Uncalimed Dividend (2019-20 Interim Dividend) shareholders ...

1

Second QuarterEnded June 30, 2017

2

Except for historical information provided herein, this presentation may contain information andstatements of a forward-looking nature concerning the future performance of Dorel Industries Inc.These statements are based on assumptions and uncertainties as well as on management's bestpossible evaluation of future events. The business of the Company and these forward-lookingstatements are subject to a number of risks and uncertainties that could cause actual results todiffer from expected results. Important factors which could cause such differences may include,without excluding other considerations, general economic conditions; changes in product costs andsupply channels; foreign currency fluctuations; customer and credit risk including the concentrationof revenues with a small number of customers; costs associated with product liability; changes inincome tax legislation or the interpretation or application of those rules; the continued ability todevelop products and support brand names; changes in the regulatory environment; continuedaccess to capital resources and the related costs of borrowing; changes in assumptions in thevaluation of goodwill and other intangible assets; and there being no certainty that Dorel’s currentdividend policy will be maintained. A description of the above mentioned items and certainadditional risk factors are discussed in the Company’s Annual MD&A and Annual Information Form,filed with the Canadian securities regulatory authorities. The risk factors outlined in the previouslymentioned documents are specifically incorporated herein by reference. The Company’s business,financial condition, or operating results could be materially adversely affected if any of these risksand uncertainties were to materialize. Given these risks and uncertainties, investors should notplace undue reliance on forward-looking statements as a prediction of actual results.

Note: All figures are in US dollars.

3

As a result of impairment losses, restructuring and other costs, remeasurementof forward purchase agreement liabilities and loss on early extinguishment oflong-term debt incurred in both 2017 and 2016, the Company is including in thisinvestor presentation the following non-GAAP financial measures: “adjusted costof sales”, “adjusted gross profit”, “adjusted operating profit”, “adjusted financeexpenses”, “adjusted income before income taxes”, “adjusted income taxesexpense”, “adjusted tax rate”, “adjusted net income”, “adjusted earnings perbasic and diluted share” and “adjusted diluted weighted average number ofshares outstanding”. The Company believes that this results in a more meaningfulcomparison of its core business performance between the periods presented.These non-GAAP financial measures do not have a standardized meaningprescribed by GAAP and therefore are unlikely to be comparable to similarmeasures presented by other issuers. Reconciliations of these non-GAAPfinancial measures to the most directly comparable financial measures calculatedin accordance with GAAP are included in the MD&A for the second quarter andsix months ended June 30, 2017.

4

• 3 business segments

• Dorel Home (2016 revenue - $735 million)

• Dorel Juvenile (2016 revenue - $929 million)

• Dorel Sports (2016 revenue - $939 million)

• $2.6 billion in sales annually

• Approximately 10,000 employees

• Sales to 100+ countries

• Facilities in over 25 countries

TSX: DII.B DII.A

5

6

(in thousands, other than EPS) 2017 2016

Total revenue $ 611,270 $ 637,296

Adjusted net income $ 12,444 $ 10,193

Adjusted EPS (diluted) $ 0.38 $ 0.31

7

(in thousands)2017 2016

Restated*

Total revenue $ 184,157 $ 171,871

Gross profit $ 32,872 $ 29,075

Operating profit $ 16,715 $ 14,762

Second Quarters ended June 30

* During the fourth quarter of 2016, the Company changed its internal organization and the composition of itsreportable segments. The design, sourcing, manufacturing, distribution and retail of the children’s furniture wastransferred from Dorel Juvenile to Dorel Home. Accordingly, the Company has restated the segmented information forthe second quarter ended June 30, 2016.

8

Second quarter revenue included the highest percentage of on-line

sales (52%) in Dorel Home’s history and exceeded reductions in

sales to brick and mortar stores.

Growth was driven by increased sales in all divisions to on-line

retailers.

Improved margins from increased on-line sales were partly offset

by slightly higher input and warehousing costs.

Higher second quarter operating profit was driven by increased

sales volumes, slightly offset by increased selling and general and

administrative expenses.

9

10

Seconds Quarters ended June 30

(in thousands)2017 2016

Restated*

Total revenue $ 218,060 $ 228,911

Adjusted gross profit $ 65,207 $ 72,646

Adjusted operating profit $ 8,086 $ 8,797

* During the fourth quarter of 2016, the Company changed its internal organization and the composition of its reportablesegments. The design, sourcing, manufacturing, distribution and retail of the children’s furniture was transferred fromDorel Juvenile to Dorel Home. Accordingly, the Company has restated the segmented information for the second quarterended June 30, 2016.

11

Over-riding strategy: Diverse, known brands; exciting, quality

products; Company-owned distribution.

Dorel Juvenile re-aligning operations to be more agile and drive

profitable sales growth with a more market-focused approach to

better react to juvenile industry trends.

With a view to allocating greatest returns, product development

projects which do not meet new growth criteria are being

cancelled, overheads are being reduced and savings re-purposed

to enhance brand support and digital capabilities.

Objective: speeding meaningful products to market.

12

Second quarter revenue decreased primarily in the U.S. and European markets.

U.S. POS at its largest customer increased versus prior year, but the customer

limited orders to reduce their own in-stock inventory levels. Sales to several other

brick and mortar customers were also lower, a reflection of challenges in this

channel overall. E-commerce sales are increasing which partially offset these

declines.

In Europe, late product launches and manufacturing challenges in China delayed

new product launches, negatively impacting sales.

Revenues and earnings in Juvenile’s other markets were up overall, led by strong

growth in Brazil and Australia.

Prior year operating profit included costs of $7.0 million associated with U.S.

product liability and the year-over-year reduction in these costs was $5.8 million in

the quarter.

Several new products are being launched across all Dorel Juvenile’s geographic

markets.

13

Production levels at the China-based facilities increased by approximately

20% from the first quarter following the development and implementation

of an intensive 60 day plan which resulted in higher costs in the short-term.

The grand opening of the new Zhongshan, China campus and best-in-class

test lab was held in May, which has allowed for the successful exit and sale

of the old campus.

The new project for China ERP/MRP system implementation launched in Q2

to establish robust operation processes for the factory. The new system will

ensure on time delivery, as well as help the factory develop from a supplier

role to a reliable integrated Dorel Juvenile manufacturing site. Go-live is

planned for mid-2018.

Various strategic initiatives were launched to grow market share. In May,

Dorel Juvenile China signed a joint business plan for a strategic partnership

with Alibaba, one of the world’s most powerful companies.

14

15

• Safety 1st brings together the latest pediatric knowledge and advanced engineering to create the new onBoard 35 LT infant car seat.

• Superior fit, as advised by pediatricians, helps create a safer ride for children from 4 to 35lbs.

• Advanced engineering also helps control the weight of the seat, making it one of the lightest infant carriers in the world.

Superior Fit

for Superior

Safety

16

Q U I N N Y Z A P P XO N E S T R O L L E R , E N D L E S S P O S S I B I L I T I E S

M E E T T H E A L L N E W Z A P P X

• Completely modular, compact and comfortable.

• Perfect from birth with Lux carrycot, Maxi-Cosi car seat or from-birth cocoon.

• Fully customisable to create your own one-of-a-kind Zapp X.

• Premium design inspired by athleisure trend.

Z A P P F L E X P L U S Z A P P F L E X Z A P P X P R E S S

17

• Infanti’s textile and shoe line is a product of our promise to have a completeand cross category brand, which allows parents to find all their infants’needs in one place.

• We present a whole range of very colourful, trendy and high quality optionsto dress the little ones. Starting from birth - Peruvian organic cottonessentials to hip 4 year old’s sneaker wear.

18

Second Quarters ended June 30

(in thousands) 2017 2016

Total revenue $ 209,053 $ 236,514

Adjusted gross profit $ 48,119 $ 48,841

Adjusted operating profit $ 5,661 $ 5,236

19

Organic revenue declined 13.4% when removing foreign exchange

fluctuations and the change in Cycling Sports Group (CSG) International’s

business model.

Part of the revenue shortfall resulted from weakness in consumer demand in

the mass bike channel due to the prolonged unfavourable North American

weather.

CSG revenue declined due to lower discounted sales. CSG’s closeout sales in

the quarter represented 7% of sales volume in 2017 compared to 21% the

prior year. Excluding these closeout sales, revenues were flat and gross

margins were improved.

In Brazil, Caloi’s top line was affected by weak consumer demand, amid

ongoing political and economic turmoil, as well as increased competitive

pressure as other key brands in the market began to reduce retail price

points.

The improvement in adjusted operating profit was due to improved margins

and a reduction in operating expenses.

20

Synapse

SuperX SE

21

Moterra

SuperX

22

23

1) Cycling Sports Group (CSG)

• IBD Division

• Premium Brands

• Innovation – continuing focus

• SUGOI – world class cycling, run and triathlon apparel and outdoor gear. Incorporates Cannondale apparel.

24

2) Pacific Cycle

• Mass merchants/sporting goods channel

• Full service provider – bikes, parts & accessories,branded apparel

• Brand building has enhanced Schwinn/Mongooseawareness

• Electric ride-on toys.

25

3) Caloi

• 100% interest (effective March 2017)

• Largest bicycle brand in LATAM and leader in Brazilian market

• Portfolio includes full range of bicycles, from high-performance to children’s mountain bikes, urban, recreational and road bikes

• Caloi’s factory in Manaus is largest bicycle manufacturing plant outside Southeast Asia

• Brazil is a Dorel production hub, assembling Caloi, Cannondale, Schwinn, Mongoose & GT brand bicycles for local and export markets.

26

Credit AgreementEffective March 24, 2017, the Company amended its Credit Agreement

with respect to its revolving bank loans and secured a term loan of

$200.0 million with the same maturity date as its revolving bank loans.

Net proceeds from the term loan were used to prepay its Series “B”

and “C” Senior Guaranteed Notes, its Brazilian non-convertible

debentures and to reduce bank indebtedness. Included in Q1 2017

finance expenses is a cost of $10.2 million or $0.30 per diluted share

for early extinguishment of long-term debt. With the lower average

interest rates of the term loan facilities going forward, the Company

expects to reduce its interest costs by approximately $4.0 million in

the balance of 2017.

27

TaxesDuring the second quarter and six months ended June 30, 2017, the

Company’s effective tax rates were 27.2% and 31.2% respectively versus

12.5% and 8.6% for the same periods in the prior year. Excluding income

taxes on impairment losses, on restructuring and other costs, on

remeasurement of forward purchase agreement liabilities and on loss on

early extinguishment of long-term debt, the Company’s second quarter

adjusted tax rate was 28.4% in 2017 and 15.4% in 2016. The adjusted tax rate

for the first six months was 24.7% in 2017 versus 16.5% in 2016. The main

cause of the variation year-over-year of the adjusted tax rate is due to

changes in the jurisdictions in which the Company generated its income. The

Company is stating that for the full year it expects its annual adjusted tax

rate to be between 20% and 25%. However, variations in earnings across

quarters mean that this rate may vary significantly between quarters.

28

The strength and flexibility of Dorel Home’s e-commerce platform has allowed for an expansion of its

on-line offerings with excellent value products at higher price points. E-commerce sales are expected

to continue to drive the segment’s overall growth and profits, both above plan and prior year levels

for the balance of the year.

At Dorel Juvenile, several factors support our confidence of a strong second half rebound. Many new

products are currently entering the market, particularly in Europe and these launches will continue

into 2018. In the U.S., there are several new placements at major retailers, and at Dorel’s largest

customer, orders are in line with point-of-sale levels, which are up over last year. This was not the

case in the second quarter as that customer reduced its in-stock levels. Further, Dorel Juvenile’s

growth with e-commerce retailers is at a greater pace than budgeted. We also expect our smaller

markets to continue their overall excellent performance. The China factory has successfully caught up

on its order back-log and sales should be strong going forward. The focus in China will now turn to

additional cost saving opportunities. Finally, the majority of our major currencies are trending

favourably which will further help our various markets around the world.

We anticipate that Dorel Sports overall will have a better second half than last year with an increased

adjusted operating profit. We are currently seeing some weakness in the mass channel which means

third quarter results are likely to be lower than last year, but expect that a solid fourth quarter

performance should more than compensate for this,” concluded Mr. Schwartz.

29

• Sustained growth in Dorel Home with a proven e-commerce growth model.

• Strategically growing Dorel Juvenile and Dorel Sports in global markets.

• A diverse portfolio of known, premium brands.

• Product development that drives growth.

• Established customer relationships.

• Annual dividend of $1.20 per share.

• Consistent generator of cash flow to support acquisitions.

• Consolidation of Chinese manufacturing facilities to reinforce supply chain and increase competitiveness.

30

APPENDIX

31

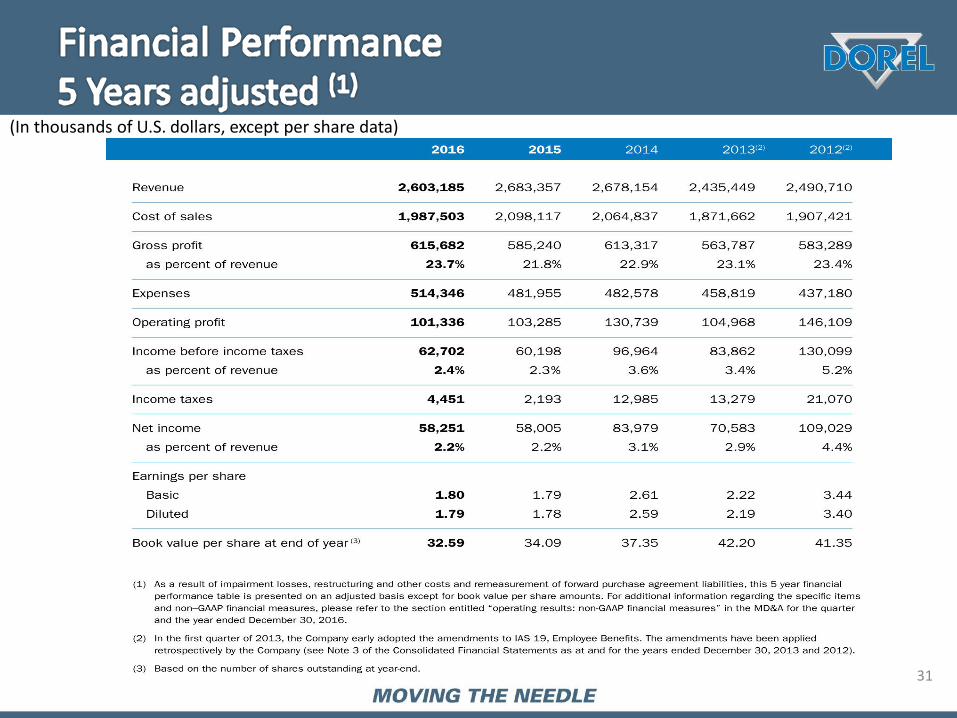

(In thousands of U.S. dollars, except per share data)

32

• 1988 Cosco Inc (DJG)

• 1990 Charleswood Corporation

• 1994 Maxi-Miliaan B.V. (Maxi-Cosi)

• 1998 Ameriwood Industries

• 2000 Safety 1st Inc.

• 2001 Quint B.V. (Quinny)

• 2003 Ampa France (Dorel Europe)

• 2004 Pacific Cycle

• 2007 IGC Australia

• 2008 Cannondale/SUGOI

• 2008 PTI Sports

• 2009 Baby Art

33

• 2009 Dorel Brazil

• 2009 Iron Horse Bicycles

• 2009 Gemini Bicycles (Australia)

• 2009 Hot Wheels, Circle Bikes (UK)

• 2011 Silfa Group (Chile, Peru, Bolivia, Argentina) - 70% interest

• 2012 Poltrade (Poland)

• 2012 Best Brands Group SA (Panama) and Baby Universe SAS(Colombia) – 70% interest

• 2013 Caloi (Brazil) – 70% interest (now a 100% interest)

• 2014 Tiny Love Ltd. (Israel)

• 2014 Right to sell Infanti brand in Brazilian market

• 2014 Juvenile business of Lerado Group (Hong Kong)

• 2014 Intercycles (Chile)

34

36%

36%

28%

DOREL JUVENILE DOREL SPORTS DOREL HOME FURNISHINGS

39%

37%

24%

2016 2015

35

2016 2015

62%

3%

21%

3%9%

2%

US Canada Europe Other Latin America Asia

60%

4%

21%

3%9%

3%

36

• Active in sustainability on several fronts throughout all three segments.

• Dorel Home Products facility is FSC certified.

• Cornwall RTA plant recycling for 10 years.

• 98% of materials are recycled or sold.

• DJG’s sustainability initiatives include zero landfill, water usage reduced by 98%; high-efficiency lighting systems.

• Strict policy in place to ensure sustainable business practices of suppliers.