SARBANES-OXLEY ACT OF 2002 Overview and Update. 2 Accounting Governance (Before Sarbanes-Oxley Act...

31

SARBANES-OXLEY ACT OF 2002 Overview and Update

-

date post

19-Dec-2015 -

Category

Documents

-

view

225 -

download

0

Transcript of SARBANES-OXLEY ACT OF 2002 Overview and Update. 2 Accounting Governance (Before Sarbanes-Oxley Act...

SARBANES-OXLEY ACT OF 2002

Overview and Update

2

Accounting Governance (Before Sarbanes-Oxley Act 2002)

SEC has always had statutory authority to oversee accounting, but delegated it to

FASB – guidelines for non-governmental financial statement reporting.

GASB - guidelines for governmental financial statement reporting.

3

Accounting Governance (Before SO Act con’t)

AICPA’s ASB (Auditing Standards Board) – guidelines for auditing practices.

Accounting Standards Executive Committee (AcSEC) – supplements FASBs.

AICPA’s SEC Practice Section (SECPS) for firms with issuers.

Public Oversight Board (POB) manages Peer Review process.

Quality Control Inquiry Committee (QCIC) Professional Ethics Division

4

The Challenges to Governance

Expectation bubbles burst Technology and telecom industries meltdown

Scandals that challenged accounting self-governance Enron – special entities & form vs. substance. Worldcom – mismatching costs on lines. Tyco – CEO special payments/contracts and falsifying

records. Aldelphia – off-balance sheet loans, excessive

capitalization, and inflated income.

5

What was Missing?

adequate disclosure in financial reporting

independence of the accounting firms

weak corporate audit committees

management was not personally responsible for financial statements and disclosure

6

Sarbanes-Oxley Getting Back on Track

SEC = Active Governance & Monitoring

Public Company Accounting Oversight Board New Corporate Responsibilities

“Real” Audit Committee Financial Statement Certification Regulating Officers & Directors New Disclosure Requirements

Other Provisions

7

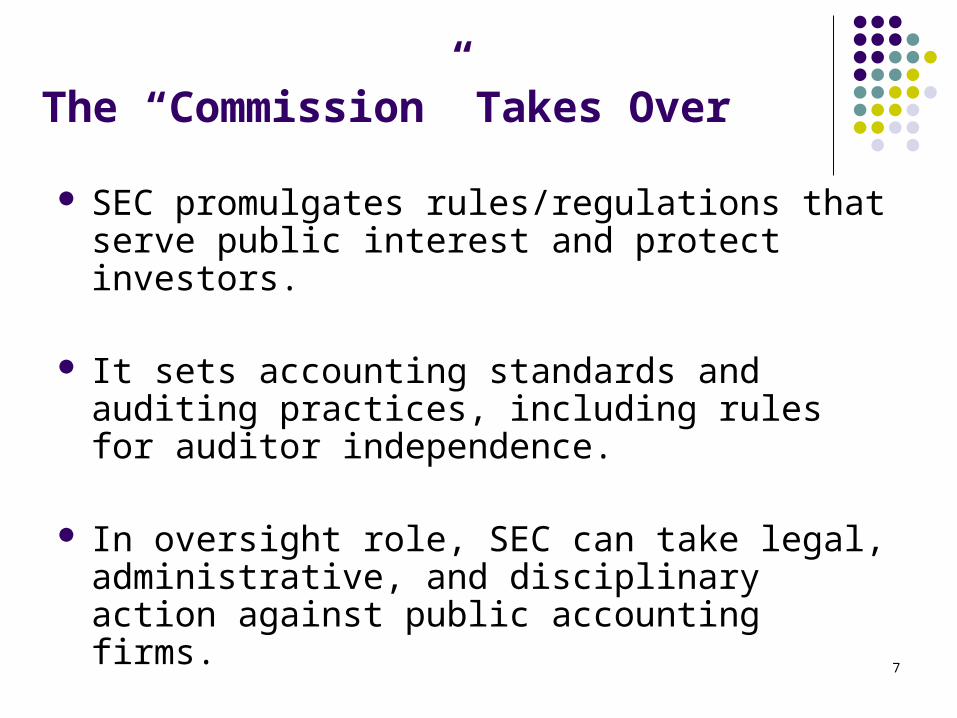

The “Commission” Takes Over

SEC promulgates rules/regulations that serve public interest and protect investors.

It sets accounting standards and auditing practices, including rules for auditor independence.

In oversight role, SEC can take legal, administrative, and disciplinary action against public accounting firms.

8

Accounting Oversight Board - New Partner in Governance

a non-governmental not-for-profit corporation registers and regulates all public accounting firms that

provide audit services to public companies has authority to establish rules governing audits, conduct

inspections and investigations, and impose sanctions SEC approved Board on 4/25/2003 with William

McDonough as President. Website: http://www.pcaobus.org/

about October 25, 2003, it becomes unlawful for any non-registered firm to prepare/issue an audit report for a public company

9

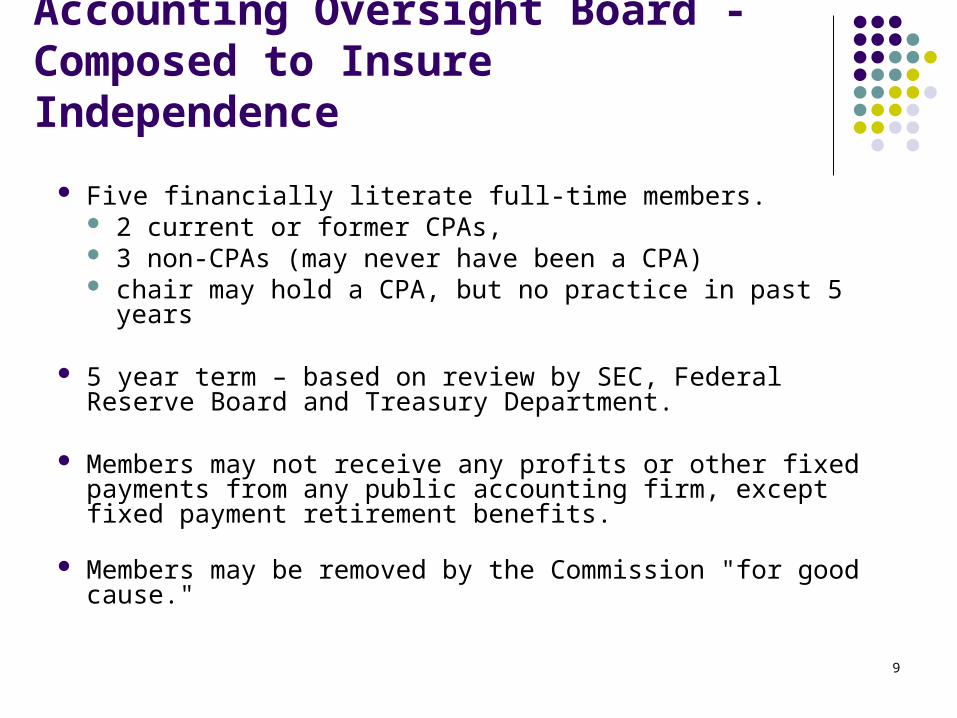

Accounting Oversight Board - Composed to Insure Independence

Five financially literate full-time members. 2 current or former CPAs, 3 non-CPAs (may never have been a CPA) chair may hold a CPA, but no practice in past 5 years

5 year term – based on review by SEC, Federal Reserve Board and Treasury Department.

Members may not receive any profits or other fixed payments from any public accounting firm, except fixed payment retirement benefits.

Members may be removed by the Commission "for good cause."

10

Accounting Oversight Board - Implications for CPA Firms

Registered CPA firms will pay an annual fee to the Board.

Issuers will be assessed a "annual accounting support fee“

Annual quality reviews (inspections) for firms handling over 100 issues; every three years for all others.

Foreign accounting firms who audit a U.S. company must register and comply.

11

Accounting Oversight Board - Implications for CPA Firms

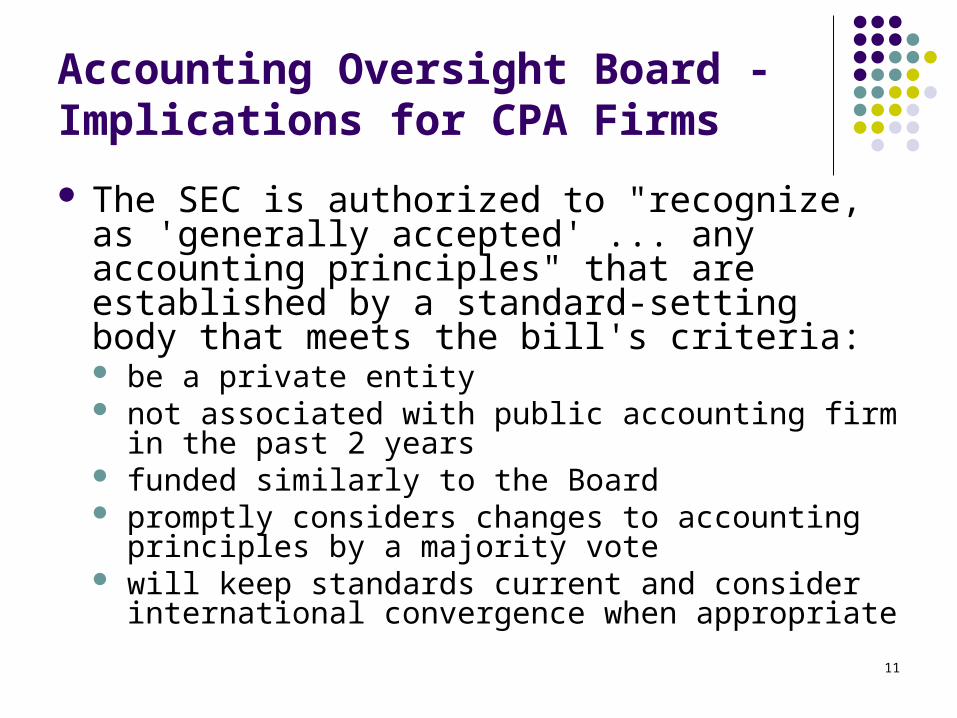

The SEC is authorized to "recognize, as 'generally accepted' ... any accounting principles" that are established by a standard-setting body that meets the bill's criteria: be a private entity not associated with public accounting firm in the past

2 years funded similarly to the Board promptly considers changes to accounting principles

by a majority vote will keep standards current and consider international

convergence when appropriate

12

Accounting Oversight Board - Implications for CPA Firms (con’t)

It shall be "unlawful" for a registered public accounting firm to provide any non-audit service to an issuer contemporaneously with the audit, including:

bookkeeping financial information systems design and implementation appraisal or valuation services, fairness opinions, or contribution-in-kind

reports actuarial services internal audit outsourcing services management functions or human resources broker or dealer, investment adviser, or investment banking services legal services and expert services unrelated to the audit any other service that the Board determines, by regulation, is impermissible

Note: Exemptions may be allowed.

13

Accounting Oversight Board - Implications for Public Companies

Lead auditor and reviewing partner are rotated every 5 years.

Accounting firm must report to Audit Committee and “discuss audit nuts & bolts”.

The CEO, controller, CFO, chief accounting officer may not have been employees of the audit firm within the past year.

State regulators decide adoption for small and mid-size non-registered accounting firms.

14

Accounting Oversight Board - Public Companies (con’t)

Issuers will be assessed a "annual accounting support fee“ based on their relative market capitalization.

Board auditing standards, such as record retention rules, second partner review, and scope of internal control testing, will affect the nature of audits.

Independence standards will limit the non-audit work that auditors can perform.

15

Accounting Oversight Board - Public Companies (con’t)

Company information will be subject to review in inspections of the independent auditor and the company can be required to testify and produce documents in an auditor disciplinary proceeding.

Companies will have to ensure compliance with any sanctions imposed by the Board, such as suspensions of auditors or their personnel from auditing.

16

Audit Committee and Relationship with the Auditor

Audit committee of an issuer: will be adequately funded;

will be directly responsible for the appointment, compensation, and oversight of audit firm;

17

Audit Committee and Relationship with the Auditor

may engage independent counsel or other advisors, as it determines necessary to carry out its duties;

establishes procedures for the "receipt, retention, and treatment of complaints" on accounting, internal controls, and auditing.

18

Audit Committee and Director Responsibilities

Unlawful for an issuer to extend credit to any director or executive officer.

Directors, officers and 10 percent owner must report designated transactions by the end of the 2nd day following the a transaction.

19

Audit Committee and Management Responsibilities

Financial statement certification required.

The CEO and CFO of each issuer will certify the "appropriateness of the financial statements and disclosures contained in the periodic report, and that those financial statements and disclosures fairly present, in all material respects, the operations and financial condition of the issuer."

A violation of this section must be knowing and intentional to give rise to liability.

20

Audit Committee and Management Responsibilities

Officer or director action to fraudulently influence audit results is unlawful.

CEO and the CFO shall "reimburse the issuer for any bonus or other incentive-based or equity-based compensation received" during the twelve months following the issuance or filing of the non-compliant document and "any profits realized from the sale of securities of the issuer" during that period.

Federal courts are authorized to "grant any equitable relief that may be appropriate or necessary for the benefit of investors“ in cases brought by the SEC.

21

Audit Committee and Management Responsibilities

SEC may bar a person from acting as an officer or director of an issuer if conduct "demonstrates unfitness".

Prohibits the purchase or sale of stock by officers and directors and other insiders during blackout periods.

Financial statement reports will now "reflect all material correcting adjustments made by the auditor.

Financial reports will disclose all material off-balance sheet transactions" and "other relationships" with "unconsolidated entities".

The SEC shall issue rules providing that pro forma financial information.

22

Audit Committee and Management Responsibilities

Requires each annual report of an issuer to contain an "internal control report“ that

states that internal control is management’s responsibility

contains an assessment of the effectiveness of the internal control structure/procedures for the reporting period (which the auditor attests to)

contains a disclosure as to whether the issuer has an ethics code in place to guide senior financial management

23

Audit Committee and Disclosure Issues

Issuers must disclose

whether at least one member of its audit committee is a "financial expert.“

material changes in the financial condition or operations of the issuer on a rapid and current basis (real-time disclosure)

24

Corporate Fraud & Accountability Act

It is a FELONY to "knowingly" destroy or create documents to "impede, obstruct or influence" any existing or contemplated federal investigation.

Auditors are required to maintain "all audit or review work papers" for five years.

The statute of limitations on securities fraud claims is now the earlier of three years from the fraud or one year from the discovery.

“Whistle blower protection" is extended to employees of issuers and accounting firms employees.

25

Corporate Fraud & Accountability Act

Legal Ramifications and Criminal Penalties Securities Fraud: to “knowingly defraud any

person in connection with a security” of a public company. Max of 25 years (rather than 5 or 10) 10 – 25 years for an individual $1.0 - $5.0 million in fines for an individual $2.5 - $25 million in fines for a company

Document tampering: 20 years in prison and a fine.

26

SARBANES-OXLEY ACT OF 2002

Approved SEC rules to date:

Mandates Electronic Filing of Ownership Reports; Prohibit Improper Influence of Auditors

Requirements for Listed Company Audit Committees

Codes of Ethics and Audit Committee Expertise Insider Trades During Pension Fund Blackout Periods

Use of Non-GAAP Measures (Pro-Forma & Off-Balance Sheet Disclosures)

MD&A Disclosures of Off-Balance Sheet Items

Visit: http://www.aicpa.org/sarbanes/index.asp

27

SARBANES-OXLEY State Perspective

Maryland Senate Bill 560 was defeated in March 2003. Called for: prohibition on non-audit services, partners

involved in prior audits, and officers who were formerly employed by audit firm

required whistleblower protection provisions employee compensation disclosure to state

procurement and grant agencies

28

SARBANES-OXLEY State Perspective

Virginia has no proposed legislation but active campaigning by interested parties is under way.

DC has no proposed legislation in front of City Council. Non-profit organizations in area may have influence on acceptance.

29

SARBANES-OXLEYViews of Organizations

AICPA – Offers overall support for SEC plan, and promotes its desire to remain involved in the process of governance (Melancon, 2002).

Maryland Association of CPAs – active task

force to improve the profession and assist members in voluntary adoption.

30

SARBANES-OXLEYViews of Organizations

Virginia Society of CPAs – supports ethical behavior, concerns about practicality of application to private companies.

Greater Washington Society of CPAs – believes many practices will be adopted in private and nonprofit sectors without legislative effort.

31

Corporate Stewardship

A matter of ethics.

Pay-for-Performance at root? Social pressure playing a role. The “Golden Business Rule”.