Sa by Aseem Trivedi

56

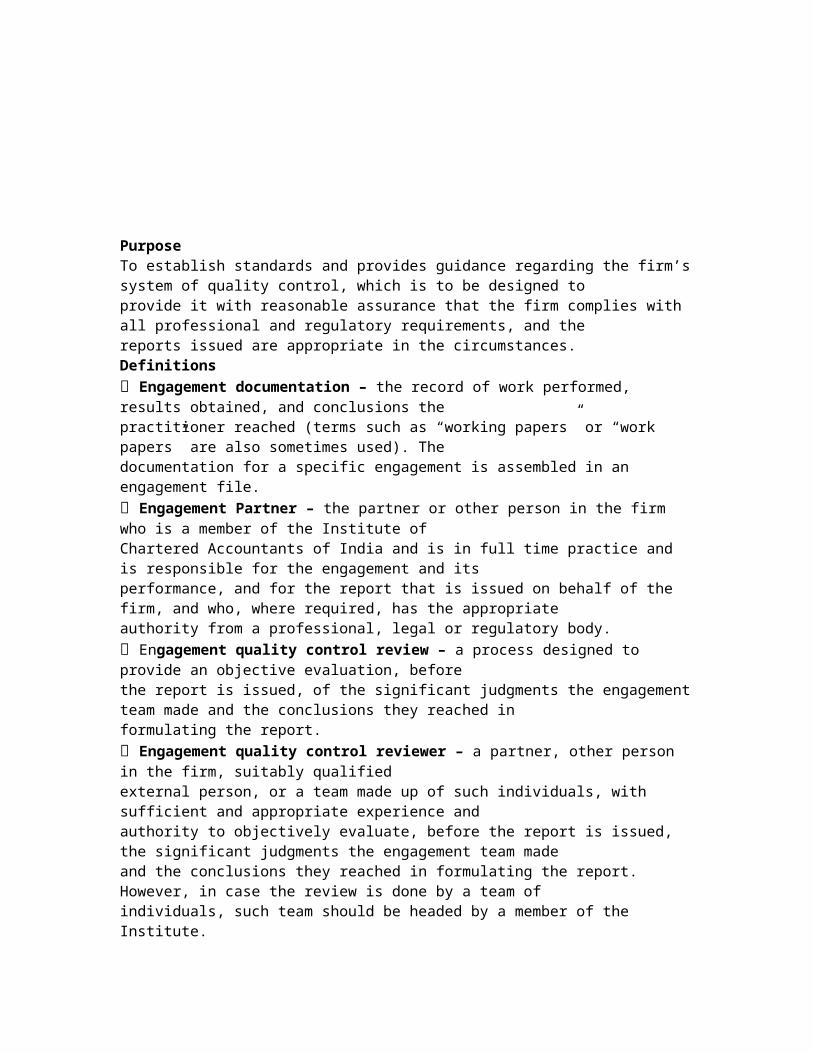

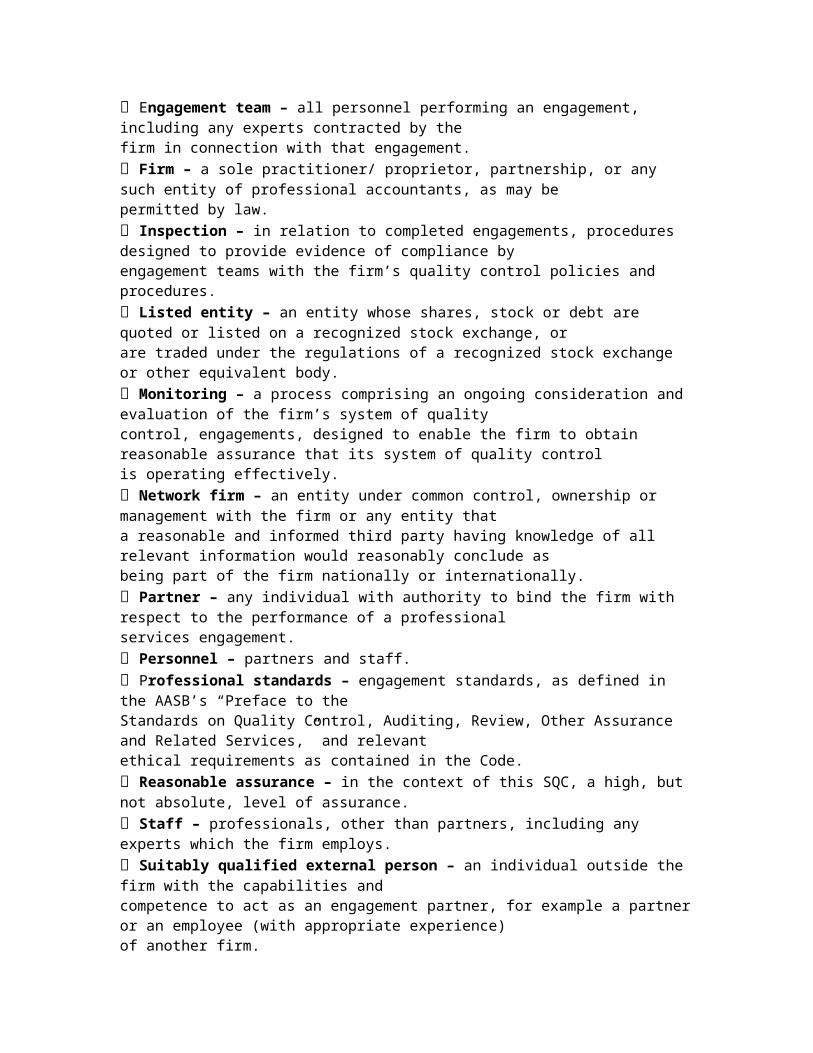

SQC – 1sqc SQC - 1 TY CONTROL FOR FIRMS THAT PERFORM AUDITS AND REVIEWS OF Purpose To establish standards and provides guidance regarding the firm’s system of quality control, which is to be designed to provide it with reasonable assurance that the firm complies with all professional and regulatory requirements, and the reports issued are appropriate in the circumstances. Definitions Engagement documentation – the record of work performed, results obtained, and conclusions the practitioner reached (terms such as “working papers” or “work papers” are also sometimes used). The documentation for a specific engagement is assembled in an engagement file. Engagement Partner – the partner or other person in the firm who is a member of the Institute of Chartered Accountants of India and is in full time practice and is responsible for the engagement and its performance, and for the report that is issued on behalf of the firm, and who, where required, has the appropriate authority from a professional, legal or regulatory body. Engagement quality control review – a process designed to provide an objective evaluation, before the report is issued, of the significant judgments the engagement team made and the conclusions they reached in formulating the report. Engagement quality control reviewer – a partner, other person in the firm, suitably qualified external person, or a team made up of such individuals, with sufficient and appropriate experience and authority to objectively evaluate, before the report is issued, the significant judgments the engagement team made and the conclusions they reached in formulating the report. However, in case the review is done by a team of individuals, such team should be headed by a member of the Institute.

-

Upload

monil-shah -

Category

Documents

-

view

440 -

download

4

Transcript of Sa by Aseem Trivedi

SQC ndash 1sqcSQC - 1

TY CONTROL FOR FIRMS THAT PERFORM AUDITS AND REVIEWS OFPurposeTo establish standards and provides guidance regarding the firmrsquos system of quality control which is to be designed toprovide it with reasonable assurance that the firm complies with all professional and regulatory requirements and thereports issued are appropriate in the circumstancesDefinitions Engagement documentation ndash the record of work performed results obtained and conclusions thepractitioner reached (terms such as ldquoworking papersrdquo or ldquowork papersrdquo are also sometimes used) Thedocumentation for a specific engagement is assembled in an engagement file Engagement Partner ndash the partner or other person in the firm who is a member of the Institute ofChartered Accountants of India and is in full time practice and is responsible for the engagement and itsperformance and for the report that is issued on behalf of the firm and who where required has the appropriateauthority from a professional legal or regulatory body Engagement quality control review ndash a process designed to provide an objective evaluation beforethe report is issued of the significant judgments the engagement team made and the conclusions they reached informulating the report Engagement quality control reviewer ndash a partner other person in the firm suitably qualifiedexternal person or a team made up of such individuals with sufficient and appropriate experience andauthority to objectively evaluate before the report is issued the significant judgments the engagement team madeand the conclusions they reached in formulating the report However in case the review is done by a team ofindividuals such team should be headed by a member of the Institute Engagement team ndash all personnel performing an engagement including any experts contracted by thefirm in connection with that engagement Firm ndash a sole practitioner proprietor partnership or any such entity of professional accountants as may bepermitted by law Inspection ndash in relation to completed engagements procedures designed to provide evidence of compliance byengagement teams with the firmrsquos quality control policies and procedures

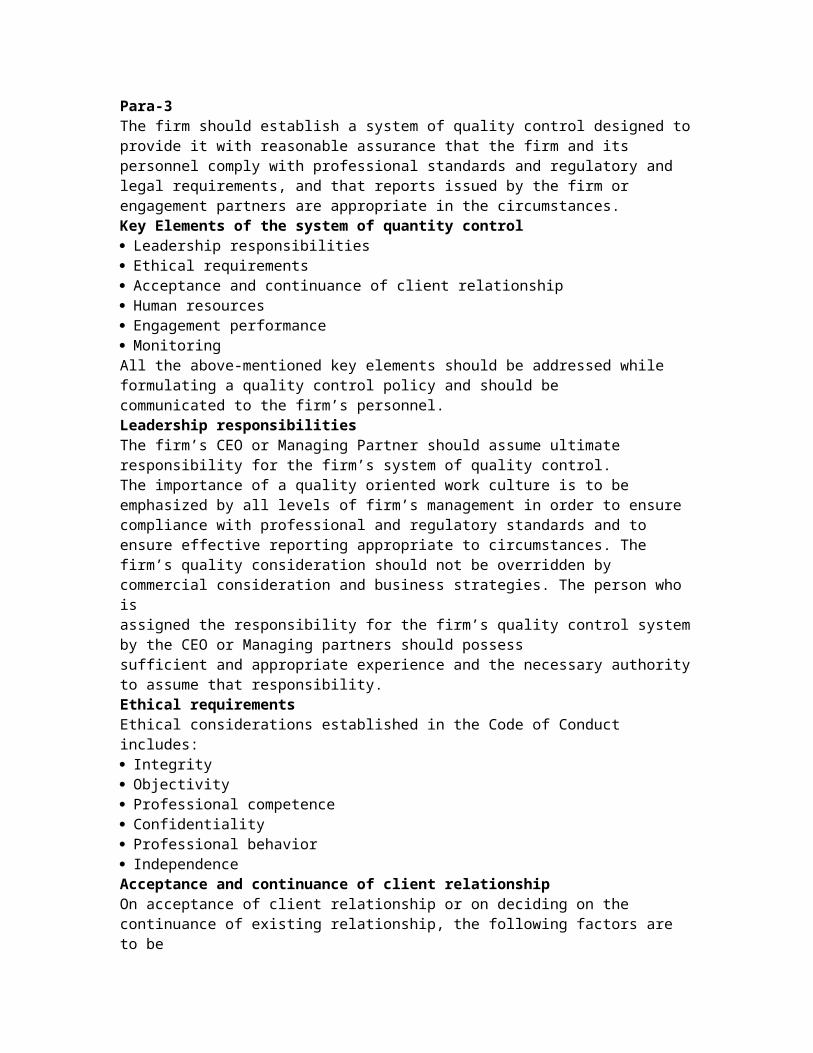

Listed entity ndash an entity whose shares stock or debt are quoted or listed on a recognized stock exchange orare traded under the regulations of a recognized stock exchange or other equivalent body Monitoring ndash a process comprising an ongoing consideration and evaluation of the firmrsquos system of qualitycontrol engagements designed to enable the firm to obtain reasonable assurance that its system of quality controlis operating effectively Network firm ndash an entity under common control ownership or management with the firm or any entity thata reasonable and informed third party having knowledge of all relevant information would reasonably conclude asbeing part of the firm nationally or internationally Partner ndash any individual with authority to bind the firm with respect to the performance of a professionalservices engagement Personnel ndash partners and staff Professional standards ndash engagement standards as defined in the AASBrsquos ldquoPreface to theStandards on Quality Control Auditing Review Other Assurance and Related Servicesrdquo and relevantethical requirements as contained in the Code Reasonable assurance ndash in the context of this SQC a high but not absolute level of assurance Staff ndash professionals other than partners including any experts which the firm employs Suitably qualified external person ndash an individual outside the firm with the capabilities andcompetence to act as an engagement partner for example a partner or an employee (with appropriate experience)of another firmPara-3The firm should establish a system of quality control designed to provide it with reasonable assurance that the firm and itspersonnel comply with professional standards and regulatory and legal requirements and that reports issued by the firm orengagement partners are appropriate in the circumstancesKey Elements of the system of quantity controlLeadership responsibilitiesEthical requirementsAcceptance and continuance of client relationshipHuman resourcesEngagement performanceMonitoringAll the above-mentioned key elements should be addressed while formulating a quality control policy and should becommunicated to the firmrsquos personnelLeadership responsibilities

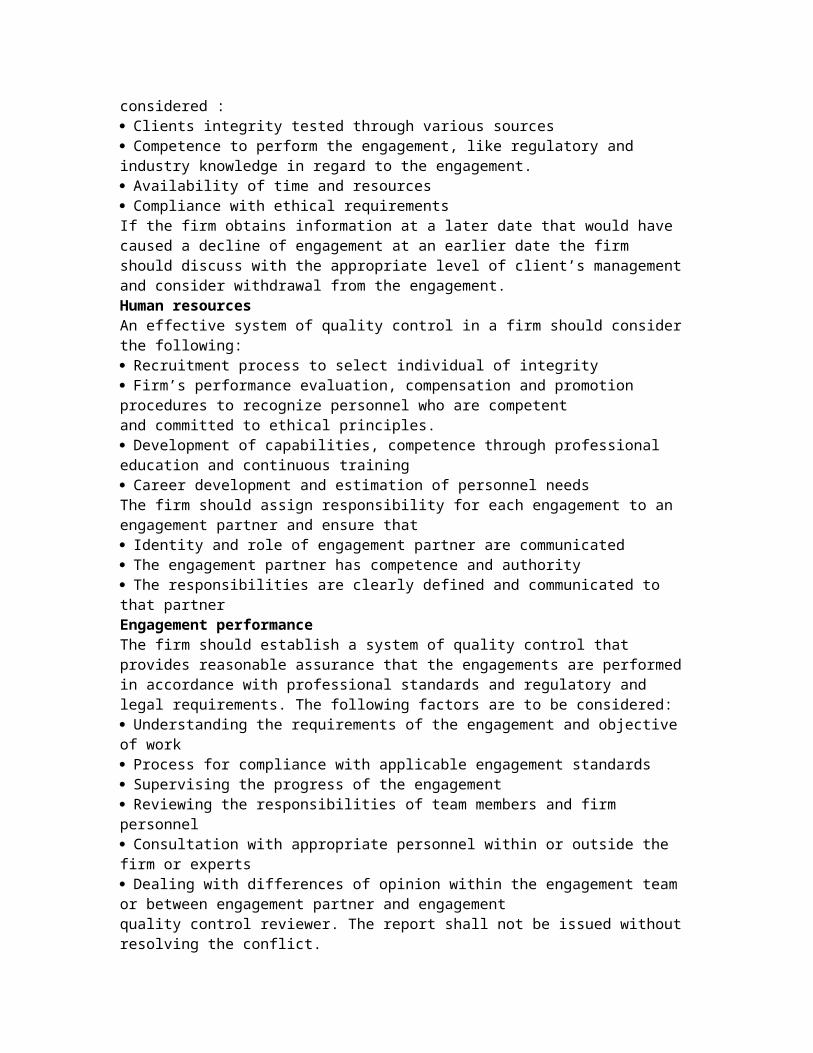

The firmrsquos CEO or Managing Partner should assume ultimate responsibility for the firmrsquos system of quality controlThe importance of a quality oriented work culture is to be emphasized by all levels of firmrsquos management in order to ensurecompliance with professional and regulatory standards and to ensure effective reporting appropriate to circumstances Thefirmrsquos quality consideration should not be overridden by commercial consideration and business strategies The person who isassigned the responsibility for the firmrsquos quality control system by the CEO or Managing partners should possesssufficient and appropriate experience and the necessary authority to assume that responsibilityEthical requirementsEthical considerations established in the Code of Conduct includesIntegrityObjectivityProfessional competenceConfidentialityProfessional behaviorIndependenceAcceptance and continuance of client relationshipOn acceptance of client relationship or on deciding on the continuance of existing relationship the following factors are to beconsidered Clients integrity tested through various sourcesCompetence to perform the engagement like regulatory and industry knowledge in regard to the engagementAvailability of time and resourcesCompliance with ethical requirementsIf the firm obtains information at a later date that would have caused a decline of engagement at an earlier date the firmshould discuss with the appropriate level of clientrsquos management and consider withdrawal from the engagementHuman resourcesAn effective system of quality control in a firm should consider the followingRecruitment process to select individual of integrityFirmrsquos performance evaluation compensation and promotion procedures to recognize personnel who are competentand committed to ethical principlesDevelopment of capabilities competence through professional education and continuous trainingCareer development and estimation of personnel needsThe firm should assign responsibility for each engagement to an engagement partner and ensure thatIdentity and role of engagement partner are communicatedThe engagement partner has competence and authorityThe responsibilities are clearly defined and communicated to that partnerEngagement performanceThe firm should establish a system of quality control that provides reasonable assurance that the engagements are performed

in accordance with professional standards and regulatory and legal requirements The following factors are to be consideredUnderstanding the requirements of the engagement and objective of workProcess for compliance with applicable engagement standardsSupervising the progress of the engagementReviewing the responsibilities of team members and firm personnelConsultation with appropriate personnel within or outside the firm or expertsDealing with differences of opinion within the engagement team or between engagement partner and engagementquality control reviewer The report shall not be issued without resolving the conflictMonitoringThe system of quality control shall establish policies and procedures to monitor the effectiveness of engagement performanceand ongoing evaluation of the quality control system The ongoing evaluation shall considerDesign effective implementation and appropriate application of quality control systemAnalysis of new developments in professional standards and legal standardsCorrective actions and improvements to be made in the system and communication of weaknesses identifiedInspection of completed engagements that shall include at least one engagement for each partner over theinspection cycle of not more than 3 yearsThe deficiencies identified should be communicated to the engagement partner along with the remedial action that wouldrequire changes in quality control policy The complaints and allegations against the firm as regards to the non-compliance of professional standards or allegations of non-compliance of firmrsquos system of quality control shall be dealt with either as perlegal regulations or by taking appropriate remedial actionDocumentationThe firm should establish policies and procedures requiring appropriate documentation to provide evidence of the operationof each element of its system of quality control The firm may use electronic databases or use of simple checklists manualnotes and forms depending on The size of the firm and the number of officesThe degree of authority both personnel and offices haveThe nature and complexity of the firmrsquos practice and organizationThe firm shall retain the documentation as per the firmrsquos policy or in compliance with the requirements of laws orregulations

SA -2OO(Revised)

Overall Objectives of the Independent Auditor and the Conduct of anAudit in Accordance with Standards on AuditingQ1 What are Overall Objectives of an Independent AuditorAccording to SA 200 Revised The overall objectives of the auditor are(a) To obtain reasonable assurance about whether the financial statements as a whole are free from materialmisstatement resulting from either due to fraud or error by this means enabling the auditor to expressan opinion on whether the financial statements are prepared in all material respects in accordance withan applicable financial reporting framework and(b) To report on the financial statements and communicate as required by the SAs in accordance with theauditorrsquos findingsFor example- if the auditor is appointed under section 224 of the Companies Act 1956 his objective will be toobtain reasonable assurance that whether Financial Statement of the company are giving true and fair view ornot Financial statement are said to be giving true and fair view only when they are complying with requirementsof companies Act 1956 like schedule VI Companies Accounting Standard Rules 2002 Schedule XIVetc Further Auditor has to report to members of the company in a manner specified in Section 227Q2 What will be consequences if auditor fails to achieve his objectiveAccording to SA 200 if auditor is unable to obtain sufficient appropriate audit evidences to support hisconclusions or we can say he is unable to obtain reasonable assurance he should either give a disclaimer of opinionor should withdraw from engagement if permitted by lawFor example - If auditee has provided auditor Photocopies of books of accounts and evidences for audit asoriginal books of accounts and evidences are ceased by Income tax department in such case auditor should eithergive a disclaimer of opinion that he is unable to form and express opinion on financial statement or he may decideto withdraw from engagement if permissibleQ3 Briefly explain the requirements of SA-200 There are 5 requirements an auditor has to fulfill according to SA-200- Ethical Requirements relating to an audit of financial statements- Requirement to have an attitude of Professional Skepticism- Requirement to exercise Professional Judgement

- Requirement to obtain Sufficient and Appropriate Audit Evidences- Requirement to follow all Standards of AuditingQ4 What do you mean by Ethical RequirementsEvery member of the ICAI is subject to ethical behaviour as described in CODE of ETHICS issued byICAI This Code of ethics requires that auditor shall subject to following ethical requirements whiledischarging his duties as an independent Auditor(a) Integrity means Honest behaviour Loyal attitude towards users of financial statements(b) Objectivity - This could be achieved only by having independence of mind and independence is appearanceof an auditor(c) Professional competence and due care - This could be achieved by acquainting himself with the latestdevelopments in the field of accounting and auditing (d) Confidentiality- Should keep all information received from client and should not disclose the same unless itis not legal or professional requirement to do so(e) Professional behaviour There must be professional relation between auditor and auditee There must not beany other interest to override the objectivityFurther SQC-1 and SA220 have suggested ways and means to achieve such independence and objectivity ofAuditorQ5 What do you mean by attitude of Professional Skepticism Professional Skepticism is nothing but an attitude of the auditor which requires auditorrsquos alertness towardsinformation provided to him from the auditee It should not be understood as doubt but should be taken as vigilantattitude For example auditor should always be alert towardsAudit evidence provided by client that contradicts other audit evidence obtained by diams the auditor himself diams Information that brings into question the reliability of documents and responses to inquiries to be used as auditevidencediams Conditions that may indicate possible frauddiams Circumstances that suggest the need for audit procedures in addition to those required by the SAsBy adopting such an attitude auditor may minimise the risk of overlooking unusual diams circumstancesdiams Over generalising when drawing conclusions from audit observationsdiams Using inappropriate assumptions in determining the nature timing and extent of the audit procedures and

evaluating the results thereofDoes it mean that auditor should place doubt over each record information or document provided by theclient tohim Answer to this question is addressed in SA200 revised according to it ldquoauditor may accept records anddocuments as genuine unless the auditor has reason to believe the contrary Nevertheless the auditor isrequired to consider the reliability of information to be used as audit evidenceIn cases of doubt about the reliability of information or indications of possible fraud (for example if conditionsidentified during the audit cause the auditor to believe that a document may not be authentic or that terms in adocument may have beenfalsified) the SAs require that the auditor investigate further and determine what modifications or additions toaudit procedures are necessary to resolve the matter Even if a belief that management and those charged withgovernance are honest and have integrity does not relieve the auditor of the need to maintain professionalskepticism or allow the auditor to be satisfied with less-than-persuasive audit evidence when obtaining reasonableassuranceFor Example - As Mr A is auditor of Y ltd from last 3 years and every year after dueexamination he found financial statement true and fair and found management ashonest and ethical does not mean that he should have a blind faith in audit ofcurrent year over all the information provided by themQ6 What is requirement of professional Judgement as per SA ndash 200 (Revised)Professional judgement means a judgment taken by the auditor out of his professional experience in a auditsituation According to SA 200 revised Professional judgment is essential to the proper conduct of an auditThis is because interpretation of relevantethical requirements and the SAs and the informed decisions required throughout the audit cannot be madewithout the application of relevant knowledge and experience to the facts and circumstances Professionaljudgment is necessary in particular regarding decisions aboutdiams Materiality and audit riskdiams The nature timing and extent of audit procedures diams Evaluating whether sufficient appropriate audit evidence has been obtained

diams The evaluation of managementrsquos judgments in applying the entityrsquos applicable financial reporting frameworkdiams The drawing of conclusions based on the audit evidence obtainedIt is required that auditors professional Judgement should be reasonable and rational Consultation on difficultor contentious matters during the course of the audit both within the engagement team and between the engagementteam and others at the appropriate level within or outside the firm assist the auditor in making informed andreasonable judgments Further the auditor is required to prepare audit documentation relating to such reasonableprofessional judgementsQ7 Explain the requirements of sufficient and appropriate Audit Evidences According to SA 200 revised ldquo Audit evidence is necessary to support the auditorrsquos opinion and reportrdquo It iscumulative in nature and is primarily obtained from audit procedures performed during the course of the audit It may however also include information obtained from other sources like experience from previous auditinformation provided and prepared by employees management and those charged with governance of the auditeeThe sufficiency and appropriateness of audit evidence are interrelated Sufficiency is the measure of thequantity of audit evidence and appropriateness means quality of Audit evidence (posers are given in previouschapter) Whether sufficient appropriate audit evidence has been obtained to reduce audit risk to an acceptablylow level and thereby enable the auditor to draw reasonable conclusions on which to base the auditorrsquos opinion is amatter of Professional judgmentQ8 Does the auditor expected to reduce audit risk to zero and can obtain absoluteassurance that the financial statements are free from material misstatement due to fraud or errorThe answer is in negative According to SA 200 Revised The auditor is not expected to and cannot reduceaudit risk to zero and cannot therefore obtain absoluteassurance that the financial statements are free from material misstatement due to fraud or error This is becausethere are inherent limitations of an audit Inherent limitations means limitations which can not be overcome andwhich are with the subject since the inception or evolution of the subject Following are contributors to inherentlimitations to audit

1 Most of the audit evidence on which the auditor draws conclusions and bases the auditorrsquos opinion beingpersuasive rather than conclusive2 The nature of financial reporting - If in financial statement some items are valued only on the basis ofmanagements estimates which are highly subjective in those cases audit procedures are insufficient tofind the reasonableness of such judgements3 The nature of audit procedures- For example Fraud may involve sophisticated and carefully organisedschemes designed to conceal it Therefore audit procedures used to gather audit evidence may beineffective for detecting an intentional misstatement that involves for example collusion to falsifydocumentation which may cause the auditor to believe that audit evidence is valid when it is not Theauditor is neither trained as nor expected to be an expert in the authentication of documents Furtherauditor has no legal power to search forcefully which may be necessary for such an investigation4 The need for the audit to be conducted within a reasonable period of time and at a reasonable costBecause of the inherent limitations of an audit there is an unavoidable risk that some material misstatements of thefinancial statements may not be detected even though the audit is properly planned and performed in accordance with SAsAccordingly the subsequent discovery of a material misstatement of the financial statements resulting from fraud or errordoes not by itself indicate a failure to conduct an audit in accordance with SAsQ9 What are the requirements of SA 200 revised to Conduct of an Audit inAccordance with SAsAuditor is required to follow SAs during his audit He is required to determine the nature timing and extent of his auditprocedures according to requirements of SAsAccording to SA 200 Revised The requirements of the SAs are designed to enable the auditor to achieve the objectivesspecified in the SAs and thereby the overall objectives of the auditor SA 230 (Revised) establishes documentation requirements in those exceptional circumstances where the auditor departs from a relevant requirement If there is anyconflict between the law with which the auditee is subject to and SA the law would prevailsQ10 What is Scope of an audit of Financial StatementsScope of audit means an area of work for the auditor Scope of audit is primarily determined by following factors- Terms of engagement of the auditor

- Requirements of legislation- Standards on Auditing and other guidance by ICAIIt should be noted that terms of engagement can not have an verriding effect over the scope decided by the legislation orSAsFollowing is not within the scope of auditor it is within the scope of Management and those charged with governance-1 Maintenance of books of accounts and records2 Formulation and Implementation of Internal Control system3 Selection and application of accounting policies4 Estimation of accounting estimates5 Preparation and presentation of financial statementIt is important to note that Auditors opinion is not an assurance about the future viability of the entity and neither it is anassurance about the future efficiency and effectiveness of the management It is just an opinion about financial position upto the date and period covered under auditER ASSURANCE ANDRELATED SERVICE ENGAGEMENTS

SA 210 (R) - AGREEING THE TERMS OF AUDIT ENGAGEMENTS

Q How an Auditor will decide whether to accept the engagement as an auditor or not According to SA 210 Revised ldquo The objective of the auditor is to accept or continue an audit engagement only when the basis upon which it is to be performed has been agreed through (a) Establishing whether the preconditions for an audit are present and (b) Confirming that there is a common understanding between the auditor and management and where appropriate those charged with governance of the terms of the audit engagement Q What do you mean by preconditions to an audit and how auditor establishes it According to SA 210 Revised Preconditions for an audit means ldquo The use by management of an acceptable financial reporting framework in the reparation of the financial statements and the agreement of management and where appropriate those charged with governance to the premise on which an audit is conducted In order to establish whether the preconditions for an audit are present the auditor shall (a) Determine whether the financial reporting framework to be applied in the preparation of the financial statements is acceptable and (b) Obtain the agreement of management that it acknowledges and understands its responsibility (i) For the preparation of the financial statements in accordance with the applicable financial reporting framework including where relevant their fair presentation (ii) For such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement whether due to fraud or error and (iii) To provide the auditor with a Access to all information of which management is aware that is relevant to the preparation of the financial statements such as records documentation and other matters

b Additional information that the auditor may request from management for the purpose of the audit and c Unrestricted access to persons within the entity from whom the auditor determines it necessary to obtain audit evidence QWhat should be auditors course of action if limitation on Scope have been imposed Prior to Audit Engagement Acceptance If management or those charged with governance impose a limitation on the scope of the auditorrsquos work in the terms of a proposed audit engagement such that the auditor believes the limitation will result in the auditor disclaiming an opinion on the financial statements the auditor shall not accept such a limited engagement as an audit engagement unless required by law or regulation to do so Q What is Audit Engagement Letter and what it contains According to SA 210 Revised The auditor shall agree the terms of the audit engagement with management or those charged with governance as appropriate The agreed terms of the audit engagement shall be recorded in an audit engagement letter or other suitable form of written agreement and shall include (a) The objective and scope of the audit of the financial statements (b) The responsibilities of the auditor (c) The responsibilities of management (d) Identification of the applicable financial reporting framework for the preparation of the financial statements and (e) Reference to the expected form and content of any reports to be issued by the auditor and a statement that there may be circumstances in which a report may differ from its expected form and content According to SA240 ldquoIt is in the interests of both the entity and the auditor that the auditor sends an audit engagement letter before the commencement of the audit to help avoid misunderstandings with respect to the auditrdquo Usually once the terms are determined auditor shall not agree to a change in the terms of the audit engagement where there is no reasonable justification for doing so or that conveys a lower level of assuranceSA 230 (R) ndash Audit Documentation

Q1What is Audit Documentation According to SA-230 Audit documentation refers to the record of

bull audit procedures performed bull relevant audit evidence obtained and bull conclusions the auditor reached

terms such as ldquoworking papersrdquo or ldquowork papersrdquo are also sometimes used for the same When ever auditor is in process of obtaining sufficient and appropriate audit evidences he prepares some working papers like audit plan program significant observations query on the other hand he obtains schedules lists confirmations from the management Process of collecting and preparing working paper is known as Documentation Q2Why Documentation According to SA-230 Audit documentation serves a number of additional purposes including the following _Assisting the engagement team to plan and perform the audit- If plan is well documented than the chances of leaving an important area under auditing will be less on the contrary with the help of documented plan one could perform the task in a sequential and coordinated manner _Assisting members of the engagement team responsible for supervision to direct and supervise the audit work - As per SA-200 the work of the assistants and employees should be supervised and reviewed time to time by the auditor If the observations findings objections are documented by the staff the auditor can supervise the process of audit more conveniently and on the basis of it he can issue further direction to staff on audit _Enabling the engagement team to be accountable for its work - Documents prepared and signed and filed by engagement team make the accountable for how they executed the planned procedure _Retaining a record of matters of continuing significance to future audits - For Example documentation relating to estimates of future earnings relating to an asset for its revaluation or impairment are relevant for future period audit _Enabling the conduct of quality control reviews and inspections in accordance with SQC-1 _Enabling the conduct of external inspections in accordance with applicable legal regulatory or other requirements- If auditor has sufficient documentation regarding any of his observation resulting in a conclusion these documents are known as audit evidence Hence most of the audit evidences are in form of documentary

evidences In external inspections if auditor required to explain evidences in support of his conclusion documentation will a great help for him Q3When Documentation According to SA 230 ldquoThe auditor shall prepare audit documentation on a timely basisrdquo Now the question arises whether preparing documentation during the audit is more effective or we can document the matters once the audit is over According to SA230 ndashldquoDocumentation prepared after the audit work has been performed is likely to be less accurate than documentation prepared at the time such work is performed Hence we can conclude that working papers shall be prepared during the audit process itself Q4What matters are required to be documented According to SA 230 The auditor shall prepare audit documentation that is sufficient to enable an experienced auditor having no previous connection with the audit to understand (a) The nature timing and extent of the audit procedures performed to comply with the SAs and applicable legal and regulatory requirements In documenting the nature timing and extent of audit procedures performed the auditor shall record

bull The identifying characteristics of the specific items or matters tested- For example Cash Sales to what extent checked what was the sample size what supportive documents were verified etc bull Who performed the audit work and the date such work was completed and bull Who reviewed the audit work performed and the date and extent of such review

(b) The results of the audit procedures performed and the audit evidence obtained and (c) Significant matters arising during the audit the conclusions reached thereon and significant professional judgments made in reaching those conclusions Some other important matters an auditor should document are as follows

(a) Discussions of significant matters with management those charged with governance and others including the nature of the significant matters discussed and when and with whom the discussions took place

(b) If the auditor identified information that is inconsistent with the auditorrsquos final conclusion regarding a significant matter the auditor shall document how the auditor addressed the inconsistency

(c) If in exceptional circumstances the auditor judges it necessary to depart from a relevant requirement in a SA the auditor shall document how the alternative audit procedures performed achieve the aim of that requirement and the reasons for the departure

(d) If in exceptional circumstances the auditor performs new or additional audit procedures or draws new conclusions after the date of the auditorrsquos report the auditor shall document the same

Q5Shall auditor assemble the Working paper file during the Audit or he may assemble later on According to SA-230 auditor shall assemble the audit documentation in an audit file and complete the administrative process of assembling the final audit file on a timely basis ( SQC-1 defined within 60 days )after the date of the auditorrsquos report Q6Can Auditor modify delete or discard such assembled documents Further it is provided that the auditor shall not delete or discard audit documentation so assembled before the end of its retention period If subsequently auditor want to modify the assembled documentation he can do so but in doing so regardless of the nature of the modifications or additions document (a) The specific reasons for making them and (b) When and by whom they were made and reviewed The retention period for audit engagements ordinarily is not shorter than ten years from the date of the auditorrsquos report ( group auditorrsquos report if any ) Q7 Whose property these working papers are Does client have any right over them

Standard on Quality Control (SQC) 1 ldquoQuality Control for Firms that Perform Audits and Reviews of Historical Financial Information and Other Assurance and Related Services Engagementsrdquo issued by the Institute provides that ldquounless otherwise specified by law or regulation audit documentation is the property of the auditor He may at his discretion make portions of or extracts from audit documentation available to clients provided such disclosure does not undermine the validity of the work performed or in the case of assurance engagements the independence of the auditor or of his

After the WorldCom and Enron debacle of United state in 2002 and in 2008 Satyam fiasco in India the auditing profession all over the world is in the eyes of users of financial statements and regulatory authorities All auditing bodies are redefining and re interpreting the auditors duties and responsibilities

SA240(R) THE AUDITORrsquoS RESPONSIBILITIES RELATING TO FRAUD IN AN AUDIT OF FINANCIAL

What is a Fraud Intentional mistakes to get unjust advantage are commonly known as fraud Fraud as defined by SA 240 is

bull An intentional act bull by one or more individuals among

1048707management 1048707those charged with governance 1048707employees 1048707or third parties

bull involving the use of deception bull to obtain an unjust or illegal advantagerdquo

Although fraud is a broad legal concept for the purposes of the SAs the auditor is concerned with fraud that causes a material misstatement in the financial statements Two types of intentional misstatements are relevant to the auditor ndash misstatements resulting from fraudulent financial reporting and misstatements resulting from misappropriation of assets eg To reflect a good financial position deliberately purchase is suppressed Here suppression of purchase is used for deception which is done intentionally by management and employees with the directions of those charged with governance As a result of this by showing inflated profit the entity will enjoy unjust or illegal advantage of fictitious financial health Hence we can conclude that Frauds are planned A person responsible for fraud has a knowledge of what he is doing Frauds are committed with due care Fraud will always result in loss to aggrieved party Frauds are deliberately concealed Usually errors are rectified and ratified but frauds should be reflected in financial statements Those charged with governance means persons charged supervising controlling and directing responsibility (include management only when they perform managerial persons) viz Audit committee under a company can be termed as committee of persons those charged with governance Illustrate by way of some example how Fraudulent Financial Reporting and Misappropriation of Asset can be done Examples of FFR

bull Manipulation falsification (including forgery) or alteration of accounting records or supporting documentation from which the financial statements are prepared

bull Misrepresentation in or intentional omission from the financial statements of events transactions or other significant information

bull Intentional misapplication of accounting principles relating to amounts classification manner of presentation or disclosure

bull Recording fictitious journal entries particularly close to the end of an accounting period to manipulate operating results or achieve other objectives

bull Inappropriately adjusting assumptions and changing judgments used to estimate account balances bull Omitting advancing or delaying recognition in the financial statements of events and transactions that have

occurred during the reporting period

Following are the examples of MOA bull Embezzling receipts (for example misappropriating collections on accounts receivable or diverting receipts in

respect of written-off accounts to personal bank accounts) bull Stealing physical assets or intellectual property (for example stealing inventory for personal use or for sale

stealing scrap for resale colluding with a competitor by disclosing technological data in return for payment) bull Causing an entity to pay for goods and services not received (for example payments to fictitious vendors

kickbacks paid by vendors to the entityrsquos purchasing agents in return for inflating prices payments to fictitious employees)

bull Using an entityrsquos assets for personal use (for example using the entityrsquos assets as collateral for a personal loan or a loan to a related party)

Who is responsible to prevent and detect Fraud According to SA-240 ldquoThe primary responsibility for the prevention and detection of fraud rests with both those charged with governance of the entity and management Management through internal control places a strong emphasis on fraud prevention which may reduce opportunities for fraud to take place How much Auditor is responsibilities for detection of Fraud According to SA-240 ldquo An auditor conducting an audit in accordance with SAs is responsible for btaining reasonable assurance that the financial statements taken as a whole are free from material misstatement whether caused by fraud or error Owing to the inherent limitations of an audit there is an unavoidable risk that some material misstatements of the financial statements will not be detected even though the audit is properly planned and performed in accordance with the SAs What are Inherent Limitations of Audit Inherent limitations means limitations obtained by the subject in inheritance ie since its evolution which cannot be overcome As per SA-240 An auditor cannot obtain absolute assurance that material misstatements in the financial statements will be detected Due to the inherent limitations of an audit there is an unavoidable risk that some material misstatements of the financial statements will not be detected even though the audit is properly planned and performed in accordance with the auditing standards generally accepted in India Followings can be listed as inherent limitation of audit

bull The use of judgment (about materiality sufficiency and appropriateness of audit evidence)

bull The use of testing (not extending deep audit procedures to a group of immaterial items)

bull The inherent limitations of internal control (defined in SA-330) and

bull The fact that much of the evidence available to the auditor is persuasive rather than conclusive in nature (Debtors confirmation is not conclusive evidence that he is good and will not result in bad in future it can only persuade the auditor to believe the existence of debtor))

bull The risk of not detecting a material misstatement resulting from fraud is higher than the risk of not detecting a material misstatement resulting from error

bull The risk of the auditor not detecting a material misstatement resulting from management fraud is greater than for employee fraud because those charged with governance and management are often in a position that assumes their integrity and enables them to override the formally established control procedures

As far as auditor lsquos responsibility is concerned as per SA240 ldquoWhen obtaining reasonable assurance the auditor is responsible for maintaining an attitude of professional skepticism throughout the audit What is Professional Skepticism Professional skepticism means vigilant attitude Auditor should not accept all the representations explanations as it is without a vigilant look over the same Unless the auditor has reason to believe the contrary the auditor may accept records and documents as genuine If conditions identified during the audit cause the auditor to believe that a document may not be authentic or that terms in a document have been modified but not disclosed to the auditor the auditor shall investigate further At the planning stage it required to communicate to the engagement team members that how and where the entityrsquos financial statements may be susceptible to material misstatement due to fraud including how fraud might occur The discussion shall occur notwithstanding the engagement team membersrsquo beliefs that management and those charged with governance are honest and have integrity What is objective of auditor as far as concerned with fraud in financial statement According to SA-240 the objectives of the auditor are (a) To identify and assess the risks of material misstatement in the financial statements due to fraud (b) To obtain sufficient appropriate audit evidence about the assessed risks of material misstatement due to fraud through designing and implementing appropriate responses and (c) To respond appropriately to identified or suspected fraud

PART-A Identifying and assessing the risk of material misstatement due to fraud

Following steps are required to be considered when auditor is assessing the risk of material misstatement due to fraud- 1 Understanding the entities business - According to SA315 auditor before planning the audit procedure should understand the entities business which helps him to identify fraud risk prone areas 2 Enquiries trough management - According to SA240 The auditor shall make inquiries of management regarding

a)Managements assessment of Fraud risk Factor - Auditor shall enquire that what is managementrsquos assessment of the fraud risk and how frequently management assesses the same further auditor shall evaluate the managementrsquos process for identifying and responding to the risks of fraud in the entity Auditor shall also enquire how management communicated such assessment to those charged with governance and employees so that the ethical behaviour can be established b)Knowledge about actual or suspected or alleged fraud- The auditor shall make inquiries of management those charged with governance and others within the entity as appropriate to determine whether they have knowledge of any actual suspected or alleged fraud affecting the entity

3 Enquiries with Internal Auditor - According to SA240 the auditor shall make inquiries of internal audit (if engaged bu entity)to determine whether it has knowledge of any actual suspected or alleged fraud affecting the entity and to obtain its views about the risks of fraud 4 Result of Auditorrsquos Analytical Procedures - At planning stage auditor applies certain analytical procedures (ie ratio analysis trend analysis ) over the financial statement When auditor applies such procedures he should evaluate the result of such procedures that whether unusual or unexpected relationships that have been identified in performing analytical procedures including those related to revenue accounts may indicate risks of material misstatement due to fraud

PART-B Obtain sufficient appropriate audit evidence about the assessed risks of material misstatement due to fraud

As in Part A we have seen how auditor assesses the Fraud Risk in financial statement now we will understand how auditor will respond through his audit procedure to address the Fraud Risk Factors Auditor will have two kind of responses to such risks 1 Overall Response - Overall response means collective impact of all fraud risk factors over the financial statement as a whole In determining overall responses to address the assessed risks of material misstatement due to fraud at the financial statement level the auditor shall depute adequately skilled and experienced engagement team which has knowledge of significant engagement responsibilities and the auditorrsquos assessment of the risks of material misstatement due to fraud for the engagement Further Auditor shall evaluate whether the selection and application of accounting policies by related to subjective measurements and complex transactions Auditor shall incorporate an element of unpredictability in the selection of the nature timing and extent of audit procedures 2 Auditorrsquos Response to Assertion Level - In accordance with SA 330 the auditor shall design and perform further audit procedures whose nature timing and extent are responsive to the assessed risks of material misstatement due to fraud at the assertion level As we know management is in a position to override the internal controls according to SA240 auditor shall apply following procedure to satisfy himself that management had not misused it lsquos position to give a room for fraud to take place (a) Test the appropriateness of journal entries recorded

bull Enquire employees involved in the financial reporting process about inappropriate or unusual activity relating to the processing of journal entries and other adjustments

bull Select journal entries and other adjustments made at the end of a reporting period and bull Consider the need to test journal entries and other adjustments throughout the period

(b) Review accounting estimates involved - As we know risk of fraud is greater where the estimates are involved auditor shall evaluate whether accounting estimates are appropriate and not biased In performing this review the auditor shall Evaluate whether the judgments and decisions made by management indicate a possible bias on the part of the entityrsquos management that may represent a risk of material misstatement due to fraud If so the auditor shall re-evaluate the accounting estimates taken as a whole and Perform a retrospective review of management judgments and assumptions related to significant accounting estimates reflected in the financial statements of the prior year8 After above response to audit risk by applying audit procedures audit will obtain sufficient and appropriate audit evidences Now it is required for auditor to evaluate the audit evidence obtained through above procedure

PART-C Response to identified or suspected fraud

1 Audit Evidences showing that there is a misstatement - As auditor found a misstatement in Financial Statement the auditor shall evaluate whether such a misstatement is indicative of fraud If there is such an indication the auditor shall evaluate the implications of the misstatement in relation to other aspects of the audit particularly the reliability of management representations recognizing that an instance of fraud is unlikely to be an isolated occurrence If the auditor identifies a misstatement whether material or not and the auditor has reason to believe that it is or may be the result of fraud and that management (in particular senior management) is involved the auditor shall re-evaluate the assessment of the risks of material misstatement due to fraud and its resulting impact on the nature timing and extent of audit procedures to respond to the assessed risks The auditor shall also consider whether circumstances or conditions indicate possible collusion involving employees management or third parties when

reconsidering the reliability of evidence previously obtained When the auditor confirms that the financial statements are materially misstated as a result of fraud the auditor shall evaluate the implications The implications may be that either he issue a qualified opinion and if the magnitude of the fraud is extremely significant auditor may issue an adverse opinion 2 Auditor unable to conclude whether or not misstatement exist or not ndash In such cases auditor may issue a reservation of opinion or if magnitude of suspected fraud is extremely significant auditor shall issue a reservation of opinion or disclaimer of opinion Can auditor may decide to withdraw from his engagement According to SA 240 If as a result of a misstatement resulting from fraud or suspected fraud the auditor encounters exceptional circumstances that bring into question the auditorrsquos ability to continue performing the audit the auditor shall (a) Determine the professional and legal responsibilities applicable in the circumstances including whether there is a requirement for the auditor to report to the person or persons who made the audit appointment or in some cases to regulatory authorities (b) Consider whether it is appropriate to withdraw from the engagement where withdrawal from the engagement is legally permitted and (c) If the auditor withdraws (i) Discuss with the appropriate level of management and those charged with governance the auditorrsquos withdrawal from the engagement and the reasons for the withdrawal and (ii) Determine whether there is a professional or legal requirement to report to the person or persons who made the audit appointment or in some cases to regulatory authorities the auditorrsquos withdrawal from the engagement and the reasons for the withdrawal What kind of Representation by Management required under SA-240 According to SA240 ldquo The auditor shall obtain written representations from management that (a) It acknowledges its responsibility for the design implementation and maintenance of internal control to prevent and detect fraud (b) It has disclosed to the auditor the results of its assessment of the risk that the financial statements may be materially misstated as a result of fraud (c) It has disclosed to the auditor its knowledge of fraud or suspected fraud affecting the entity involving (i) Management (ii) Employees who have significant roles in internal control or (iii) Others where the fraud could have a material effect on the financial statements and (d) It has disclosed to the auditor its knowledge of any allegations of fraud or suspected fraud affecting the entityrsquos financial statements communicated by employees former employees analysts regulators or others What are the Auditors responsibilities of communication of fraud or Suspected fraud According to SA240 - If the auditor has identified a fraud or has obtained information that indicates that a fraud may exist the auditor shall communicate these matters on a timely basis to the appropriate level of management The auditor shall communicate these matters to those charged with governance also on a timely basis Is it required for the auditor to communicate to Regulatory and Enforcement Authorities In India presently it is not required by any law to communicate the instance of fraud to regulatory or enforcement authorities but SA240 has a provision that if law requires such reporting auditor should report accordingly Although the auditorrsquos professional duty to maintain the confidentiality of client information may preclude such reporting the auditorrsquos legal duty may have an overriding effect over the same Give some Examples of circumstances that Indicate the Possibility of Fraud The following are examples of circumstances that may indicate the possibility that the financial statements may contain a material misstatement resulting from fraud

bull Transactions that are not recorded in a complete or timely manner or are improperly recorded as to amount accounting period classification or entity policy

bull Unsupported or unauthorized balances or transactions bull Last-minute adjustments that significantly affect financial results bull Evidence of employeesrsquo access to systems and records inconsistent with that necessary to perform their

authorized duties bull Tips or complaints to the auditor about alleged fraud bull Missing documents bull Documents that appear to have been altered bull Unavailability of other than photocopied or electronically transmitted documents when documents in original form

are expected to exist bull Significant unexplained items on reconciliations

bull Unusual balance sheet changes or changes in trends or important financial statement ratios or relationships for example receivables growing faster than revenues

bull Inconsistent vague or implausible responses from management or employees arising from inquiries or analytical procedures

bull Unusual discrepancies between the entitys records and confirmation replies bull Large numbers of credit entries and other adjustments made to accounts receivable records bull Unexplained or inadequately explained differences between the accounts receivable sub-ledger and the control

account or between the customer statements and the accounts receivable sub-ledger

SA 250 (R) - Consideration of Laws and Regulations in an Audit of Financial Statements

Q What is the term Noncompliance with laws and regulation means Non-compliance means acts of omission or commission by the entity either intentional or unintentional which are contrary to the prevailing laws or regulations Non-compliance does not include personal misconduct (unrelated to the business activities of the entity) by those charged with governance management or employees of the entity Q What is Auditorrsquos Duty in relation to the same Following are the Duties of auditor as per SA250 1 Duty to understand the entities Environment and to obtain general understanding about (a) The legal and regulatory framework applicable to the entity and the industry or sector in which the entity operates and (b) How the entity is complying with that framework 2 Duty to obtain sufficient appropriate audit evidence The auditor shall obtain sufficient appropriate audit evidence regarding compliance with the provisions of those laws and regulations generally recognised to have a direct effect on the determination of material amounts and disclosures in the financial statements 3Duty to perform procedures The auditor shall perform the following audit procedures to help identify instances of non-compliance with other laws and regulations that may have a material effect on the financial statements (a) Inquiring of management and where appropriate those charged with governance as to whether the entity is in compliance with such laws and regulations and (b) Inspecting correspondence if any with the relevant licensing or regulatory authorities 4 Duty to Remain Alert - The auditor shall remain alert to the possibility that other audit procedures applied may bring instances of non-compliance or suspected non-compliance with laws and regulations to the auditorrsquos attention 5Duty to obtain Representations by Management - The auditor shall request management and where appropriate those charged with governance to provide written representations that all known instances of non-compliance or suspected non-compliance with laws and regulations whose effects should be considered when preparing financial statements have been disclosed to the auditor Q What Audit Procedures required to applied by the auditor when Non-Compliance is Identified or Suspected If the auditor becomes aware of information concerning an instance of non-compliance or suspected non-compliance with laws and regulations the auditor shall obtain (a) An understanding of the nature of the act and the circumstances in which it has occurred and (b) Further information to evaluate the possible effect on the financial statements If the auditor suspects there may be non-compliance the auditor shall discuss the matter with management and where appropriate those charged with governance If management or as appropriate those charged with governance do not provide sufficient information that supports that the entity is in compliance with laws and regulations and in the auditorrsquos judgment the effect of the suspected non-compliance may be material to the financial statements the auditor shall consider the need to obtain legal advice If sufficient information about suspected non-compliance cannot be

obtained the auditor shall evaluate the effect of the lack of sufficient appropriate audit evidence on the auditorrsquos opinion Q What are reporting responsibility of the Auditor for non compliance with the laws and regulations by the entity under audit In case where those charged with governance are not directly involved in the management of the business auditor shall communicate with those charged with governance matters involving non-compliance with laws and regulations that come to the auditorrsquos attention during the course of the audit If Auditor finds that non-compliance is believed to be intentional and material the auditor shall communicate the matter to those charged with governance as soon as practicable If the auditor suspects that management or those charged with governance are involved in non-compliance the auditor shall communicate the matter to the next higher level of authority at the entity if it exists such as an audit committee or supervisory board Where no higher authority exists or if the auditor believes that the communication may not be acted upon or is unsure as to the person to whom to report the auditor shall consider the need to obtain legal advice Q What shall be effect of Non Compliance on Auditorrsquos Report 1 When Auditor has Sufficient and Appropriate Audit evidence that non compliance exist- If the auditor concludes that the non-compliance has a material effect on the financial statements and has not been adequately reflected in the financial statements the auditor shall in accordance SA-700 express a qualified or adverse opinion on the financial statements 2 When auditor has limitations on scope of Audit - If the auditor is precluded by management or those charged with governance from obtaining sufficient appropriate audit evidence regarding non-compliance the auditor shall express a qualified opinion or disclaim an opinion on the financial statements on the basis of a limitation on the scope of the audit in accordance with SA-700 Furhter If the auditor has identified or suspects non-compliance with laws and regulations the auditor shall determine whether the auditor has a responsibility to report the identified or suspected non-compliance to parties outside the entity

SA- 260 (Revised) - Communication with Those Charged with Governance

What do you mean by Those Charged with Governance According to SA 260 Those charged with governance refers to person(s) or organisation(s) (ega corporate trustee) with responsibility for overseeing the strategic direction of the entity and obligations related to the accountability of the entity This includes overseeing the financial reporting process For some entities those charged with governance may include management personnel for example executive members of a governance board of a private or public sector undertakings or an owner-manager In some cases those charged with governance are responsible for approving the entityrsquos financial statements (in other cases management has this responsibility) On the other hand the word management refers to person(s) with executive responsibility for the conduct of the entityrsquos operations What is Objective of auditor to communicate with those charged with governance According to SA-260 -The objectives of the auditor are to (a) Communicate clearly with those charged with governance

bull the responsibilities of the auditor in relation to the financial statement audit bull and an overview of the planned scope and timing of the audit

(b) Obtain information relevant to the audit from those charged with governance (c) Provide timely significant observations arising from the audit relevant to oversee the financial reporting process for those charged with governance (d) Promote effective two-way communication between the auditor and those charged with governance What matters are required to be communicated 1 The Auditorrsquos Responsibilities in Relation to the Financial Statement Audit The auditor shall communicate that he is responsible for forming and expressing an opinion on the financial statements that have been prepared by management with the oversight of those charged with governance and the audit of the financial statements does not relieve management or those charged with governance of their responsibilities 2Planned Scope and Timing of the Audit The auditor shall communicate an overview of the planned scope and timing of the audit

3 Significant Findings from the Audit a)The auditor shall communicate his views about significant qualitative aspects of the entityrsquos accounting practices including accounting policies accounting estimates and financial statement disclosures (b) Significant difficulties if any encountered during the audit (c) Unless all of those charged with governance are involved in managing the entity (i) Material weaknesses if any in the design implementation or operating effectiveness of internal control that have come to the auditorrsquos attention and have been communicated to management as required by SA 315 or SA 330 (ii) Significant matters if any arising from the audit that were discussed or subject to correspondence with management and (iii) Written representations the auditor is requesting and (d) Other matters if any arising from the audit that in the auditorrsquos professional judgment are significant to the oversight of the financial reporting process In Case of Listed entities what are additional communication auditor is required to do According to SA260 In the case of listed entities the auditor shall communicate with those charged with governance that the engagement team and others in the firm as appropriate the firm and when applicable network firms have complied with relevant ethical requirements regarding independence and all relationships and other matters between the firm network firms and the entity that in the auditorrsquos professional judgment may reasonably be thought to bear on independence This shall include total fees charged during the period covered by the financial statements for audit and nonaudit services provided by the firm and network firms to the entity and components controlled by the entity These fees shall be allocated to categories that are appropriate to assist those charged with governance in assessing the effect of services on the independence of the auditor and The related safeguards that have been applied to eliminate identified threats to independence or reduce them to an acceptable level

What other consideration are required under this SA260 1 The auditor shall communicate in writing with those charged with governance when in the auditorrsquos professional judgment oral communication would not be adequate Where matters required by this SA to be communicated are communicated orally the auditor shall document them and when and to whom they were communicated Where matters have been communicated in writing the auditor shall retain a copy of the communication as part of the audit documentation 2 The auditor shall communicate with those charged with governance on a timely basis 3 The auditor shall evaluate whether the two-way communication between the auditor and those charged with governance has been adequate for the purpose of the auditInadequacy may lead auditor to suspicion about existence of misstatement

SA 265 (Newly issued) COMMUNICATING DEFICIENCIES IN INTERNAL CONTROL TO THOSE CHARGED WITH GOVERNANCE AND MANAGEMENT

NOTE- Students shall note that usually this kind of communication is known as ldquo Letter of Weaknessrdquo What should be the objective of Auditor according to this SA265 According to SA265 - The objective of the auditor is to communicate appropriately to those charged with governance and management deficiencies in internal control that the auditor has identified during the audit and that in the auditorrsquos professional judgment are of sufficient importance to merit their respective attentions What do you mean by deficiency in Internal Control According to SA 265 - Deficiency in internal control ndash This exists when a control is designed implemented or operated in such a way that it is either unable to prevent or detect and correct misstatements in the financial statements on a timely basis or it is missing What are the requirements under this SA265

According to SA265 The auditor shall determine whether he has identified one or more deficiencies in internal control If yes he shall determine whether individually or in combination they constitute significant deficiencies If auditor concludes that deficiencies are significant he shall communicate in writing significant deficiencies in internal control identified during the audit to management and those charged with governance on a timely basis It is further explained in SA265 that The auditor shall give full description of the deficiencies and an explanation of their potential effects so that to enable those charged with governance and management to understand the context of the communication Further it is required that auditor shal explain that the purpose of the audit was for the auditor to express an opinion on the financial statements and the audit included consideration of internal control relevant to the preparation of the financial statements in order to design audit procedures that are appropriate in the circumstances but not for the purpose of expressing an opinion on the effectiveness of internal control

SA-450 EVALUATION OF MISSTATEMENTS IDENTIFIED DURING THE AUDIT

What is Auditorrsquos objective in this SA The objective of the auditor is to evaluate (a) The effect of identified misstatements on the audit and (b) The effect of uncorrected misstatements if any on the financial statements What do you mean by misstatement and uncorrected misstatements Misstatement refers to A difference between the amounts classification presentation or disclosure of a reported financial statement item and the amount classification presentation or disclosure that is required for the item to be in accordance with the applicable financial reporting framework Misstatements can arise from error or fraud On the other hand uncorrected misstatements refer to Misstatements that the auditor has accumulated during the audit and that have not been corrected Requirements Step-1 Consideration of Identified Misstatements as the Audit Progresses The auditor shall determine whether the overall audit strategy and audit plan need to be revised if (a) The nature of identified misstatements and the circumstances of their occurrence indicate that other misstatements may exist that when aggregated with misstatements accumulated during the audit could be material or (b) The aggregate of misstatements accumulated during the audit approaches materiality determined in accordance with SA 320 (Revised) If at the auditorrsquos request management has examined a class of transactions account balance or disclosure and corrected misstatements that were detected the auditor shall perform additional audit procedures to determine whether misstatements remain Step-2 Communication and Correction of Misstatements The auditor shall communicate on a timely basis all misstatements accumulated during the audit with the appropriate level of management unless prohibited by law or regulation5The auditor shall request management to correct those misstatements If management refuses to correct some or all of the misstatements communicated by the auditor the auditor shall obtain an understanding of managementrsquos reasons for not making the corrections and shall take that understanding into account when evaluating whether the financial statements as a whole are free from material misstatement Step-3 Communication with Those Charged with Governance The auditor shall communicate with those charged with governance uncorrected misstatements and the effect that they individually or in aggregate may have on the opinion in the auditorrsquos report unless prohibited by law or regulation The auditorrsquos communication shall identify material uncorrected misstatements individually The auditor shall request that uncorrected misstatements be corrected The auditor shall also communicate with those charged with governance the effect of uncorrected misstatements related to prior periods on the relevant classes of transactions account balances or disclosures and the financial statements as a whole Step-5 Written Representation The auditor shall request a written representation from management and where appropriate those charged with governance whether they believe the effects of uncorrected misstatements are immaterial individually and in aggregate to the financial statements as a whole A summary of such items shall be included in or attached to the written representation Step-5 Documentation 15 The audit documentation shall include (a) The amount below which misstatements would be regarded as clearly trivial (b) All misstatements accumulated during the audit and whether they have been and (c) The auditorrsquos conclusion as to whether uncorrected misstatements are material individually or in aggregate and the basis for that conclusion

What do you mean by Audit Evidences

Audit evidence ndash Information used by the auditor in arriving at the conclusions on which the auditorrsquos opinion is based Audit evidence includes both information contained in the accounting records underlying the financial statements and other information What is duty of an auditor regarding audit evidences As per SA-200 The auditor should obtain sufficient appropriate audit evidence through the performance of compliance and substantive procedures to enable him to draw reasonable conclusions there from on which to base his opinion on the financial information further under point no 9 of SA-200 ldquoAudit conclusion and reportingrdquo it is concluded that the auditor should review and assess the conclusions drawn from the audit evidence obtained and from his knowledge of business of the entity as the basis for the expression of his opinion on the financial information Hence from the above we can conclude that auditors opinion should be supported by reasonable conclusions and reasonable conclusions should be backed by sufficient and appropriate audit evidences According to SA500 The auditor shall design and perform audit procedures that are appropriate in the circumstances for the purpose of obtaining sufficient appropriate audit evidence What is Phenomenon of Sufficient and Appropriate Audit Evidence SA 500 defined the term Sufficient and Appropriate as follows- Sufficiency of audit evidence ndash The measure of the quantity of audit evidence The quantity of the audit evidence needed is affected by the auditorrsquos assessment of the risks of material misstatement and also by the quality of such audit evidence viz at least two evidences are required to conclude about the balance in bank - copy of Bank Statement and bank reconciliation statement) Appropriateness of Audit Evidence - The measure of the quality of audit evidence that is its relevance and its reliability in providing support for the conclusions on which the auditorrsquos opinion is based (Copy of bank statement should be duly certified by the bank manager and BRS shall be passed by Managers account and corresponding entries required have been made in books of acounts) It is auditorrsquos professional judgement whether he obtained SampA audit evidences or not It all depends upon how much the item concerned is material whether risk of misstatement is there or not relating to any item of financial statement nature and complexity of financial information etc What are the sources of Audit Evidences According to SA500 (revised) Audit evidences can be obtained by the auditor from sources within the entity (generally known as internal sources) viz bank reconciliation statement and Sources independent from the entity (generally known as external sources ) viz Copy of bank statement duly signed by the manager of the bank Evidences obtained from internal sources commonly known as Internal audit evidences and evidences obtained from source independent of entity is commonly known as external audit evidences As far as nature of the audit evidences concern they may be documentary (viz registry of land) oral (viz oral confirmation by management )or visual ( viz Physical Verification by management) What are the Audit Procedures prescribed under SA500 According to SA-500 As required by and explained further in SA 315 and SA 330 audit evidence to draw reasonable conclusions on which to base the auditorrsquos opinion is obtained by performing (a) Risk assessment procedures and (b) Further audit procedures which comprise (i) Tests of controls (previously known as Compliance Procedures) when required by the SAs or when the auditor has chosen to do so and (ii) Substantive procedures including tests of details and substantive analytical procedures (a) As Risk Assessment procedures are defined in SA 315 and SA330 let us understand What are test of control and Substantive procedures

SA 500 Revised ndash Audit Evidence

What do you mean by Audit Evidences Audit evidence ndash Information used by the auditor in arriving at the conclusions on which the auditorrsquos opinion is based Audit evidence includes both information contained in the accounting records underlying the financial statements and other information What is duty of an auditor regarding audit evidences As per SA-200 The auditor should obtain sufficient appropriate audit evidence through the performance of compliance and substantive procedures to enable him to draw reasonable

conclusions there from on which to base his opinion on the financial information further under point no 9 of SA-200 ldquoAudit conclusion and reportingrdquo it is concluded that the auditor should review and assess the conclusions drawn from the audit evidence obtained and from his knowledge of business of the entity as the basis for the expression of his opinion on the financial information Hence from the above we can conclude that auditors opinion should be supported by reasonable conclusions and reasonable conclusions should be backed by sufficient and appropriate audit evidences According to SA500 The auditor shall design and perform audit procedures that are appropriate in the circumstances for the purpose of obtaining sufficient appropriate audit evidence What is Phenomenon of Sufficient and Appropriate Audit Evidence SA 500 defined the term Sufficient and Appropriate as follows- Sufficiency of audit evidence ndash The measure of the quantity of audit evidence The quantity of the audit evidence needed is affected by the auditorrsquos assessment of the risks of material misstatement and also by the quality of such audit evidence viz at least two evidences are required to conclude about the balance in bank - copy of Bank Statement and bank reconciliation statement) Appropriateness of Audit Evidence - The measure of the quality of audit evidence that is its relevance and its reliability in providing support for the conclusions on which the auditorrsquos opinion is based (Copy of bank statement should be duly certified by the bank manager and BRS shall be passed by Managers account and corresponding entries required have been made in books of acounts) It is auditorrsquos professional judgement whether he obtained SampA audit evidences or not It all depends upon how much the item concerned is material whether risk of misstatement is there or not relating to any item of financial statement nature and complexity of financial information etc What are the sources of Audit Evidences According to SA500 (revised) Audit evidences can be obtained by the auditor from sources within the entity (generally known as internal sources) viz bank reconciliation statement and Sources independent from the entity (generally known as external sources ) viz Copy of bank statement duly signed by the manager of the bank Evidences obtained from internal sources commonly known as Internal audit evidences and evidences obtained from source independent of entity is commonly known as external audit evidences As far as nature of the audit evidences concern they may be documentary (viz registry of land) oral (viz oral confirmation by management )or visual ( viz Physical Verification by management) What are the Audit Procedures prescribed under SA500 According to SA-500 As required by and explained further in SA 315 and SA 330 audit evidence to draw reasonable conclusions on which to base the auditorrsquos opinion is obtained by performing (a) Risk assessment procedures and (b) Further audit procedures which comprise (i) Tests of controls (previously known as Compliance Procedures) when required by the SAs or when the auditor has chosen to do so and (ii) Substantive procedures including tests of details and substantive analytical procedures (a) As Risk Assessment procedures are defined in SA 315 and SA330 let us understand What are test of control and Substantive procedures (b) Further Audit Procedures (i)Test of Controls (Previously known as Compliance Procedure in old version of SA500)-Tests of controls are designed to

bull evaluate the operating effectiveness of controls in preventing or detecting and correcting material misstatements at the assertion level

bull to obtain relevant audit evidence that indicate o performance of a control and o deviation conditions which indicate departures from adequate performance

The presence or absence of those conditions can then be tested by the auditor

Example of Test of Control -Following is the conversation between the auditor of X ltd and accountant of the X Ltd on 31032005

Auditor Do you prepare bank reconciliation statements

Accountant Yes

Auditor Please show me the latest BRS

Accountant This is latest BRS prepared as on 30102009

Auditor Whats this You have not given any effect to the pending entries from August and September 09 What is your frequency to prepare BRS

Accountant Half yearly

From the above we can conclude that although internal control over the bank operations is in existence but it is neither effective and nor continuously in operation over the period of reliance to be placed on it (ii)Substantive Procedures - Substantive procedures are designed to detect material misstatements at the assertion level They comprise tests of details and substantive analytical procedures Designing substantive procedures includes identifying conditions relevant to the purpose of the test that constitute a misstatement in the relevant assertion If auditor applies substantive procedure over and item of financial statement like building we can correlate the observations under substantive procedure mentioned above nce Physical verification of the building

Rights and Obligations Whether the building is in the name of the company