Sales and Use Tax on Digital Products and Services in...

74

Sales and Use Tax on Digital Products and Services in 2013 Managing Multi-State Compliance Challenges for Vendors and Customers Today’s faculty features: 1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific Please refer to the instructions emailed to the registrant for the dial-in information. Attendees can still view the presentation slides online. If you have any questions, please contact Customer Service at 1-800-926-7926 ext. 10. TUESDAY, FEBRUARY 12, 2013 Presenting a live 110-minute teleconference with interactive Q&A Laurie Wik, Tax Director, Deloitte Tax, San Jose, Calif. Martin Eisenstein, Managing Partner, Brann & Isaacson, Lewiston, Maine Charles Kearns, Attorney, Sutherland Asbill & Brennan, Washington, D.C. For this program, attendees must listen to the audio over the telephone.

Transcript of Sales and Use Tax on Digital Products and Services in...

Sales and Use Tax on Digital

Products and Services in 2013 Managing Multi-State Compliance Challenges for Vendors and Customers

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

Please refer to the instructions emailed to the registrant for the dial-in information.

Attendees can still view the presentation slides online. If you have any questions, please

contact Customer Service at 1-800-926-7926 ext. 10.

TUESDAY, FEBRUARY 12, 2013

Presenting a live 110-minute teleconference with interactive Q&A

Laurie Wik, Tax Director, Deloitte Tax, San Jose, Calif.

Martin Eisenstein, Managing Partner, Brann & Isaacson, Lewiston, Maine

Charles Kearns, Attorney, Sutherland Asbill & Brennan, Washington, D.C.

For this program, attendees must listen to the audio over the telephone.

Sound Quality

Call in on the telephone by dialing 1-866-873-1442 and enter your PIN when

prompted.

If you have any difficulties during the call, press *0 for assistance. You may also

send us a chat or e-mail [email protected] immediately so we can address

the problem.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

Attendees must stay on the line throughout the program, including the Q & A

session, in order to qualify for full continuing education credits. Strafford is

required to monitor attendance.

Record verification codes presented throughout the seminar. If you have not

printed out the “Official Record of Attendance,” please print it now (see

“Handouts” tab in “Conference Materials” box on left-hand side of your computer

screen). To earn Continuing Education credits, you must write down the

verification codes in the corresponding spaces found on the Official Record of

Attendance form.

Please refer to the instructions emailed to the registrant for additional

information. If you have any questions, please contact Customer Service

at 1-800-926-7926 ext. 10.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the + sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides and the Official Record of Attendance for today's program.

• Double-click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

Sales and Use Tax on Digital Products and Services in 2013 Seminar

Martin Eisenstein, Brann & Isaacson

Feb. 12, 2013

Laura Wik, Deloitte Tax

Charles Kearns, Sutherland Asbill & Brennan

Today’s Program

Background Issues With Sales Tax And Digital Products

[Laurie Wik]

Special Issues, Latest Developments On Cloud Computing

[Martin Eisenstein]

Legislative Developments

[Charles Kearns]

Meaningful Actions At The SSTP

[Charles Kearns]

Problematic Digital Products And Services

[Martin Eisenstein, Laurie Wik and Charles Kearns]

Practical Issues Faced By Business Taxpayers

[Laurie Wik, Martin Eisenstein and Charles Kearns]

Slide 8 – Slide 16

Slide 63 – Slide 74

Slide 17 – Slide 31

Slide 32 – Slide 34

Slide 35 – Slide 40

Slide 41 – Slide 62

Notice

ANY TAX ADVICE IN THIS COMMUNICATION IS NOT INTENDED OR WRITTEN BY

THE SPEAKERS’ FIRMS TO BE USED, AND CANNOT BE USED, BY A CLIENT OR ANY

OTHER PERSON OR ENTITY FOR THE PURPOSE OF (i) AVOIDING PENALTIES THAT

MAY BE IMPOSED ON ANY TAXPAYER OR (ii) PROMOTING, MARKETING OR

RECOMMENDING TO ANOTHER PARTY ANY MATTERS ADDRESSED HEREIN.

You (and your employees, representatives, or agents) may disclose to any and all persons,

without limitation, the tax treatment or tax structure, or both, of any transaction

described in the associated materials we provide to you, including, but not limited to,

any tax opinions, memoranda, or other tax analyses contained in those materials.

The information contained herein is of a general nature and based on authorities that are

subject to change. Applicability of the information to specific situations should be

determined through consultation with your tax adviser.

BACKGROUND ISSUES WITH SALES TAX AND DIGITAL PRODUCTS

Laurie Wik, Deloitte Tax

Copyright © 2012 Deloitte Development LLC. All rights reserved. 9

Who, What, Where, Why And When

Digital products: Products and services provided or furnished

electronically

Popular terms include: SaaS, hosted, cloud computing, Web-enabled,

Web-based

Digital products examples

Sales to businesses: Software, data, information services,

searchable databases

Sales to consumers: Movies, songs, video games, premium-level

subscriptions to online social networks

Copyright © 2012 Deloitte Development LLC. All rights reserved. 10

Who, What, Where, Why And When (Cont.)

• States may assign a cloud computing transaction to one of the following

taxable categories:

Sale, rental or access to pre-written software

Data processing or data storage service

“Digital automated service”

Computer service or computer exchange Service

“Canned” information service

Digital equivalent to traditional tangible personal property, a.k.a.

digital goods

Copyright © 2012 Deloitte Development LLC. All rights reserved. 11

States’ positions on cloud computing include:

Not taxable because:

Not a sale or lease of software (TPP), because customer does not have

physical possession

Not a sale or lease of software, because vendor’s server is not in the state

The product is not pre-written software and not an enumerated taxable service.

Taxable because:

Taxable sale or lease of software (TPP) despite no physical transfer, because

customer has “constructive possession”

Taxable lease or rental of tangible personal property despite no physical

possession, because server is single-tenant server

Not an enumerated exemption from general tax on services

Customer receives the benefit of a taxable service, such as data processing or

information service, in the state.

Who, What, Where, Why And When (Cont.)

Copyright © 2012 Deloitte Development LLC. All rights reserved. 12

To which state is the transaction sourced?

Software applications or digital goods: Generally to the state where

accessed/downloaded by “user”

• Hosted services

– “Benefit received”

– “Principal place of business”

– “Point of delivery” or place from which accessed

• Global contracts often do not recognize users in multiple jurisdictions.

Who, What, Where, Why And When (Cont.)

Copyright © 2012 Deloitte Development LLC. All rights reserved. 13

Click-through legislation Affiliate nexus provisions

State Date legislation enacted Effective date of legislation Annual threshold Date legislation enacted Effective date of legislation

Arkansas 4/1/2011 10/24/2011 $10,000 4/1/2011 7/27/2011

California

ABX1-28 Enacted

6/28/2011, Retroactively

repealed 9/23/2011 AB 155

enacted 9/23/2011

9/15/12 $10,000 6/28/2011 9/15/12

Connecticut

Original enactment date

5/4/11, Second enactment

date 6/21/2011

5/4/2011

(Originally effective 7/1/11) $2,000

Georgia 4/19/2012 10/1/2012 $50,000

New York 4/23/2008 6/1/2008 $10,000

North Carolina 8/7/2009 8/7/2009 $10,000

Oklahoma 6/9/2010 7/1/2010 — $100,000 Threshold

Rhode Island 6/30/2009 7/1/2009 $5,000 6/30/2009 7/1/2009

South Dakota 3/11/2011 7/1/2011

Texas 7/19/2011 1/1/2012

Vermont 5/24/2011 When 15 other

states adopt $10,000 5/24/2011

When 15 other

states adopt

Illinois —

Unconstitutional 3/10/2011 7/1/2011 Unconstitutional as of 5/7/12 3/10/2011 7/1/2011

Other

Colorado 2/24/2010 3/1/2010

The Dept. of Revenue is

blocked from imposing the

notification requirements

pending the outcome of the

case effective 3/30/12

2/24/2010 3/1/2010

Maryland The Maryland House and Senate have been unable to reach an agreement regarding the version of the law. A conference committee has been appointed and is

reviewing the law.

Click-through And Affiliate Nexus Summary

Copyright © 2012 Deloitte Development LLC. All rights reserved. 14

Examples of states with guidance about in-state use of third-party servers:

• California

• Massachusetts

• New Mexico

• New York

• Ohio

• Pennsylvania

• Vermont

• Washington

• Texas

Sales Tax Nexus

Copyright © 2012 Deloitte Development LLC. All rights reserved. 15

Generally, states hold digital products purchasers responsible for unpaid

sales tax, when the vendor has not collected it from the purchaser. Sellers

may not collect because:

• Seller may not have established nexus for sales and use tax purposes

in the purchaser’s state; OR

• Seller may have established nexus for sales and use tax purposes,

but does not realize it or have the systems to handle sales tax

collection; OR

• Seller may have established nexus for sales and use tax purposes,

but has not researched or does not understand the proper taxability of

digital product offering; OR

• Seller may not be required to collect sales tax when the Streamlined

Sales Tax Project sourcing hierarchy is applicable.

Sellers And Purchasers: The Great Divide

Copyright © 2012 Deloitte Development LLC. All rights reserved. 16

Introduced federal legislation to require use tax collection by remote

sellers:

The Main Street Fairness Act (see also S.1452), H.R. 2701

The Marketplace Equity Act, H.R. 3179

The Marketplace Fairness Act, S. 1832

Legislation In Congress

SPECIAL ISSUES, LATEST DEVELOPMENTS ON CLOUD COMPUTING

Martin Eisenstein, Brann & Isaacson

Cloud Computing: What Is it?

• Amalgam of computer services

– Provider owns or leases equipment and software from third parties.

• Normally maintained in a data center

– Cloud computing customer contracts to access host equipment and/or software, and/or to obtain related services from the provider, on demand or on a usage/subscription fee basis.

– Access is usually over the Internet through any of a number of platforms (mobile devices, laptops, tablets, desktops).

18

Cloud Computing: What Is It? (Cont.)

• Types of service

– IaaS: Infrastructure as a service

• Access to data storage and computing resources

• E.g., Amazon Web services (“elastic compute cloud … elastic block storage”)

– SaaS: Software as a service (e.g., Salesforce.com)

• Access to software and/or applications

• Similar to application services

• Software remains on provider’s equipment and is not downloaded or physically delivered on CDs or DVDs.

19

Cloud Computing: What Is It? (Cont.)

– PaaS: Platform as a service

• Use by customer of customer’s created or owned applications on

provider’s software (languages, libraries, tools)

• E.g., Google app. engine

• May be a hybrid of SaaS and IaaS, but is treated most often as SaaS

as true object

– Hosting and managing e-mail

– Miscellaneous services such as privacy protection, or hosting Web page

or virtual private network within the cloud

20

Slide Intentionally Left Blank

Drivers Of Taxability Determination:

The Framework

• Characterization of the service

– Is it tangible personal property or a taxable service?

– Statutory/rule treatment: E.g., pre-written software

• Sourcing

– Where is the host situated?

– Where is the service used, and what documentation must be

provided to the provider?

» PA Form Rev – 1220

» Certificate of Multistate Points of Use

22

Drivers Of Taxability Determination:

The Framework (Cont.)

• State statutes re: whether taxable sale or lease takes place

• Bundled charge or separate charge by service

• Pertinent exemptions

• Nexus for customers and providers

• Resale exemptions for providers

23

Taxability Test By Service: IaaS

• Characterization

– Data processing or computer service

• TX, DC, CT and OH

– Lease or rental of computer space if provider’s computer is

situated there

• FL

• Storage: Chicago (lease tax) and UT (Utah Op. No. 06-

004)

– WA statute (digital automated services): Unclear at this point.

– General services statute: NM, SD, HI

24

Taxability Test By Service: IaaS (Cont.)

• Sourcing

– Where benefit received

• TX, WA, OH, CT

• Chicago re: data processing terminals

– Where service provided

• FL, Chicago, UT

– Where first use occurs

• WA: At host or customer’s terminals?

25

Taxability Test By Service: SaaS/PaaS

• Characterization

– As tangible personal property: 12 states do not tax pre-written

software delivered electronically.

– Increasing of states have dealt with taxability of SaaS and App

service provider services

• Generally treated under a true object test as pre-written

software delivered electronically

– CT treats it as a computer service.

– TX treats it as a data processing service. See, e.g., Letter Ruling No.

200401223L

– SC treats it as a communications service.

26

Taxability Test By Service:

SaaS/PaaS (Cont.)

• Sourcing

– To state where software is hosted and not where used

• KS: Private letter rulings 0-2010-005, P-2007-006, P-2011-010

– To state where used/accessed

• Increasing number of states: PA, UT, NY, TX, OH, DC, WA,

NM and HI

– Not taxable (e.g., MD)

– SC taxes only intrastate communications.

27

Taxability Test By Service:

SaaS/PaaS (Cont.)

• Has a sale taken place of SaaS (when treated as tangible personal

property)?

– Expansive definition

• NY: Sale is “any transfer of title or possession or both and

any lease or license to use” and a right to use constitutes a

license to use. 20 N.Y. Comp. Codes R and Regs. Sect.

526.7(e)(4)(iii)

– Narrow definition

• AZ (Ariz. Reg. 15-5-154.B), IL 86 IL Admin. Code Sec.

130.1935(a)(1) and RI (RI Code R. SU11-25.7(2) may

also restrict taxability, because SaaS is not deemed a sale.

28

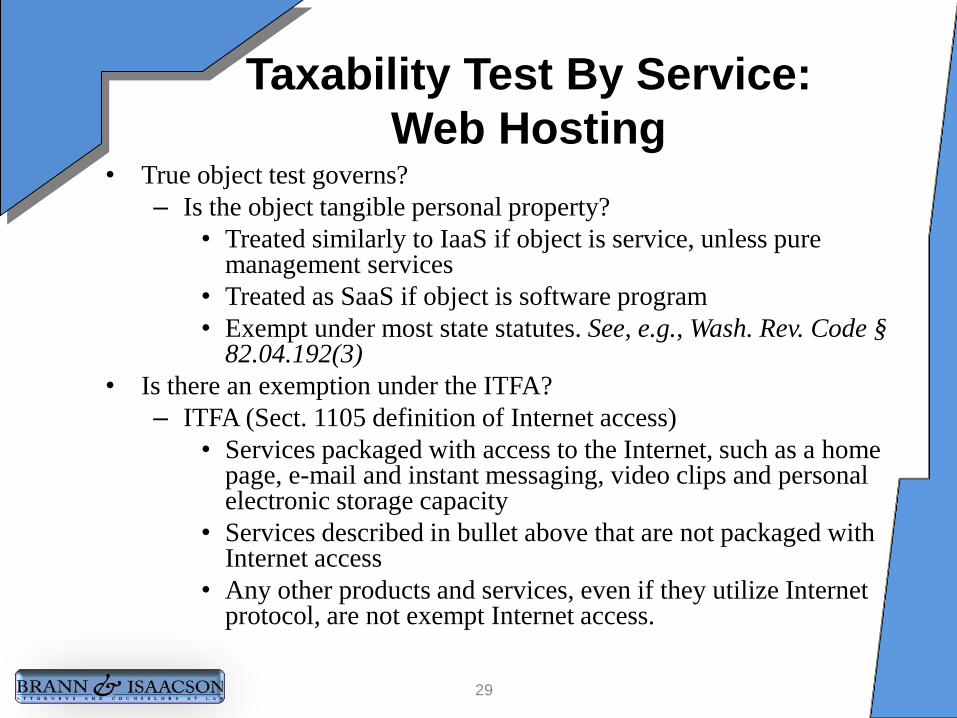

Taxability Test By Service:

Web Hosting • True object test governs?

– Is the object tangible personal property?

• Treated similarly to IaaS if object is service, unless pure management services

• Treated as SaaS if object is software program

• Exempt under most state statutes. See, e.g., Wash. Rev. Code § 82.04.192(3)

• Is there an exemption under the ITFA?

– ITFA (Sect. 1105 definition of Internet access)

• Services packaged with access to the Internet, such as a home page, e-mail and instant messaging, video clips and personal electronic storage capacity

• Services described in bullet above that are not packaged with Internet access

• Any other products and services, even if they utilize Internet protocol, are not exempt Internet access.

29

New Developments

• SaaS taxable where accessed

– PA Letter Ruling No. SUT-12-001: Reverses prior ruling so taxable if used in PA

• Presumption used in PA if billed to PA, unless submit PA certificate REV-1220

– UT: Letter Ruling No. 10-001 reverses course like PA

• True object tax

– TN Revenue Ruling No. 12-11: Electronic access to books on server located outside TN is deemed sale of tangible personal property in TN.

• Exemption of SaaS in certain states

– VT: Statutory moratorium until 6/30/13 on tax on SaaS

– WI: 1/25/13 – SaaS and IaaS not taxable

30

Other Issues Regarding Taxability

• Billing

– Should there be a bundled fee or a fee by type of service?

• SSTA may not permit unbundling as relates to cloud

computing. See also TN ruling

• Some state statutes may permit

– 34 Texas Admin. Code Sect. 3.330(d)(2)

• Ideal is to break up fee into separate charges by service.

– Into IaaS, SaaS/PaaS, and other services

– Characterization on invoice is important.

31

LEGISLATIVE DEVELOPMENTS Charles Kearns, Sutherland Asbill & Brennan

Digital Economy Legislation

• Tax base expansion

• Minnesota

• Maine

• Massachusetts

• Exemptions

• Utah

• Washington State

• Vermont

• Michigan

33

Digital Economy Legislation (Cont.)

• Video game taxes

• New York

• Connecticut

• Credits and incentives

• Data center equipment

• Video game development

• Streamlined conformity legislation

• Federal legislation affecting state taxes

• Marketplace Fairness Act

• Digital Goods and Services Tax Fairness Act

34

MEANINGFUL ACTIONS AT THE SSTP

Charles Kearns, Sutherland Asbill & Brennan

©2012 Sutherland Asbill & Brennan LLP

DC

Streamlined Sales Tax Overview

SSTP member states

SSTP associate member

states

States with SSTP

legislation

introduced/considered

in 2012

SSTP bills drafted but

not yet introduced

WA

OR

CA

NV

ID

MT

WY

UT

AZ

CO

NM

TX

ND

LA

SD

NE

KS

OK

MN

IA

MO

AR

WI

IL

MI

IN OH

KY

TN

MS AL GA

FL

SC

NC

WV VA

PA

NY

VT NH

ME

NJ

MA

RI

NH

CT

MD

DE

AK

As of Feb. 23, 2012

36

©2012 Sutherland Asbill & Brennan LLP

Uniform Definitions

• “Specified digital products”

Digital audio works (includes “ringtones”)

Digital audio-visual works

Digital books

Digital codes

• “Transferred electronically”

As used in the digital goods context, defined as “obtained by

the purchaser by means other than tangible storage media”

Compare “delivered electronically,” as used in the computer

software context, with “delivered to the purchaser by means

other than tangible storage media”

Implications on cloud computing in SSTP member states

37

©2012 Sutherland Asbill & Brennan LLP 38

Operating Rules

Sect. 332

• Operating rules that permit member states to select “toggles” in

their digital goods tax imposition statutes, or mandate how

certain transactions should be taxed

“Electronically transferred” or “specified digital products”

• “End user”

• “Permanent use”

• “Continued payment”

• Subscriptions

38

©2012 Sutherland Asbill & Brennan LLP

Digital Products Sourcing

SLAC sourcing work group

SLAC formed a digital products sourcing work group in

October 2011 to address sourcing regime for digital goods

under the Agreement.

Definitions of “receipt,” recordkeeping and MPU

39

Slide Intentionally Left Blank

PROBLEMATIC DIGITAL PRODUCTS AND SERVICES

Martin Eisenstein, Brann & Isaacson

Laurie Wik, Deloitte Tax

Charles Kearns, Sutherland Asbill & Brennan

Digital Products

• Typical situation: Download of books, music, videos to computer

• Access on servers situated outside of state

– TN: Digital products that can be viewed or downloaded in TN

are deemed sales of digital products.

• Providing online code to access products

– True object test as to taxability

– States vary as to when taxable

• TX, IL and NY

• TN and SSUTA states

42

Taxability Of E-Books, Digital Audio Works

(Music), Software And Digital Video

State Electronic Books

Taxable?

Digital Music

Taxable?

Digital Canned

Software Taxable?

Digital Video Taxable?

AL Yes Yes Yes Yes

AK n/a n/a n/a n/a

AZ Yes Yes Yes Yes

AR* No No No No

CA No No No No

CO Yes Yes No** Yes

CT Yes, at a reduced rate

of 1%

Yes, at a reduced rate

of 1%

Yes, at a reduced rate

of 1%

Yes, at a reduced rate

of 1%

DE n/a n/a n/a n/a

.

DC Yes Yes Yes Yes

43

* Per SSTA Taxability Matrix Appendix ** Changed from presentation of March 2012

Taxability Of E-Books, Digital Audio Works

(Music) Software And Digital Video (Cont.)

State Electronic Books

Taxable?

Digital Music

Taxable?

Digital Canned

Software Taxable?

Digital Video

Taxable? FL No No No No

GA* No No No No

HI Yes Yes Yes Yes

ID Yes Yes Yes Yes

IL No No Yes, unless qualified as

an exempt software

license

No

IN* Yes Yes Yes Yes

IA* No No No No

KS* No No Yes No

KY* Yes Yes Yes No**

LA Yes Yes** Yes Yes

44

* Per SSTA Taxability Matrix Appendix ** Changed from presentation of March 2012

Taxability Of E-Books, Digital Audio Works

(Music) Software And Digital Video (Cont.)

State Electronic Books

Taxable?

Digital Music

Taxable?

Digital Canned

Software Taxable?

Digital Video

Taxable? ME Yes Yes Yes Yes

MD No No No No

MA No No Yes No

MI* No No Yes No

MN* No No Yes No

MS Yes Yes Yes Yes

MO No No No No

MT n/a n/a n/a n/a

NE* Yes Yes Yes Yes

NV* No No No No

45

Taxability Of E-Books, Digital Audio Works

(Music) Software And Digital Video (Cont.) State Electronic Books

Taxable?

Digital Music

Taxable?

Digital Canned

Software Taxable?

Digital Video

Taxable? NH n/a n/a n/a n/a

NJ* Yes Yes Yes Yes

NM Yes Yes Yes Yes

NY No, provided e-book is

not revised or updated

more than annually and

is not designed to work

with software other than

the e-reader software**

Generally, products

transferred

electronically are not

taxable unless they are

taxable software or

otherwise qualify as

taxable TPP.

Yes No

NC* Yes Yes Yes Yes

ND* No No Yes No

OH* No No Yes No

OK* No No No No

OR n/a n/a n/a n/a

PA No No Yes No

46

* Per SSTA Taxability Matrix Appendix **Changed from presentation of March 2012

Taxability Of E-Books, Digital Audio Works

(Music) Software And Digital Video (Cont.)

State Electronic Books

Taxable?

Digital Music

Taxable?

Digital Canned

Software Taxable?

Digital Video

Taxable? RI* No No Yes No

SC No No No No

SD* Yes Yes Yes Yes

TN Yes Yes Yes Yes

TX* Yes Yes Yes Yes

UT* Yes Yes Yes Yes

VT* Yes Yes Yes Yes

VA No No No No

WA* Yes Yes Yes Yes

WV* No No Yes No

WI* Yes Yes Yes Yes

WY* Yes Yes Yes Yes

47

Data Processing

• TX, CT, OH and DC tax

• Includes storage, processing of information and retrieval of information

• Examples include:

– Entry of data

– Maintenance of employee work time

– Preparing payroll

• Who operates the computers?

– TX (taxable) vs. OH (non-taxable), if operated by customers

48

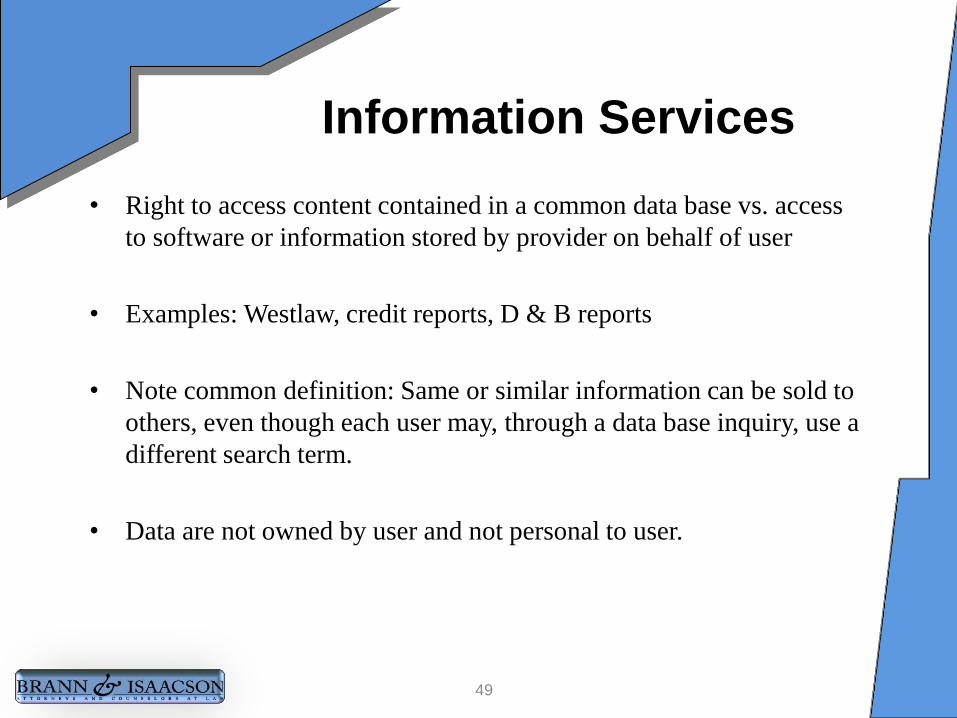

Information Services

• Right to access content contained in a common data base vs. access

to software or information stored by provider on behalf of user

• Examples: Westlaw, credit reports, D & B reports

• Note common definition: Same or similar information can be sold to

others, even though each user may, through a data base inquiry, use a

different search term.

• Data are not owned by user and not personal to user.

49

Information Services (Cont.)

• Many big states (including FL, OH, NY, NJ, TX and CT) impose tax, with varying exemptions and rates/

– Texas exempts 20%/

– CT tax is s reduced rate of 1%/

• But, note that MA and many other states do not tax. See, e.g., MA Letter Ruling 11-2

– Internet-based service can be exempt under ITFA.

• Varying interpretation of term and taxability

– NY: Broad interpretation includes individual reports/

– FL: More narrow interpretation excludes furnishing of information of a personal nature.

– NY taxes information provided electronically; FL does not.

– Taxability of webinars: Follows taxability of information services, except in FL and NJ

50

What Is A Communication Service?

• In general, a communication service is the transmission of signals,

images, sounds, data or other information between two points. In

general, it includes related services such as voice mail.

• FL statute (Sect. 202.11(2)) as an example:

– Taxable communications services means the “transmission,

conveyance, or routing of voice, data, audio, video, or any other

information or signals … to a point or between or among points …

[and includes] computer processing applications that are used to act

on the form … of the content for purposes of the transmission.” But,

the term excludes Internet access service, e-mail or similar computer

services.

• The emphasis is on the transmission of data and not on the content.

51

How Sourcing Can

Become Problematic

• Three sourcing situations:

1) Delivery within the state by a provider situated in the state

2) Customer has access via a terminal connected to a server in another state.

3) Receipt of service at more than one location

52

How Sourcing Can

Become Problematic (Cont.)

1) Delivery within the state by a provider situated in the state

• All states treat this as an intra-state sale and subject to tax only in the state of service.

• No other state has nexus with the transaction and could tax the sale under the Commerce Clause. See Goldberg v. Sweet, 488 U.S. 252 (1989)

53

Sourcing Issues: State

Approaches To Interstate Delivery

2) Customer has access via a terminal connected to a server in another state.

• All states tax 100% of taxable services delivered in the state, except for FL’s tax on use of a server situated in FL, Chicago’s tax on lease of personal property insofar as storage space (but not on data processing/information services), and SSTA states in limited circumstances (as described in a subsequent slide).

54

Slide Intentionally Left Blank

Sourcing Issues: State

Approaches (Cont.) – Interstate delivery: The general rule

• The location of the terminal for access to the service controls; see, e.g., NYS (TSB-A-10(52)S 10/18/10); CT (ADC 12-426-27(d)); TX (Rules 3.330 and 3.342)

• Issue is the proof of where the service is received.

• OH and WA permit use of billing address as a proxy of where the service is used, in the absence of a certificate of use. Ohio Rev. Code Sect. 5739.033.

• Test under Goldberg: Is the billing address or service address in the state, and does service originate or terminate in the state?

56

Sourcing Issues: State

Approaches (SSTA)

• The SSTA waterfall approach (OH: R.C. 5739.033(C))

• If service received (i.e., first use) at the vendor’s place of

business, sourced at the vendor’s place of business

• If not received at the vendor’s place of business, sourced at

the location of receipt known to the vendor

• If neither of the above, then sourced at the address of the

customer, as known from the vendor’s business records

• If none of the above, then the address given in the transaction

• If none of the above, from where the service was provided

57

Sourcing Issues: State Approaches

(Several Locations For Receipt Of Service)

3) Receipt of service at more than one location

• NY, CT, DC rules are generally silent on multi-office access.

• In TSB-A-10(52)S 10/18/10, New York permitted apportionment based on the ratio of New York-based employees with access to the service to the number of employees located throughout the U.S. with access.

• In TSB-A-03(5)S, 1/31/03, acceptance of certificate relieved a provider of liability for non-NY employees, so long as the provider obtains detailed information regarding address of employees of customer. Provider is still liable for tax for NY-based employees.

• This is consistent with Goldberg and avoids multiple-taxation.

58

Sourcing Issues: State Approaches (Several

Locations For Receipt Of Service), Cont.

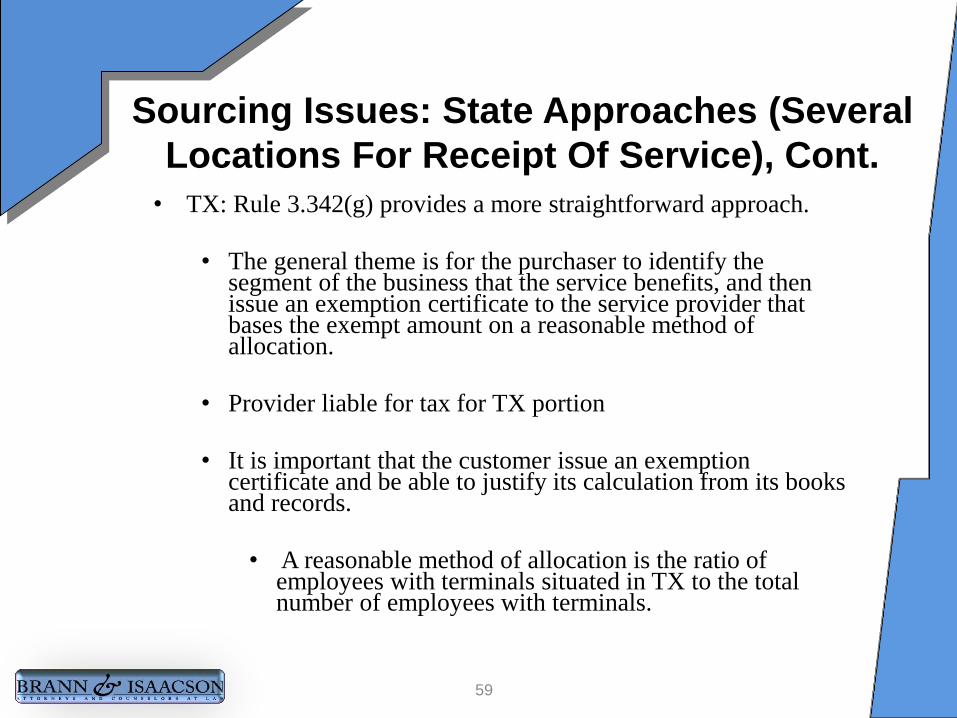

• TX: Rule 3.342(g) provides a more straightforward approach.

• The general theme is for the purchaser to identify the segment of the business that the service benefits, and then issue an exemption certificate to the service provider that bases the exempt amount on a reasonable method of allocation.

• Provider liable for tax for TX portion

• It is important that the customer issue an exemption certificate and be able to justify its calculation from its books and records.

• A reasonable method of allocation is the ratio of employees with terminals situated in TX to the total number of employees with terminals.

59

Sourcing Issues: State Approaches (Several

Locations For Receipt Of Service), Cont.

• OH approach: R.C. 5739.033(D)

• If the purchaser provides an exemption certificate, then the

vendor is relieved of collection responsibility for the entire

tax, and the purchaser may use any reasonable, consistent and

uniform method of apportioning purchases by jurisdiction.

• In the absence of an exemption certificate, the vendor and

customer can work out a reasonable, consistent and uniform

method of apportionment. If the customer certifies to the

same, then this method governs, and the provider pays tax on

the OH percentage.

• If the customer does not certify, the law requires reversion to

the SSTA waterfall approach. But, that leads to uncertainty.

60

Sourcing Issues: Multi-State Uses

• Use of exemption certificates

• WA (WA Rev. Code Sect. 82.08.02088) permits provider to obtain an exemption certificate from the user for services used outside of the state, if the customer accepts responsibility for payment of the tax due on services used in the state.

61

Copyright © 2012 Deloitte Development LLC. All rights reserved. 62

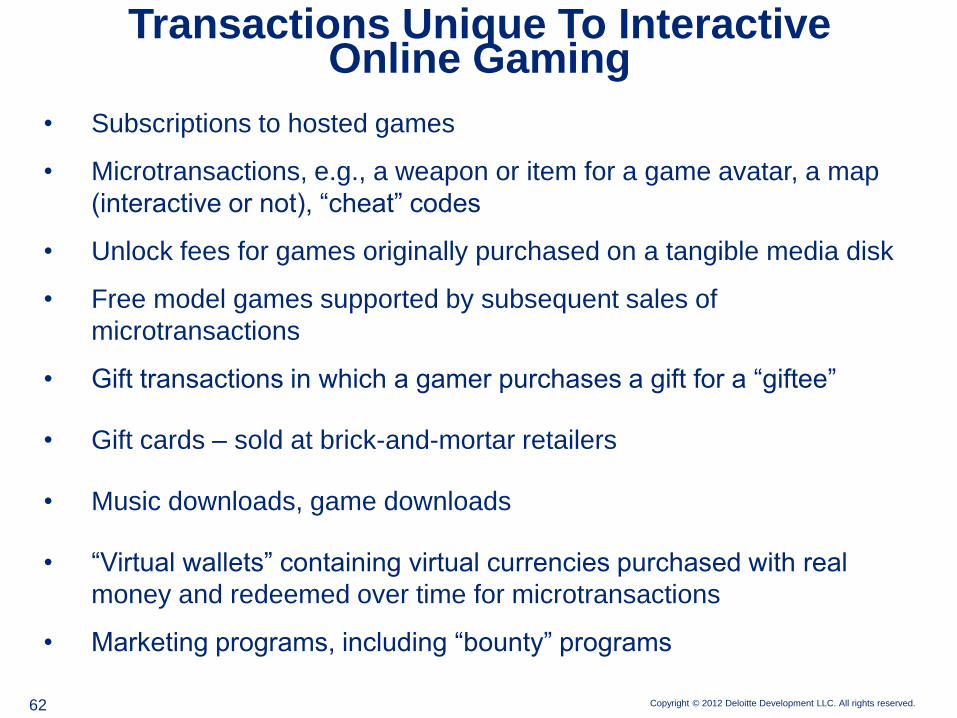

• Subscriptions to hosted games

• Microtransactions, e.g., a weapon or item for a game avatar, a map

(interactive or not), “cheat” codes

• Unlock fees for games originally purchased on a tangible media disk

• Free model games supported by subsequent sales of

microtransactions

• Gift transactions in which a gamer purchases a gift for a “giftee”

• Gift cards – sold at brick-and-mortar retailers

• Music downloads, game downloads

• “Virtual wallets” containing virtual currencies purchased with real

money and redeemed over time for microtransactions

• Marketing programs, including “bounty” programs

Transactions Unique To Interactive Online Gaming

PRACTICAL ISSUES FACED BY BUSINESS TAXPAYERS

Laurie Wik, Deloitte Tax

Martin Eisenstein, Brann & Isaacson

Charles Kearns, Sutherland Asbill & Brennan

Copyright © 2012 Deloitte Development LLC. All rights reserved.

A company will purchase certain commercial information from a vendor

that provides the information via its “risk management solutions

database”. The company’s users will access the vendor’s database from

California, Massachusetts and New Jersey.

How should tax apply in each state tor the vendor’s product offerings?

Core service offering: For a subscription fee, the company can access

business information about potential or existing customers and suppliers

through the “core service offering,” which is an interactive, customizable,

Web-based application. It provides the company’s users access to the

vendor’s global database of more than 110 million businesses. The

company’s users will be able to run searches and create customizable

reports containing summary trade data, basic credit scores, legal filings

and general company information.

Case Study (Deloitte)

57

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Workflow “add-ons”: The company can add to the core service offering

by purchasing workflow add-ons for a separately invoiced additional fee.

The company will not receive any software to install on its server. The

workflow add-ons include the following:

1. Decision-making tool: A customizable tool that enables users to

establish rules and approval limits to automate credit decisions. It

provides access to a credit service and has the ability to verify trade

and bank references.

2. Account manager: A feature with which the company can manage the

risk of its customer base by blending the company’s credit policy and

customer's accounts receivable data with information from the

vendor’s database.

Case Study (Deloitte), Cont.

58

Copyright © 2012 Deloitte Development LLC. All rights reserved.

Workflow “add-ons” (Cont.)

3. Collection tool: The collection tool is an on-demand tool to help manage

overall risk exposure. It enables the company to enter invoice-level trade

details and provides workflow information related to collection activities.

4. Online credit application: The online credit application allows the user

to create a customizable credit application. The data entered into the

application is analyzed by the vendor’s software, and that analysis is

made available to the user. The software provides internal automatic

alerts when an application is submitted.

Case Study (Deloitte), Cont.

59

Copyright © 2012 Deloitte Development LLC. All rights reserved. 67

This presentation contains general information only and Deloitte is

not, by means of this presentation, rendering accounting, business,

financial, investment, legal, tax, or other professional advice or

services. This presentation is not a substitute for such professional

advice or services, nor should it be used as a basis for any decision

or action that may affect your business. Before making any decision

or taking any action that may affect your business, you should

consult a qualified professional advisor. Deloitte shall not be

responsible for any loss sustained by any person who relies on this

presentation.

Copyright © 2012 Deloitte Development LLC. All rights reserved. 68

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited,

a UK private company limited by guarantee, and its network of

member firms, each of which is a legally separate and independent

entity. Please see www.deloitte.com/about for a detailed description

of the legal structure of Deloitte Touche Tohmatsu Limited and its

member firms. Please see www.deloitte.com/us/about for a detailed

description of the legal structure of Deloitte LLP and its subsidiaries.

Certain services may not be available to attest clients under the

rules and regulations of public accounting.

Hypotheticals

(From Brann & Isaacson)

• Cloud service provider with data centers in Ohio but

with offices in Tennessee and Texas

• Cloud service provider provides the following services:

– Bundled service including storing customer’s data,

processing data, use of provider’s SAS accounting

software, hosting e-mail

– Remote access services provided from the data

center that allow a customer to establish a secure

connection between a customer’s home-based

computer and remote computers

69

Hypotheticals (From Brann

& Isaacson), Cont.

• Customer 1, headquartered in Texas but with offices in Illinois

and New York, has contracted for the bundled service, for which

it is billed at its Texas headquarters. Where, if anywhere, is the

service taxable?

– Would the answer differ if the customer did not use

exemption certificates?

• Customer 2, which has offices in Massachusetts (home base),

New York and Maryland, contracts for the remote access

services.

– Is the service taxable, and if so, where?

– Where does the customer have nexus?

– Where should the provider collect tax on orders?

– Where must the customer pay taxes?

70

Slide Intentionally Left Blank

©2012 Sutherland Asbill & Brennan LLP

Bundled Transactions

• Existing bundled transaction rules may be ill-equipped to

address innovative digital bundles.

• Problematic areas

• Streamlined states vs. non-Streamlined states

• Bundles involving communications services

• Divergent sourcing regimes

• Application of Internet Tax Freedom Act’s “accounting rule”

• Promotions and reallocation of sales price

72

©2012 Sutherland Asbill & Brennan LLP

Hypothetical (Sutherland Asbill)

Bundled transactions

• Kentucky

• Bundles involving tangible personal property, “digital

property” and/or streaming video

• Sales and use taxes

• Excise tax

• Gross revenues tax

• Florida

• Bundles involving tangible personal property, digital goods

and/or “communications services”

• Sales and use taxes

• Communications services tax

73

©2012 Sutherland Asbill & Brennan LLP

Hypothetical (Sutherland Asbill), Cont.

• Over-the-top video customer purchases a subscription with a vendor-supplied converter box in:

Miami

Chicago

Indianapolis

Kenner, La.

Seattle

• Over-the-top video customer purchases a subscription for viewing on laptop in:

Miami

Chicago

Indianapolis

Kenner, La.

Seattle

• Do the results change if the customer purchases on-demand video for one-time viewing, rather than a subscription?

74