RTI, MUMBAI - ENV. AUDITING DAY 2.1.1 1 Performance Audit, Compliance Audit, Financial Audit The SAI...

40

RTI, MUMBAI - ENV. AUDITI NG DAY 2.1.1 1 Performance Audit, Compliance Audit, Financial Audit • The SAI may undertake environmental audits under its mandate to carry out regularity (financial and compliance) audits or performance audits as defined in the INTOSAI Auditing Standards.

-

Upload

herbert-reed -

Category

Documents

-

view

215 -

download

0

Transcript of RTI, MUMBAI - ENV. AUDITING DAY 2.1.1 1 Performance Audit, Compliance Audit, Financial Audit The SAI...

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

1

Performance Audit, Compliance Audit, Financial Audit

• The SAI may undertake environmental audits under its mandate to carry out regularity (financial and compliance) audits or performance audits as defined in the INTOSAI Auditing Standards.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

2

Performance Audit, Compliance Audit, Financial Audit (Cont)

• Regularity audit comprises• Compliance audit, financial audit• Compliance audit deals examination of the entity’s

response in matters relating to provisions of acts, rules and regulations of the land. Its obligations and the likely aftereffects for not complying with them– penalties may be levied. Some times the units will be closed for the offence

Financial audit relates to attesting of the correctness of the financial statements, assets and liabilities, contingent liabilities etc.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

3

Contd..

• Environmental accounting envisages estimating and considering the value of environmental assets, natural resources accounting, provision of liabilities etc.

• Environmental cost plays a major role in the environmental accounting

• It is both the upfront and back end cost• It is some times merged with other costs and loses

its importance as an environmental cost on which top management wants to take cognizance of

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

4

Contd..

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

5

Taking Account of Environmental Issues in a

Regularity Audit • Governments are increasingly recognizing that the

costs arising from environmental policies and obligations – such as the cost of pollution abatement equipment or the cost of decontamination of land – may be significant. These policies and obligations may also introduce material liabilities or contingent liabilities where the costs depend on the possible occurrence of a future event. Environmental impacts can also significantly affect the valuation of land, buildings, plant and equipment.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

6

Taking Account of Environmental Issues in a Regularity Audit (Cont...)

• These environmental costs, liabilities and impacts on asset values affect both the preparation and audit of financial statements. Some Governments have made specific commitments about their disclosure. The difficulty can be that the audited entity might not distinguish environmental costs from expenditure associated with its ongoing activities.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

7

Taking Account of Environmental Issues in a Regularity Audit (Cont...)

• The regularity auditor will need to assess the completeness and accuracy of the figures reported. To do so, the auditor will need a sound understanding of the environmental issues, operation and activities which could affect the audited entity’s financial position, in the long as well as the short term.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

8

Taking Account of Environmental Issues in a Regularity Audit (Cont...)

• Established professional national and international accounting and auditing standards set out the principles underlying the treatment of costs, assets and liabilities in financial statements which would apply to the treatment of environmental costs and liabilities. The SAI can apply these standards in judging the need for disclosing environmental impacts on costs, liabilities and assets in Government financial statements.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

9

The SAI may need to audit estimates of the extent of such costs and liabilities.

• The auditor -– Should consider both the actual and potential costs

and impacts of environmental issues.– Will need to confirm existing and likely changes to

the legislative or other requirements, the technology to be applied, and the costing used in the estimates.

– Will need to reach a judgement on the reliability of the assumptions used for predicting future costs, liabilities and asset values, and the accuracy of the calculations

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

10

Involvement of third parties

• The SAI may seek to rely on the work of third parties in making these audit judgments, in which case it will need to take particular care to satisfy itself of the qualifications and independence of the experts involved.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

11

Performance Auditing and the Environment

• Performance audit, in the context of an audited entity’s performance in carrying out Government environmental programmes and activities, may where applicable, be concerned with– The Economy of administrative practices;– The Efficiency of utilization of human, financial or

activity; and– The Effectiveness of the programme or activity in

achieving its objectives and its intended impact.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

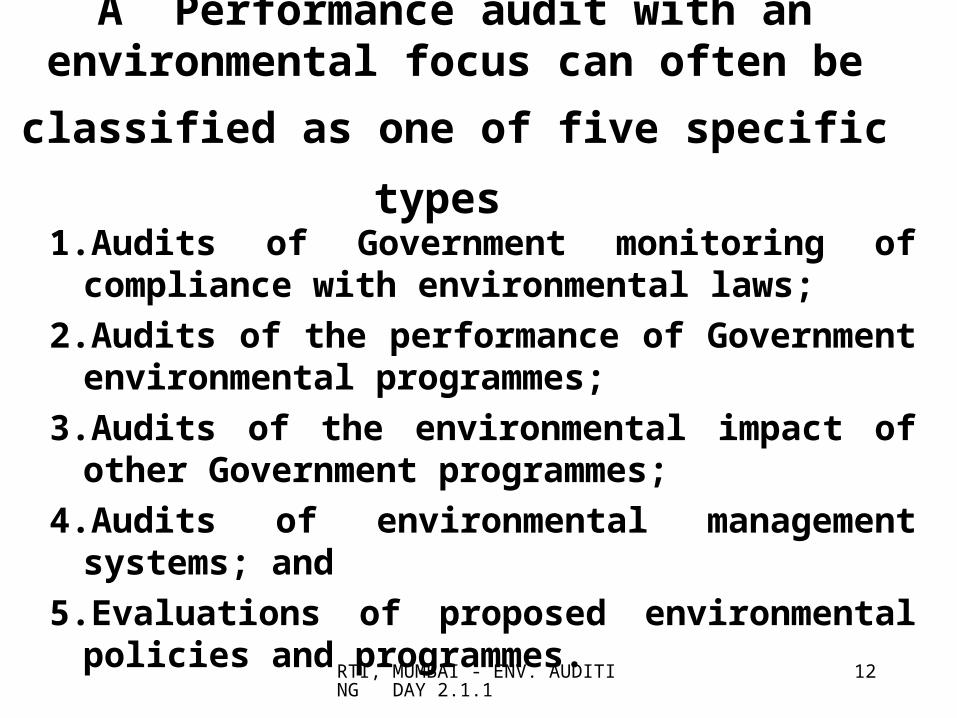

12

A Performance audit with an environmental focus can often be classified as one of five

specific types 1.Audits of Government monitoring of compliance

with environmental laws;

2.Audits of the performance of Government environmental programmes;

3.Audits of the environmental impact of other Government programmes;

4.Audits of environmental management systems; and

5.Evaluations of proposed environmental policies and programmes.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

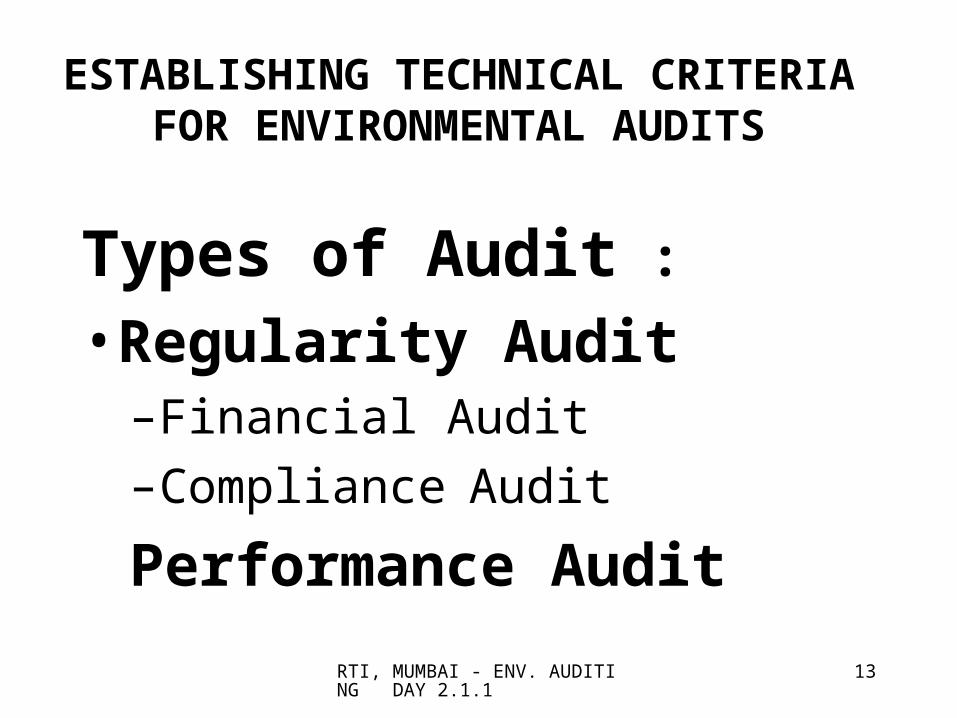

13

ESTABLISHING TECHNICAL CRITERIA FOR ENVIRONMENTAL AUDITS

Types of Audit :

• Regularity Audit– Financial Audit

– Compliance Audit

Performance Audit

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

14

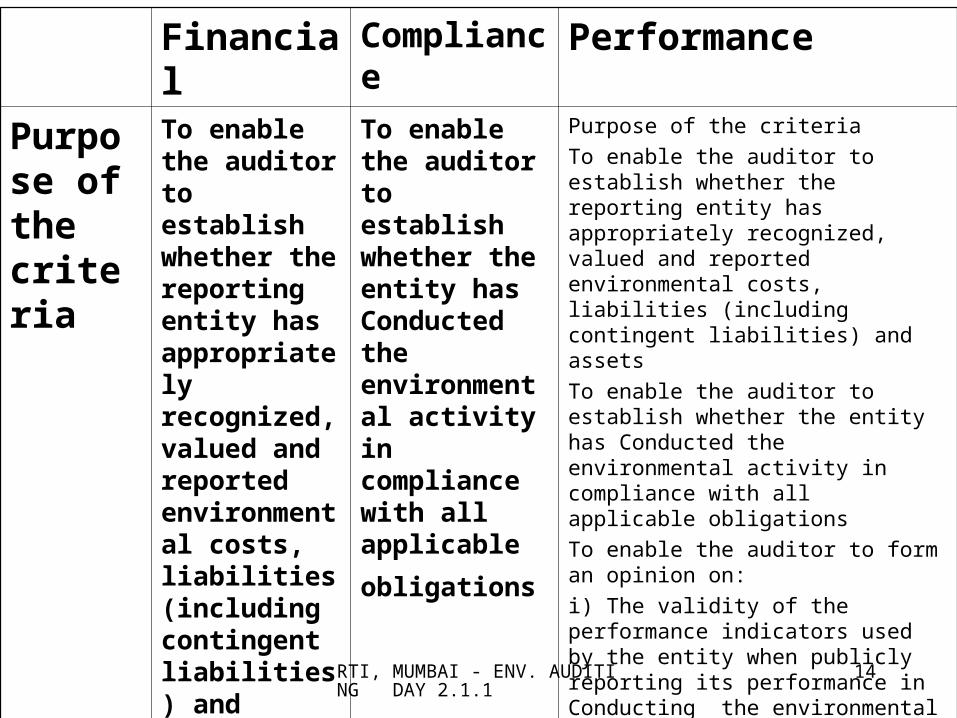

Financial Compliance Performance

Purpose of the criteria

To enable the auditor to establish whether the reporting entity has appropriately recognized, valued and reported environmental costs, liabilities (including contingent liabilities) and assets

To enable the auditor to establish whether the entity has Conducted the environmental activity in compliance with all applicable

obligations

Purpose of the criteria

To enable the auditor to establish whether the reporting entity has appropriately recognized, valued and reported environmental costs, liabilities (including contingent liabilities) and assets

To enable the auditor to establish whether the entity has Conducted the environmental activity in compliance with all applicable obligations

To enable the auditor to form an opinion on:

i) The validity of the performance indicators used by the entity when publicly reporting its performance in Conducting the environmental activity.

ii) Whether the entity has Conducted the environmental activity in an effective, efficient, and economical manner consistent with the applicable governmental policy and any other factors affecting the Conduct of the activity over which the entity has no control.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

15

Guidance on Conducting Audits of Activities with an Environmental Perspective

Sources of the

criteria -

Authoritative (= “certainty”)

i) Any source falling within the meaning of “generally accepted accounting practice” (or its equivalent term) in the jurisdiction in which the entity is reporting. Sources could include:

Mandatory standards issued by an authoritative standard-setting body.

Standards issued by some other recognized body.

International standards issued by a recognized body.

i) National:

Laws.

Official governmental policies.

Binding standards.

Contracts

Policy directives.

ii) International

Laws.

Agreements (such as treaties with other jurisdiction and United Nations Conventions).

i) Performance indicators or measures of effectiveness, efficiency and economy that are prescribed by law or in the official governmental policy, or that are otherwise mandatory on the entity.

ii) Generally accepted standards issued by a recognized body.

iii) Codes of professional practice.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

16

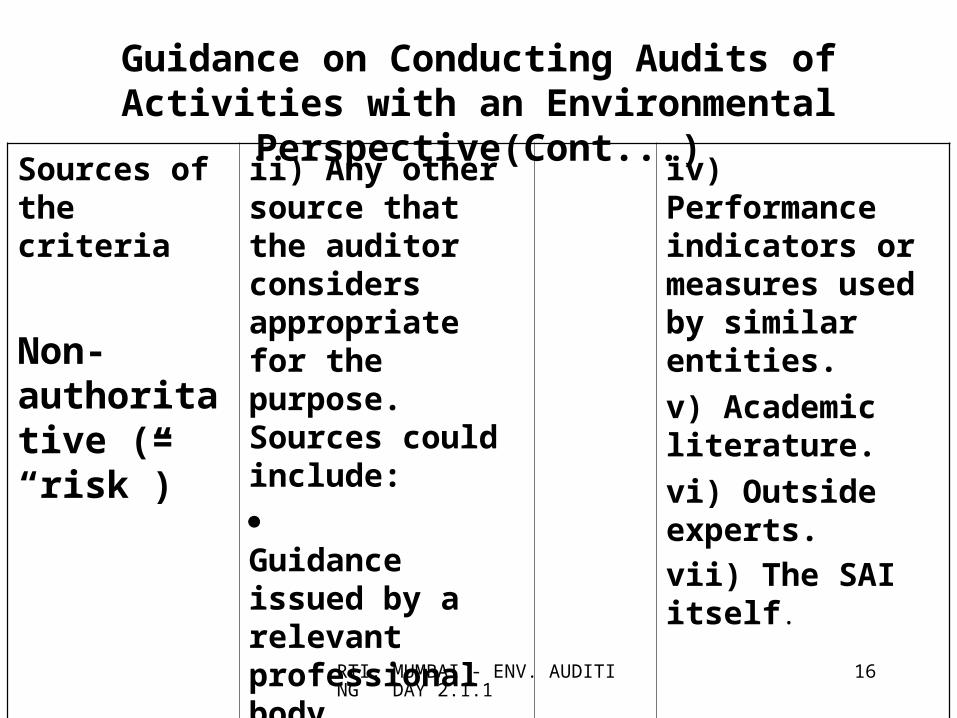

Guidance on Conducting Audits of Activities with an Environmental Perspective(Cont...)

Sources of the criteria

Non-authoritative (= “risk”)

ii) Any other source that the auditor considers appropriate for the purpose. Sources could include:

Guidance issued by a relevant professional body.

Academic literature.

iv) Performance indicators or measures used by similar entities.

v) Academic literature.

vi) Outside experts.

vii) The SAI itself.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

17

Powers and Functions of

Pollution Control Boards

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

18

Functions of Central Board

1. Subject to the provisions of this Act, and without prejudice to the performance of its functions under the Water (Prevention and Control of pollution) Act, 1974 (6 of 1974), the main functions of the Central Board shall be to improve the quality of Air, Water, Soil and to prevent, control or abate pollution in the country.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

19

Functions of Central Board (continue)

2) In particular and without prejudice to the generality of the foregoing functions, the Central Board may:-

a) advise the Central Government on any matter concerning the improvement of the quality of Air, Water, Soil and the prevention, control or abatement of pollution;

b) plan and cause to be executed a nationwide programme for the prevention, control or abatement of pollution;

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

20

c) co-ordinate the activities of State Board and resolve disputes among them;

d) provide technical assistance and guidance to the State Boards, carry out and sponsor investigations and research relating to problems of pollution and prevention, control or abatement of pollution; resolve disputes among them;

e) perform such of the functions of any State Board as may be specified in an order made sub-section (2) of Section 18;

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

21

f) plan and organize the training of persons engaged or to be engaged in programmes for the prevention, control or abatement of pollution on such terms and Conditions as the Central Board may specify.

g) collect, compile and publish technical and statistical data relating to pollution and the measures devised for its effective prevention, control or abatement and prepare manuals, codes or guides relating to prevention, control or abatement of pollution;

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

22

h) lay down standards for the quality of Air, Water, Soil, Land, etc.

i) collect and disseminate information is respect of matters relating to pollution;

j) perform such other functions as may be prescribed.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

23

Functions of State Board

1) Subject to the provisions of this Act, and without prejudice to the performance of its functions, if any, under the Water (Prevention and Control of Pollution) Act, 1974 (6 of 1974), the functions of a State Board are specified under this section.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

24

Power to give directions:-1) In the performance of its functions under this Act:-

a) the Central Board shall be bound by such directions in writing as the Central Government may give to it; and

b) every State Board shall be bound by such directions in writing as the Central Board or the State Government may give to it:

Provided that where a direction given by the State Government is inconsistent with the direction given by the Central Board, the matter shall be referred to the Central Government for its decision.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

25

2)Where the Central Government is of the opinion that any State Board has defaulted in complying with any directions given by the Central Board under sub-section (1) and as a result of such default a grave emergency has arisen and it is necessary or expedient so to do in the public interest, it may, by order, direct the Central Board to perform any of the functions of the State Board in relation to such area, for such period and for such purposes, as may be specified in the order.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

26

3) Where the Central Board performs any of the functions of the State Board in pursuance of a direction under sub-section (2) the expenses, if any, incurred by the Central Board with respect to the performance of such functions may, if the State Board is empowered to recover such expenses, be recovered by the Central Board with interest (at such reasonable rate as the Central Government may, by order, fix) from the date when a demand for such expenses is made until it is paid from the person or persons concerned as arrears of land revenue or of public demand.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

27

4) For the removal of doubts, it is hereby declared that any direction to perform the functions of any State Board given under sub-section (2) in respect of any area would not preclude the State Board from performing such functions in any other area in the State or any of its other functions in that area.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

28

Environmental Legislation in India

• India is perhaps the first country to provide for the protection of environment its constitution. An extract of Article 51 (g) of the constitution reads as follows, “It shall be the duty of every citizen of India to protect and improve the natural environment including forests, lakes, rivers and wildlife and to have compassion for living creatures”

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

29

Environmental Legislation in India (Cont...)

• The law differs between the various states in India. The ministry does the planning, prompting, co-ordination and policy formulation at the national level. The executive responsibility rest with the Central and State Pollution Control Boards.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

30

The Environment (Protection) Act, 1986

• The Environment (Protection) Act, 1986, has important constitutional implications, with an international background. The Act clearly drew its inspiration from the proclamation adopted by the United Nations Conference on the Human Environment which took place at Stockholm from 5th to 16th June, 1972, in which the Indian delegation led by the then Premier of India took a leading role.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

31

The Environment (Protection) Act, 1986 (Cont....)

• This is an act, which provides for the protection and improvement of the environment. Rules were simultaneously made in 1986. This is a comprehensive act which covers air, water, land, human beings and living creatures, plants, micro organisms, property, and the interrelationship of all these. More specific provisions are included in the act. EPA 1986 is the direct result of Bhopal Tragedy in 1984. SPCB can only make the provisions (i.e. Rules, regulations, modifications, standards etc.) stricter under this act (EPA). Hence power to annul, modify or reduce is no longer applicable for EPA, rules, regulations, standards etc.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

32

Obligations

a)Comply with directions of PCB such as closure, prohibition, regulation, stoppage of operation, process, electric supply, water or any other service.

b)Control discharges or emissions of environmental pollutants as per prescribed standards.

c) Furnish information to concerned agencies, if above standards (b) not being met.

Allow entry to PCB personnel and access to documents, records, plant, equipment including facility to take samples of water, air, soil, other pollutants.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

33

Rules to regulate environmental pollution

1. The Central Government may, by notification in the Official Gazette, make rules in respect of all or any of the matters referred to in the section 3.

2. In particular, and without prejudice to the generality of the foregoing power, such rules may provide for all or any of the following matters namely:-

a) The standard of quality of air, water or soil for various areas and purposes;

b) The maximum allowable limit of concentration of various environmental pollutants (including noise) for different areas;

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

34

Rules to regulate environmental pollution (Cont...)

c) The procedures and safeguards for the handling of hazardous substances;

d) The prohibition and restrictions on the handling of hazardous substances in different areas;

e) The prohibition and restrictions on the location of industries and the carrying on of processes and operations in different areas;

f) The procedures and safeguards for the prevention of accidents which may cause environmental pollution and for providing for remedial measures for such accidents

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

35

Direction of Supreme Court

• The Supreme Court has issued direction to the concerned authorities to control and prevent and pollution of Ganga water at Kanpur, inter alia, being

a) prevention from waster gathered at the dairiesb)Enlargement of sewers and construction of sewers where

absentc)Provision for public latrines to avoid use of open landd)High courts should not ordinarily stay Criminal

proceedings in such matterse)Corpses of Half cremated bodies are not thrown in the

river

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

36

Direction of Supreme Court (Cont...)

f)New industries to get licensees only after making provision for treatment of effluents and immediate action against existing pollution industries.

g)Central Government to include environment as a subject in educational institutions.

h)People should be made aware of the environmental problems;

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

37

Brundtland Commission• General principles, rights and responsibilities for environment

protection and sustainable development adopted by the Brundtland Commission are as under:

1. Fundamental Human Right: All human beings have the fundamental right to an environment adequate for their health and well-being.

2. Inter-Generational and natural resources for the benefit of present and future generations.

3. Conservation and Sustainable Use: States shall maintain ecosystems and future and ecological processes essential for the functioning of the biosphere, shall preserve biological diversity, and shall observe the principal of optimum sustainable yield in the use of living natural resources and ecosystems.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

38

Brundtland Commission (Cont...)1. Environmental Standards and Monitoring: States shall establish adequate

environmental protection standards and monitor changes in and publish relevant data on environmental quality and resource use.

2. Prior Environmental Assessments: States shall make or require prior environmental assessments of proposed activities which may significantly affect the environment or use of a natural resource.

3. Prior Notification, Access, and Due Process: States shall inform in a timely manner all persons likely to be significantly affected by a planned activity and to grant them equal access and due process in administrative and judicial proceedings.

4. Sustainable Development and Assistance: States shall ensure that conservation is treated as an integral part of the planning and implementation of development activities and provide assistance to other states, especially to developing countries, in support of environmental protection and sustainable development.

5. General obligation to Co-operate: States shall co-operate in good faith with other States in implementing the preceding rights and obligations.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

39

Earth Summit• The United Nations Conference on Environment And

Development (UNCED), properly known as Earth Summit, was held in June 1992 at Rio de Janeiro wherein more than 150 governments participated. This was the larges UN conference ever held and it put the world on a path of sustainable development which aim at meeting the needs of the present without compromising the ability of future generations to meet their own needs. The Earth Summit was inspired and guided by a remarkable document of 1987, i.e., Brundtland report, The Earth Summit forced the people worldwide to re-think how their lives affect natural environment and resources and to confront a new what determines the surroundings in which they live.

RTI, MUMBAI - ENV. AUDITING DAY 2.1.1

40

Earth Summit (Cont...)• Some of the major achievements of Earth summit lie in the form of

following documents which it produced 1. The Rio Declaration on Environment and Development: A series of

principles defining the rights and responsibilities of States in this area.

2. Agenda 21: a comprehensive blue print for global action to affect the transition to sustainable management of development.

3. Forest Principles: a set of principles to support the sustainable management of forests worldwide.

4. Two legally binding conventions, i.e., the Convention on Climate Change and Convention on Biodiversity, which are aimed at preventing global climate change and the eradication of biologically diverse species. These conventions were signed by the

representatives of more than 150 countries.