SAP Services Capability

51

Capture Share Report – Asia Pacific SAP Services Providers October, 2012 Authored by Phil Hassey: - Founder capioIT

-

Upload

shamim-sarwar-pappu -

Category

Documents

-

view

13 -

download

0

description

SAP-services-capability

Transcript of SAP Services Capability

Capture Share Report – Asia

Pacific SAP Services Providers

October, 2012 Authored by

Phil Hassey: - Founder capioIT

Capture Share– Asia Pacific SAP

Services Providers

Executive Summary 3

Top-line Methodology 6

Core Findings 10

SAP Capture Share - Vendor Breakdown 22

AP SAP Services Capture Share Final Takeaways 40

Detailed Methodology 43

2 Prepared by capioIT 2/01/2013

Executive Summary

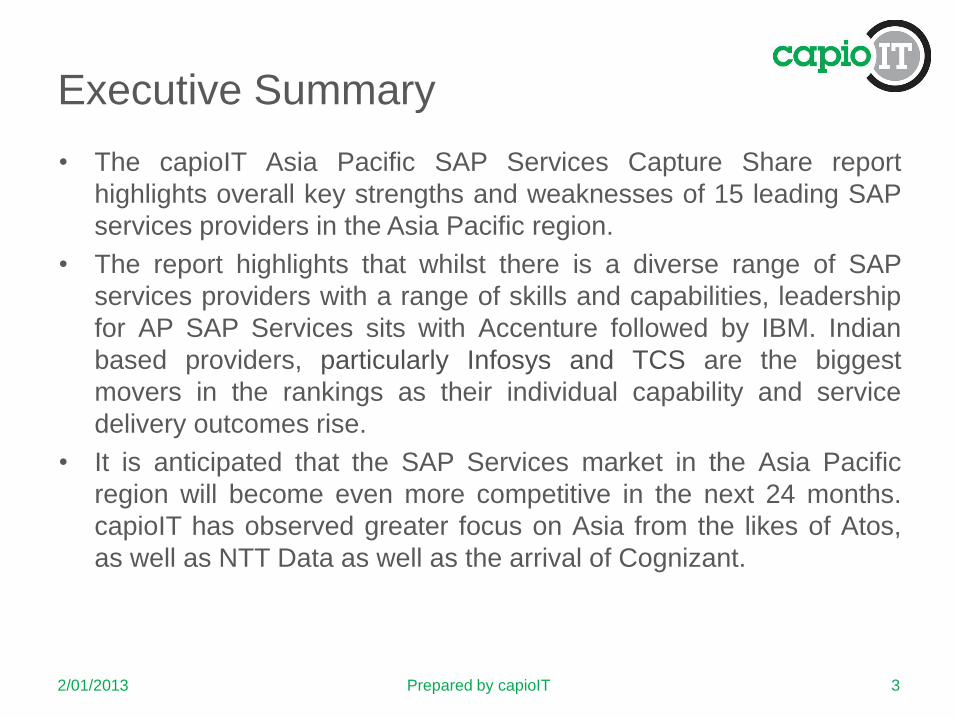

• The capioIT Asia Pacific SAP Services Capture Share report

highlights overall key strengths and weaknesses of 15 leading SAP

services providers in the Asia Pacific region.

• The report highlights that whilst there is a diverse range of SAP

services providers with a range of skills and capabilities, leadership

for AP SAP Services sits with Accenture followed by IBM. Indian

based providers, particularly Infosys and TCS are the biggest

movers in the rankings as their individual capability and service

delivery outcomes rise.

• It is anticipated that the SAP Services market in the Asia Pacific

region will become even more competitive in the next 24 months.

capioIT has observed greater focus on Asia from the likes of Atos,

as well as NTT Data as well as the arrival of Cognizant.

3 Prepared by capioIT 2/01/2013

Executive Summary

• Furthermore the Chinese providers such as Vanceinfo will continue

to emerge, firstly in China, but more broadly as they look to replicate

the Indian provider market.

• Competition is also going to be enhanced by the changing dynamic

of the SAP application portfolio. As this expands through cloud

adoption of existing offerings and acquisitions, it is clear that the

services delivery environment will be particularly disruptive.

• SAP is going to have to work closely with the partners to ensure that

they can maintain the pace of change that is impacting the overall IT

space in the Asia Pacific region. This will be particularly true for

dissemination of IP and R&D as well as optimisation of account and

opportunity management.

4 Prepared by capioIT 2/01/2013

Capture Share– Asia Pacific SAP

Services Providers

Executive Summary 3

Top-line Methodology 6

Core Findings 10

SAP Capture Share - Vendor Breakdown 22

AP SAP Services Capture Share Final Takeaways 40

Detailed Methodology 43

5 Prepared by capioIT 2/01/2013

Top-line Methodology

• Capture Share reports are based on the analysis of 17 key

capabilities and attributes of services providers. These attributes are

focused in two key areas, Transform and Leverage.

• In order to undertake the appropriate level of analysis and data

integrity, the individual attributes are weighted in percentage terms

on the basis of the overall influence for the Transform and Leverage

capabilities.

• Clearly data and process integrity are a critical component of a

report of this type. It is fundamental that the data be valid and

untarnished. To help ensure this, all information for the

measurement and assessment of these attributes comes from a

range of sources to ensure a range of opinions. Sources of

information include vendor briefings and meetings, media sources,

the IT services ecosystem and specific end-user feedback.

• A full methodology is highlighted at the end of this report.

6 Prepared by capioIT 2/01/2013

Methodology – Transform Attributes

• There has been nine attributes

identified by capioIT that

contribute to the measurement

of IT Services providers ability

to transform clients SAP

requirements and provide

leadership in a market.

• As mentioned these attributes

are all weighted to determine

their overall importance. The

weighting is highlighted in the

accompanying table .

• The following section defines

each Transform attribute

2/01/2013 Prepared by capioIT 7

Attribute Weighting

Internal R&D 10%

Leverage SAP R&D 15%

SAP Ecosystem Partnership 8%

Global Solution Development 10%

Industry Solution Development 10%

Country Solution Development 10%

SAP Infrastructure

Implementation 20%

Strength of Brand 7%

Ability to Influence External

Market 10%

Total 100%

Methodology – Leverage Attributes

• There are 8 attributes that

contribute to the measurement

of a IT Services providers

ability to leverage capabilities

to provide scale and efficiency

to clients.

• These attributes are all

weighted to highlight their

overall importance. The

weighting is highlighted below.

• The following section defines

each Leverage attribute

2/01/2013 Prepared by capioIT 8

Attribute Weighting

Asia Pacific SAP Services

Revenue 14%

Portfolio Depth 18%

Dedicated SAP Services

headcount 11%

In Country Strength 15%

Salesforce Strength 11%

Delivery Partnerships 10%

In Country Geographic Reach 8%

Country Localisation 13%

Total 100%

Capture Share– Asia Pacific SAP

Services Providers

Executive Summary 3

Top-line Methodology 6

Core Findings 10

SAP Capture Share - Vendor Breakdown 22

AP SAP Services Capture Share Final Takeaways 40

Detailed Methodology 43

9 Prepared by capioIT 2/01/2013

SAP Capture Share – 2012 Findings

10 Prepared by capioIT 2/01/2013

IBM

HP

CSC

Atos

Accenture

Fujitsu

UXC

Wipro

Cognizant

TCS

Deloitte

Infosys

HCL

Capgemini

Vanceinfo

Tra

ns

form

Leverage

Transform Focus

Leverage Focus

Market Maker

Market Developer

SAP Capture Share Leverage Findings

2/01/2013 Prepared by capioIT 11

• This section highlights the results of each leverage attribute for the AP SAP Services market.

• Clearly the region can be considered to have an inconsistent level of maturity and scale from the provider perspective. As a result there is no surprise that AP SAP Services Revenue is the weakest attribute.

• Revenue aside, Overall the results largely cluster. Whilst this is in part due to the number being an average, it does highlight that differentiation comes from doing specific measures well. This could include delivery partnerships or country localisation..

Leverage Attribute Average Score

Asia Pacific SAP Services

Revenue

5.4

Portfolio Depth 6.7

No. of dedicated SAP

Services headcount

6.2

Country Strength 6.5

Salesforce strength 6.4

Delivery Partnerships 6.4

In Country Geographic Reach 6.3

Country localisation 6.3

SAP Capture Share Leverage Findings for

Vendors

2/01/2013 Prepared by capioIT 12

• The average scores for leverage for the vendors is highlighted. The average score or rating is 6.3. Accenture had the highest score at 7.5. It was closely followed by IBM at 7.4. This highlights the overall scale and volume that these two vendors are able to provide comparatively consistently across the region.

• Atos was identified as having the most limited capability for leverage. It’s average score was 4.9.

• HCL was the most limited of the Indian providers with an average score of 6.3.

• The results reinforce that the scale for delivery in the region is helped by a core global delivery infrastructure.

Vendor

Vendor

Leverage

Rating

Accenture 7.5

IBM 7.4

TCS 7.0

Infosys 6.8

HP 6.7

Wipro 6.6

Fujitsu 6.6

CSC 6.4

Capgemini 6.3

HCL 6.3

UXC 5.9

Deloitte 5.8

Cognizant 5.3

Vanceinfo 5.0

Atos 4.9

Average Rating 6.3

SAP Capture Share Transform Findings

2/01/2013 Prepared by capioIT 13

• This section highlights the results of each transform attribute for the AP SAP Services market.

• The strongest attribute was the ability to leverage SAP R&D. This is not surprising and reflects on both SAP and the partner environment. However, work needs to be done by vendors focusing on developing their own R&D.

• Whilst the global and industry solution development results are strong, there is a real need to focus more energy on developing solutions that are country specific. This is still a high customer demand area.

Transform Average Score

Internal R&D 6.2

Leverage SAP R&D 6.8

SAP Ecosystem Partnership 6.6

Global Solution Development 6.7

Industry Solution

Development 6.7

Country Solution

Development 6.3

SAP Infrastructure

Implementation 6.1

Strength of Brand 6.2

Ability to influence external

market 6.2

SAP Capture Share Transform Findings

2/01/2013 Prepared by capioIT 14

• This section outlines the transform scores for selected vendors in the Asia Pacific SAP Services market.

• The average score or rating is 6.4. Accenture had the number one position with a score of 7.2 This was followed by Infosys and Capgemini on 6.9.

• Vanceinfo was the poorest performer in this classification with an average score for leverage of 4.5.

• Clearly IP development in all its forms is a critical metric for the ability to transform the client agenda. It also requires the development of an ecosystem approach to SAP service delivery.

Vendor

Vendor

Transform

Rating

Accenture 7.2

Capgemini 7.0

Infosys 7.0

IBM 6.9

TCS 6.8

Fujitsu 6.8

Wipro 6.6

HP 6.6

CSC 6.6

HCL 6.4

Deloitte 6.3

Cognizant 5.9

Atos 5.8

UXC 5.5

Vanceinfo 4.5

Average Rating 6.4

Leverage to Transform Ratio

2/01/2013 Prepared by capioIT 15

• The Leverage To Transform Ratio

is another way to test the relative

strengths of a services provider.

• A negative delta indicates firms

have a stronger transform

capability. Conversely, a positive

delta indicates a stronger leverage

capability.

• A high delta percentage indicates

an imbalanced capability between

the ability to transform a client and

leverage capabilities.

• capioIT believe that a believe that a

delta score of > +/-7.5% is of

concern for a vendor.

Vendor

Leverage to

Transform Ratio

Vanceinfo 9.7%

UXC 7.2%

IBM 6.5%

Accenture 5.2%

TCS 1.9%

HP 1.1%

Wipro -0.4%

HCL -1.6%

Infosys -2.5%

Fujitsu -3.1%

CSC -3.6%

Deloitte -7.8%

Cognizant -8.9%

Capgemini -10.0%

Atos -15.3%

Total 2.8%

SAP Capture Share Overall Findings -

Market Makers

Accenture

• Accenture is the leader in the Asia

Pacific SAP Services marketplace.

It is consistently strong and has

provided a deep level of client

capability for several years and

across the region.

• It leads in a range of categories

from portfolio depth, sales force

strength, industry solution

development and the ability to

influence the market.

IBM

• IBM has a large level and depth of

capability in SAP services across

the region. As the analysis

indicates, it was very close call for

leadership in this market.

• It has leadership in the strength of

the brand for SAP services as well

as for SAP Infrastructure

Implementations

2/01/2013 Prepared by capioIT 16

SAP Capture Share Overall Findings -

Market Makers

Infosys • Infosys has had particular focus

on enhancing the “transform”

capability in the past 12-24

months for SAP Services. This

has created the capability that

means It is not just a scale

provider.

• It has made considerable

progress in developing asset

based solutions for customers.

This has been undertaken with a

focus on internal R&D integrated

with SAP R&D.

TCS

• TCS has matured with a strong pan regional approach to SAP capability. It has strong presence in three of the five major regions.

• It has also driven an increase focus on IP not just delivery scale.

• It also enjoys broader in country geographic reach than many of the other Indian based provider.

2/01/2013 Prepared by capioIT 17

SAP Capture Share Overall Findings

Market Makers

• SAP – SAP has to draw a fine balance between its own capabilities

in services and not cannibalising partner revenue. Clearly the

strength for it is in consulting and emerging SAP solutions.

• Capgemini – Clearly Capgemini does not have the scale in the Asia

Pacific region it has in Europe, but it has strength particularly from a

transformational perspective. It needs further scale to reach

potential in the region.

• Fujitsu – Fujitsu has a long history and has made acquisitions

particularly in Australia to enhance its SAP presence. However

capability is not consistent across the Asia Pacific region.

2/01/2013 Prepared by capioIT 18

SAP Capture Share Overall Findings

Leverage Focus

• HP – HP has a slight leverage focus. The overall SAP practice post

EDS acquisition has deteriorated. It has a lack of industry focus and

is reliant upon capability being driven from the strength it has in

delivery of SAP infrastructure on the HP platform. It needs to invest

in industry capability and R&D to re-capture the strength the EDS

and HP components used to provide customers.

• Wipro – Wipro is increasing, but needs to shift the perception that it

has a “body shop” focus to a more strategic capability. Increased

investment in SAP consulting will be critical for driving this.

2/01/2013 Prepared by capioIT 19

SAP Capture Share Overall Findings

Transform Focus

• Capgemini – Capgemini leads in some key areas of the Asia Pacific

Services market for SAP. However, it lacks scale across the region,

and needs to invest more significantly to grow in capability.

• HCL – HCL have made investments in key markets through Axon.

They still need to grow in scale and capability but have made SAP a

corporate focus.

• CSC – Key investments by CSC in the Mining and Resources

industries in addition to Public Sector is important for its ongoing

success. The clear limitation is the lack of scale in Asia in general,

and for SAP in the region.

• Fujitsu – Fujitsu is really two business in the AP market (excluding

Japan). In Australia it is one of the leaders in the market. In the rest

of the region it lags behind other providers. Investment in AP is well

overdue across the offerings of Fujitsu, not just in SAP.

2/01/2013 Prepared by capioIT 20

SAP Capture Share Overall Findings

Market Developer Focus

• Market Developers include

– Cognizant

– Deloitte

– Vanceinfo

– UXC

– HCL

• The key challenge for the market developers is scale. Without it they

have limited Asia Pacific wide coverage and the ability to offer depth

in vertical markets.

• This applies to both local AP based providers such as Vanceinfo and

UXC as well as global players such as Atos and Deloitte.

2/01/2013 Prepared by capioIT 21

Capture Share– Asia Pacific SAP

Services Providers

Executive Summary 3

Top-line Methodology 6

Core Findings 10

SAP Capture Share - Vendor Breakdown 22

AP SAP Services Capture Share Final Takeaways 40

Detailed Methodology 43

22 Prepared by capioIT 2/01/2013

SAP Capture Share - Vendor

Breakdown

• The following section highlights the performance of key vendors to

further understand their strengths and weaknesses.

• Analysis of the strengths and weaknesses is undertaken to

determine the core requirements from a competitive point of view.

• The relative capability is also highlighted. For firms that score above

the overall average, this is highlighted by a +

• Conversely, firms that score below the average are highlighted by a

–

• Where firms scores can not be split, indication of relative strength or

weakness is highlighted by the distance from the average for all

firms. That is, relatively higher scores are indicated as strengths.

Relatively lower scores are indicated as weaknesses.

2/01/2013 Prepared by capioIT 23

SAP Capture Share - Vendor

Breakdown

• If this provides identical results, values are then weighted by the

overall importance of each attribute. For example, if a firm has

identical scores for Strength of Brand and Ability to Influence the

External Market, the weighting of Ability to Influence the External

Market at 10%, vs. 6% for Strength of Brand will indicate that Ability

to Influence the External Market would be listed as a strength or

weakness.

2/01/2013 Prepared by capioIT 24

Accenture AP SAP Services Capability

Top Three Leverage Strengths

• Salesforce Strength +

• Asia Pacific SAP Services

Revenue +

• Dedicated SAP headcount +

Top Three Transform

Weaknesses

• Country Solution Development -

• SAP Ecosystem Partnerships +

• SAP Infrastructure Implementation +

2/01/2013 Prepared by capioIT 25

Top Three Leverage

Weaknesses

• Delivery Partnerships -

• In Country Geographic Reach +

• Country Localisation +

Top Three Transform Strengths

• Ability to Influence External

Market +

• Global Solution Development +

• Industry Solution Development +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

IBM AP SAP Services Capability

Top Three Leverage Strengths

• Number of Dedicated SAP

Services Headcount +

• Portfolio Depth+

• Asia Pacific SAP Services

Revenue +

Top Three Transform

Weaknesses

• Country Solution Development +

• Leverage SAP R&D -

• SAP Ecosystem Partnerships -

2/01/2013 Prepared by capioIT 26

Top Three Leverage

Weaknesses

• Delivery Partnerships -

• In Country Geographic Reach +

• Country Localisation +

Top Three Transform Strengths

• SAP Infrastructure

Implementation +

• Industry Solution Development +

• Ability to Influence External Market

+

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Infosys AP SAP Services Capability

Top Three Leverage Strengths

• Asia Pacific SAP Services Revenue +

• Dedicated SAP Services Headcount +

• Salesforce Strength +

Top Three Transform Weaknesses

• SAP Ecosystem Partnerships +

• Country Solution Development +

• SAP Infrastructure Implementation

+

2/01/2013 Prepared by capioIT 27

Top Three Leverage

Weaknesses

• In Country Geographic Reach –

• Country Localisation +

• Portfolio Depth +

Top Three Transform Strengths

• Internal R&D +

• Strength of Brand +

• Ability to Influence the Market +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

TCS AP SAP Services Capability

Top Three Leverage Strengths

• No. Of Dedicated SAP Services Headcount +

• Asia Pacific SAP Services Revenue +

• Salesforce Strength +

Top Three Transform Weaknesses

• Country Solutions Development +

• Leverage SAP R&D +

• SAP Infrastructure Implementation

–

2/01/2013 Prepared by capioIT 28

Top Three Leverage Weaknesses

• In Country Geographic Reach +

• Portfolio Depth +

• Country Localisation +

Top Three Transform Strengths

• Internal R&D +

• Ability to Influence the External Market

+

• Strength of Brand +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Wipro AP SAP Services Capability

Top Three Leverage Strengths

• Asia Pacific SAP Services Revenue +

• No. Of Dedicated SAP Services Headcount +

• Country Strength +

Top Three Transform Weaknesses

• Country Solution Development –

• SAP Ecosystem Partnerships –

• Ability to Influence the External

Market –

2/01/2013 Prepared by capioIT 29

Top Three Leverage

Weaknesses

• In Country Geographic Reach –

• Country Localisation –

• Salesforce Strength –

Top Three Transform Strengths

• Internal SAP R&D +

• Strength of Brand +

• Industry Solution Development +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

HP AP SAP Services Capability

Top Three Leverage Strengths

• Delivery Partnerships +

• Country Strength +

• In Country Geographic Reach +

Top Three Transform Weaknesses

• Industry Solution Development –

• Strength of Brand -

• Global Solution Development -

2/01/2013 Prepared by capioIT 30

Top Three Leverage Weaknesses

• Salesforce Strength +

• Country Localisation +

• Portfolio Depth +/-

Top Three Transform Strengths

• SAP Ecosystem +

• Internal R&D +

• SAP Infrastructure

implementation +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Fujitsu AP SAP Services Capability

Top Three Leverage Strengths

• Asia Pacific SAP Services Revenue+

• In Country Geographic Reach +

• No. Of Dedicated SAP Services Headcount +

Top Three Transform Weaknesses

• Ability to Influence Market -

Industry Solution -

• Global Solution +

2/01/2013 Prepared by capioIT 31

Top Three Leverage Weaknesses

• Portfolio Depth +/ –

• Country Strength –

• Salesforce Strength –

Top Three Transform Strengths

• SAP Infrastructure Implementation +

• Country Solution Development +

• SAP Ecosystem Partnership +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Capgemini AP SAP Services Capability

Top Three Leverage Strengths

• Delivery Partnerships +

• Portfolio Depth +

• Salesforce Strength +

Top Three Transform Weaknesses

• Strength of Brand +

• Internal SAP R&D +

• Country Solutions +

2/01/2013 Prepared by capioIT 32

Top Three Leverage

Weaknesses

• Country Strength –

• Asia Pacific SAP Services

Revenue –

• In Country Geographic Reach –

Top Three Transform Strengths

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

• Industry Solutions +

• Ability to Influence External Market

+

• Global Solutions +

CSC AP SAP Services Capability

Top Three Leverage Strengths

• Asia Pacific SAP Services Revenue +

• Portfolio Depth +

• Delivery Partnerships +

Top Three Transform

Weaknesses

• SAP Ecosystem Partnership -

• Strength of Brand -

• Internal R&D -

2/01/2013 Prepared by capioIT 33

Top Three Leverage

Weaknesses

• Number of Dedicated SAP

Services Headcount -

• In Country Geographic Reach -

• Country Strength -

Top Three Transform Strengths

• SAP Infrastructure Implementation

+

• Country Solutions +

• Industry Solutions +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Deloitte AP SAP Services Capability

Top Three Leverage Strengths

• Salesforce Strength +

• Country Localisation +

• Portfolio Depth +/-

Top Three Transform Weaknesses

• SAP Infrastructure Implementation

–

• Country Solutions –

• SAP Ecosystem Partnerships –

2/01/2013 Prepared by capioIT 34

Top Three Leverage

Weaknesses

• AP SAP Services Revenue –

• Country Strength –

• Delivery Partnerships –

Top Three Transform Strengths

• Strength of Brand +

• Internal SAP R&D +

• Industry Solution Development +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

UXC AP SAP Services Capability

Top Three Leverage Strengths

• Country Strength +

• In Country Geographic Reach +

• Country Localisation +

Top Three Transform Weaknesses

• Ability to Influence Market –

• Global Solution Development –

• Industry Solution Development –

2/01/2013 Prepared by capioIT 35

Top Three Leverage Weaknesses

• No. Of Dedicated SAP Services Headcount –

• Asia Pacific SAP Services Revenue –

• Salesforce Strength –

Top Three Transform Strengths

• Country Solution Development +

• Leverage SAP R&D +/–

• SAP Ecosystem Partnerships –

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

HCL AP SAP Services Capability

Top Three Leverage Strengths

• No. Of Dedicated SAP Services

Headcount +

• Salesforce Strength +

• Portfolio Depth +

Top Three Transform Weaknesses

• SAP Ecosystem Partnerships –

• Leverage SAP R&D –

• Strength of Brand –

2/01/2013 Prepared by capioIT 36

Top Three Leverage

Weaknesses

• Delivery Partnerships –

• Country Localisation –

• In Country Geographic Reach –

Top Three Transform Strengths

• SAP Infrastructure Implementation +

• Internal SAP R&D +

• Global Solution Development +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Cognizant AP SAP Services Capability

Top Three Leverage Strengths

• No. Of Dedicated SAP Services

Headcount –

• Salesforce Strength –

• Delivery Partnerships –

Top Three Transform Weaknesses

• Country Solution Development –

• Strength of Brand–

• SAP Infrastructure Implementation

–

2/01/2013 Prepared by capioIT 37

Top Three Leverage

Weaknesses

• Asia Pacific SAP Services

Revenue –

• In Country Geographic Reach –

• Country Localisation –

Top Three Transform Strengths

• SAP Ecosystem Partnership +

• Global Solution Development +

• Internal R&D +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Atos AP SAP Services Capability

Top Three Leverage Strengths

• In Country Geographic Reach –

• Country Localisation –

• Salesforce Strength –

Top Three Transform Weaknesses

• Internal R&D –

• Strength of Brand–

• Ability to Influence the External

Market –

2/01/2013 Prepared by capioIT 38

Top Three Leverage

Weaknesses

• Asia Pacific SAP Services Revenue –

• Number of Dedicated SAP Services Headcount –

• Country Strength –

Top Three Transform Strengths

• Leverage SAP R&D + /–

• Global Solution Development +

• Industry Solution Development +

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Vanceinfo AP SAP Services Capability

Top Three Leverage Strengths

• Country Strength +

• Country Localisation +

• Delivery Partnerships –

Top Three Transform Weaknesses

• Internal R&D –

• Global Solution Development –

• Strength of Brand –

2/01/2013 Prepared by capioIT 39

Top Three Leverage

Weaknesses

• Asia Pacific SAP Services Revenue –

• Dedicated AP SAP Service Headcount –

• Portfolio Depth –

Top Three Transform Strengths

• SAP Ecosystem Partnership –

• Ability to Influence Market –

• Country Solution Development –

Note + indicates a capability rated above the average

- indicates a capability rated below the average

Bold indicates Market Leader

Capture Share– Asia Pacific SAP

Services Providers

Executive Summary 3

Top-line Methodology 6

Core Findings 10

SAP Capture Share - Vendor Breakdown 22

AP SAP Services Capture Share Final Takeaways 40

Detailed Methodology 43

40 Prepared by capioIT 2/01/2013

AP SAP Services Capture Share

Final Takeaways • Overall the SAP Services market in the Asia Pacific region is in a

healthy state of maturity. It varies by country of course, ANZ is the

strongest sub-region, with Singapore, China and Korea all key

geographies. India, the Philippines and China as well as Indonesia

represent key growth opportunities for SAP in the region.

• Accenture is the leading SAP Services provider in the Asia Pacific

region. It is closely followed by IBM. There is a gap to the next level

of contenders.

• Accenture and IBM’s success is due to more than just the scale

available for clients SAP requirements. They are able to develop

solutions for clients based on industry and geographic parameters

as well as driving SAP specific R&D into solutions. Opportunities

include working better with the SAP ecosystem, and a need to

improve geographic reach in smaller Indian and Chinese cities.

Prepared by capioIT 41 2/01/2013

• SAP has kept a reasonable balance in terms of services capabilities.

It needs to ensure that it is able to maintain this focus and balance

moving forward. It cannot afford to alienate partners in light of the

dramatic change to the market for procurement of ERP related

solutions. SAP needs to take the lead to help fast track SAP enabled

professionals to ensure that the skills gap is managed.

• HP has particular strength in SAP from an infrastructure point of

view. It needs to leverage EDS and the end to end HP capability

more strategically.

• Providers such as Fujitsu and CSC struggle with a lack of consistent

regional scale. They are strong in Australia, and patchy in other

markets.

• The Indian providers have not had the same success in the Asia

Pacific region that they have experienced in other markets. They

need to quickly leverage their strong reputation to scale in Asia

Pacific client delivery. Prepared by capioIT 42 2/01/2013

AP SAP Services Capture Share

Final Takeaways

Capture Share– Asia Pacific SAP

Services Providers

Executive Summary 3

Top-line Methodology 6

Core Findings 10

SAP Capture Share - Vendor Breakdown 22

AP SAP Services Capture Share Final Takeaways 40

Detailed Methodology 43

43 Prepared by capioIT 2/01/2013

Methodology – Transform Attributes

• There has been nine attributes

identified by capioIT that

contribute to the measurement

of IT Services providers ability

to transform clients SAP

requirements and provide

leadership in a market.

• As mentioned these attributes

are all weighted to determine

their overall importance. The

weighting is highlighted in the

accompanying table .

• The following section defines

each Transform attribute

2/01/2013 Prepared by capioIT 44

Attribute Weighting

Internal R&D 10%

Leverage SAP R&D 15%

SAP Ecosystem Partnership 8%

Global Solution Development 10%

Industry Solution Development 10%

Country Solution Development 10%

SAP Infrastructure

Implementation 20%

Strength of Brand 7%

Ability to Influence External

Market 10%

Total 100%

Methodology – Transform Attributes

• Internal SAP R&D

– The depth of investment by an enterprise in SAP related Research and

Development, linked with the successful development of solutions and

customer outcomes from the Research and Development

• Leverage SAP R&D

– The ability to leverage SAP Research and Development to both offer

solutions for the enterprise and for SAP. This requires development of

solutions and customer outcomes.

• SAP Ecosystem Partnership

– The ability to develop, maintain and maximise value of partnerships with

other SAP related entities to ensure that customer outcomes are

maximised.

• Global Solution Development

– Development of globally relevant and differentiated service or solution

offerings

45 Prepared by capioIT 2/01/2013

Methodology – Transform Attributes

• Industry Solution Development

– Development of industry based relevant and differentiated service or

solution offerings.

• Country Solution Development

– Development of country (or sub-region) based relevant and

differentiated service or solution offerings.

• SAP Infrastructure Implementation

– Ability to provide infrastructure solutions for SAP deployment based

upon a vendors, or partners hardware capabilities.

• Strength of Brand

– The strength and value of the brand to determine the scope of

awareness of the service provider and its offerings.

• Ability to influence external market

– The ability through thought leadership, executive engagement and

depth of proven delivery capability to influence the general and specific

direction of the SAP Services marketplace.

46 Prepared by capioIT 2/01/2013

Methodology – Leverage Attributes

• There are 8 attributes that

contribute to the measurement

of a IT Services providers

ability to leverage capabilities

to provide scale and efficiency

to clients.

• These attributes are all

weighted to highlight their

overall importance. The

weighting is highlighted below.

• The following section defines

each Leverage attribute

2/01/2013 Prepared by capioIT 47

Attribute Weighting

Asia Pacific SAP Services

Revenue 14%

Portfolio Depth 18%

Dedicated SAP Services

headcount 11%

In Country Strength 15%

Salesforce Strength 11%

Delivery Partnerships 10%

In Country Geographic Reach 8%

Country Localisation 13%

Total 100%

Methodology – Leverage Attributes

• Asia Pacific SAP Services Revenue

– Level of total revenue for IT related services in the Asia Pacific Region

• Portfolio Depth

– The depth of SAP services portfolio and capability. Key Services areas

include

• SAP Infrastructure Services

• SAP Application Management Services

• SAP Application Support and Integration Services

• SAP Hosted Services

• SAP Consulting

48 Prepared by capioIT 2/01/2013

Methodology – Leverage Attributes

• Dedicated SAP Services headcount

– The number of dedicated SAP services headcount in the region. These

are offshore and onshore resources as appropriate, but must be

focused on the region.

• In Country Strength

– SAP capability in the various markets of Asia Pacific at a country level,

key regions follow;

• ASEAN

• Australia and New Zealand

• Greater China

• India

• Korea

49 Prepared by capioIT 2/01/2013

Methodology – Leverage Attributes

• Salesforce Strength

– Depth of capability for the SAP service provider sales force. This is both from a commoditised services point of view as well as the higher order consultative sales capabilities.

• Delivery Partnerships

– The depth and capability of SAP delivery partnerships to ensure high quality of delivery capability for customers

• In country Geographic Reach

– The ability to deliver national capability across geographically dispersed markets. Key markets in Asia Pacific with this requirement are Australia, India and the PRC, but it is also relevant in markets such as Malaysia and Indonesia

• Country Localisation

– The ability to provide local capabilities in country to acknowledge local capabilities and requirements from a cultural, regulatory and governance perspective.

50 Prepared by capioIT 2/01/2013

For Further Information

Phil Hassey: - Founder capioIT

Blog – http://capioit.wordpress.com

Twitter - phassey

www.capioIT.com

Ph - +61 422 231 793

![[SAP] Perforce Administrative Self Services at SAP](https://static.fdocuments.us/doc/165x107/5454eef1af7959f56f8b4b33/sap-perforce-administrative-self-services-at-sap-5584af27d84f8.jpg)