Sa Ppt ANISH

19

SECURI TY ANAL YSI S: V ALUA TION OF PHARMACEUTICAL INDUSTRY Presented by: ANISH GUPT A ABHEEK GUPT A ANAMIKA SAHOO ANKIT A TIW ARI PRIYANKA GOEL PRIYANKA AGARWAL Presented to: Prof. D. S. Prasad

Transcript of Sa Ppt ANISH

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 1/19

SECURITY ANALYSIS: VALUATION

OF PHARMACEUTICAL INDUSTRY

Presented by: ANISH GUPTA

ABHEEK GUPTA ANAMIKA SAHOO

ANKITA TIWARI PRIYANKA GOEL

PRIYANKA AGARWAL

Presented to:Prof. D. S. Prasad

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 2/19

CONTENT

Objective

Fundamental

analysis◦ Economic

◦ Industry SWOT

Porter

◦ Valuation

Methodology

Assumptions

DCF Trading

Comparables

Conclusion

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 3/19

OBJECTIVE

To apply the concepts of fundamental analysis

For the same 6 Pharmaceutical companies have beenconsidered.

Valuation of the same has been done using DCF and Tradingcomparables.

It enabled in understanding whether they are over priced or

under priced.

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 4/19

FUNDAMENTAL ANALYSIS

Determining a value of security by focusing on underlyingfactors that affect a company’s actual business and its futureprospects.

It is performed on historical and present data, but with thegoal of making financial forecasts.

The end goal of performing fundamental analysis is toproduce a value that an investor can compare with thesecurity's current price,

With the aim of figuring out what sort of position to take with that security (underpriced = buy, overpriced = sell orshort).

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 5/19

ECONOMIC ANALYSIS

It is the analysis of macro economic environment in order tounderstand the behavior of the stock prices.

Inflation indicators are pointing down.

Industrial production growth as measured by the IIP or Index of Industrial Production came in at 3.3% for the month of July 2011against a growth rate of 8.8% seen in June 2011.

Tight banking system liquidity restricts banks from growing their

loan books leading to lower credit off take.

During the last few years the changed growth trajectory of theIndian economy has also fuelled opportunities in healthcare andgrown the pharmaceuticals sector in particular.

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 6/19

INDUSTRY ANALYSIS

The Indian Pharmaceutical Industry ranks very high in the third world, in terms of technology, quality and range of medicinesmanufactured

India's pharmaceutical industry is now the third largest in the worldin terms of volume.

Indian Pharma Industry is estimated to be worth $ 4.5 billion,growing at about 8 to 9 percent annually.

The Indian pharmaceuticals market is expected to reach US$ 55billion in 2020 from US$ 12.6 billion in 2009

it was also mentioned that in an aggressive growth scenario, thepharma market has the further potential to reach US$ 70 billion by 2020.

Overview

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 7/19

INDUSTRY ANALYSIS

Strengths:Largely untapped marketLowest cost producers of drugs in the world.Possesses excellent chemistry and process reengineeringskills

Weakness: Marred by the price regulationLack of product patentLow penetrationLow barriers to entry

Opportunities Product patent based regime is likely to transform industryThe expected growth in per capita income are key growthdrivers

Threats: concerns over the patent regime regarding its current

SWOT

PORTER’S FIVE FORCESPORTER’S FIVE FORCESPORTER’S FIVE FORCESPORTER’S FIVE FORCESPORTER’S FIVE FORCESPORTER’S FIVE FORCES

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 8/19

INDUSTRY ANALYSIS

PORTER’S FIVE FORCES

PORTER ’S FIVE FORCES PORTER ’S FIVE FORCES PORTER ’S FIVE FORCES PORTER ’S FIVE FORCES PORTER ’S FIVE FORCES PORTER ’S FIVE FORCES

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 9/19

INDUSTRY ANALYSIS

Industry competition

The entry barriers to pharma industry are very low.The fixed cost requirement is low but working capital is high.The product differentiation is one key factor

Bargaining power of buyers End user of the product is different from the influencer

Low bargaining power

Bargaining power of suppliers Low bargaining power

Barriers to entry The most easily accessible industriesQuality regulations by the government may put somehindranceNew patent regime will raise the barriers to entry

Threat of substitutes Demand for pharma products continues

PORTER’S FIVE FORCES

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 10/19

VALUATION

Methodology

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 11/19

VALUATIONAssumptions

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 12/19

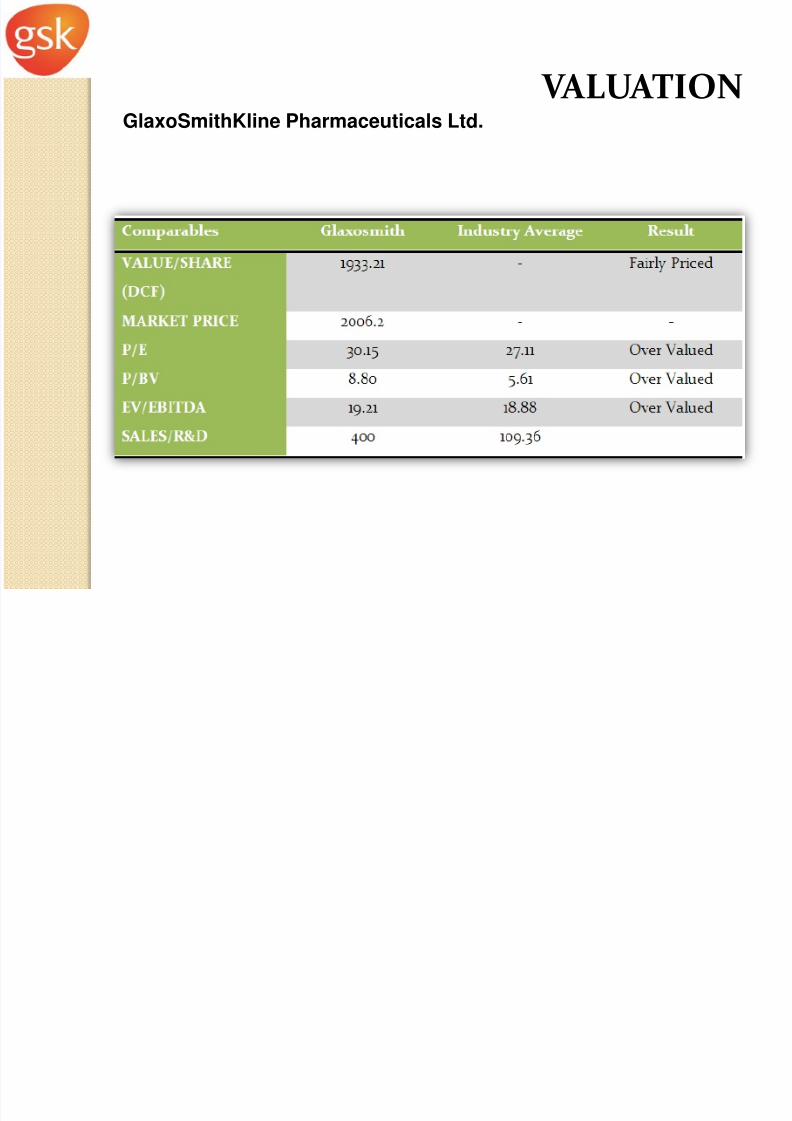

VALUATIONGlaxoSmithKline Pharmaceuticals Ltd.

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 13/19

VALUATIONDr. Reddy's Laboratories Ltd

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 14/19

VALUATIONRanbaxy

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 15/19

VALUATIONAventis

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 16/19

VALUATIONGlen Mark Pharmaceuticals

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 17/19

VALUATIONCipla Limited

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 18/19

CONCLUSIONWe have shown how to evaluate stocks from fundamental aspect sothat an investor can determine whether to buy the stock or not.

We have used price earnings (P/E), P/BV , EV/EBITDA &Sales/R&D multiple and DCF technique as the valuation metric.

Since DCF valuation is based upon an asset’s fundamentals, it is

less exposed to market moods and perceptions.

Investors should go for Dr. Reddy & Ranbaxy as they are goodinvestment.

Relative valuation is much more likely to reflect marketfundamentals.

It is understood that Ranbaxy, Aventis & Cipla are undervalued andtheir market value is more likely to appreciate in future.

For pharmaceutical companies most important relative valuationmetric is R&D/Sales as companies

We can say that Dr. Reddy’s, Ranbaxy, Glen mark & Cipla have

8/3/2019 Sa Ppt ANISH

http://slidepdf.com/reader/full/sa-ppt-anish 19/19