SADC Financial Integration - World Banksiteresources.worldbank.org/.../PM-ArthurCousinsSADC.pdf ·...

30

SADC Financial Integration CPSS - World Bank Forum on Retail Payments Cape Town – December 2013

Transcript of SADC Financial Integration - World Banksiteresources.worldbank.org/.../PM-ArthurCousinsSADC.pdf ·...

SADC Financial Integration

CPSS - World Bank Forum on Retail Payments

Cape Town – December 2013

Agenda

• Where the region started

• When the integration agenda got going

• Strategic approach to integration

• Where are we now

• Where to next

• Questions

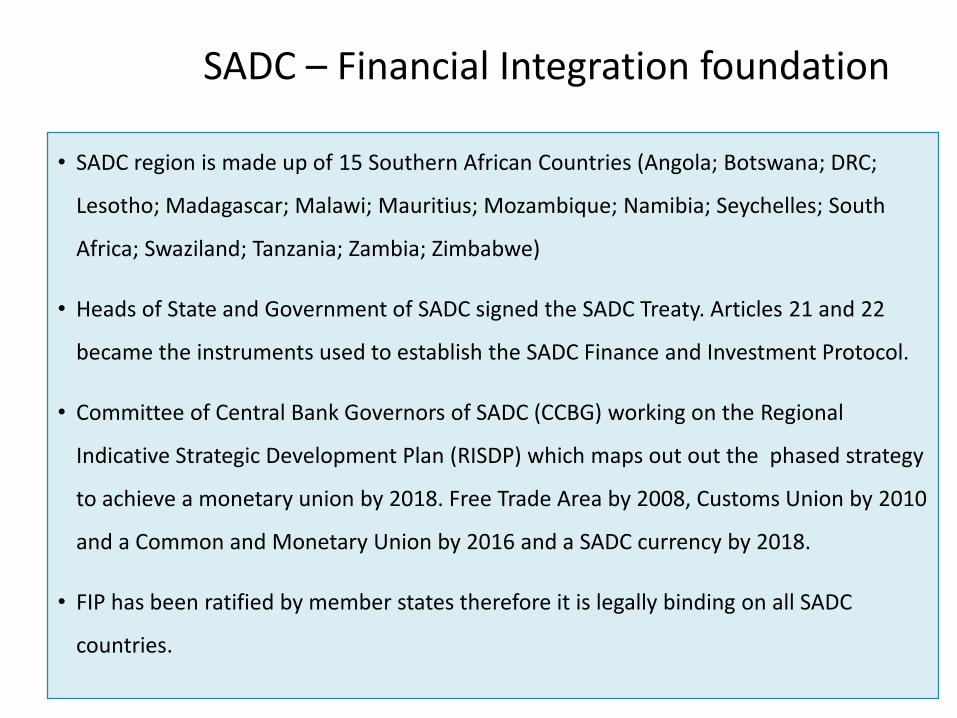

SADC – Financial Integration foundation

• SADC region is made up of 15 Southern African Countries (Angola; Botswana; DRC;

Lesotho; Madagascar; Malawi; Mauritius; Mozambique; Namibia; Seychelles; South

Africa; Swaziland; Tanzania; Zambia; Zimbabwe)

• Heads of State and Government of SADC signed the SADC Treaty. Articles 21 and 22

became the instruments used to establish the SADC Finance and Investment Protocol.

• Committee of Central Bank Governors of SADC (CCBG) working on the Regional

Indicative Strategic Development Plan (RISDP) which maps out out the phased strategy

to achieve a monetary union by 2018. Free Trade Area by 2008, Customs Union by 2010

and a Common and Monetary Union by 2016 and a SADC currency by 2018.

• FIP has been ratified by member states therefore it is legally binding on all SADC

countries.

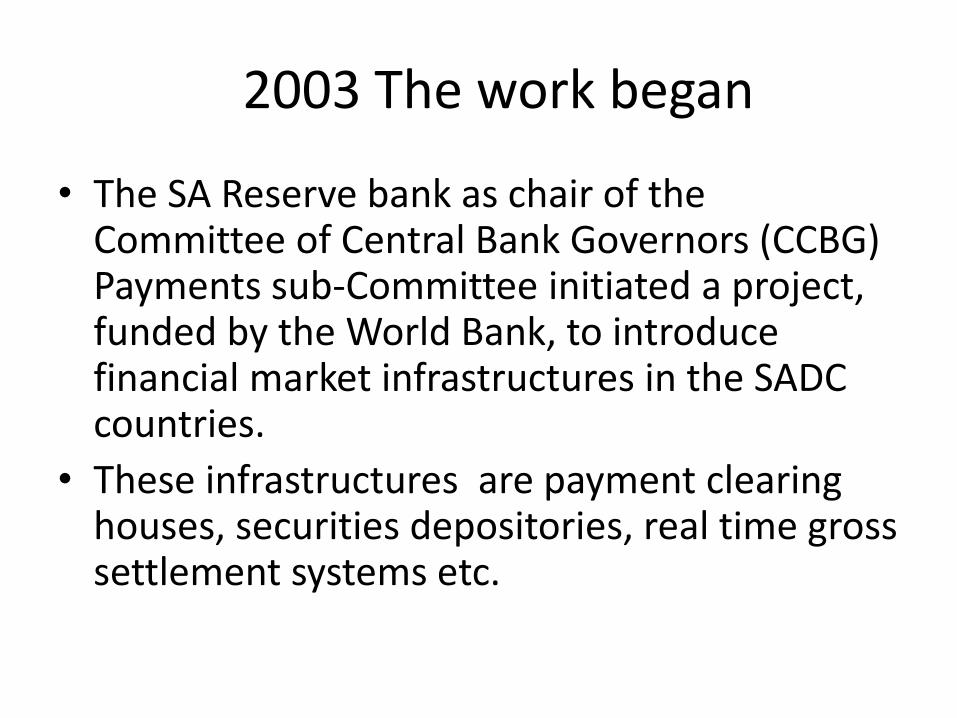

2003 The work began

• The SA Reserve bank as chair of the Committee of Central Bank Governors (CCBG) Payments sub-Committee initiated a project, funded by the World Bank, to introduce financial market infrastructures in the SADC countries.

• These infrastructures are payment clearing houses, securities depositories, real time gross settlement systems etc.

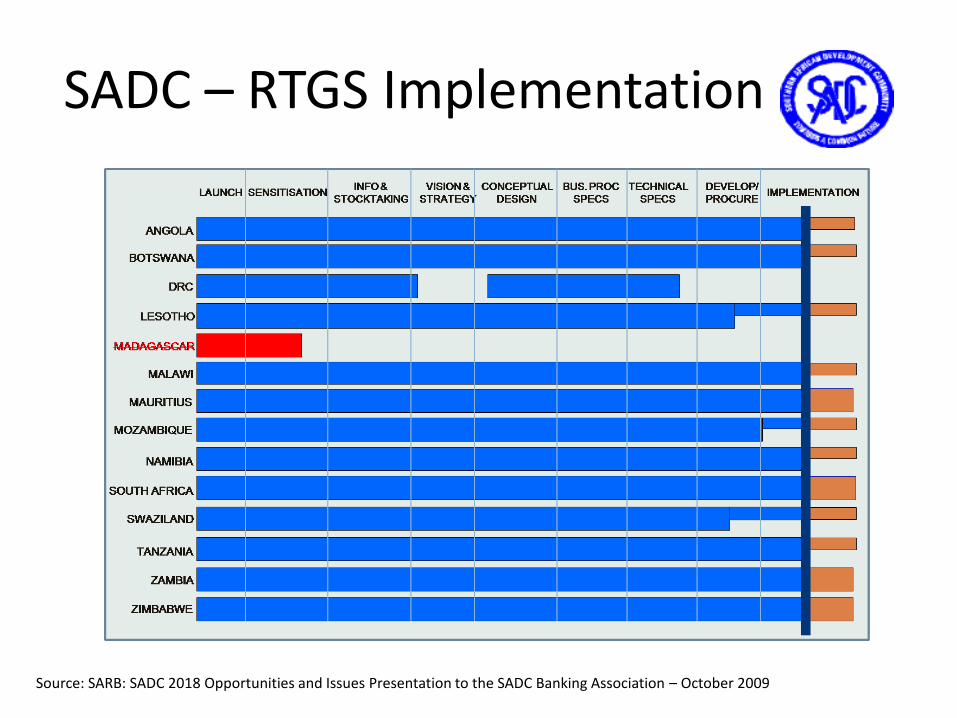

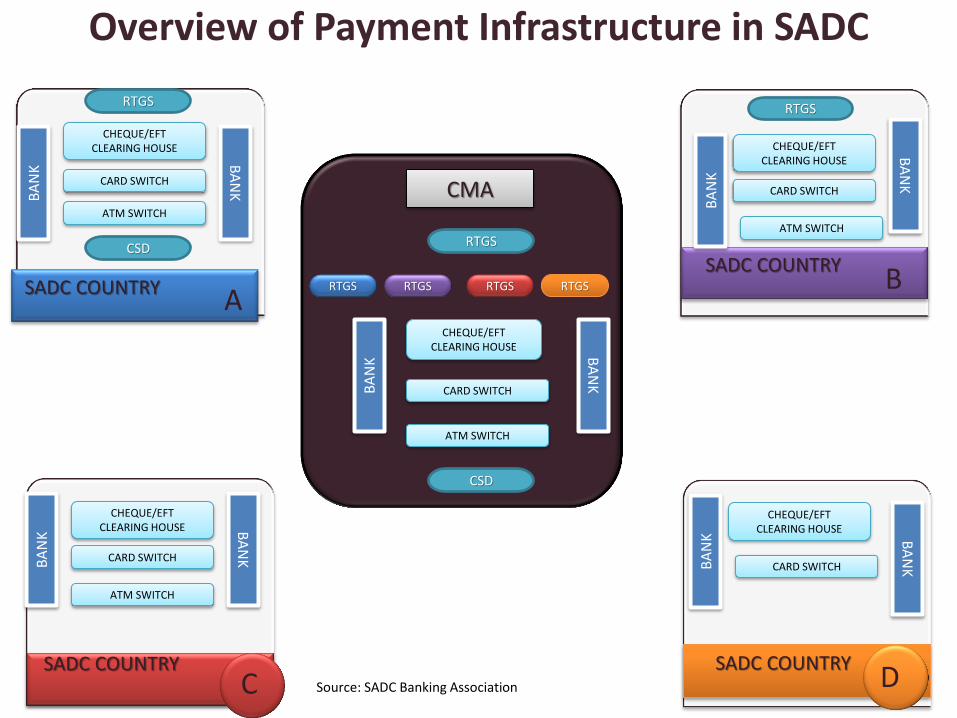

SADC – RTGS Implementation

Source: SARB: SADC 2018 Opportunities and Issues Presentation to the SADC Banking Association – October 2009

Overview of Payment Infrastructure in SADC

RTGS

BA

NK

RTGS

CHEQUE/EFT CLEARING HOUSE

CARD SWITCH

ATM SWITCH

CSD

BA

NK

BA

NK

RTGS RTGS RTGS RTGS

CMA

SADC COUNTRY B

RTGS

CHEQUE/EFT CLEARING HOUSE

CARD SWITCH

ATM SWITCH

BA

NK

BA

NK

D SADC COUNTRY

CHEQUE/EFT CLEARING HOUSE

CARD SWITCH BA

NK

BA

NK

CHEQUE/EFT CLEARING HOUSE

CARD SWITCH

ATM SWITCH

BA

NK

BA

NK

C SADC COUNTRY

Source: SADC Banking Association

CHEQUE/EFT CLEARING HOUSE

CARD SWITCH

ATM SWITCH

CSD

SADC COUNTRY A

BA

NK

When the integration agenda got going

• As can be seen from the previous slides much progress has been achieved

• Using this situation as a base the CCBG then decided to move to the next phase in 2010

• The next phase entailed inter-linking the financial infrastructures of the SADC countries

• The pre-planning phase commenced in late 2009

Key Strategic Principles

1. Project focus: cross border & intra-SADC transactions

2. Use of existing infrastructures wherever possible – banks choose providers

3. Use of international standards to ensure interoperability

4. Invest for straight through processing

5. Each country will keep its own currency and financial infrastructure

6. Regional settlement currency to be the ZAR (South African Rand)

7. Start with Common Monetary Area and build out

8. Cross-border cheques to be phased out

Proposed Infrastructures

The following key infrastructures were proposed for the SADC region:

1. A regional inter-bank settlement system to be run by the CCBG – SIRESS

2. A regional clearing capability for EFT credits and debits

3. A regional clearing capability for Card/ATM transactions

4. A clearing and settlement capability for cross border securities transactions

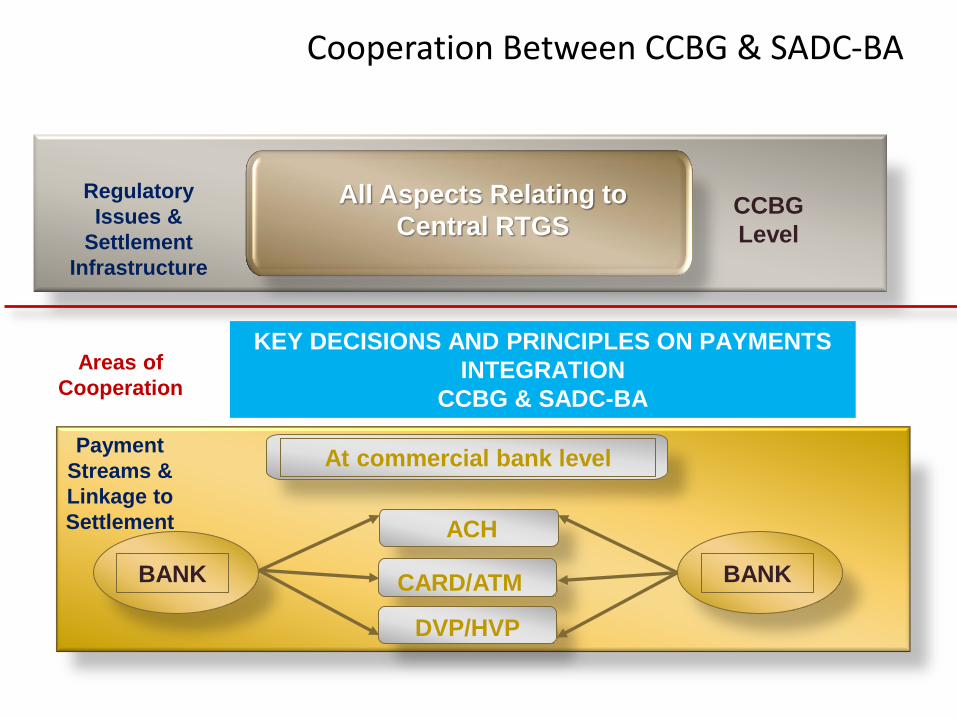

Cooperation Between CCBG & SADC-BA

Regulatory

Issues &

Settlement

Infrastructure

CCBG

Level

Payment

Streams &

Linkage to

Settlement ACH

BANK BANK

At commercial bank level

KEY DECISIONS AND PRINCIPLES ON PAYMENTS

INTEGRATION

CCBG & SADC-BA

Areas of

Cooperation

All Aspects Relating to

Central RTGS

CARD/ATM

DVP/HVP

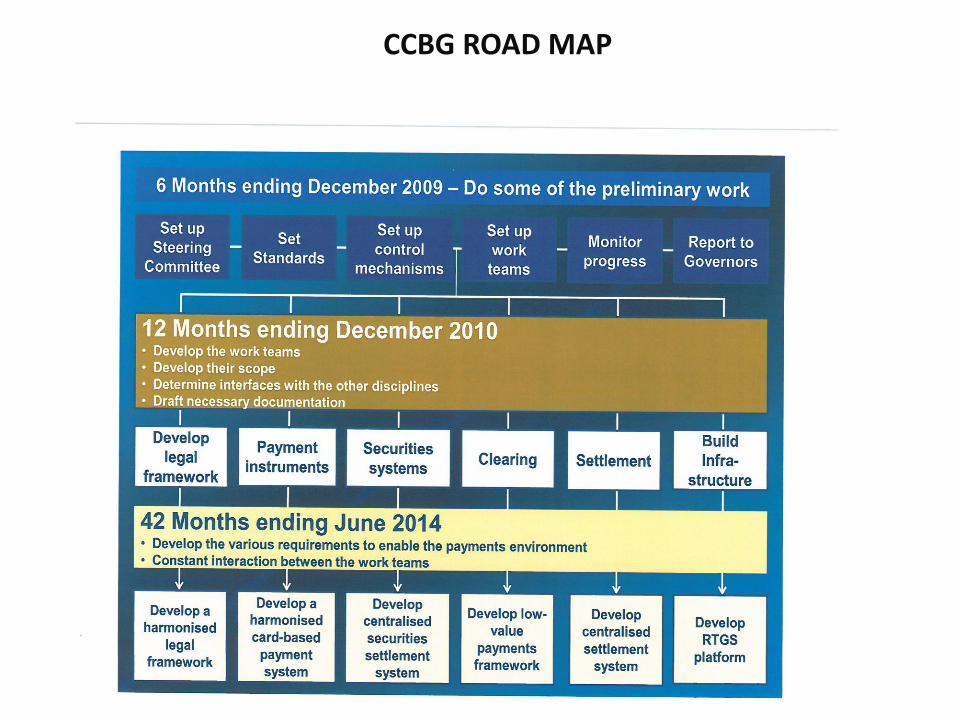

CCBG ROAD MAP

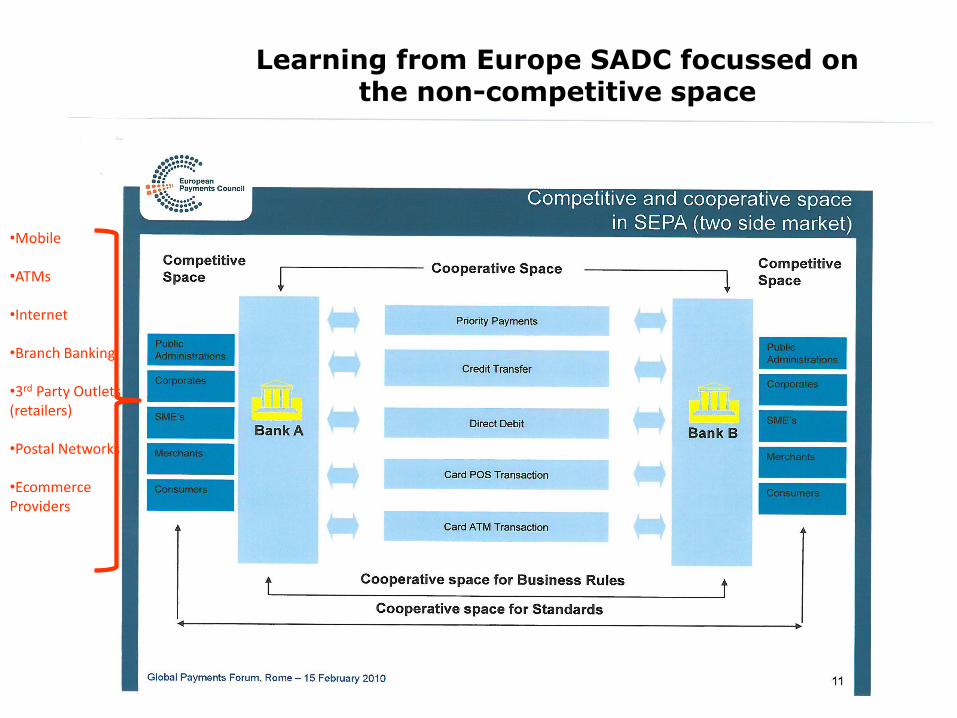

Learning from Europe SADC focussed on the non-competitive space

•Mobile •ATMs •Internet •Branch Banking •3rd Party Outlets (retailers) •Postal Networks •Ecommerce Providers

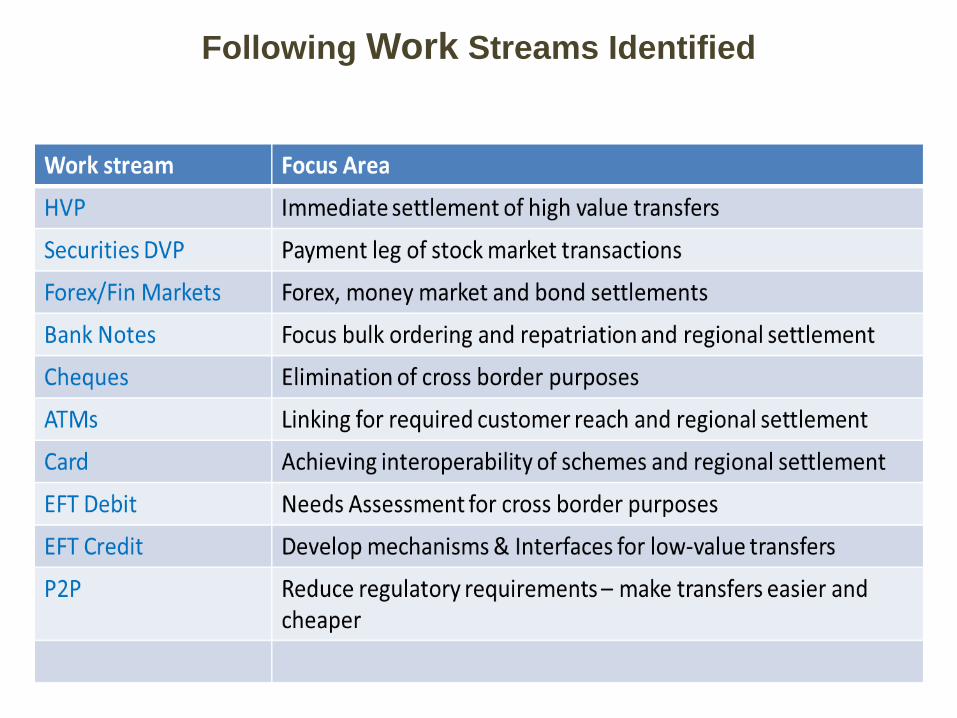

Following Work Streams Identified

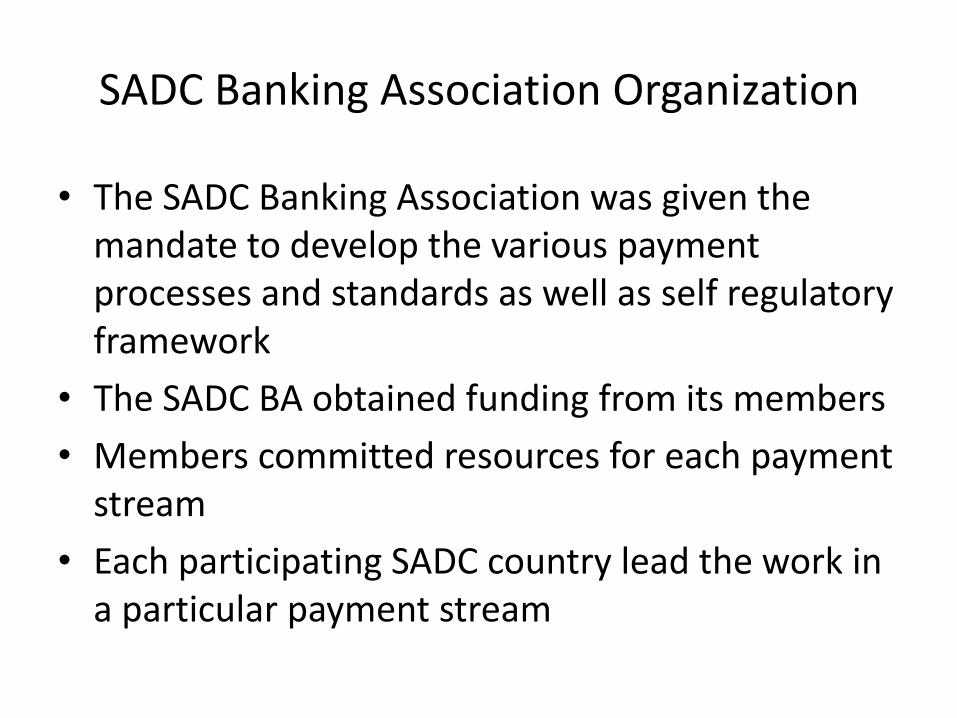

SADC Banking Association Organization

• The SADC Banking Association was given the mandate to develop the various payment processes and standards as well as self regulatory framework

• The SADC BA obtained funding from its members

• Members committed resources for each payment stream

• Each participating SADC country lead the work in a particular payment stream

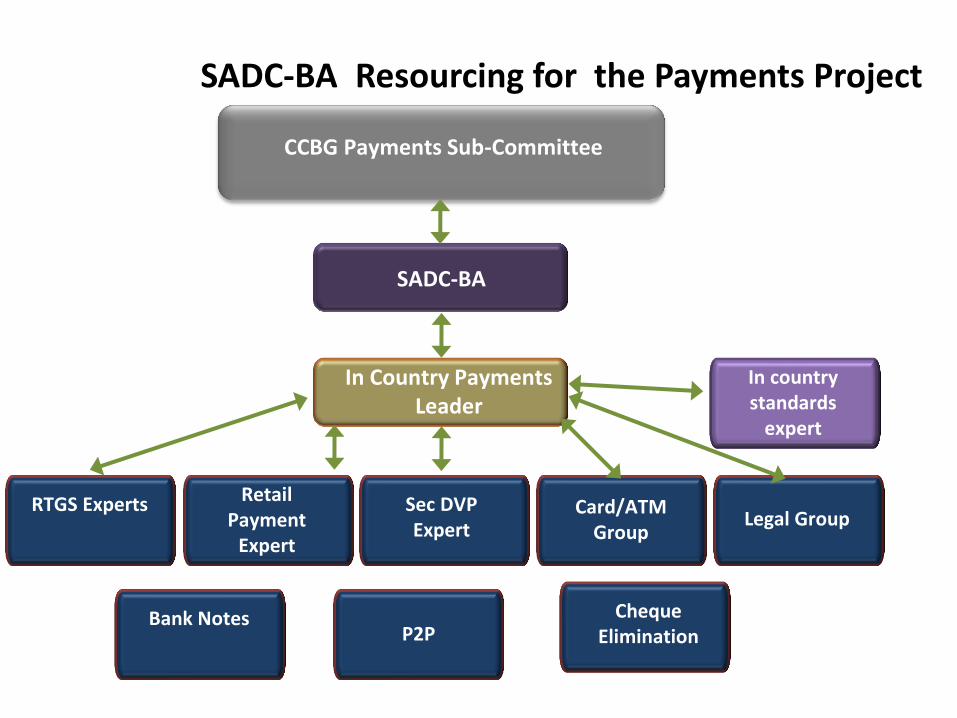

SADC-BA Resourcing for the Payments Project

CCBG Payments Sub-Committee

SADC-BA

In Country Payments Leader

RTGS Experts Retail Payment

Expert

Sec DVP Expert

Card/ATM Group

Legal Group

In country standards

expert

Bank Notes P2P

Cheque Elimination

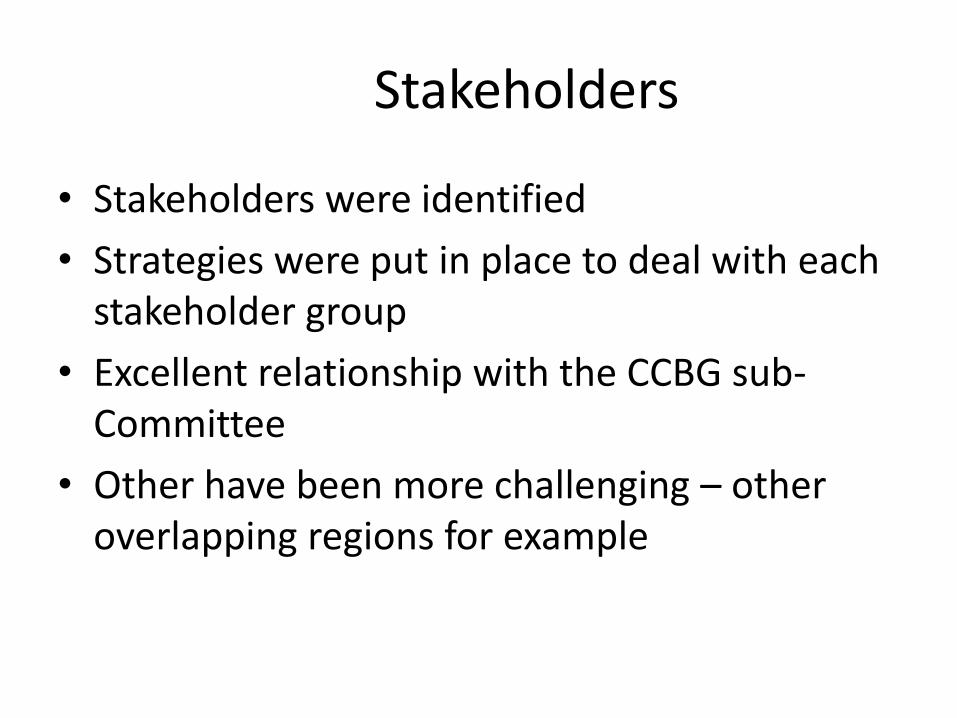

Stakeholders

• Stakeholders were identified

• Strategies were put in place to deal with each stakeholder group

• Excellent relationship with the CCBG sub-Committee

• Other have been more challenging – other overlapping regions for example

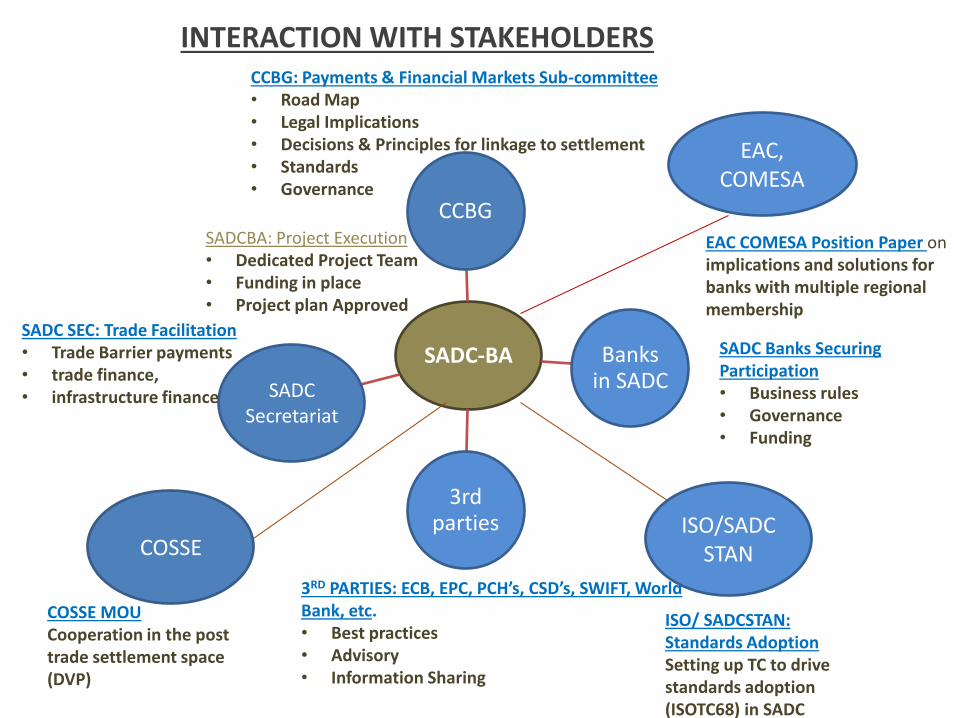

SADC-BA

CCBG

Banks in SADC

3rd parties

SAD

SADC SEC: Trade Facilitation • Trade Barrier payments • trade finance, • infrastructure finance

SADC Banks Securing Participation • Business rules • Governance • Funding

3RD PARTIES: ECB, EPC, PCH’s, CSD’s, SWIFT, World Bank, etc. • Best practices • Advisory • Information Sharing

CCBG: Payments & Financial Markets Sub-committee • Road Map • Legal Implications • Decisions & Principles for linkage to settlement • Standards • Governance

INTERACTION WITH STAKEHOLDERS

EAC, COMESA

COSSE

EAC COMESA Position Paper on implications and solutions for banks with multiple regional membership

COSSE MOU Cooperation in the post trade settlement space (DVP)

SADC Secretariat

SADCBA: Project Execution • Dedicated Project Team • Funding in place • Project plan Approved

ISO/SADC STAN

ISO/ SADCSTAN: Standards Adoption Setting up TC to drive standards adoption (ISOTC68) in SADC

Challenges of Regional Integration

• Lack of political will

• Fear of loss of sovereignty

• Countries at different levels of infrastructural development.

• Countries at different levels of institutional capacity.

• Larger economies marginalising smaller ones – “Big Brother syndrome” or perception thereof.

• Challenges observed in other regions e.g. Euro-Zone

Presented by T.E Mawocha to the Onstitute of Internal Auditors – 22 April 2010 – Orion Hotel – Piggs Peak

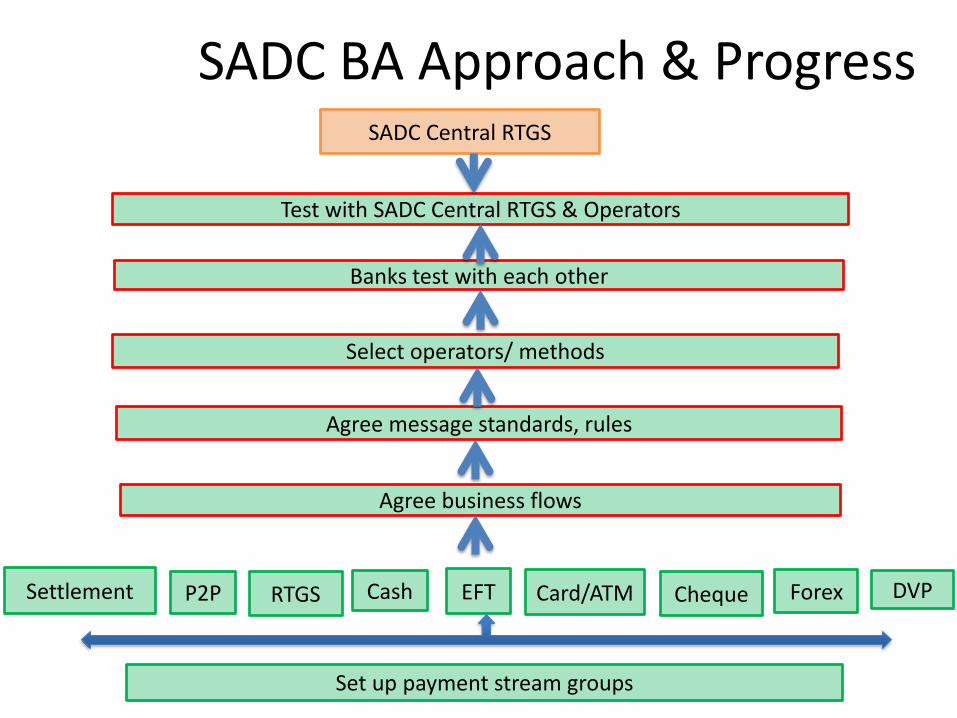

SADC Central RTGS

Banks test with each other

Select operators/ methods

Agree message standards, rules

Agree business flows

Test with SADC Central RTGS & Operators

Set up payment stream groups

SADC BA Approach & Progress

Settlement P2P RTGS Cash EFT Card/ATM Cheque Forex DVP

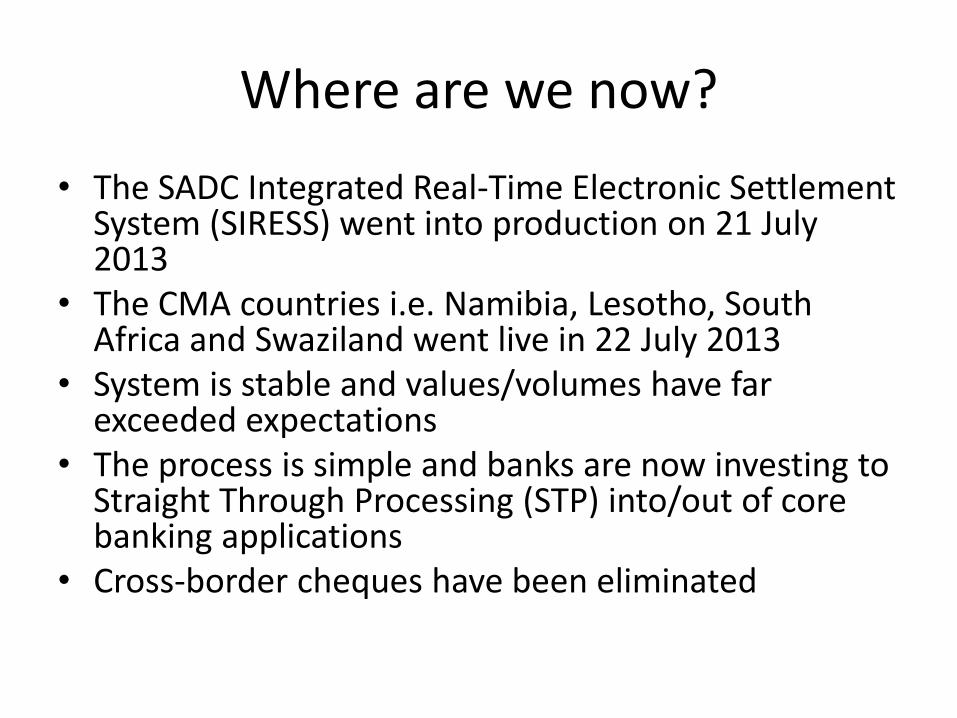

Where are we now?

• The SADC Integrated Real-Time Electronic Settlement System (SIRESS) went into production on 21 July 2013

• The CMA countries i.e. Namibia, Lesotho, South Africa and Swaziland went live in 22 July 2013

• System is stable and values/volumes have far exceeded expectations

• The process is simple and banks are now investing to Straight Through Processing (STP) into/out of core banking applications

• Cross-border cheques have been eliminated

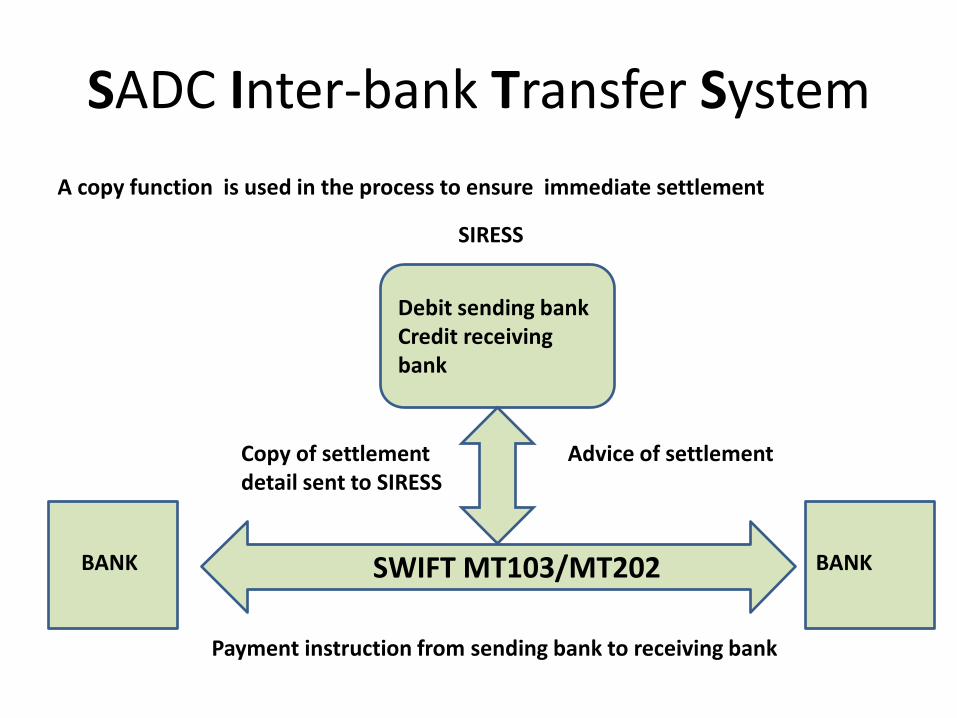

SADC Inter-bank Transfer System

A copy function is used in the process to ensure immediate settlement

SIRESS

Debit sending bank Credit receiving bank

Copy of settlement detail sent to SIRESS

Advice of settlement

Payment instruction from sending bank to receiving bank

SWIFT MT103/MT202 BANK BANK

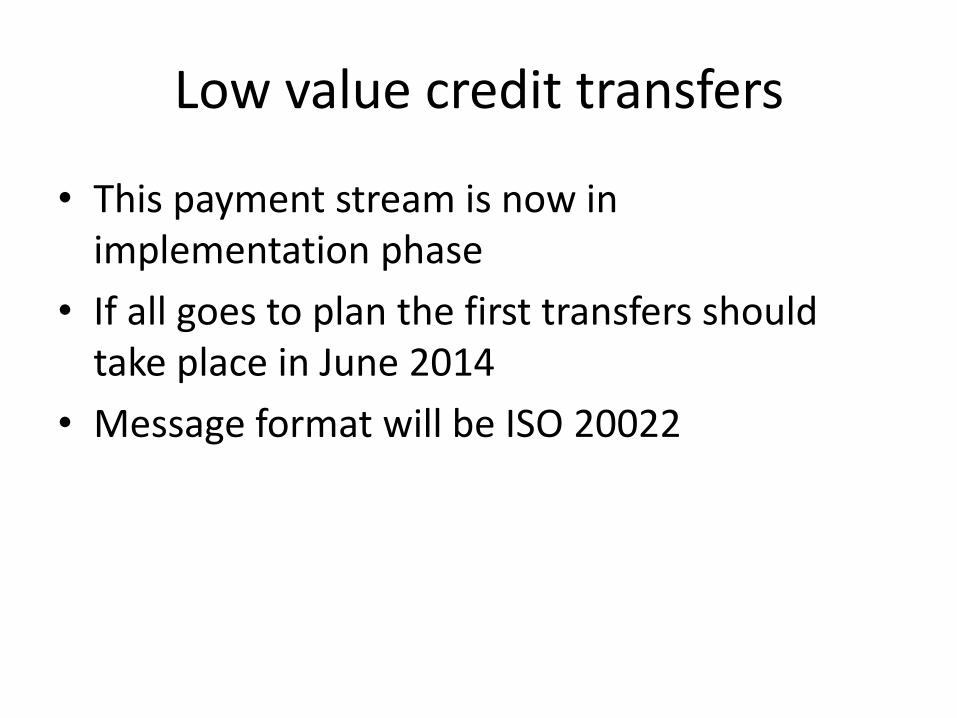

Low value credit transfers

• This payment stream is now in implementation phase

• If all goes to plan the first transfers should take place in June 2014

• Message format will be ISO 20022

SADC ACH Transfer System

Regional Automated Clearing House

SIRESS

Domestic RTGS

Send files to banks Send files to banks domestic transactions are kept separate from regional transactions

Send inter-bank settlement figures to SADC Central Bank in regional settlement currency

If regional ACH processes transactions on behalf of banks in a particular country figures are sent in currency of that country

Daily clearing process

Direct debits

• The business model, operator model, mandate model and operating rules and standards have been finalised

• Implementation is scheduled for June 2015

Card based transaction

• Here SADC is working with VISA/MasterCard etc. to introduce regional settlement of their branded card transactions

• Operators in SADC are working on linking their domestic switches to enable external usage of domestic and other cards

• Implementation will be scheduled once all relevant models and, agreements and documents have been completed - 2015

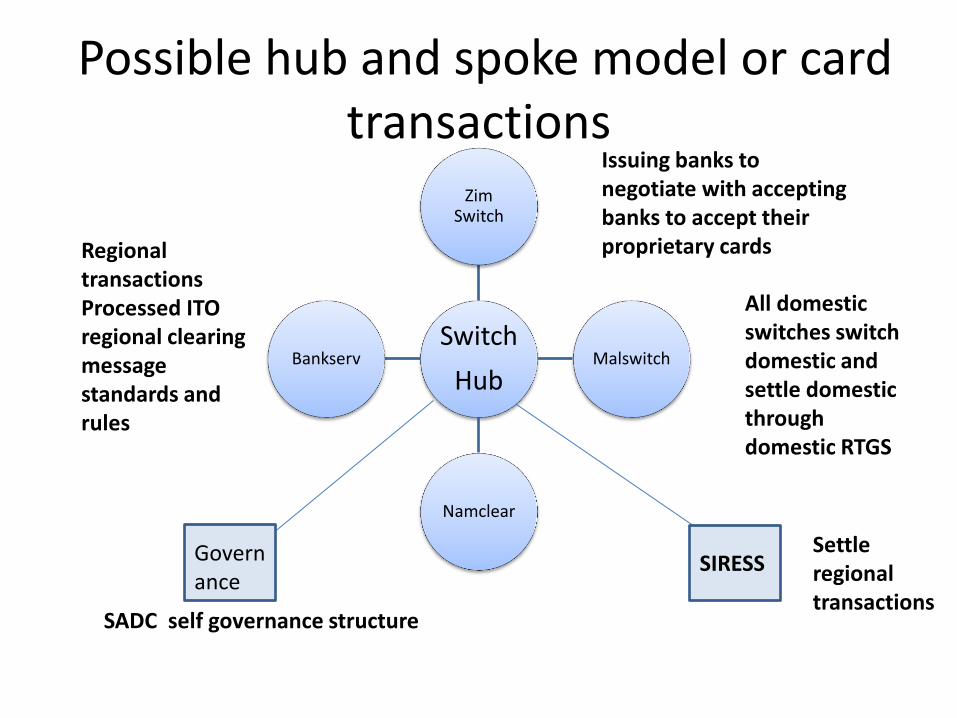

Possible hub and spoke model or card transactions

Switch

Hub

Zim Switch

Malswitch

Namclear

Bankserv

Governance

SIRESS

All domestic switches switch domestic and settle domestic through domestic RTGS

Settle regional transactions

SADC self governance structure

Regional transactions Processed ITO regional clearing message standards and rules

Issuing banks to negotiate with accepting banks to accept their proprietary cards

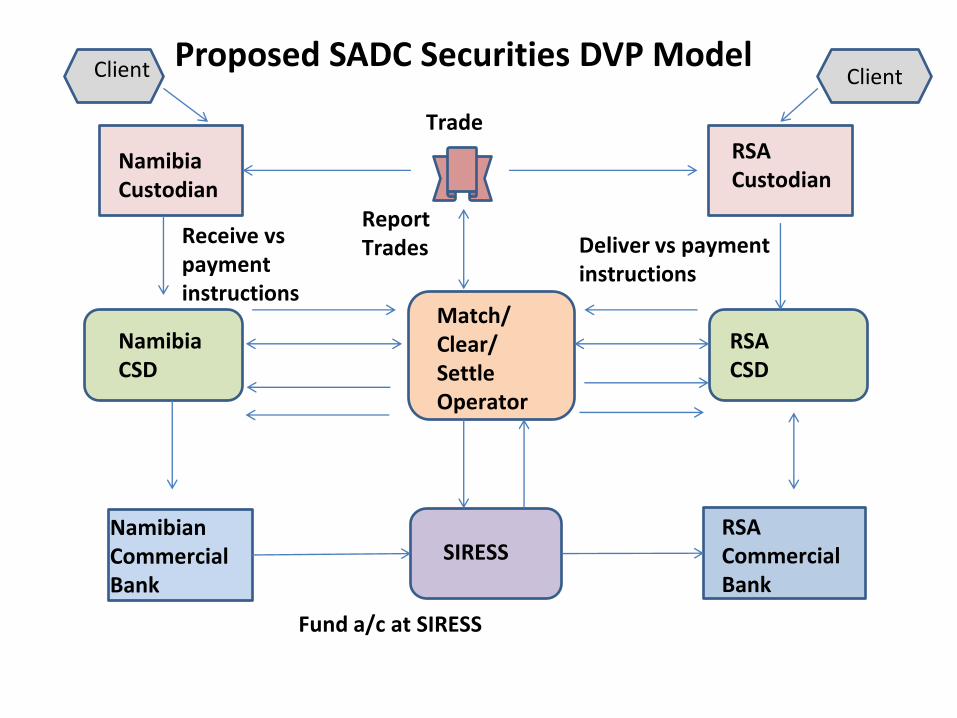

Cash leg of securities transactions

• SADC BA and a work group from the Committee of SADC Stock Exchanges (COSSE) are working on the business model and related agreements, rules etc. for the settlement of the cash leg of securities trades.

• Cash dividends will also be settled via SIRESS

• Implementation will be scheduled once all models, agreements etc. have been signed off.

Proposed SADC Securities DVP Model

Trade

Namibia Custodian

RSA Custodian

Namibia CSD

Match/ Clear/ Settle Operator

RSA CSD

Namibian Commercial Bank

SIRESS

Receive vs payment instructions

Deliver vs payment instructions

Client

Fund a/c at SIRESS

RSA Commercial Bank

Report Trades

Client

Where to next?

• Four non-CMA countries will be brought into the SIRESS Settlement System in the first quarter of next year

• The remaining non-CMA countries will be scheduled thereafter

• Other payment streams (retail) will be implemented in 2014/2015

Questions