Schantl Dissertation FINAL - unipub.uni-graz.at

103

Stefan Schantl The determinants of the firm coverage and earnings forecasting behavior of sell-side equity analysts Doctoral Thesis to be awarded the degree of Doctor of Social and Economic Sciences (Dr. rer.soc.oec.) at the University of Graz, Austria Name of first supervisor Institute of Accounting and Auditing, Prof. Dr. Ralf Ewert Name of second supervisor Institute of Accounting and Control, Prof. Dr. Dr.h.c Alfred Wagenhofer Graz, April 30, 2014

Transcript of Schantl Dissertation FINAL - unipub.uni-graz.at

Stefan Schantl

The determinants of the firm coverage and

earnings forecasting behavior of sell-side equity

analysts

Doctoral Thesis

to be awarded the degree of

Doctor of Social and Economic Sciences (Dr. rer.soc.oec.)

at the University of Graz, Austria

Name of first supervisor

Institute of Accounting and Auditing, Prof. Dr. Ralf Ewert

Name of second supervisor

Institute of Accounting and Control, Prof. Dr. Dr.h.c Alfred

Wagenhofer

Graz, April 30, 2014

Author´s Declaration

Unless otherwise indicated in the text or references, or acknowledged above, this thesis is

entirely the product of my own scholarly work. Any inaccuracies of fact or faults in reasoning

are my own and accordingly I take full responsibility. This thesis has not been submitted

either in whole or part, for a degree at this or any other university or institution. This is to

certify that the printed version is equivalent to the submitted electronic one.

g

Graz, April 30, 2014 (Stefan Schantl)

Acknowledgements

I am deeply indebted to my dissertation advisors Ralf Ewert and Alfred Wagenhofer for

introducing me to theoretical accounting research and for their unremitting support during my

endeavors exploring this, for me, new point of view. The numerous cutting edge lectures they

gave throughout the past years as well as their encouraging and constructive feedback on my

ongoing projects inspired (or better incentivized) me to continuously work on my economic

understanding and further my technical skills.

Special thanks go to Paul Fischer, who generously volunteered to be a doctoral thesis

committee member as well as Mirko Heinle and Ro Verrecchia for their perpetual coaching

during and after my stay at the University of Pennsylvania. I explored previously unimagined

perspectives about the economics behind accounting through the discussions with them.

Further, I very much enjoyed the interesting workshops and eye-opening discussions with

Brian Bushee, Chris Ittner, Wayne Guay, Luzi Hail, Thomas Hemmer, Bob Holthausen, Rick

Lambert, Wayne Landsman, and Cathy Schrand.

I moreover want to thank my fellow doctoral students Kristina Berger, Terrence Blackburne,

Anna Boisits, Björn Brand, Michael Carniol, Jacky Chau, Mike Chin, Marina Ebner, Thomas

Gaber, Christian Gross, Jessica Kim-Gina, Brigitte Klotz, Peter Krenn, Sebastian

Kronenberger, Sandra Kukec, Beatrice Michaeli, Konrad Lang, Tanja Sestanj Peric, Spencer

Pierce, Olivers Schinnerl, David Tsui, Dennis Völler, Katrin Weiskirchner-Merten, David

Windisch, Jason Xiao, and Hang Yu for their continuous help throughout my doctoral

studies, for helpful comments on my work and for fruitful and lively discussions and debates.

Financial support from the Doctoral Program in Accounting, Reporting, and Taxation

(DART) funded by the FWF Austrian Science Fund, from the Social and Economic Faculty

of the University of Graz, and from the Austrian state of Styria is much appreciated.

Last but not least I want to thank my parents Inge and Hubert and my friends Carsten,

Dominik, Eva, Florian, and Gernot for their incessant support which was crucial for the

completion of this thesis.

Thank you!

I

Table of Contents

1. Introduction 1

1.1. Methodology 2

1.2. Literature Review 2

1.2.1. The Determinants of Analyst Forecast Properties 4

Analyst Reputation and Accuracy 4

Trading Volume Generation and Overoptimism 5

Career Concerns and Herding 7

Investors’ and Employers’ Inference of Analysts’ Abilities 10

Analysts’ Endowment with Private vs. Public Fundamental Information 11

The Relevance of Non-Fundamental Information 14

1.2.2. The Causes and Consequences of Analyst Coverage Behavior 15

Analyst Information Acquisition Costs and Coverage Initiation 15

Consequences of Changes in Analyst Following 18

1.3. Contribution 20

1.3.1. Analysts’ Career Concerns, Forecast Biasing and Firm Coverage Selection 20

1.3.2. Analyst Information Acquisition and the Informativeness of Forecasts and

Managed Earnings 21

1.3.3. Discretionary Analyst Coverage and Capital Market Characteristics 21

1.4. Structure of the Dissertation 22

2. Analysts’ Career Concerns, Forecast Biasing and Firm Coverage Selection 23

2.1. Introduction 24

2.2. Economic Setting 27

2.3. Model Solution and Equilibrium 31

2.3.1. Analysts’ Forecasting Strategy in the Monopoly Case 31

2.3.2. Analysts’ Forecasting Strategy in the Duopoly Case 32

2.3.3. The Coverage Initiation Threshold 34

II

2.4. Analysts’ Career Concerns and Firm Coverage Selection 36

2.5. Empirical Implications 40

2.6. Conclusion 41

Appendix (Paper 1) 42

Proof of Proposition 1 42

Proof of Corollary 3 45

Proof of Corollary 4 46

Proof of Corollary 5 47

3. Analyst Information Acquisition and the Informativeness of Forecasts and Managed

Earnings 48

3.1. Introduction 49

3.2. Economic Setting 51

3.3. Model Solution and Equilibrium 53

3.4. Analyst Information Acquisition and the Informativeness of Managed Earnings 54

3.5. Conclusion 58

Appendix (Paper 2) 59

Proof of Proposition 1 59

Proof of Corollary 1 60

Proof of Corollary 2 61

4. Discretionary Analyst Coverage and Capital Market Characteristics 62

4.1. Introduction 63

4.2. Economic Setting 66

4.3. Model Solution and Equilibrium 71

4.4. Discretionary Analyst Coverage and Capital Market Characteristics 73

4.5. Extension: Discretionary Analyst Coverage and Market Liquidity 77

4.6. Conclusion 79

Appendix (Paper 3) 80

III

Proof of Proposition 1 80

Proof of Corollary 1 81

Proof of Corollary 2 82

Proof of Corollary 3 83

Proof of Proposition 2 83

Proof of Corollary 4 85

5. Discussion and Conclusion 87

Bibliography 91

Table of Figures

Figure 1: Prototypical Sequence of Decisions of an Equity Analyst 3

Figure 2: Sequence of Events (Paper 1) 28

Figure 3: Sequence of Events (Paper 2) 51

Figure 4: Sequence of Events (Paper 3) 67

Introduction

1

1. Introduction

Sell-side equity analysts are one of the primary information sources for stakeholders in

modern capital markets. Numerous empirical studies claim that reports, especially earnings

forecasts, provided by analysts are informative about the value of a firm (e.g., Givoly &

Lakonishok 1979, Lys & Sohn 1990, Frankel et al. 2006).1 By means of a time-series

regression on the decomposition of cumulative abnormal returns, Beyer et al. (2010) provide

evidence that almost one quarter of the financial information about a firm is disseminated by

equity analysts. Additionally, there is evidence showing that analysts not only provide new

information but also reiterate and reinterpret previously disclosed firm information (e.g.,

Asquith et al. 2005, Chen et al. 2010).2 This interpretation function also seems to matter for

shareholders: analysts who are more responsive to the information in an earnings

announcement and revise their forecasts shortly after the earnings disclosure help to reduce

the post-earnings announcement drift effect (Zhang 2008). Ayers & Freeman (2003), Gleason

& Lee (2003) and Piotroski & Roulstone (2004) present results showing that this effect is

triggered with a larger analyst following since this generally increases the pace of the pricing

process with respect to future earnings of a stock. Chang et al. (2006) and Bowen et al.

(2008) present evidence consistent with the argument that firms with greater analyst coverage

receive better financing contracts. Closely associated with the latter observation is the

evidence of Rajan & Servaes (1997) and James & Karceski (2006), who show that a larger

analyst following yields a more successful initial public offering. Additionally, Alfond &

Berger (1999) and Roulstone (2003) show that a larger analyst following yields an increased

liquidity of a firm’s stock. Altogether, it can be concluded that these empirical observations

yield a lowered cost of equity capital associated with larger analyst following. Furthermore,

firms seem to be aware of the benefits associated with analyst firm coverage since they are

even willing to pay for analyst services (Kirk 2011). It follows that the significance of

analysts in their different roles as information sources and information interpreters cannot be

overemphasized. However, besides the large attention of empiricists over the past twenty

years, the answer to the following question is yet to be found: What determines both analysts’

1 However, there is conflicting evidence on the informativeness of stock recommendations issued by sell-side

security analysts (e.g., Barber et al. 2001, Jegadeesh et al. 2004, Howe et al. 2009). Moreover, the information

role is not constant over time but depends crucially on the timing relative to firm disclosures (Francis et al.

2002, Ivkovic & Jegadeesh 2004, Chen et al. 2010). 2 The importance of information interpretation issues is pointed out by the theoretical contribution of Dutta &

Trueman (2002). They show that the assumption of an uncertain information interpretations leads to a non-

trivial voluntary disclosure strategy.

Introduction

2

forecasting and coverage behavior and how are observable patterns in their decisions

reconcilable to these incentives?

1.1. Methodology

Although the properties of financial analysts’ information as well as the consequences of

their work are empirically well-investigated, theoretical contributions that provide empirical

implications on the sources and consequences of analysts’ distinct incentives are still scarce.

The current cumulative doctoral thesis aims to fill some significant gaps in the theoretical

literature on analyst incentives and provides a number of novel empirical implications.

The advantages of the application of microeconomic models to increase our understanding of

the key determinants of analyst behavior compared to the widely used empirical method are

manifold. First and most importantly, it can be stated that the data availability on analysts’

behavior is still mediocre. This especially holds true for data on the decision of an analyst to

initiate or abandon firm coverage. A second advantage can be found with respect to potential

endogeneity issues which are inevitable with the use of empirical methods: As will be clear

throughout the dissertation, the interactions of analysts with others such as peer analysts,

investors or firm managers are determined by multiple, particularly complex relations and

economic forces. Theoretical models on the other hand enable us to isolate these forces and

ensure a pure analysis of the economics behind the interactions of analysts with other

economic agents.

1.2. Literature Review

In this chapter I provide a brief literature review of existing theoretical and empirical research

on analysts’ forecasting and firm coverage decisions.3 Kothari (2001), Ramnath et al. (2008)

and Beyer et al. (2010) also provide reviews on analyst research, but Kothari (2001)

exclusively summarizes the empirical research, whereas Beyer et al. (2010) impose a

structure which divides theoretical research from empirical evidence. Moreover, Ramnath et

al. (2008) provide only an incomplete discussion of theoretical research on the topic. In

contrast, the approach applied herein involves imposing a topical structure rather than a

methodological one. This approach enables me to reconcile theory and empirical evidence in

my discussion of the literature. Since the main chapters of this doctoral thesis apply formal

3 The focus of this thesis is on analyst forecasting and firm coverage. Consequently, it excludes other reports of

analysts such as price targets or stock recommendations.

Introduction

3

Analyst gathers

information for the

forecasting of

subsequent earnings

Analyst discloses

earnings forecast

Analyst manipulates

private information

signal and formulates

earnings forecast

Analyst observes

private information

signal and decides

whether to release it

Analyst decides

whether to start

collecting information

about a firm

Coverage Initiation Stage (Chapter 1.2.2.)

Forecast Reporting Stage (Chapter 1.2.1.)

t=1 t=2 t=3 t=4 t=5

theoretical modeling, this approach has the advantage of identifying several research issues of

high relevance that need further theoretical guidance.4

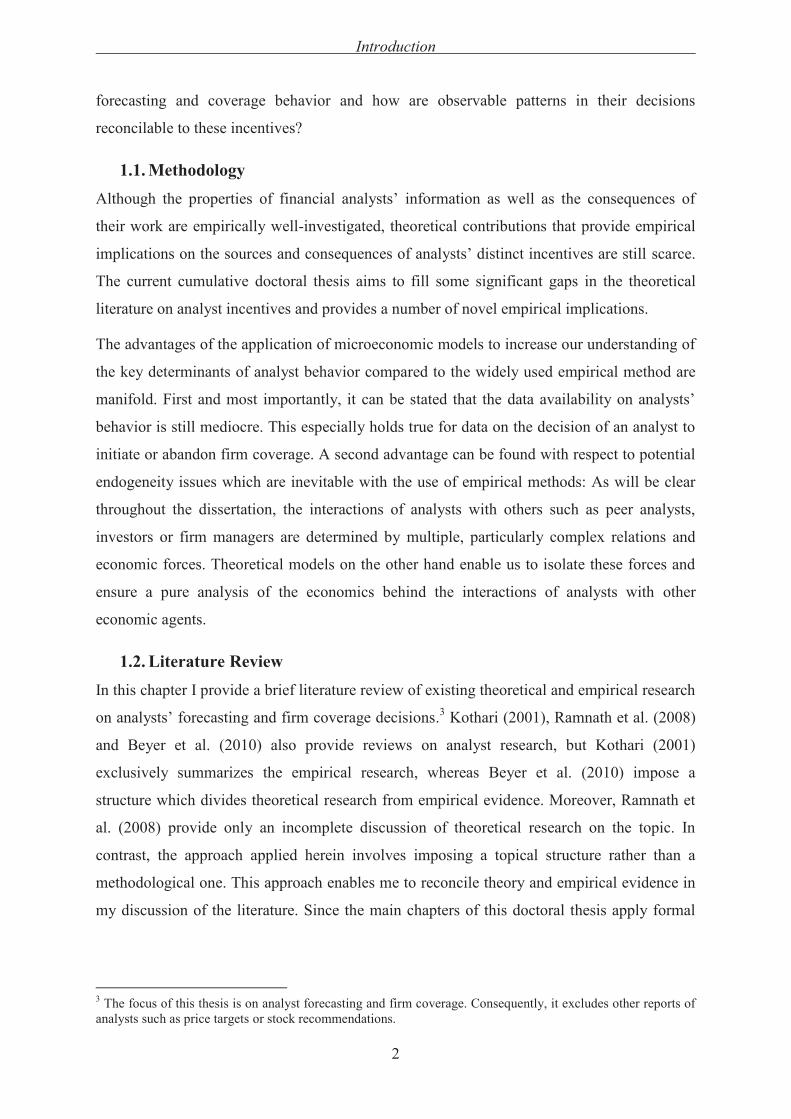

In order to add more structure to the literature review, Figure 1 depicts the prototypical

process of an analyst’s decisions.5 First, the analyst decides on whether to start collecting

information, which is subsequently carried out if this optimizes ex-ante his utility.6 After the

information acquisition comes the discretionary reporting stage ( ), in which the analyst

evaluates whether the disclosure of the obtained private information is beneficial for him.

This may happen in conjunction with the action in stage ( ), in which he decides on an

appropriate level of manipulation to complete the formulation of his forecast. In the last stage

he discloses his forecast to his clients.7

The literature review is structured in an inverse fashion and starts with the discussion of a

codetermination of analyst forecasts’ properties by distinct influential factors (i.e., particular

incentives, information endowment). In a second chapter the focus lies on the state of

research concerning analysts’ firm coverage initiation (or abandonment of coverage)

behavior. In addition, in the latter section a summary of the consequences of analyst firm

coverage for the firm is presented in order to provide a sufficiently broad perspective on the

current state of the art of the economic research on analysts.8

4 It shall be noted that for practical reasons the review will not be able to summarize all available contributions

on the topic. Instead, I focus on the most important contributions in the field, whereby the selection is naturally

driven by the author’s subjectivity. 5 For the sake of the readability of the dissertation I use male pronouns to refer to an individual equity analyst or

other stakeholders, although these are interchangeable with pronouns in the female form without any limitations. 6 In this stage he may use some proprietary information on which to base his decision (e.g., see Hayes 1998,

Fischer & Stocken 2010). 7 In further stages the analyst may obtain additional information and may decide whether or not to disclose a

revised version of his forecast. However, this decision can be seen as a repetition of all actions between

and . 8 The reason for the inverse structure is that the drivers behind analyst forecast properties are much better

investigated than those behind coverage initiation or abandonment. Thus, this approach gives the reader a much

better overview over the distinct factors that are influential in analysts’ decisions and enables me to highlight

gaps in the coverage literature.

Figure 1: Prototypical Sequence of Decisions of an Equity Analyst

Introduction

4

1.2.1. The Determinants of Analyst Forecast Properties

Analysts have a variety of objectives that they follow to optimize their overall utility.

However, I identify and subsequently discuss the following factors, which influence the

behavior of analysts with respect to their forecasting strategies: (i) analyst reputation and

accuracy, (ii) the trading volume generation objective and overoptimism, (iii) career concerns

and herding, (iv) investors’ and employers’ inference of analysts’ abilities, and analysts’

endowment with (v) fundamental and (vi) non-fundamental information.

Analyst Reputation and Accuracy

Reputation is assumed to be one of the main driving forces behind analysts’ behavior, which

is the reason why almost all of the discussed models incorporate it in their structure in one

way or another (e.g., Lim 2001, Beyer 2008, Beyer & Guttman 2011). Several empirical

studies proxy reputational concerns by the use of forecast accuracy, which is measured by the

ex-post absolute forecast error. This perspective is established by Stickel (1992), who shows

that members of the Institutional Investor All-American Research Team, a group of analysts

considered to be superior and who thus possess a very good reputation, deliver more accurate

earnings forecasts than non-members of this group.9 Additionally, he also documents a more

pronounced stock market reaction to All-American analyst forecasts.10

In line with the research of Stickel (1992), the reputation incentive is usually theoretically

modeled by assuming that an analyst minimizes either the expected quadratic (Lim 2001) or

absolute forecast error (Beyer 2008).11

Lim (2001) develops a model in which an analyst

chooses the bias of his earnings forecast. He shows that the forecast distortion is positive and

decreases with the predictability of earnings, which he subsequently confirms with an

archival analysis. Beyer (2008) establishes a framework that considers the endogeneity issue

involved in this process: According to existing evidence, managers manipulate earnings such

that the previously published forecast is met or bet. This is rewarded with a market premium

9 Stickel (1992) reasons that there may be a positive relationship between compensation and forecasting

performance under the assumption that All-Star recognition is associated with higher compensation. This

hypothesis is confirmed by Groysberg et al. (2011) by means of internal brokerage house data. 10

Another well-known pattern associated with forecasting accuracy is consistent with experience learning:

Analysts’ forecasting performance measured by ex-post absolute forecast errors increases over time. Notable

empirical contributions in this field of research are Mikhail et al. (1997, 2003), Clement (1999), Jacob et al.

(1999) and Clement et al. (2007). 11

In the absence of other objectives (e.g., the stimulation of trading), these two functions yield the same

solution. However, Basu & Markov (2004) provide empirical evidence pointing to a higher appropriateness of

the absolute rather than the quadratic forecast error loss function, which indicates that other objectives are also

relevant for the forecasting behavior of an equity analyst.

Introduction

5

(Kasznik & McNichols 2002, Matsumoto 2002, Bhojraj et al. 2009).12

However, the model’s

results indicate that a privately informed analyst positively exaggerates his prediction for

most of the possible realizations of reported earnings.

Further, the results provided by Groysberg et al. (2011) together with the ones of Louis et al.

(2013) are consistent with the argument that forecast accuracy is a criterion for the research

house’s interior performance evaluation of an analyst rather than a measure of his reputation

with his clients. Louis et al. (2013) highlight the difference of forecast accuracy and forecast

informativeness in the presence of earnings and earnings guidance management by the firm.

They show that analysts sometimes side with their clients (shareholders) rather than with the

followed firm’s management and that the provision of informative forecasts, which may

predict natural rather than reported earnings, can encourage trading in the stock. This aspect

may be connected to analysts’ trading volume generation objective and the nomination to

equity analyst rankings such as the Institutional Investor All-Star ranking: Analysts providing

information which earns their clients an abnormal rate of return are nominated to be included

in the ranking by these investors. In finance theory, abnormal returns are generated by

underlying investment decisions, where these are based on private information such as the

information that is provided by analysts. Groysberg et al. (2011) provide evidence that

analysts are better compensated if they are recognized to be superior and also if they

stimulate trading.

Trading Volume Generation and Overoptimism

By means of a unique dataset, Groysberg et al. (2011) ascertain that an influential factor for

analysts’ compensation is the amount of trading stimulated with reports on a covered stock

and thus brokerage profits for the investment banking branch of an affiliated analyst. Jackson

(2005) and Beyer & Guttman (2011) provide in-depth theoretical guidance on the issue of

analyst forecasting behavior incentivized by the objective of trading volume generation.13

Jackson (2005) considers a setting in which an analyst trades off the long term incentive to

build a reputation with the short term objective to generate trading volume. His theory

suggests that forecast overoptimism is a result of investors’ uncertainties regarding the type

of the analyst and the existence of short-selling constraints, even if trading commissioning

objectives are restricted to a very low level. He also confirms this with archival evidence.

12

This situation is even exacerbated when pre-forecast firm earnings guidance is present. 13

Another representative of this field of literature is Hayes (1998). However, this paper focuses more on the

relevance of trading volume for the analysts’ information acquisition strategy (see Chapter 1.2.2.).

Introduction

6

Jackson’s (2005) framework considers analysts’ reporting strategies with a high level of

abstraction on the side of the market. Beyer & Guttman (2011) overcome this shortage by

integrating an analyst’s reporting decision with the market model of Grossman & Stiglitz

(1980). The tradeoff of the analyst’s incentives is incurred from Jackson (2005): Every

investor who receives the analyst forecast adjusts his position in the stock. The change in the

market price is also informative to the other investors who do not directly observe the

forecast. Thus, the analyst forecast is private information and causes information asymmetry

across investors. Beyer & Guttman (2011) provide a variety of implications. First, they show

that the (dynamic) forecast bias is an increasing function in the analyst’s private information

and that the bias is within a finite interval. Second, the analyst is, on average, more likely to

bias his forecast upward than downward, which is a direct result of investors’ risk aversion

and the residual uncertainty they have to incur for their investment in the firm. A last

implication is that an analyst with a high level of private information endowment

(represented by a highly precise private estimation signal over earnings in the model) does

not necessarily disclose a more accurate forecast because he knows that he will have a

relatively high impact on the trading in equilibrium, which incentivizes him to deviate more

from a truthful revelation strategy. This partly opposes the common belief that more private

information is necessarily associated with a more accurate forecast.

The empirical side of trading volume incentives of brokerage house affiliated analysts

provides mixed evidence on analysts’ overoptimism bias. Dugar & Nathan’s (1995) results

are such that affiliated analysts are more optimistic in their forecasting than non-affiliated

analysts. Additionally, they seem to not provide more informative forecasts and are, on

average, as accurate as their non-affiliation counterparties. In contrast, Frankel et al. (2006)

claim that analyst forecast informativeness increases with potential brokerage profits, which

partly contradicts the findings of Beyer & Guttman (2011). Additionally, Cowen et al. (2006)

provide evidence showing that analysts affiliated with investment banks that perform a firm’s

underwriting have a lower level of overoptimism in their forecasts than analysts who are

funded by a non-underwriter brokerage house. Thus, the effect is partly counter to the

discussed theoretical studies, which assume that analysts have an interest in stimulating

trading because of their underwriter affiliation. However, even Cowen et al. (2006, 119)

conclude that “optimism is at least partially driven by trading incentives”.

Introduction

7

Career Concerns and Herding

Equity analysts exhibit reputational or career concerns and, as will be clear in this subchapter,

their (relative) ability and performance is an important factor behind this objective. There

exists a solid theoretical base with a number of signaling models on the association of

analysts’ reputational concerns and their attempts to communicate their ability to clients or

employers by means of forecasting strategies which show patterns consistent with herding.

Scharfstein & Stein (1990) develop a theoretical model on the sequential investment

decisions of managers who are concerned about their labor market reputation. In their model

two groups of managers exist (but cannot be distinguished a priori by the labor market), a

good group with a high level and a bad group with a poor level of ability. The ability of each

type is modeled such that the good ones obtain an imperfectly informative signal about a

future state of nature determining the success of a project, whereas the bad type observes a

purely random signal without any information content. Scharfstein & Stein (1990) provide

results showing that good managers want to communicate their type by means of an unbiased

investment decision, whereas bad managers partially mimic the behavior of a good type (i.e.,

they herd in their investment decision) in order to receive a better reputation as if they would

communicate their type based on their (weak) information. The labor market, which

determines the reputation, infers two distinct pieces of information from the observation of an

investment decision, namely whether the investment decision yields a profitable or

unprofitable outcome and whether the behavior of managers is similar to that of others. They

argue that these are two separate pieces of information because a bad decision is not

considered to be a very bad signal over a manager’s ability if the other manager made the

same decision. However, the observation of a profitable decision is of large reputational

value if the peer manager made a contrary one. Graham (1999) adopts Scharfstein & Stein‘s

(1990) model and reinterprets it based on an analyst setting to include pre-existing public

information about the prediction of an uncertain future state in the game. He provides

theoretical implications and consistent evidence that if the public information conflicts with

the private information of a bad analyst, he is more likely to herd because he suspects his

private information to be wrong. This association is mitigated in situations when he has a

high initial reputation and a low real ability. Trueman (1994) develops a signaling structure in

which both types again want to signal a high ability to influence their reputational standing

with their clients and their employers. He shows that there is a general tendency to issue a

forecast that overweighs the prior expectations and/or other publicly available information

and underweights the analyst’s private information. In sum, it can be concluded that the

Introduction

8

information disclosure policy of analysts (or managers) is also shaped by their incentive to

communicate their ability, which ultimately yields a pattern consistent with an overweighing

of prior expectations relative to private information, i.e., herding on priors.

Clarke & Subramanian (2006) develop a theoretical Bayesian learning framework with

multiple periods and analysts. They highlight the importance of prior forecasting performance

for the assessment of analysts’ employment risk, and they consider three types of analysts,

good, bad and intermediate ones: Under- and over-performing analysts rather than

intermediate analysts issue bolder forecasts to manage their employment risk. This is because

high ability analysts will not be fired anyway due to their superiority, which means that they

put more weight on their private signal and are thus bolder than the intermediate analysts. In

contrast, low ability analysts also have an incentive to be bolder than their intermediate

counterparties because with a bold forecasting strategy they introduce noise, which makes it

harder for their employers to evaluate their abilities (i.e., partially pooling with high ability

analysts). Clarke & Subramanian’s (2006) theory of a non-monotonic association between

ability and forecasting policy, which in turn dynamically influences career concerns through

the assessment of the employment risk over time, is further supported by their empirical

investigation.

Existing empirical evidence emphasizes the association between relative performance and

analyst career outcomes, where the former is usually proxied by the relative magnitude of the

ex-post absolute forecast error. Mikhail et al. (1999) investigate the association between

forecast accuracy and the likelihood of analyst turnover, and provide evidence that increases

of absolute forecast accuracy are not associated with a larger probability of termination of

employment. However, they show that analysts which are less accurate than their peers have

a significantly higher risk of being fired, which establishes the claim that career concerns are

associated with the ex-post forecasting performance of an analyst relative to his peer(s). Hong

& Kubik (2003) also study the influence of analyst career concerns on the properties of their

forecasts and present the result that relatively less accurate forecasters are generally less

likely to move up the career ladder, which is in line with the findings of Mikhail et al. (1999).

In addition, they also highlight the fact that analysts who are overly optimistic in their

Introduction

9

forecasts are promoted more frequently after controlling for the already mentioned primary

effect. This is especially the case if they work for the underwriter of the stock.14

Based on the observation that relatively less accurate forecasters have to bear a significantly

larger employment risk, Hong et al. (2000) and Clement & Tse (2005) argue that the

knowledge about this association establishes an incentive for analysts to optimize this

association in expectation, i.e., a pattern that is in line with herding behavior. Further, they

perform studies on the variations of the association between relative forecasting performance

and career risk with the field experience of an analyst. They show that relatively

inexperienced analysts exhibit a higher tendency to bias their forecast in the direction of the

(expected) mean forecast than their more experienced counterparties.15

Thus, it can be

concluded that the group of analysts who have an especially high employment risk tend to

exhibit herding strategies in their forecasts in order to manage this risk.

Based on these empirical observations and the existing theoretical guidance, the following

argument can be established: Analysts who are relatively less accurate in their forecasts of a

firm’s earnings than their peers are punished with a less favorable career outcome (i.e., a

higher risk of termination). This association establishes an implicit incentive of an individual

analyst to choose the forecasting strategy such that the anticipated difference between one’s

own forecast error and the average peer forecast error is minimized. It is straightforward to

assume that all analysts exhibit career concerns. Thus, the relative performance objective is

bi- or multilateral and effectively yields an underreaction of an analyst to his own private

information and an overweighing of the prior expectations with respect to earnings.16

Moreover, this implicit incentive is strongest for those who can lose most from a termination

of employment, namely analysts who are at the beginning of their careers.17

14

Based on the results of the study of Clarke et al. (2007), it can be noted that analyst job changes do not seem

to alter their forecasting behavior. Thus, the summarized incentive seems to be unaltered even if analysts start in

a new workplace. It follows that career concerns do not depend on a career within only one research department. 15

An additional result provided by Clement & Tse (2005) is that bold forecasts are on average more accurate

than herding forecasts. 16

This claim is easily proven by means of a standard noisy rational expectations equilibrium model with two

forecasters obtaining independent private information signals to forecast earnings based on the objective of

relative performance. This model is available upon request from the author. 17

It shall be noted that other information-based reasons may exist for analysts to herd in their forecasts. For

example, Welch (2000) explores the situation of sequential release of stock recommendations by analysts. He

points out a positive association between an early recommendation of an analyst and the later recommendation

of other analysts. It shall be noted that herding, according to Welch (2000), is information based and determined

by the sequence of forecast releases rather than driven by analysts’ incentives. See Chapter 1.2.2. for further

discussion.

Introduction

10

Investors’ and Employers’ Inference of Analysts’ Abilities

In the previous chapter, I summarized theory and evidence on the relevance of career

concerns for analyst forecasting behavior. A related research topic is the literature on the

inference effort of the abilities of analysts performed by their employers and clients. Thus, I

consider the other side of the communication process than in the previous subchapter, namely

that of the recipients.

Theoretical research is provided by Gerardi & Yariv (2008) that utilizes an agency setting

with multiple experts as agents and one decision maker as the principal. The objectives of the

experts include not only the costly acquisition of expertise but also the effort to utilize the

gained expertise for the purpose of a profitability evaluation of a risky project to help the

principal with his investment decision.18

The decision variables of the principal are the

number of contracted experts and the weighting (and/or recognition) of their

recommendations. The model provides the result that the principal hires only at most two

experts and sometimes even decides not to follow their recommendations. If two experts are

selected, the principal wishes to choose the ones who have the most extreme preferences

relative to himself because this eases the weighing of recommendations. However, he may

also choose to sometimes ignore the recommendations provided by the experts. Moreover,

the experts consider this preference dependence in their expertise acquisition strategies.

The empirical literature generally focuses more on the client’s side of this interaction.

However, the results are also partly applicable to the employer’s communication process with

the analyst. It is shown by archival studies that superior analysts are considered to deliver

more informative forecasts, which is why investors react more strongly to them compared to

inferior analysts (e.g., Park & Stice 2000).19

Clement & Tse (2003) build on this viewpoint

and test whether investors would only focus on the accuracy of an analyst’s forecast revision

to assess his abilities. They generate results showing that investors react more strongly to

analysts who are associated with larger brokerage houses and forecasts that are released in the

first half of a fiscal year. Building on the assumption that analysts with a higher ability are

more likely to be employed by the well-funded research departments of larger investment

banks (e.g., Groysberg et al. 2011), it can be reasoned that the affiliation is a criterion for the

assessment of an analyst’s abilities. In an attempt to reconcile their results with prior

research, Chen et al. (2005) develop a simple model on the inference problem of investors

18

The latter objective of the experts contains a notion of career concerns. 19

Cox & Kleiman (2000) provide evidence that All-American analysts have superior skills rather than luck.

Introduction

11

with respect to the ability of an analyst. They provide theoretical and empirically confirmed

results showing that the more forecasting periods already occurred, the more information

investors receive not only about fundamentals but also about the analyst’s ability. This in turn

shapes their pricing behavior such that they place a larger weight on a forecast if the analyst

is “proven” to be accurate over a longer duration.20

The evidence presented in this subsection has an important link to the career concerns

literature discussed above: If an analyst is ignored by his clients due to a lack of accuracy

over a long period, the employer may interpret this as a lack of ability and may decide to

terminate his employment. Thus, the provocation of a market reaction represents another

facet of analyst career concerns.

Analysts’ Endowment with Private vs. Public Fundamental Information

In the previous chapters I already discussed several theoretical papers. Almost all of them,

except Graham (1999), assume a strictly private fundamental information endowment of

analysts, where the observed information may or may not be of value for the forecast

recipients. The relative contribution of public and private fundamental information for the

forecasting of earnings is the main point of this part of the literature discussion. Moreover, it

can be noted that the theoretical side of this branch of literature has a strong focus on the

reconciliation of individual forecast properties with more abstract properties such as the mean

consensus forecast (error) or forecast dispersion, since both constructs are frequently used in

empirical research, i.e., to proxy for earnings expectations (e.g., O’Brien 1988).

In an extension of the theoretical work of Kim & Verrecchia (1991) on patterns in price

variability and expected trading volume, Abarbanell et al. (1995) introduce analyst forecasts

as a source of private information of investors. The forecasts follow an exogenously

predetermined structure and include a common estimation error term and an analyst-specific

estimation error term. The former captures the public information component, whereas the

latter establish differential private informedness of analysts and investors. They show that

analyst forecasts are, at best, a noisy measure of investor’s differential beliefs and that the

relative forecasting properties (i.e., consensus among analysts) are influential in the reactions

of the market to forecasts.21

In particular, both expected trading volume and the variance of

20

Bonner et al. (2007) show that not only past performance or the length of the track record or affiliation can

influence the perceived informativeness of analyst forecasts, but also the sophistication of investors. Moreover,

media coverage of so called “celebrity analysts” also mitigates the effect of a lack of sophistication of investors

on the pricing of a forecast. 21

For a related investigation on consensus vs. informedness, see Holthausen & Verrecchia (1990).

Introduction

12

the price change are shown to increase in forecast dispersion. Abarbanell et al. (1995) is

closely associated with the theoretical investigation of Barron et al. (1998). They go a step

further and disentangle analyst forecast properties from analysts’ information environment.

They utilize the facts that consensus forecast error and forecast dispersion are differentially

influenced by the idiosyncratic and systematic estimation errors in analysts’ private

information signals: “[T]he expected dispersion in forecasts is an increasing function of

uncertainty but a decreasing function of consensus [among analysts], while the expected

squared error in the mean forecast is an increasing function of both uncertainty and

consensus.” (Barron et al. 1998, 422) Based on these properties, the empirical investigation

by Barron et al. (2002) yields unique estimates of the weighing of private and public

information. Their empirical study concludes that the idiosyncratic component increases in its

relative magnitude to the systematic component after the release of an earnings

announcement, which is reconcilable to prior theories on the existence of event-period private

information such as that of Kim & Verrecchia (1997). Further, Kim et al. (2001) develop a

parsimonious model with a finite number of non-strategic analysts and point out that the

mean consensus forecast inefficiently summarizes all of the available information and

overweighs public information relative to analysts’ private information.

Further, the discussed theories are not very explicit about which pieces of information are

summarized under the term “public information”. Several empirical and theoretical studies

investigate analysts’ processing of different sources of public information. Their results can

be summarized as follows:22

· Information impounded in prior stock price changes: As is commonly believed by

accounting and finance scholars, investors impound their private information into

market prices through their trading activities, which generates noisy public

information. Thus, there is considerable information in stock price changes, which can

be inferred by analysts. However, analysts seem to underreact to the information in

these stock returns (Lys & Sohn 1990, Abarbanell 1991), where analysts’ information

extraction ability may mitigate this underreaction (Elgers & Lo 1994).23

Recently,

Clement et al. (2011) provide evidence supporting the argument that the ability to

extract information from stock returns may be a distinct feature of analyst expertise.

22

Furthermore, the recent empirical literature uses components of public information to predict analyst forecast

errors in order to improve their estimates for further purposes such as in investigations of the implied cost of

capital or trading strategy developments (i.e., Hughes et al. 2008, Mohanram & Gode 2013, So 2013). 23

See Chapter 1.2.1. for a discussion of analyst experience.

Introduction

13

· Previously released peer forecasts: In an early and well-known study Stickel (1990)

shows that analysts also use information from previously released peer forecasts, i.e.,

from forecasts of other analysts that also follow the same firm.

· Earnings guidance and other voluntary firm information: A special tension exists

between the provisions of (potentially biased) earnings guidance, the (strategically

chosen) analyst forecast as a proxy for the earnings expectation and (potentially

managed) earnings. In particular, a manager with an interest in the end-of-period

share price may want to first guide expectations downward in order to make the

subsequently disclosed forecast easier to beat with annual earnings (Baginski &

Hassell 1990).24

Versano & Trueman (2013) develop a theoretical model to give some

guidance on this association. They show that only privately but not publicly disclosed

earnings guidance would be chosen to guide analyst expectations downward. Contrary

to Versano & Trueman (2013), empirical evidence shows significant results in support

of the use of public earnings guidance to guide forecasts (a proxy for earnings

expectations) downward (Cotter et al. 2006). Such an interconnectedness of disclosure

may even be beneficial from the analyst’s perspective because it stimulates trading in

the window between the earnings guidance disclosure and the earnings announcement

(Feng & McVay 2010). With respect to the informativeness of earnings guidance,

Lang & Lundholm (1996) show that more informative firm disclosure policies are

associated with more accurate earnings predictions. In line with this result, Chen et al.

(2011) document the fact that firms which commit to stopping the disclosure of

earnings guidance are followed by less accurate analysts. Moreover, Hilary & Shen

(2013) argue that the ability to extract information from management earnings

guidance is also a distinct feature of analyst expertise.

Another issue, which is relevant in a discussion on analysts’ use of public relative to private

information, is analysts’ aggregation of these two types of information. Several studies argue

that analysts would underreact to the available public information and would thus overreact

to their privately obtained information (e.g., Mikhail et al. 2003, Zhang 2008). In a more

recent, jointly theoretical and empirical investigation, Chen & Jiang (2006) establish the

claim of an overweighting or underweighting of private information relative to public

information depending on the influence of other incentives on an analyst’s forecasting

24

The consequences of a setting in which an analyst predicts (potentially) managed earnings are discussed by

Beyer (2008), as summarized already in Chapter 1.2.1. Her economic framework assumes that managers may

want to meet or beat analyst forecasts.

Introduction

14

strategy. In particular, they present data showing that the weighting distribution is skewed

towards positive forecasts relative to the consensus forecast, where the level of skewness

depends on the realization of an analyst’s private information: In more favorable forecasts

private information is overweighted, whereas in less favorable forecasts it is underweighted.

On average this yields an overweighting pattern. They conclude that the strategic incentives

(discussed in Chapter 1.2.1.) are of great relevance for the observable properties of forecasts.

Moreover, their results, which are obtained by means of a probability-based method that is

considered to be statistically very robust, confirms the findings of the underreaction

hypothesis of available public information, i.e., an information-based herding pattern similar

to the one reasoned by Welch (2000).

The Relevance of Non-Fundamental Information

Existing theories argue that the endowment with fundamental information is not the only

possible information which may be relevant for analysts’ behavior. So far, the literature has

assumed the existence of fundamental information about the followed firm such as firm value

and/or earnings, but little research (especially empirical research) has been performed on

non-fundamental information in general and analysts’ use of this class of information in

particular. It shall be noted that all models discussed in this chapter utilize a Kyle (1985) style

market model, which considers single or multiple privately informed speculators and a

market maker under the assumption of general risk neutrality.

There are three notable theoretical contributions on the use of non-fundamental information

for speculative reasons. Madrigal (1996) develops an intertemporal asset market with two

sorts of informed trades, those made by an insider endowed with fundamental information

and those implemented by a speculator endowed with non-fundamental information about

forthcoming (random) liquidity demand. The speculator may not have fundamental

information, but he can better infer it from past rounds of trading than the market maker. It

shall be noted that the non-presence of the insider (who is endowed with fundamental

information) yields a worthlessness of the speculator’s non-fundamental information. By

means of this model, Madrigal (1996) shows that the existence of a speculator trading on

non-fundamental information may incentivize the insider to gather less fundamental

information due to a decreased marginal rate of return of this information. This may even

yield situations with an overall decreased price efficiency in equilibrium. Similar results are

obtained by Yu (1999). He considers the case in which there is only an insider, who is

endowed with two signals, fundamental information and a noisy signal about the demand of

Introduction

15

the liquidity trader. He shows that the profitability of this knowledge depends on the

precision of the latter signal: If it is perfectly informative, the insider can obtain positive

rents, whereas an imperfect signal may even be detrimental for his investment decision and

thus the profitability of his trading orders.

In a setting with a strategic manager who manipulates earnings and has an uncertain interest

in the market price similar to the setting of Fischer & Verrecchia (2000), Fischer & Stocken

(2004) provide some intuition about a strategic manager’s manipulation behavior when the

speculator is endowed with some information about the incentives of the manager. They

show that if the speculator has more information about the manager’s uncertain interest in the

price, the price would be increasingly responsive to earnings, which ex-ante incentivizes the

manager to bias earnings even more. This in turn yields the outcome that the presence of the

non-fundamentally endowed speculator increases the price efficiency in equilibrium only if

the speculator does not know too much about the manager’s objective relative to the

fundamentals of a firm.

The sole theoretical contribution of an information intermediary possessing private

information about a non-fundamental aspect of the market environment is that of Cheynel &

Levine (2012). Their analyst takes the role of an information seller and endogenously chooses

the price of the non-fundamental information, which he subsequently sells to a subgroup of

investors. They show that more precise non-fundamental information is more widely

disseminated among investors for a smaller fee but (again) it is reasoned that price efficiency

does not necessarily increase with the presence of a non-fundamental information seller.25

1.2.2. The Causes and Consequences of Analyst Coverage Behavior

In this chapter, I will summarize and discuss the state of research (ii) on the determinants

behind the decision of an analyst to initiate coverage and start acquiring information about a

firm and (ii) on some of the documented consequences of analyst coverage for the followed

firms.

Analyst Information Acquisition Costs and Coverage Initiation

In the chapters above I treated the amount of public and private information as if it were

exogenously given. In reality analysts actively collect information in order to predict a firm’s

25

As will be discussed below, Hayes (1998) assumes that the analyst, whose aim it is to influence the trading

decision of an investor, is endowed with some proprietary information about the random shocks in the future

share price. He moreover bases his decision to initiate coverage and collect information on this piece of

information.

Introduction

16

earnings. The analyst coverage literature has a strong focus on the information acquisition

logic because it is argued that the likelihood of coverage initiation is identical to the

propensity of an analyst to start collecting information. Notable theoretical contributions are

Hayes (1998), Mittendorf & Zhang (2005), Langberg & Sivaramakrishnan (2008) and

Fischer & Stocken (2010). Hayes (1998) develops a theoretical framework with a strategic

analyst and an investor, where the latter receives some information from the former and

either buys or sells shares. She shows that an analyst, who aims to maximize stock trading,

has an incentive to acquire more information only for well-performing firms, which is in line

with the empirical evidence of McNichols & O’Brien (1997). She argues that this effect

would especially occur in the existence of short-selling constraints.

There are several notable theoretical contributions on analyst coverage initiation. Fischer &

Stocken (2010) develop a cheap talk model with credibility issues between a biased

information sender (e.g., the “analyst” who wants to stimulate trade) and a receiver (e.g., the

“investor”). The analyst first observes a public information signal (e.g., earnings guidance,

information in stock price changes) and then decides whether to initiate coverage and, in the

case that coverage is initiated, how much private information to acquire. Their results

highlight the non-monotonic relationship between public information precision and private

information acquisition incentives. They predict that the introduction of public information

can yield a suboptimal total information endowment of the investor due to the credibility

costs in the cheap talk structure because these costs may be high enough to dissuade the

analyst from initiating coverage. Closely related to Fischer & Stocken (2010) is the theory of

Mittendorf & Zhang (2005), which extends the perspective established in Chapter 1.2.1.

about biased earnings guidance by means of a principal-agent relationship in the presence of

a third party, the analyst. The authors argue that the manipulation of earnings guidance is a

“necessary evil” because it introduces the uncertainty needed to motivate the analyst to

initiate coverage. Coverage is assumed to benefit the manager because the interaction

between manager and analyst is assumed to be part of the manager’s incentive contract, i.e.,

he benefits when there is analyst coverage. In a third setting, a voluntary disclosure model,

Langberg & Sivaramakrishnan (2008) raise the question of the likelihood of voluntarily

disclosed firm information in the potential presence of an analyst. The authors derive

conditions consistent with the argument that good news is disclosed even if it is imprecise,

whereas bad news is only disclosed if it is sufficiently precise. Regarding the role of analysts,

it is pointed out that good news is more likely to be covered than bad news and that analysts

Introduction

17

may have a preference for well-performing firms. This is generally in line with the

implications of Hayes (1998).26

In all of the mentioned theories an analyst has to pay a cost, which is a linear or convex

function of the information precision of the obtained private signal. Empirical research has

identified a variety of factors that shape these costs of information acquisition. These articles

usually use the notion of forecasting complexity or other analyst-specific factors as a

determinant of the analyst’s information acquisition strategy and thus the likelihood of

analyst coverage:

· Firm-specific factors:27

A first factor can be identified as the complexity of a firm’s

organizational structure. Bhushan (1989) and Frankel et al. (2006) argue that the

forecasting complexity and thus the costs of analyst information acquisition increase

in the number of business segments of a firm. Closely related to this first point is a

firm’s international diversification, which can be mentioned as another firm-specific

factor and which has been empirically shown to be a significant factor in the analyst’s

information acquisition strategy: Larger diversification is associated with a lower

accuracy of forecasts since a geographically specialized analyst has to bear larger

marginal costs of information gathering, which decreases his optimal information

precision level (Duru & Reeb 2002). Thus, both the organizational and the

geographical complexity of a firm increase information acquisition costs and thus

decrease the likelihood of analyst coverage. Moreover, Tan et al. (2011) document the

fact that the mandated change from local GAAP to IFRS led to an increase in analyst

following through increased comparability. Under the assumption that IFRS is

superior in terms of financial information quality, this is in line with the observations

of Lang & Lundholm (1996), namely that firms with a better disclosure quality and

policy show higher analyst following because this lowers the costs of information

acquisition. A last result on firm-specific factors is provided by Barth et al. (2002),

who show that the composition of a firm’s assets is also relevant in the information

acquisition strategy of an analyst. In particular, they claim that analysts would be

drawn to firms with a larger stake in intangible assets, which can be assumed to

26

Empirical research by Branson et al. (1998), Irvine (2003) and Das et al. (2006) indicates that an analyst’s

decision to initiate firm coverage has information content for the stock market. The presented theories are not

able to explain this phenomenon. 27

It shall be noted that the firm-specific factors may directly influence earnings’ priors. However, the

argumentation through costs yields qualitatively similar results, due to the assumption that the implications for

analyst information acquisition are the same for ex-ante less precise earnings or higher information acquisition

costs.

Introduction

18

increase a firm’s valuation uncertainty. This result is somewhat counter to those

discussed before since it implies that analysts would prefer firms with larger innate

information acquisition costs. The authors argue that the brokerage profit component

may explain this result since a higher uncertainty may be associated with larger

brokerage profits.

· Coverage portfolio specific factors: Analysts are assumed to face a decision of either

collecting information about a particular firm or gathering information about a whole

industry or geographical area. This tradeoff is especially relevant in the decision on

the firm coverage portfolio of an analyst, i.e., whether he chooses to specialize in an

industry or geographical area. Therefore, it is straightforward to argue that a

segmental or regional specialization is positively associated with forecast accuracy,

which is consistent with empirical observations (Clement 1999, Malloy 2005, Kini et

al. 2009). In a recent study, Sonney (2009) presents evidence showing that analysts

with a country specialization significantly outperform their counterparts with an

industry focus.

A last topic of high relevance for an analyst’s coverage initiation decision is the special event

of an Initial Public Offering (henceforth IPO) of a firm due to the newly created potential of

underwriter profits. Empirical research documents mixed evidence on the association

between the event of an IPO, analyst following and underwriter affiliation. Rajan & Servaes

(1997) and Cliff & Denis (2004) present evidence showing that higher underpricing

stimulates analyst coverage due to overoptimism. In particular underwriter affiliated analysts

are more likely to initiate coverage (Cliff & Denis 2004) and hence issue high target prices

and more favorable information in the case that the aftermarket performance of the firm is

below prior expectations (James & Karceski 2006). Moreover, it has been claimed that this

favorable coverage would be “discounted” by the market (Michaely & Womack 1999).

Contrary to these findings, Bradley et al. (2008) find evidence neither for the relationship

between aftermarket performance and affiliation of coverage-initiating analysts, nor for the

claim that investors would underreact to affiliated analysts’ information releases.

Consequences of Changes in Analyst Following

The existing literature in finance and accounting has documented a number of different

consequences for firms associated with (changes of) analyst firm coverage. These can be

summarized with the following three main consequences:

Introduction

19

· Facilitation of changes in a firm’s cost of capital: Alfond & Berger (1999) and

Roulstone (2003) use simultaneous equations models to show that higher analyst

coverage is associated with more stock liquidity. As is argued by Lambert et al.

(2011), this implies a decrease in a firm’s cost of capital. Another observation is made

by Chang et al. (2006), who argue that larger analyst following leads to better

financing terms and thus to a decrease in the cost of capital.

· Facilitation of changes in a firm’s disclosure policy: By means of a product market

oligopoly setting with a potential analyst following the firms in an industry, Arya &

Mittendorf (2007) provide theoretical guidance on the role of analysts as information

intermediaries. They show that a firm which benefits from analyst coverage (e.g.,

through a decrease of the firm’s cost of capital), initiates a more revealing disclosure

policy even if this means that it would need to reveal information which can be used

“against” it by its industry competitor. In line with this argument, Yu (2008) provides

evidence consistent with the conclusion that a higher analyst following decreases a

manager’s incentive to bias his information and initiate a more truthful and thus more

informative disclosure policy. It is straightforward to reason that this also has an

indirect effect on the cost of capital (Strobl 2013).

· Changes in the pricing of earnings: The existence of one (or multiple) analyst(s) that

provide firm information to (a part of) the market can have implications for the

pricing of earnings which are reported by the firm. First, it is assumed that analysts

provide new information prior to an earnings release (Asquith et al. 2005). However,

empirical studies show mixed evidence on the relation between the informativeness of

analyst earnings forecasts and reported earnings: Francis et al. (2002) and Frankel et

al. (2006) argue that they are complements (i.e., forecasts reinforce earnings), whereas

Chen et al. (2010) advocate the viewpoint that they are substitutes (i.e., forecasts pre-

empt earnings). Second, other empirical research by Dempsey (1989), Ayers &

Freeman (2003) and Gleason & Lee (2003) provide evidence that higher coverage

accelerates the pricing of earnings information released by the firm. These studies

analyze various reasons for this effect such as an increased motivation for investors to

“be prepared” for the interpretation of an earnings announcement (Dempsey 1989) or

the delegation of this interpretation role to analysts, where more analysts are assumed

to yield a higher responsiveness of the market to corporate financial information

releases due to the increased information processing capacity of the market (Ayers &

Freeman 2003).

Introduction

20

1.3. Contribution

The current dissertation provides three main contributions to the previously discussed

literature, which are based on the interactions of analysts with three major interest groups

(and involve the consideration of particular decisions which have been summarized in the

sequence of decisions in Figure 1), namely (i) peer analysts, i.e., analysts, who follow the

same firm and provide similar services (stages and ), (ii) the followed firm (stage

) and (iii) their clients (stage ), respectively. It is shown that the behavior of an

individual analyst is shaped by and shapes others’ actions in important ways.

1.3.1. Analysts’ Career Concerns, Forecast Biasing and Firm Coverage

Selection

Prior research has shown that career concerns influence equity analysts’ (and other economic

agents’) behavior. In particular, it is argued that intensified analyst career concerns yield

patterns in forecasts consistent with herding on prior expectations (e.g., Scharfstein & Stein

1990, Trueman 1994, Hong et al. 2000, Hong & Kubik 2003).

The first paper of this dissertation contributes to the literature by taking analysts’ herding

incentives as given and analyzing a setting with two equity analysts, who (simultaneously)

decide on the coverage of a firm by means of the provision of earnings forecasts. The

coverage is rewarded by a partially stochastic outcome, which is split in two halves in the

case that both analysts decide to follow the firm and is influenced by the realized forecasts in

a positive manner. However, both analysts obtain private proprietary information on the

stochastic elements of their halves of the reward and decide whether to start gathering

fundamental earnings information and to subsequently release a manipulated forecast. In the

case that they both decide to cover the firm, their performance is not only evaluated by

absolute forecast accuracy (as is the case when an analyst is the sole follower of a firm) but

with absolute forecast precision relative to the respective other analyst.

By means of this setting I am able to show that career concerns impact an individual analyst’s

coverage decision in a non-trivial way. In particular, the inherent effects in the model are

such that increased analyst career concerns keep the analyst from following a firm (i) if the

stock in question is relatively illiquid (i.e., trading volume is not very responsive to changes

in the forecast) and (ii) if the average private information quality of analysts is relatively

high. In addition, the paper presents the result that the decision against the coverage of a firm

(based on non-fundamental information) has information value to the peer analyst.

Introduction

21

1.3.2. Analyst Information Acquisition and the Informativeness of Forecasts

and Managed Earnings

Empirical studies show mixed evidence on the question of whether the informativeness of

pre-earnings analyst information and the information content of (potentially) managed

earnings announcements are substitutes (Chen et al. 2010) or complements (Francis et al.

2002, Frankel et al. 2006). However, since the informativeness of earnings announcements is

of great interest for standard setters, the issue of whether analyst information pre-empts or

reinforces the information content of earnings is of general importance.

In a second setting I show that an analyst who obtains a noisy signal over natural earnings

and wants to predict manipulated earnings chooses his information acquisition effort in such

a way that he matches the noise in the endogenous reporting bias. This in turn also shapes a

manager’s costly earnings management strategy, which optimizes the uncertain objective to

influence the price and moreover the meet-or-beat-analyst-forecast incentive. The paper

provides an intuition behind the empirical results and qualifies meet-or-beat incentives as the

reason for the so called interpretation or disciplining role of analyst earnings forecasts. It is

moreover shown that this role dominates the information role if information acquisition costs

are sufficiently high such that the weight in front of the analyst forecast in a regression of

price on earnings and the forecast shows a negative sign.

1.3.3. Discretionary Analyst Coverage and Capital Market Characteristics

The empirical as well as analytical literature on analyst coverage initiation or abandonment

imposes the presumption that analysts, incentivized by a tradeoff between stimulating

informed trade and reputational costs, would always disclose earnings forecasts if they have

previously gathered information (e.g., Hayes 1998, Cowen et al. 2006, Beyer & Guttman

2011). For example, the contributions of Hayes (1998), Mittendorf & Zhang (2005) and

Fischer & Stocken (2010) assume that once an analyst has started collecting information he

always discloses the information that he acquired and either does or does not distort it (i.e., an

application of an ex-ante coverage perspective). However, it is straightforward to assume that

an analyst has some discretion about whether he wants to withhold or release the already

acquired information, which is more consistent with an ex-post coverage concept.

The third contribution of this dissertation focuses on the discretionary coverage decision of

an analyst, who may provide a private information signal to a subset of the market and thus

chooses whether or not to create private information asymmetry among investors. As a

consequence, informed investors choose their stock trade order based on this information,

Introduction

22

whereas investors who are not clients of the analyst may infer some of the communicated

information from the market price. It is shown that the analyst’s coverage strategy, which

optimizes the tradeoff between the stimulation of informed trade and the costs stemming

from reputational concerns, is crucially dependent on the market’s properties and on the fact

that the analyst only initiates coverage and provides forecasted information if the information

is sufficiently extreme. In particular, it is shown that the likelihood of analyst coverage is a

non-monotonic function of the risk attitude of investors and the market penetration of the

analyst’s information: The likelihood of analyst coverage decreases with investors’ risk

tolerance and with the market penetration of the information (i.e., the fraction of the market

that the analyst directly supplies with the forecasting information) if the liquidity shock is

minor but reputational costs are significant, and increases otherwise.

In an extension with an imperfectly competitive capital market in which a few large traders

are aware that their demand order impacts the share price it is shown that analysts are more

likely to follow more liquid stocks. Prior empirical research such as that of Roulstone (2003)

shows that analyst following increases the liquidity of a stock. However, it has been unclear

whether analysts would consciously pick stocks with larger market liquidity.28

Moreover, this

result runs counter to the argumentation of studies such as those of Bhushan (1989), Ackert &

Athanassakos (2003) as well as Ljungqvist et al. (2007), who advocate the viewpoint that

analysts would prefer to supply large institutional investors with private information. Such an

argument is contradictive because large investors, whose trades substantially impact the stock

price, trade less based on their private information. This consequently impairs the liquidity in

the market.

1.4. Structure of the Dissertation

The cumulative dissertation proceeds such that the following chapters investigate the

previously derived research questions: (i) Analysts’ Career Concerns, Forecast Biasing and

Firm Coverage Selection (Chapter 2), (ii) Analyst Information Acquisition and the

Informativeness of Forecasts and Manipulated Earnings (Chapter 3) and (iii) Discretionary

Analyst Coverage and Capital Market Characteristics (Chapter 4). Chapter 5 provides a

comparative discussion and concludes the dissertation.

28

Beyer et al. (2010, 328) reason as follows: “Further, the direction of causality, that is, whether analyst

following leads to changes in liquidity or changes in cost of capital for firms, or vice versa, is not clear.”

Analysts’ Career Concerns, Forecast Biasing and Firm Coverage Selection

23

2. Analysts’ Career Concerns, Forecast Biasing and Firm

Coverage Selection

Chapter Abstract

In this paper I develop a rational expectations equilibrium model with two equity analysts,

who simultaneously decide whether or not to initiate coverage of a firm by providing

manipulated earnings forecasts. In line with empirical evidence on analysts’ career concerns,

I assume that analysts exhibit herding in the case that another analyst also follows a firm in

order to manage the risk of termination of employment. The main result of the paper is that

the likelihood of coverage initiation is a non-monotonic function of analyst career concerns.

In particular, it is shown that the association between coverage initiation and career concerns

is negative if the average analyst private information precision is sufficiently large and if the

responsiveness of the reward to the forecast is relatively small. In addition, I show that the

coverage initiation decision has information content to stakeholders such as peer analysts.

Keywords: analyst following, herding, forecast bias, non-fundamental information

JEL: D82, G20, M41

Analysts’ Career Concerns, Forecast Biasing and Firm Coverage Selection

24

2.1. Introduction

Equity analyst coverage is of great importance for firms because a larger analyst following is

associated with benefits for the firms, such as a more efficient pricing process (Ayers &

Freeman 2003, Barth & Hutton 2004), a higher market liquidity (Alfond & Berger 1999,

Roulstone 2003), and better equity financing terms (Chang et al. 2006), which altogether

decrease the firm’s cost of equity capital. Companies seem to be aware of the benefits, since

they are even willing to pay analysts for their services (Kirk 2011). Thus, analyst coverage

has a variety of consequences for the firm being covered. However, not a lot has been said

about the factors behind an analyst’s decision to initiate coverage.29

Due to the limited

availability of data on analysts’ decisions against the coverage of a firm, the investigation of

the issue of the causes of analyst following is a theoretical one.

In this paper I develop a symmetric and simultaneous rational expectations equilibrium model

to investigate the influence of analysts’ career concerns as a cause for coverage initiation. In

particular, I consider the decision of two peer analysts to initiate coverage of a particular firm

by means of earnings forecasting. I assume that each analyst receives a partly random reward

(i.e., brokerage profits and subscription fees net of information acquisition and other costs

such as opportunity costs), which is an increasing function of the analyst’s forecast.

Moreover, the analyst observes part of the random reward (i.e., non-fundamental or

proprietary information) and bases his decision on this observation.30

The key feature of the

model is introduced with the assumption that an individual analyst, in the presence of another

analyst who can serve as a forecasting performance benchmark for the first analyst’s

employer, has career concerns and realizes a herding pattern in his forecast because he also

optimizes the ex-ante expected difference of forecast errors (henceforth referred to as

“relative forecast accuracy”).31

A large set of prior research papers argues that analysts’ career concerns would have a

significant effect on their behavior. Scharfstein & Stein (1990) show theoretically that

managers who have reputational concerns partly ignore their private information and make a

29

Only the effect of the provision of earnings guidance on analyst following is already theoretically (e.g.,

Mittendorf & Zhang 2005, Arya & Mittendorf 2007, Fischer & Stocken 2010) as well as empirically (e.g., Chen

et al. 2011) well investigated. 30