SD - Ketchikan Gateway Borough School District 13 · This report was issued by BDO USA, LLP, a...

97

This report was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO International Limited, a UK company limited by guarantee. Ketchikan Gateway Borough School District (A Component Unit of the Ketchikan Gateway Borough) Basic Financial Statements, Required Supplementary Information, Additional Supplementary Information, and Single Audit Reports Year Ended June 30, 2013

Transcript of SD - Ketchikan Gateway Borough School District 13 · This report was issued by BDO USA, LLP, a...

This report was issued by BDO USA, LLP, a Delaware limited liability partnership and the U.S. member of BDO International Limited, a UK company limited by guarantee.

Ketchikan Gateway Borough School District (A Component Unit of the Ketchikan Gateway Borough)

Basic Financial Statements, Required Supplementary Information, Additional Supplementary Information, and Single Audit Reports Year Ended June 30, 2013

Ketchikan Gateway Borough School District

(A Component Unit of the Ketchikan Gateway Borough)

Basic Financial Statements, Required Supplementary Information, Additional Supplementary Information,

and Single Audit Reports Year Ended June 30, 2013

Ketchikan Gateway Borough School District

Contents

2

Exhibit Page Independent Auditor’s Report 5-7 Management’s Discussion and Analysis 10-16 Basic Financial Statements

Government-Wide Financial Statements: Statement of Net Position A-1 18 Statement of Activities A-2 19 Fund Financial Statements: Balance Sheet – Governmental Funds B-1 20 Reconciliation of Governmental Funds Balance Sheet to Statement of Net Position B-2 21 Statement of Revenues, Expenditures and Changes In Fund Balances – Governmental Funds B-3 22 Reconciliation of Changes in Fund Balances of Governmental Funds to Statement of Activities B-4 23 Statement of Fiduciary Assets, Liabilities and Net Position C-1 24 Statement of Changes in Fiduciary Net Position C-2 25 Notes to Basic Financial Statements 26-39

Required Supplementary Information

Required Budgetary Comparison Schedule: School Operating Fund D-1 41 Student Transportation Special Revenue Fund D-2 42

Supplementary Information School Operating Fund – Schedule of Revenues, Expenditures and Changes in Fund Balance E-1 44-47 Nonmajor Governmental Funds: Combining Balance Sheet F-1 48-49 Combining Statement of Revenues, Expenditures and Changes in Fund Balances (Deficit) F-2 50-52

Ketchikan Gateway Borough School District

Contents

3

Exhibit Page Supplementary Information, continued

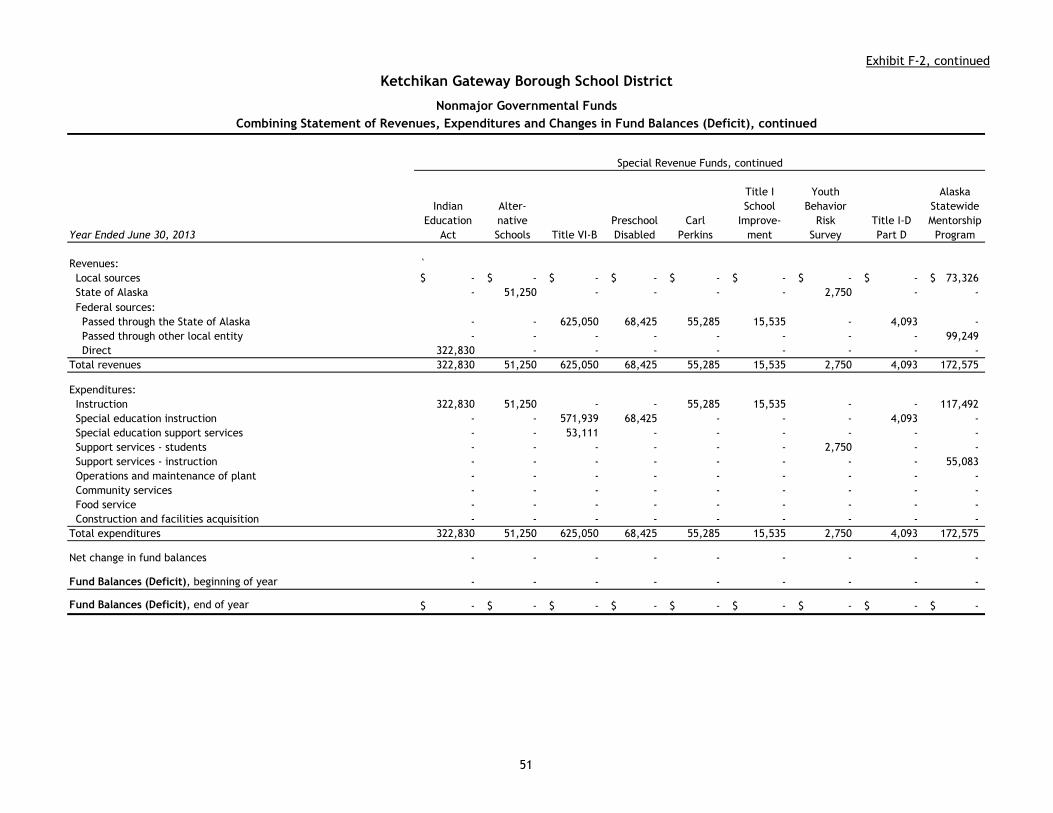

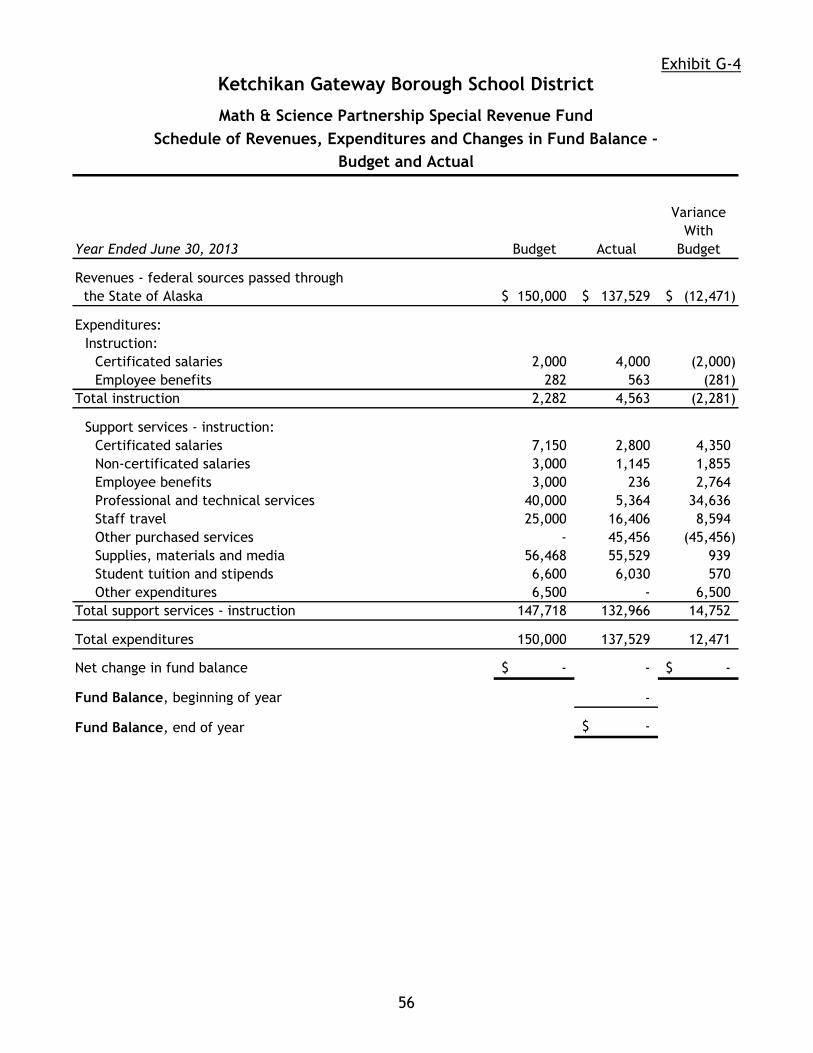

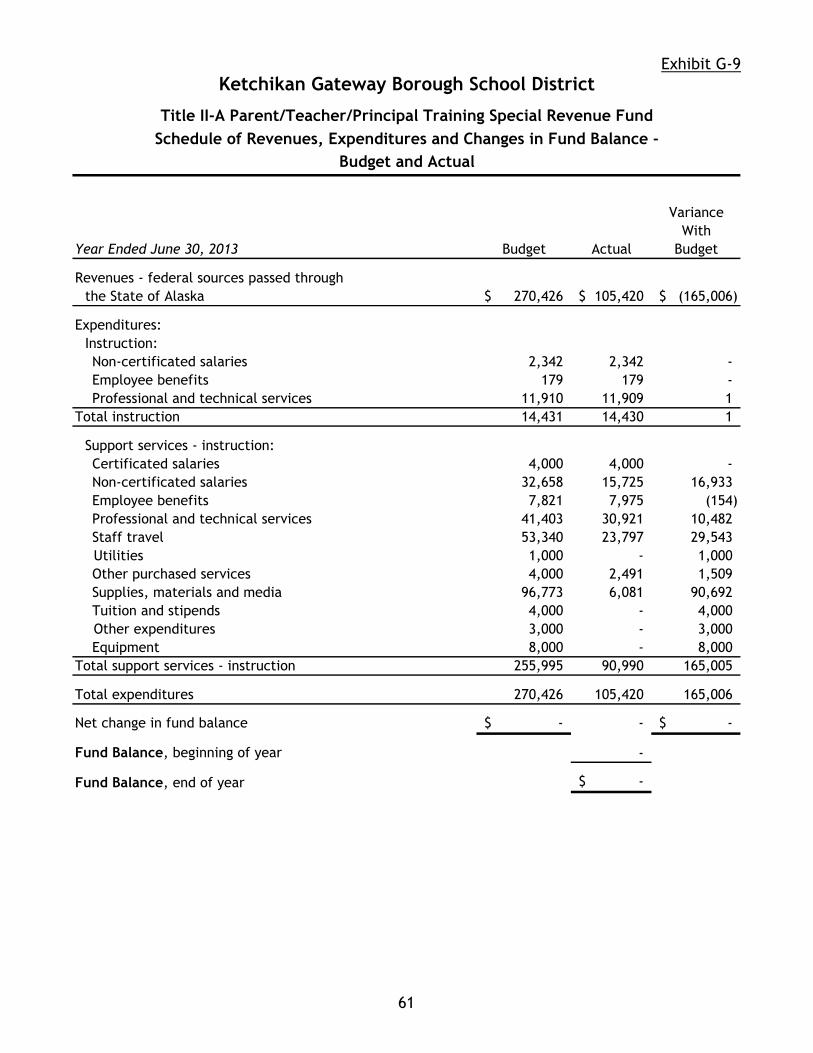

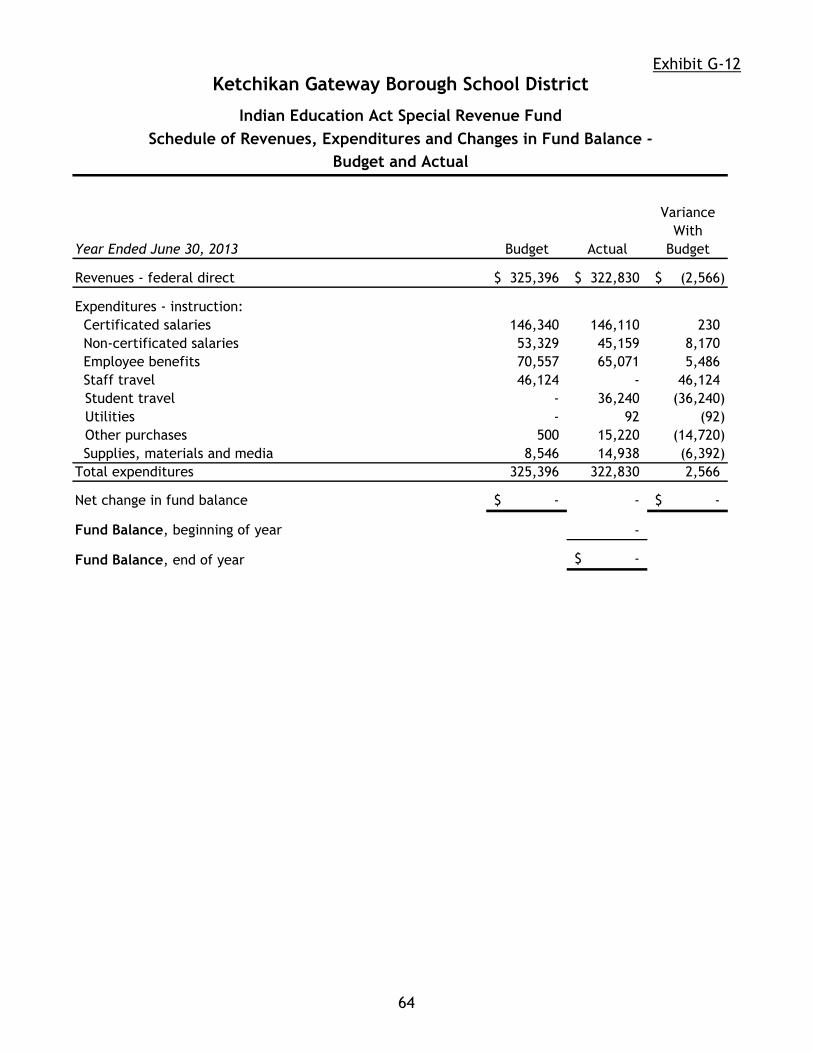

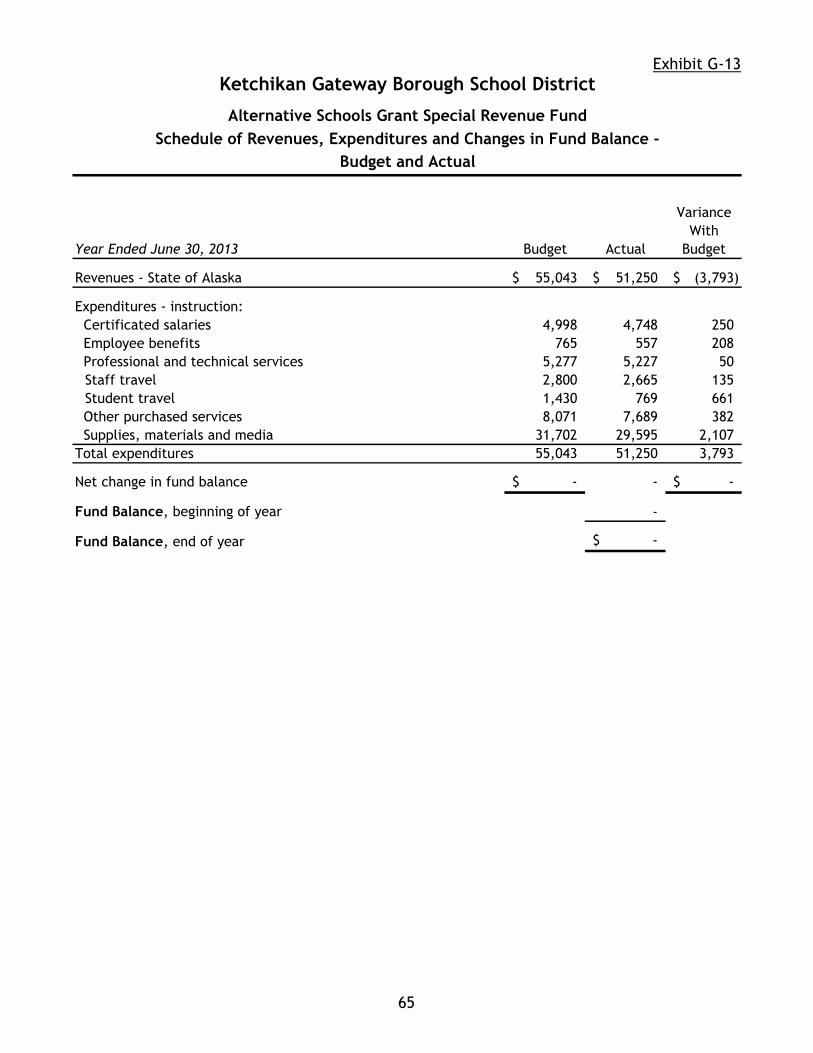

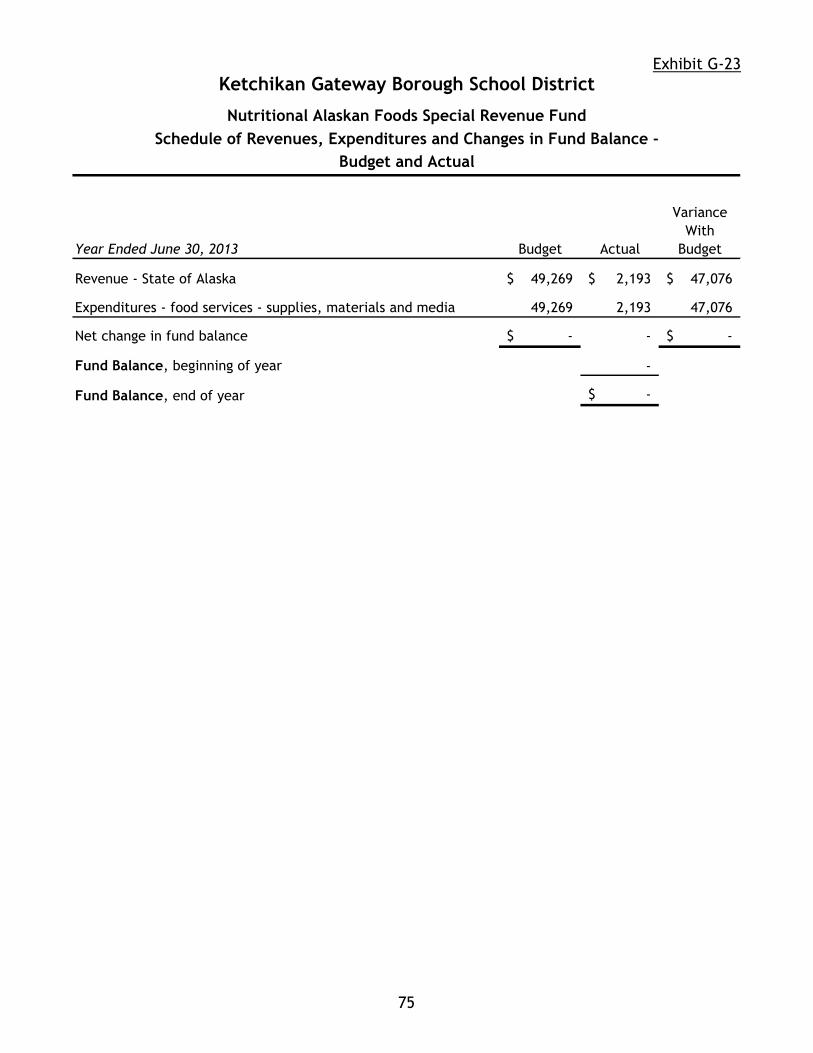

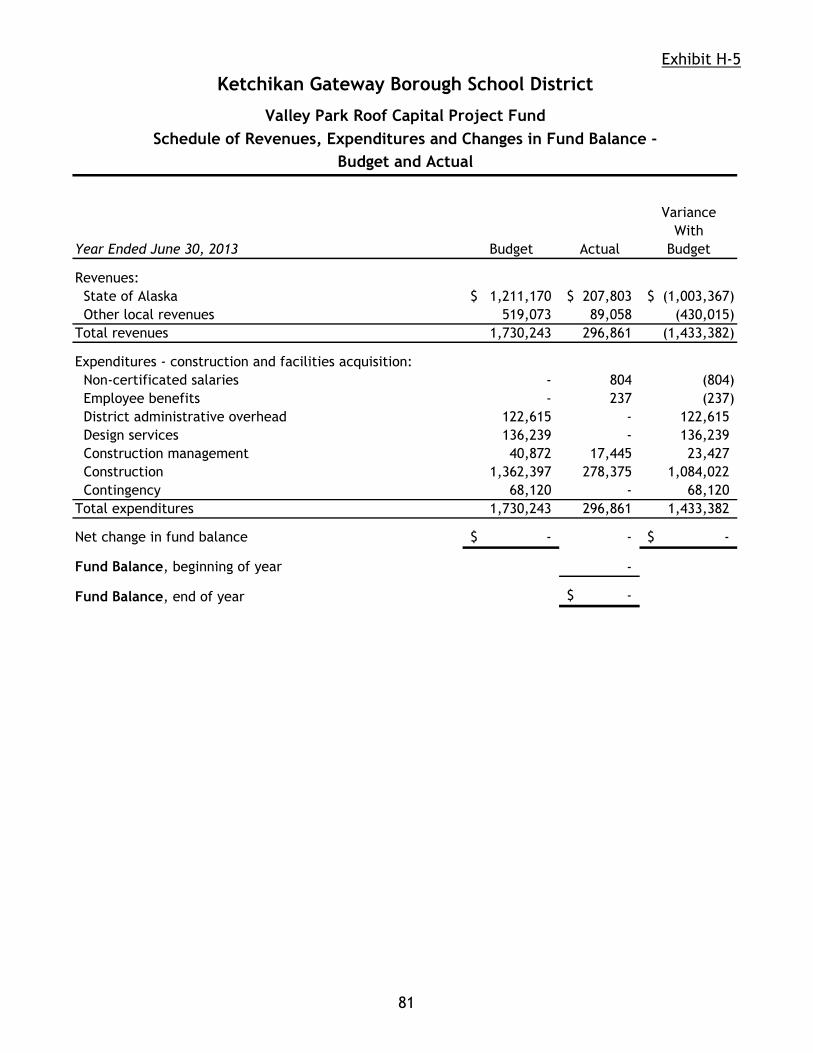

Schedule of Revenues, Expenditures and Changes in Fund Balance (Deficit) – Budget and Actual: Special Revenue Funds: Food Service G-1 53 PAT G-2 54 Ketchikan Construction Academy G-3 55 Math & Science Partnership G-4 56 Student Transportation G-5 57 Ketchikan Regional Youth Facility G-6 58 Public Use of Facilities G-7 59 Youth in Detention G-8 60 Title II-A Parent/Teacher/Principal Training G-9 61 Staff Development G-10 62 Title I G-11 63 Indian Education Act G-12 64 Alternative Schools Grant G-13 65 Title VI-B G-14 66 Preschool Disabled Grant G-15 67 Carl Perkins G-16 68 Title I School Improvement Grant G-17 69 Youth Risk Behavior Survey G-18 70 Title I-D, Part D G-19 71 Statewide Alaska Mentorship Program G-20 72 Salad Bars to School G-21 73 Fresh Fruits and Vegetables G-22 74 Nutritional Alaskan Foods G-23 75 Education Jobs G-24 76 Capital Project Funds: Esther Shea Field Improvements H-1 77 Point Higgins Fire Department Connection H-2 78 Major Maintenance Upgrades H-3 79 Fawn Mountain Elementary Upgrades H-4 80 Valley Park Roof H-5 81

Schedule of Compliance J-1 82 Schedule of Expenditures of Federal Awards K-1 83 Schedule of State Financial Assistance L-1 84 Notes to Schedules of Expenditures of Federal Awards and State Financial Assistance 85

Ketchikan Gateway Borough School District

Contents

4

Page Single Audit Reports

Independent Auditor’s Report on Internal Control Over Financial Reporting and on Compliance and Other Matters Based on an Audit of Financial Statements Performed in Accordance With Government Auditing Standards 87-88

Independent Auditor’s Report on Compliance For Each Major Federal Program and Report on Internal Control Over Compliance Required by OMB Circular A-133 89-90 Independent Auditor’s Report on Compliance For Each Major State Program and Report on Internal Control Over Compliance Required by the State of Alaska Audit Guide and Compliance Supplement for State Single Audits 91-92

Schedule of Findings and Questioned Costs 93-94 Summary Schedule of Prior Audit Findings 95 Corrective Action Plan 96

BDO USA, LLP, a Delaware limited liability partnership, is the U.S. member of BDO International Limited, a UK company limited by guarantee, and forms part of the international BDO network of independent member firms. BDO is the brand name for the BDO network and for each of the BDO Member Firms.

5

3601 C Street, Suite 600 Anchorage, AK 99503

Tel: 907-278-8878 Fax: 907-278-5779 www.bdo.com

Independent Auditor's Report Members of the School Board Ketchikan Gateway Borough School District Ketchikan, Alaska Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, each major fund, and the aggregate remaining fund information of the Ketchikan Gateway Borough School District, a component unit of the Ketchikan Gateway Borough, Alaska, as of and for the year ended June 30, 2013, and the related notes to the financial statements, which collectively comprise the Ketchikan Gateway Borough School District’s basic financial statements as listed in the table of contents. Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error. Auditor’s Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement. An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

6

Opinions In our opinion the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, each major fund and the aggregate remaining fund information of the Ketchikan Gateway Borough School District, as of June 30, 2013, and the respective changes in financial position for the year then ended in accordance with accounting principles generally accepted in the United States of America. Other Matters Required Supplementary Information Accounting principles generally accepted in the United States of America require that management’s discussion and analysis on pages 10 through 16 and the budgetary comparison schedules on pages 42 through 43 be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance. Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the Ketchikan Gateway Borough School District’s basic financial statements. The accompanying Schedule of Expenditures of Federal Awards, the Schedule of State Financial Assistance, and the combining and individual fund financial statements and schedules listed in the table of contents are presented for purposes of additional analysis and are not a required part of the basic financial statements. The Schedule of Expenditures of Federal Awards and the Schedule of State Financial Assistance are required by OMB Circular A-133 and the State of Alaska Audit Guide and Compliance Supplement for State Single Audit, respectively. The Schedule of Expenditures of Federal Awards, the Schedule of State Financial Assistance, and the combining and individual fund financial statements and schedules are the responsibility of management and were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the basic financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the basic financial statements or to the basic financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, the accompanying supplementary information is fairly stated, in all material respects, in relation to the basic financial statements as a whole.

7

Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated November 4, 2013 on our consideration of the Ketchikan Gateway Borough School District's internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, and grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering Ketchikan Gateway Borough School District’s internal control over financial reporting and compliance.

Anchorage, Alaska November 4, 2013

8

This page intentionally left blank.

9

Management’s Discussion and Analysis

Ketchikan Gateway Borough School District

Management’s Discussion and Analysis Year Ended June 30, 2013

10

This section of Ketchikan Gateway Borough School District’s annual financial report represents its discussion and analysis of the District’s financial performance during the fiscal year ended June 30, 2012. Please read it in conjunction with the District’s financial statements, which immediately follow this section. Financial Statements Key financial highlights for 2013 are as follows:

The assets of the Ketchikan Gateway Borough School District exceeded its liabilities at the end of the fiscal year by $2,466,364 (net position). Of this amount, $1,633,223 (unrestricted net position) may be used to meet the Districts ongoing obligations to students, teachers, citizens and creditors.

In total, net position increased by $864,221, which represents a 55 percent change of net assets from 2012. All activities in the District are governmental activities. There were no business-type activities in 2012.

Total general revenues accounted for $35,695,914 or 88 percent of all revenues. Program specific revenues in the form of charges for services (lunch sales and teacher housing) and grants accounted for $195,831 or less than 1 percent of total revenues of $40,674,967.

The District had $39,810,746 in expenses. Typical of Alaska School District operations, only $4,979,053 or 13 percent of these expenses was offset by program specific charges for services and grants. The remainder of expenses, $34,831,693, is covered by general revenues.

As of the close of the current fiscal year, Ketchikan Gateway Borough School District’s governmental funds reported combined ending fund balances of $2,036,922. Of the total fund balance, $43,713 is in nonspendable form, $232,038 is committed, $394,939 is assigned and the remaining balance of $1,366,232 is unassigned.

Overview of the Financial Statements This discussion and analysis is intended to serve as an introduction to Ketchikan Gateway Borough School District’s basic financial statements. Ketchikan Gateway Borough School District’s basic financial statements are comprised of 1) government-wide financial statements 2) fund financial statements, and 3) notes to the financial statements.

Government-wide financial statements provide both short-term and long-term information about the District’s overall financial status.

Fund financial statements focus on individual parts of the District, reporting the District’s operations in more detail than the government-wide statements and on a current (short-term) perspective.

Ketchikan Gateway Borough School District

Management’s Discussion and Analysis

11

Fund financial statements include the governmental fund statements which tell how basic services, such as, instruction were financed in the short-term as well as what remains for future spending. The fiduciary fund statement provides information about the financial relationship in which the District acts solely as an agent for the benefit of student groups.

The financial statements also include notes that explain some of the information in the statements and provide more detailed data. The basic statements are followed by three additional sections (1) required supplementary information related to budgetary presentation (2) additional supplementary information on individual fund activity and a Schedule of State Financial Assistance and Schedule of Expenditures of Federal Awards and (3) single audit and compliance reporting. Government-wide Statements The government-wide statements report information about the District as a whole using accounting methods similar to those used by private-sector companies. The statement of net position includes all of the District’s assets and liabilities, with the difference between the two reported as net position. The two government-wide statements report the District’s net position and how they have changed. Net position – the difference between the District’s assets and liabilities – is one way to measure the District’s financial position.

Over time, increases or decreases in the District’s net position are an indicator of whether its financial position is improving or deteriorating, respectively.

To assess the overall financial position, you need to consider additional nonfinancial factors such as the condition of school buildings and other facilities.

The government-wide financial statements include all the District’s governmental activities, which accounts for all of the District’s basic services such as instruction, maintenance and operations, and administration. Fund Financial Statements The fund financial statements provide more detailed information about the District’s funds, focusing on its most significant or “major” funds – not the District as a whole. Funds are accounting devices the District uses to keep track of specific sources of funding and spending on particular programs:

Some funds are required by state law and/or by governmental accounting standards.

The District establishes other funds to control and manage money for a particular purpose or to show that it is properly using certain fund revenues (such as federal grants).

Ketchikan Gateway Borough School District

Management’s Discussion and Analysis

12

The District has two kinds of funds:

Governmental Funds: Most of the District’s basic services are included in governmental funds. Unlike the government-wide financial statements, governmental fund financial statements focus on short-term inflows and outflows of spendable resources, as well as balances of spendable resources left at fiscal year-end. Consequently, the governmental funds statements provide a detailed short-term view that helps to establish whether there are more or fewer financial resources that can be spent in the near future to finance the District’s programs. Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the district’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities. Ketchikan Gateway Borough School District maintains several individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures, and changes in fund balances for each major fund. The School Operating Fund which is currently the District’s largest major fund. Data from the other governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these nonmajor governmental funds is provided in the form of combining statements and individual budget to actual schedules in the additional supplementary information section of this report.

Fiduciary Funds: The District is the agent, or fiduciary, for assets that belong to others as is the case with the Private Purpose Trust Fund and the Agency Fund. The District is responsible for ensuring that the assets are reported in these funds are used only for their intended purposes and by those to whom the assets belong. The District excludes these activities from the government-wide financial statements because it cannot use these assets to finance its operations.

The Individual major fund statements and combining statements for other governmental funds referred to earlier are presented immediately following the required supplementary information on pensions. This includes combining the individual fund statements and schedules. Government-wide Financial Analysis As noted earlier, net position may serve over time as a useful indicator of a District’s financial position in the case of Ketchikan Gateway Borough School District, assets exceeded liabilities by $2,466,364 at June 30, 2013. A significant portion of the Ketchikan Gateway Borough School District’s net position are reported as invested in capital assets, primarily equipment and artwork. The District uses its capital assets to provide services to students; however these assets are not available for future spending, and thus are reported separately from unrestricted net assets. By agreement with the Ketchikan Gateway Borough, land and buildings are reported on the Borough’s financial statements and are not reflected in these financial statements. The District has a balance of unrestricted net position of $1,633,223.

Ketchikan Gateway Borough School District

Management’s Discussion and Analysis

13

Financial Analysis of the District as a Whole The following table provides a summary of the district’s net assets for 2013 compared to 2012:

Condensed Statement of Net Position Governmental Activities – Total % Change

2013 2012 ChangePercentage

Change Assets Current assets $ 3,614,379 $ 3,277,413 $ 336,966 10% Non-current 813,141 776,018 37,123 5 Total Assets $ 4,427,520 $ 4,053,431 $ 374,089 9% Liabilities Current liabilities $ 1,577,457 $ 2,109,788 $ (532,331) 25% Non-current liabilities 403,699 361,500 (42,199) 12 Total Liabilities $ 1,981,156 $ 2,471,288 $ (490,132) 20% Net Position Net investment in capital assets $ 813,141 $ 776,018 $ 37,123 5% Unrestricted 1,633,223 806,125 827,098 103 Total Net Position $ 2,446,364 $ 1,582,143 $ 864,221 55% The following tables shows the changes in net assets for fiscal year 2013 compared to 2012: 2013 2012 Revenues:

Program revenues: Charges for services $ 195,831 $ 239,807 Operating grants and contributions 4,571,919 4,850,484 Capital grants and contributions 211,302 10,274

General revenues: Borough appropriations 8,239,518 8,650,000 E-Rate revenue 53,847 60,421 Unrestricted grants and contributions 27,310,079 23,163,797 Miscellaneous 92,470 65,281

Total revenues 40,674,966 37,040,129

Ketchikan Gateway Borough School District

Management’s Discussion and Analysis

14

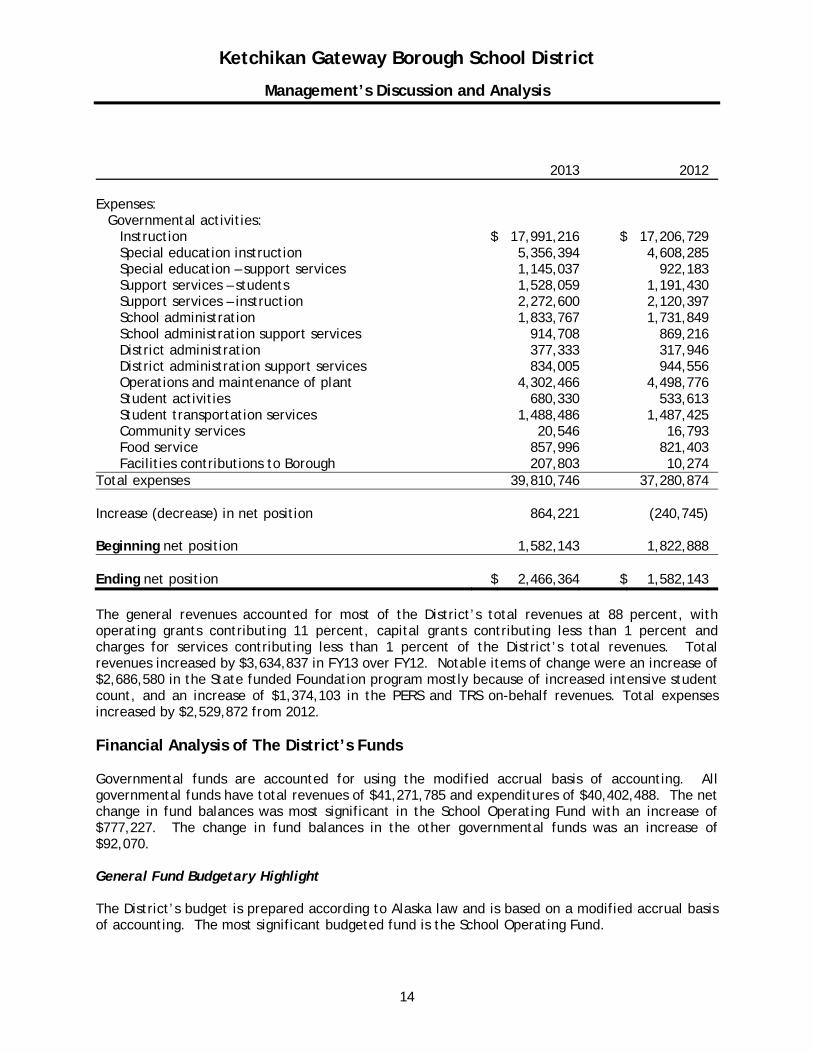

2013 2012 Expenses:

Governmental activities: Instruction $ 17,991,216 $ 17,206,729 Special education instruction 5,356,394 4,608,285 Special education – support services 1,145,037 922,183 Support services – students 1,528,059 1,191,430 Support services – instruction 2,272,600 2,120,397 School administration 1,833,767 1,731,849 School administration support services 914,708 869,216 District administration 377,333 317,946 District administration support services 834,005 944,556 Operations and maintenance of plant 4,302,466 4,498,776 Student activities 680,330 533,613 Student transportation services 1,488,486 1,487,425 Community services 20,546 16,793 Food service 857,996 821,403 Facilities contributions to Borough 207,803 10,274

Total expenses 39,810,746 37,280,874 Increase (decrease) in net position 864,221 (240,745) Beginning net position 1,582,143 1,822,888 Ending net position $ 2,466,364 $ 1,582,143 The general revenues accounted for most of the District’s total revenues at 88 percent, with operating grants contributing 11 percent, capital grants contributing less than 1 percent and charges for services contributing less than 1 percent of the District’s total revenues. Total revenues increased by $3,634,837 in FY13 over FY12. Notable items of change were an increase of $2,686,580 in the State funded Foundation program mostly because of increased intensive student count, and an increase of $1,374,103 in the PERS and TRS on-behalf revenues. Total expenses increased by $2,529,872 from 2012. Financial Analysis of The District’s Funds Governmental funds are accounted for using the modified accrual basis of accounting. All governmental funds have total revenues of $41,271,785 and expenditures of $40,402,488. The net change in fund balances was most significant in the School Operating Fund with an increase of $777,227. The change in fund balances in the other governmental funds was an increase of $92,070. General Fund Budgetary Highlight The District’s budget is prepared according to Alaska law and is based on a modified accrual basis of accounting. The most significant budgeted fund is the School Operating Fund.

Ketchikan Gateway Borough School District

Management’s Discussion and Analysis

15

The actual School Operating Fund expenditures were $677,756 below budget. In its third year, Medicaid Direct Billing revenue of approximately $150,000 can now be depended upon to be a regular part of the District’s operating fund revenue budget. During the year, the District increased its overall School Operating Fund budget expenditures by $792,938. This increase was directly tied to additional grant revenues received. The State rescinded funding for two intensive students, the operating fund budget was revised to reflect this. However, the payments were already made, so the district fund balance will appear to be overstated. The State will reduce the District’s FY14 funding proportionate to the two intensive student funding. Capital Assets (Net of Accumulated Depreciation) As of June 30, 2013 and 2012, the District had invested $813,141 and $771,814, respectively, in machinery and equipment and artwork; all as governmental activities. 2013 2012 Machinery and equipment $ 458,284 $ 421,161 Non depreciable art 354,857 354,857 Total $ 813,141 $ 776,018 Additional information on the District’s capital assets can be found in the notes to the financial statements. Long-Term Debt At June 30, 2013 and 2012, the District’s only reported long-term debt was for accrued compensated absences and termination benefits. Additional information regarding the District’s long-term debt activities can be found in the notes to the financial statements. Economic Factors

The State of Alaska claims it is under financial pressure due to uncertainty and will not commit to sustained and predicable funding. In FY14 it is resorting to its third year of “one-time” funding. While the funding is more than modest in FY14 (1.2 percent of total direct revenue) there is no guarantee for funding in FY15. A loss of 1.2 percent to this District would strain the budgetary process.

Ketchikan Gateway Borough School District

Management’s Discussion and Analysis

16

Foundation funding is based on the annual student count which determines the Average Daily Membership or ADM. A large part of the budget is based on Foundation funding. ADM is determined over a 20-day period during the month of October. Four months into the fiscal year. In addition, Final ADM is not delivered by the state until April. If intensive classifications are contested, such as they were in FY13, a resolution may not be reached for several months; in other words well past the end of the fiscal year. This causes Administration to prudently maintain a strong reserve for such contingencies. However, this is not the most efficient use of funds. Therefore, the state’s procedures for finalizing student count create a chilling effect, which negatively impacts the students of the school district. For FY14 the District’s overall ADM projections appear to be accurate but the distribution between schools did not meet expectations. Also, the District is entering into negotiations with several bargaining groups in FY14. Given negotiations protracted nature as of late, this may create uncertainty impacting the FY15 budget process. Not to mention the actual conclusion of negotiations. Additionally, in tough economic times the local contribution may not be predictable. From 2013 to 2014, the local contribution is projected to decrease by $189,518. Contacting the District’s Financial Management This financial report is designed to provide the District’s citizens, parents, investors and creditors with a general overview of the District’s finances and to demonstrate the District’s accountability for the money it receives. If you have any questions about this report or need additional financial information, contact Matt Groves, Business Manager, Ketchikan Gateway Borough School District, 333 Schoenbar rd. Ketchikan, Alaska 99901.

17

Basic Financial Statements

Exhibit A-1

Governmental

June 30, 2013 Activities

Assets

Cash and cash equivalents 2,135,669$

Accounts receivable 823,150

Receivable from trust fund 11,530

Receivable from Ketchikan Gateway Borough 600,317

Inventories 43,713

Capital assets, not being depreciated 354,857

Depreciable capital assets,

net of accumulated depreciation 458,284

Total Assets 4,427,520$

Liabilities and Net Position

Liabilities:

Accounts payable 631,969$

Payable to agency fund 19,124

Accrued payroll liabilities 478,296

Unearned revenue 448,068

Accrued annual leave 398,899

Termination benefits due within one year 4,800

Total liabilities 1,981,156

Net position:

Net investment in capital assets 813,141

Unrestricted 1,633,223

Total net position 2,446,364

Total Liabilities and Net Position 4,427,520$

The notes to the financial statements are an integral part of this statement.

Statement of Net Position

Ketchikan Gateway Borough School District

18

Exhibit A-2

Net (Expense)

Revenue and

Changes in

Net Position

Operating Capital

Charges Grants & Grants & Govern-

for Contri- Contri- mental

Year Ended June 30, 2013 Expenses Services butions butions Activities

Governmental activities:

Instruction 17,991,216$ -$ 1,179,170$ -$ (16,812,046)$

Special education instruction 5,356,394 - 718,538 - (4,637,856)

Special education support services -

students 1,145,037 - 53,111 - (1,091,926)

Support services - students 1,528,059 - 2,750 - (1,525,309)

Support services - instruction 2,272,600 - 349,445 - (1,923,155)

School administration 1,833,767 - - - (1,833,767)

School administration support services 914,708 - - - (914,708)

District administration 377,333 - - - (377,333)

District administration support services 834,005 - - - (834,005)

Operations and maintenance of plant 4,302,466 - 4,226 - (4,298,240)

Student activities 680,330 - - - (680,330)

Student transportation services 1,488,486 - 1,576,239 - 87,753

Community services 20,546 38,271 - - 17,725

Food service 857,996 157,560 688,441 - (11,995)

Facilities contributed to primary

government 207,803 - - 211,302 3,499

Total governmental activities 39,810,746$ 195,831$ 4,571,920$ 211,302$ (34,831,693)

General revenues:

Borough appropriations 8,239,518

Investment income 62

Grants not restricted to specific programs 27,310,079

E-rate 53,847

Other 92,408

Total general revenues 35,695,914

Change in net position 864,221

Net Position, beginning of year 1,582,143

Net Position, end of year 2,446,364$

The notes to the financial statements are an integral part of this statement.

Program Revenues

Statement of Activities

Ketchikan Gateway Borough School District

19

Exhibit B-1

Student Non-major Total

School Tranportation Esther Shea Govern- Govern-

Operating Special Revenue Field Valley Park mental mental

June 30, 2013 Fund Fund Improvements Roof Funds Funds

Assets

Cash and investments 1,216,992$ 503,916$ -$ 359,010$ 55,751$ 2,135,669$

Accounts receivable 48,489 - - - 774,661 823,150

Receivable from trust fund 11,530 - - - - 11,530

Receivable from Ketchikan Gateway Borough - - 373,285 89,058 137,974 600,317

Due from other funds 1,142,713 - - - - 1,142,713

Inventory - - - - 43,713 43,713

Total Assets 2,419,724$ 503,916$ 373,285$ 448,068$ 1,012,099$ 4,757,092$

Liabilities and Fund Balances

Liabilities: - -

Accounts payable 265,844$ 168,026$ -$ -$ 198,099$ 631,969$

Payable to agency fund 19,124 - - - - 19,124

Accrued payroll liabilities 476,077 - - - 2,219 478,296

Unearned revenue - - - 448,068 - 448,068

Due to other funds - - 373,285 - 769,428 1,142,713

Total liabilities 761,045 168,026 373,285 448,068 969,746 2,720,170

Fund balances:

Nonspendable - - - - 43,713 43,713

Committed 232,038 - - - - 232,038

Assigned - 335,890 - - 59,049 394,939

Unassigned (deficit) 1,426,641 - - - (60,409) 1,366,232

Total fund balances 1,658,679 335,890 - - 42,353 2,036,922

Total Liabilities and Fund Balances 2,419,724$ 503,916$ 373,285$ 448,068$ 1,012,099$ 4,757,092$

The notes to the financial statements are an integral part of this statement.

Balance Sheet - Governmental Funds

Ketchikan Gateway Borough School District

Major Funds

Capital Project Funds

20

Exhibit B-2

Total fund balances of governmental funds 2,036,922$

Total net assets reported for governmental activities in the

Statement of Net Position is different because:

Capital assets used in governmental activities are not financial

resources and therefore are not reported in the funds. These

assets, net of accumulated depreciation, consist of:

Works of art 354,857$

Improvements other than buildings 11,970

Equipment 2,324,105

Total capital assets 2,690,932

Accumulated depreciation (1,877,791)

Total capital assets, net 813,141

Long-term liabilities are not due and payable in the current period and

therefore are not reported as fund liabilities.

Long-term liabilities reported in these statements consist of:

Accrued leave (398,899)

Termination benefits (4,800)

Total net position of governmental activities 2,446,364$

The notes to the financial statements are an integral part of this statement.

Reconciliation of Governmental Funds Balance Sheet

to Statement of Net Position

Ketchikan Gateway Borough School District

Year Ended June 30, 2013

21

Exhibit B-3

Student Non-major Total

School Tranportation Esther Shea Govern- Govern-

Operating Special Revenue Field Valley Park mental mental

Year Ended June 30, 2013 Fund Fund Improvements Roof Funds Funds

Revenues:

Local sources 8,385,835$ -$ 373,285$ 89,058$ 508,426$ 9,356,604$

State of Alaska 27,161,471 1,576,239 - 207,803 127,307 29,072,820

Federal sources 148,608 - - - 2,693,753 2,842,361

Total revenues 35,695,914 1,576,239 373,285 296,861 3,329,486 41,271,785

Expenditures:

Instruction 16,793,119 - - - 1,179,170 17,972,289

Special education instruction 4,642,676 - - - 718,538 5,361,214

Special education support services -

students 1,091,072 - - - 53,111 1,144,183

Support services - students 1,528,354 - - - 2,750 1,531,104

Support services - instruction 1,979,301 - - - 349,445 2,328,746

School administration 1,823,477 - - - - 1,823,477

School administration support services 913,538 - - - - 913,538

District administration 379,740 - - - - 379,740

District administration support services 824,242 - - - - 824,242

Operations and maintenance of plant 4,262,506 - - - 16,996 4,279,502

Student activities 680,330 - - - 680,330

Student transportation - 1,488,486 - - - 1,488,486

Community services - - - - 20,546 20,546

Food service 332 - - - 846,639 846,971

Construction and facilities acquisition - - 373,285 296,861 137,974 808,120

Total expenditures 34,918,687 1,488,486 373,285 296,861 3,325,169 40,402,488

Net change in fund balances 777,227 87,753 - - 4,317 869,297

Fund Balances, beginning of year 881,452 248,137 - - 38,036 1,167,625

Fund Balances, end of year 1,658,679$ 335,890$ -$ -$ 42,353$ 2,036,922$

The notes to the financial statements are an integral part of this statement.

Statement of Revenues, Expenditures and Changes in Fund Balances -

Governmental Funds

Ketchikan Gateway Borough School District

Major Funds

Capital Project Funds

22

Exhibit B-4

Net change in fund balances - total governmental funds 869,297$

The change in net position reported for governmental activities in the

Statement of Activities is different because:

Governmental funds report capital outlay as expenditures.

However, in the Statement of Activities, the cost of those

assets is allocated over their estimated useful lives and

reported as depreciation expense. These are the amounts

reported for capital outlay and depreciation.

Depreciation expense (70,217)$

Acquisition of capital assets 107,340

37,123

Some expenses reported in the Statement of Activities do not

require the use of current financial resources and, therefore, are

not reported as expenditures in governmental funds. These are

the net changes in long-term liability balances.

Increase in accrued annual leave (50,173)

Decrease in termination benefits 7,974

(42,199)

Change in net position of governmental activities 864,221$

The notes to the financial statements are an integral part of this statement.

Reconciliation of Changes in Fund Balances of

Governmental Funds to Statement of Activities

Ketchikan Gateway Borough School District

Year Ended June 30, 2013

23

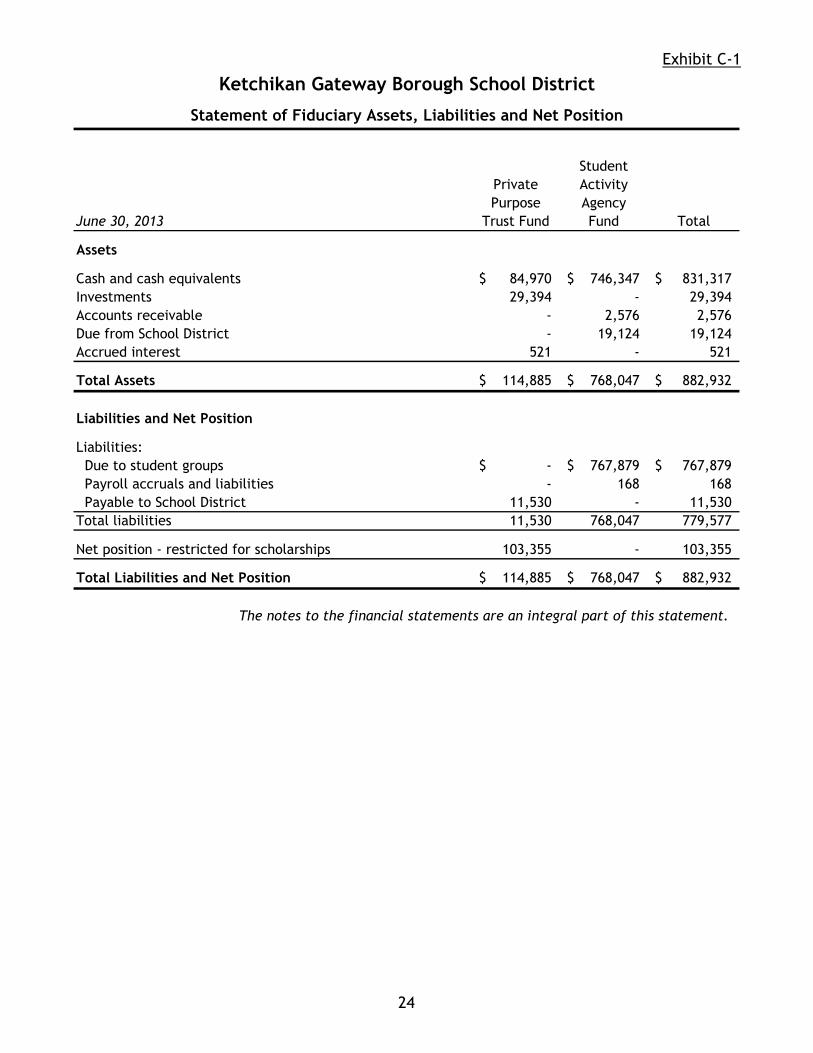

Exhibit C-1

Student

Private Activity

Purpose Agency

June 30, 2013 Trust Fund Fund Total

Assets

Cash and cash equivalents 84,970$ 746,347$ 831,317$

Investments 29,394 - 29,394

Accounts receivable - 2,576 2,576

Due from School District - 19,124 19,124

Accrued interest 521 - 521

Total Assets 114,885$ 768,047$ 882,932$

Liabilities and Net Position

Liabilities:

Due to student groups -$ 767,879$ 767,879$

Payroll accruals and liabilities - 168 168

Payable to School District 11,530 - 11,530

Total liabilities 11,530 768,047 779,577

Net position - restricted for scholarships 103,355 - 103,355

Total Liabilities and Net Position 114,885$ 768,047$ 882,932$

The notes to the financial statements are an integral part of this statement.

Statement of Fiduciary Assets, Liabilities and Net Position

Ketchikan Gateway Borough School District

24

Exhibit C-2

Private

Purpose

Year Ended June 30, 2013 Trust Fund

Additions:

Earnings on investments 280$

Donations 17,700

Other local revenues 87

Total additions 18,067

Deletions - other expenditures 8,500

Change in net position 9,567

Net Position, beginning of year 93,788

Net Position, end of year 103,355$

The notes to the financial statements are an integral part of this statement.

Statement of Changes in Fiduciary Net Position

Ketchikan Gateway Borough School District

25

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements Year Ended June 30, 2013

26

1. Summary of Significant Accounting Policies Reporting Entity The Ketchikan Gateway Borough School District (the District) operates under the statutes of the State of Alaska applicable to borough school districts. The Board of Education is composed of seven members elected at large to three year terms. The accounting and financial reporting policies are regulated by the State of Alaska Department of Education and Early Development in accordance with generally accepted accounting principles for state and local governments. The Ketchikan Gateway Borough School District is a component unit of the Ketchikan Gateway Borough because the Borough has accountability for all significant fiscal matters. The Borough is responsible for approving the School District’s expenditure authority in total and appropriating Borough funds for school district operations. It is responsible for general obligation bonds issued for school construction. The Ketchikan Gateway Borough School District provides elementary and secondary education services to Borough residents. Government-Wide and Fund Financial Statements The government-wide financial statements (i.e., the statement of net position and the statement of activities) report information on all of the nonfiduciary activities of the School District. For the most part, the effect of interfund activity has been removed from these statements. The District engages only in governmental activities, which are normally supported by intergovernmental revenues. It does not engage in business-type activities, which rely to a significant extent on fees and charges for support. The District does not have any component units. The statement of activities demonstrates the degree to which the direct expenses of a given function or segment is offset by program revenues. Direct expenses are those that are clearly identifiable with a specific function. Program revenues include 1) charges to customers who purchase, use, or directly benefit from goods, or services provided by a given function; and 2) grants that are restricted to meeting the operational requirements of a particular function. Intergovernmental revenues and other items not properly included among program revenues are reported instead as general revenues. The District does not currently negotiate or employ an indirect rate to allocate charges to grants. Separate financial statements are provided for governmental funds and fiduciary funds, even though the latter are excluded from the government-wide financial statements. Major individual governmental funds are reported as separate columns in the fund financial statements. Measurement Focus, Basis of Accounting and Basis of Presentation The government-wide financial statements are reported using the economic resources measurement focus and the accrual basis of accounting, as are the fiduciary fund financial statements. Revenues are recorded when earned and expenses are recorded when a liability is incurred, regardless of the timing of related cash flows. Grants and similar items are recognized as revenue as soon as all eligibility requirements imposed by the provider have been met.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

27

Governmental fund financial statements are reported using the current financial resources measurement focus and the modified accrual basis of accounting. Revenues are recognized as soon as they are both measurable and available. Revenues are considered to be available when they are collectible within the current period or soon enough thereafter to pay liabilities of the current period. For this purpose, the District considers revenues to be available if they are collected within 90 days of the end of the current fiscal period. Expenditures generally are recorded when a liability is incurred, as under accrual accounting, except expenditures related to compensated absences and claims and judgments, which are recorded only when payment is due. The District reports the following major governmental funds based on the required quantitative criteria:

The School Operating Fund is the District’s primary operating fund. It accounts for all resources used to finance District maintenance and operations except those required to be accounted for in other funds. The Student Transportation Special Revenue Fund accounts for the District’s student transportation activities. The Esther Shea Field Improvements and Valley Park Roof Capital Project Funds account for those two capital projects of the District.

Additionally, the District reports the following fiduciary fund types:

The Private-Purpose Trust Fund is used to account for the resources legally held in trust for student scholarships. All earnings from the investment in the endowment may be used for scholarships. The endowment must be preserved as capital. Agency Funds are used to account for resources where the District’s role is purely custodial. Accordingly, all assets reported in an agency fund are offset by a liability to the parties on whose behalf they are held. The District is custodian of funds raised by student groups.

The District follows the Uniform Chart of Accounts for School Districts as required by the State of Alaska, Department of Education and Early Development. This manual sets guidelines for financial reporting and requirements for basic accounting systems, which are uniform throughout Alaska. Estimates The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenditures during the reporting period. Actual results could differ from those estimates. Summarized below are the major sources of revenues and applicable recognition policies.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

28

Intergovernmental Revenue State of Alaska Public School Funding (Foundation) and pupil transportation revenues, federal impact aid, and federal aid for the school lunch program are susceptible to accrual and are recorded in the year to which they relate. State of Alaska and Federal government cost reimbursable grants and contracts are recorded to the extent of allowable expenditures in the period which the expenditures were incurred. Local Revenue Interest earned is recorded in the School Operating Fund unless otherwise specified by the awarding source. Rental income from District owned property is recorded in the period to which it relates. Both interest and rental income is susceptible to accrual. Assets, Liabilities and Net Position or Fund Balance Cash and Cash Equivalents The District’s cash and cash equivalents are considered to be cash on hand, demand deposits, and short-term investments with original maturities of three months or less from the date of acquisition. There are no statutory limitations on the type of investment allowed. State statutes authorize the Borough to establish a central cash treasury at the Borough. Interest earnings of central cash treasury investments accrue to the Ketchikan Gateway Borough, except for the capital project funds, which by law, accrue to those funds. The District maintains some cash in its own checking accounts to facilitate payments in a timely manner. Agency funds are maintained by the District rather than deposited into the central cash treasury. Receivables and Payables During the course of operations, numerous transactions occur between individual funds for goods provided or services rendered. These receivables and payables are classified as “due from other funds” or “due to other funds” on the balance sheet of fund financial statements and are eliminated in the preparation of the government-wide financial statements. Inventories and Prepaid Items Teaching and maintenance supplies are recorded as expenditures when purchased rather than as consumed. Accounting for inventory of heating fuel and food supplies is on the consumption method. The consumption method records the expenditures when consumed rather than when purchased. Inventories are valued at cost using the first-in, first-out (FIFO) method. Reported inventories are equally offset by a fund balance classified as nonspendable, which indicates they do not constitute “available spendable resources” even though they are a component of net current assets. Payments made to vendors for services that are applicable to future accounting periods are recorded as prepaid items. The prepaid items recorded in the governmental fund types do not reflect current available resources and, an equivalent portion of fund balance is nonspendable. Capital Assets Capital assets, which include equipment and improvements to property, are reported in the government-wide financial statements. Capital assets are defined by the District as assets with an initial, individual cost of more than $5,000 and an estimated useful life in excess of one year. Such assets are recorded at historical cost or estimated historical cost if purchased or constructed. Donated capital assets are recorded at estimated fair value at the date of donation.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

29

Land, buildings, infrastructure assets, and construction-in-progress are reported by the Ketchikan Gateway Borough since they hold the title to the land and buildings, and engage the architects, engineers, and contractors to construct new facilities. The cost of normal maintenance and repairs that do not add to the value of the asset or materially extend asset lives are not capitalized. Equipment and improvements to property of the School District are depreciated using the straight line method over the following estimated useful lives: Assets Years Office equipment 7-30 Computer equipment 3-7 Vehicles 7 Furniture 10-30 Other equipment 5-15 Works of art are not depreciated if the art work is removable from the building. Artwork that has become part of the building such as ceramic walls is depreciated over 70 years. Compensated Absences It is the District’s policy to permit employees to accumulate earned but unused annual leave (vacation) and sick pay benefits. There is no liability for unpaid accumulated sick leave since the District does not have a policy to pay any amounts when employees separate from service with the District. All annual leave pay is accrued when earned in the government-wide financial statements. Fund Balance The governmental funds report aggregate amounts for five classifications of fund balances based on the constraints imposed on the use of these resources as follows: Nonspendable fund balance includes amounts that cannot be spent because they are either (a) not in spendable form, such as prepaid items or inventories; or (b) legally or contractually required to be maintained intact. Restricted fund balance reflects the constraints imposed on resources either (a) externally by creditors, grantors, contributors, or laws or regulations of other governments; or (b) imposed by law through constitutional provisions or enabling legislation. Committed fund balance can only be used for specific purposes pursuant to constraints imposed by formal resolutions of the School Board—the government’s highest level of decision making authority. Those committed amounts cannot be used for any other purpose unless the School Board removes the specified use by taking the same type of action imposing the commitment. Assigned fund balance reflects the amounts constrained by the District’s “intent” to be used for specific purposes, but are neither restricted nor committed. The School Board has the authority to assign amounts to be used for specific purposes in the School Operating Fund. Assigned fund balances include all remaining amounts (except negative balances) that are reported in governmental funds, other than the School Operating Fund, that are not classified as nonspendable and are neither restricted nor committed.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

30

Unassigned fund balance is the residual classification for the School Operating Fund. It is also used to report negative fund balances in other governmental funds. When both restricted and unrestricted resources are available for use, it is the District’s policy to use externally restricted resources first, then unrestricted resources—committed, assigned, and unassigned—in order as needed. Net Position In the government-wide financial statements, net position is reported in three categories; net investment in capital assets (net of debt, when applicable); restricted net position; and unrestricted net position. Net position is reported as restricted when constraints placed on net assets use are either externally imposed by creditors (such as through debt covenants), grantors, contributors, or laws or regulations of other governments or imposed by law through constitutional provisions or enabling legislation. 2. Stewardship, Compliance and Accountability Budgetary Information Annual budgets are adopted by the School Board for all revenues, expenditures and interfund transfers of the Operating Fund and all special revenue funds. Budgets are prepared and presented on the modified accrual basis of accounting. Pursuant to Alaska Statutes, the adopted Operating Fund budget is submitted to the Ketchikan Gateway Borough Assembly for review and approval. All special revenue fund budgets are also submitted to the Ketchikan Gateway Borough Assembly so that they may review and approve the total expenditure authority. Upon their review, the Borough Mayor provides a letter to the District stating the amount of local appropriations the District will receive from the Borough in its Operating Fund. The approved Operating Fund budget is then submitted to the State of Alaska Department of Education and Early Development for review to determine compliance with Alaska Statutes and Department regulations. The School Board retains line item authority once the annual local appropriation to the Operating Fund is set by the Borough Assembly. Special revenue fund budgets are revised to agree with the actual grant budget as set by the granting agency. The Superintendent may approve budget revisions of up to ten percent of each line item provided the total program budget does not change. Deficits in Funds The following Special Revenue Fund had a net fund deficit at June 30, 2013: Food Service $ 16,696 This deficit is expected to be recovered in subsequent years from revenues generated from the activities of the Fund and transfers, if necessary, from the School Operating Fund.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

31

3. Cash and Investments The District maintains a central treasury that is available for use by all the funds. Each fund’s portion of the central treasury is displayed on the balance sheet as “Cash and investments” or included in “Due to other funds.” Custodial Credit Risk – Deposits In the case of deposits, this is the risk that in the event of bank failure, the District’s deposits may not be returned to it. As of December 31, 2012 Federal Deposit Insurance Company (FDIC) insures $250,000 deposited per financial institution, without regard to the number of accounts, or if it is an interest bearing or non-interest bearing account. Bank balances, deposited with Wells Fargo Bank, N.A., were covered by federal depository insurance or insured by a tri-party agreement between BNY Western Trust Company, Wells Fargo and Ketchikan Gateway Borough School District. The agreement provides insurance for cash deposited with Wells Fargo Bank only, and it doesn’t insure cash deposited with other financial institutions. The total uninsured amount of cash as of 6/30/2013 is $551,435

June 30, 2013 Carrying Amount Bank

Governmental Funds:

Demand deposits $ 566,036 $ 1,230,961 Equity in Borough treasury 1,569,633 -

Total $ 2,135,669 $ 1,230,961 Private Purpose Trust Fund and Agency Funds – demand deposits $ 831,317 $ 847,699 Investments The Ketchikan Gateway Borough School District does not have an investment policy. By practice it invests its non-expendable scholarship funds in U.S. Government securities. At year end the District had the following investments and maturities: June 30, 2013 Years U.S. Treasury Bonds 8 $ 7,249 AAA U.S. Government Agencies 3 22,145 AAA Total $ 29,394 For investments, custodial credit risk is that, in the event of the failure of the counterparty, the District will not be able to recover the value of its investments or collateral securities that are in the possession of an outside party. All of these investments are held by the counterparty, in the name of the Ketchikan Gateway Borough School District.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

32

4. Accounts Receivable Receivables as of year end for the District’s individual major funds and non-major funds are as follows:

School Operating

Fund

Valley Park Roof CapitalProject Fund

Esther Shea Field

Improvement Capital Project

Fund

Non-Major Governmental

Funds Total Grants $ - $ - $ - $ 774,661 $ 774,661Miscellaneous 48,489 - - - 48,489Trust Fund 11,530 - - - 11,530Ketchikan Gateway Borough - 89,058 373,285 137,974 600,317

Total $ 60,019 $ 89,058 $ 373,285 $ 912,635 $ 1,434,997 Management has determined that all receivables are collectable; therefore no allowance for doubtful accounts has been established. 5. Capital Assets Capital asset activity for the year ended June 30, 2013 follows:

Year ended June 30, Balance

July 1, 2012 Additions DeletionsBalance

June 30, 2013 Capital assets not being

depreciated – works of art $ 354,857 $ - $ - $ 354,857 Capital assets being depreciated:

Improvements other than buildings 11,970 - - 11,970

Equipment 2,216,765 107,340 - 2,324,105 Total capital assets being

depreciated 2,228,735 107,340 - 2,336,075 Accumulated depreciation:

Improvements other than buildings (11,970) - - (11,970)

Equipment (1,795,604) (70,217) - (1,865,821) Total accumulated depreciation (1,807,574) (70,217) - (1,877,791) Net depreciable capital assets 421,161 37,123 - 458,284 Total Capital Assets $ 776,018 $ 37,123 $ - $ 813,141

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

33

Depreciation expense was charged to functions of the District as follows: Instruction $ 26,901 Special education instruction 438 Support services – students 780 Support services – instruction 20,716 School administration support services 1,071 Operations and maintenance of plant 16,729 Food service 3,582 Total Depreciation Expense $ 70,217 6. Interfund Receivables, Payables and Transfers Interfund receivables and payables are shown as “Due to Other Funds” and “Due From Other Funds” in each of the individual funds. These balances at June 30, 2013, were as follows:

June 30, 2013 Due to Other

FundsDue from

Other Funds School Operating Fund $ - $ 1,142,713Esther Shea Field Improvement Captial Project Fund 373,285 -Non-major Governmental Funds 769,428 - $ 1,142,713 $ 1,142,713 The outstanding balances between funds result mainly from the time lag between the dates that (1) interfund goods and services are provided or reimbursable expenditures occur, (2) transactions are recorded in the accounting system, and (3) payments between funds are made. 7. Defined Benefit Pension Plans The District participates in two defined benefit pension plans. The Teachers’ Retirement System (TRS) is a cost-sharing multiple employer plan which covers teachers and other eligible participants. The Public Employees’ Retirement System (PERS) is a cost-sharing multiple employer plan which covers eligible State and local government employees, other than teachers. Both Plans were established and are administered by the State of Alaska to provide pension, postemployment healthcare, death, and disability benefits. Benefit and contribution provisions are established by State law and may be amended only by the State Legislature.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

34

The Plans are included in comprehensive annual financial reports that include financial statements and other required supplemental information. The reports are available at the following address: Department of Administration Division of Retirement and Benefits P.O. Box 110203 Juneau, Alaska 99811-0203 PERS Conversion to Cost Sharing In April 2008, the Alaska Legislature passed legislation which converted the existing Public Employees Retirement System (PERS) from an agent-multiple employer plan to a cost-sharing plan with an effective date of July 1, 2008. Under the cost-sharing arrangement, the State of Alaska Division of Retirement and Benefits no longer tracks individual employer assets and liabilities. Rather, all plan costs and past service liabilities are shared among all participating employers. That same year, the State of Alaska passed additional legislation which statutorily capped the employer contribution, established a state funded “on-behalf” contribution, and required that employer contributions be calculated against all PERS eligible wages, including wages attributable to the defined contribution plan described later in these footnotes. Employee Contribution Rates Regular employees are required to contribute 6.75% of their annual covered salary (2.97% for pension and 3.78% for healthcare) for PERS and 8.65% (4.45% for pension and 4.20% for healthcare) for TRS. Employer and Other Contribution Rates There are three contribution rates associated with the pension and healthcare contributions and related liabilities: Contractual Rate: This is the required funding rate for participating employers. The contractual PERS rate is statutorily capped at 22% of eligible wages, subject to a wage floor, and other termination events. The contractual TRS rate is statutorily capped at 12.56%. Both PERS and TRS contributions are calculated against all participating PERS and TRS payroll, respectively, including those wages attributable to employees in the defined contribution plans. ARM Board Adopted Rate: This is the rate formally adopted by the Alaska Retirement Management Board. This rate is actuarially determined to calculate annual funding requirements of the Plans, without regard to the statutory rate caps. There are no constraints or restrictions on the actuarial cost method or other assumptions used in this valuation, other than those established and agreed to by the ARM Board. Current legislation provides that the State of Alaska will contribute the difference between the ARM Board adopted rate and the contractual (statutory) rate. These additional contributions are recognized by each employer as an on-behalf payment and are reflected as revenue and expense/expenditure within the financial statements.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

35

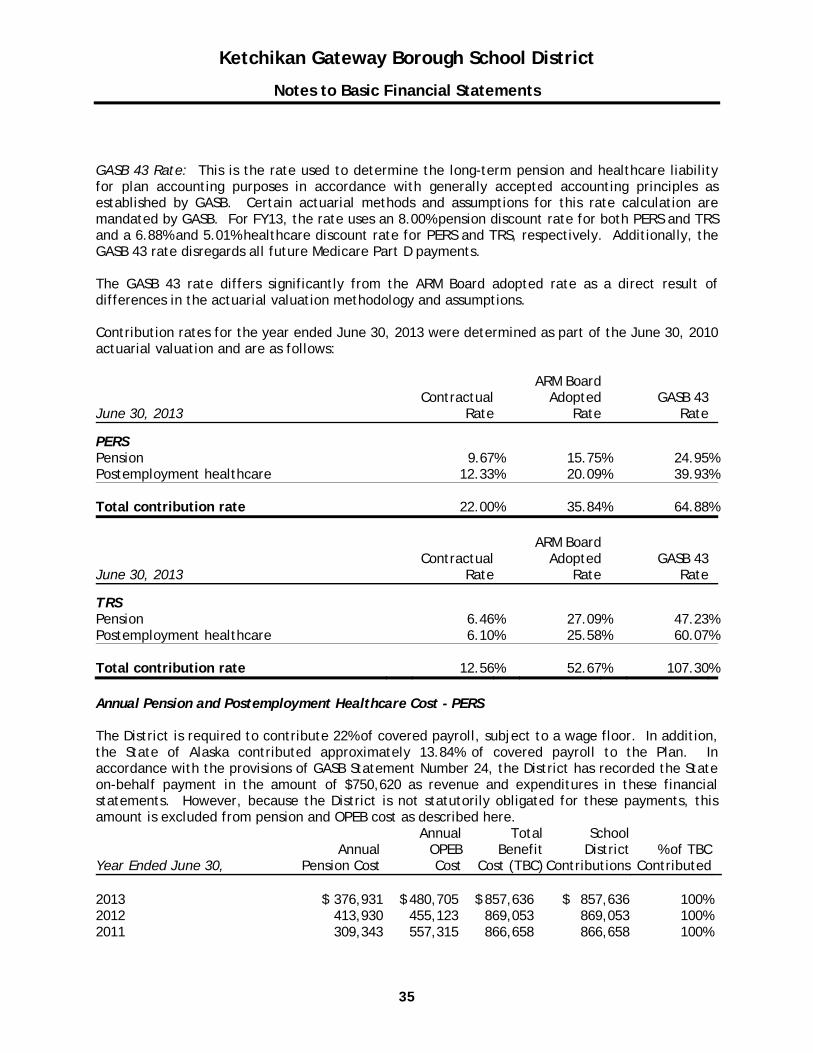

GASB 43 Rate: This is the rate used to determine the long-term pension and healthcare liability for plan accounting purposes in accordance with generally accepted accounting principles as established by GASB. Certain actuarial methods and assumptions for this rate calculation are mandated by GASB. For FY13, the rate uses an 8.00% pension discount rate for both PERS and TRS and a 6.88% and 5.01% healthcare discount rate for PERS and TRS, respectively. Additionally, the GASB 43 rate disregards all future Medicare Part D payments. The GASB 43 rate differs significantly from the ARM Board adopted rate as a direct result of differences in the actuarial valuation methodology and assumptions. Contribution rates for the year ended June 30, 2013 were determined as part of the June 30, 2010 actuarial valuation and are as follows:

June 30, 2013 Contractual

Rate

ARM Board Adopted

RateGASB 43

Rate

PERS Pension 9.67% 15.75% 24.95% Postemployment healthcare 12.33% 20.09% 39.93% Total contribution rate 22.00% 35.84% 64.88%

June 30, 2013 Contractual

Rate

ARM Board Adopted

RateGASB 43

Rate

TRS Pension 6.46% 27.09% 47.23% Postemployment healthcare 6.10% 25.58% 60.07% Total contribution rate 12.56% 52.67% 107.30% Annual Pension and Postemployment Healthcare Cost - PERS The District is required to contribute 22% of covered payroll, subject to a wage floor. In addition, the State of Alaska contributed approximately 13.84% of covered payroll to the Plan. In accordance with the provisions of GASB Statement Number 24, the District has recorded the State on-behalf payment in the amount of $750,620 as revenue and expenditures in these financial statements. However, because the District is not statutorily obligated for these payments, this amount is excluded from pension and OPEB cost as described here.

Year Ended June 30, Annual

Pension Cost

AnnualOPEBCost

Total Benefit

Cost (TBC)

School District

Contributions% of TBC

Contributed 2013 $ 376,931 $ 480,705 $ 857,636 $ 857,636 100% 2012 413,930 455,123 869,053 869,053 100% 2011 309,343 557,315 866,658 866,658 100%

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

36

Annual Pension and Postemployment Healthcare Cost - TRS The District is required to contribute 12.56% of covered payroll, subject to a wage floor. In addition, the State of Alaska contributed approximately 40.11% of covered payroll to the Plan. In accordance with the provisions of GASB Statement Number 24, the District has recorded the State on-behalf payment in the amount of $5,197,183 as revenue and expenditures in these financial statements. However, because the District is not statutorily obligated for these payments, this amount is excluded from pension and OPEB cost as described here.

Year Ended June 30, Annual

Pension Cost

AnnualOPEBCost

Total BenefitCost (TBC)

SchoolDistrict

Contributions% of TBC

Contributed 2013 $ 656,848 $ 620,321 $ 1,277,169 $ 1,277,169 100% 2012 828,441 498,126 1,326,567 1,326,567 100% 2011 732,579 657,591 1,390,170 1,390,170 100% 8. Defined Contribution Pension Plans Employees hired after July 1, 2006 participate in PERS Tier IV and TRS Tier III Defined Contribution Retirement Plans. Both Plans are administered by the State of Alaska, Department of Administration. Benefit and contribution provisions are established by State law and may be amended only by the State Legislature. The Alaska Retirement Management Board may also amend contribution requirements. Included in the Plans are individual pension accounts, retiree medical insurance plan and a separate Health Reimbursement Arrangement account that will help retired members pay medical premiums and other eligible medical expenses not covered by the medical plan. Employee Contribution Rates Employees are required to contribute 8.0% of their annual covered salary. This amount goes directly to the individual’s account. Employer Contribution Rates The District is required to contribute the following amounts based on covered salary: June 30, 2013 PERS Tier IV TRS Tier III Individual account 5.00% 7.00% Retiree medical plan 0.48% 0.49% Occupational death and disability benefits 0.14% 0.00% 5.62% 7.49%

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

37

In addition, the employer must contribute to the Health Reimbursement Arrangement. AS 39.30.370 establishes this contribution amount as “three percent of the average annual employee compensation of all employees of all employers in the plan”. As of July 1, 2012, for actual remittance, this amount is calculated as a flat rate for each full time or part-time employee per pay period and approximates $1,848 per year for each full-time employee and $1.18 per hour for each part-time employee. Employees are immediately vested in their own contributions and vest 25% per year in employer contributions. The District and employee contributions to PERS including the HRA contribution for the year ended June 30, 2013 were $273,676 and $193,644, respectively. The District and employee contributions to TRS for the year ended June 30, 2013 were $362,509 and $259,755, respectively. 9. Long-Term Debt In January, 2009, two teachers elected to receive their retirement bonuses in equal annual installments over a period of five years. A schedule of the District’s change in long-term obligations is as follows:

June 30, 2013 Beginning

Balance Additions ReductionsEnding

Balance

Due Within

One Year Termination benefits $ 12,774 $ - $ 7,974 $ 4,800 $ 4,800 Accrued leave 348,726 309,836 259,663 398,899 398,899 $ 361,500 $ 309,836 $ 267,637 $ 403,699 $ 403,699 10. Fund Balances Fund balances, reported in aggregate on the governmental funds balance sheet is subject to the following constraints:

June 30, 2013 General

FundStudent

TransporationNonmajor

Funds Totals Nonspendable – inventory $ - $ - $ 43,713 $ 43,713 Committed – charter schools 232,038 - - 232,038 Assigned:

Instruction - - 607 607 Student transportation - 335,890 - 335,890 Community services - - 58,442 58,442

Total assigned - 335,890 59,049 394,939 Unassigned (deficit) 1,426,641 - (60,409) 1,366,232 Total Fund Balances $ 1,658,679 $ 335,890 $ 42,353 $ 2,036,922

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

38

11. Risk Management The School District is exposed to various risks of loss related to torts; theft of, damage to, and destruction of assets; errors and omissions; job-related illnesses or injuries to employees; and natural disasters. The School District participates with the Ketchikan Gateway Borough, in purchasing commercial policies to cover most of these risks. Insurance coverage includes general liability, property and casualty coverage, Worker’s Compensation at statutory amounts, and marine coverage, as applicable. In addition, the School District participates with the Ketchikan Gateway Borough in a partially self-funded health plan to cover its employees’ health care coverage (including dental and vision) effective September 1, 1996. It purchases stop loss insurance at $150,000 per covered individual and in an aggregate amount based on employee coverage. It also purchases life and accidental death and dismemberment insurance for eligible employees. Both the School District and Borough participate in the internal service fund established to record transactions involving the partially self-funded health plan. The Borough and the School District contribute to the Borough’s internal service fund and the payments from the fund are used to pay administration and employee health care claims. The Ketchikan Gateway Borough provides an accounting of the internal service fund balances for the Borough and School District on a quarterly basis. The Plan is based on actuarially determined monthly fixed costs and actual claims up to the stop loss of $150,000 per person. The difference between the liability recorded and actual incurred but unrecorded claims may be material. At June 30, 2013, the School District’s share of the deficit is estimated at $268,677 and it is anticipated that this deficit will be reduced through future premium increases. There were no significant reductions in insurance coverage from the prior year, and there have been no settlements that exceed the Borough’s insurance coverage during the past three years. 12. Commitments and Contingencies Amounts received or receivable from grantor agencies are subject to audit and adjustment by the grantor agencies, principally the federal and State governments. Any disallowed claims, including amounts already collected, may constitute a liability of the School Operating Fund. The amount, if any, of expenditures which may be disallowed by the grantor cannot be determined at this time, although the District expects such amounts, if any, to be immaterial. 13. New Accounting Pronouncements The Governmental Accounting Standards Board has passed several new accounting standards with upcoming implementation dates. Management has not fully evaluated the potential effects of these statements, but believes that that GASB Statement 68 will result in the biggest reporting change. Actual impacts have not yet been determined: GASB 66 – Technical Corrections – 2012 – Effective for year-end June 30, 2014 – This statement contains certain technical corrections to prior GASB statements on the topics of Risk Financing, Operating Leases, Loan Purchases, and Servicing Fees.

Ketchikan Gateway Borough School District

Notes to Basic Financial Statements

39

GASB 67 – Financial Reporting for Pension Plans – Effective for year-end June 30, 2014 – This statement changes the reporting and disclosure requirements for government Pension Plans. This statement modifies the Plan-side reporting. GASB 68 – Accounting and Financial Reporting for Pensions – Effective for year-end June 30, 2015 – This statement changes the reporting and disclosure requirements for governments that participate in pension plans. This statement modifies the participating employer side reporting in connection with the Plan side reporting at GASB 67. GASB 69 – Government Combinations and Disposals of Government Operations – Effective for year-end June 30, 2015 – This statement contains certain disclosures to be made about government combinations and disposals of government operations to enable financial statement users to evaluate the nature and effects of these transactions. GASB 70 – Accounting and Financial Reporting for Nonexchange Financial Guarantees – Effective for year-end June 30, 2014 – This statement contains reporting requirements when a government financially guarantees the obligations of another government, non-profit, or private entity without receiving equal value in exchange.

40

Required Supplementary Information

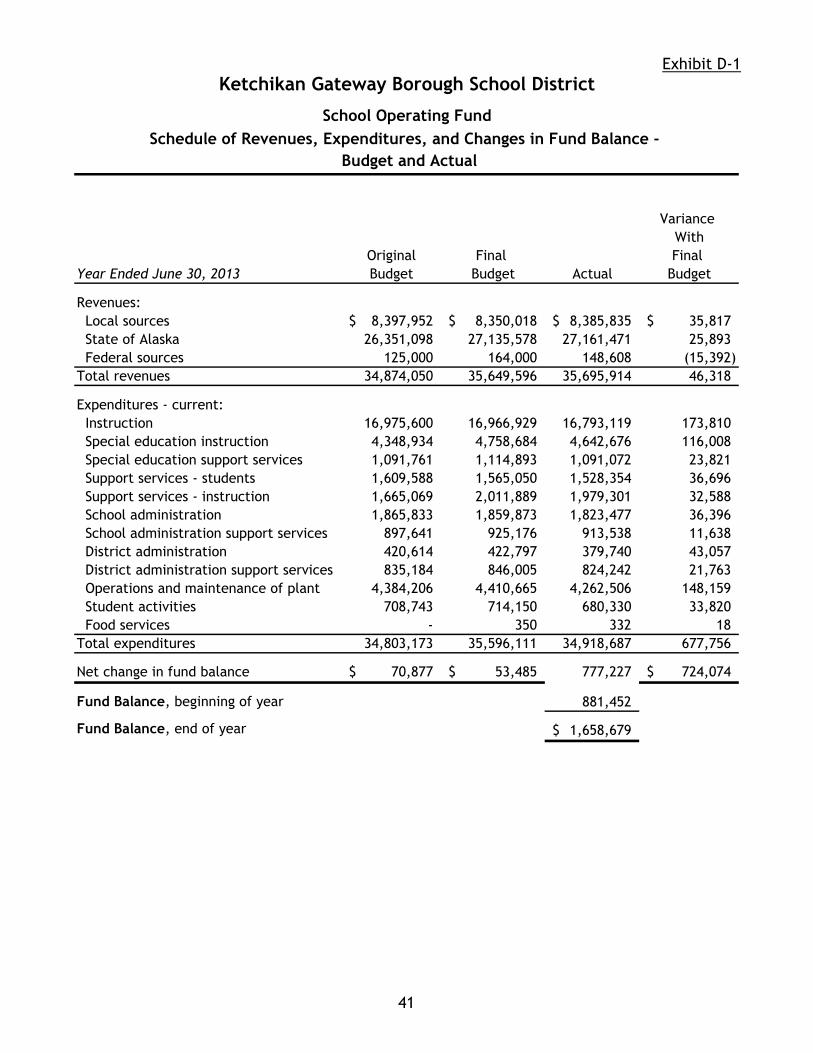

Exhibit D-1

Variance

With

Original Final Final

Year Ended June 30, 2013 Budget Budget Actual Budget

Revenues:

Local sources 8,397,952$ 8,350,018$ 8,385,835$ 35,817$

State of Alaska 26,351,098 27,135,578 27,161,471 25,893

Federal sources 125,000 164,000 148,608 (15,392)

Total revenues 34,874,050 35,649,596 35,695,914 46,318

Expenditures - current:

Instruction 16,975,600 16,966,929 16,793,119 173,810

Special education instruction 4,348,934 4,758,684 4,642,676 116,008

Special education support services 1,091,761 1,114,893 1,091,072 23,821

Support services - students 1,609,588 1,565,050 1,528,354 36,696

Support services - instruction 1,665,069 2,011,889 1,979,301 32,588

School administration 1,865,833 1,859,873 1,823,477 36,396

School administration support services 897,641 925,176 913,538 11,638

District administration 420,614 422,797 379,740 43,057

District administration support services 835,184 846,005 824,242 21,763

Operations and maintenance of plant 4,384,206 4,410,665 4,262,506 148,159

Student activities 708,743 714,150 680,330 33,820

Food services - 350 332 18

Total expenditures 34,803,173 35,596,111 34,918,687 677,756

Net change in fund balance 70,877$ 53,485$ 777,227 724,074$

Fund Balance, beginning of year 881,452

Fund Balance, end of year 1,658,679$

School Operating Fund

Schedule of Revenues, Expenditures, and Changes in Fund Balance -

Budget and Actual

Ketchikan Gateway Borough School District

41

Exhibit D-2

Variance

Original Final With

Year Ended June 30, 2013 Budget Budget Actual Budget

Revenues -

State of Alaska 1,602,456$ 1,602,456$ 1,576,239$ (26,217)$

Total revenues 1,602,456 1,602,456 1,576,239 (26,217)

Expenditures - current -

Student transportation 1,602,456 1,602,456 1,488,486 113,970

Total expenditures 1,602,456 1,602,456 1,488,486 113,970

Net change in fund balance -$ -$ 87,753 87,753$

Fund Balance, beginning of year 248,137

Fund Balance, end of year 335,890$

Ketchikan Gateway Borough School District

Student Transportation Special Revenue Fund

Schedule of Revenues, Expenditures and Changes in Fund Balance -

Budget and Actual

42

43

Supplementary Information

Exhibit E-1

Final

Budgeted

Year Ended June 30, 2013 Amounts Actual Variance

Revenues:

Local sources:

Borough appropriation 8,239,518$ 8,239,518$ -$

Earnings on investment - 62 (62)

E-Rate revenues 60,000 53,847 6,153

Other local revenues 50,500 92,408 (41,908)

Total local sources 8,350,018 8,385,835 (35,817)

State of Alaska:

Foundation program 20,624,228 20,772,323 (148,095)

On behalf TRS revenue 5,353,723 5,197,183 156,540

On behalf PERS revenue 743,905 750,620 (6,715)

SB 160 revenue 413,722 441,345 (27,623)

Total State of Alaska 27,135,578 27,161,471 (25,893)

Federal sources - medicaid 164,000 148,608 15,392

Total revenues 35,649,596 35,695,914 (46,318)

Expenditures:

Instruction:

Certificated salaries 8,634,581 8,633,102 1,479

Non-certificated salaries 578,133 585,071 (6,938)

Employee benefits 6,710,020 6,608,420 101,600

Professional and technical services 7,476 4,658 2,818

Staff travel 15,600 13,131 2,469

Student travel 5,100 8,485 (3,385)

Utilities 40 39 1

Other purchased services 82,580 77,287 5,293

Supplies, materials and media 913,299 846,026 67,273

Equipment 20,000 16,820 3,180

Other expenditures 100 80 20

Total instruction 16,966,929 16,793,119 173,810

School Operating Fund

Schedule of Revenues, Expenditures, and Changes in Fund Balance -

Budget and Actual

Ketchikan Gateway Borough School District

44

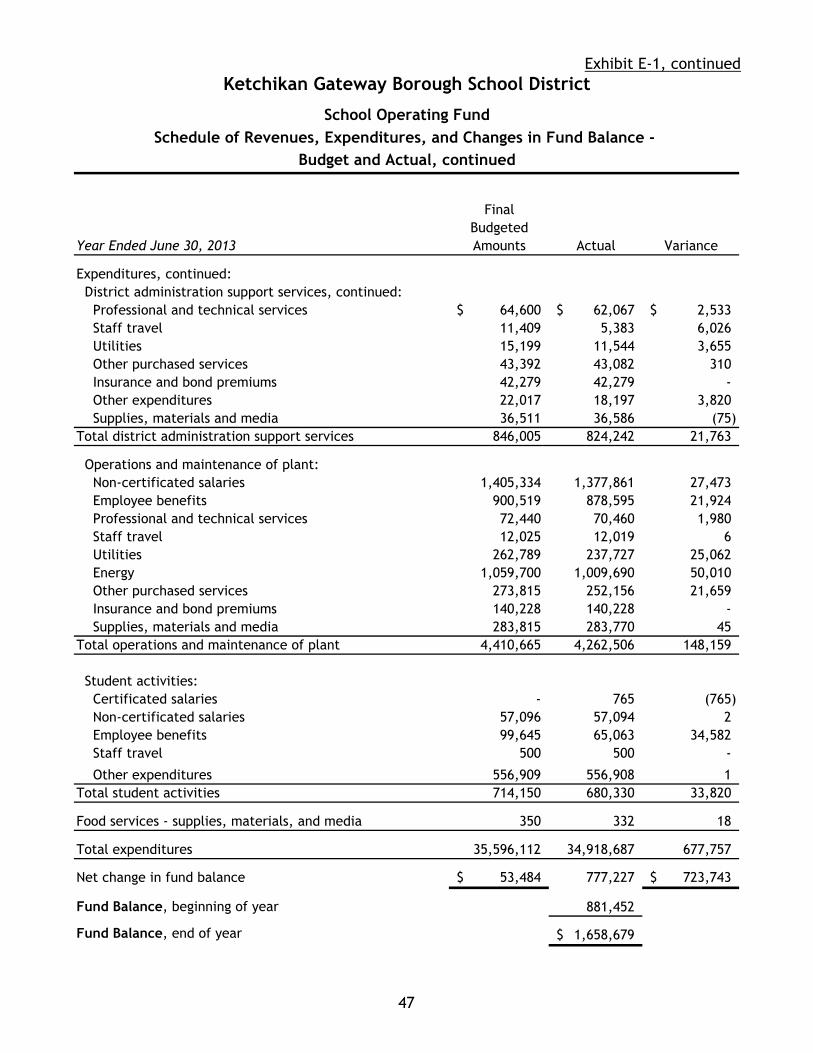

Exhibit E-1, continued

Final

Budgeted

Year Ended June 30, 2013 Amounts Actual Variance

Expenditures, continued:

Special education instruction:

Certificated salaries 1,458,991$ 1,393,017$ 65,974$

Non-certificated salaries 1,216,411 1,217,917 (1,506)

Employee benefits 1,915,174 1,865,102 50,072

Professional and technical services 53,131 53,098 33

Staff travel 1,800 1,715 85

Supplies, materials and media 25,052 23,730 1,322

Other expenditures 88,125 88,097 28

Total special education instruction 4,758,684 4,642,676 116,008

Special education support services - students:

Certificated salaries 597,825 597,837 (12)

Non-certificated salaries 38,404 37,416 988

Employee benefits 464,213 449,923 14,290

Staff travel 2,100 2,100 -

Utilities 5,024 1,961 3,063

Other purchased services 100 95 5

Supplies, materials and media 7,227 1,740 5,487

Total special education support services - students 1,114,893 1,091,072 23,821

Support services - students:

Certificated salaries 364,029 363,657 372

Non-certificated salaries 293,178 264,207 28,971

Employee benefits 476,417 468,635 7,782