SAHPMM Fall Conference - Arkansas Hospital Association

30

SAHPMM Fall Conference Little Rock, Arkansas October 18, 2013 Doug Jones AVP, Business Development HealthTrust

Transcript of SAHPMM Fall Conference - Arkansas Hospital Association

SAHPMM Fall Conference Little Rock, Arkansas

October 18, 2013

Doug Jones AVP, Business Development HealthTrust

3. Reform

4. Implications and Early Results

2. The Players

1. The Market

Medical Devices in the Era of Healthcare Reform

Gaining Physician Alignment Understanding the physician mindset

Managing successful relationship with physician and c-suite

The supplier perspective

Medical Device Expenditures

$6.8

Spine

$6.7

Hips & Knees

$5.2

Osteobiologics

$6.3

Cardiac Rhythm Management

$1.9

Drug Eluting Stents

US Market (Billions)

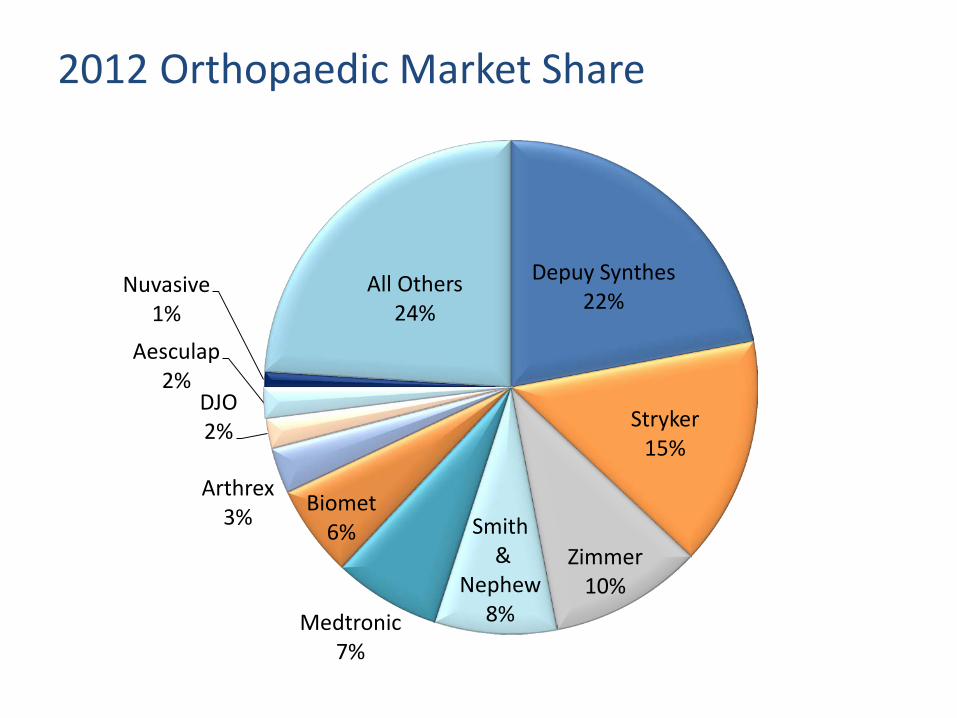

2012 Orthopaedic Market Share

Depuy Synthes 22%

Stryker 15%

Zimmer 10%

Smith &

Nephew 8% Medtronic

7%

Biomet 6%

Arthrex 3%

DJO 2%

Aesculap 2%

Nuvasive 1%

All Others 24%

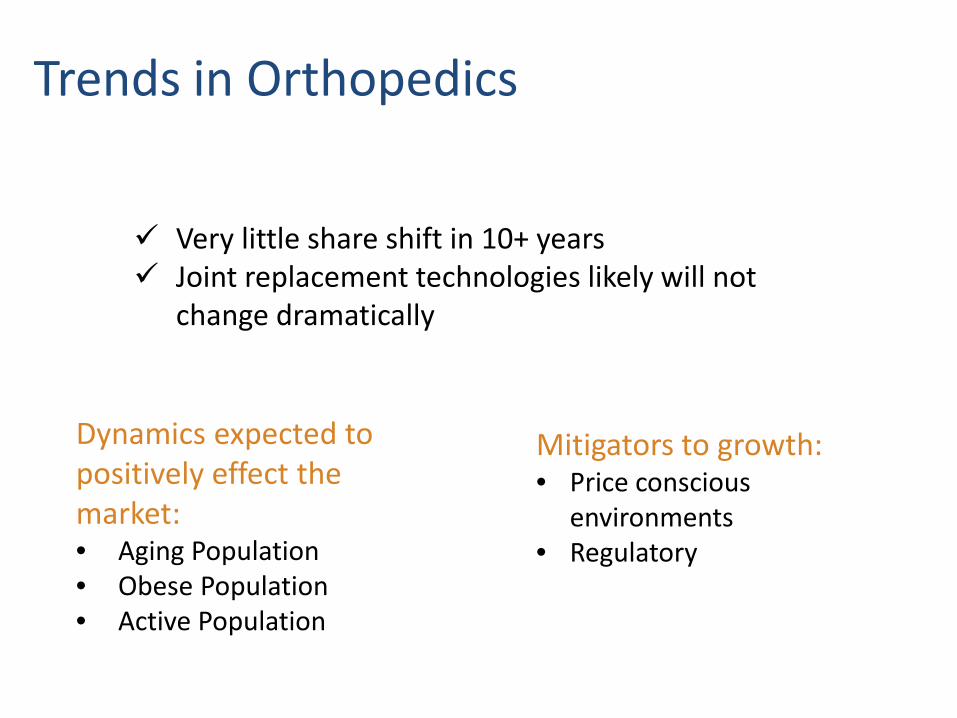

Trends in Orthopedics

Very little share shift in 10+ years Joint replacement technologies likely will not

change dramatically

Dynamics expected to positively effect the market: • Aging Population • Obese Population • Active Population

Mitigators to growth: • Price conscious

environments • Regulatory

Spine Market Highly competitive

Medtronic 36%

Depuy Synthes 25%

• 90% controlled by top 10 players

• Serious competition from smaller players

Intensely price sensitive

Challenging reimbursement environment

Healthcare Reform

Requires quality data analytics that can be difficult

AUC & quality outcomes a must for payment

Vendor Partnerships

Find value in market share and alignment

Look to help with process efficiencies; not just “widgets”

Supply Chain Costs PPI has “commoditized” in recent years – alignment comes easier

Difficult to find year-over-year savings anymore

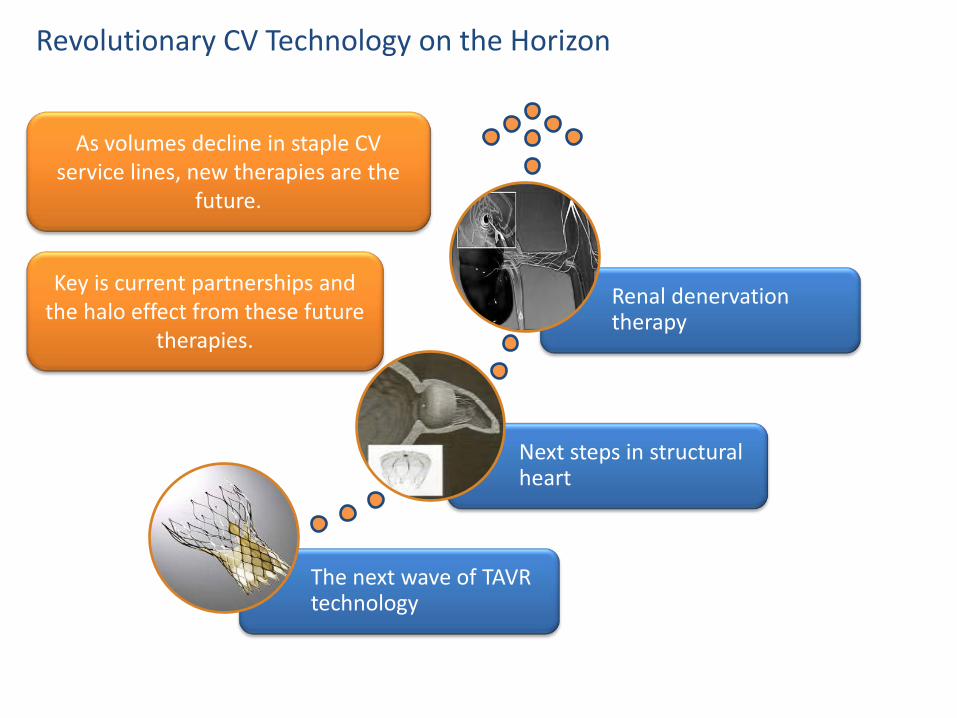

Trends in the Cardiovascular Space

The next wave of TAVR technology

Next steps in structural heart

Renal denervation therapy

As volumes decline in staple CV service lines, new therapies are the

future.

Key is current partnerships and the halo effect from these future

therapies.

Revolutionary CV Technology on the Horizon

Market Overview Osteobiologics: Class of materials that promote the healing of fractures and bone defects

There are over 1500 biologic products from nearly 400 companies.

An est. 84% of osteobiologics are used in spine surgeries

Challenges There are very few human clinical studies in this market, making it difficult to prove product efficacy

Because of the numerous surgical approaches in spine surgery, physician utilization and product mixing vary tremendously

Osteobiologics presents the largest implant growth opportunity for suppliers

There is a large cost variation between suppliers (ex. 10cc/ml DBM product)

Osteobiologic Platforms 2012 National US Sales

•Machined Bone Allograft

•Demineralized Bone Matrix (DBM)

•Cell Based (Stem Cell)

•Bone Morphogenetic Protein (BMP)

• Synthetic

$564 million

$285 million

$315 million

$230 million

$220 million

$6.7 billion in 2010

$9.6 billion by 2015

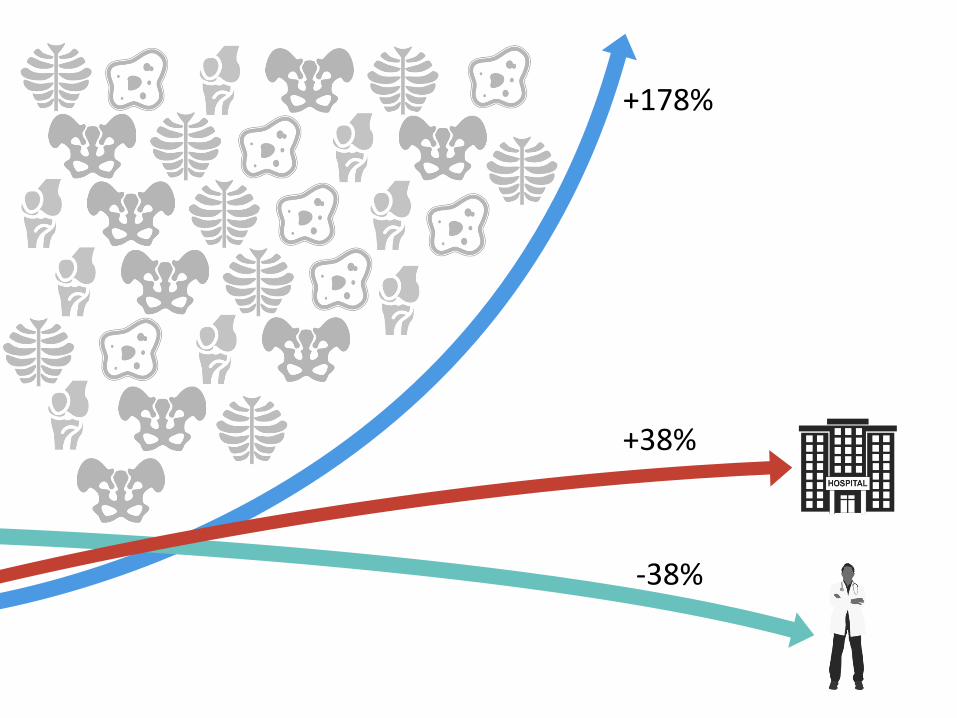

The spend on hip and knee implants is growing.

+ +

Over $20 billion

More than we spend as a nation for space exploration.

That pays for all the scientists working to colonize Mars.

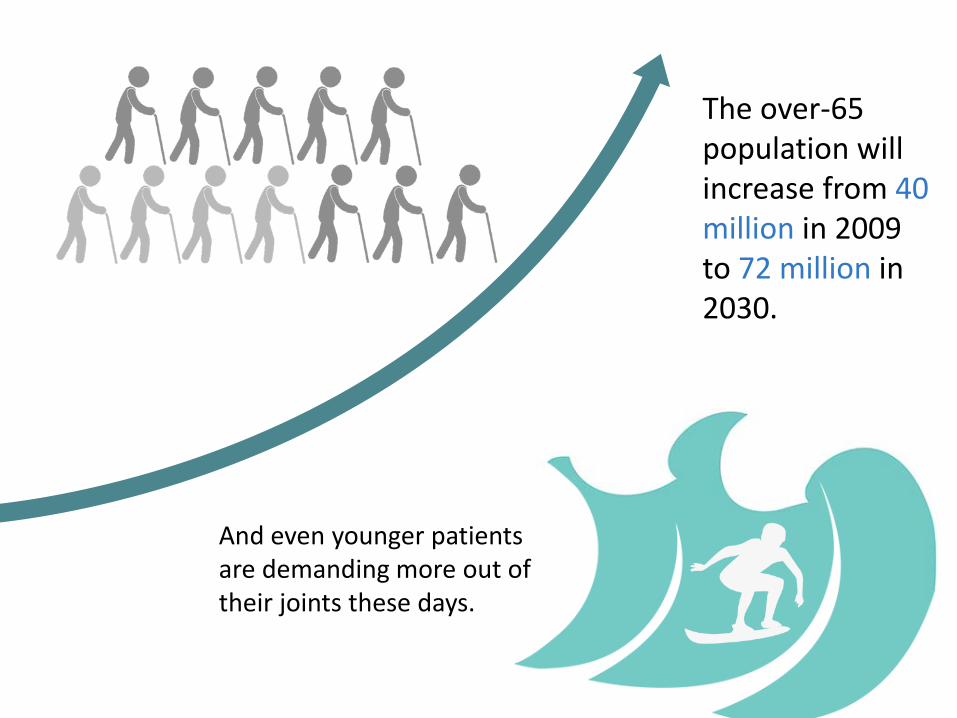

The over-65 population will increase from 40 million in 2009 to 72 million in 2030.

And even younger patients are demanding more out of their joints these days.

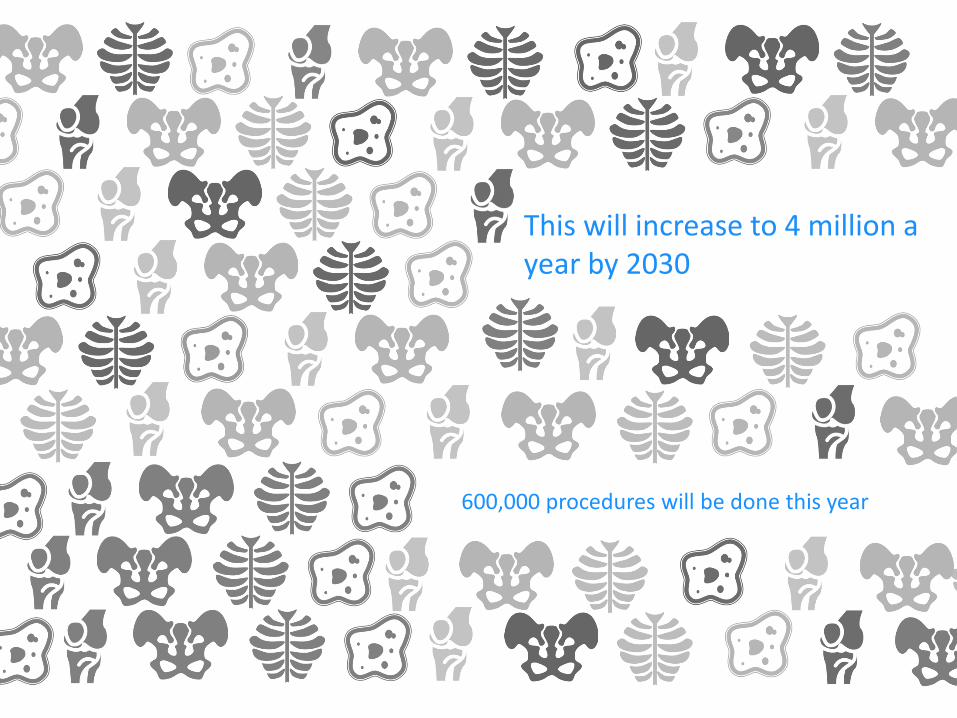

600,000 procedures will be done this year

This will increase to 4 million a year by 2030

+178%

+38%

-38%

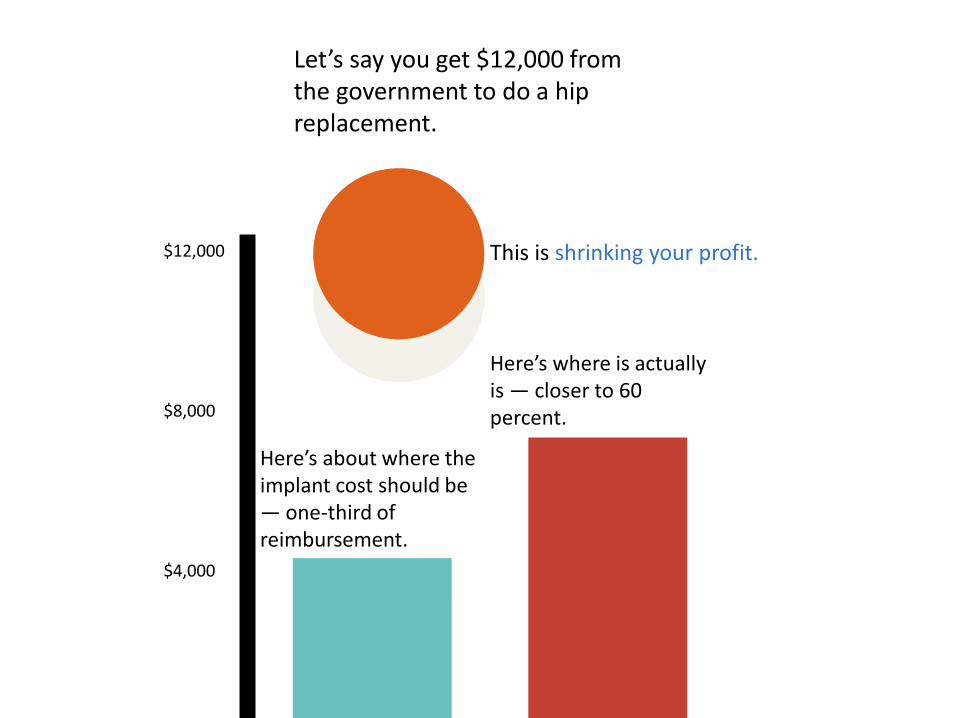

Let’s say you get $12,000 from the government to do a hip replacement.

$12,000

$8,000

$4,000

Here’s about where the implant cost should be — one-third of reimbursement.

Here’s where is actually is — closer to 60 percent.

This is shrinking your profit.

Doctors don’t think like we do.

2. The Players

MBAs MDs

The Problem

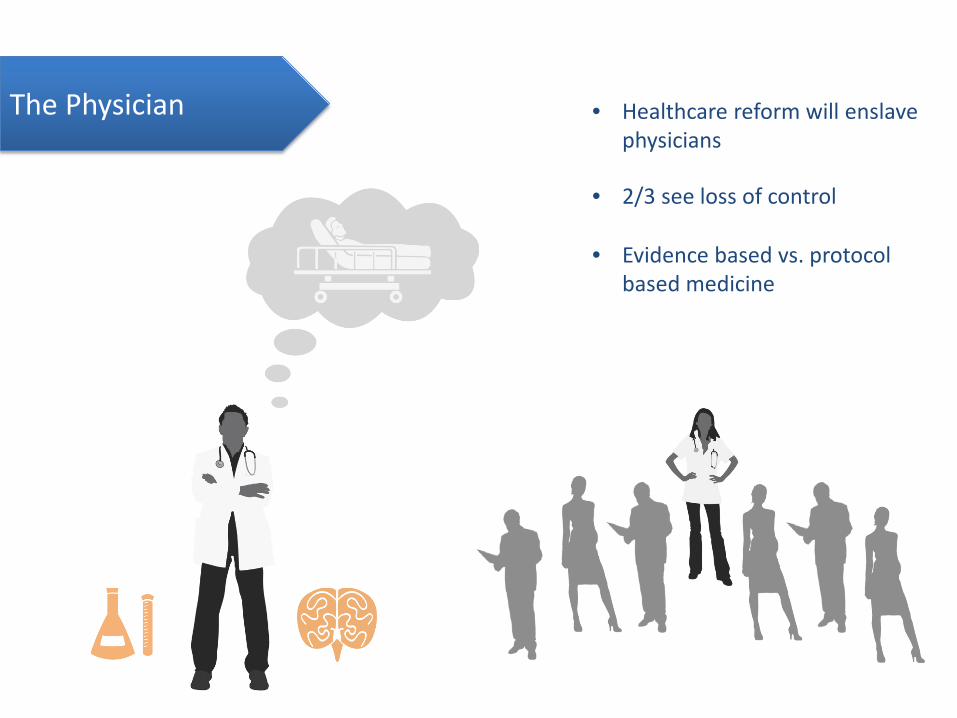

The Physician • Healthcare reform will enslave physicians

• 2/3 see loss of control

• Evidence based vs. protocol based medicine

Doctors see a one-dimensional relationship

$ $ $ $

The Physician Who has responsibility for reducing costs?

• Trial lawyers 60% • Insurance companies 59% • Hospitals/suppliers 56% • Patients 53% • Doctors 36%

Employed Physicians

The Physician

300% rise

60% “not happy”

“I didn’t go to provider school”

The sales rep fills the service “gap”.

The Rep-Less Model Service vs. Sales

Alternate Service Roles

• PA

Supplier Perspective

Product Development • Innovation or Marketing? • Evolutionary or Revolutionary • Stair-step Approach

Who is the customer? • Aligned Incentives?

Medical Device Tax

3. Reform

Regulatory Financial

Insurers

The Drivers of Reform

Direct: Government intervention

Indirect:

FDA Sunshine Act Joint Registry ACOs/Value-Based

To 7%

Impact of Joint Registry

In the US 1% Reduction = $30M

They provide evidence that, if delivered to physicians in a timely and understandable fashion, will positively influence physician behavior to the benefit of patients and society.

Early Warning System Recalls Product Algorithm

Revision Rate From 17%

FDA Approvals

2 Current Paths 510(K)

PMA

Proposed Changes 515 Project

• Device Reclassification

ACOs to Date

• Pioneer sites – Modest savings/quality improvements

• Potential to change dynamics

• Creating environment for physician and provider collaboration

• Future???

From volume-based to value-based

4. Implications and Early Results

Cultural Change Hospitals take back control Decision making

Physician as partner Maintain clinical autonomy Patient-centric

What Will It Take?

Questions?