Scientex 3Q15 BriefingSlides Final 150629 › web › img › investor › Q2_FY2015_2.pdf ·...

19

Powered by Twin Engines Corporate Presentation 9M15 Corporate Update & Financial Results IR Adviser (Company No.: 7867-P)

Transcript of Scientex 3Q15 BriefingSlides Final 150629 › web › img › investor › Q2_FY2015_2.pdf ·...

Po

were

d b

y T

win

En

gin

es

Corporate Presentation9M15 Corporate Update & Financial Results

IR Adviser

(Company No.: 7867-P)

2

Po

were

d b

y T

win

En

gin

es

CONTENTS

• Operations Review & Growth Plans

• 9M15 Financial Review

• Investment Merits

Po

were

d b

y T

win

En

gin

es

OPERATIONS REVIEW

& GROWTH PLANS

4

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

2.8

3.2

4.1

4.3

4.6

12

.0

FY13 FY14 1Q15 2Q15 3Q15 FY17

7.3

8.9

9.0

9.3

10

.2

12

.3

FY13 FY14 1Q15 2Q15 3Q15 FY17

Operations Review: Manufacturing

Consumer packaging expansion plans progressing smoothly… on track to reach

approximately 25K MT sales tonnage per month by beginning FY2017

Operations Review

Average monthly sales tonnage

(MT ‘000)

Products:

• Base film

• Functional films

Prod. Output: 48,000 MT p.a.Location: Rawang

PE FilmPE Film

Prod. Output: 6,000 MT p.a.Location: Rawang

BOPP

Film

BOPP

Film

Output: 6,000 MT p.a.Location: Shah Alam & Indonesia

AdhesiveAdhesive

Consumer PackagingConsumer Packaging

Prod. Output: 120,000 MT p.a.Location: Pulau Indah, Klang

Stretch

Film

Stretch

Film

Prod. Output: 18,000 MT p.a.Location: Melaka

PP

Strapping

Band

PP

Strapping

Band

Prod. Output: 10,000 MT p.a.Location: Vietnam

RaffiaRaffia

Industrial PackagingIndustrial Packaging

10.1 12.1 13.1 13.6 25.0

Industrial Packaging

14.8

Consumer Packaging

5

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

Industrial

60.1%

Consumer

39.9%

3Q15 Manufacturing Revenue

RM318.8 mil

Operations Review: Manufacturing

Revenue growth driven by consumer packaging segment on larger capacity and

clientele… industrial film revenue slightly lower due to weaker crude oil prices

Operations Review

� Industrial Packaging

� 3Q15 revenue declined 6.4% yoy to RM191.6 mil due to

lower selling prices in line with lower crude oil prices

� Overall sales tonnage rose about 12% from FY2014 average

on higher export demand for stretch film

� Consumer Packaging

� 3Q15 revenue rose 13.0% yoy to RM127.1 mil mainly due to

enlarged PE film production capacity and larger clientele

� PE film production capacity expanded from 24,000 MT p.a.

to 48,000 MT p.a. in end-2014

� Commenced production of 9-layer barrier film in end-2014

Industrial

60.3%

Consumer

39.7%

9M15 Manufacturing Revenue

RM966.1 mil

-6.4%

yoy

+13.0%

yoy

-0.7%

yoy

+24.5%

yoy

6

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

Growth Plans: Manufacturing

On track to become the largest blown film manufacturer in Malaysia by 2016…

embarking on vertical expansion in consumer packaging

Growth Strategies

30,000MT

Per Annum

24,000 MT PE

6,000 MT BOPP

120,000MT

Per Annum

48,000 MT PE

60,000 MT BOPP

12,000 MT CPP

Completed

in end-2014

2014 2016

Consumer packaging expansion plan

To be completed

in end-2015/2016

� New 10-color printing machine to be installed in July

2015

� To increase sales of more value-added production

� Construction of new CPP film plant to be completed in

July 2015

� On track for commercial run by end-2015 with

total capacity of 12,000 MT p.a

� To complement PE and BOPP businesses and

leverage on existing clientele in Malaysia and

South East Asia

� Commenced BOPP plant construction in February 2015

� Commercial run targeted to commence in mid-

2016

� BOPP production to be increased to 60,000 MT

p.a. from 6,000 MT p.a. currently

� Further expansion of PE film from 48,000 MT p.a. to

60,000 MT p.a. targeted for completion in mid-2016

CPP plant in Melaka, slated for

completion in July 2015

Site progress of BOPP plant in

Pulau Indah

7

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

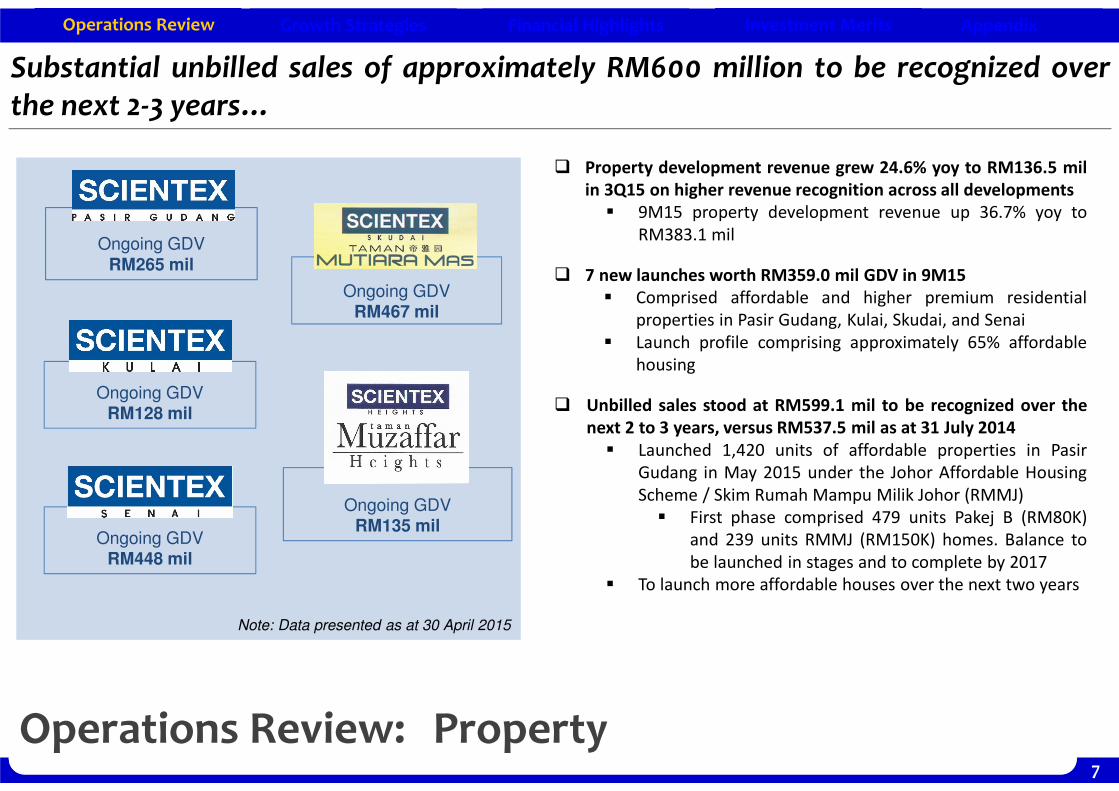

Operations Review: Property

Substantial unbilled sales of approximately RM600 million to be recognized over

the next 2-3 years…

Operations Review

Ongoing GDV

RM265 mil

Ongoing GDVRM467 mil

� Property development revenue grew 24.6% yoy to RM136.5 mil

in 3Q15 on higher revenue recognition across all developments

� 9M15 property development revenue up 36.7% yoy to

RM383.1 mil

� 7 new launches worth RM359.0 mil GDV in 9M15

� Comprised affordable and higher premium residential

properties in Pasir Gudang, Kulai, Skudai, and Senai

� Launch profile comprising approximately 65% affordable

housing

� Unbilled sales stood at RM599.1 mil to be recognized over the

next 2 to 3 years, versus RM537.5 mil as at 31 July 2014

� Launched 1,420 units of affordable properties in Pasir

Gudang in May 2015 under the Johor Affordable Housing

Scheme / Skim Rumah Mampu Milik Johor (RMMJ)

� First phase comprised 479 units Pakej B (RM80K)

and 239 units RMMJ (RM150K) homes. Balance to

be launched in stages and to complete by 2017

� To launch more affordable houses over the next two years

Note: Data presented as at 30 April 2015

Ongoing GDVRM128 mil

Ongoing GDVRM135 mil

Ongoing GDVRM448 mil

8

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

Recent Developments: Property

Recently proposed acquisition of 326-acre land in Skudai… Group’s ongoing and

undeveloped landbank increases to 1,200 acres to last for 10 years

Operations Review

New lands

� On 29 June 2015, entered into agreements with Bukit

Gambir Company Sdn Bhd and Jayaplus Bakti Sdn Bhd to

acquire 326 acres of land in Pulai for RM218.97 million

� Located 33 km from Johor Bahru City Centre, 25 km from

MY-SG Second Link Customs Checkpoint, and 5 km from

proposed Pulai Jaya Interchange Exit to the Second Link

� To contribute towards long term development profile

and boosts ongoing and undeveloped landbank to

approx. 1200 acres from 870 acres currently

� To benefit from established branding of existing 150 acre

Taman Mutiara Mas development, good road connectivity

and proximity to various mature townships such as Taman

Pulai Indah and Bandar Baru Kangkar Pulai

� To be financed by approximately 80% bank borrowings

and 20% cash

� Proposed acquisition subject to approvals by shareholders

at upcoming Extraordinary General Meeting and other

relevant authorities

Po

were

d b

y T

win

En

gin

es

9M15 FINANCIAL REVIEW

10

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

20

.6

20

.2

19

.7

23

.4

24

.9

25

.6

29

.5

27

.1

26

.0

33

.9

36

.3

48

.8

30

.3

36

.1

43

.0

5.2 9

.7 3.1

Quarterly PATMI (RM ‘mil)

Forex differences

Charting commendable growth from both core segments… margins recovering

from 2Q15 from forex losses as USD loans pared down significantly

3Q15 Income Statement Summary

Financial Highlights2

13

.8

21

4.5

22

6.8

22

6.0

24

1.6

27

1.1

34

5.1

37

1.2

36

4.8

38

3.5

42

6.8

41

5.4

43

1.1

46

2.9

45

5.3

Quarterly Revenue (RM ‘mil)

26

.3

25

.8

25

.5

29

.5

31

.3

33

.2

38

.2

40

.2

32

.9

44

.4

48

.1

56

.0

40

.2

47

.3

56

.5

5.2 9

.7 3.1

Quarterly PBT (RM ‘mil)Forex differences

3Q15 3Q14 Change RM'mil 9M15 9M14 Change Remarks

455.3 426.8 6.7% Revenue 1,349.2 1,175.1 14.8%Driven by higher property development and

consumer packaging sa les

69.4 58.9 17.8% EBITDA 180.3 162.9 10.7%

15.2% 13.8% 1.4 pt EBITDA margin 13.4% 13.9% (0.5 pt)

56.5 48.1 17.5% PBT 144.0 130.3 10.5%

12.4% 11.3% 1.1 pt PBT margin 10.7% 11.1% (0.4 pt)

43.0 36.3 18.2% PATMI 109.3 99.6 9.7%

9.4% 8.5% 0.9 pt Net margin 8.1% 8.5% (0.4 pt)

19.02 16.43 15.8% Basic EPS (sen) 48.69 45.04 8.1%

Profi t increased largely in l ine wi th higher topl ine

Margins s l ightly dampened due to forex losses

incurred in 1H15; vastly improved in 3Q15 compared

to 2Q15 as USD loans were pared down s ignifi cantly

In l ine with above

11

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

41.9%

58.1%

9M15 Group EBITDA*: RM198.3 mil

Property segment leading growth in 9M15… manufacturing segment profitability

benefitting from higher contribution from consumer packaging sales

Revenue & EBITDA Segmentation

Financial Highlights

71.6%

28.4%

9M15 Group Revenue: RM1,349.2 mil

Manufacturing Property

76.2%

23.8%

9M14 Group Revenue: RM1,175.1 mil

Manufacturing Property

+36.7%

yoy

+8.0%

yoy

47.9%52.1%

9M14 Group EBITDA*: RM163.4 mil

35.4%

yoy5.6%

yoy

*EBITDA presented excludes gains/losses from foreign exchange

12

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

483 635 763587 583

153

284430

308 383

2012 2013 2014 9M14 9M15

RM’mil

Manufacturing Revenue (by Segment)

Industrial Packaging Consumer Packaging

Financial Review: Manufacturing

Manufacturing growth mainly driven by expanded consumer packaging division…

Financial Highlights

58

77

10

7

78

83

9.1% 8.4% 9.0% 8.8% 8.6%

2012 2013 2014 9M14 9M15

RM’milEBITDA & EBITDA Margin

EBITDA EBITDA Margin

63

7

91

9

1,1

92

89

5

96

6

11.0% 11.1%9.8% 10.0% 9.9%

2012 2013 2014 9M14 9M15

RM’mil

Manufacturing Revenue & Gross Margin

Revenue Gross Margin

9M15 EBITDA growth in

line with expanded sales,

margin remains stable

9M15 EBITDA growth in

line with expanded sales,

margin remains stable

9M15 manufacturing

revenue primarily driven

by consumer packaging

growth; GP margin

remains stable

9M15 manufacturing

revenue primarily driven

by consumer packaging

growth; GP margin

remains stable

Industrial packaging revenue declined

slightly (-0.7%) due to lower crude oil

prices, but overall sales tonnage higher

on steady growth in industrial demand

Industrial packaging revenue declined

slightly (-0.7%) due to lower crude oil

prices, but overall sales tonnage higher

on steady growth in industrial demand

Higher consumer packaging revenue

+24.5% with expanded PE film capacity

and clientele

Higher consumer packaging revenue

+24.5% with expanded PE film capacity

and clientele

13

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

15

0

21

9

24

5

31

0

39

8

28

0 38

337.8%42.6% 44.2% 47.0% 44.1% 44.4%

41.0%

2010 2011 2012 2013 2014 9M14 9M15

RM’milRevenue & Gross Margin

Revenue Gross Margin

34

63

73

10

0

12

2

85

11

5

22.8%

28.8% 29.8%32.3% 30.7% 30.4% 30.1%

2010 2011 2012 2013 2014 9M14 9M15

RM’milEBITDA & EBITDA Margin

EBITDA EBITDA Margin

Financial Review: Property Development

Financial Highlights

Property segment continues commendable performance on sturdy demand for

affordable properties in Johor… also enhanced by well-priced premium properties

Steady demand for affordable housing,

particularly in Pasir Gudang and Senai, as well as

well-priced higher-premium properties in Skudai

Steady demand for affordable housing,

particularly in Pasir Gudang and Senai, as well as

well-priced higher-premium properties in Skudai

14

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

Net gearing at comfortable level even as capacity expansions are ongoing…larger

asset base reflecting recent landbanking and expanded manufacturing operations

1 Based on share capital of 225.9 mil shares after deducting treasury shares of 4.1 mil shares

Financial Highlights

Balance Sheet (Highlights)

As at As at

30.4.2015 31.7.2014

Property, Plant & Equipment 568,252 552,100 In l ine wi th consumer packaging expans ion

Investment Property & Other Investments 11,508 9,571

Land Held & Property Development Costs 394,972 365,019 Due to increased property development activi ties

Investment in Jointly Control led Enti ty &

Associated Company39,536 37,465

Inventories 85,945 108,998

Trade & Other Receivables 325,235 243,459 In l ine with increase in revenue

Cash & Bank Ba lances 63,491 83,766

TOTAL ASSETS 1,488,939 1,400,378

Trade & Other Payables 255,643 254,441

Borrowings (ST + LT) 282,665 340,420

Tax & Deferred Tax 36,146 35,059

Shareholders ’ Equi ty 851,566 712,718 Due to higher reta ined earnings and share premium account

Minority Interest 43,697 22,705Due to equity parti cipation of Futamura Chemica l Co., Ltd into Scientex

Great Wal l Sdn Bhd

Net Tangible Assets / Sha re (RM) 1 3.77 3.22

Net Gearing 0.26x 0.36x On paring down of borrowings due to s trong cashflow

Balance Sheet (RM ‘000) Remarks

15

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

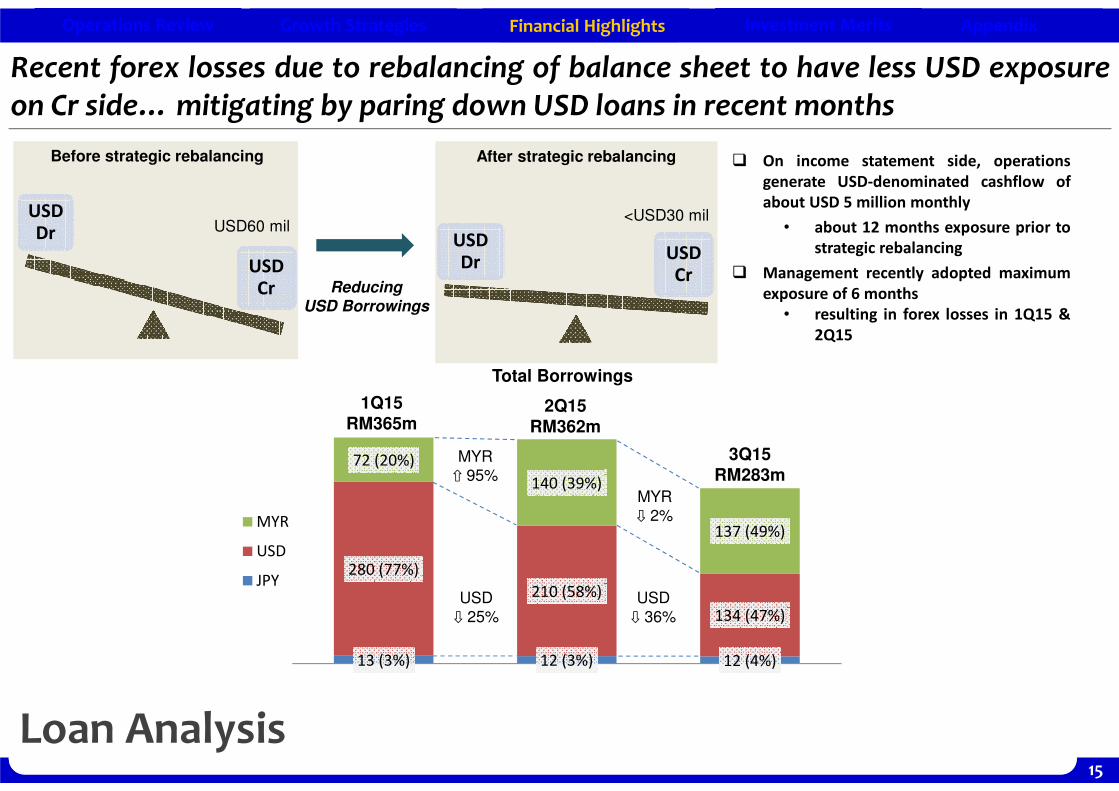

USD

DrUSD

Cr

USD

Dr

USD

Cr

Recent forex losses due to rebalancing of balance sheet to have less USD exposure

on Cr side…mitigating by paring down USD loans in recent months

Financial Highlights

Loan Analysis

� On income statement side, operations

generate USD-denominated cashflow of

about USD 5 million monthly

• about 12 months exposure prior to

strategic rebalancing

� Management recently adopted maximum

exposure of 6 months

• resulting in forex losses in 1Q15 &

2Q15

Before strategic rebalancing

USD60 mil

After strategic rebalancing

<USD30 mil

Reducing

USD Borrowings

13 (3%) 12 (3%) 12 (4%)

280 (77%)

210 (58%)

134 (47%)

72 (20%)

140 (39%)

137 (49%)MYR

USD

JPY

MYR

⇩ 2%

USD

⇩ 36%

USD

⇩ 25%

MYR

⇧ 95%

1Q15

RM365m2Q15

RM362m

3Q15

RM283m

Total Borrowings

Po

were

d b

y T

win

En

gin

es

INVESTMENT MERITS

17

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix

Investment Merits

A high-growth proposition all-round... attractive proxy to the burgeoning packaging sector

and Southern Malaysia property market

Investment Merits

MANUFACTURING

• Top 3 stretch film producer in the world

• Consumer packaging segment facilitates

entry into burgeoning F&B and FMCG sectors

• Further integration and expansion initiatives

position Group to cater to larger regional

clientele and enhance competitiveness

PROPERTY DEVELOPMENT

• Reputable developer in the southern states

of Johor and Melaka

• Current projects of RM1.4 bil

• Pipeline GDV of RM4.0 bil on existing

landbank to sustain another 8 years

• Future projects displaying higher GDV/acre

• Strong fundamentals with strong upside to profit and margin expansion

• Dividend policy of minimum 30% payout

� 31.7% dividend payout in FY2014

• Valuations to be compressed with foreseeable earnings boost

• Trading at trailing 12-month PE of 9.8x and EV/EBITDA of 7.4x (as at 26 June 2015)

18

Operations Review Growth Strategies Financial Highlights Investment Merits Appendix2

.7

2.7

2.7

4.5

8.1

14

.2

4.2

17

.2

10

.8

19

.4

25

.8

30

.1

35

.4

47

.1

20

.3

22

.1

49.2% 48.0%

74.0%

26.6%

36.6%

49.8%

28.7%36.1%

28.8%32.1% 33.4% 35.9%

52.1%

31.7%

18.6%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 9M15

RM’mil Dividend History

Net Dividend Payout Special Dividend Payout Ratio

Group has dividend policy of minimum 30% net profit payout…

Dividend History

� FY2014 Dividends (Total dividend of 21 sen):

• Paid interim dividend of 8 sen per share on 8 August 2014

• Paid final dividend of 13 sen per share on 6 February 2015

� FY2015 Dividends :

• Declared first interim dividend of 9 sen per share (Ex-date: 15 July 2015, payable: 7 August 2015)

Dividend Policy:

Minimum 30% of Net Profit(effective FY2011)

Investment Merits

FY14 Dividend Payout

RM47.1Million

FY14 Dividend Payout

RM47.1Million

Share Dividend

5.9

Po

were

d b

y T

win

En

gin

es

Thank You

Contacts:

Ms. Jocelyn Ng [email protected] T: 03-5519 1325

Ms. Julia Pong [email protected] T: 03-2711 1391

Question and Answer Session