Second Edition - acc.com

152

Renewable Energy 2022 Practical cross-border insights into renewable energy law Second Edition Contributing Editor: Mhairi Main Garcia Dentons & Co.

Transcript of Second Edition - acc.com

Renewable Energy 2022

Practical cross-border insights into renewable energy law

Second Edition

Contributing Editor:

Mhairi Main GarciaDentons & Co.

DisclaimerThis publication is for general information purposes only. It does not purport to provide comprehen-sive full legal or other advice. Global Legal Group Ltd. and the contributors accept no responsibility for losses that may arise from reliance upon information contained in this publication. This publication is intended to give an indication of legal issues upon which you may need advice. Full legal advice should be taken from a qualified professional when dealing with specific situations.

ISBN 978-1-83918-142-9ISSN 2634-4300

Published by

59 Tanner StreetLondon SE1 3PLUnited Kingdom+44 207 367 0720 [email protected] www.iclg.com

Strategic Partners

©2021 Global Legal Group Limited. All rights reserved. Unauthorised reproduction by any means, digital or analogue, in whole or in part, is strictly forbidden.

Printed by Ashford Colour Press Ltd.

Cover image www.istockphoto.com

Publisher James Strode

Production Editorial Assistant Charlotte Garcia

Senior Editor Sam Friend

Head of Production Suzie Levy

Chief Media Officer Fraser Allan

CEO Jason Byles

Second Edition

Contributing Editor:

Mhairi Main GarciaDentons & Co.

Renewable Energy 2022

Table of Contents

Q&A Chapters

Expert Analysis Chapter

1 The Potential for Low Carbon HydrogenMhairi Main Garcia, Dentons & Co.

6 AustraliaMinterEllison: Joel Reid, Kathryn Finlayson, Joshua Dellios & David Moore

16 EgyptMazghouny & Co: Donia El-Mazghouny

23 FranceDS Avocats: Véronique Fröding & Stéphane Gasne

31 GermanyPOSSER SPIETH WOLFERS & PARTNERS: Dr. Wolf Friedrich Spieth, Niclas Hellermann, Sebastian Lutz-Bachmann & Dr. Jakob von Nordheim

39 GreeceSardelas Petsa Law Firm: Panagiotis G. Sardelas & Konstantina (Nantia) Kalogiannidi

47 IndonesiaOentoeng Suria & Partners in association with Ashurst: Frédéric Draps, Elizabeth Sidabutar & Khairunissa (Nissa) Yuliandhini

55 JapanNishimura & Asahi: Sadayuki Matsudaira

61 MaltaGVZH Advocates: Gayle Kimberley, Nicole Sciberras Debono & Nina Fauser

70 MexicoGalicia Abogados, S.C.: Carlos de Maria y Campos, Francisco Fernandez Cueto, Mariana Herrero & Cecilia Azar

77 OmanDentons & Co.: Mhairi Main Garcia & Yasser Taqi

84 Portugal Uría Menéndez – Proença de Carvalho: João Louro e Costa & Francisco Fráguas Mateus

92 Saudi ArabiaThe Law Firm of Wael A. Alissa in association with Dentons & Co.: Mahmoud Abdel-Baky & Mhairi Main Garcia

99 South AfricaCliffe Dekker Hofmeyr Inc: Tessa Brewis, Alecia Pienaar, Margo-Ann Werner & Jerome Brink

107 Sweden Wistrand Law Firm: Rudolf Laurin & Aaron Coster

115 United Arab EmiratesDentons & Co.: Mhairi Main Garcia

125 United KingdomBracewell (UK) LLP: Oliver Irwin, Nicholas Neuberger, Adam Quigley & Robert Meade

133 USA Pillsbury Winthrop Shaw Pittman LLP: Mona E. Dajani

138 ZimbabweWintertons: Nikita Madya

Welcome

From the Publisher

James StrodePublisherGlobal Legal Group

Dear Reader,

Welcome to the second edition of ICLG – Renewable Energ y, published by Global Legal Group.

This publication provides corporate counsel and international practitioners with comprehensive jurisdiction-by-jurisdiction guidance to renewable energy laws and regulations around the world, and is also available at www.iclg.com.

This year, an expert analysis chapter covers the potential for low carbon hydrogen.

The question and answer chapters, which in this edition cover 18 jurisdictions, provide detailed answers to common questions raised by professionals dealing with renewable energy laws and regulations.

As always, this publication has been written by leading renewable energy lawyers and industry specialists, for whose invaluable contributions the editors and publishers are extremely grateful.

Global Legal Group would also like to extend special thanks to contributing editor Mhairi Main Garcia of Dentons & Co. for her leadership, support and expertise in bringing this project to fruition.

Welcome

Renewable Energy 2022

Chapter 1 1

The Potential for Low Carbon Hydrogen

Dentons & Co. Mhairi Main Garcia

© Published and reproduced with kind permission by Global Legal Group Ltd, London

■ greyhydrogenderives from methane (natural gas or other fossil fuel feedstock) with catalysts used to break hydro-carbon bonds, releasing excess carbon, resulting in carbon dioxide emissions;

■ browncarbonderivesfromcoalgasification,againreleasingexcess carbon resulting in carbon dioxide emissions;

■ bluehydrogenisacleanerversionofgreyhydrogenusingcarbon capture, utilisation and storage (CCUS), reducing emissions; and

■ green hydrogen derives fromwater, using electrolysis toseparate water into its component elements of hydrogen and oxygen and, when using electricity generated from renewable sources, may result in zero carbon hydrogen.

Currently, almost all hydrogen production is grey or brown hydrogen (99.6%) (Why green hydrogen is reaching a tipping point, Wood Mackenzie, 9 June 2021). In spite of this, the pipe-linelooksverydifferent.Withtheincreasedcommitmentsbystates around the world towards net zero, electrolysis-based low carbonproductionnowmakesup67%oftheoverallpipelineforhydrogen (Wood Mackenzie, ibid.).

Uses and Relevance to DecarbonisationLowcarbonhydrogenisversatileandhasanumberofpossibleuses,generallydiversifyingenergysupplyandreducingrelianceon fossil fuels. It can, among other things, be used to decar-bonise “hard to decarbonise” industrial processes, including the chemical, refining, cement, iron and steel industries, reducing the emissions these sectors generate.

Once produced, low carbon hydrogen can be used for a variety of industrial, agricultural and transportation appli-cations. It can be used as a fuel, either in liquid form or by converting the hydrogen into ammonia, which can then betransported and exported. It can also provide green fuel forthe transportation sectors. Hydrogen transport technologies offer short refuelling times and lighter weight (when compared tobattery-poweredelectricvehicles),leadingtolong-rangesolu-tions.Whilecarsandsmallcommercialvehiclesarelesslikelyto switch tohydrogengiven thedevelopmentofbattery tech-nology, hydrogen (or synthetic low carbon fuels made from hydrogen), has the ability to fuel long-distance haulier fleets and themaritimeandaviationsectors.

Low carbon hydrogen can generate power and heat in a fuel cell, and can be used in district heating and cooling. Its poten-tialisparticularlyimportantgiventhesustainedandincreasingdominance of intermittent, renewable energy generation across the globe. Low carbon hydrogen can offer the renewable energy sector clean solutions for:■ long-term and large-scale storage of renewable energy

which cannotbeserviced by current battery technology;

IntroductionThere is an increasing recognition of the role which low carbon hydrogen can play as part of states’ net zero commitments. The exponential growth in renewables has been supported by ambi-tiousrenewableenergytargetswhichhavebeensetbycountriesacrosstheglobe.However,ifthegoalofnetzeroistobereal-ised, the focus needs to shift beyond the power sector and states need to consider how to decarbonise economies, in particular the industrial, heating and transportation sectors. Coupled with renewable power and other decarbonisation technologies, low carbonhydrogenhastheabilitytoplayakeyroleinachievingnet zero commitments and bridging the decarbonisation gap for “hard to decarbonise” industries.

But, it is not a panacea; there are a number of challenges around realising the full potential of low carbon hydrogen, including:■ low carbon hydrogen is not currently cost-competitive

when compared with other energy sources; ■ the technology is still at relatively nascent stages of

development;■ thereisalackofdedicatedinfrastructure,withtransporta-

tionandstorageinfrastructuregenerallyunderdeveloped;■ thereisalackofaglobalsupplychain,withunpredictable

demandanduncertainrevenue;and■ notwithstanding increasingcommitmentsbystatesaround

theworldtodeveloplowcarbonhydrogenandaccelerateitsproduction and/or its use, many countries lack comprehen-sivepoliciesandtailoredregulations.

This chapter will consider some of these challenges further below, as well as their interplay with the renewable energy sector. This chapter focuses on general principles and does not attempt to examine the technical processes or technical chal-lenges; these are complex in nature and there are a number of detailed studies by technical authoritieswhich provide expertanalysis on these matters, including studies by the International Renewable Energy Agency (IRENA), the International Energy AgencyandtheHydrogenCouncil,whichreaderscanreviewtounderstand more about the technical aspects.

What is Low Carbon Hydrogen?Hydrogen is the most abundant chemical element on Earth. However,hydrogencurrentlysuppliesonlyanegligibleamountof the world’s energy, and most of that supply does not come from low carbon hydrogen, but rather from grey hydrogen.

This chapter focuses on low carbon hydrogen. There are a number of different colours used when considering hydrogen, includinggrey,brown,blue andgreen. However, the coloursused to describe hydrogen are not universally agreed. Forpurposes of this chapter:

2 The Potential for Low Carbon Hydrogen

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

TechnologyLow carbon hydrogen technology is still at relatively nascentstagesofdevelopmentandlackseconomiesofscale.Linkedtotherelativelyhighcosts,itrequireslargeamountsofenergytoproduce, compress, store and transport low carbon hydrogen to end users.

Green hydrogen production requires a steady supply of water as a feedstock and renewable energy as a power source to split the hydrogen and oxygen from water in an electrolyser. There are currently different types of electrolyser designs, each presenting challenges, with varying capital costs and varyingefficiencies. Green hydrogen suffers measurable energy losses at eachstageofthevaluechain;around30–35%oftheenergyusedto produce hydrogen through electrolysis is lost (Green Hydrogen, A Guide to Policy Making, IRENA, 2020). There are also consid-erableenergylossesinconvertinghydrogenfortransportation,transporting the hydrogen and using it in fuel cells. The greater the energy loss, the larger amount of renewable electricity needed to produce green hydrogen.Thereisthusaclearpotentialfortechnologicaladvancesto

enable both the costs to come down and efficiencies to increase, and this, coupled with the continued reduction in the cost of renewable energy, may accelerate the speed and scale of deploy-ment of green hydrogen.As mentioned above, scaling-up is essential; economies of

scale should, in time, enable electrolyser costs to drop more and lead to reductions in the overall costs of the productionanddeliveryof greenhydrogen,with the costof electrolysersbecomingincreasinglycompetitiveasthesupplychaindevelops.This scaling-up has already begun, with electrolyser manufac-turing capacity increasing exponentially during the last two to three years. This growth is expected to continue.

Blue hydrogen faces technical challenges as well. Countries whichhavehydrocarbonresourcescanproducebluehydrogento reduce their carbon footprint. Nevertheless, while CCUStechnology is not new, it has not been widely deployed, largely duetoprohibitivecosts.Thedrivetowardsnetzeroischangingpriorities, nonetheless; many of the major oil and gas compa-nies arenowcommitted todevelopingCCUS technology andproducing blue hydrogen, and a number are even looking atgreen hydrogen projects. The challenge for the blue hydrogen projects is to reduce production costs in a project where a unit of hydrogen yields less energy than a unit of natural gas, so more gas isneededtosupplyanequivalentamountofcleanenergy.As with the scaling-up of electrolyser use, the scaling-up of CCUS technology is expected to increase efficiencieswhile atthe same time reduce costs.CCUS is not limited to oil and gas projects; it is already

successfullyusedandcanbedevelopedandscaled-upinminingand cement sectors. It can likewise be used in other industrial sectors,suchasfertilisers,steelandiron,withrelativelymodestcapitalinvestments.

Infrastructure, Storage and TransportationFor renewable energy generators, where there is a developedelectricity network, transporting the electricity to end users is not normally problematic. The position of low carbon hydrogen producers is different. Hydrogen transportation infrastructure remainsunderdevelopedinmostareas.Asalow-densityfuel,hydrogeniscomplextotransport.For

hydrogen to be transported, it must be compressed or liquefied (using electricity), making storage and transportation complex and costly. There are three primary forms in which to transport hydrogen: compressed hydrogen; liquefied hydrogen; or bound

■ gridbalancingand the capacity to address seasonal imbal-ances between electricity generation and consumption;

■ energysystemflexibility,withtheabilitytoabsorbexcessrenewable electricity production at times when demand is lowandwholesaleprices arenegativeor generation isotherwise curtailed;

■ exporting excesspowerbypipelineor shipwhere coun-tries generate excess renewable electricity and produce excess low carbon hydrogen, avoiding interconnectionrisks; and

■ providing long-term offtakers, on a corporate powerpurchase agreement (PPA) basis.

In addition, low carbon hydrogen can be used as an energy source by injecting it into natural gas networks, making the gas cleaner.However,this“blending”hasitslimitations(seebelowin relation to the challenges related to transportation).

As a fuel, hydrogen is a clean power source, with zero carbon emissions at use. It is also considered a facilitator in job creation and job repurposing in a post-COVID-19 world.

CostLow carbon hydrogen is not currently cost-competitivewhencompared with other energy sources. The cost of hydrogen varies significantly across regions; estimates vary, with greenhydrogen costs reported to cost anything from two to seventimes more to produce than grey hydrogen (the costs varypredominantlydependingontheavailabilityandcostofrenew-able energy). In addition to production costs, hydrogen storage and transportation are high and energy intensive, particularlyas a result of its low density. The gap between the costs of raw materials, electrolysers, production, transportation, storage and use of low carbon hydrogen and the costs of producing and using grey hydrogen, brown hydrogen, natural gas and the other fossil fuels that it seeks to displace needs to be narrowed if the low carbon hydrogen industry is to flourish.Positively, Wood Mackenzie (ibid.) estimates that green

hydrogen will be competitive with fossil fuels by 2028 to2033,assumingaUS$30/MWhpowerpricein2030,whiletheHydrogen Council predicts that the cost of producing “clean hydrogen” should decline by up to 60% by 2030, with theoptimal production option highly dependent on the region, and hydrogendeliverycostsreducingbyupto70%over thesameperiod (Path to hydrogen competitiveness, A cost perspective, Hydrogen Council, 20 January 2020).

Hydrogen production costs are expected to fall as a result of declining costs of renewables (the cost of solar and wind power is thelargestdriverofgreenhydrogenproductioncosts),scaling-upand standardisation of electrolyser designs, the scaling-up of hydrogenproductionandthedevelopmentoflower-costCCUSfacilities. At the same time, carbon prices may rise, although it is unlikelytheywillrisetoalevelrepresentingthefullsocio-eco-nomicandenvironmentalcostsofgreenhousegasemissions.In addition to the cost of renewables, the availability of

renewable electricity for green hydrogen must be considered if thehydrogenistobeconsidered“green”inanygivenmoment.Where a project is connected to the grid, this may include elec-tricity produced from conventional electricity producers and,therefore,mayhaveanegativeimpactonthelowcarbonnatureof the hydrogen being produced. Green hydrogen producers will need to balance the cost of being connected to the grid (and thecostimplicationsofrelativecarbonemissions)versus the risks andcostsofarenewablescaptive(includingtheriskofoutages).

In addition to production costs, producers and end users may face substantial, one-off capital coststofundthedevelopmentofnewfacilitiesand/ortheconversion of existing facilities.

3Dentons & Co.

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

Commission’s 2020 strategy, A hydrogen strateg y for a climate-neutral Europe(COM(2020)301final,8July2020),setsoutamongotherthings the strategy for boosting demand in end use sectors, with industrialapplicationsandmobilitytobedevelopedgraduallytoefficiently use hydrogen. The industrial sector strategy follows a two stage approach: firstly, an immediate application to reduce andreplacetheuseofcarbon-intensivehydrogeninrefineries,ammonia production, new forms of methanol production and partial replacement of fossil fuels in steel making; and secondly, hydrogencanformthebasisforinvestingin,andconstructing,zero carbon steel-making processes.

Legal and Regulatory ConsiderationsThereisalackofspecificlegislationgoverningtheproductionof low carbon hydrogen; indeed in a number of jurisdictions, there is a rish that the regulatory regime operates as a barrier to investingin,anddeveloping,lowcarbonhydrogenprojects.Inmostjurisdictions,hydrogenproductionwillbegovernedbyamyriadofexistinggas,energy,water,health,safetyandenviron-mental regulations. Most jurisdictionswill alreadyhave inplacegeneral regula-

tions around the use of hydrogen. As a highly flammable gas, the production, storage and transportation of hydrogen will usually be subject to detailed safeguards, use of specialised equipment, and recording and reporting requirements. Hydrogen produc-tionwillbesubjecttolocalenvironmentallawsandregulations,andwilltypicallybesubjecttodetailedapprovalsandconsents,including environmental impact assessments and reportingrequirements. Moreover, a number of chemicals other thanhydrogen may be present during the production process, which may similarly be subject to detailed health, safety and reporting requirements. However, most regulatory frameworks do notcontemplate the large-scale production of low carbon hydrogen.

If a project includes supply of low carbon hydrogen into the existing natural gas network, the rules around third party access (TPA) to the domestic gas market will need to be considered. Whileregulationsaroundthegasnetworksarelikelytobeverydetailed, including in relation to the TPA regime, and while somejurisdictionsalreadyhaveinplacelimitsaroundblendingand requirements in relation to materials and retrofitting, many donothaveregulationsspecifictohydrogen.Adaptingregula-tionswhich facilitateaccessandblendingwillprovide regula-tors with another opportunity to support the low carbon sector.Furthermore,forgreenhydrogen,sourcingofwateriscrucial

and, again, many regulatory frameworks will simply not contem-plate the large-scale use of electrolysers in green hydrogen production. For a green hydrogen project to be sustain-able, developers will need to source a sufficient and sustain-ablevolumeofsuitablequalitywaterforuseintheelectrolysisprocess. The requirements around using such water will need to be fully understood, including permits for connecting to the localwaternetwork,permitsforusingriverwater,or,ifseawaterwillbethesource,therelevantapprovalsandconsentsrequiredto construct and operate a desalination facility (including issues such as water temperature management and disposal of brine). Not all jurisdictionswill have inplace the regulations, or theregulations may not be tailored to green hydrogen production. Anassessmentoftheenvironmental impactofanysuchwaterusage will also be essential, particularly in areas where there is water scarcity or there could be an impact on other sectors, such as agriculture and fisheries.

Another consideration is the need for regulators in different jurisdictionstoco-operate:ifregulationsandstandardsaredevel-oped in isolation, this could impede the growth of the low carbon hydrogen sector. Notwithstanding increasing commitments by

into molecules which are easier to transport, such as ammonia and liquid organic hydrogen carriers. Depending on the form, it can be transported by gas pipeline or tanker (ship, lorry or train). The relative costs of pipeline and tanker vary with both thedistancetravelledandthevolumeofhydrogentransported.Itislikelythatnewpipelinesmayhavetobedevelopedorexistinginfrastructure retrofitted in order to transport hydrogen.

The process in which hydrogen is compressed and liquefied usesalotofenergy;ifthereisnorenewableenergyavailableforthisprocess,thiswillhaveanegativeimpactonthelowcarbonnatureofthehydrogenthathasbeenproduced.Availabilityofrenewable energy sources for compression and liquefaction will therefore be a concern.

Hydrogen may be blended with natural gas and transported in existing natural gas pipelines. This has its own challenges; depending on the regulations, hydrogen may make up only around10–20%oftheblendandtherearetechnicalchallengesincluding possible requirements to reinforce and retrofit pipes. The blending limit will reduce the impact of the decarbonisa-tion benefits and, for some end users, such a blend may not be suitable if they require either pure hydrogen or gas with a higher content of hydrogen. Technical studies will likewise be required to assess the suitability of existing gas pipeline infrastructure for handling hydrogen.Where low carbon hydrogen is converted into and from

ammonia or a liquid organic hydrogen carrier for shipping, this facilitates long-distance low carbon hydrogen supply. Usingammonia as the hydrogen carrier has the benefit of being estab-lished technology and can benefit from using existing infra-structure for shipping. However, where end users requirepure hydrogen, the technology to convert ammonia back intohydrogenisrelativelyunderdeveloped.Additionally,theconver-sion into and from ammonia (or a liquid organic hydrogen carrier) andshippingcomesatacostandsizeableenergyloss(13–25%;IRENA, ibid.). It is likely that, for any such shipping to be sustain-able, itwillneedtodevelopinmuchthesamewasastheLNGmarkethasdeveloped;producerswillneedtodemonstratestrongdemand backed by long-term sale and purchase agreements to fundtheinitialrequiredinfrastructure,withaspotmarketeven-tuallydevelopinginthemediumtolongerterm.

Lastly, in relation to storage, large-scale storage is likely to be a strategic part of the low carbon hydrogen supply chain (in particular with regard to the role that hydrogen can play in balancing energy supply). The types of storage and capacity will vary depending on availability of existing facilities and localgeology. Geographies with natural underground storage or salt cavernsmaybewellsuitedtodevelopingstoragefacilities.

Supply and DemandExceptinperiodsofoveralllowsystemdemandwhenwholesalepricesmayturnnegative,renewableenergygeneratorsfacelittledemand risk. The position of low carbon hydrogen producers is different. There is a lack of a global hydrogen supply chain; there are high capital costs and unpredictable demand and revenuestreams.Thereisalackofaliquidwholesalemarketforhydrogenproducerstosellintoandthereisalackofadevelopedpublic transportation infrastructure for hydrogen.

There is no ready-made list of end users already using hydrogen; many will be new customers and encounter costs as a resultofchangingorconvertingtechnologies.Whileendusersalready using hydrogen as a feedstock (for example, refineries and ammonia producers) would not need to incur any capital costs in switching from grey or brown hydrogen to low carbon hydrogen, other possible users, such as the steel industry, would incurmaterialcostsinconvertingtheirfacilities.TheEuropean

4 The Potential for Low Carbon Hydrogen

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

should not be considered in isolation and will need to take into account applicable state aid rules and restrictions; the importance of tailored regulatory regimes will be essential and will be signifi-cant in attracting commercial financing for projects.

ConclusionsLowcarbonhydrogenhastheabilitytomakeapositivecontri-butiontowardsstatesachievingtheirnetzeroobjectives. Forthis to be realised, there are multiple and interlinked factors which will need to be considered. The scaling-up of technology will be fundamental to increasing efficiencies and reducing costs, in addition to encouraging developers and funders toinvestinprojectsandpersuadingenduserstoswitchtechnolo-gies, with the ultimate goal of creating predictable demand and supplyandanestablishedhydrogenmarket.Significantinvest-ment in either developing new infrastructure or retrofittingexisting infrastructure will be needed.

Low carbon hydrogen producers will need to mitigate the risksbytakingvariousmeasures,including:■ considerationsaroundsecurityofrenewableenergysupply

and long-term PPAs;■ understandingrisksaroundproximityofpowersupplyand

end users, to mitigate transportation and storage risks and costs;

■ using, where possible, existing natural gas pipelinenetworks but also understanding the TPA restrictions, limits in relation to blending and any requirements that maygiverisetoretrofittingobligations;

■ contractual protection where counterparties sufferprolonged outages or elect to change technology;

■ counterparty due diligence in terms of creditworthinessand contractual protection in relation to defaults and insol-vency-relatedevents;and

■ long-termfixed-pricesaleandpurchaseagreementstogivepredictability of demand and return, and thereby facilitate financing.

Centraltoallofthiswillbethedevelopmentoftransparentand tailored regulatory regimes to support the low carbon hydrogen sector, coupled (at least initially) with financial and/or taxincentives.Inorderforthelowcarbonhydrogensectortoreach its full potential, regulators will need to make sure existing regulations are adequate and keep up with the scale and pace of technologicaladvances.Tailoredstandardsandregulationsareneededtoattractinvestorsanddevelopersandensurethelong-term success of the sector.

states around the world to develop low carbon hydrogen andincrease its production and/or its use, their policies and regula-tions differ substantially. If the benefits around the export of hydrogen are to be realised, common definitions and methodolo-gies for defining emissions from each unit of hydrogen produced and transported, common standards and international sustaina-bilitycriteriawillneedtobedeveloped.Regulationsaroundtheexport (and import) of hydrogen will need to be considered and, insofar as possible, aligned.

IncentivesIn many countries, financial and/or tax incentives may berequired in the short term to allow the low carbon hydrogen sector to scale-up at the pace required and recognise the role it playsinreducingcarbonemissions.TheEUiscurrentlydrivingforward growth, representing the majority of the low carbon hydrogenpipeline,which isnot surprisinggiven the financialcommitments and electrolyser capacity targets included in the EU’s 2020Green Recovery Package. Outside the EU, otherleading jurisdictions include Australia, Canada, Chile, Japan and SouthKorea.

Globally, the solar and wind electricity generation sectors thrived off the back of government financial and regula-tory incentives,which stimulateddemandand led to the rapidscaling-up of projects, consequential reduced costs and more demand. Although there are differences between renewable electricity generation and low carbon hydrogen, governmentsandregulatorscanusethelessonslearned–bothgoodandbad–indevelopingandadministeringrenewableelectricitygenerationsupport incentives to consider what supportmechanismsmayfacilitate not only the growth of low carbon hydrogen, but also ensuring that such growth can be sustained in the longer term.Asmentionedabove,inmostjurisdictions,regulationswhich

are specific to the production, storage, transportation and use of low carbon hydrogen are generally lacking. Regulatory change willprovideanopportunityforpolicymakersandregulatorstoaddress these issues and to put in place adequate support mecha-nisms, which recognise the low carbon nature of the projects and givetransparenteconomicsupport(whereapplicableequivalenttosimilarprojectsintherelevantjurisdiction);forexample,finan-cial incentives, efficiency incentives, tax credits, offset creditsand/or some form of tradable green certificates. As recognised by the European Commision (ibid.), incentives are likely to berequired for some timegiven theneed to scale-up lowcarbonhydrogenuntilitbecomescost-competitive.Anysuchsupport

5Dentons & Co.

Renewable Energy 2022

Mhairi Main Garcia is a partner and Dentons’ Middle East Regional Head of Energy, Transport and Infrastructure. She is a corporate and commercial lawyer specialising in project development in the energy and infrastructure sectors. Mhairi’s expertise includes advising on utili-ties projects (including solar (CSP and solar PV), wind, hydropower and waste-to-energy projects), many of which are first-of-a-kind projects, as well as advising on distributed energy projects (rooftop and C&I) and the regulation of power and water projects.Mhairi is a member of the Board and Vice-Chair of the Clean Energy Council, a non-profit organisation providing a forum for both private and public sector organisations participating in the clean energy sector across the Middle East and North Africa.

Dentons & Co.Level 18, Boulevard Plaza 2Burj Khalifa District, PO Box 1756DubaiUnited Arab Emirates

Tel: +971 4 402 0859Email: [email protected]: www.dentons.com

Dentons is the world’s largest law firm, delivering quality and value to clients around the globe. Dentons’ polycentric approach and world-class talent challenge the status quo to advance client interests in the communi-ties in which we live and work.Dentons offers vast experience across the world’s energy markets. Dentons’ energy team comprises more than 1,200 lawyers offering tailored advice across the energy spectrum, including in project development, acquisitions and disposals, regulatory, financing, intellectual property and dispute resolution. Dentons is a trusted adviser to developers, contractors, governments and financiers operating in the renewable energy sector. Clients throughout the renewable energy value chain rely on Dentons’ strategic support for legal advice that is commercially astute and delivers innovative solutions.

www.dentons.com

© Published and reproduced with kind permission by Global Legal Group Ltd, London

Renewable Energy 2022

Chapter 26

Australia

MinterEllison

Australia

Joshua Dellios David Moore

Joel ReidKathryn Finlayson

© Published and reproduced with kind permission by Global Legal Group Ltd, London

The large-scale renewable energy target for 2021 and each yearthroughto2030is33,000GWhper annum which, in 2021, equates to approximately 18.54% of electricity consumed onAustralia’s major grids.

There is already more than enough accredited renewable capacity in Australia to meet this target through to expiry of the scheme.However,theschemeisalsobecomingade facto carbon offsetmechanism. This isbecausethevoluntarysurrenderofLGCs by electricity consumers is recognised as an offset to their scope 2 emissions under Australia’s National Greenhouse & EnergyReportingScheme.

1.2 Describe the main participants in the renewable energy sector and the roles which they each perform.

The main participants in the renewable energy sector in Australia are: ■ Utility-scale renewable energy generators which, as

discussedabove,areabletobeaccreditedundertheLRETtoderiverevenuethroughthesaleofLGCs.

■ Small-scale and distributed energy resources (DER) owners/installerswho,asdiscussedabove,areabletobeaccreditedundertheSRETtoderiverevenuethroughthesaleofSTCs.

■ Theeconomicallyregulatedtransmission and distribu-tion networks in each State and Territory of Australia,which deliver power from renewable energy generators(and traditional thermal generators) to end-users.

■ The Australian Energy Market Operator (AEMO) which:■ operates the National Electricity Market (NEM)

and an associated ancillary services market in theAustralian Capital Territory (ACT),NewSouthWales(NSW),Queensland, SouthAustralia,Tasmania andVictoria and also operates and manages the intercon-nected electricity system within those jurisdictions;

■ operates the Wholesale Electricity Market (WEM) acrosstheSouth-WestInterconnectedSystem(SWIS) inSouthern-WesternAustralia;

■ undertakes network planning for, and coordinatesaccess to, the transmission network in Victoria; and

■ has recently been appointed to be the ‘ConsumerTrustee’inNSWto,amongstotherthings,haveover-sightoverthecoordinatedplanningandinvestmentinelectricity generation, storage and transmission in that jurisdiction.

■ Energy retailers who have renewable energy targetsimposed upon them under the LRET and SRET, withpenalties applying if they do not meet those targets. Energy retailers are also increasingly offering products

1 Overview of the Renewable Energy Sector

1.1 What is the basis of renewable energy policy and regulation in your jurisdiction and is there a statutory definition of ‘renewable energy’, ‘clean energy’ or equivalent terminology?

At the federal level in Australia, the Mandatory RenewableEnergy Target incentivises investment in ‘small-scale’ and‘large-scale’renewablefacilities.TheSmall-scaleRenewableEnergyTargetScheme (SRET)

incentivisesenergyconsumerstoinstall:■ solarphotovoltaic(PV) systems with a capacity of no more

than 100kW and a total annual electricity output of less than250MWh;

■ windturbineswithacapacityofnomorethan10kWandatotalannualelectricityoutputoflessthan25MWh;and

■ hydrosystemswithacapacityofnomorethan6.4kWandatotalannualelectricityoutputoflessthan25MWh.

The scheme legislates an annual target requiring a percentage of all power consumed on Australia’s major grids to be met by small-scale renewable facilities. It does so by:■ permittingSmall-scaleTechnologyCertificates(STCs) to

be created from eligible facilities upon installation for their deemedgenerationthroughto2030;and

■ obligingliableentities(e.g.retailers)toacquireandsubse-quentlysurrenderSTCstotheCleanEnergyRegulatorona quarterly basis to progressively meet an annual targeteachyear(throughto2030).

Thesmall-scalerenewableenergytargetfor2021is28.80%,whichequatestoapproximately50,600GWhper annum(i.e.50.6million small-scale technology certificates). Bycontrast,theLarge-scaleRenewableEnergyTargetScheme

(LRET) incentivises investment in ‘large-scale’ renewableenergy generation (including solar PV, wind and hydro facilities with capacities and annual outputs that exceed the kW or MWh ceilingsundertheSRET).ItisenforcedinasimilarwaytotheSRETbyimposingannualstatutorytargetsonmajorwholesalepurchasers of power (e.g. retailers). One Large-scale Generation Certificate (LGC) can be created for each MWh of electricity producedbyaccreditedrenewablefacilities.LiketheSRET,theLRETislegislatedtoremaininplaceuntil2030.

There are 19 eligible categories of renewable energy sources undertheLRET.Theyarehydro,wave,tideandoceanpower,wind, solar, geothermal, hot dry rocks, energy crops, wood waste, agricultural waste, agricultural processing waste, food waste, food processing waste, bagasse (i.e. sugar cane waste), black liquor, municipal solid waste, landfill gas and gas & biomass from sewage.

7MinterEllison

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

In Tasmania, the State Government has passed legislationto enshrine a target of renewable generation equal to 150%of current consumption by 2030, and 200% by 2040. Thegovernment expects to achieve 100% renewable generationfor domestic consumption by 2022; thus, the higher targets are intended to support the installation of new renewable generation for export to the mainland Australian states.OtherAustralianjurisdictionshavealsopreviouslyrunreverse

auctionsorhaveprovidedfundingtotheirgovernment-ownedentitiestodoso.Forexample,Queenslandhascommitted$2billiontofundrenewabledevelopmentsbyitsstate-ownedenti-ties. Other governments (including local governments) havegone out to tender to procure renewable-sourced power for the electricity load of their departments and agencies.Inaddition,NSW,QueenslandandVictoriahavecommitted

funding for, and are consulting on, the development ofRenewable Energy Zones (REZ) for the most prospectiverenewable regions in each of those jurisdictions. At a minimum, these developments involve the commitment of governmentfunding for the extension or upgrade of the transmission network in the identified zones. In some cases, that funding mayberecoveredbyauctioningoffaccessrightstotheneworupgraded sections of the networks. However, the structuresunderwhichthatwilloccurarestillbeingdeveloped(asatthedate of writing).

Lastly, there are battery and rooftop solar grants, loans or rebatesintheACT,Queensland,SouthAustraliaandVictoria.

2 Renewable Energy Market

2.1 Describe the market for renewable energy in your jurisdiction. What are the main types of renewable energy deployed and what are the trends in terms of technology preference and size of facility?

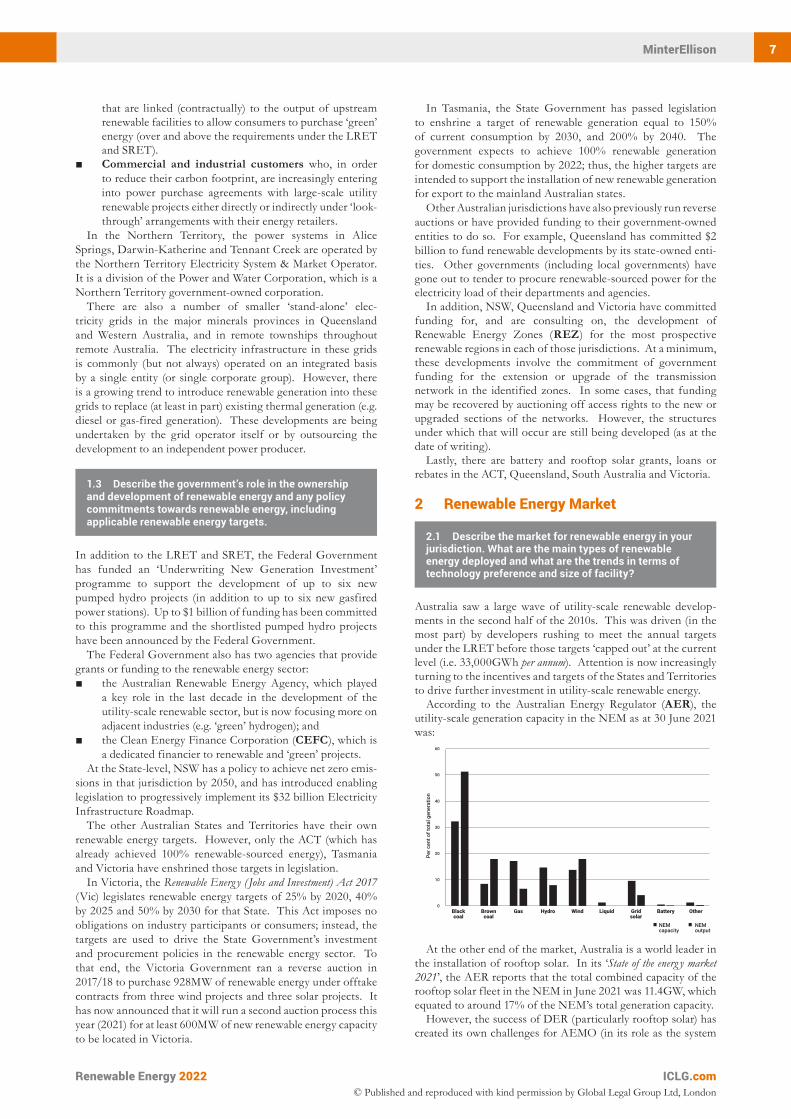

Australia saw a largewave of utility-scale renewable develop-mentsinthesecondhalfofthe2010s.Thiswasdriven(inthemost part) by developers rushing to meet the annual targetsundertheLRETbeforethosetargets‘cappedout’atthecurrentlevel(i.e.33,000GWhper annum). Attention is now increasingly turningtotheincentivesandtargetsoftheStatesandTerritoriestodrivefurtherinvestmentinutility-scalerenewableenergy.

According to the Australian Energy Regulator (AER), the utility-scalegenerationcapacityintheNEMasat30June2021was:

At the other end of the market, Australia is a world leader in theinstallationofrooftopsolar.Inits‘State of the energ y market 2021’, the AER reports that the total combined capacity of the rooftopsolarfleetintheNEMinJune2021was11.4GW,whichequated to around 17% of the NEM’s total generation capacity. However,thesuccessofDER(particularlyrooftopsolar)has

created its own challenges for AEMO (in its role as the system

that are linked (contractually) to the output of upstream renewablefacilitiestoallowconsumerstopurchase‘green’energy(overandabovetherequirementsundertheLRETandSRET).

■ Commercial and industrial customers who, in order to reduce their carbon footprint, are increasingly entering into power purchase agreements with large-scale utility renewableprojectseitherdirectlyorindirectlyunder‘look-through’ arrangements with their energy retailers.

In the Northern Territory, the power systems in Alice Springs,Darwin-KatherineandTennantCreekareoperatedbytheNorthernTerritoryElectricitySystem&MarketOperator.ItisadivisionofthePowerandWaterCorporation,whichisaNorthernTerritorygovernment-ownedcorporation.There are also a number of smaller ‘stand-alone’ elec-

tricity grids in the major minerals provinces in Queenslandand Western Australia, and in remote townships throughout remote Australia. The electricity infrastructure in these grids is commonly (but not always) operated on an integrated basis byasingleentity (orsinglecorporategroup). However, thereis a growing trend to introduce renewable generation into these grids to replace (at least in part) existing thermal generation (e.g. dieselorgas-firedgeneration). Thesedevelopmentsarebeingundertaken by the grid operator itself or by outsourcing the developmenttoanindependentpowerproducer.

1.3 Describe the government’s role in the ownership and development of renewable energy and any policy commitments towards renewable energy, including applicable renewable energy targets.

InadditiontotheLRETandSRET,theFederalGovernmenthas funded an ‘Underwriting New Generation Investment’programme to support the development of up to six newpumped hydro projects (in addition to up to six new gasfired powerstations).Upto$1billionoffundinghasbeencommittedto this programme and the shortlisted pumped hydro projects havebeenannouncedbytheFederalGovernment.TheFederalGovernmentalsohastwoagenciesthatprovide

grants or funding to the renewable energy sector: ■ the Australian Renewable Energy Agency, which played

a key role in the last decade in the development of theutility-scale renewable sector, but is now focusing more on adjacentindustries(e.g.‘green’hydrogen);and

■ theCleanEnergyFinanceCorporation(CEFC), which is adedicatedfinanciertorenewableand‘green’projects.

AttheState-level,NSWhasapolicytoachievenetzeroemis-sionsinthatjurisdictionby2050,andhasintroducedenablinglegislationtoprogressivelyimplementits$32billionElectricityInfrastructure Roadmap. The otherAustralian States andTerritories have their own

renewableenergytargets. However,onlytheACT(whichhasalready achieved 100% renewable-sourced energy), TasmaniaandVictoriahaveenshrinedthosetargetsinlegislation.

In Victoria, the Renewable Energ y ( Jobs and Investment) Act 2017 (Vic) legislatesrenewableenergytargetsof25%by2020,40%by2025and50%by2030forthatState.ThisActimposesnoobligations on industry participants or consumers; instead, the targets are used to drive the State Government’s investmentand procurement policies in the renewable energy sector. To that end, the Victoria Government ran a reverse auction in2017/18topurchase928MWofrenewableenergyunderofftakecontracts from three wind projects and three solar projects. It has now announced that it will run a second auction process this year (2021) for at least 600MW of new renewable energy capacity to be located in Victoria.

8 Australia

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

Conversely, generation below 5MW capacity is exempt from registration.However,toderivespotmarketrevenue,thesmall-scale facility must be exported into the NEM by a registered market customer (e.g. a retailer) or a registered small generation aggregator. Generation (including renewable generation) at or above

30MWcapacitymustberegisteredwithAEMOaseither‘sched-uled’ (i.e. dispatchable) generation or as ‘semischeduled’ (i.e.semidispatchable)generationwithAEMO.Scheduledgenera-tors compete on a lowest-price basis to be dispatched into the wholesalemarket. Similarly,semischeduledgeneration(whichisthecategorythatappliestovariablerenewableenergygenera-tion)alsocompetestobedispatchedintothemarket.However,semi-scheduled generation is excused under the market rules if it does not meet its dispatch targets due to a lack of renewable resources (e.g. wind, solar, etc.).InsomejurisdictionsintheNEM,additionalStateorTerritory

generation licences/authorities also need to be obtained from thejurisdictionalenergyregulatororgovernmentdepartment.

Transmission and distributionThe major transmission and distribution networks in the NEM are regulated monopolies. They are economically regulated by theAERandtheirannualrevenueentitlementsaredetermined,inadvance,infive-yearcycles.

In addition, the owner, operator or controller of the trans-mission or distribution network must also be registered as a ‘network service provider’ with AEMO. Also, the operatorsof the major network businesses are usually required to hold a distribution authority or network licence from the energy regu-latororgovernmentdepartmentinthejurisdiction(i.e.theStateor Territory) in which they are located.

An open access policy applies to the interconnected grid that underpins the NEM. The process for renewable projects to obtain access to the network under that principle is set out in the National Electricity Rules.

The construction of connecting lines into the regulated network is not restricted to the regulated network entity. However, if the line is30kmor longer, itmustbebuilt tothedesign standard of the regulated network and, once built, must be handed over to be operated and maintained by the regu-lated network entity (under contract). The owner of these large connecting assets must also publish an access policy outlining the basis on which it will enable others to connect into the line.As mentioned above, some jurisdictions in the NEM are

developingtheirownframeworksforREZ,andtheopenaccessmodel might be disapplied to those zones. Instead, a finite amount of access to the REZ might be auctioned to renewable developers.The above discussion relates only to the NEM. System-

specific requirements apply to the other major transmission or distribution systems in Australia (e.g. the WEM in Western Australia and the power systems in the Northern Territory).

2.5 What are the main challenges that limit investment in, and development of, renewable energy projects?

Australia’s transmission grids, particularly those in the NEM, were built on a ‘hub and spoke’ model to bring electricityfrom large-scale thermal generation into major cities and other demandcentres.However,increasingly,generationintheNEMis becoming decentralised as thermal generation is being replaced or displaced by dispersed renewable generation across the grid.

This means that:■ the transmission networks are in need of substantial

upgrades to accommodate new renewable generation; and

operator for the NEM). This is because AEMO has little control overthedispatchabilityofexportedpowerfromtherooftopsolarfleet. Instead, export from rooftop solar comes into the system (and the wholesale market) ahead of utility-scale generation, to meetsystemdemand.Thisisprovingtobeunsustainableasthegrid increasinglyoperatesona ‘two-way’basis, and significantreformsareunderdevelopmenttogiveAEMO(andthedistri-butionnetworks)greateroversight,insightandcontrolofDER.

2.2 What role does the energy transition have in the level of commitment to, and investment in, renewables? What are the main drivers for change?

On13July2021,AEMO’sCEO&ManagingDirectorannouncedin a public forum that:

‘Under my leadership, AEMO will work closely and collaboratively with governments, industry and communities to design the affordable, reliable energ y system that Australia needs … an energ y system that’s capable of handling 100% renewable energ y, at any moment of the day, by 2025.’

This marked a significant increase in planning by AEMO for the integration and penetration of renewable energy in the NEM. However, this does not mean that the generation fleet in

theNEMwillbewhollyrenewableby2025,orthatrenewableenergywilldominatedispatchatalltimesineachdayin2025.Instead, it is a recognition that, like what actually occurred in South Australia in October 2020, by 2025 there will beincreasing instances whereby some regions in the NEM will be wholly supplied by renewable energy.Thisreflectstheimpactthattheenergytransitionishavingon

investmentinrenewablesinAustralia.Thattransitionisbeingdrivenby,amongstotherthings:■ sustained demand for the installation of rooftop solar/

DER by consumers (in the residential, commercial and industrial sectors);

■ thedecreasingcapitalcostforrenewableenergy,batteriesand associated technology;

■ theprogressiveretirementofcoal-firedpowerstationsatthe end of their technical or economic life; and

■ jurisdictional policies supporting the development ofrenewableenergyprojects(seequestion1.3,above).

2.3 What role, if any, has civil society played in the promotion of renewable energy?

Civil society in Australia has played a significant role in thepromotion of renewable energy through:■ theveryhighpopularityandtake-uprateofDER(particu-

larly rooftop solar) amongst households and the business community; and

■ in the commercial and industrial sector, an increasedappetite to reduce their carbon footprint. This is being achieved through, amongst other things, the acquisitionof renewable energy under power purchase agreements or renewable-linked retail contracts.

2.4 What is the legal and regulatory framework for the generation, transmission and distribution of renewable energy?

GenerationIn theNEM, generation facilities of 5MWorhigher capacityare generally required to be registered with AEMO as a ‘marketgenerator’iftheyexport power into the power system.

9MinterEllison

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

due diligence on the project and submit a final and best offer. After that, negotiations ideally are finalised quickly with a final preferred bidder through to signing of a sale and purchase agree-ment (and any related documentation). Completion of the trans-action would occur sometime after signing, depending on the amount of time required for the parties to undertake pre-comple-tion requirements.

2.7 To what extent is your jurisdiction’s energy demand met through domestic renewable power generation?

Asperquestion2.1above,inits‘State of the energ y market 2021’, the AER reported that the total combined capacity of domestic renewablepowergeneration in June2021was11.4GW,whichequated to around 17% of the NEM’s total generation capacity.

In Western Australia, in October 2020, the Western Australian MinisterforEnergynotedthat300,000householdsintheSWIShadrooftopsolar,whichaccountedforover20%oftheannualelectricity generated in that power system. A further 1MW of DER was continuing to be added to the system on a week-on-week basis.

3 Sale of Renewable Energy and Financial Incentives

3.1 What is the legal and regulatory framework for the sale of utility-scale renewable power?

The energy regulatory framework for the sale of utility-scale renewable power into the NEM (and major Australian power systems)onamerchantbasisisdescribedinquestion2.4,above.However, inorder to secure the revenue streams for anew

project, the developer will commonly look to enter into apower purchase agreement with one or more offtakers from the project.Thesecontractsarecommonlyreferredtoas‘contractsfordifferences’ (i.e. financialderivatives) and,before enteringintosucharrangements,thedevelopershouldconsiderwhethertheywillneedtoholdanAustralianfinancialserviceslicenceinorder to lawfully do so.

The sale of utility-scale renewable power in off-grid scenarios, remotelocationsandisolatedgridsissubjecttolowerlevelsofregulation;however,theowneroroperatorofthefacilitymayberequiredtoholdaState-orTerritory-specificgenerationorretaillicence or authority.

3.2 Are there financial or regulatory incentives available to promote investment in/sale of utility-scale renewable power?

AnumberoffinancialorregulatoryincentiveshavebeenofferedbytheFederal,StateandTerritoryGovernments.Seequestion1.3aboveformoredetails.

3.3 What are the main sources of financing for the development of utility-scale renewable power projects?

Australia has a mature market for the financing of utility-scale renewable power projects. Participants in the market include the major Australian banks, as well as local branches of interna-tional financiers.Inaddition,theCEFC(aFederalGovernmentagency)hasa

specificmandatetofinancerenewableand‘green’projects.

■ thedistributionnetworksarebeingcalledontooperateina‘two-way’fashion,bothtodistributepowerstoend-useconsumers and take back and re-distribute power from their on-site generation and battery facilities.

At the utility-scale end of the sector, securing timely access to the grid is an ongoing challenge. Each connection is subject to detailed consideration by the regulated network entity and by AEMO,particularlyinrelationtotheimpactthatnewvariablerenewablegenerationwillhaveonthedispatchofothergenera-tion facilities in the system, and more broadly on system security.

These impacts are difficult to assess and may result in:■ newprojectshavingtocommitadditionalcapitaltoinstall

equipmenttoalleviateanysystemsecurityimpactsarisingfromtheirproject,ortoensurethattheydonotadverselyimpact the output of generators already connected to the system; and/or

■ delays inachievingcommissioningandenergisationofanew project at its connection point into the power system.

Even once connection is achieved, the output from someutility-scale renewable plants has, at times, been partly constrained (i.e. reduced) by AEMO to allow it to manage systemsecurityrequirements(e.g.voltageorfrequencyfluctu-ations, low inertia, low system strength, etc.) in the applicable section of the grid.

At the DER side of the sector, a number of pending reforms are proposed to:■ provideAEMOwiththeabilitytodisconnectandrecon-

nect DER to better manage system stability and relia-bilityinthepowersystem.InitialreformsapplyinSouthAustralia but are under broader consideration for the rest of the NEM;

■ permit distribution networks to price for the ‘two-way’servicestheyareincreasinglyprovidingtothemarket(i.e.‘importservices’ forpowerconsumedbyconsumersand‘export services’ for power exported by consumers backinto the grid from DER); and

■ permit distribution networks to create network pricingstructures that reward customers for exporting energy at times of high demand and charge customers when the network is congested.

2.6 How are large utility-scale renewable power projects typically tendered?

Project proponents typically engage merchant banks to run an auction process for the sale of all or part of a renewable project (or equity in the project). This can occur at different points in thedevelopmentofaproject.However,ataminimum,projectscommonly need to have agreed the generator performancesstandardsfortheprojectwithAEMO,holdapplicabledevelop-mentapprovalsand, ideally,haveapowerpurchaseagreementwith a credible buyer for all or some of the projected output of the project.Iftheprojectisfullyfinancedor,evenbetter,fullyconstructed

andconnectedtothegrid,thisgenerallyimprovesthechancesofsecuringabuyer(orbuyers).Inaddition,thefurtherdevel-opedaproject is, thehigher thepurchaseprice (ona$/MWhbasis) is likely to be. Formostsaleprocesses,theassetisinitiallywidelymarketedto

receiveindicativebids.Keyfinancialinformationandaninfor-mationmemorandumisgenerallyprovidedatthisstage.Onceindicativeoffersarereceived,asmallernumberofbidders

areusuallyshortlistedtoreceivefurtherinformationto undertake

10 Australia

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

Some forms of renewable energy generation are requiredto operate under specific legislative frameworks (such asgeothermal generation sources in some States) which includetitling requirements for both exploration and production phases of the project.

Other forms of renewable energy generation (such as utility- scale solar farms and wind farms) are typically regulated under general frameworks that control the use and development ofland, as well as the environmental impacts of developments.In particular, a proponent of a utility-scale renewable energy facilitywill usually require aplanningpermitordevelopmentconsent for theuse anddevelopmentof land for thepurposeof the renewable energy facility. Such a permissionmay alsocoverassociatedinfrastructure(suchasasubstationandpowerlines) and authorise ancillary matters (such as native vegeta-tionremoval).Insomecases,proponentsmaybeexemptfrompermit or consent requirements, or have access to alternativeapprovalpathways(forinstance,thefacilitymaybespecificallyauthorisedandregulatedundertherelevantplanningscheme).

Various studies and assessments are typically required to support the application for a planning permit or develop-mentconsent forautility-scale renewableenergy facility. Forexample, forawind farm,aproponent typicallymustprovideexpert reports that assess impacts such as noise, shadow flicker and electromagnetic interference. As part of the application process, notifications to adjacent owners and occupiers and referralstorelevantauthorities,whocanprovidecommentsorobjections in respect of the application, may also be required. In somejurisdictions,theapplicationwillbesubjecttoreviewbyindependent assessment bodies, and a public inquiry or hearing process may be required as part of the decision-making process. Permitsorapprovalsaretypicallygrantedsubjecttoarangeofconditions, relating to matters such as noise, blade glint, shadow flicker and electromagnetic impact.Inadditiontotherequirementforaplanningpermitordevel-

opment consent, there may be a range of other permit or consent requirementsunderStatelaws.Forexample,aproponentmaybe required to obtain approvals from network operators fortransmission lines, an environmental protection licence maybe required for the construction and operation of the facility (addressing issues such as noise pollution), and approvals orconsents may be required relating to matters such as aboriginal heritage, water, national parks and wildlife.

Where a proposed utility-scale renewable energy facility has, willhaveorislikelytohaveasignificantimpactonanyofthemattersofnationalenvironmentalsignificance(suchasthreat-ened species or ecological communities), the project is required tobereferredtotheCommonwealthMinisterforEnvironmentto assess whether federal environmental approval is requiredunder the Environmental Protection and Biodiversity Conservation Act 1999(Cth).Ifapprovalisrequired,theprojectmustgothroughanassessmentandapprovalprocessinaccordancewithsaidAct,which inmany cases canbeundertaken inparallelwithStateapprovalprocesses.

4.2 What are the primary consents and permits required to construct, commission and operate distributed/C&I renewable energy facilities?

Building and construction registration requirements, both for corporationsandindividuals,applyinallStatesandTerritoriesof Australia. In addition, electrical safety licensing and compli-ance requirements apply on a per-jurisdiction basis.

The Clean Energy Council also operates and administers a well-regarded industry accreditation programme for solar and

3.4 What is the legal and regulatory framework applicable to distributed/C&I renewable energy?

In the NEM, the market rules permit retailers and small gener-ation aggregators to:■ purchase ‘excess’ generation from DER facilities for a

fixed price; and■ subsequentlyexport(i.e.on-sell)thatpowerintotheNEM

attheprevailingwholesalemarketspotprice.In addition, some energy retailers have developed offer-

ings under trial conditions to centrally manage DER facilities to providegridsupportandderiverevenueintheancillaryservicesmarkets associated with the NEM. A significant reform package is under consideration by the Australian Energy Market Commission (AEMC) to streamline the participation of DER in these markets.

3.5 Are there financial or regulatory incentives available to promote investment in distributed/C&I renewable energy facilities?

There are battery and rooftop solar grants, loans or rebates availableintheACT,Queensland,SouthAustraliaandVictoria.

3.6 What are the main sources of financing for the development of distributed/C&I renewable energy facilities?

A number of equipment manufacturers, installers, retailers and third-party financiers provide finance (or deferred paymentcontracts) for the installation of distributed/C&I renewable energy facilities.

3.7 What is the legal and regulatory framework that applies for clean energy certificates/environmental attributes from renewable energy projects?

Seetheresponsetoquestion1.1above.

3.8 Are there financial or regulatory incentives or mechanisms in place to promote the purchase of renewable energy by the private sector?

If private sector participants purchase LGCs and voluntarilysurrender them to the Clean Energy Regulator, they can claim an offset to their carbon emissions under the National Greenhouse andEnergyReportingScheme.Inaddition,underthe‘GreenPower’accreditationprogramme,

consumerscanelecttopayapremiumtotheirretailerfor‘green’power. The retailer must then acquire and surrender LGCs (in addition to their surrender requirements under the LRET to meettheirannualtargets)equaltotheamountof‘green’powerthattheircustomershavepaidapremiumtoacquire.

4 Consents and Permits

4.1 What are the primary consents and permits required to construct, commission and operate utility-scale renewable energy facilities?

The permissions that are required to construct, commission andoperateutility-scalerenewableenergyfacilitieslargelyvarybased upon the type, size and location of the facility.

11MinterEllison

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

There are examples of both types of microgrids in the NEM; however, the regulatory framework is in need of clarificationand refinement. A regulatory reform package is being consid-ered by the AEMC and is expected to be rolled out in the next one to two years.

4.6 Are there health, safety and environment laws/regulations which should be considered in relation to specific types of renewable energy or which may limit the deployment of specific types of renewable energy?

Health and safety MostStatesandTerritories inAustraliahave implementedthemodel Commonwealth Work Health and Safety legislation.AlthoughVictoriaandWesternAustraliahaveaseparateframe-work, similar health and safety duties apply in these jurisdictions. Underthesehealthandsafetyframeworks,personsconducting

abusinessorundertaking,suchasabusinessthatisdevelopingarenewable energy facility, are under a general duty to ensure the health and safety of workers so far as is reasonably practicable. Inaddition,specificdutiesapplytoadevelopmentinvolvingthedesign, installation, construction or commission of a plant or structures (such as a renewable energy facility) in order to mini-mise risks of health and safety at a workplace. Forexample,aproponentdesigningawindfarmorinstallinga

renewable energy facility may be required to identify, assess and reduce the risk of hazards as far as is reasonably practicable, as wellasmaintainrecordsofrelevantactions.Thiscouldincludedeveloping systems and activities for ignition source control,security requirements and implementing a safety management plan that includes safe work guidelines and processes such as permits to work, incident management and access to site.

In addition, specific regulatory framework relating to elec-trical safetymayapply and regulate the safedevelopment andoperation of the facility.

Environment The environmental protection regulatory framework similarlyvaries between Australian States and Territories. However,mostStatesandTerritorieshaveadoptedasimilarduties-basedframework, modelled on occupational health and safety legis-lation,thatfocusesonpreventingimpactstotheenvironmentfrom pollution and waste. In particular, individuals and organisations involved in the

deployment of a renewable energy facility may be subject to thegeneralenvironmentalduty. Atahigh level, thistypicallyrequires a personwho is engaging in an activity to eliminateor otherwise minimise risks of harm to human health and the environment frompollution andwaste so far as is reasonablypracticable.

In some jurisdictions, specific renewable energy generation typeswillrequireauthorisationunderenvironmentalprotectionregulatoryframeworks.Forexample,somejurisdictionsrequirethataproponentalsoholdanenvironmentalprotectionlicence(orsimilar)forawindfarmora‘green’hydrogenfacility.

5 Storage

5.1 What is the legal and regulatory framework which applies to energy storage and specifically the storage of renewable energy?

At the date of writing, stand-alone (e.g. utility-scale) energy storage in the NEM is required to be registered with AEMO as both a market load (for power imported from the grid for

battery installers,which has been approved by theAustralianCompetition and Consumer Commission (ACCC). DER facili-ties must be installed by accredited installers in order to qualify togenerateSTCsundertheSRET.

All distributed/C&I renewable energy facilities must be approvedbytheapplicableregulateddistributionentityinordertoconnecttothedistributiongrid.Seequestion4.4belowformore details.

4.3 What are the requirements for renewable energy facilities to be connected to and access the transmission network(s)?

In the NEM, in order to be connected to and access the trans-missionnetwork,renewableenergyfacilitiesmusthave:■ agreed the ‘generator performance standards’ for the

facility with AEMO;■ negotiated a connection and access agreement with the

regulated transmission entity; and■ completedacommissioningandenergisationprogramme

with AEMO and the regulated transmission entity.These aspects of the ‘open access’ regime are outlined and

regulated under the National Electricity Law and National Electricity Rules.

A slightly different process applies in Victoria due to AEMO havingagreaterroleinplanningandmanagingtheaugmenta-tion of the transmission network than in other jurisdictions in the NEM.Furthermore, going forward, the Renewable Energy Zone

programmes being considered and implemented in Queensland, NSWandVictoriamight seedifferent rulesbeingapplied forrenewableprojectstoconnecttothetransmissionnetworkviathosezones.Seequestion2.4forafurtherdiscussionofthis.

4.4 What are the requirements for renewable energy facilities to be connected to and access the distribution network(s)?

In the NEM, a similar ‘open access’ process to that whichcurrently applies to the transmission grid also generally applies for the connection of utility-scale renewable generation to the distribution network. ForDER, connection to the distribution grid in theNEM

is,exceptinVictoria,mostlygovernedbytheNationalEnergyRetailLaw,theNationalEnergyRetailRulesandrelatedprovi-sions in the National Electricity Rules. In Victoria, State-specific requirements apply.

4.5 Are microgrids able to operate? If so, what is the legislative basis and are there any financial or regulatory incentives available to promote investment in microgrids?

In Australia, a microgrid is generally understood as being either:■ astand-alonepowersystemwhichgenerates,deliversand

supplies electricity to multiple customers, and is not physi-cally connected to the national grid/NEM; or

■ an embedded network that is connected to the NEMthrough a single connection point, but which is capable of operating independently from the NEM. This type of microgrid arrangement can be distinguished from a regular embedded network by having generation andstorage capabilities that enable it to operate autonomously (withouthaving to importpower fromtheNEM)understandard operation.

12 Australia

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

■ investments in businesses or entities with a contractual relationship with the Australian Department of Defence in the energy sector (including renewable energy);

■ investmentsinabusinessorentitythatownsoroperatesan electricity generation station (including storage) with a generation capacity (or proposed capacity) of at least 50MW(noting thatmandatory filing requirementsapplyatcertainlevelshigherthanthis);and

■ investmentsinanenergyretailer(gasorelectricity)wherethe foreign person would subsequently hold interests in energy retailers with more than 100,000 customers (noting that mandatory filing requirements apply for networks, systemsandinterconnectorsthatultimatelyservicemorethan 100,000 customers).

Seeking and obtaining clearance on a voluntary basisprecludes the Treasurer of Australia from calling in a transac-tionforreviewiftherearenationalsecurityconcerns.Withoutamandatoryorvoluntarynotificationandassociatedclearance,the Treasurer has the ability to call in a transaction for up to 10 years(withvery limitedexceptions). Forcompleteness,pleasenotethatevenwithamandatoryorvoluntaryclearanceinhand,theTreasurerretainsa‘lastresort’powertoreviewthedecisionand make certain orders if there are national security risks.

6.2 Are there any currency exchange restrictions or restrictions on the transfer of funds derived from investment in renewable energy projects?

General laws, including banking, anti-money laundering and counter-terrorism financing and sanctions laws apply. As above, specific conditions may be imposed on any clearanceissuedundertheFATA.

6.3 Are there any employment limitations or requirements which may impact on foreign investment in renewable energy projects?

GeneralemploymentlawsinAustraliaapply.Asabove,specificconditions may be imposed on any clearance issued under the FATA.

6.4 Are there any limitations or requirements related to equipment and materials which may impact on foreign investment in renewable energy projects?

There are customs rulings, including trade measures, that may apply for major projects, depending on the goods and their country of origin.

7 Competition and Antitrust

7.1 Which governmental authority or regulator is responsible for the regulation of competition and antitrust in the renewable energy sector?

The ACCC is responsible for the regulation of competition and antitrust in the renewable energy sector.

7.2 What power or authority does the relevant governmental authority or regulator have to prohibit or take action in relation to anti-competitive practices?

TheACCCdoesnothavethepowertoprohibitanti-competitivepractices without a court order.

charging)andamarketgeneratororequivalent(toallowwhole-salemarketrevenuetobederivedfromthesaleofexcesspowerexported into the NEM).

This has seen batteries incur:■ network,marketandsystemsecuritycostsintheircapacity

as a load; and■ marketandsystemsecuritycosts,butnotnetworkcosts,in

their capacity as a market generator,whereas other generation facilities have been able to net-offtheir imports from, and exports to, the NEM to reduce their exposure to such costs.

A significant reform proposal has been released by the AEMC which proposes to, among other things:■ enablestoragetoparticipateintheNEMandrelatedancil-

laryservices/systemsecuritymarketsunderasingled‘inte-gratedresourceprovider’registrationcategory;and

■ ensurethatallNEMmarketparticipantsbeartheirshareof system and network costs on gross rather than netted energy streams in the same way that batteries currently do.

5.2 Are there any financial or regulatory incentives available to promote the storage of renewable energy?

Therearesolarandbatterygrants,loansorrebatesavailableintheACT,Queensland,SouthAustraliaandVictoria.

6 Foreign Investment and International Obligations

6.1 Are there any special requirements or limitations on foreign investors investing in renewable energy projects?

UnderAustralia’s foreign investment regime, ‘foreignpersons’arerequiredtonotifytheAustralianTreasurer,advisedbytheForeignInvestmentandReviewBoard(FIRB), of certain trans-actions and obtain clearance before proceeding with the trans-action.Thisincludesinvestmentinrenewableenergyprojectsand related acquisitions (such as any acquisition of interests in Australian land required for such projects).Australia’s foreign investment regimeconsistsof theForeign

Acquisitions and Takeovers Act 1975 (Cth) (FATA), associated legis-lation and various regulations. The regime is also supportedby Australia’s Foreign Investment Policy and guidance notesreleasedbyFIRB(Guidance Notes), which are updated from timetotime.TheAustralianTreasureradministerstheFATAwith the advice and assistance of FIRB. The regime aimsto ensure that foreign direct investment is not ‘contrary toAustralia’s national interest’. The Treasurer can: ■ provideunconditionalclearanceforthetransaction,onthe

basis it is not contrary to Australia’s national interest; ■ prohibitthetransactionfromproceeding,onthebasisitis

contrary to Australia’s national interest; or ■ imposeconditionsonthetransaction,sothatthetransac-

tion will not be contrary to Australia’s national interest. TheAustralianenergysectorisconsideredasensitivesector

for foreign investments. As renewable energy plays a greaterroleinAustralia’senergymix,FIRBconsidersthatinvestmentsin this sector may affect Australia’s national interest (including with regard to national security). Accordingly, where manda-toryFIRBclearanceisnotrequired,voluntarynotificationcanbemadeandisrecommendedbyFIRBtobemadeforcertaininvestmentsrelatingtorenewableenergyprojects.Forexample,under FIRB’s Guidance Note 8 as last updated 9 July 2021,foreigninvestorsareencouragedtoseekvoluntaryFIRBclear-anceforarangeofrelevanttransactionsincluding:

13MinterEllison

Renewable Energy 2022© Published and reproduced with kind permission by Global Legal Group Ltd, London

8.2 Are alternative dispute resolution or tiered dispute resolution clauses common in the renewable energy sector?

It is common for contracts in the renewable energy sector to use alternativedisputeresolutionmechanisms.Tiereddisputereso-lutionprovisionsarealsocommon.These mechanisms can have particular advantages in the

energy sector, including the renewable energy sector. Parties may prefer all disputes, or at least technical disputes, to be deter-mined by an appropriate subject-matter expert, rather than in thecourts.Similarly,therecanbeaperceptionthatcommercialarbitrationprovidesforgreaterspeed,flexibilityandconfidenti-ality for the resolution of a contractual dispute.

8.3 What interim or emergency relief can the courts grant?

Australiancourtshavebroadandoftendiscretionarypowerstogrant interlocutory and interim injunctions.

In order to obtain interim or emergency relief, a party typi-callyneedstodemonstratetothecourtthattheyhavea‘prima facie case’ or that there is a ‘serious question to be tried’, andthat the balance of convenience favours granting the relief.A party applying for interim relief will usually be required to giveanundertakingtopayanydamagestheotherpartysuffersas a result of the interim relief if the other party is ultimately successfulintheoverarchingdispute.

8.4 Is your jurisdiction a party to and has it ratified the New York Convention on the Recognition and Enforcement of Foreign Arbitral Awards and/or the Convention on the Settlement of Investment Disputes between States and Nationals of Other States and/or any significant regional treaty for the recognition and enforcement of judgments and/or arbitral awards?

Australia is a party to and has ratified both the New York Convention on the Recognition and Enforcement of ForeignArbitral Awards and the Convention on the Settlement ofInvestment Disputes between States and Nationals of OtherStates,towhichtheInternational Arbitration Act 1974(Cth)giveseffect. Foreign judgmentsmay be enforced inAustralia under the

Foreign Judgements Act (the FJA). The FJA is limited to ‘finaland conclusive’ monetary judgments in certain jurisdictions(listedintheregulationstotheFJA)determinedonthebasisof‘substantialreciprocity’forAustralianjudgments(usuallyonthebasis of a bilateral or multilateral agreement, of which there are currently35listedintheregulations).Australiaisalsopartytothe Agreement between the Government of Australia and the Government of New Zealand on Trans-Tasman Court Proceedings and Regulatory Enforcement. Pursuant to the Trans-Tasman Proceedings Act 2010 (Cth), this provides a separate regime for the enforcement ofjudgments of New Zealand courts.

8.5 Are there any specific difficulties (whether as a matter of law or practice) in litigating, or seeking to enforce judgments or awards, against government authorities or the state?

Although a doctrine ofCrown (or State) immunity applies inAustralia,governmentauthoritiesandStatebodiesareusuallynot subject to sovereign immunity in Australia. CommercialpartiesregularlyseekandobtaincivilreliefagainstStateparties.

Ithasbroadpowerstoinvestigateandtakeactioninrelationto anti-competitive practices, including to require productionof documents and information, to obtain a search warrant to enter premises, seize documents and items, and to undertake telephonesurveillance.

7.3 What are the key criteria applied by the relevant governmental authority or regulator to determine whether a practice is anti-competitive?

The prohibitions on anti-competitive practices are set out inPart IV of the Competition and Consumer Act 2010 (Cth).

The key criteria the ACCC has regard to when determining whetherapracticeisanti-competitivearetheprohibitionsthem-selves. In summary terms, the following is prohibited: (A)agreements between competitors or potential competitors with the purpose, effect or likely effect of fixing prices or with the purposeof sharingmarkets,preventing, restrictingor limitingthevolumeortypeofparticulargoodsorservicesavailableorriggingbids(knownas‘cartelconduct’);(B)agreementsorcoop-erativebehaviourbetweencompetitorswiththepurpose,effector likely effect of substantially lessening competition; (C) unilat-eral conduct by a firm with a substantial degree of market power which has the purpose, effect or likely effect of substantially less-eningcompetition;and(D)exclusivedealingwiththepurpose,effect or likely effect of substantially lessening competition.

The ACCC’s focus is on maintaining and promoting compe-tition and remedying market failure, as well as protecting the interests and safety of consumers and supporting fair trading in markets.Itismorelikelytoinvestigateandtakeactioninrela-tion to conduct that is of significant public interest, results in substantialconsumerorsmallbusinessdetriment,orinvolvingsignificant new market issues.

8 Dispute Resolution

8.1 Provide a short summary of the dispute resolution framework (statutory or contractual) that typically applies in the renewable energy sector, including procedures applying in the context of disputes between any applicable government authority/regulator and the private sector.

Participants in the renewable energy sector are commonly partiestoavarietyofcontractsunderwhichdisputesaredeter-minedpursuanttotherelevantcontractualterms.