Scotia Asian FX Strategy Update

2

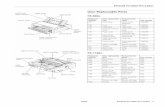

Sacha Tihanyi Senior Currency Strategist +852 2861-4770 [email protected] GLOBAL FX STRATEGY Scoa Asian FX Update Thursday, September 11, 2014 EM FX AND USD/ASIA DIRECTION CONSISTENT WITH OUR VIEWS • Trading paerns and recoupling in EM currencies over the past few sessions is highly suggesve of what is to come. • Weaker Asian VX emanates from worries over hawkish shiſt in Fed guidance, and rising US rates volality. • We maintain our structural view for upwards pressure on USD/Asia, to be driven Despite the stabilizaon in USD strength today, the trading paerns of the past few sessions have been very suggesve of the key structural theme relevant for Asian FX that informs our longer term forecasts as we move further away from the summer and into the end of the year. Over the past four sessions we’ve see general EM FX under a reasonable amount of pressure, with EM vol finally picking up, though sll nowhere in line with the relave increase in G7 vol. EM Asian vol, typically a laggard compared to overall EM vol this year, has also made an equivalent move higher (see chart), in line with increased US rates volality, a key metric we have pointed out in the past as what to watch for an indicaon of a turn in the suppressed vol environment. A pickup in rates volality is reflecve of the ‘pricing-in’ of increased risk that the Fed is shiſting more hawkish, a key factor in our view on USD/Asia. Scanning key correlave metrics, besides US rates volality (which rates opon volality indices are showing a trend pickup), the EM currency complex that took it on the chin so heavily last year is also seeing significant pressure. ZAR and BRL are down over 2% in the past five sessions, while TRY has fallen 1.7%. Asia has fared beer but is sll showing tell-tale signs of pressure that global macro-financial condions are turning inhospitable. KRW and INR have shed nearly 1% over the same me period, and both of these currencies as well as IDR and PHP are showing daily trading paerns much like those in BRL, TRY and ZAR. This is consistent with our direconal view towards the end of the year. The driver of the move, which has come despite weaker US nonfarm data last week, remains concern over the potenal change in signals coming from the Federal Reserve. This has been driven by the San Francisco Fed paper we noted earlier this week, as well as a couple of stories in major financial press outlets that have suggested that the Fed is likely to alter its state- ment to provide greater guidance and clarity on Fed Funds. This is an element we had suggested in recent months that would be required, given the improved economic data and the complete lack of guidance provided by Chair Yellen at the Jackson Hole conference. Indeed if anything, Chair Yellen’s address increased uncertainty by suggesng that essenally every eco- nomic indicator is imperfect insofar as it informs potenal Fed policy decisions (there is truth to this of course). This increases the event risk at the upcoming FOMC meeng next week, though as with all market posioning on the pro- spect of increased risk, it also suggests that should the FOMC not put in place a significant change in messaging, markets could unwind current posioning on the assumpon that Chair Yellen’s and the more dovish members of the FOMC remain in control of general consensus. This looks less likely at the moment (thus market posioning is jusfied) as guidance will need to ghten up in the not too distance future, if not at the next meeng. While we may retrace to some degree the move of recent sessions, we are confident that the medium to longer term direconal risk implied by the moves is correct. 6.0 6.5 7.0 7.5 8.0 8.5 9.0 87.00 87.50 88.00 88.50 89.00 89.50 Jan-14 Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Scotia USD/Asia ex-JPN Index EM Asia FX 1yr Vol Source: Bloomberg, Scoa FX Strategy EM FX VOLATILITY FINALLY KICKING OFF

-

Upload

brattanyu4171 -

Category

Documents

-

view

6 -

download

4

description

Scotia Asian FX Strategy Update

Transcript of Scotia Asian FX Strategy Update

Sacha Tihanyi Senior Currency Strategist +852 2861-4770 [email protected]

GLOBAL FX STRATEGY

Scotia Asian FX Update Thursday, September 11, 2014

EM FX AND USD/ASIA DIRECTION CONSISTENT WITH OUR VIEWS • Trading patterns and recoupling in EM currencies over the past few sessions is highly suggestive of what is to come. • Weaker Asian VX emanates from worries over hawkish shift in Fed guidance, and rising US rates volatility. • We maintain our structural view for upwards pressure on USD/Asia, to be driven Despite the stabilization in USD strength today, the trading patterns of the past few sessions have been very suggestive of the key structural theme relevant for Asian FX that informs our longer term forecasts as we move further away from the summer and into the end of the year. Over the past four sessions we’ve see general EM FX under a reasonable amount of pressure, with EM vol finally picking up, though still nowhere in line with the relative increase in G7 vol. EM Asian vol, typically a laggard compared to overall EM vol this year, has also made an equivalent move higher (see chart), in line with increased US rates volatility, a key metric we have pointed out in the past as what to watch for an indication of a turn in the suppressed vol environment. A pickup in rates volatility is reflective of the ‘pricing-in’ of increased risk that the Fed is shifting more hawkish, a key factor in our view on USD/Asia. Scanning key correlative metrics, besides US rates volatility (which rates option volatility indices are showing a trend pickup), the EM currency complex that took it on the chin so heavily last year is also seeing significant pressure. ZAR and BRL are down over 2% in the past five sessions, while TRY has fallen 1.7%. Asia has fared better but is still showing tell-tale signs of pressure that global macro-financial conditions are turning inhospitable. KRW and INR have shed nearly 1% over the same time period, and both of these currencies as well as IDR and PHP are showing daily trading patterns much like those in BRL, TRY and ZAR. This is consistent with our directional view towards the end of the year. The driver of the move, which has come despite weaker US nonfarm data last week, remains concern over the potential change in signals coming from the Federal Reserve. This has been driven by the San Francisco Fed paper we noted earlier this week, as well as a couple of stories in major financial press outlets that have suggested that the Fed is likely to alter its state-ment to provide greater guidance and clarity on Fed Funds. This is an element we had suggested in recent months that would be required, given the improved economic data and the complete lack of guidance provided by Chair Yellen at the Jackson Hole conference. Indeed if anything, Chair Yellen’s address increased uncertainty by suggesting that essentially every eco-nomic indicator is imperfect insofar as it informs potential Fed policy decisions (there is truth to this of course). This increases the event risk at the upcoming FOMC meeting next week, though as with all market positioning on the pro-spect of increased risk, it also suggests that should the FOMC not put in place a significant change in messaging, markets could unwind current positioning on the assumption that Chair Yellen’s and the more dovish members of the FOMC remain in control of general consensus. This looks less likely at the moment (thus market positioning is justified) as guidance will need to tighten up in the not too distance future, if not at the next meeting. While we may retrace to some degree the move of recent sessions, we are confident that the medium to longer term directional risk implied by the moves is correct.

6.0

6.5

7.0

7.5

8.0

8.5

9.0

87.00

87.50

88.00

88.50

89.00

89.50

Jan

-14

Jan

-14

Feb

-14

Ma

r-1

4

Ap

r-1

4

Ma

y-1

4

Jun

-14

Jul-

14

Au

g-1

4

Scotia USD/Asia ex-JPN Index

EM Asia FX 1yr Vol

Source: Bloomberg, Scotia FX Strategy

EM FX VOLATILITY FINALLY KICKING OFF

2

Global FX Strategy Thursday, September 11, 2014

IMPORTANT NOTICE and DISCLAIMER:

This publication has been prepared by The Bank of Nova Scotia (Scotiabank) for informational and marketing purposes only. Opinions, estimates and projections contained

herein are our own as of the date hereof and are subject to change without notice. The information and opinions contained herein have been compiled or arrived at from sources believed reliable, but no representation or warranty, express or implied, is made as to their accuracy or completeness and neither the information nor the forecast shall be taken as

a representation for which Scotiabank, its affiliates or any of their employees incur any responsibility. Neither Scotiabank nor its affiliates accept any liability whatsoever for any

loss arising from any use of this information. This publication is not, and is not constructed as, an offer to sell or solicitation of any offer to buy any of the currencies referred to herein, nor shall this publication be construed as an opinion as to whether you should enter into any swap or trading strategy involving a swap or any other transaction. The gen-

eral transaction, financial, educational and market information contained herein is not intended to be, and does not constitute, a recommendation of a swap or trading strategy

involving a swap within the meaning of U.S. Commodity Futures Trading Commission Regulation 23.434 and Appendix A thereto. This material is not intended to be individu-ally tailored to your needs or characteristics and should not be viewed as a “call to action” or suggestion that you enter into a swap or trading strategy involving a swap or any

other transaction. You should note that the manner in which you implement any of the strategies set out in this publication may expose you to significant risk and you should

carefully consider your ability to bear such risks through consultation with your own independent financial, legal, accounting, tax and other professional advisors. Scotiabank, its affiliates and/or their respective officers, directors or employees may from time to time take positions in the currencies mentioned herein as principal or agent, and may have

received remuneration as financial advisor and/or underwriter for certain of the corporations mentioned herein. Directors, officers or employees of Scotiabank and its affiliates

may serve as directors of corporations referred to herein. All Scotiabank products and services are subject to the terms of applicable agreements and local regulations. This pub-lication and all information, opinions and conclusions contained in it are protected by copyright. This information may not be reproduced in whole or in part, or referred to in any

manner whatsoever nor may the information, opinions and conclusions contained in it be referred to without the prior express written consent of Scotiabank.

™Trademark of The Bank of Nova Scotia. Used under license, where applicable. Scotiabank, together with “Global Banking and Markets”, is a marketing name for the global

corporate and investment banking and capital markets businesses of The Bank of Nova Scotia and certain of its affiliates in the countries where they operate, all members of the

Scotiabank group and authorized users of the mark. The Bank of Nova Scotia is incorporated in Canada with limited liability and is authorised and regulated by the Office of the Superintendent of Financial Institutions Canada. The Bank of Nova Scotia and Scotiabank Europe plc are authorised by the UK Prudential Regulation Authority. The Bank of

Nova Scotia is subject to regulation by the UK Financial Conduct Authority and limited regulation by the UK Prudential Regulation Authority. Scotiabank Europe plc is author-

ised by the UK Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and the UK Prudential Regulation Authority. Details about the extent of The Bank of Nova Scotia's regulation by the UK Prudential Regulation Authority are available on request. Scotiabank Inverlat, S.A., Scotia Inverlat Casa de Bolsa, S.A. de C.V.,

and Scotia Inverlat Derivados, S.A. de C.V., are each authorized and regulated by the Mexican financial authorities.Not all products and services are offered in all jurisdic-tions. Services described are available in jurisdictions where permitted by law.

GLOBAL FX STRATEGY CONTACTS THE MAJORS & PRIMARY CURRENCIES Camilla Sutton CFA, CMT Chief Currency Strategist 416-866-5470 [email protected] Eric Theoret CFA, CMT Currency Strategist 416-863-7030 [email protected] LATAM CURRENCIES Eduardo Suarez Senior Currency Strategist 416-945-4538 [email protected] ASIAN CURRENCIES Sacha Tihanyi Senior Currency Strategist 852-6117-6070 [email protected]

Should you wish to be added to anyone of our three distribution lists, please reach out to one of the above authors.