![pdf - Mathematics - Encyclopedia Dictionary of Mathematics [Section C]](https://static.fdocuments.us/doc/165x107/546c8b5fb4af9fb8698b4ce0/pdf-mathematics-encyclopedia-dictionary-of-mathematics-section-c.jpg)

pdf - Mathematics - Encyclopedia Dictionary of Mathematics [Section C]

Upload

ellis-gravelyCategory

view

215download

2

Section 1.1, Slide 1

Copyright © 2014, 2010, 2007 Pearson Education, Inc.Copyright © 2014, 2010, 2007 Pearson Education, Inc.

Section 8.3, Slide 1

Consumer Mathematics

The Mathematics of Everyday Life

8

Copyright © 2014, 2010, 2007 Pearson Education, Inc.Copyright © 2014, 2010, 2007 Pearson Education, Inc.

Section 8.3, Slide 2

Consumer Loans8.3• Determine payments for an add-

on loan.• Compute finance charges on a

credit card using the unpaid balance method.

Copyright © 2014, 2010, 2007 Pearson Education, Inc.Copyright © 2014, 2010, 2007 Pearson Education, Inc.

Section 8.3, Slide 3

• Use the average daily balance method to compute credit card charges.

• Compare credit card finance charge methods.

Consumer Loans8.3

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 4

The Add-On Interest Method

Loans having a fixed number of payments are called closed-ended credit agreements (or installment loans).

Each payment is called an installment.

The interest charged on a loan is often called a finance charge.

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 5

The Add-On Interest Method

This method is sometimes called the add-on interest method because we are adding on the interest due on the loan before determining the payments.

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 6

• Example: If you take out an add-on loan for $720 for 2 years at an annual interest rate of 18%, what will be your monthly payments?

The Add-On Interest Method

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 7

• Example: If you take out an add-on loan for $720 for 2 years at an annual interest rate of 18%, what will be your monthly payments?

• Solution: First calculate the interest:

Add interest to the purchase price:

Find the payment:

The Add-On Interest Method

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 8

The Unpaid Balance Method

With open-ended credit, you may be making monthly payments on your loan, but you may also be increasing the loan by making further purchases.

With the unpaid balance method, the interest is based on the previous month’s balance.

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 9

The Unpaid Balance Method

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 10

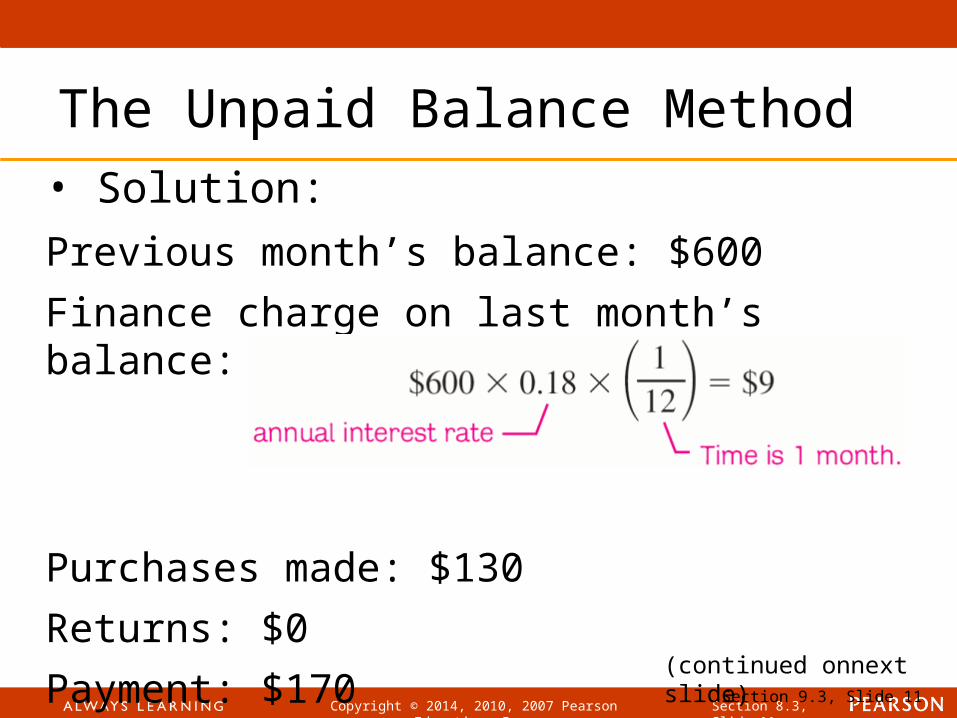

• Example: The annual interest rate on a credit card is 18% and the unpaid balance at the beginning of last month was $600. Since then, a purchase of $130 and a payment of $170 were made.

Using the unpaid balance method, what is the credit card bill this month? What is the finance charge next month?

The Unpaid Balance Method

(continued on next slide)

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 11Section 9.3, Slide 11

• Solution:

Previous month’s balance: $600

Finance charge on last month’s balance:

Purchases made: $130

Returns: $0

Payment: $170

The Unpaid Balance Method

(continued onnext slide)

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 12

Amount owed:

The Unpaid Balance Method

Finance charge for next month:

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 13

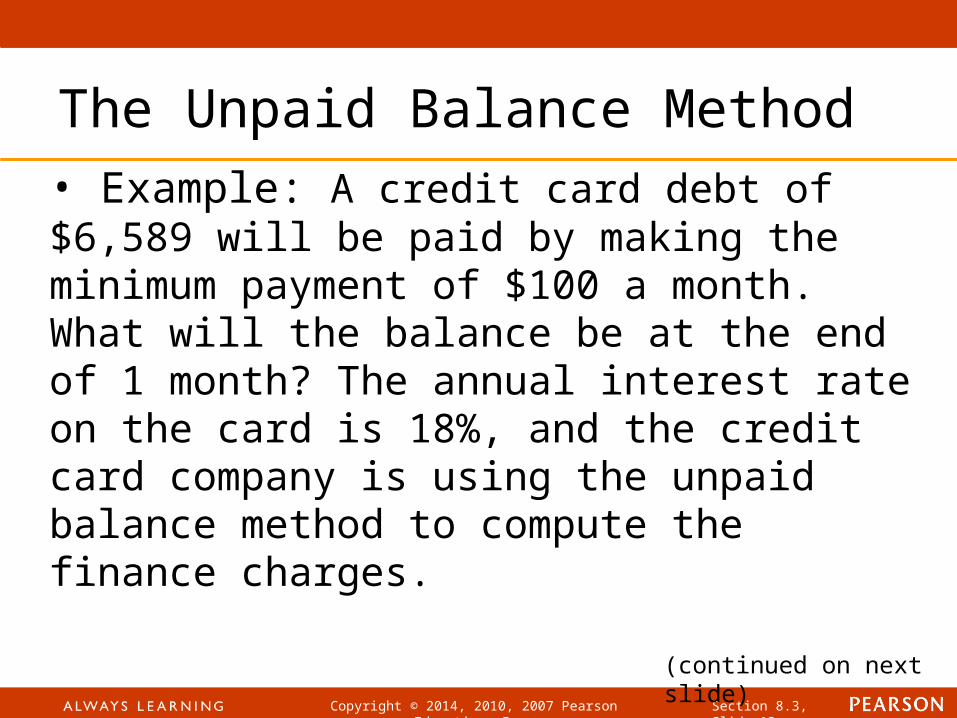

• Example: A credit card debt of $6,589 will be paid by making the minimum payment of $100 a month. What will the balance be at the end of 1 month? The annual interest rate on the card is 18%, and the credit card company is using the unpaid balance method to compute the finance charges.

The Unpaid Balance Method

(continued on next slide)

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 14

• Solution:

Unpaid balance: 6,589 – 100 = $6,489

Amount owed:

Your $100 payment has reduced your debt by only 6,589 – 6,586.34 = $2.66.

The Unpaid Balance Method

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 15

The Average Daily Balance Method

In the average daily balance method, the balance is the average of all daily balances for the previous month.

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 16

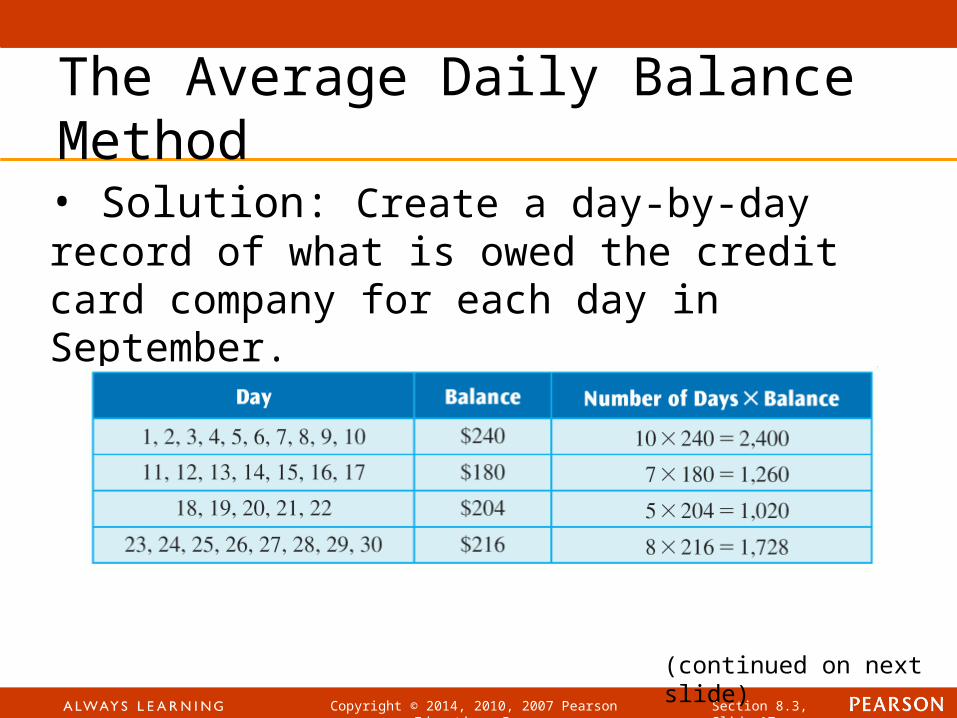

• Example: At the beginning of September a credit card has a balance of $240. The card has an annual interest rate of 18%, and during September the following adjustments were made on the account:

September 11: payment - $60 creditSeptember 18: charge - $24 iTune downloadsSeptember 23: charge - $12 gasoline.

Use the average daily balance method to compute the finance charge that will appear on the next statement.

(continued on next slide)

The Average Daily Balance Method

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 17

• Solution: Create a day-by-day record of what is owed the credit card company for each day in September.

The Average Daily Balance Method

(continued on next slide)

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 18

The Average Daily Balance Method

Average daily balance:

We see that P = 213.60, r = 0.18, and t =

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 19

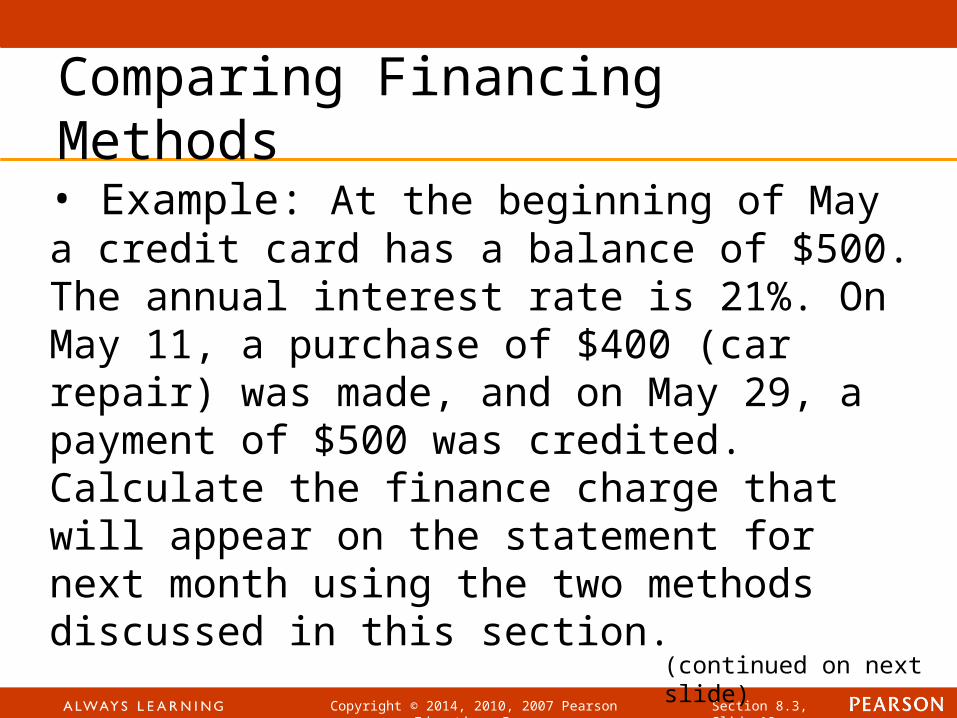

• Example: At the beginning of May a credit card has a balance of $500. The annual interest rate is 21%. On May 11, a purchase of $400 (car repair) was made, and on May 29, a payment of $500 was credited. Calculate the finance charge that will appear on the statement for next month using the two methods discussed in this section.

(continued on next slide)

Comparing Financing Methods

Copyright © 2014, 2010, 2007 Pearson Education, Inc. Section 8.3, Slide 20

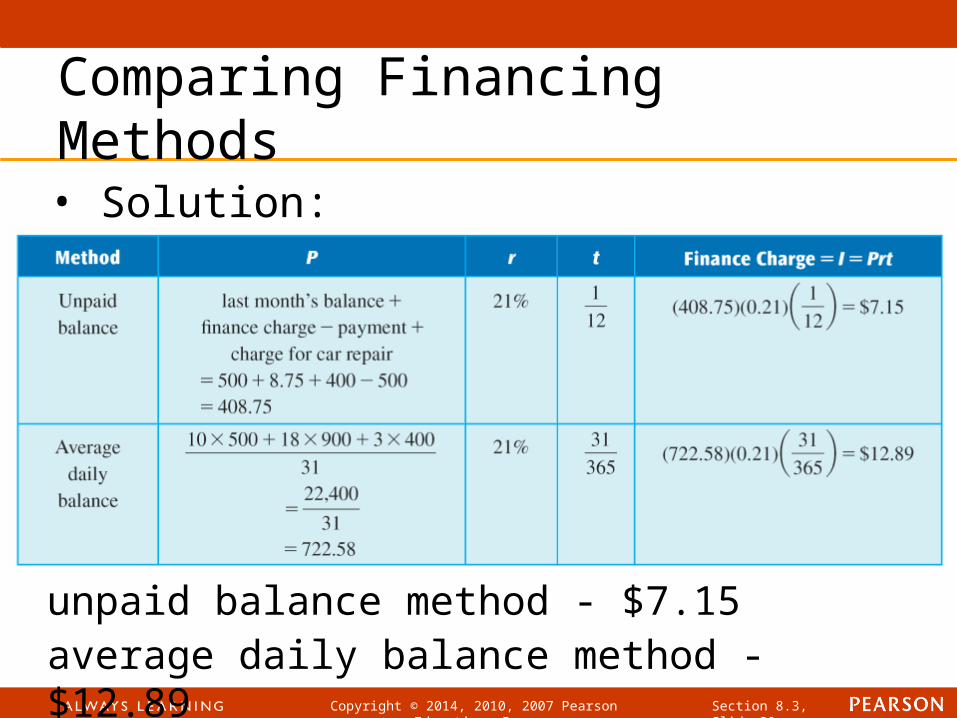

• Solution:

Comparing Financing Methods

unpaid balance method - $7.15 average daily balance method - $12.89

![(eBook-PDF) - Mathematics - Encyclopedia Dictionary of Mathematics [Section D]](https://static.fdocuments.us/doc/165x107/553eeb774a7959c30f8b4642/ebook-pdf-mathematics-encyclopedia-dictionary-of-mathematics-section-d.jpg)