SAMP Company Report

17

COMPANY UPDATE 1 | P age July 2014, Sri Lanka Equity Research Sampath Bank Softlogic Stockbrokers (Pvt) Ltd #06,37 th Lane, Queens Road Colombo 03, Sri Lanka +94 11 7277000 [email protected] Lead Analyst : Kavindu Ranasinghe Secondary Analyst : Asanka Ranasinghe Third Largest Private Commercial Bank offers good value on 1.0X PBV. The share offers good value trading on book value whilst at 7.5x 2014E net profit and 6.5x 2015 Earnings. At present SAMP accounts for approximately 7.4% of the market share among commercial banks in Sri Lanka with a total asset base of LKR387.6 bn and a branch network of 213. Furthermore the Bank is well renowned for the introduction of innovative practices to the banking industry. SAMP has been able to grow its core banking earnings at a CAGR of c.20% over the last decade. However in 2013 Sampath witnessed a notable decline in bottom line due to impairments as a result of the decline in global gold prices (in 2012 bank had a 25% exposure to pawning). However gold prices have been stable during 2014 and also the bank has been able to reduce the pawning exposure to 17% by 1Q14. In addition we expect a 38% dividend payout for 2014E and 2015E generating a dividend yield of of 5.1% and 6.2% respectively. As per our previous banking update (17 th June 2014), a price upside of 24% was forecasted when the price was at LKR190.9. Since then the price moved north to record a gain of 8.7% as of today. We believe there is further 15% upside and we recommend maintain BUY. Loan book is expected to pick up supported by corporate sector. SAMP witnessed a strong growth in its loan book by 25% in 2013, the highest growth levels among licensed commercial bank during the period, due to the strong growth recorded in the corporate book. Bank’s corporate banking portfolio (accounts c. 34% of the loan book) grew strongly by 38% YoY. We expect credit activity to pick up from 2H2014 where we expect Sampath to further increase corporate sector book to areas where domestic economic growth is expected to fuel from. These areas include Energy, tourism, trade and infrastructure sectors. Asset quality is expected to improve. Sampath has been able to maintain one of the lowest NPL ratios over the years due to the centralized credit appraisal system. However in 2013 the bank saw a c.60 bps increase in NPL ratio to 2.7%. This was mainly due to the decline in global gold prices which resulted in a notable impairment in the pawning related advances. However we expect impairment charges on pawning to decline going forward given SAMP has already recognized most of the losses in the portfolio in 2013. In addition prudent measures taken by bank to minimize the risk arising from the pawning portfolio is also expected to reduce impairment charges which include immediate auctioning of pawning articles which are not redeemed after one year, lesser loan to value ratio on pawning and also the efforts made to reduce the exposure to pawning products. Expected reduction in cost/income ratio. SAMP cost/income (ex.prov) ratio increased to 54.4% in 2013 (cf. 51.5% in 2012) due to the drop in non-interest income as a result of the drop in FCBU gains during the year. In addition during the year bank carried out an island-wide programe to upgrade the interior design of all the branches to a consistent standard which further increased cost to income ratio. We believe the bank would be able to maintain cost/income below 55% in the medium term given the low cost branch model the bank operates. The bank currently has one of the lowest staff per branch ratio in the industry (11 staff per branch). In addition given the likely absence of major upgrades in branches going forward and the moderation of branch expansion we expect further improvement in cost/income ratio. Key risks. Sampath Bank currently has a 17% exposure to pawning in the loan book (LKR44.8 bn). Hence bank’s bottom line is susceptible fluctuation in global gold prices. A notable downtrend in gold prices could result in pawning related impairments as witnessed in 2013. Furthermore with the policy of auctioning articles which are not redeemed within one year could also result in interest losses. As a result this could adversely impact banks bottom-line. SHARE INFO N - 12 Month (High/ Low) 211.5/ 161.6 NV- 12 Month (High/ Low) N- Price Chg (1m/ 1Q/1Y) 10.2 /12.2/ 9.3 NV-Price Chg (1m/ 1Q/1Y) Market Cap. (LKR bn) 34.4 Market Cap. (USD mn) 261.0 Avg. Daily T/O (LKR mn) 15.7 Avg. Daily T/O (USD ‘000) 119.3 N - Issued Shares 167.9 NV - Issued Shares Free Float (%) 54.0 VOTING SHAREHOLDERS As at 31 st March ’14 Vallibel One PLC 14.9% Employees Provident Fund 9.9% Mr. Y.S.H.I. Silva 9.9% Rosewood (Pvt) Ltd 6.8% MATTHEWS International Funds 4.2% Caravel Fund (International) Ltd 2.8% Employees' Trust Fund 2.7% SHARE PRICE CHART 150 160 170 180 190 200 210 220 8-Jul-13 27-Aug-13 16-Oct-13 5-Dec-13 24-Jan-14 15-Mar-14 4-May-14 23-Jun-14 (LKR) Expanding into high growth areas… Rating: BUY Ticker : SAMP.SL;LKR209.00 EARNINGS FORECAST YE 31 Dec/ (LKR mn) 2011 2012 2013 2014E 2015E Net Profit (LKR mn) 3,683.3 5,436.7 3,635.0 4,678.9 5,754.8 YoY growth (%) 5.7% 47.6% -33.1% 28.7% 23.0% EPS (LKR) 21.9 32.4 21.7 27.9 34.3 YoY growth (%) 5.7% 47.6% -33.1% 28.7% 23.0% PER (x) 4.5 6.0 9.7 7.5 6.1 DPS (LKR) 9.0 12.0 8.0 10.6 13.0 Div Yield (%) 4.3% 5.7% 3.8% 5.1% 6.2% BVPS (LKR) 135.9 165.4 188.7 218.0 239.2 PBV (x) 1.5 1.3 1.1 1.0 0.9 ROE (%) 16.1% 19.6% 11.5% 12.8% 14.3% Recurrent Basis Net Profit (LKR mn) 3,683.3 4,975.9 3,635.0 4,678.9 5,754.8 YoY growth (%) 24.7% 35.1% -26.9% 28.7% 23.0% EPS (LKR) 21.9 29.6 21.7 27.9 34.3 YoY growth (%) 24.7% 35.1% -26.9% 28.7% 23.0% PER (x) 9.5 7.1 9.7 7.5 6.1

-

Upload

randora-lk -

Category

Documents

-

view

516 -

download

0

Transcript of SAMP Company Report

COMPANY UPDATE

1 | P a g e July 2014, Sri Lanka Equity Research

Sampath Bank

Softlogic Stockbrokers (Pvt) Ltd #06,37

th Lane, Queens Road

Colombo 03, Sri Lanka +94 11 7277000

Lead Analyst : Kavindu Ranasinghe

Secondary Analyst : Asanka Ranasinghe

Third Largest Private Commercial Bank offers good value on 1.0X PBV. The share offers good value trading on book value whilst at 7.5x 2014E net profit and 6.5x 2015 Earnings. At present SAMP accounts for approximately 7.4% of the market share among commercial banks in Sri Lanka with a total asset base of LKR387.6 bn and a branch network of 213. Furthermore the Bank is well renowned for the introduction of innovative practices to the banking industry. SAMP has been able to grow its core banking earnings at a CAGR of c.20% over the last decade. However in 2013 Sampath witnessed a notable decline in bottom line due to impairments as a result of the decline in global gold prices (in 2012 bank had a 25% exposure to pawning). However gold prices have been stable during 2014 and also the bank has been able to reduce the pawning exposure to 17% by 1Q14. In addition we expect a 38% dividend payout for 2014E and 2015E generating a dividend yield of of 5.1% and 6.2% respectively. As per our previous banking update (17

th June 2014), a price upside of 24% was

forecasted when the price was at LKR190.9. Since then the price moved north to record a gain of 8.7% as of today. We believe there is further 15% upside and we recommend maintain BUY.

Loan book is expected to pick up supported by corporate sector. SAMP witnessed a strong growth in its loan book by 25% in 2013, the highest growth levels among licensed commercial bank during the period, due to the strong growth recorded in the corporate book. Bank’s corporate banking portfolio (accounts c. 34% of the loan book) grew strongly by 38% YoY. We expect credit activity to pick up from 2H2014 where we expect Sampath to further increase corporate sector book to areas where domestic economic growth is expected to fuel from. These areas include Energy, tourism, trade and infrastructure sectors.

Asset quality is expected to improve. Sampath has been able to maintain one of the lowest NPL ratios over the years due to the centralized credit appraisal system. However in 2013 the bank saw a c.60 bps increase in NPL ratio to 2.7%. This was mainly due to the decline in global gold prices which resulted in a notable impairment in the pawning related advances. However we expect impairment charges on pawning to decline going forward given SAMP has already recognized most of the losses in the portfolio in 2013. In addition prudent measures taken by bank to minimize the risk arising from the pawning portfolio is also expected to reduce impairment charges which include immediate auctioning of pawning articles which are not redeemed after one year, lesser loan to value ratio on pawning and also the efforts made to reduce the exposure to pawning products.

Expected reduction in cost/income ratio. SAMP cost/income (ex.prov) ratio increased to 54.4% in 2013 (cf. 51.5% in 2012) due to the drop in non-interest income as a result of the drop in FCBU gains during the year. In addition during the year bank carried out an island-wide programe to upgrade the interior design of all the branches to a consistent standard which further increased cost to income ratio. We believe the bank would be able to maintain cost/income below 55% in the medium term given the low cost branch model the bank operates. The bank currently has one of the lowest staff per branch ratio in the industry (11 staff per branch). In addition given the likely absence of major upgrades in branches going forward and the moderation of branch expansion we expect further improvement in cost/income ratio.

Key risks. Sampath Bank currently has a 17% exposure to pawning in the loan book (LKR44.8 bn). Hence bank’s bottom line is susceptible fluctuation in global gold prices. A notable downtrend in gold prices could result in pawning related impairments as witnessed in 2013. Furthermore with the policy of auctioning articles which are not redeemed within one year could also result in interest losses. As a result this could adversely impact banks bottom-line.

SHARE INFO

N - 12 Month (High/ Low) 211.5/ 161.6

NV- 12 Month (High/ Low)

N- Price Chg (1m/ 1Q/1Y) 10.2 /12.2/ 9.3

NV-Price Chg (1m/ 1Q/1Y)

Market Cap. (LKR bn) 34.4

Market Cap. (USD mn) 261.0

Avg. Daily T/O (LKR mn) 15.7

Avg. Daily T/O (USD ‘000) 119.3

N - Issued Shares 167.9

NV - Issued Shares

Free Float (%) 54.0

VOTING SHAREHOLDERS

As at 31st March ’14

Vallibel One PLC 14.9%

Employees Provident Fund 9.9%

Mr. Y.S.H.I. Silva 9.9%

Rosewood (Pvt) Ltd 6.8%

MATTHEWS International Funds 4.2%

Caravel Fund (International) Ltd 2.8%

Employees' Trust Fund 2.7%

SHARE PRICE CHART

150

160

170

180

190

200

210

220

8-J

ul-13

27

-Au

g-1

3

16

-Oct-

13

5-D

ec-1

3

24

-Jan-1

4

15

-Mar-

14

4-M

ay-1

4

23

-Jun-1

4

(LKR)

Expanding into high growth areas…

Rating: BUY Ticker : SAMP.SL;LKR209.00

EARNINGS FORECAST

YE 31 Dec/ (LKR mn) 2011 2012 2013 2014E 2015E

Net Profit (LKR mn) 3,683.3 5,436.7 3,635.0 4,678.9 5,754.8

YoY growth (%) 5.7% 47.6% -33.1% 28.7% 23.0%

EPS (LKR) 21.9 32.4 21.7 27.9 34.3

YoY growth (%) 5.7% 47.6% -33.1% 28.7% 23.0%

PER (x) 4.5 6.0 9.7 7.5 6.1

DPS (LKR) 9.0 12.0 8.0 10.6 13.0

Div Yield (%) 4.3% 5.7% 3.8% 5.1% 6.2%

BVPS (LKR) 135.9 165.4 188.7 218.0 239.2

PBV (x) 1.5 1.3 1.1 1.0 0.9

ROE (%) 16.1% 19.6% 11.5% 12.8% 14.3%

Recurrent Basis

Net Profit (LKR mn) 3,683.3 4,975.9 3,635.0 4,678.9 5,754.8

YoY growth (%) 24.7% 35.1% -26.9% 28.7% 23.0%

EPS (LKR) 21.9 29.6 21.7 27.9 34.3

YoY growth (%) 24.7% 35.1% -26.9% 28.7% 23.0%

PER (x) 9.5 7.1 9.7 7.5 6.1

COMPANY UPDATE

2 | P a g e July 2014, Sri Lanka Equity Research

THIRD LARGEST PRIVATE COMMERCIAL BANK

Sampath Bank is the third largest private commercial bank accounting for

approximately 7.4% of the total asset base of commercial banks in Sri

Lanka. At present group operates with a total asset base of LKR387.6 bn

and a branch network of 213, Bank is well renowned for the introduction

of innovative practices to the banking industry. In the past the bank

pioneered in the introduction of ATMS, “one day clearing” for all the

cheques drawn on any Sampath Bank, first cheque Imagine and

Truncating (CIT) site in Sri Lanka, foreign currency Atms and “cardless

cash ATMs etc.However in 2013 Sampath witnessed a notable decline in

bottom line due to impairments as a result of the decline in global gold

prices (in 2012 bank had a 25% exposure to pawning).

Bank has been able to grow its core banking earnings at a CAGR of circa

20% over the last decade. Moreover excluding profit dip in 2013 due to

the pawning impairment, bank’s earnings CAGR grew by c.28% over the

last decade. SAMP is adequately capitalized with Tier I CAR at 9.8% and

TIER II CAR at 13.6% and continued to maintain healthy loan book

(excluding the hit on the pawning portfolio)

STRONG LENDING BASE

SAMP with c.8% market share in loans saw its advances portfolio

growing 25% YoY to LKR265 bn in 2013, the highest growth levels

among licensed commercial bank in the period, due to the strong growth

recorded in the corporate book. However personal banking portfolio

witnessed a lower growth as a result of the moderation in the pawning

portfolio. In 2013 personal banking advances (accounts c. 59% of the

loan book) grew by 17% YoY, leveraging on the expanded business

volumes though the well covered branch network. However growth in the

personal banking advances was notably impacted by the efforts taken to

reduce the pawning portfolio. For an example the bank reduced its

pawning exposure from 25% in 2012 to 20% by the end of 2013 and 17%

by 1Q14. In addition bank’s corporate banking portfolio (accounts c. 34%

TKS Research/ Annual Report

Total Asset Share

24.2%

19.7%

12.4%

10.2%

7.4%

4.3% 4.1% 3.4% 2.7%

1.3% 0.7%

6.0%

2.5%

0.6% 0.5%

“7.4% market share among

commercial banks”

“Loan growth is expected to be

fuelled from the corporate sector”

Source : Company Annual Reports/ Softlogic Equity Research

COMPANY UPDATE

3 | P a g e July 2014, Sri Lanka Equity Research

of the loan book) grew strongly by 38% YoY. The growth was mainly due

to the improved customer service levels, continuous marketing efforts to

canvas new customers etc. For an example in 2013 online process for

documentary credit was further streamlined with the addition of security

features which further improved level of customer experience in the

segment.

Loan growth was rather slow in 1Q14 where bank also recorded a 4% dip

YTD by Mar’14 despite the several measures taken by central bank to

stimulate private sector credit demand (Reduced interest rates cut in

statutory reserve ratio etc). However we expect credit activity to pick up

from 2H2014 where we expect Sampath to further increase funding to

corporate sector especially to areas where domestic economic growth is

expected to fuel from. These areas include Energy, tourism, trade and

infrastructure sectors. This was evident in 2013 where construction

(+27% YoY), tourism (89% YoY), transport (50% YoY) and infrastructure

(25% YoY) lending grew significantly. In addition we expect some

moderation in the personal banking portfolio due to the measures taken to

reduce the pawning portfolio. Therefore we forecast SAMP’s advance

portfolio to grow c.12% in the medium run fuelled by macroeconomic

upside and with more attention placed on the corporate sector.

Loans and Advances

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

300

350

400

2012 2013 2014E 2015E

(LKR bn)

Gross loans & advances YoY growth

Gross Loans and Advances

0

100

200

300

400

500

600

700

800

900

LKR bn

Gross loans & advances - 2012 Gross loans & advances - 2013

6% YoY

4% YoY

13% YoY

17% YoY

26% YoY

8% YoY

11% YoY

19% YoY 14% YoY

5% YoY 23% YoY

Source : Company Annual Reports/ Softlogic Equity Research

Source : Company Annual Reports/ Softlogic Equity Research

COMPANY UPDATE

4 | P a g e July 2014, Sri Lanka Equity Research

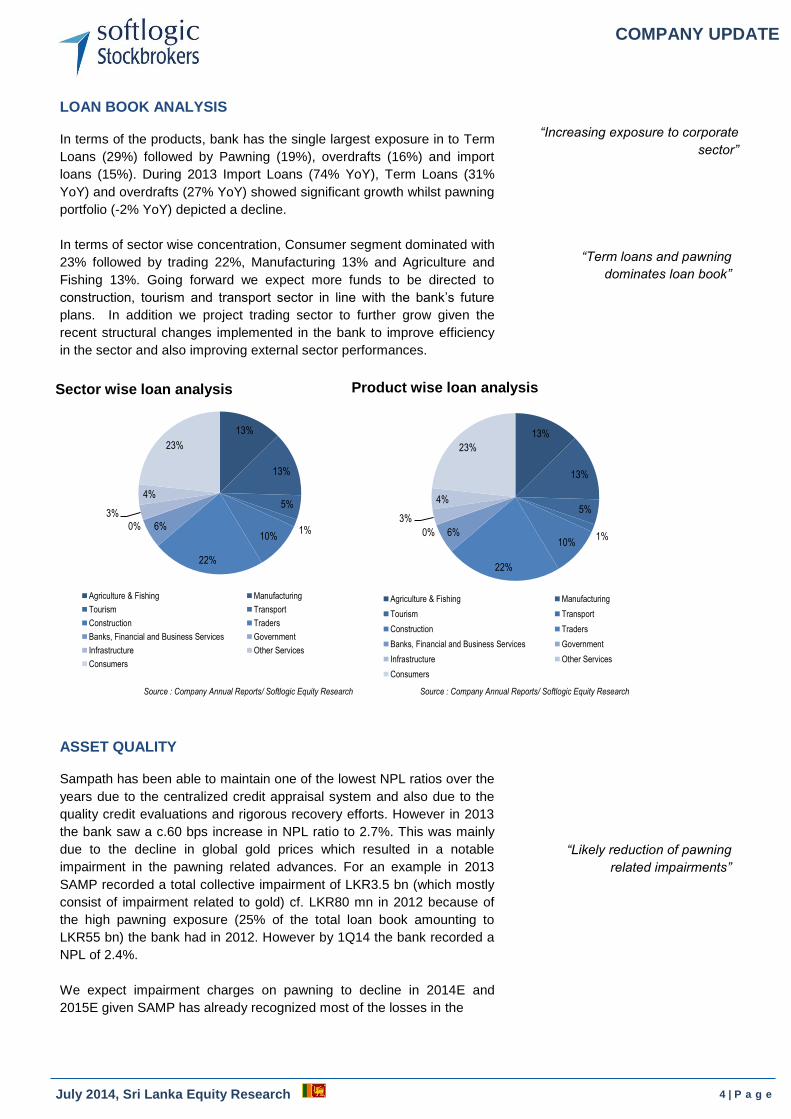

LOAN BOOK ANALYSIS

In terms of the products, bank has the single largest exposure in to Term

Loans (29%) followed by Pawning (19%), overdrafts (16%) and import

loans (15%). During 2013 Import Loans (74% YoY), Term Loans (31%

YoY) and overdrafts (27% YoY) showed significant growth whilst pawning

portfolio (-2% YoY) depicted a decline.

In terms of sector wise concentration, Consumer segment dominated with

23% followed by trading 22%, Manufacturing 13% and Agriculture and

Fishing 13%. Going forward we expect more funds to be directed to

construction, tourism and transport sector in line with the bank’s future

plans. In addition we project trading sector to further grow given the

recent structural changes implemented in the bank to improve efficiency

in the sector and also improving external sector performances.

ASSET QUALITY

Sampath has been able to maintain one of the lowest NPL ratios over the

years due to the centralized credit appraisal system and also due to the

quality credit evaluations and rigorous recovery efforts. However in 2013

the bank saw a c.60 bps increase in NPL ratio to 2.7%. This was mainly

due to the decline in global gold prices which resulted in a notable

impairment in the pawning related advances. For an example in 2013

SAMP recorded a total collective impairment of LKR3.5 bn (which mostly

consist of impairment related to gold) cf. LKR80 mn in 2012 because of

the high pawning exposure (25% of the total loan book amounting to

LKR55 bn) the bank had in 2012. However by 1Q14 the bank recorded a

NPL of 2.4%.

We expect impairment charges on pawning to decline in 2014E and

2015E given SAMP has already recognized most of the losses in the

Sector wise loan analysis

13%

13%

5%

1% 10%

22%

6% 0%

3%

4%

23%

Agriculture & Fishing Manufacturing

Tourism Transport

Construction Traders

Banks, Financial and Business Services Government

Infrastructure Other Services

Consumers

TKS Research/ Annual Report

Product wise loan analysis

13%

13%

5%

1% 10%

22%

6% 0%

3%

4%

23%

Agriculture & Fishing Manufacturing

Tourism Transport

Construction Traders

Banks, Financial and Business Services Government

Infrastructure Other Services

Consumers

“Increasing exposure to corporate

sector”

“Likely reduction of pawning

related impairments”

“Term loans and pawning

dominates loan book”

Source : Company Annual Reports/ Softlogic Equity Research Source : Company Annual Reports/ Softlogic Equity Research

COMPANY UPDATE

5 | P a g e July 2014, Sri Lanka Equity Research

portfolio in 2013. In addition prudent measures taken by bank to minimize

the risk arising from the pawning portfolio is also expected to reduce

impairment charges. These include immediate auctioning of pawning

articles which are not redeemed or re-pawned after one year, lesser loan

to value ratio on pawning (roughly 60% cf. nearly 80% before) and also

the efforts made to reduce the exposure to pawning products.

Furthermore bank increased exposure to pawning when the gold prices

were bottoming out in 2013 (by 3Q 2013) which would provide further

support to the pawning portfolio with lower average cost. However it

should be noted these forecasts are made on the assumption that we

would not envisage another significant downtrend in global gold prices

(especially in the short to medium term).

Therefore given the strong credit track record, possible upgrade of the

Finacle system during 2014 and with stabilised global gold prices we

believe the bank would be able to maintain its NPL ratio below 2.5% in

the medium term.

Asset Quality

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

BOC* Peoples* COMB HNB SAMP SEYB NDB DFCC NTB PABC UBC

Gross NPL Net NPL

NPL Ratio

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

2011 2012 2013 2014E 2015E

Gross NPL ratio Net NPL ratioSource : Company Annual Reports/ Softlogic Equity Research

Source : Company Annual Reports/ Softlogic Equity Research

COMPANY UPDATE

6 | P a g e July 2014, Sri Lanka Equity Research

Pawning

Pawning in simple terms means over the counter lending against gold

(acts as the collateral). Pawning is a very short term lending product

ranging from 1 month to a year maximum. With rising gold prices in 2012

pawning became a very popular and profitable lending product for banks

which saw significant growth in their pawning portfolios. A special feature

in pawning is that it is considered a zero risk lending product when

calculating your risk weighted assets. Thereby expanding pawning base

does not impact your capital base which is another reason why some

banks used pawning to expand their asset base.

However gold prices in the world market declined considerably during

2013 where it fell c.28% (declined c.35% from its high of USD1,790.0) in

2013. Declining gold prices reduces the collateral value of gold loans, but

the impact would not be reflected immediately in the income statement.

Impact would be realized in the income statement when the collateral

(gold) of the defaulted loans are sold at the auction at lower prices.

However sentimental value of jewellery may reduce the customer default

rates in pawning as they would not be refinanced even when the gold

prices decline.

During 2012 banks were giving out c.80-85% (loan/value) of the gold

value as pawning loans (which would act as a buffer if gold prices

decline). However steep fall in gold prices has resulted in loan value

dropping beyond the collateral value which has posted a bad loan risk to

the banks which has relatively high exposure in to pawning. Sampath had

one of the highest pawning exposures by 2012 (25% of the loan book)

During 2013the system lost c.LKR100.0 bn in value on gold loans and

almost all the banks have taken a decision to auction the gold and cut

their losses. Further the banks have considerably reduced the loan to

value ratio to 60-65% enabling a higher cushion against future gold price

reductions. Therefore we believe banks would be able to fully clear their

books by end of this year.

“Customer confidence & attractive

products to drive deposits”

“Expected to maintain the gross

NPL ratio below 2.5% in the

medium term”

Gold Prices

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

1,900

Aug-12 Nov-12 Feb-13 May-13 Aug-13 Nov-13 Feb-14 May-14

USD/Oz

Source : Bloomberg/ Softlogic Research

COMPANY UPDATE

7 | P a g e July 2014, Sri Lanka Equity Research

DEPOSIT MOBLISATION

Customer deposit (LKR311.8 bn as at 1Q14) which accounts for c.77% of

the funding witnessed c.24% YoY upside in 2013 and 4% YTD growth by

end of 1Q14. In a highly competitive deposit market with the declining

interest rates we believe SAMP would be able to grow its deposit base by

c.11% in the coming few years. The growth in deposits would be

leveraged on well covered branch network and through the introduction of

innovative products which improves customer convenience. These value

added channel products include mobile banking, internet banking, value

added ATMs, debit cards, credit cards, M-commerce products and E-

remittance etc. Furthermore integrating technology into these channel

products would further assist bank’s deposit mobilization efforts. For an

example Sampath ATMs provide value added facilities such as

exchanging foreign currencies, paying utility bills etc on top of the normal

ATM functions. Moreover in 2013 the bank introduced first cardless ATM

in Asia/South East Asia which enables users to withdraw cash from ATMs

without using a debit card. Bank’s current loan to deposit ratio is 82%

mainly due to the moderation in the pawning portfolio (1Q14) and was

89% in 2013. We believe going forward bank would maintain it at 90%

level with the expected pick up in the private sector credit growth.

Deposits

0%

5%

10%

15%

20%

25%

30%

0

50

100

150

200

250

300

350

400

2011 2012 2013 2014E

(LKR bn)

Deposits YoY growth

“Growth in deposits fuelled by

value added products”

Source : Company Annual Report/ Softlogic Research

Deposit Growth

0

100

200

300

400

500

600

700

800

900

LKR bn

Deposits - 2012 Deposits - 2013

22% YoY

11% YoY

15% YoY

13% YoY

24% YoY

14% YoY

11% YoY

21% YoY 29% YoY

12% YoY 23% YoY

Source : Company Annual Report/ Softlogic Research

COMPANY UPDATE

8 | P a g e July 2014, Sri Lanka Equity Research

GROWING CASA FRANCHISE

Despite relatively low interest rates, SAMP’s CASA mix deteriorated

slightly to c.33% (34% in 2012). However despite the fall in the ratio bank

was able to increase the savings base by 22% YoY in 2013. Therefore

with the low interest rates we believe the bank would see an improvement

in the CASA mix going forward.

SATISFACTORY CAPITALIZATION LEVEL

By end 1Q14, SAMP had a Tier I CAR of 9.8% (minimum regulatory limit

5%) and Tier II CAR of 13.6% (minimum regulatory limit 10%). During the

year 2013 bank successfully completed LKR5.0 bn debenture issue to

further strengthen its total capital base. In addition the bank also raised

USD100 mn in a single transaction during the year. Furthermore USD20

mn was also raised from Proparco, the private investment arm of the

French development agency (AFD). Therefore we believe SAMP is

adequately capitalized to support medium term growth and risks.

However if sustained low growth in profit is recorded SAMP might need to

strengthened its Tier I capital in near future to support the growth

potential. Bank’s liquid asset ratio is at 27.2% (regulatory limit of 20%).

“CASA mix to improve with decline

in interest rates”

“Bank is adequately capitalized”

CASA Base

6% 6% 6% 6% 6%

34% 28% 28% 28% 29%

60% 66% 67% 66% 65%

2011 2012 2013 2014E 2015E

Current accounts Savings accounts Time deposits

CASA Mix

38% 37%

45%

39%

35% 33%

26%

18%

26%

22%

18%

Source : Company Annual Reports/ Softlogic Research

Source : Company Annual Reports / Softlogic Research

COMPANY UPDATE

9 | P a g e July 2014, Sri Lanka Equity Research

Capital adequacy

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

2011 2012 2013 2014E 2015E

Tier I CAR Tier II CAR

Tier I Regulatory limit Tier II Regulatory limit

Capital adequacy

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

BOC* Peoples* COMB HNB SAMP SEYB NDB DFCC NTB PABC UBC

Tier I CAR Tier II CAR

Tier II Regulatory Limit

Source : Company Annual Report/ Softlogic Research

Source : Company Annual Reports/ Softlogic Research

COMPANY UPDATE

10 | P a g e July 2014, Sri Lanka Equity Research

FINANCIAL PERFORMANCE

Net Interest Income (NII)

NII increased 25% YoY to LKR15,094.8 mn in 2013 largely due to a 29%

YoY rise in interest income to LKR42,320.2 mn. The growth in interest

income was mainly on account of the 25.1% YoY growth in the loan book

and effective management of the fund base. In addition during the year

the bank converted part of the foreign currency reserve of the FCBU into

local currency to facilitate local lending. This was carried out on the view

to reduce the volatile income. Therefore this initiative also contributed to

the the increase in interest income. However growth in interest income

was partly limited by the lack of credit growth in the overall economy and

dip in the pawning portfolio (-2%YoY). In addition interest expense rose

by 31.7% YoY to LKR27,255.5 mn due to the 23.6% YoY increase in

deposits and rise in foreign borrowings. Going forward we expect a flat

growth in NII in 2014E due to the the possible loss of accrued interest on

auctioned pawning articles. During 2013, bank’s net interest margin was

at 4.2% with an average interest yield of 13.4% and and average intersest

cost of 8.6%.

Non-interest income

Non interest income declined by 16.7%YoY to LKR5,265.5 mn in 2013 as

a resutl of the 34.2% YoY drop in other operating income. The dip in other

opearating income was on account of the drop in foreign exchange

revaluation gain by 84.5%YoY due to the conversion of foreign currency

reserves to expand local lending. Furthermore less volatility of rupee

during the year also contributed drop in forex gains. However these

losses were partially offset by the strong growth (+18.9% YoY in 2013) in

the the fees and commsision income supported by robust growth in the

trade related services (+12.0% YoY), Credit card and debit cards (+18.6%

YoY) and foreign remittance (+25.7% YoY). We expect cards and

remittance to play a pivotal role in driving bank’s fee based business.

Furthermore Sampath Bank recorded the highest growth in fees and

commision income cf. its main peers over the years.

NII

0%

5%

10%

15%

20%

25%

30%

35%

0

2

4

6

8

10

12

14

16

18

2012 2013 2014E 2015E

(LKR bn)

Net interest income (NII) YoY growth

“NII to grow 21% YoY in 2014E

“Non-interest income accounts

17% of total income”

Source : Company Annual Report/ Softlogic Research

COMPANY UPDATE

11 | P a g e July 2014, Sri Lanka Equity Research

Cost/income Ratio

SAMP cost/income (ex.prov) ratio increased to 54.4% in 2013 (cf. 51.5%

in 2012) due to the drop in non interest income as a result of the drop in

FCBU gains during the year. In addition during the year bank carried out

an island-wide programe to upgrade the interior design of all the branches

to a consistent standard which further increased cost to income ratio. We

believe the bank would be able to maintain cost/income below 55% in the

medium term given the low cost branch model the bank operate with the

centralization of specialized functions. The bank currently has one of the

lowest staff per branch ratio in the industry (11 staff per branch). In

addition given the likely absesnse of major upgrades in branches going

forward and the moderation of branch expansion we expect further

improvement in cost/income ratio.

Total Income Composition

79% 84% 89% 88% 88%

21% 16% 11% 12% 12%

2011 2012 2013 2014E 2015E

Interest income Other income

Cost : Income

48%

49%

50%

51%

52%

53%

54%

55%

56%

57%

58%

0

2

4

6

8

10

12

14

2011 2012 2013 2014E 2015E

(LKR bn)

Operating Costs Cost (ex.prov)/income ratio

Source :Company Annual Repor/t Softlogic Equity Research

Source :Company Annual Report/ Softlogic Equity Research

COMPANY UPDATE

12 | P a g e July 2014, Sri Lanka Equity Research

Net Interest Margin

Sampath Bank has been able to maintain NIMs above 4.0% due to the

timely and efficient and repricing of assets and liabilities and also due to

the exposure to higher yielding assets such as pawning and cards.

However in 1Q14 bank’s NIMs dropped by 118 bps to 3.0% cf. 4Q13

owing to the loss in interest income with the auctioning non-redeemed

pawning articles. Therefore going forward we expect a dip in NIMs in

2014E as a result of the possible loss of interest income with the

auctioning of pawning articles. Furthermore in the medium term we

expect a slight deterioation in NIMs (near 4.0%) from the average level

with more funds being divered to the corporate sector.

Net Interest Margin

3.2%

3.7%

4.2%

2011 2012 2013 2014E 2015ENII margin

“NI margin to be maintained in the

range of 3.5-4.0%”

Cost : Income Per Comparison

51%

45% 40%

52% 54%

57%

48%

42%

58%

69%

78%

Source : Company Annual Reports/ Softlogic Equity Research

Source :Company Annual Report Softlogic Equity Research

COMPANY UPDATE

13 | P a g e July 2014, Sri Lanka Equity Research

KEY RISKS

Possible reduction in Gold prices – Sampath Bank currently has a 17%

exposure to pawning in the loan book (LKR44.8 bn). Hence bank’s bottom

line is susceptible fluctuation in global gold prices. A notable downtrend in

gold prices could result in pawning related impairments as witnessed in

2013. Furthermore with the policy of auctioning articles which are not

redeemed within one year could also result in interest losses. As a result

this could adversely impact banks bottom-line. However we believe pawning

related risk is only present to the medium term growth in the profitability.

Persistent weaker asset quality - Sustained weaker asset quality might also

insert pressure on capital adequacy. Currently Sampath has one of the

lowest Tier 1 capital adequacy ratio in the industry (industry average

c.11.0%). Pressure on capital adequacy might also limit loan book

expansion or may lead to assume riskier underwriting standards to increase

profitability. This could further deteriorate credit profile.

VALUATION

Forecast 2014E net profit up 29% to LKR4,678.9 mn. SAMP’s NIM would

be intact around 4.0% whilst continuing to benefit from wider coverage.

Credit growth is expected to pick up from 2H2014 and less pawning related

impairment with gold prices stabilizing would help bank to grow its core

income. Furthermore expected growth in fee based business would further

strengthen the operating income. In addition moderation of the branch

network would enable the bank to bring down cost to income below 55%

boosting the earnings. Samp’s outlook is positive. Therefore we forecast

2014E net profit to rise 28.7% YoY to LKR4,678.9 mn and 2015E net

earnings to grow 23.0%YoY to LKR5,754.8 mn.

Attractive valuation compared local peers. Sampath offers better

valuations compared to local peers both in terms of PBV (x) and PER (x).

Hence the bank is trading at a notable discount.

Attractive valuation compared regional peers. The bank is one of the

cheapest banking counters compared to its regional peers.

Name Mkt Cap (LKR mn) PER (X) PBV (X) ROE (%) Tot Assets (LKR Bn)

SAMPATH BANK PLC 35,009 8.9 1.0 12.7 387.6

NATIONAL DEVELOPMENT BANK PL 34,291 10.4 1.4 14.0 213.1

DFCC BANK 42,416 13.4 1.0 8.2 177.3

SEYLAN BANK 12,142 9.9 1.0 10.3 217.5

COMMERCIAL BANK OF CEYLON PL 124,040 12.1 2.1 18.6 648.6

HATTON NATIONAL BANK PLC 62,751 8.6 1.1 13.9 536.7

Name Mkt Cap (LKR mn) PER (X) PBV (X) ROE (%) Tot Assets (LKR Bn) Country

NIB BANK 30,315 17.3 1.4 8.3 234.5 PAKISTAN

PHILIPPINE SAVINGS BANK 98,505 22.9 1.9 7.7 411.4 PHILIPPINES

BANK OF JORDAN 74,163 9.6 1.3 15.0 400.5 JORDAN

FNB NAMIBIA HOLDINGS LTD 75,233 10.0 2.7 25.9 295.8 NAMIBIA

FIRST NATIONAL BANK BOTSWANA 131,129 12.3 4.3 38.8 242.2 BOTSWANA

Source : Bloomberg/ Softlogic Equity Research

Source : Bloomberg/ Softlogic Equity Research

COMPANY UPDATE

14 | P a g e July 2014, Sri Lanka Equity Research

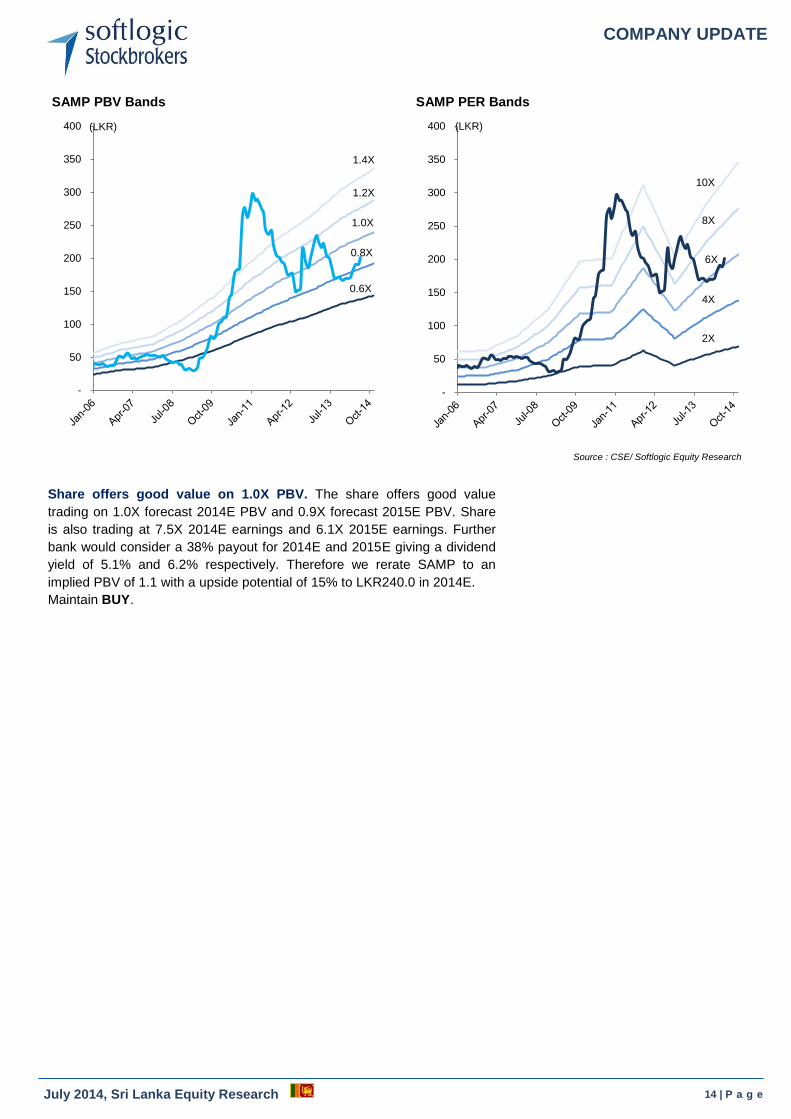

Share offers good value on 1.0X PBV. The share offers good value

trading on 1.0X forecast 2014E PBV and 0.9X forecast 2015E PBV. Share

is also trading at 7.5X 2014E earnings and 6.1X 2015E earnings. Further

bank would consider a 38% payout for 2014E and 2015E giving a dividend

yield of 5.1% and 6.2% respectively. Therefore we rerate SAMP to an

implied PBV of 1.1 with a upside potential of 15% to LKR240.0 in 2014E.

Maintain BUY.

Source : CSE/ Softlogic Equity Research

SAMP PER Bands

-

50

100

150

200

250

300

350

400

2X

4X

6X

8X

10X

(LKR)

SAMP PBV Bands

-

50

100

150

200

250

300

350

400

0.6X

0.8X

1.0X

1.2X

1.4X

(LKR)

COMPANY UPDATE

15 | P a g e July 2014, Sri Lanka Equity Research

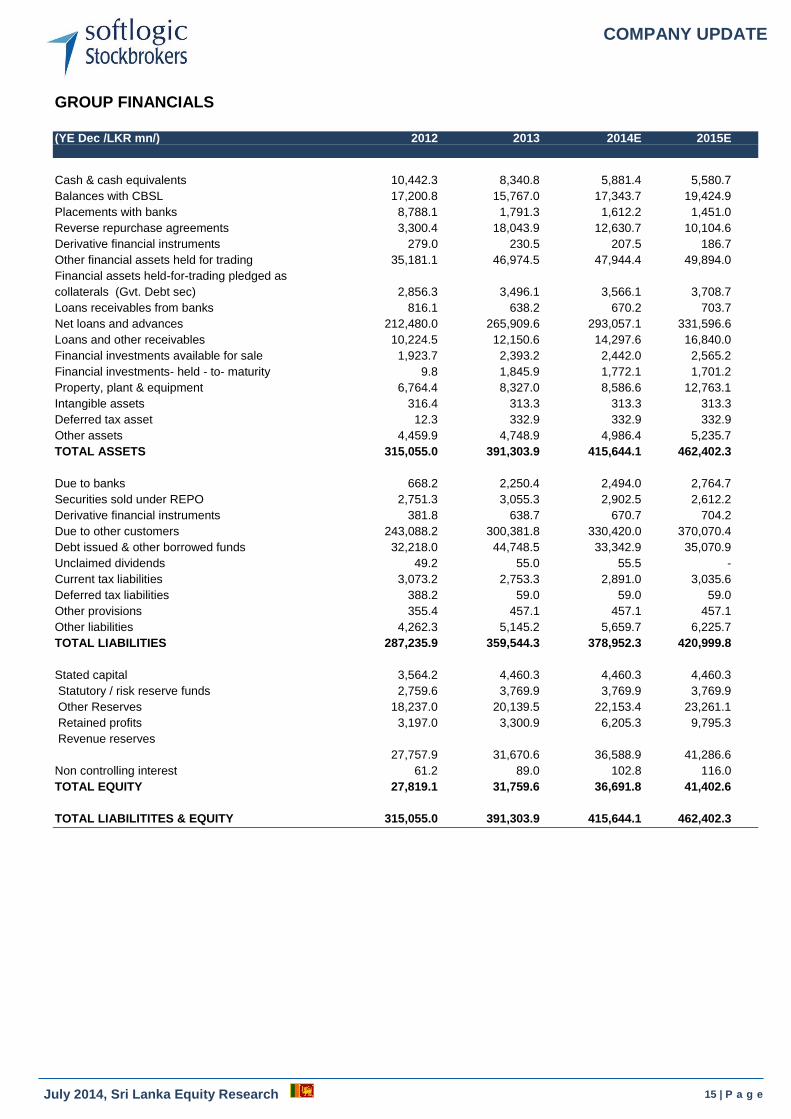

GROUP FINANCIALS

(YE Dec /LKR mn/) 2012 2013 2014E 2015E

Cash & cash equivalents 10,442.3 8,340.8 5,881.4 5,580.7

Balances with CBSL 17,200.8 15,767.0 17,343.7 19,424.9

Placements with banks 8,788.1 1,791.3 1,612.2 1,451.0

Reverse repurchase agreements 3,300.4 18,043.9 12,630.7 10,104.6

Derivative financial instruments 279.0 230.5 207.5 186.7

Other financial assets held for trading 35,181.1 46,974.5 47,944.4 49,894.0

Financial assets held-for-trading pledged as

collaterals (Gvt. Debt sec) 2,856.3 3,496.1 3,566.1 3,708.7

Loans receivables from banks 816.1 638.2 670.2 703.7

Net loans and advances 212,480.0 265,909.6 293,057.1 331,596.6

Loans and other receivables 10,224.5 12,150.6 14,297.6 16,840.0

Financial investments available for sale 1,923.7 2,393.2 2,442.0 2,565.2

Financial investments- held - to- maturity 9.8 1,845.9 1,772.1 1,701.2

Property, plant & equipment 6,764.4 8,327.0 8,586.6 12,763.1

Intangible assets 316.4 313.3 313.3 313.3

Deferred tax asset 12.3 332.9 332.9 332.9

Other assets 4,459.9 4,748.9 4,986.4 5,235.7

TOTAL ASSETS 315,055.0 391,303.9 415,644.1 462,402.3

Due to banks 668.2 2,250.4 2,494.0 2,764.7

Securities sold under REPO 2,751.3 3,055.3 2,902.5 2,612.2

Derivative financial instruments 381.8 638.7 670.7 704.2

Due to other customers 243,088.2 300,381.8 330,420.0 370,070.4

Debt issued & other borrowed funds 32,218.0 44,748.5 33,342.9 35,070.9

Unclaimed dividends 49.2 55.0 55.5 -

Current tax liabilities 3,073.2 2,753.3 2,891.0 3,035.6

Deferred tax liabilities 388.2 59.0 59.0 59.0

Other provisions 355.4 457.1 457.1 457.1

Other liabilities 4,262.3 5,145.2 5,659.7 6,225.7

TOTAL LIABILITIES 287,235.9 359,544.3 378,952.3 420,999.8

Stated capital 3,564.2 4,460.3 4,460.3 4,460.3

Statutory / risk reserve funds 2,759.6 3,769.9 3,769.9 3,769.9

Other Reserves 18,237.0 20,139.5 22,153.4 23,261.1

Retained profits 3,197.0 3,300.9 6,205.3 9,795.3

Revenue reserves

27,757.9 31,670.6 36,588.9 41,286.6

Non controlling interest 61.2 89.0 102.8 116.0

TOTAL EQUITY 27,819.1 31,759.6 36,691.8 41,402.6

TOTAL LIABILITITES & EQUITY 315,055.0 391,303.9 415,644.1 462,402.3

COMPANY UPDATE

16 | P a g e July 2014, Sri Lanka Equity Research

INCOME STATEMENT

(YE Dec /LKR mn) 2012 2013 2014E 2015E

Interest income 32,712.0 42,320.2 42,805.4 47,243.6

Interest expenses 20,673.0 27,225.5 27,413.7 30,114.5

Net interest income 12,039.0 15,094.7 15,391.8 17,129.1

Other income 6,340.6 5,265.5 5,709.3 6,192.5

Net income 18,379.6 20,360.2 21,101.1 23,321.6

Impairment changes on loans 80.1 3,574.1 1,683.5 1,307.1

Total OPEX 9,470.2 11,066.0 11,942.5 12,820.5

PBT 8,829.3 5,720.1 7,475.1 9,194.0

Taxation 3,389.3 2,082.4 2,792.7 3,434.9

PAT 5,440.0 3,637.7 4,682.4 5,759.1

Equity holder profit 5,436.7 3,635.0 4,678.9 5,754.8

Ratios

2012 2013 2014E 2015E 1Q2014

Tier I CAR 11.87% 10.08% 9.80% 9.70% 9.75%

Tier II CAR 13.75% 14.14% 13.12% 12.39% 13.57%

Gross NPL ratio 2.07% 2.68% 2.50% 2.40% 2.38%

Net NPL ratio 0.22% 0.59% 0.50% 0.40% 0.93%

NII margin 4.18% 4.27% 3.82% 3.90% 2.98%

ROA (before tax) 2.61% 1.46% 1.80% 1.99% 1.78%

ROE (after tax) 22.33% 11.48% 12.79% 13.94% 16.78%

Ave. Interest yield 13.3% 13.4% 11.7% 11.9% 11.0%

Ave. Interest cost 8.2% 8.6% 7.6% 7.7% 7.5%

Cost/income (Ex Prov) 51.5% 54.4% 56.6% 55.0% 63.1%

CASA mix 33.8% 33.3% 34.5% 34.7% 34.7%

Loan/Deposit 0.87 0.89 0.89 0.90 0.82

Liquid asset ratio - DBU 21.50% n/a n/a n/a 28.60%

COMPANY UPDATE

17 | P a g e July 2014, Sri Lanka Equity Research

Softlogic Stockbrokers (Pvt) Ltd # 06, 37

th Lane, Queens Road, Colombo 03

Sri Lanka

Telephone +94 117 277 000 |Fax +94 117 277 099

E-mail [email protected]

Equity Research Danushka Samarasinghe Asanka Ranasinghe

[email protected] [email protected]

+94 11 7277001 + 94 11 7277052, +94 77-1078497

Kavindu Ranasinghe Chamithri R.atnapala

[email protected] [email protected]

+94 11 7277031 + 94 11 7277030, +94 77-3723506

Imalka Hettiarachchi Nishanthi Hettiarachchi

[email protected] [email protected]

+94 11 7277032 +94 11 7277030, +94 11 77 1078499 Equity Sales Dihan Dedigama [email protected] 011 7277010 / 0117277055, 0777689933

Hussain Gani [email protected] 011 7277020 / 777209986

Prasanna Chandrasekera [email protected] 011 7277056

Eardley Kern [email protected] 011 7277053, 0777348018

Andre Lowe [email protected] 011 7277034,

Zimry Liyabdeen [email protected] 011 7277057

Achindi.Silva [email protected] 011 7277054 077 3825087

Chandima Kariyawasam [email protected] 011 7277058, 0777885778

Hisham Haniffa [email protected] 0773828781

Branches Horana

Madushanka Rathnayaka [email protected] 034 7451000 0773566465

Negombo

Krishan Williams [email protected] 031 7451000 0773569827 The information contained in this report is for general information purposes only. This report and its content is copyright of Softlogic Stockbrokers and all rights reserved. This report- in whole or in part- may not, except with the express written permission of Softlogic Stockbrokers be reproduced or distributed or commercially exploited in any material form by any means whether graphic, electronic, mechanical or any means. Nor may you transmit it or store it in any other website or other form of electronic retrieval system. Any unauthorised use of this report will result in immediate proceedings. The report has been prepared by Softlogic Stockbrokers (Private) Limited. The information and opinions contained herein has been compiled or arrived at based upon information obtained from sources believed to be reliable and in good faith. Such information has not been independently verified and no guaranty, representation or warranty, express or implied is made as to its accuracy, completeness or correctness, reliability or suitability. All such information and opinions are subject to change without notice. This document is for information purposes only, descriptions of any company or companies or their securities mentioned herein are not intended to be complete and this document is not, and should not be construed as, an offer, or solicitation of an offer, to buy or sell any securities or other financial instruments. In no event will Softlogic Stockbrokers be liable for any loss or damage including without limitation, indirect or consequential loss or damage, or any loss or damage whatsoever arising out of, or in connection with the use of this report and any reliance you place on such information is therefore strictly at your own risk. Softlogic Stockbrokers may, to the extent permissible by applicable law or regulation, use the above material, conclusions, research or analysis in which they are based before the material is disseminated to their customers. Not all customers will receive the material at the same time. Softlogic Stockbrokers, their respective directors, officers, representatives, employees, related persons and/or Softlogic Stockbrokers, may have a long or short position in any of the securities or other financial instruments mentioned or issuers described herein at any time and may make a purchase and/or sale, or offer to make a purchase and/or sale of any such securities or other financial instruments from time to time in the open market or otherwise, in each case either as principal or agent. Softlogic Stockbrokers may make markets in securities or other financial instruments described in this publication, in securities of issuers described herein or in securities underlying or related to such securities. Softlogic Stockbrokers may have entirely underwritten the securities of an issuer mentioned herein.

Softlogic Research Guide to Investment Rating BUY : Share price may exceed 15% over the next 12 months

Trading BUY : Share price may exceed 7.5% over the next 3 months, however longer-term outlook could vary

Neutral : Share price may fall within the range of +/- 7.5% over the next 12 months

Take Profit : Target price has been attained. Look to accumulate at lower levels

Sell : Share price may fall by more than 15% over the next 12 months

Not Rated : Stock is not within regular research coverage