Sam Won, Managing Director, GRMA Risk … · Sam Won, Managing Director, GRMA Risk Management Best...

14

Sam Won, Managing Director, GRMA Risk Management Best Practices Best Practices for Risk Management in the Single Family Office Edited by Timothy S. Wilson, Managing Director & Head of Risk Services, GRMA Contributions by Mingyang Liu, Senior Analyst, GRMA

Transcript of Sam Won, Managing Director, GRMA Risk … · Sam Won, Managing Director, GRMA Risk Management Best...

Sam Won, Managing Director, GRMA

Risk Management Best Practices Best Practices for Risk Management in the Single Family Office

Edited by Timothy S. Wilson, Managing Director & Head of Risk Services, GRMA

Contributions by Mingyang Liu, Senior Analyst, GRMA

Cover Photo: © Jakub Jirsák | Dreamstime.com

THE FAMILY OFFICE ASSOCIATION

Risk Management Best PracticesBest Practices for Risk Management in the Single Family Office

Copyright © Family Office Association and Angelo Robles. All rights reserved. This white paper or parts thereof may not be reproduced in any form or redistributed for commercial use. For more information about this publication, please contact [email protected].

Disclaimer: The Family Office Association (FOA) is an affinity group dedicated primarily to the interests of Single Family Offices. FOA is intended to provide members with educational information and a forum in which to exchange information of mutual interest. FOA does not participate in the offer, sale or distribution of any securities nor does it provide investment advice. Further, FOA does not provide tax, legal or financial advice.

Materials distributed by FOA are provided for informational purposes only and shall not be construed to be a recommendation to buy or sell securities or a recommendation to retain the services of any investment adviser or other professional adviser. The identification or listing of products, services, links or other information does not constitute or imply any warranty, endorsement, guaranty, sponsorship, affiliation or recommendation by FOA. Any investment decisions you may make on the basis of any information provided by FOA is your sole responsibility.

The FOA logo and all related product and service names, designs, and slogans are the trademarks or service marks of Family Office Association. All other product and service marks on materials provided by FOA are the trademarks of their respective owners. All of the intellectual property rights of FOA or its contributors remain the property of FOA or such contributor, as the case may be, such rights may be protected by United States and international laws and none of such rights are transferred to you as a result of such material appearing on the FOA web site.

The information presented by FOA has been obtained by FOA from sources it believes are reliable. However, FOA does not guarantee the accuracy or completeness of any such information. All of such information has been prepared and provided solely for general informational purposes and is not intended as user specific advice.

TABLE OF CONTENTSRisk Management Best PracticesBest Practices for Risk Management in the Single Family Office

Executive Summary

Overview

Section 1: Risk Management Strategy & Governance

Section 2: Risk Management Infrastructure

Section 3: Risk Management Processes & Controls

Section 4: Risk Measurement, Monitoring & Reporting

Conclusion: The Importance of an Integrated Process

About the Global Risk Management Advisors

About Family Office Association

004

005

006

007

009

011

012

013

014

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

Executive Summary

The purpose of the following sound practices guidelines for risk management is to provide family offices with a better understanding of the key elements that constitute sound and institutional quality risk management. In addition, this document is intended to provide best practices recommendations so that a family office can begin to do the necessary work, either internally and/or externally, with the guidance of qualified and experienced risk management practitioners, to implement and maintain an institutional-quality risk management program.

About the Key Sound Practices Recommendations

You will see Key Sound Practices designated by the above icon throughout the document. These Key Sound Practices Recommendations are not intended to be an exhaustive list of what a family office needs to do in order to have institutional quality risk management. Rather, the purpose is to highlight major recommendations that we have found from extensive experience working with institutional investors are most essential for having institutional-quality risk management this is actionable and should be integrated into a family’s overall process for effective investment management.

004

Staff

Overview

Risk Management Best Practices

Today, family offices are invested in a wide range of increasingly more complex and diversified assets. As a result, there is a growing trend among family offices that are now adopting a model that is similar to what institutional investors such as pensions, endowments and foundations do for risk management. These family offices have chosen to take a more formal and institutional-quality approach to risk management. By doing so, a family office is not only better fulfilling its fiduciary responsibilities and obligations to family stakeholders but also creating the basis for more superior, repeatable and sustainable investment management results through economic and market cycles both good and bad.

Typically, an “institutional-quality” approach for risk management is characterized by having a risk management framework that includes four core elements, namely:

005

1. Risk Management Strategy and Governance

2. Risk Management Infrastructure

3. Risk Management Processes and Control

4. Risk Measurement, Risk Monitoring and Risk Reporting

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

006

Section 1

Risk Management Strategy & Governance

In order to have institutional-quality risk management, a family office should begin by putting in place a sound governance structure and process for risk management that is well defined and fully integrated into a family’s overall investment management process.

Typically, institutional investors use their investment policy statement (“IPS”) to describe and document their risk management governance structure and processes and controls.

Key Sound Practices Recommendations

Risk Management CommitteeA Risk Management Committee should serve as the governance body for a family office’s risk management. The Risk Committee should be responsible for the oversight of risk management of the investment portfolio. Typically, this Committee is responsible for developing, reviewing and approving risk management processes and controls and the corresponding risk management policies and procedures to execute its governance.

Formal and Written Document for GovernanceThe risk management governance structure and roles and responsibilities of the Risk Management Committee should be in a formal written document. For most institutional investors, risk management governance is often covered as a section within their IPS.

As part of this documentation, it highly advisable that the family’s overarching strategy and objectives for risk management should be spelled out within the document.

Investment Policy Statement (IPS)An IPS is a document, typically between an investor and the assisting manager, which records the agreements between the two parties regarding issues of money management.

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

007

Section 2

Risk Management Infrastructure

A family office cannot expect to do real and substantive investment risk management without the proper infrastructure or resources in place to perform the risk management function properly. Typical examples of critical infrastructure for risk management include but are not limited to: specialized risk management staff, a risk management analytic system and data management tools and software. All of these kinds of infrastructure are essential for a family office to have robust and actionable risk management.

Key Sound Practices Recommendations

Risk Management PersonnelA family office needs proper risk management personnel if it is going to effectively execute its governance strategy for risk management. So long as the risk management personnel are qualified and experienced in risk management, this staffing can either be internal or external staff. The primary responsibility of risk management staff is to ensure that a family’s investment risks and investment portfolio are independently monitored, reported and managed in accordance to risk management policies and procedures approved by the family’s Risk Management Committee.

Given both the breadth and depth of risk management skills that are required in risk management staff, consideration should be given to utilizing an experienced external risk management advisory firm that can provide these resources more cost effectively on a managed services basis.

Risk Analytics SystemGenerally, the data a family office receives from its asset managers does not provide adequate or meaningful insights of the on-going investments risks of a family’s investment. Furthermore, most family offices do not have the internal capabilities to the rigorous risk analysis necessary to properly measure, monitor and have aggregate view of the investment risks of the family’s investment portfolio across all of its asset managers and accounts. Therefore, a family should either have an internal risk management system or external risk management advisor that can assist them to “risk screen” investments, monitor the investment risks for existing investments and provide an aggregate portfolio-wide risk management report that summarizes not only the family’s current investment risks but also the potential investment risks under different market and economic scenarios management should be spelled out within the document.

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

008

Section 2, Risk Management Infrastructure, cont.

Key Sound Practices Recommendations

Data Management Tools/WarehouseDepending upon the size and complexity of a family office’s investment portfolio, essential risk management infrastructure may include the need for data management tools and a data warehouse. The primary function of a data warehouse is to store portfolio and market data over time and facilitate ongoing tracking of current and past investment risks and returns.

A well-developed data warehouse should be able to perform:

• Data aggregation from multiple sources (e.g., brokerage, invested funds, custodian bank, etc.)• Data reconciliation• Exposure and performance calculations• Historical data storage

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

009

Section 3

Risk Management Processes & Controls

In order for a family office’s governance to be effective, there must be well-defined and documented risk management processes and controls that operationalize this governance. Typically, key risk processes and controls are described and documented in a risk management policies and procedures manual.

These policies and procedures should describe the specific protocols and detail the processes and controls by which investment risks are measured, monitored, and controlled. Examples of essential risk management policies and procedures that institutional investors typically have in their manual include escalation policies and procedures as well as procedures for valuation, liquidity risk management and credit and counterparty risk management.

Key Sound Practices Recommendations

Risk Policy GuidelinesRisk Policy Guidelines that describe in granular detail a family office’s parameters or “budget” for investment risks such as maximum drawdown, volatility and exposure concentrations should either be in an accompanying document or as an appendix to the IPS.

Escalation Policies & ProceduresEscalation Policies and Procedures should define a family’s process and specific actions that will be taken to defease investment risk(s) in the event that a particular investment and/or the portfolio is nearing or has exceeded a family’s budget or stated limits for risk (e.g. market risk, concentration risk, credit risk, liquidity risk, etc.).

Liquidity Risk Management Policy The financial crisis in 2008 proved that even financial instruments and assets that were once universally deemed “liquid” could become illiquid in a financial crisis or under highly stressed market conditions. Therefore, a family office should have a well thought out liquidity risk management policy in place to prescribes how liquidity risks will be measured, monitored and managed to ensure that family stakeholders do not have undue liquidity issues or can minimize its liquidity risks in times when markets become turbulent or stressed.

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

010

Section 3, Risk Management Process & Controls, cont.

Key Sound Practices Recommendations

Valuation PolicyGiven that most family offices have a large and meaningful portion of the portfolio illiquid investments, the development of sensible valuation policies and procedures is essential for sound investment risk management. The objectives of valuation policies are to: prescribe the methodology and the manner in which investments should be valued; ensure that investments are valued accurately and consistently; and set a process to prevent incorrect valuation or, if required, detect and correct errors in valuations.

These policies and procedures should also include guidelines to treat exceptions; and, to test and review compliance with the valuation policies and procedures.

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

011

Section 4

Risk Measurement, Monitoring & Reporting

Simply put, a family office cannot properly manage its investment risks if those risks have not been identified and are not being measured, monitored and reported to the family’s Risk Management Committee.

The risk measurement and management process should address all major potential drivers that may affect or change the value of a single investment or the investment portfolio in aggregate. For family offices, these “risk drivers” often include the following types of major investment risks: market risk (including leverage), liquidity risk, credit risk, operational risk, legal/compliance risk and model risk.

Key Sound Practices Recommendations

Meaningful Risk & Performance MetricsIt is crucial that family office has meaningful risk metrics, performance attribution and risk and performance benchmarks so that it can effectively and actionably monitor, evaluate and manage its investment risks.

Periodic Risk Reporting & Risk Policy Guideline MonitoringA family office’s Risk Management Committee and family stake holders should receive periodic risk management reports that clearly delineate the major investment risks that are and may potentially affect the investment portfolio. In addition, these reports should show where the portfolio stands versus the prescribed Risk Policy Guidelines (“limits”) set by the family’s Risk Management Committee.

Correlations MatterIt is important for a family office to understand that while investments have not only stand-alone risks but also that there are correlative effects that may greatly impact the portfolio in aggregate. Therefore, it is crucial for a family office to measure, monitor and understand the correlations across investments within their portfolio so that these risks can be properly monitored and managed.

Stress Testing & Scenario AnalysisIn order to understand both the potential the risk “downside” and “upside” in the investment portfolio, a family office should be performing stress testing and scenario analysis to assess the potential impact from economic or market-related factors under stressed and highly stressed market conditions. Only then, can a family begin to properly gauge and act upon its exposures to market, credit and liquidity risks in their investment portfolio and do management of risks.

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

012

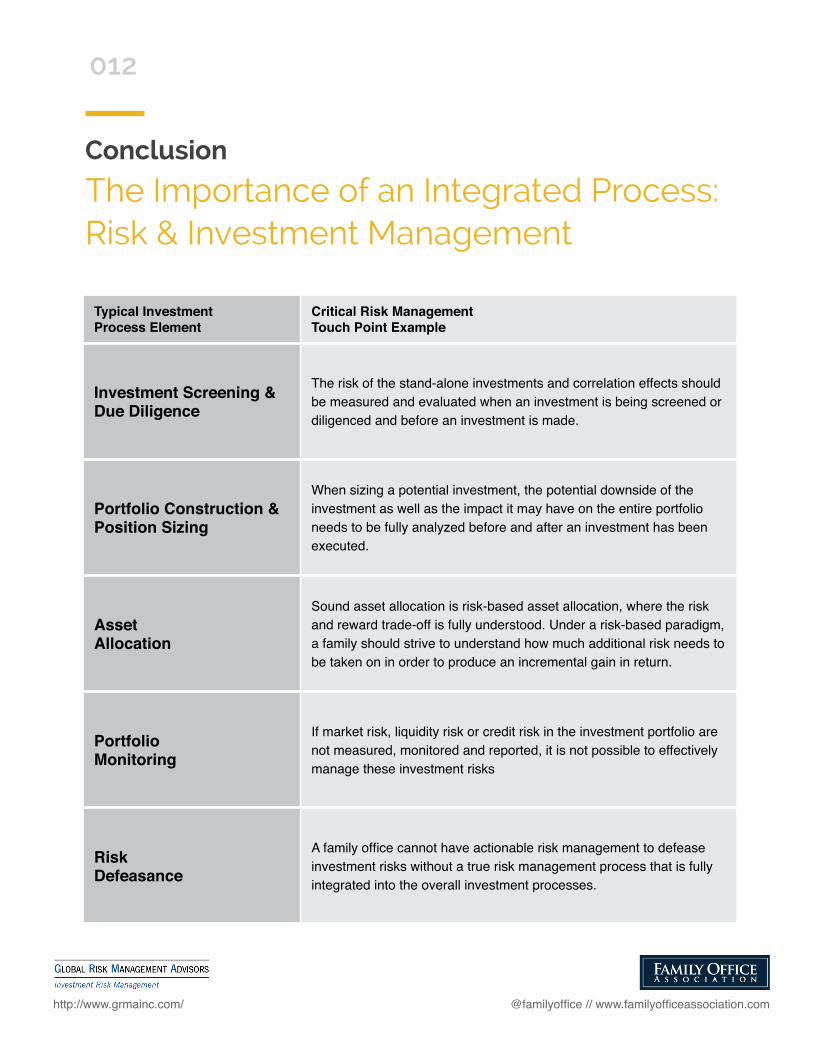

Conclusion

The Importance of an Integrated Process: Risk & Investment Management

Typical Investment Process Element

Critical Risk Management Touch Point Example

Investment Screening & Due Diligence

The risk of the stand-alone investments and correlation effects should be measured and evaluated when an investment is being screened or diligenced and before an investment is made.

Portfolio Construction & Position Sizing

When sizing a potential investment, the potential downside of the investment as well as the impact it may have on the entire portfolio needs to be fully analyzed before and after an investment has been executed.

Asset Allocation

Sound asset allocation is risk-based asset allocation, where the risk and reward trade-off is fully understood. Under a risk-based paradigm, a family should strive to understand how much additional risk needs to be taken on in order to produce an incremental gain in return.

Portfolio Monitoring

If market risk, liquidity risk or credit risk in the investment portfolio are not measured, monitored and reported, it is not possible to effectively manage these investment risks

Risk Defeasance

A family office cannot have actionable risk management to defease investment risks without a true risk management process that is fully integrated into the overall investment processes.

http://www.grmainc.com/ @familyoffice // www.familyofficeassociation.com

013

ABOUT

Global Risk ManagementAdvisors (GRMA)Global Risk Management Advisors, Inc. (GRMA) is the leading RiskTech and risk management advisory firm providing asset managers and investors with institutional-quality risk measurement, risk monitoring, risk reporting and risk management advisory as a complete and cost-effective managed service. GRMA principals are seasoned risk professionals with over 25 years each of front-line practitioner experience at major global financial institutions, asset management firms and in the government. Learn more at www.grmainc.com.

Samuel K. Won, Author, Founder and Managing Director of GRMAMr. Won has over 25 years of risk management, capital markets, trading and portfolio management experience at major financial institutions in the public and private sectors. In the investment management industry, Mr. Won was Chief Risk Officer at Brencourt Advisors, Chief Risk Officer at Ospraie Management, and he headed up investment risk management of over $44 billion in alternative assets for Citigroup Alternative Investments. On Wall Street, Mr. Won led trading risk management for institutional customer trading, proprietary trading and capital markets for Citigroup Global Markets, and he played a similar role at Dresdner Kleinwort Benson. In the public sector, Mr. Won was in charge of risk management for the capital markets portion of the bailout of the Savings and Loan industry during the 1980s. Mr. Won played a leading role, as Co-Chair of the Chief Risk Officers Steering Committee in creating the risk management section of the Managed Funds Association’s Sound Practices for Hedge Fund Managers. He has advised leading hedge funds, private equity funds, other asset managers, institutional-investors and regulatory agencies, including the SEC, the CFTC, the Federal Reserve, the Office of the Comptroller of the Currency and the FSA, on major risk management, trading and capital markets issues and policies.

Timothy S. Wilson, Editor, Managing Director & Head of Risk Services of GRMAMr. Wilson has over 25 years of experience in the fields of finance and financial risk management. He served as Chief Risk Officer for the investment management company Caxton Associates LP for eight years through 2011. Prior to joining Caxton, he worked for almost ten years in the firm-wide risk function at Morgan Stanley including heading the market risk function for Europe and Asia based in London. He had previously served as an Economist in the Division of International Finance of the Federal Reserve Board and as a Research Fellow in Economic Policy Studies at the Brookings Institution. Mr. Wilson played a leading role, as Co-Chair of the Chief Risk Officers Steering Committee in creating the risk management section of the Managed Funds Association’s Sound Practices for Hedge Fund Managers. He has also over time played a major role in a wide range of industry and joint public sector – private sector efforts to promote enhanced financial risk management practices.

Mingyang Liu, Contributor, Senior Analyst, Quantitative Risk Management and Strategy Group, GRMAHe has had experience working with a number of major asset manager and institutional investor clients. He competed a B.A. at Fudan University and received a Masters degree in Operations Research from Columbia University.

ABOUT the

FAMILY OFFICE ASSOCIATION

014

Family Office Association is a global community of ultra-high net worth families and their single family offices. We are committed to creating value for each family that we serve; value that grows wealth, strengthens legacy, and unites multiple generations by speaking to shared interests and passions. FOA has the resources to solve your most difficult challenges and help you achieve your collective goals: to invest intelligently, give strategically, and learn exponentially.

FOA is the community leader in serving all the key imperatives for ultra-high net worth families, respecting your privacy but enabling an intimate community of global families like yours. Our organization delivers private education and networking opportunities, proprietary research, and access to salient thought leadership that will interest all generations of your family.

Contact Family Office Association500 West Putnam Ave, Suite 400Greenwich, CT 06830Email: [email protected]: www.familyofficeassociation.comTwitter: @familyofficePhone: (203) 570.2898