Secrets to our Success at CSUN Margo L Dutton, Director, Accounting and Reporting Robin Patterson,...

17

Secrets to our Success at CSUN Margo L Dutton, Director, Accounting and Reporting Robin Patterson, Assistant Director CSU, Northridge April 24, 2015

-

Upload

jessie-oliver -

Category

Documents

-

view

213 -

download

0

Transcript of Secrets to our Success at CSUN Margo L Dutton, Director, Accounting and Reporting Robin Patterson,...

Secrets to our Successat CSUN

Margo L Dutton, Director, Accounting and Reporting

Robin Patterson, Assistant Director

CSU, Northridge

April 24, 2015

Campus InformationMain Campus Located in Northridge

Fall 2014 enrollment 40,131

Nine Colleges (Includes Extended Learning)

65 Baccalaureate

24 Credential Programs

18 Certificate Programs

58 Master’s Degrees

3 Doctoral Programs

Five Auxiliary Organizations

April 2015 Year-End GAAP Training

2

Organization Chart

Director

Financial Accounting

Support Specialist

Assistant Director

GAAP and Fund Accounting

Financial Accounting

Support Specialist

Student Assistant

Financial Accounting

Support Specialist

Student Assistant

Accountant

State Trust

April 2015 Year-End GAAP Training

3

Learning Objectives

• Planning for Interim and Year-end• Develop a Campus PBC list• Effectively Utilize and Manage Staff• Develop campus relationships • Manage campus deadlines

April 2015 Year-End GAAP Training 4

Wang, Lily

What I will share

• Interim planning• CSUN Approach• Campus PBC• KPMG Matrix

• Year - End Planning• CSUN Approach• Campus PBC

April 2015 Year-End GAAP Training 5

Interim planning

• During Interim, KPMG reviews and tests:• Internal Controls• Updates campus procedures • Compliance Testing Only

April 2015 Year-End GAAP Training 6

Campus preparation for Interim• Receive the Approved KPMG Interim PBC• Create Campus PBC • Done immediately upon receipt from the CO• Add columns for Responsible person and deadline

due to GAAP Coordinator

• Work with KPMG staff before arrival• to Obtain the Sample Selections• Set up necessary meetings with Key Employees to

discuss internal control procedures

April 2015 Year-End GAAP Training 7

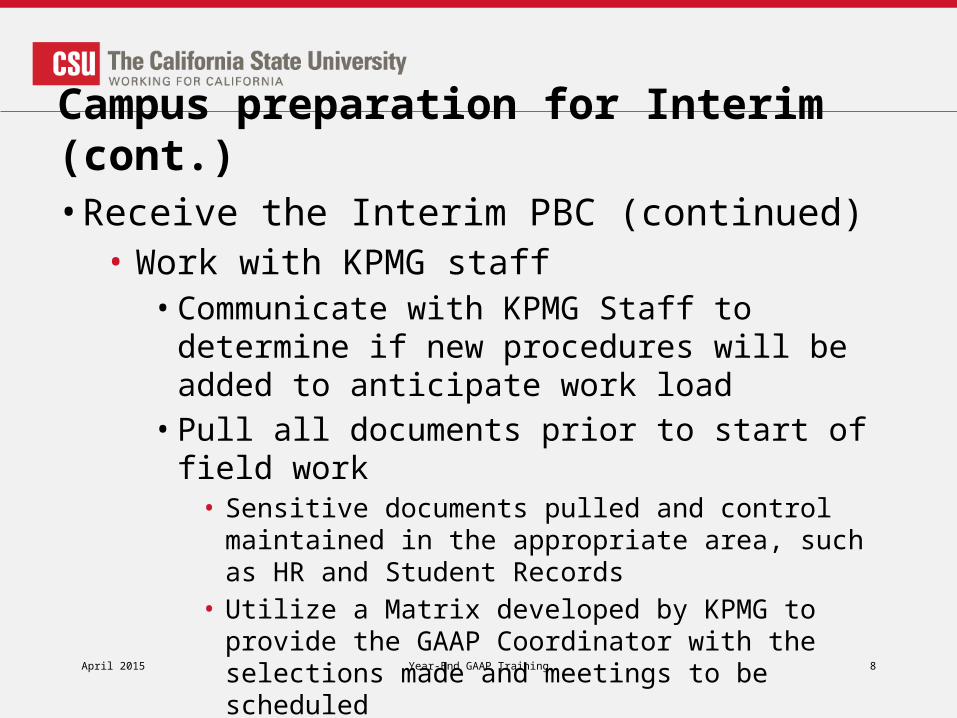

Campus preparation for Interim (cont.)• Receive the Interim PBC (continued)• Work with KPMG staff • Communicate with KPMG Staff to determine if new

procedures will be added to anticipate work load• Pull all documents prior to start of field work

• Sensitive documents pulled and control maintained in the appropriate area, such as HR and Student Records

• Utilize a Matrix developed by KPMG to provide the GAAP Coordinator with the selections made and meetings to be scheduled

April 2015 Year-End GAAP Training 8

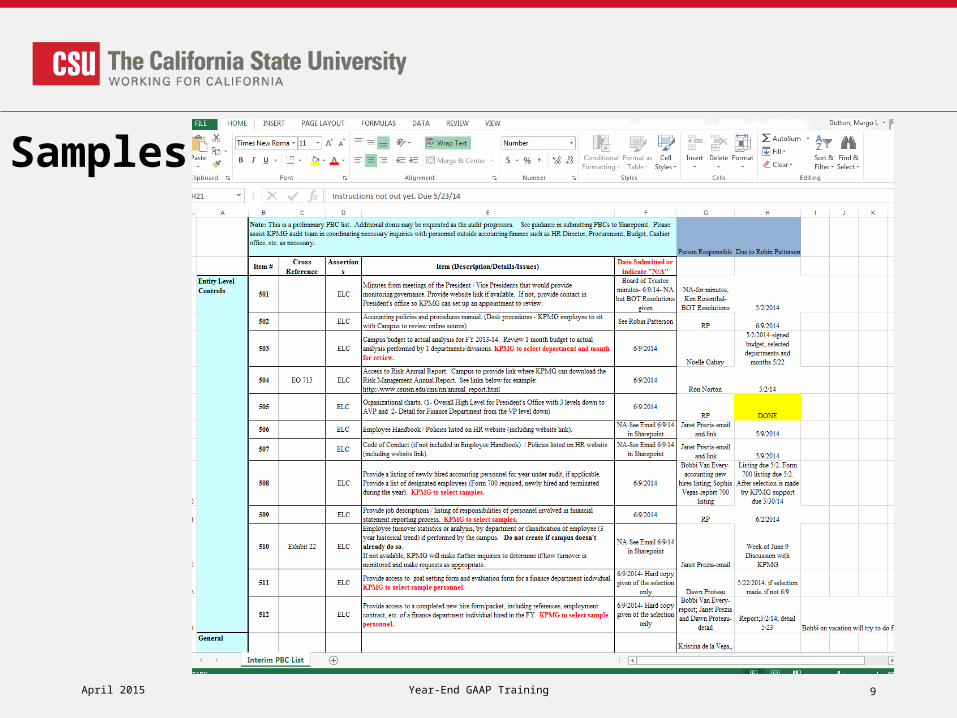

April 2015 Year-End GAAP Training 9

Samples

April 2015 Year-End GAAP Training 10

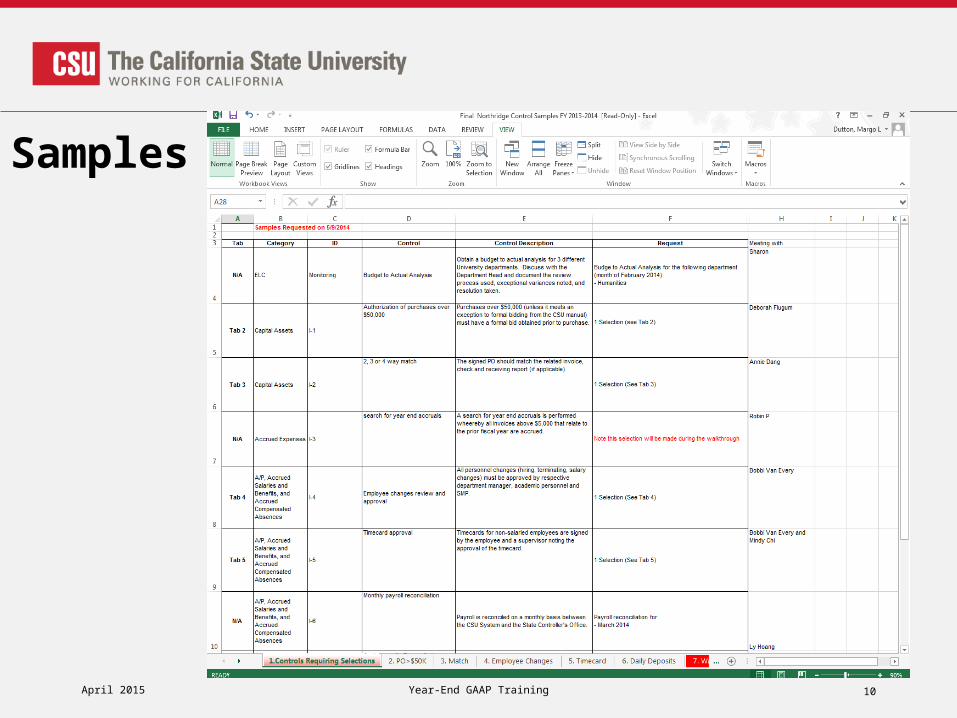

Samples

April 2015 Year-End GAAP Training 11

Samples

Year End Planning and Management

• Campus receives the approved PBC list• Build campus PBC adding several items:• Adds the two columns for the Responsible Party

and the Due Date to the GAAP coordinator• Campus only PBC’s such as Depository• Additional detailed supporting documents• The person who “owns” the work during the year

“owns” the preparation of specific schedules• Deferred Revenue Reasonableness test• Detailed support for Accrued Salaries

April 2015 Year-End GAAP Training

12

Year End Planning and Management (cont.)

• Build campus PBC adding several items (cont.)• Accounting and Reporting staff complete lead

sheets from the detailed supporting documents

• Emails the Campus PBC to all campus personnel identified as being responsible for items• Sends reminder emails a day or two before due if

not yet received.

April 2015 Year-End GAAP Training13

Year End Planning and Management (cont.)

• GAAP Coordinator manages the entire process• Cultivates relationships with responsible parties• Sets due dates. Strategy for setting due dates• In conjunction with the Director, assigns lead

sheets and other tasks.• Books and/or oversees the recording of all pass

down entries.

April 2015 Year-End GAAP Training 14

Year End Planning and Management (cont.)

• GAAP Coordinator manages the entire process• Requires explanations of significant differences

from year to year on supporting documents and lead. • This saves significant time in the Fluctuation

Analysis, and SRB audit responses• Minimizes follow up questions from the auditor.

April 2015 Year-End GAAP Training 15

Campus PBC

April 2015 Year-End GAAP Training16