Ross Template - Texas Christian University€¦ · PPT file · Web view · 2009-05-13Chapter 8 -...

14

Sources of Short- Term Financing Chapter 8

Transcript of Ross Template - Texas Christian University€¦ · PPT file · Web view · 2009-05-13Chapter 8 -...

Sources of Short-Term

Financing

Chapter 8

Chapter 8 - Outline

Sources of Short-Term FinancingTrade CreditNet Credit PositionBank Credit TerminologyTypes of Bank LoansCorporate and Foreign Borrowing

TerminologyAccounts Receivable Financing

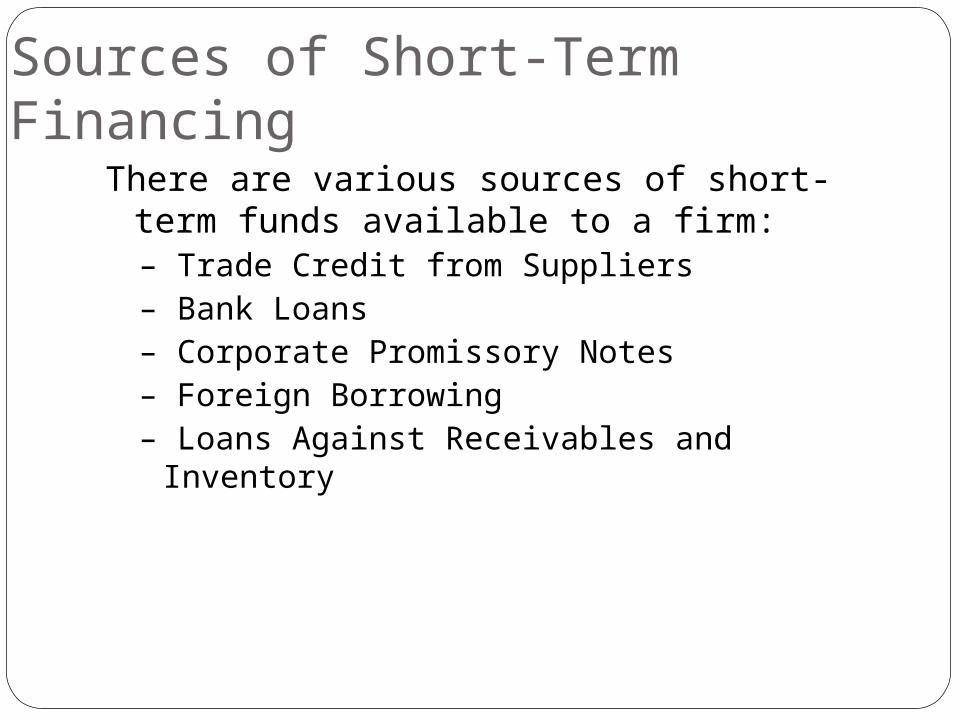

Sources of Short-Term FinancingThere are various sources of short-term

funds available to a firm:– Trade Credit from Suppliers– Bank Loans– Corporate Promissory Notes– Foreign Borrowing– Loans Against Receivables and Inventory

Trade CreditThe largest source of short-term financing for a firm.

Approximately 40 percent of short-term financing is in the form of accounts payable or trade creditAccounts payable

Is a Spontaneous source of funds Grows as the business expands Contracts when business declines

Extending the payment period to an unacceptable period results in:Alienate suppliers Diminished ratings with credit bureaus

It is usually a 30-60 day grace period before a bill is dueA cash discount is often given if payment is made within a

specified time– Ex., 2/10 net 30 means a 2% discount is given if paid in 10

days; if not, the full amount is due in 30 days

Net-Credit PositionDetermined by examining the difference

between accounts receivable and accounts payablePositive if accounts receivable is greater than

accounts payable and vice versa Larger firms tend to be net providers of trade

credit (relatively high receivables)Smaller firms in the relatively user position

(relatively high payables)

Cash Discount PolicyAllows reduction in price if payment is

made within a specified time periodExample: A 2/10, net 30 cash discount

means: Reduction of 2% if funds are remitted 10 days after

billingFailure to do so means full payment of amount by

the 30th day

Cost of NOT taking a discount:

Bank Credit TerminologyPrime Rate:

– the interest rate charged to a bank’s best customers– acts as a benchmark for calculating other interest

ratesCompensating Balance:

– when a bank requires a minimum average account balance for business customers in order to qualify for a loan

– can be thought of as a form of collateralEffective Interest Rate:

– the actual interest rate or “true” cost of a loan– also known as the annual percentage rate (APR)

Types of Bank LoansDiscounted Loan:

– when a bank deducts the interest on the loan in advance and lends the balance

Installment Loan:– calls for a series of equal payments over the

life of the loan– ex., most car loans and home mortgages

Compensating Balance Loan:– when a compensating balance is required as

part of the loan

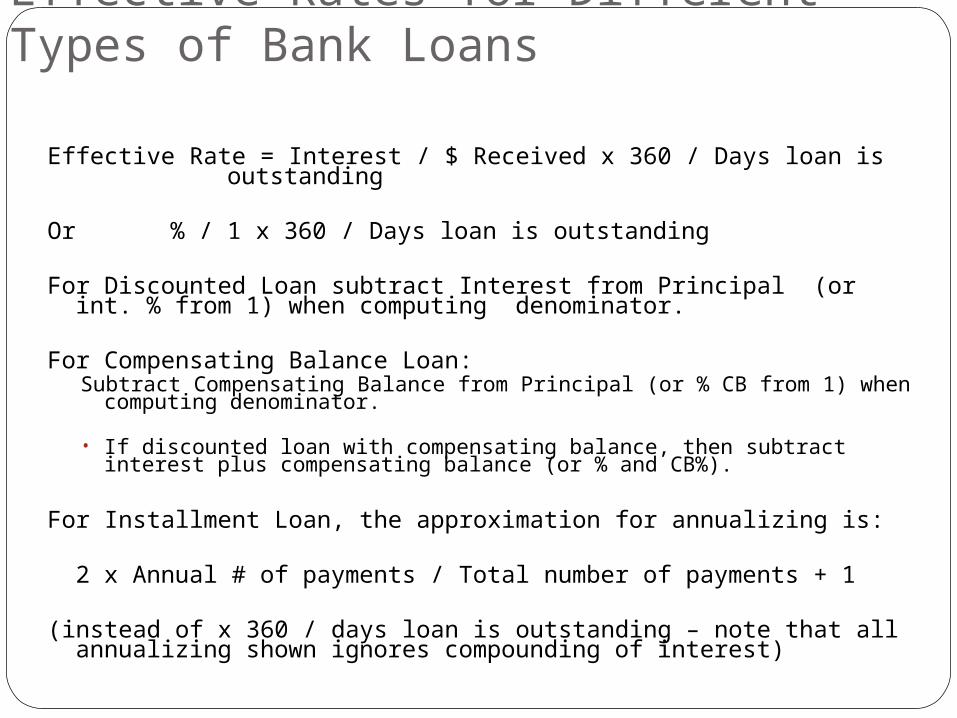

Effective Rates for Different Types of Bank Loans

Effective Rate = Interest / $ Received x 360 / Days loan is outstanding

Or % / 1 x 360 / Days loan is outstanding

For Discounted Loan subtract Interest from Principal (or int. % from 1) when computing denominator.

For Compensating Balance Loan:Subtract Compensating Balance from Principal (or % CB from 1) when computing denominator.• If discounted loan with compensating balance, then subtract interest plus compensating balance (or % and CB%).

For Installment Loan, the approximation for annualizing is:

2 x Annual # of payments / Total number of payments + 1

(instead of x 360 / days loan is outstanding – note that all annualizing shown ignores compounding of interest)

Corporate and Foreign Borrowing Terminology

Commercial Paper:– a short-term unsecured promissory note issued

to the public in minimum units of $25,000– total amount of commercial paper outstanding

has increased greatly in recent yearsEurodollar:

– a U.S. dollar held or deposited in a foreign bank– loans from foreign banks denominated in

American dollars are called Eurodollar loans

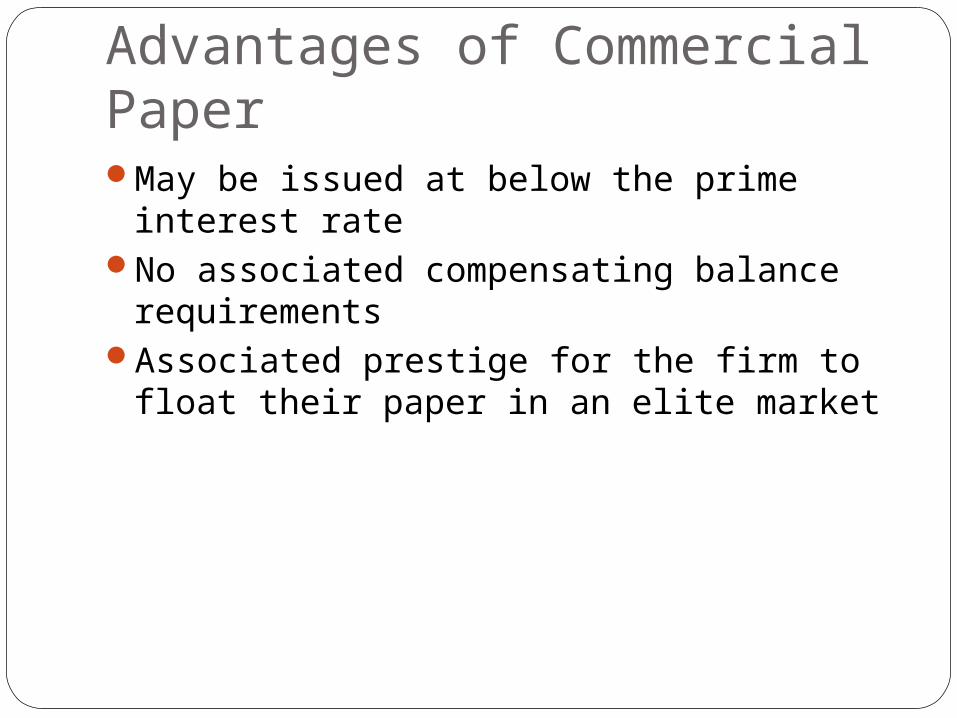

Advantages of Commercial PaperMay be issued at below the prime interest

rateNo associated compensating balance

requirements Associated prestige for the firm to float

their paper in an elite market

Disadvantages of Commercial Paper Many lenders have become risk-averse

post a multitude of bankruptcies Firms with downgraded credit rating do

not have access to this market The funds generation associated with this

is less predictable Lacks the degree of commitment and

loyalty associated with bank loans

Accounts Receivable FinancingA/R financing includes 2 choices:

– pledging accounts receivable as collateral for a loan

OR– an outright sale (also called factoring) of

receivables to a bank or finance companyTends to be a relatively expensive source

of financing

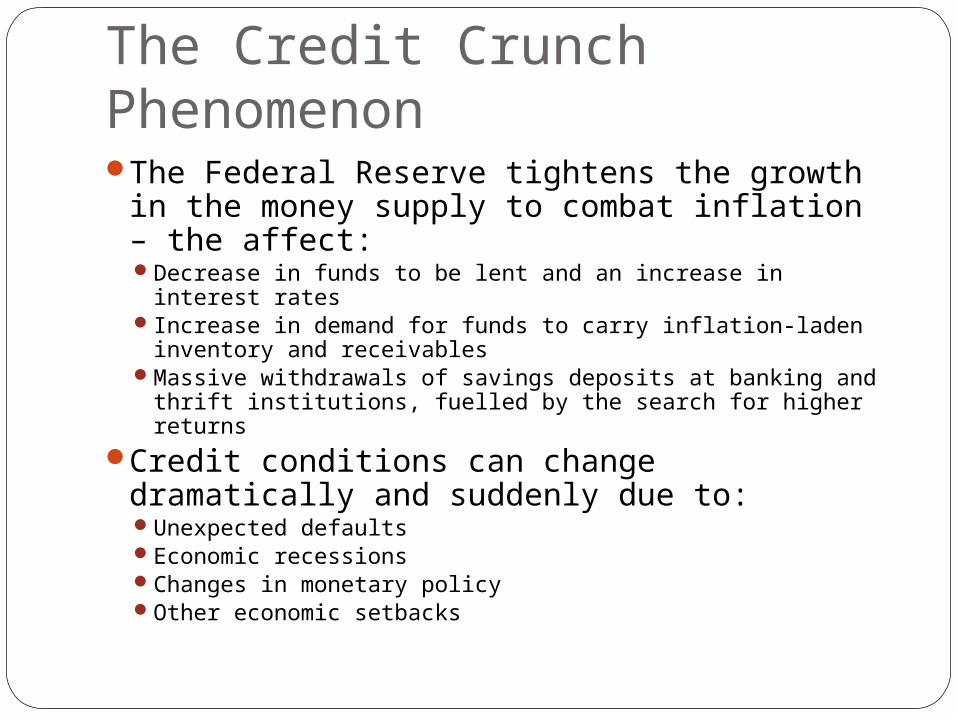

The Credit Crunch PhenomenonThe Federal Reserve tightens the growth in

the money supply to combat inflation – the affect: Decrease in funds to be lent and an increase in interest ratesIncrease in demand for funds to carry inflation-laden

inventory and receivablesMassive withdrawals of savings deposits at banking and thrift

institutions, fuelled by the search for higher returnsCredit conditions can change dramatically

and suddenly due to:Unexpected defaultsEconomic recessionsChanges in monetary policyOther economic setbacks

![Earnings Report · 2017-11-08 · Short -term liabilities [Loans and borrowings, accounts receivables, wages, taxes to be paid, etc.] Short-term loans and borrowing increased 5.1%](https://static.fdocuments.us/doc/165x107/5ed018f5e537c63ba210a78d/earnings-report-2017-11-08-short-term-liabilities-loans-and-borrowings-accounts.jpg)