted ebooks, tablets could prove to offer the

best user experience and provide significant opportunities for an upcoming

mass adoption of ebook applications.

In the online music , the battle has begun between the different business

models (download / streaming, advertising / subscription / purchase, etc.),

with Apple, Google/YouTube, Spotify, Deezer and Rdio as the main

combatants. However, winners are not quite defined yet.

Micro-transactions and virtual currencies moved in 2010 beyond the

original gaming sphere with customers increasingly conceiving to buy

certain goods online rather than at their local stores. As micro-payments

exploded, we anticipate the same to happen on mobile in 2011.

Several players in the electric and hybrid vehicles space have

demonstrated that innovation and quality could be combined to produce

affordable and reliable cars. Tesla Motors in the US (listed since June

2010), Micro-Vett and Ashwoods Automotive in Europe are expected to

continue expanding their production in 2011. Mass adoption is still to come

however.

Consolidation within the solar PV value chain has been one of the key

Cleantech themes of the year. Strategic and Asian players are driving this

consolidation (e.g. LDK / Solar Power). Large PV manufacturers are also

acquiring successful developers and their pipelines (e.g. First Solar /

NextLight and Edison Mission, Sharp / Recurrent Energy).

2010 Predictions:

“The year of Behavioral re-targeting”

“Augmented reality is becoming a reality...”

“Cloud computing drives green IT initiatives”

“Mobile applications become a mainstay”

“Virtual currencies & micro-transactions expand beyond games”

“The return of the tablet PC”

“ebook applications will explode across a multitude of devices and channels”

“Affordable electric and hybrid vehicles reach the broad demographics”

“Consolidation within the solar photovoltaics supply chain”

“Industry shakeout in online music distribution as the winners are defined”

–

–

����

����

����

–

����

–

����

����

TMT PREDICTIONS 2011

3

GP Bullhound LLP January 2011

Start-ups to lookout for:

London, UK

Mountain View, US

Mountain View, US

London, UK

Toulouse, France

GOOGLE’S ANDROID DISTANCING APPLE’S iOS

We expect that Android will increase its lead over Apple’s operating

systems (iOS) in 2011 due to its open platform benefits and increasing

mindshare amongst end users as well as developers. For the first time in

November, 2010, Android surpassed the iPhone in the US in a total

installed base of 61.5m smartphone subscribers. Android has already been

for months the leading operating system among recent acquirers.

Exhibit 1 – Top Smartphone Platforms in the US

19.6% 26.0%33.0%

45.0%

24.2%25.0%

27.0%

30.0%37.6%

33.5%

33.0%25.0%10.8% 9.0%

3.0%4.6% 3.9%

0%

20%

40%

60%

80%

100%

August 10 November 10 End of 2011 End of 2014

3-m

onth

ave

rage

-U

S s

mar

tpho

ne s

ubs.

age

d 13

+

Google / Android Apple RIM / Blackberry Microsoft Palm

Source: ComScore for 2010 data, GP Bullhound estimates for projections

After having competed on mobile devices only, rival operating systems

have now added the tablets market as a new battleground with specifically

designed versions (e.g. Android Honeycomb).

Exhibit 2 – Tablets and Mobile Handsets using Andro id and iOS

vs.

Source: Google, Samsung, Motorola, Apple

Google’s long time strategy to open up its technology to a variety of

manufacturers and application developers will be paying off as multiple

devices will hit the market (especially from Asian players such as Samsung,

LG or Acer keen to create fierce competition to US-based Apple) with a

plethora of quality apps being made available. In the meantime, Symbian

(Nokia-led rival open-source OS) has seen its market share consistently

shrinking mainly due to smartphones manufacturers preferring Android for

their best brand and user interface. Another competitive advantage for

Android lies in its wide range of potential mobile operators when Apple has

signed exclusivity agreements in several countries.

Even in terms of apps store, Google has opted for an open approach by

allowing other web merchants to enter the game. As an example, Amazon

has recently announced it will launch its own apps store for Android.

TMT PREDICTIONS 2011

4

GP Bullhound LLP January 2011

Start-ups to lookout for:

Paris, France

San Francisco, US

Rome, Italy

Munich, Germany

Palo Alto, US

MOBILE PAYMENTS SET TO SURGE IN 2011 – GET READY FOR THE RACE

The mobile landscape continues to grow strongly including a continued

slew of new payments providers emerging along with established players

increasingly diversifying their offerings. There are however a number of

more established players such as allopass, ZONG, Boku, Neomobile,

Obopay who are actively looking to partner with tier 1 merchants to

increase their reputational profile as trusted payment specialists.

The mobile payments market can be mapped out in various subsectors

incorporating pure play startups such as Square, Mi-Pay, Luup, Tyfone and

Bling Nation which have recently entered the market, to more established

players such as Allopass.

Exhibit 3 – Mobile Finance Taxonomy

Mobile BankingHandset Contact

Mobile

Payments

Remote Mobile

Payments

P2P Mobile

Payments

Mobile

Finance

Providers

/ Zetawire

Source: GP Bullhound

There are a number of technology trends which have surfaced and resulted

in a more favorable environment for the development of mobile payments

services. Firstly, the rise of smartphones has resulted in users having

access to Internet on the go and through high quality usable interfaces thus

reducing friction in the buying process. As a result, iPhones and other

smartphones have enabled mass consumption of diverse mobile content

and services, such as music, games, banking and shopping.

The mobile payments landscape is currently taking shape, resulting in a

fragmented position today where there around 5-10 key players. M&A

naturally follows, with recent market rumors that Google and Apple have

been bidding at five times revenue for US mobile payments specialist Boku.

We expect consolidation to accelerate and come from various angles

including handset manufacturers, social networks, Internet players,

payment processors, banks and telco carriers.

TMT PREDICTIONS 2011

5

GP Bullhound LLP January 2011

Start-ups to lookout for:

Palo Alto, US

Los Angeles, US

Zappli, San Francisco, US

Richmond, UK

London, UK

Stockholm, Sweden

Petah Tikva, Israel

New York, US

Melbourne, Australia

London, UK

London, UK

SOCIAL SHOPPING, DATING AND GAMBLING APPLICATIONS WILL THRIVE ON MOBILE

Three Internet services that revolutionise everyday life of millions of users

in the last few years are expected to massively hit the mobile space in

2011: Social Shopping, Dating and Gambling. They all share inherent

potential around location-based functionalities – tailored for the mobile.

More than just providing a mobile version of their online equivalents,

successful companies will create a different experience entirely dedicated

to mobile users. Winning suppliers will provide seamless interaction

between the three main mobile platforms (Blackberry, Android, iPhone).

Exhibit 4 – Three Key Options on Mobile in 2011

+ +

Dating Gambling Social Shopping

Source: GP Bullhound

As social shopping will continue to grow on the Int ernet in 2011, the

move to mobile will be based on the same success factors: bringing

together shopping communities and sharing recommend ations .

Following the explosion of social networks usage on smartphones in 2010,

retailers can initially only integrate popular sites to their platforms to make

sure shopping recommendations can easily be shares among friends’

networks via feeds page. In a more advanced move to mobile, several

mobile apps are based on in-store barcode scanning.

Group shopping will also find its mobile equivalent . Groupon acquired

mobile development firm Mob.ly in May 2010 and has since successfully

developed applications for iPhone and Android. We can easily imagine

group shopping websites suggesting local deals thanks to location-based

features in smartphones.

Online gambling is expected to experience significant geographic

expansion as it potentially becomes legal in several key US states in 2011

(e.g. New Jersey and California) while several additional European markets

will be deregulated (following France and Italy). The move to mobile will

allow punters to place bets or play ‘in casinos’ anytime and anywhere, thus

significantly increasing user options. As an example, UK bookmakers, after

having successfully transitioned to online gambling, have recently launched

mobile applications to allow real-time betting via smartphones.

After several years of uncertain results, mobile dating will finally become a

reality. Location-based mobile data applications are flourishing at a fast

pace, indicating in real-time who is single around you (e.g. in an airport or

even simply in the street). Thanks to 24/7 access and 3G-enabled video

chat, mobile smartphones will offer a very strong medium for dating

communities.

TMT PREDICTIONS 2011

6

GP Bullhound LLP January 2011

Start-ups to lookout for:

San Francisco, CA, USA

Denver, CO, USA

Amsterdam, Netherlands

Boston, MA, USA

London, UK

Boston, MA, USA

AUGMENTED REALITY APPLICATIONS TAKE OFF, DRIVEN BY A LOCATION BASED SERVICES FOOTPRINT

Since 2008, LBS applications have grown exponentially to the current level

of approximately 6,000 applications. Leveraging the groundwork laid by

LBS applications and enabled devices, mobile augmented reality

applications garnered significant buzz and from bloggers, media and early

adopters in 2010. We hereby repeat our 2010 prediction with the added

momentum of these LBS. With the anticipated relase of the next-generation

iPad and other tablets and growing smartphone adoption, we expect LBS

devices to reach critical mass in 2011, driving widespread popularity of

augmented reality (AR) applications.

Exhibit 5 – LBS Subscriber Forecast

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

2007 2008 2009 2010 2011 2012 2013

Americas Europe Asia

Source: Gartner, GP Bullhound

Gartner Research expects that over one-third of the mobile workforce will

use AR applications by 2014, as today’s consumers exhibit increasing

reliance on mobile access to information for everyday life.

Exhibit 6 – Yell Employs AR Application for Listing s

Source: Yell.com

According to a recent quote by metaio, “Everyone will be on the AR

bandwagon in 2011. Even industrial companies and the military will use

mobile AR applications, especially for improving workflows and security.”

TMT PREDICTIONS 2011

7

GP Bullhound LLP January 2011

Start-ups to lookout for:

Cambridge, United Kingdom

Laguna Beach, CA, USA

Germantown, MD, USA

MOBILE AND SMART GRID APPLICATIONS OPEN THE DIGITAL HOME

Today’s smart phones and tablets have captivated consumers for their

personal communication and entertainment capabilities, and now, suppliers

of home control systems are leveraging these next-generation devices to

help consumers control and manage the equipment in their homes.

After years of sluggish developments, leveraging the new mobile devices

and platforms, homeowners are finally being given the proper tools to

access and control their light, heating, air conditioning and more via the

Internet, irrespective of their physical location.

Exhibit 7 – Intel Home Dashboard

Source: Intel

Furthermore, as AMI deployment continues to fuel smart grid growth,

companies including Cisco, GE, Intel, and Microsoft are creating consumer

energy management solutions that integrate with the smart grid

infrastructure. Many of these suppliers have enabled their solutions for use

on everyday consumer devices. As shown below, the GE Nucleus software

is enabled for access from any browser-enabled phone or PC.

Exhibit 8 – GE Nucleus Software

Source: GE

TMT PREDICTIONS 2011

8

GP Bullhound LLP January 2011

Start-ups to lookout for:

Bellevue, WA, USA

Morristown, NJ, USA

Ottawa, Canada

Evanston, IL, USA

PRIVACY BECOMES A PRIORITY FOR SOCIAL NETWORK USERS

Social networks have undoubtedly become an integral part of the Internet

experience, overtaking search engines as the primary site through which

people access the Internet in 2010. As shown below, our actual networks

are significantly more complex than those currently reflected on Facebook.

Exhibit 9 – Facebook Social Graph

Source: Forrester

As our digital relationships continue to grow in depth and reach, privacy

amongst our relationship pools will play an increasingly important role in the

social web.

In today’s competitive job market, a growing number of employers and

recruiters are employing searches on social networks and search engines

to research potential candidates. According to the AOL Technology Blog,

Switched.com, “78 percent of recruiters and HR professionals use search

engines to research applicants. 63 percent use social networking sites and

59 percent turn to photo and video sharing sites like YouTube or Flickr.”

Further, many corporations have established dedicated groups to monitor

employees’ Facebook presence.

Accordingly, social network “cleaning” services have recently gained

momentum. As social networks quickly become the primary channel for

personal communication, it is increasingly important for users to have full

clarity surrounding the access given and content present on their social

profiles.

Eventually, we anticipate the need for privacy will drive users to separate

their social networks into core life functions, such as friends, family,

colleagues, etc., thereby rerestricting messages and status updates to each

applicable groups.

TMT PREDICTIONS 2011

9

GP Bullhound LLP January 2011

Start-ups to lookout for:

Loveland, US

Bitterfeld-Wolfen, Germany

Santa Clara, US

San Jose, US

Frankfurt, Germany

THIN FILM MAKES A COMEBACK AND VCS START TO EXIT TO STRATEGICS IN DROVES...

Having been around since the mid-eighties, thin film PV technologies only

had their first significant breakthrough about a decade ago as the industry

was looking for next-gen technologies to replace the maturing c-Si. Large

amounts of venture capital investment went into the promising new

technologies such as CIGS, CdTe and a-Si. In the last few years, thin film

companies have largely disappointed the market by not being able to

improve conversion efficiency and to scale down its cost structure as

quickly as originally anticipated.

However, we have recently observed several critical trends suggesting that

thin film might be staging a late comeback. Firstly, silicon prices which have

been steadily falling are on their way up again, driven by increasing supply

constraints. Polysilicon, the raw material in c-Si cells, still represents a

meaningful portion of the total manufacturing cost.

We are also detecting increased interest recently in thin film by industrial

companies who understand the potential and have much to offer in terms of

manufacturing expertise and deep pockets. Companies such as GE, Saint-

Gobain, Hyundai, TSMC and Walsin have all recently announced strategic

alliances, investments and/or acquisitions into the thin film sector.

Many of the inherent thin film advantages remain intact and have proven

their value as the market has matured. CIGS and a-Si are lighter, flexible

and more aesthetic than c-Si and as such are appealing solutions for the

BIPV segment.

Exhibit 10 – Historic and Projected Polysilicon Pri ces

5970

94

6070

0

20

40

60

80

100

2006A 2007A 2008A 2009A 2010E

US

$ pe

r kg

Source: GP Bullhound

With more than 150 individual thin film companies in thin film, we predict

massive consolidation driven by the entry of industrial players with their

capital and manufacturing might.

We believe VCs will need to realign their expectations as returns are likely

to disappoint. Unlike the chip sector which provided VC style returns

supported by Moore’s Law, the solar sector has natural efficiency ceilings

and cost floors and as such improvements are in steps rather than bounds.

Hence, risk capital is more suited from strategic players that can take a

longer view on returns. VCs will use renewed momentum to get out of these

investments as they will not be able to continue to support the capital

intensive nature of this industry.

TMT PREDICTIONS 2011

10

GP Bullhound LLP January 2011

Start-ups to lookout for:

Palo Alto, US

Bellevue, US

Aliso Viejo, US

San Francisco, US

Los Angeles, US

Paris, France

GAMING MOVES INTO THE CLOUD

Following the massive and sudden upsurge of casual and social gaming

over the last two years, the interactive entertainment industry continues to

move into the cloud. Whether it is called cloud gaming, server-based

gaming, game-on-demand, or game-as-a-service, we expect this new

delivery method to gain significant traction in 2011. Companies like Onlive,

Steam or Gaikai have successfully launched their service and pose a

serious threat to the long-lasting console vendors’ oligopoly. Pressured by

gaming publishers and developers (keen to reduce development and

porting costs), platform vendors like Nintendo, Microsoft and Sony face

unprecedent challenges and will likely have to reinvent their business

models.

Exhibit 11 – Cloud Gaming vs. Traditional Gaming Ec osystem

Console Gaming Environment

PlatformVendors

Wii / DS

Xbox 360

PS3 / PSP

iPhone / iPad

GamingContent

1st Party Publishers

3rd Party Publishers

etc.

Distribution

Retail Distribution

etc.

Digital Distribution

Cloud Gaming Environment

Providers GamingContent

3rd PartyPublishers

Independentself-published

developers

Distribution

� Subscription-

based

� Per-game

download

� Time-based

All Digital

Source: GP Bullhound

Using powerful compression technology, cloud gaming enables gamers to

stream content in real-time from centralised servers while providing access

to extended libraries of premium gaming content across a variety of genres

on both a PC or a Mac through either a Web-browser or a micro-TV

adapter. As opposed to the platform-led gaming environment, cloud gaming

companies provide a pervasive single entry-point to interactive

entertainment combined with both flexible and attractive pricing models.

Certain independent developers like Valve Software launched Steam (c. 25

million subscribers) a cloud platform which distributes digitally both

proprietary and third-party content.

Non-traditional gaming players such as carriers see in cloud gaming the

potential to drive additional revenues while reducing subscribers churn.

SFR recently launched a commercial IPTV games-on-demand service

using their existing set-top box for playing games. In November 2010,

Portugal Telecom launched Meo Jogos, a gaming-on-demand service

powered by Playcast Media, as part of their triple-play offering. The service

is only available on PCs running Microsoft Windows.

Although there is still some sceptism about whether these systems can

deliver a high-quality gaming experience in massive demand situations, we

expect console gaming as we know it to disapeear either with this current

console cycle or the next. We believe the focus will continue to shift away

from the actual hardware to the network.

TMT PREDICTIONS 2011

11

GP Bullhound LLP January 2011

Start-ups to lookout for:

San Francisco, US

New York, US

New York, US

San Francisco, US

London, UK

San Francisco, US

New York, US

SHORT MESSAGING FORMAT WILL GAIN WIDER SUPPORT AND MOMENTUM

If Facebook confirmed its immense potential in 2010, 2011 might well be

the year of Twitter in the context of an increased use of short messaging

format on the Internet, at the expense of blogs and long format emails.

Exhibit 12 –Twitter’s Follow-Buttons and Tweet-Butt ons Flourish on the Web

Source: GP Bullhound, Twitter

Driven by a data, information and communication overflow, Internet and

mobile users will increasingly rely on short messaging format to easily

share their thoughts, locations, articles, videos and invites… Twitter and

live news feeds in other social networks such as Facebook or LinkedIn are

today the most popular platforms. Like in the past you used to call a friend,

in 2011 you will use your smartphone to tweet and start a discussion with

the same friends but also with a list of followers you often merely know.

This trend will have a negative impact on the number of blogs and personal

websites as well as on the press and public relations sectors. To share

personal opinion or important news to a large audience, Twitter and

equivalent platforms such as Yammer or Tumblr will increasingly be a

viable alternative (e.g. details of Prince William’s wedding have been made

public on Twitter instead of a traditional press release via traditional media).

Blog articles, longer to write, will predominantly be expert views based on a

detailed analysis. For less formal and straight-to-the-point ideas, shorter

messages will be preferred.

Exhibit 13 – Twitter can also easily be integrated within Blogs via Widgets

Source: GP Bullhound, Bloggerbuster.com

In professional environments, technology and policy will enforce people’s

choice of shorter format messaging in internal communications. As e-mail

tends to take too long to respond to and can suffer inbox overflow,

companies will be encouraged to implement policies favouring getting faster

at responding such as short messaging.

A new approach to handle emails detailed on http://two.sentenc.es/

suggests treating email responses just like SMS by using a limited number

of letters and sentences per email. This way, emails become faster to write

and more likely to be read with the recipient feeling less intimidated than in

front of a long and well-structured email.

TMT PREDICTIONS 2011

12

GP Bullhound LLP January 2011

Start-ups to lookout for:

Redwood City, US

Chicago, US

Fort Washington, US

London, UK

Berlin, Germany

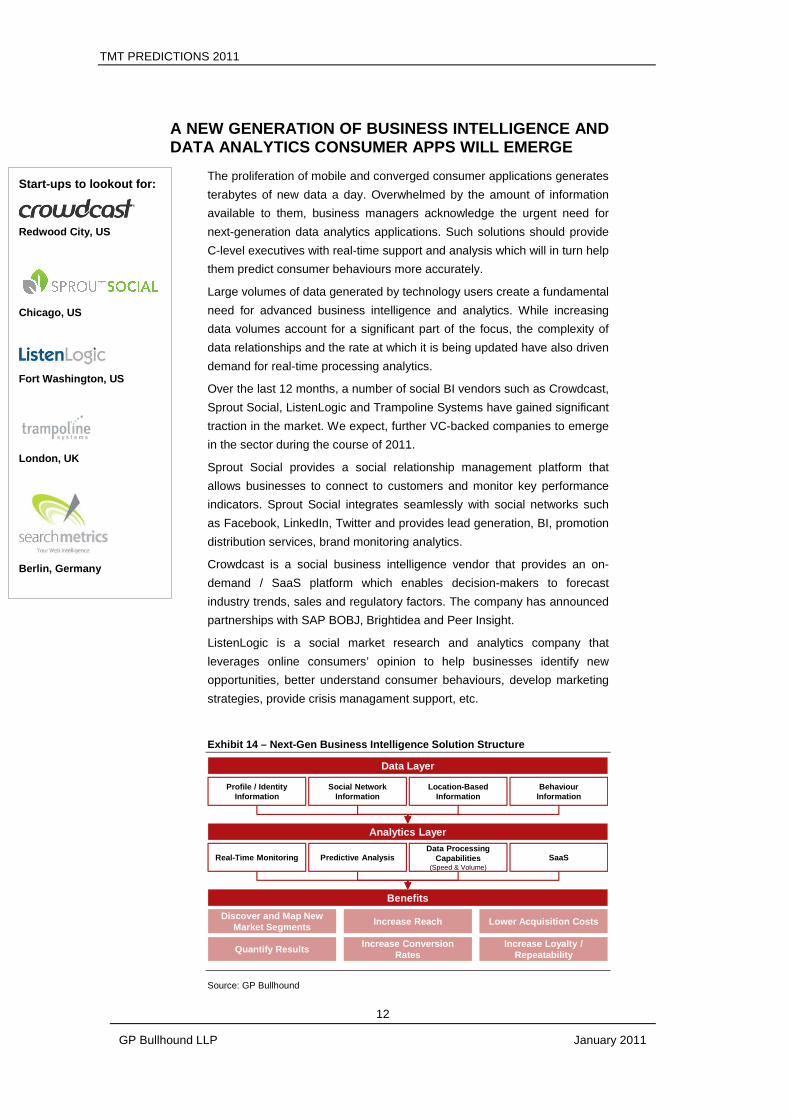

A NEW GENERATION OF BUSINESS INTELLIGENCE AND DATA ANALYTICS CONSUMER APPS WILL EMERGE

The proliferation of mobile and converged consumer applications generates

terabytes of new data a day. Overwhelmed by the amount of information

available to them, business managers acknowledge the urgent need for

next-generation data analytics applications. Such solutions should provide

C-level executives with real-time support and analysis which will in turn help

them predict consumer behaviours more accurately.

Large volumes of data generated by technology users create a fundamental

need for advanced business intelligence and analytics. While increasing

data volumes account for a significant part of the focus, the complexity of

data relationships and the rate at which it is being updated have also driven

demand for real-time processing analytics.

Over the last 12 months, a number of social BI vendors such as Crowdcast,

Sprout Social, ListenLogic and Trampoline Systems have gained significant

traction in the market. We expect, further VC-backed companies to emerge

in the sector during the course of 2011.

Sprout Social provides a social relationship management platform that

allows businesses to connect to customers and monitor key performance

indicators. Sprout Social integrates seamlessly with social networks such

as Facebook, LinkedIn, Twitter and provides lead generation, BI, promotion

distribution services, brand monitoring analytics.

Crowdcast is a social business intelligence vendor that provides an on-

demand / SaaS platform which enables decision-makers to forecast

industry trends, sales and regulatory factors. The company has announced

partnerships with SAP BOBJ, Brightidea and Peer Insight.

ListenLogic is a social market research and analytics company that

leverages online consumers’ opinion to help businesses identify new

opportunities, better understand consumer behaviours, develop marketing

strategies, provide crisis managament support, etc.

Exhibit 14 – Next-Gen Business Intelligence Solutio n Structure

Data Layer

Profile / Identity Information

Social Network Information

Location-Based Information

BehaviourInformation

Analytics Layer

Quantify Results

Lower Acquisition Costs

Increase Loyalty / Repeatability

Increase Conversion Rates

Discover and Map New Market Segments

Increase Reach

Real-Time Monitoring Predictive AnalysisData Processing

Capabilities(Speed & Volume)

SaaS

Benefits

Source: GP Bullhound

TMT PREDICTIONS 2011

13

GP Bullhound LLP January 2011

THE GP BULLHOUND TEAM

GP Bullhound is a research-centric investment bank headquartered in

London, with offices in San Francisco.

Hugh CampbellFounder / PartnerCitibank,Goldman Sachs

Guillaume BonnetonPartnerJefferies International,Deutsche Bank

Frank SchmittDirectorUBS, Arma Partners

Amanjit DhamiAssociateUBS

Helene JonssonAssistantKaplan Financial

Cecilia RomanDirector of MarketingArthur Andersen,Morgan Stanley

Manish Madhvani Founder / PartnerBarclays PE

Lord Clive HollickPartnerKKR, ProsiebenNielsen, Diageo

Claudio AlvarezVice PresidentEdison InvestmentExecution Ltd

Remy ValetteAssociateSociété Générale

Eve LimAssistantNEA

Rakhdeep DhaliwalFinancial ControllerSevacare

Christian LagerlingFounder / PartnerBarclays Capital,BZW

Graeme BayleyPartner / CFO & COOHSBC

Julien OussadonVice PresidentArma Partners,Société Générale

Justine ChanAssociateHarris Williams

Nataly BeanReceptionistSuper Yacht Cup

Lina EinarssonEvents ManagerIndigoferaKempinski

Martin SmithNon-exec ChairmanCSFB/DLJ, New Star

Alec DaffernerPartner / Head of USUBS, Volpe Brown W.

Antony NorthropSenior AdvisorLazard, Touchstone

Carl BergholtzVice PresidentJefferiesInternational

Sofie EmtesjoAssistantLansdowne Partners, Accenture

Florent RouletAnalystBofA Merrill Lynch,Bryan Garnier

Per RomanFounder / PartnerAutoDesk,Lehman Brothers

André ShortellPartnerCitibank

Mats JohanssonSenior AdvisorFuturemedia plc, Thursley Group

Sasha AfanasievaAssociateMerrill Lynch

Sofia SturessonAssistantOfcom

Malcolm FergusonAnalystBofA Merrill Lynch

Registered office: GP Bullhound LLP, 52 Jermyn Street, London, SW1Y 6LX http://www.gpbullhound.com, [email protected], +44 20 7101 7560 GP Bullhound LLP is or has been engaged as an advisor in the past twelve months to the following companies mentioned in this report: Calyxo, Mobcast and Neomobile.

Disclaimer: Information contained in the document does not constitute an offer to buy or sell or the solicitation of any offer to buy or sell any securities. This document is made available for general information purposes only and is intended for professional investors who have a high degree of financial sophistication and knowledge. This document and any of the products and information contained herein are not intended for the use of retail investors in the UK or any other territory. Although all reasonable care has been taken to ensure that the information contained in this document is accurate and current, no representation or warranty, express or implied, is made by GP Bullhound LLP as to its accuracy, completeness and currency. This report contains forward-looking statements, which involve risks and uncertainties. Actual results may differ significantly from the results described in the forward-looking statements. In particular, but without limiting the preceding sentences, you should be aware that statements of fact or opinion made, may not be up-to-date or may not represent the current opinion (whether public or confidential) of GP Bullhound LLP. In addition, opinions and estimates are subject to change without notice. This report does not constitute a specific investment recommendation or advice upon which you should rely based upon, or irrespective of, your personal circumstances. Use of this document is not a substitute for obtaining proper investment advice from an authorized investment professional. Potential retail investors are urged to consult their own authorized investment professional before entering into any investment agreement. Past performance of securities is not necessarily a guide to future performance and the value of securities may fall as well as rise. In particular, investments in the technology sector can involve a high degree of risk and investors may not get back the full amount invested. GP Bullhound LLP is authorised and regulated by the Financial Services Authority in the United Kingdom and is registered in England No. OC352636