Ross Stores, Inc. - Texas Tech...

162

Ross Stores, Inc. Equity Valuation Report Michael Moss [email protected] Dee Foster [email protected] Alex Hart [email protected] Neil Merkling [email protected] Garrett Harless [email protected] Emily Dale [email protected]

Transcript of Ross Stores, Inc. - Texas Tech...

Ross Stores, Inc.

Equity Valuation Report

Michael Moss [email protected] Dee Foster [email protected] Alex Hart [email protected] Neil Merkling [email protected] Garrett Harless [email protected] Emily Dale [email protected]

2

Table of Contents

Executive Summary 5

Business and Industry Analysis 12

Company Overview 12

Industry Overview 13

Five Forces Model 14

Rivalry Among Existing Firms 14

Threat of New Entrants 19

Threat of Substitute Products 22

Bargaining Power of Buyers 23

Bargaining Power of Suppliers 25

Analysis of Key Success Factors 27

Firm Competitive Advantage Analysis 32

Tight Cost Control System 32

Differentiation 35

Accounting Analysis 36

Key Accounting Policies 38

Operating and Capital Lease Disclosure 38

Company Growth Statistics 39

Purchasing, Merchandise, and Inventory 39

Goodwill and Hedging 40

Potential Accounting Flexibility 41

3

Actual Accounting Strategy 44

Qualitative Analysis of Disclosure 45

Quantitative Analysis 48

Core Sales Manipulation Diagnostics 48

Expense Manipulation Diagnostics 54

Identifying Potential “Red Flags” 55

Analysis of Investment Activities 56

Undoing Accounting Distortions 58

Financial Analysis, Forecast Financials, and Cost of Capital 60

Financial Ratio Analysis 61

Liquidity Ratios 61

Profitability Ratios 69

Capital Structure Analysis 76

Altman Z-Score 79

Internal and Sustainable Growth Rate Analysis 80

Financial Forecast Analysis 82

Forecasted Income Statement 83

Forecasted Balance Sheet 84

Forecasted Statement of Cash Flows 87

Weighted Average Cost of Capital 89

Cost of Equity 89

Cost of Debt 92

Weighted Average Cost of Capital 93

4

Financial Valuations 93

Method of Comparables 93

Intrinsic Valuations 98

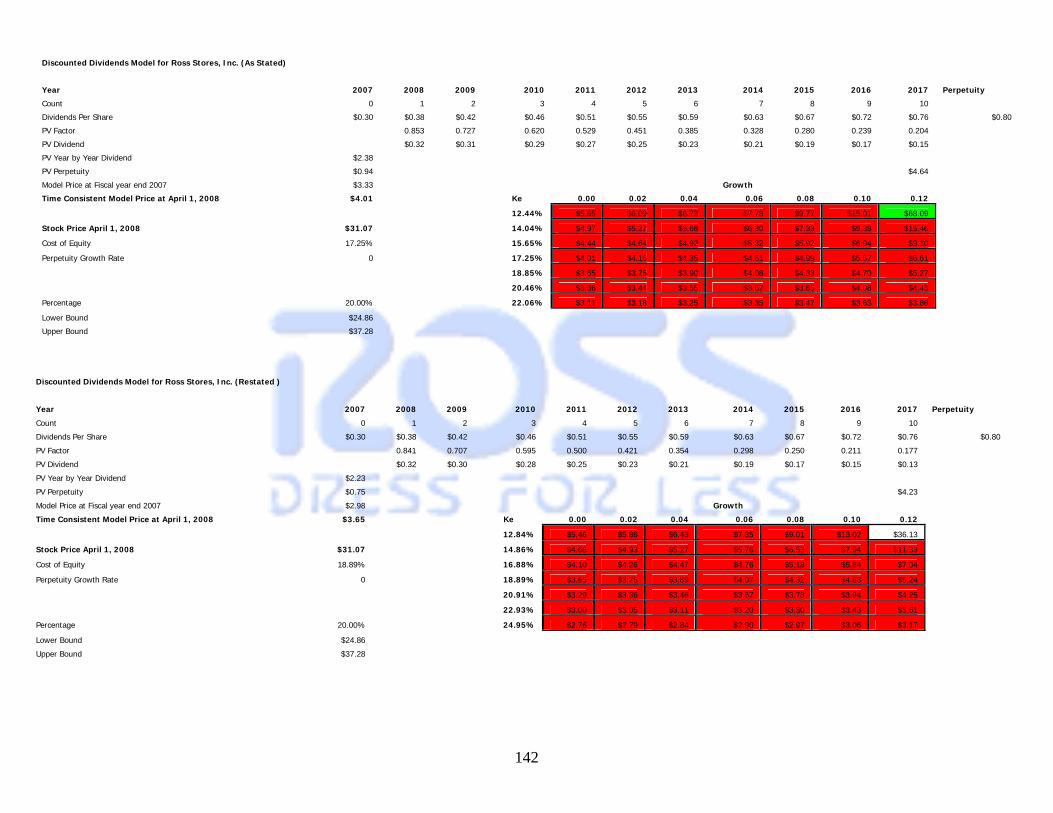

Discounted Dividend Model 99

Discounted Free Cash Flows Model 101

Residual Income Model 103

Abnormal Earnings Growth Model 105

Long Run Residual Income Perpetuity Model 106

Analyst Recommendation 109

Appendix 111

Ross Financial Statements as Stated 112

Ross Financial Statements Restated 116

Kohl’s Financial Statements 120

T.J. Maxx Financial Statements 123

J.C. Penney Financial Statements 126

Manipulation Diagnostics 129

Lease Capitalization 132

Financial Ratios 134

Altman Z-Scores 141

Intrinsic Valuations 142

Regressions 149

Reference 162

5

Executive Summary

Investment Recommendation: Overvalued, Sell April 1, 2008

ROST - NASDAQ (04/01/2008) $31.07 Altman Z-Scores 52 week range $21.23 - $34.69 2002 2003 2004 2005 2006 2007 Revenue $5.57 B As Stated 7.27 6.08 6.25 5.76 5.85 5.26 Market Capitalization $4.32 B Restated 3.66 3.36 3.45 3.44 3.55 3.31 Shares Outstanding 139.02 M Percentage Institutional Ownership 97.30% Market Price 04/01/2008 $31.07 As Stated Restated Financial Based Estimated Valuations As Stated Restated Book Value per Share $6.54 $6.54 P/E (Trailing) $24.59 $29.70 Return on Equity 28.90% 34.86% P/E (Forecasted) $24.85 $31.82 Return on Assets 12.46% 9.13% P/B $15.42 $15.42 D/P $19.47 $19.47 Cost of Capital P.E.G. $17.27 $23.75 Estimated R-square Beta Ke EV/EBITDA $31.26 $52.59 3-month 0.1067 0.7395 7.20% EV/FCF $42.86 $77.74 1-year 0.1071 0.7408 7.14% 2-year 0.1068 0.7395 7.00% Intrinsic Valuations As Stated Restated 5-year 0.1058 0.7356 7.78% Discounted Dividends $4.01 $3.65 10-year 0.1049 0.7325 8.72% Free Cash Flows $38.73 $65.20 Residual Income $10.00 $10.19 As Stated Restated AEG $8.55 $8.16 Ke Based on Long-Run Residual Income 17.25% 18.89% Long Run Residual Income $22.26 $24.80 Published Beta 0.04 Cost of Debt 5.94% 5.91% WACC (BT) 14.17% 13.41% WACC (AT) 13.54% 12.44%

http://moneycentral.msn.com

6

Industry Analysis

Ross Stores Inc. started out as a junior retail store in the small California

town of San Bruno in 1957. The business remained relatively unchanged for

over 25 years until it was bought out by a group of investors in 1982. These

investors, lead by Stuart Moldaw and Don Rowlett, created a discount retail giant

out of a few junior retail stores. They were able to do this by saturating the

west coast market with discount retail stores before its competitors.

In the discount retail industry there is high rivalry among firms, high

threat of substitute products, and high bargaining power of buyers. These three

factors would imply that it is a commodity industry. Due to economies of scale

there is also low threat of new entrants. Suppliers have low bargaining power

due to the nature of the firms’ buying strategies. The standard industry practice

is to buy off-season merchandise, factory overruns, and overstocked

merchandise. They then place these purchases into storage until the next

appropriate selling season.

We have concluded that Ross’ main competitors are T.J. Maxx, Kohl’s, and

J.C. Penney. These companies operate similarly to Ross in their buying

strategies and asset management. They also all target consumers looking for

fashionable clothing at affordable prices. Therefore, companies in this industry

compete on product selection and cost.

In order to remain viable in the industry, firms must maintain low input

costs, tight cost control system, cost leadership, and economies of scale. Firms’

input cost can be controlled through their buying strategy. Tight cost control

systems are implemented using technology and minimal waste. This allows the

firms to compete on cost. Economies of scale translate into volume purchasing

and mass merchandising of goods. This requires a large number of stores and a

solid distribution network, making it difficult to enter the discount retail industry.

7

These are the key success factors that must be met in order to succeed in the

discount retail industry.

Accounting Analysis

When valuing a firm, it is important to look closely at the firm’s financial

statements. In order to provide an accurate valuation, it is necessary to question

the accuracy of these statements. Though the SEC regulates the level of

disclosure that firms must provide through GAAP, it is preferable that a firm

discloses more information than the required amount. GAAP also allows a fair

amount of flexibility when it comes to making key accounting practice decisions.

This often can lead to managers manipulating financial statement data to paint a

better picture of the company. It is necessary to identify any manipulations that

may be taking place and evaluate their impact on the financials.

We determined that Ross has a high level of disclosure in their

statements. They provide detailed information on the use of operating leases,

purchasing and inventory practices, and goodwill and other long-term assets.

Ross also disclosed their investment activities in detail. Because of this high level

of disclosure, we were able to easily determine their key accounting policies.

The only policy that had any significant effect on the appearance of the

financials was Ross’ decision to use operating leases for their stores. By using

operating leases instead of capital leases, Ross avoided recording a substantial

amount of liabilities and assets. We found it necessary to capitalize the leases to

see the effect it would have on the balance sheet. The result was significant

enough that we decided to restate all of Ross’s financial statements in order to

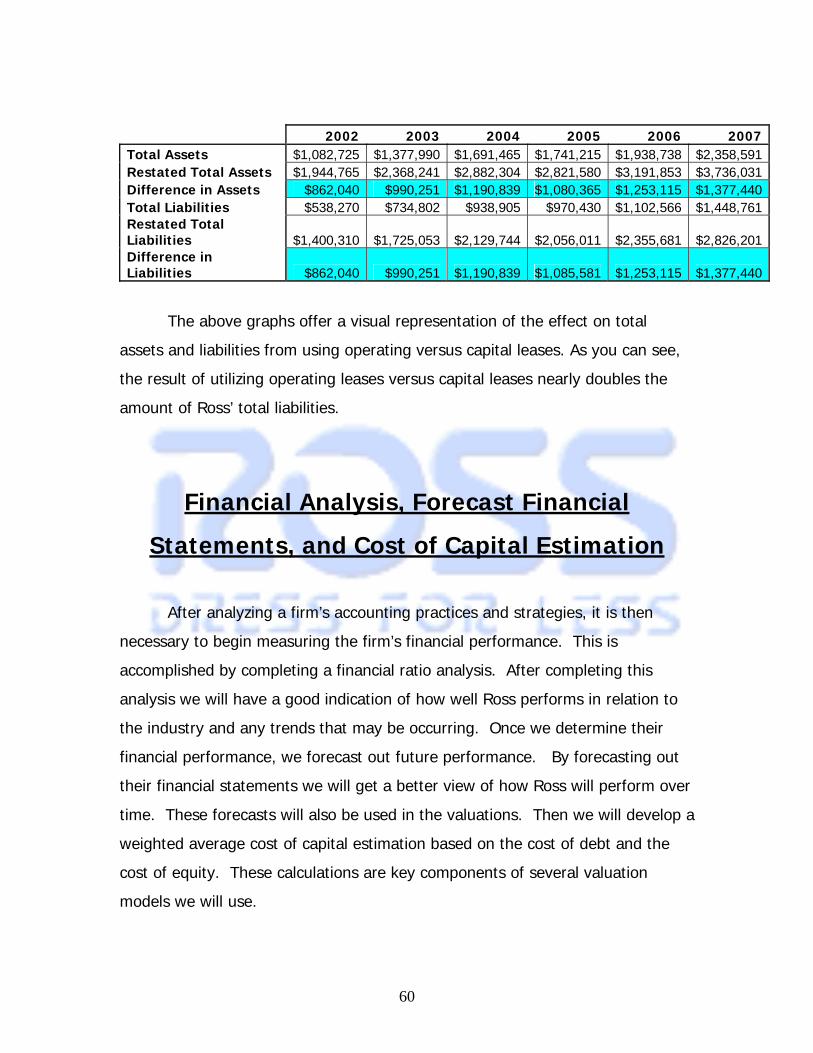

ensure we had an accurate picture of Ross. Because of the capitalization of the

leases, Ross’s assets and liabilities in 2007 increased from $2.3 billion to $3.7

billion. This means that Ross avoided recording over $1.37 billion in assets and

8

liabilities. These restatements proved to be crucial to our forecasts and

valuations.

In order to detect manipulation in the sales and core expenses, we

performed several diagnostics. These diagnostics are designed to discover

abnormal changes in key expense ratios. As certain elements change, the results

can cause us to question the validity of the financial information presented by

the company. During our review of these diagnostics we did not find any

abnormal or unusual results.

Financial Analysis, Forecast Financials, & Cost of

Capital Estimation

When looking at a firm and attempting to perform a financial analysis,

there are three areas that need to be evaluated. Each one contains its own set of

ratios in order to perform this task. These ratios are categorized into liquidity,

profitability, and capital structure. Each of these gives a better understanding of

how the company works. Also, it is necessary to use past and current data in

order to forecast out the firm’s financial statements and gain an idea of how the

company may perform in the future. Lastly, a regression model must be created

in order to configure a Beta, cost of debt, cost of equity, and a weighted average

of the cost of capital so that we may use these key components in valuation

models later on.

After calculating all of the liquidity ratios, we found that Ross is a little less

liquid than other firms in the industry. This means that Ross is less able to

convert current assets into cash than its competitors. For example, Ross’ six-

year average current ratio was 1.49 in comparison to an industry average of

1.86. Also, Ross’ performance is not in keeping with the industry average when

9

it comes to inventory turnover. The industry average was 4.23, and Ross was

3.80. In regards to Ross’ profitability, they are doing a good job keeping up with

the industry average. In most cases Ross’ ratios were either at or above the

industry average. However, in comparing Ross’ ratios with the restated

financials, some of the results differed from the original ones. As for evaluating

their capital structure, we found that Ross is primarily financed through debt

rather than equity. This is likely due to the fact that Ross has a lower cost of

debt than cost of equity.

We then, with the aid of the financial ratios, were able to forecast

Ross’ financial statements ten years out. We did this by analyzing past data as a

benchmark to determine any trends in growth. In order to do this, we needed to

establish an average growth rate for Ross. We used the average sales growth

over the past three years, and our knowledge of current economic events, to

determine the growth rate to be 10.26%. We then used different ratios to link

all of the financial statements together based on this sales growth figure. We

were then able to forecast all of the important line items for all of the financial

statements. These forecasts would be used to help us predict future business

performance, and were also used in performing certain valuation models.

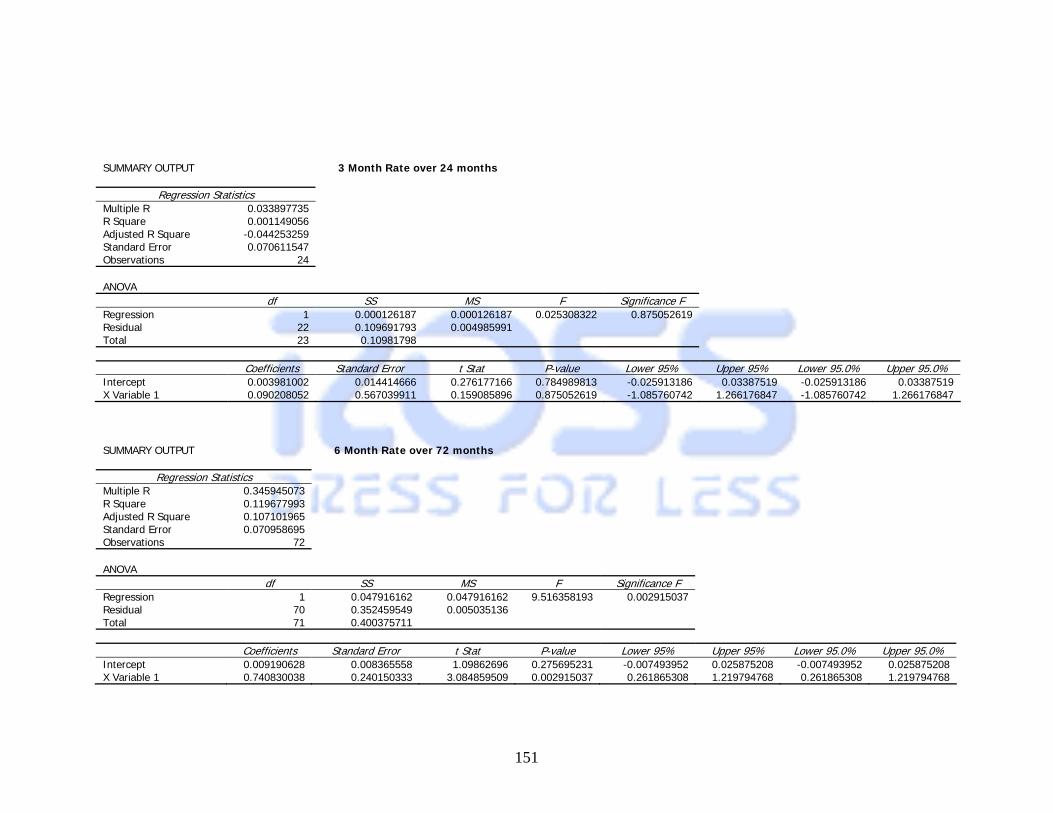

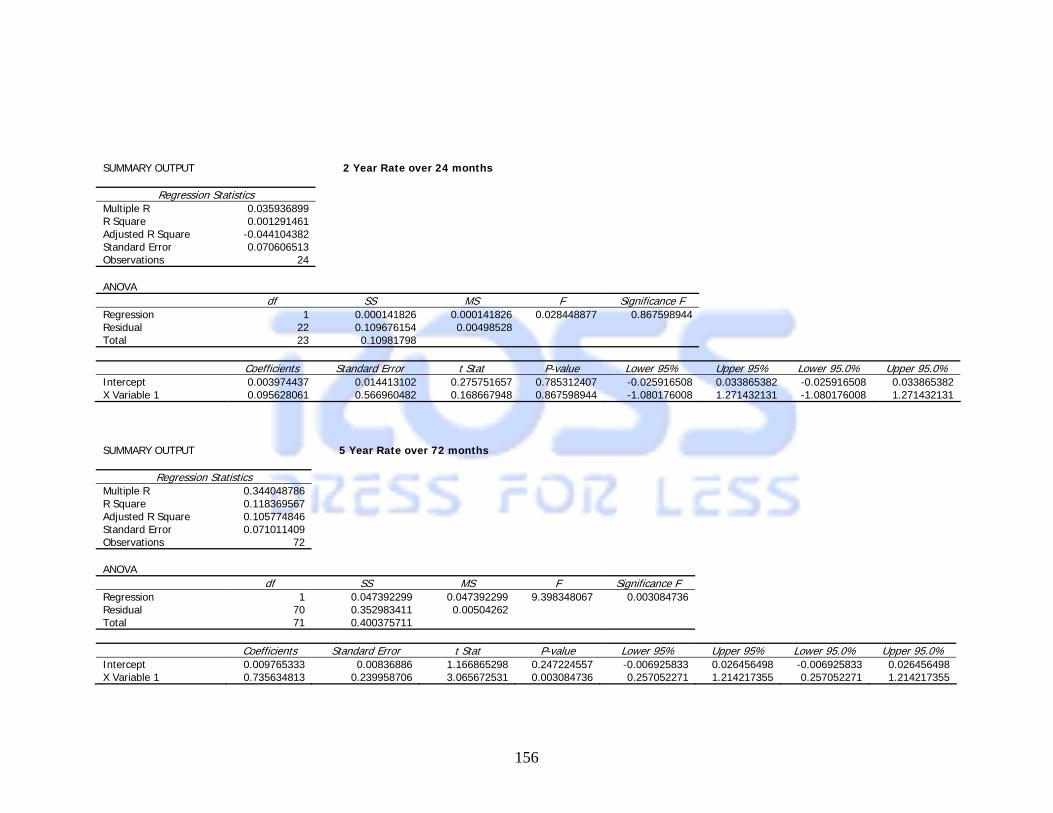

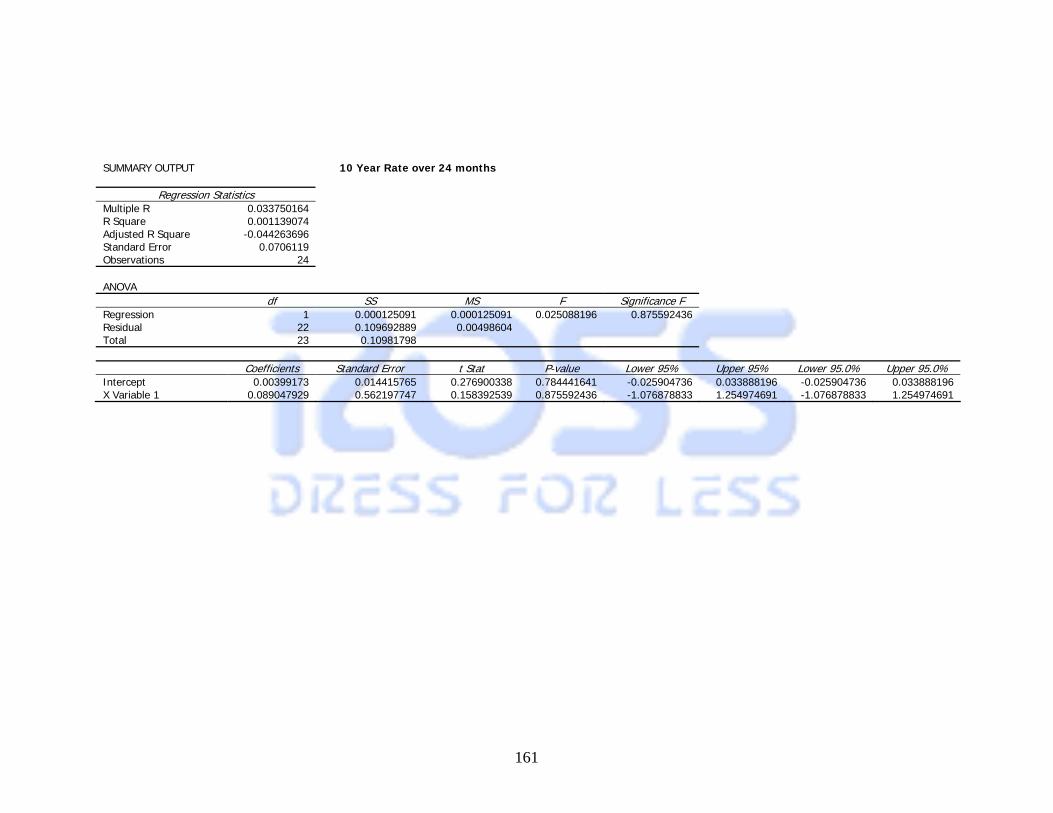

As far as our cost of capital analysis, we first used the CAPM model to find

the cost of equity. After running several regressions, we soon found that the

explanatory power was too insufficient to provide an accurate beta for Ross.

Instead, we were forced to use the long run residual income perpetuity model to

find the cost of equity. Using this model we found it to be 17.25% as stated and

18.89% restated. Cost of debt was fairly simple to calculate since they had only

a few liability accounts and few interest rates involved. We calculated Ross’ cost

of debt to be 5.94% as stated and 5.91% restated. We then used the cost of

equity and the cost of debt to calculate the weighted average cost of capital to

be 13.54% as stated and 12.44% restated.

10

Valuations

The valuations are the capstone of the entire analysis. At this point in the

process, we have all of the information needed to begin. We valued Ross two

ways; we used the method of comparables and we used intrinsic models.

The first type of valuation uses simple ratios; this is called the method of

comparables. The method of comparables is a popular way to value companies

because it is easy to understand and explain to investors. There are six ratios

that are generally used in valuing the company. These include: P/E trailing and

forecasted, P.E.G., P/B, P/EBITDA, EV/EBITDA, and P/FCF. Utilizing the method

of comparables, most ratios indicated that we were overvalued. When we

computed Ross’ EV/EBITDA we came up with $31.26; this closely mirrors the

published stock price as of April 1, 2008. This is probably due to the fact that

EV/EBITDA has become the new standard in comparables valuations. Although

easy to compute and understand, there is no financial theory backing the

method of comparables.

Intrinsic models are preferred by financial analysts because they are

backed by financial theory. The intrinsic models used were: the discounted

dividend model, discounted free cash flows, residual income, abnormal earnings

growth, long run residual income. We ran sensitivity analysis on each model to

determine the sensitivity to variables such as cost of equity, weighted average

cost of capital, return on equity, and growth rates. Through this analysis it

became apparent that the DFCF model is unreliable because of its extreme

sensitivity to variable changes. The dividend discount model is also unreliable

due to its heavy reliance on the perpetuity growth rate. This model is generally

inapplicable because investors can never recoup their initial investment from

dividends.

The abnormal earnings growth model, residual income model, and long

run residual income model are more reliable models. These models take into

11

account more factors which allows for a more complete valuation of the firm.

When we ran a sensitivity analysis on the residual income model, long run

residual income, and abnormal earnings growth model we found that all models

are very sensitive to the cost of equity. This shows that the models rely more on

forecasted information than the perpetuity because growth rates cause minimal

changes.

We found Ross to be overvalued in four of the five models and therefore

conclude that it is overvalued. The only model that differs from this is the

discounted free cash flows model, which we disregard due to the extreme range

of values that it returned.

12

Business and Industry Analysis

Company Overview

Ross Stores, Inc. (ROST) first opened its doors to the people of California

in 1957 as a junior’s specialty retailer. The company continued its business as a

junior’s specialty retailer until August of 1982 when two investors, Stuart Moldaw

and Donald Rowlett, gained control of the company and began to shape the

company into its current form.

These two men had plenty of experience in the off-price retail industry

and put that experience to work. They realized that the discount retail industry

had yet to pioneer the West, and decided the market for discount clothing was

there. They took advantage of the lack of competition by first adding men and

women’s clothing to the store and selling them at discount prices. They decided

soon to expand quickly into other cities and opened 20 stores within the first two

years of ownership, expanding the Ross company more than threefold. This

rapid expansion was intended to saturate the market and make it difficult for

competitors to in enter the market.

This extraordinary growth has continued for more than 20 years, and

Ross Stores, Inc. is now the nation’s second largest discount retailer next to the

TJX Companies, Inc. Ross Stores, Inc. now does business in 771 Ross Dress for

Less stores across 27 states and Guam. The company also runs 26 dd’s

Discounts stores spread out over the state of California. However, Ross

maintains a market cap of approximately $4.32 billion, which is relatively small,

compared to its competitors.

Ross Stores, Inc. competitors include TJX Companies, Inc., Kohl’s, and

J.C. Penney. These three competitors are the biggest competitors to Ross

Stores, Inc.

13

Ross Stores, Inc. stock price has been indicative of how well the company

has done for that specific year. They have kept their commitment to maintain

competitive prices and continue company growth. The total assets as well as the

net sales are constantly increasing from year to year. This is important because

it proves that Ross’s strong growth is good news for stockholders.

Industry Overview

Ross Stores, Inc. is currently operating in the off-price retail apparel

industry with its main competitors being T.J. Maxx, Kohl’s, and J. C. Penney.

The off-price retail apparel industry is a highly competitive industry but does

allow all companies to have increases in net sales. The way this is possible is by

companies buying low, and selling low. This is possible because every company

in the industry has several stores and warehousing to store inventory goods.

Industry leaders benefit from trouble in high-end retail industries by capitalizing

on inventory liquidity. (WSJ.com: TJX, Ross benefit from other retailer

downturns)

Each company in the industry competes in six different submarkets.

These submarkets are ladies’ apparel, men’s apparel, fine jewelry accessories

lingerie and fragrances, shoes, and children’s clothing. The sales of these goods

directly determine the net sales for the companies. This allows companies to

decide what to compete in.

14

Five Forces Model

The five forces model is a model that helps to define and classify an

industry. The model helps to identify who the players are in a given industry, as

well as, the overall size and condition of the industry. The model is divided into

two broad sections: Actual and Potential Competition and the Bargaining Power

of Buyers and Sellers. These broad categories give a picture of the macro view

of an industry. These broad categories are then broken down into smaller

categories. The sub-categories for the competition category are Rivalry Among

Existing Firms, Threat of New Entrants, and Threat of Substitute Products.

Bargaining Power is divided into buyer’s bargaining power and supplier’s

bargaining power. Analysts can use the information contained in the five forces

model to determine the potential profitability of an industry and/or a particular

firm within the industry.

Ross Stores, Inc.

Rivalry Among Existing Firms High

Threat of New Entrants Low

Threat of Substitute Products High

Bargaining Power of Buyers High

Bargaining Power of Suppliers Low

Rivalry Among Existing Firms

Rivalry among existing firms is very useful for determining what kind of

profits are possible in a given industry or sector of an industry. Firms compete

against other firms in an industry for the same consumers’ dollars. There are

15

two basic ways that firms compete: price and differentiation. The degree of

rivalry and type of product or service that is being sold will determine the

strategy that firms pursue. The degree of rivalry for Ross in the retail apparel

industry is very high. The sector that includes Ross, Kohl’s, T.J. Maxx and J.C.

Penney competes on price.

Industry Growth

Industry growth is an important measure of how firms are doing as a

whole. The most recent five years of data provide an indication of trends and

cycles within the industry. They also give an indication of the industry’s potential

for future growth. Growth is also an indicator of how a firm will compete. Firms

have to fiercely compete for other firms’ existing customers in a stale growth

environment. Conversely, there will be plenty of new customers to increase an

individual firm’s market share in a high growth situation. The retail apparel and

home accents industry is a highly competitive and segmented industry and relies

heavily on the middle class as its primary customers. The off-price retail industry

is a very competitive segment of the overall retail environment. Discount retailers

do better as other department stores do worse (WSJ.com, Lookahead:Retail

Check-up). There are well-established firms that have been controlling and

In d u s try G ro w th R a te

-5 0 .0 0 %

-4 0 .0 0 %

-3 0 .0 0 %

-2 0 .0 0 %

-1 0 .0 0 %

0 .0 0 %

1 0 .0 0 %

2 0 .0 0 %

3 0 .0 0 %

2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6

Y e a r

R o s sK o h l'sT .J . M a x xJ .C . P e n n yIn d u s try

c

16

growing majority market share for years. As seen in the preceding graph, the

industry itself is not a very quickly growing entity. Its sales growth ratio for the

past five years has remained fairly level. Ross’ sales growth ratio trends have

remained in keeping with that of the industry.

Concentration

Relative Market Share

8%

21%

27%

44%Ross Stores, Inc

Kohl's Corporation

T.J. Maxx

J.C. Penney

Industry concentration refers to the number of firms in an industry. An

industry may have thousands of small firms or only a few large ones. It also

defines the relative size of firms to others in the industry and the proportion of

market share they hold in the industry as a whole.

The off-price retail industry is one of medium-low concentration. The

number of firms within the industry is somewhat limited; however, sufficient

competitive pressures exist to limit any one firm’s ability to earn extraordinary

gains. The main players in the industry are J.C. Penney (JCP), Kohl’s (KSS), Ross

(ROST), and T.J. Maxx (TJX). Each firm within the industry is competing for

17

essentially the same resources. These resources include employees, product,

store space, and customers. The firms with greater resources are able to

compete more aggressively for these assets, which can lead to competitive

advantages for them.

In the off-price retail industry, there are a few large firms controlling the

market share, as shown in the preceding graph. J.C. Penney controls the

greatest percentage of the industry at 44 percent, whereas Ross commands the

least amount at eight percent. In this aspect, Ross is at somewhat of a

disadvantage in that it has fewer resources with which to compete against such

strong competitors as J.C. Penney and T.J. Maxx.

Differentiation

The term differentiation refers to how similar or dissimilar competing

firm’s products are when compared to each other. If two firms have very similar

products, then they are extremely likely to engage in competition based on price.

Firms with more differentiated products are able to compete on other factors

such as style or features. There are varying levels of differentiation within the

retail apparel industry. Typically, price is the largest indicator of the level of

differentiation for a particular retailer’s products. Higher quality and more elite

brands will typically carry a higher price. The off-price retail apparel industry

sells national and recognizable name brands at heavily discounted prices. In this

way, these firms differentiate themselves from mass merchandisers such as Wal-

Mart or K Mart, but not to the same extent as firms like Nordstrom’s. Off-price

retailers are, however, very price competitive among themselves.

Switching Costs

Switching costs are the cost of buying from one firm versus another.

Firms within the off-price retail industry compete mainly on the basis of price.

With many of the firms within the industry offering identical and/or similar

products, customers have a high propensity to follow the price leader. Switching

18

costs are minimal for customers and therefore are of great concern to firms.

Switching costs for firms are different from that of customers. For instance, if

firm A and firm B offer similar quality products, a customer can buy from either

based solely on price. With firms in the off-price retail industry offering similar or

identical product mixes, there are very few switching costs for customers.

Economies of Scale

The term, economies of scale, refers to factors mainly involving the size of

operations. In an industry where economies of scale are of great importance,

the size of a firm can be vital to its survival. High volumes in purchases and

capital investments can give a firm a more profitable operation. Economies of

scale are of strategic importance to firms within this industry. Firms with the

resources to purchase in mass quantities have a distinct advantage over those

who cannot. It is imperative that firms have the ability to offer large quantities

of high quality goods at the lowest possible prices. Additionally, firms must have

the space to offer large amounts of product for sale and also store the products

they purchased.

In the off-price retail industry, each firm uses large scale centralized

distributing centers to supply a minimum of 750 stores. Ross is at the lower end

with 771 stores, while J.C. Penney leads the industry with 1073 locations. Ross’

other two main competitors, T.J. Maxx and Kohl’s, each have 800 and 930

stores, respectively. Such even numbers create a fairly level space distribution

physically amongst the firms in this industry, establishing an industry where

obtaining economy of scale is vital to a firm’s sustainability.

Excess Capacity

Excess capacity in an industry is basically when the supply of goods or

services is higher than the demand for those goods or services. When this

situation occurs, firms are inclined to cut prices to dump excess capacity

(product). Higher priced products do them no good setting on the shelves.

19

Firms within the retail industry must carefully plan and execute purchase and

sales plans. If not, a problem of excess capacity will arise. When firms within

the retail apparel industry experience excess capacity, price competition shortly

follows. A very intense and/or lengthy price war can lead to damaging results

for a firm and industry. Intense price competition can lead to pricing below

marginal costs.

Exit Barriers

Exit barriers are essentially the costs and/or legal problems

associated with a firm’s exiting an industry. Firms that have specialized assets

will have an especially hard time exiting an industry because of the difficulty in

liquidating their assets. The retail industry has little specialized equipment or

legal barriers to leaving the industry, making the exit barriers very low.

Conclusion

The industry has experienced respectable growth over the past five years

making it an attractive market. However, there are currently a large number of

competitors with little differentiation between firms making it very hard to stand

out amongst the crowd. In order to achieve the necessary economies of scale,

companies have to work hard to acquire resources before their competitors do.

Combined with the low switching costs for consumers, firms become highly

competitive amongst themselves in order to make a profit.

Threat of New Entrants

The threat of new entrants refers to the ability for a new firm to enter the

existing market. The overall profitability is largely determined by how easily new

firms can enter the arena. Large profits within an industry will be attractive to

new firms; therefore existing firms in the market will lower their pricing and

reduce their profits in order to discourage new entrants. Due to the large

20

economies of scale needed and the presence of large established companies, the

threat of new entrants is low.

Economies of Scale

For new entrants, the economy of scale refers to how much capital

resources they need in order to make a profit and be competitive in the industry.

The off-price retail sector requires a company to have a large amount of

inventory and a wide product mix. This means that it needs a great deal of initial

investment money in order to buy beginning inventory. Profit margins are slim,

averaging about 7% of sales. In order to make the business profitable, large

amounts of sales are needed. Additionally, the common business tactic in off-

price retail of buying products at a discount at the end of the season and storing

them until the next year requires large warehousing capabilities in order to be

effective.

In order to successfully enter the industry, new entrants need a large

amount of capital to achieve the necessary economies of scale. This makes it

very hard for new firms to enter the market. In the following table, we

document the number of stores that each firm had at the end of that year.

Considering the large number of stores needed, it would take a significant

amount of capital to be able to enter into the industry.

Number of Stores at Year End 2002 2003 2004 2005 2006Ross Stores 507 586 649 734 797Kohl's 457 542 637 732 817T.J. Maxx 713 745 771 799 821J.C. Penney 1043 1020 1017 1019 1033

21

First Mover Advantage

Traditionally, the first firm to enter a market has a great advantage over

any future competitor. First entrants can buy up vital resources and establish

exclusive relationships with key suppliers, making it harder for followers to set up

shop. Prime locations can be acquired without intense competition from related

firms. Name recognition is another advantage of the first mover. Typically,

consumers associate an industry with the first firm to establish itself within that

industry. The off-price retail industry already has several existing well-established

firms, such as Ross, J.C. Penney, Kohl’s and T.J. Maxx. Therefore, new entrants

will have a hard time gaining name recognition among consumers in the face of

existing competition.

Access to Channels of Distribution and Relationships

In the retail industry, the channels of distribution refer to the suppliers

and how a company gets its merchandise to the store. Established relationships

along with the high costs of creating new distribution channels present a

formidable barrier to new entrants. To be competitive, off-price retailers need a

large number of suppliers and have to spend resources in order to find and

maintain relationships with these suppliers. Ross has four centralized distribution

centers with which they supply all stores. There they use third party cross docks

to distribute merchandise that is then delivered to stores through contracted

vendors.

Legal Barrier

The legal barriers to entering an industry are the licensing fees,

regulations, copyrights, patents, and other government regulated requirements

for operating a business. For the retail industry, these are mostly licensing and

registration fees. There are minimal legal barriers to entry for the retail industry.

22

Conclusion

The threat of new entrants into the off-price retail industry is low.

Economies of scale are necessary for survival in this industry, and it is very

challenging for a new firm to achieve the amount of initial investment money

needed to enter this segment successfully. Also, prospective entrants are at a

disadvantage because this industry already has several existing, well-established

firms and would face great difficulty in pulling market share away from them.

Finally, a fledgling company would not easily be able to set up distribution

channels because of the strong relationships between existing suppliers and

firms.

Threat of Substitute Products

It is important to understand that, in many cases there are products or

services that serve the same purpose and are of similar quality and value. This

situation creates the possibility that consumers will choose a substitute product

over a product being offered by a competitor. In the off-price retail apparel

industry, there are not very many direct substitutes for clothing. However,

abundant substitution opportunities exist within the clothing market for

consumers to choose from. Many firms also carry the exact same name brand

clothing lines. This leads to a high threat of substitution. Customers will

purchase from the cost leader, given identical or similar products. Ross and its

competitors offer similar, if not identical, name brands and product mixes.

Therefore, the danger of substitute products is high within the industry.

23

Bargaining Power of Buyers

Buyers have power over the retail apparel industry to the degree that they

can affect changes in price. How they exercise this power and their reasons for

doing so influences, to a great extent, the business strategy of a company. When

buyers have a high degree of power they can demand and reasonably expect low

prices and a wide range of benefits from a company. Conversely, a low degree of

power on the buyer’s side gives the company more flexibility in pricing and what

they are willing to offer.

During strong economic growth, retailers’ bargaining power rises as

buyers are less likely to purchase based on price and are more willing to buy

entertainment items. That shifts the balance of power to the retailers favor.

Currently, the retail market is entering into a recession, with January sales being

the worst recorded (WSJ.com, Retailers' Sales Results for January Could Be

Worst Since 1969). Consumers are becoming more conservative in their

purchases. As a result, retailers have to lower prices and offer more concessions

in order to attract customers. Consequently the buyer’s power has risen.

Price Sensitivity

Price sensitivity refers to how much effort the average consumer is willing

to exert in order to find the price they are willing to pay. This effort can be either

through price comparison, bargaining, or simply waiting for a sale or discount.

When consumers in an industry are highly price sensitive, companies compete on

a cost-leader basis. This places a greater emphasis on finding cheap suppliers,

low overhead costs, and efficient distribution chains. The combined costs-of-

goods sold and operating expenses averages 90% of sales for this sector of the

retail apparel industry. With such a narrow profit margin, companies are

dependent on attracting a large number of customers.

24

For customers, especially the value-conscious group who go to Ross, there

is little differentiation within the industry. They look for quality apparel at

discount prices and brand loyalty gives way to price savings. So for them, it does

not matter where they make purchases. Additionally, there is no cost in

switching between retailers in order to find what they want at the price they

want. The increasing cultural emphasis on fashion combined with a large number

of manufacturers means that there are a lot of clothing styles out on the market.

The product assortment offered by any retail store is no longer unique to one

store or retail chain. Since clothes can last for a long time and be a large

purchase for the average consumer, there is a greater willingness to delay

purchases in order to find the best deal. The combination of these factors means

that consumers within this market sector are highly price sensitive.

Relative Bargaining Power

The buyer’s bargaining power is determined by the volume of consumers

relative to the number of retailers and the scale of purchases made by those

consumers. When there is a large number of consumers and a small number of

providers, the providers have power over the buyers. In the case of Ross and

other off-price department stores, there are a lot of buyers and a large number

of competing retailers. So individual buyers have little bargaining power, but

when large numbers of buyers decide to go to other locations, it drives the

company to respond. The high price sensitivity of consumers means that there is

a large probability that they will abandon any company that does not meet their

expectations. This tendency is deadly to retail companies due to the previously

mentioned narrow profit margin. Although an individual consumer does not make

large-scale purchases, meaning that the loss of one customer is statistically

insignificant in regard to total sales, it is in the store’s best interest to keep as

many customers as possible. Easy return policies are one way of keeping

customers happy (WSJ.com, Many Happy Returns? It Depends). This trait of the

retail industry means that buyers have a high level of bargaining power.

25

Conclusion

The high price sensitivity and level of relative bargaining power means

that the retail apparel industry is very susceptible to pressure from the buyers.

This means that retailers must keep prices low in order to stay competitive. In

order to make a profit they have to focus on reducing costs. In this sector of the

retail industry, buyers have a high level of bargaining power.

Bargaining Power of Suppliers

The suppliers’ bargaining power determines how much they can charge

retailers for goods and services. This directly affects a company’s costs-of-goods

sold expense, profit margin, and pricing structure. The level of power suppliers

have is based on the ratio of suppliers to retailers, the number of substitute

products available to retailers, and the degree to which a supplier’s product is

necessary for the retailer’s success. A high power level means that suppliers can

set prices and control the distribution schedule to firms in their target industry.

When suppliers have a low level of power, they are not in control of pricing their

own products and have to deliver goods when retailers want them.

In the off-price retail industry, the current strategy is to buy manufacturer

overruns, canceled orders, and overstocked merchandise. Suppliers are eager to

sell these dead-weight items in order to either recover manufacturing costs or to

clear space for the next shipment of goods. This allows retailers to bargain for

lower prices. However, the recent trend of retailers to have minimal levels of

inventory (WSJ.com, Retail Squeeze Felt Far Beyond Malls) means that there is

less need for offering discounts or selling off overstocked inventory.

26

Price Sensitivity

A supplier’s price sensitivity determines the price at which they are willing

to sell their product. This sensitivity varies depending on the season, economic

market, and a product’s quality and popularity. Apparel choices vary according to

the weather, making summer styles very cheap in winter and vice versa. Low

economic growth creates a reduction in prices in order to spur purchasing and

consumers are more willing to spend more when a product is of higher quality or

very popular, so suppliers can sell at a higher price.

Because of the nature of off-price retail, suppliers are not price sensitive.

Their major concern is to sell leftover merchandise as quickly as possible.

Suppliers have no incentive in retaining merchandise for later sales. In fact, it

can be more costly for a firm to store merchandise than to sell it at below-cost.

Relative Bargaining Power

In the off-price retail industry, firms usually have a large number of

potential suppliers. Ross, for example, deals with more than 6,000 vendors and

manufacturers. This high level of competition amongst suppliers significantly

reduces their bargaining power. Most products that retailers buy are not unique

to any one manufacturer, though there are some exceptions (WSJ.com, Kohl’s to

License Liz Claiborne Brand), so they are not dependent on any one product for

their business. This makes it hard for suppliers to gain a competitive advantage

because they have nothing unique to offer.

Conclusion

Suppliers have a low level of bargaining power. The market pressure to

dispose of unwanted goods makes it hard for suppliers to set prices they want.

The sheer number of potential vendors makes the individual contributions

insignificant in the market. Retailers have large amount of leeway in determining

from whom they will buy from and at what price.

27

Analysis of Key Success Factors

Overall Industry Classification

When looking at the industry in which Ross competes, it is easy to see

that this is an industry that contains high rivalry among existing firms, with a

very low threat of new entrants. This is due to the costs associated with entering

the industry. The segment in which Ross competes tends to focus on “off –

priced” products that they can sell to the masses at a discount. There also tends

to be a fairly high threat of substitute products in the industry, but this is likely

due to the lack of differentiation throughout the industry as a whole. A few of

the important factors in the industry as far as value creation are: utilizing

economies of scale and scope, being able to focus on the consumer’s wants and

needs, maintaining solid relationships with merchandisers and vendors, and also

operating within a tight cost control system.

In order to successfully compete within the retail industry, a company

must be able to distinguish itself from the masses. Doing this is easier said than

done. The firm must be able to utilize their resources in order to convert raw

inputs into a product with value. This is done through competitive strategies that

are often determined by the industry itself, and followed by firms such as Ross,

T.J. Maxx, J.C. Penney, and Kohl’s. In order to achieve and sustain a competitive

advantage in this industry a firm must have the capabilities to implement a

strategy using both a cost leadership and slightly differentiated approach. This is

essential in order to maximize the profits and reach the full capacity of the

market.

28

Competitive Strategy

In order to compete within the retail industry, a firm must be able to

adapt to the demands of its consumers. This is done by using a cost leadership

approach, yet some differentiation approaches are needed in order to create a

unique value for the firm. As stated before this is all done by implementing

economies of scale and scope, implementing efficient production systems,

utilization of brand recognition, and bringing into play a tight cost control

system.

Economies of Scale and Scope

The industry in which Ross finds itself in is very susceptible to economies

of scale. In an industry with large economies of scale, new entrants are faced

with the problem of creating enough beginning capital in order to get their

business launched off the ground. Even when a firm is able to accumulate

enough capital to start a business, there is no guarantee that the funds will be

utilized properly right away. Therefore, as mentioned above there are very few

new entrants that pose a serious threat to market share in the retail industry.

This is a perfect example as to why economies of scale are so important. In the

long – run firms can decrease the cost of making their goods by increasing their

volume to a point where they can mass produce and therefore cut down on their

ratio of fixed to variable costs. A good way to accomplish this task in the retail

industry would be to construct large distribution warehouses that are centrally

located within their retail stores. It is also beneficial to carry the same inventories

at each store, so that the products are made readily available to all consumers.

Economies of scope refer to the strategy associated with increasing or

decreasing the scope of marketing and distribution within an industry. This

is where the aspect of advertising and other marketing techniques

becomes extremely valuable because familiarizing potential customers with

29

the brands available is a vital key to the success of a firm in the retail

industry.

Low Input Costs

One of the key ways to increase profits within the retail industry is

to cut costs, specifically input costs. A simple way for large retailers in the

industry to do so is to maintain strong relationships with their suppliers.

Because most retailers place orders of such large quantities, most

suppliers are inclined to give large discounts for their raw goods. This

obviously allows retailers to sell their products for less, which once again

ties into the strategy of cost leadership. One aspect of the retail industry

that makes it difficult to cut input costs is that their business is extremely

volatile within the seasons. This means that firms within the industry are

likely to have a lot of excess inventory at the end of each season. Hence,

providing sales at huge discounts. This often makes it hard for retailers to

turn a profit during certain “slow months” of the fiscal year.

Tight Cost Control System

When operating a firm within the retail industry, it is essential to

employ a tight cost control system. This aspect of cost leadership is

basically the backbone of such a competitive strategy. Without a firm’s

dedication to operating within a tight cost control system, ultimately it will

fail within the retail industry. In essence, it holds all other cost leadership

practices together as one. As mentioned above, retailers benefit from

having large distribution warehouses throughout the country / world that

allow them to do most of their shipping from a few centrally located

warehouses. Also, retailers are at an advantage in that they often have the

30

same products at each store and are not very differentiated which

familiarizes the consumer with the products being offered.

Product Quality and Variety

Up until now the focus of this analysis has been completely on cost

leadership. Yet, in the retail industry there is also a need to differentiate

yourself from your competitors. Retailers must somehow find a way to

bring something “extra” to the table. This is where product quality and

variety come into play. As most retailers carry numerous brands, it is often

a focus to sell particular brands that contain a certain level of brand

recognition among consumers. This brand recognition is extremely

important not only so that you can sell these products, but it also brings

potential consumers into the store so that they might purchase other

products as well. However, this particular segment of the retail industry

deals primarily with durable products that are sold primarily for an “off –

price” while also selling a very diverse range of high quality products at

reasonably affordable prices.

Investment in Brand Image

In the retail industry, it is important to have brand recognition. Not

only do consumers generally have an idea of what they are looking for and

a price range to which they are willing to pay, but often times their

tendencies are swayed because of brand recognition. Most large retailers

in the industry try to gain contractual agreements with major brands so

that they can continue to employ the brand name in their stores. These

agreements are the basis behind getting customers through the doors to

shop in their stores.

31

Investment in Research and Development

In the retail industry research and development is important

because firms always want to know where the next trend is heading. In

order to stay ahead of the curve, firms must always have a good sense of

where the industry is headed. Consumers always want to feel like they are

getting the newest items on the market, and in order to do this retailers

must keep their shelves stocked with the latest fashionable items. A lot of

retailers’ research is done by analyzing feedback from their consumers. Yet

in order to maximize market share, retailers must be aware of the

direction that their competitors are going as well. This is especially true

with department store retailers.

Industry Analysis Conclusion

In conclusion, it has been determined that the ultimate goal for a

firm in the retail industry is to focus on cost leadership while also varying

their products enough to keep them differentiated from competitors.

Finding ways to bring value to the company and maximizing profits by

cutting costs and implementing a tight cost control system is key to

excelling in the industry. Economies of scale and scope keep the big

players on top by not allowing new entrants into the market and brand

recognition and investment in research and development pave the way for

the future of the firm.

32

Firm Competitive Advantage Analysis

In the highly competitive industry of apparel retail, it is essential for a

company to be able to set itself apart from the competition. A firm is able to do

this by capitalizing on the industry’s key success factors and implementing

strategies based on those factors to differentiate themselves from the

competition. Ross Stores Inc. is able to do this through a combination of

different strategies. Cost control and differentiation are areas that Ross Stores

excel in.

Tight Cost Control

Purchasing System

Ross employs a unique purchasing system that caters directly to the off-

price retailer. The company practices what they call “close out” and “packaway”

purchases. Close out purchases are purchases of a manufacturer’s excess

product. This is a strategy that allows Ross to take advantage of the imbalance

between manufacturers’ supply and retailers’ demand. (Ross 10-K) Packaway

purchases work much the same way as close out purchases, but where close out

purchases are more in-season, packaway purchases are bought out-of-season

and packed away until the next corresponding season. Packaway items

accounted for 38% of total inventory as of February 3, 2007. Also, Ross has a

network of over 6,000 vendors. A unique practice that Ross employs with their

vendors is that they do not require that manufacturers provide promotional

allowance, return privileges, or delayed deliveries. (Ross 10-K) By doing this

Ross is able to acquire merchandise at a cheaper cost than competitors.

33

Stores

The Ross stores are set up in such a way as to eliminate as much cost a

possible. All stores are laid out according to a flexible design plan, but they are

generally very similar. (Ross 10-K) Merchandise is relatively in the same place in

each store. These layouts help reduce cost when it comes to building and

converting existing buildings into new stores. This allows Ross to build without

wasting time and money on new designs for each of its new stores. Another

way that Ross uses its stores to cut costs also derives from the layouts. The

stores are designed with self-service for the customer in mind. This reduces cost

in the form of fewer employees. Fewer employees helping customers

throughout the store means a lower wage expense. One other way that Ross

controls their costs at a store level is a weekly review done by management of

specific departments in order to assess what product is not selling and what

could be done, like sales or markdowns, to encourage faster turnaround. (Ross

10-K)

Economies of Scale

Ross is able to use economies of scale to its advantage in several ways.

For one, Ross is not the largest discount retailer, but makes up for deficit in

number of stores by clustering their stores into a certain region, predominantly

the south and the southwest. As of February 3, 2007 Ross operated 771 stores

in 27 states, including one in Guam, and 26 dd’s DISCOUNTS in California. (Ross

10-K) Compared to Kohl’s 817 stores in 45 states and T.J. Maxx’s 821 stores in

48 sates Ross’ concentration of stores is greater than the competition (Kohl’s 10-

K, TJX Companies 10-K). Ross’ purpose for clustering their stores is to better

achieve economies of scale for that certain region. Also, Ross has a total of

seven distribution centers (four owned and three leased) spread out across the

country. Two of these centers are 1.3 million square feet each. (Well above any

distribution centers owned by Kohl’s or T.J. Maxx.) With all of its distribution

centers combined, Ross has a total of 4.449 million square feet of property, and

34

485,000 of that space is designated to storage of packaway items. (Ross 10-K)

The large amount of storage and distribution space allows for a high volume of

product to pass through, which leads to economies of scale. A central office for

merchandising, purchasing, and marketing decisions also leads to economies of

scale as for general and administrative costs. (Ross 10-K)

Information systems

Ross has, and is in the process of developing, many information systems

geared towards lowering costs. For example, a recent system put in to place is a

store-level Task Management System. This system allows Ross to monitor

employee efficiency and provides new avenues of communication between front-

line and higher-level management. (Ross 10-K) Being able to identify problems in

personnel effectiveness quickly leads to a faster solution of those problems

affectedly reducing labor costs by increasing individual productivity. Another

system that Ross had made recent enhancements on is their Warehouse

Management System. This system is in place for inventory control and

transaction accountability.

2002 2003 2004 2005 2006Merchandise Inventory $716,518 $841,112 $853,112 $938,091 $1,051,729

*Taken from Ross Selected Financial Data, in 1,000’s

The above graph illustrates how important an inventory management system is

to Ross. The amount of inventory that Ross handles is a major part of their

business and that much inventory not being sold translates to high costs to Ross.

By enhancing the inventory management system Ross stands to lower costs

exponentially.

35

Differentiation

Product Quality and Variety

Ross prides itself on the quality and the variety of their product line. As

an off-price retailer Ross offers brand name, designer products at %20 to %60

off the price of department stores. (Ross 10-K) Ross also offers a wider product

range than most people recognize. They offer everything from apparel to home

furnishing and even fine jewelry in some cases. Though Ross is known mostly

for the apparel section of their business, actually 22% of their sales for 2006

were generated by Home Accents and Bed and Bath. This is second only to

Women’s Apparel which was 33%. (Ross 10-K) These figures demonstrate how

much Ross depends on the width of their product range.

Investment in Brand Image

Ross’ investment in brand images is interesting in that they invest in other

companies’ brand image. Ross builds its brand image on the product mix that it

carries. By carrying top brands such as Polo, Tommy Hilfiger, Adidas, Nike, and

Reebok, Ross sets itself apart from the competition in creating an image of top

quality for a discount price. They rely very heavily on the image of each of the

brands they carry, in addition to their discounts, to create value for the

customers.

36

Accounting Analysis

Domestic publicly traded companies are required to prepare financial

statements for their shareholders and potential investors to provide a clear and

useful picture of the company’s value. The company’s largest financial report

would generally be the company’s 10-k annual report. In this document,

companies should provide investors with valid information through accurate and

transparent reporting. The Securities Exchange Commissions (SEC) protects

investors by requiring managers to follow Generally Accepted Accounting Policies

(GAAP). These Generally Accepted Accounting Policies give managers several

options in accounting so they can illustrate their company in the context of the

industry. The problem with this is that managers are often given incentives to

manipulate the balance sheet to improve the company’s performance. Because

managers have incentives to manipulate financial statements investors should be

skeptical of the information provided by companies.

Accounting analysis is a tool we use to assess the relevance of information

given in a firm’s 10-k. There are six steps in accounting analysis that must be

executed in order to provide a clear view of the company’s value. These steps in

order are: identify principal accounting policies, assess accounting flexibility,

evaluate accounting strategy, evaluate the quality of disclosure, identify potential

red flags, and undo accounting distortions.

The first step is to identify the principal accounting policies. We decide

the principal accounting policies by looking at “… the policies and the estimates

the firm uses to measure its critical factors and risks” (Palepu & Healy 3-7). It is

important to understand how they estimate items and their policies. These

policies and estimates may cause companies to overstate assets and/or

understate liabilities; both are problems when we try to value a company.

Second, we need to assess the accounting flexibility the company uses.

Not all companies have the same amount of flexibility in their choice of

37

accounting policies. We must determine amount of flexibility the firm has to

change the numbers. For instance most retail stores have the ability to measure

their inventory using LIFO, FIFO, or Weighted Average. Each accounting method

produces different results but is allowed under GAAP.

Once we have assessed the accounting flexibility we need to evaluate the

accounting policies the firm has used. We should compare the accounting

policies with the industry norm and if the managers had an incentive to use

these strategies. For instance, if Ross decides to use FIFO in a time of rising

costs then they will be lowering their COGS and improve the net income.

Understanding the company’s accounting strategy is critical in clearly valuing the

company.

When we feel the accounting strategy is understood we check for the

quality of disclosure. Does the company give us enough information to make a

good decision on their value? A company is required to give basic information to

investors. If they decide to disclose more than the minimum, they are adding

value to the company and reassuring investors of their investment.

The fifth step in the accounting analysis is identifying potential red flags.

We do this step to insure that managers not trying to ‘cook the books’.

Examples of red flags include “… unexplained transactions that boost profits,

unusual increases in inventories in relation to sales increases” (book) and a

whole host of others. This step insures that our valuation of the firm is accurate

and true.

The final step we would use to analyze the firms accounting practices

would be to undo the accounting distortions. The past five steps we used to find

the accounting distortions. Now we need to correct these distortions. Without

correcting these accounting distortions it is impossible to accurately value the

company with its competitors.

In conclusion, accounting analysis is a key factor in valuing a company; if

the accounting is wrong then the valuation of the company is wrong.

38

Key Accounting Policies

Firms have to disclose a lot of information in their financial reports. What

they choose to disclose and how much information they give out determines how

well an investor can make a decision about the firm. The information that they

disclose shows how they measure their key success factors and how they

manage risk. Their choice of aggressive or conservative accounting methods can

influence the potential investor’s view of the company’s financial health.

Disclosure related to core business activities are the most relevant to

determining the success of a firm.

Ross Stores, Inc. being in the highly competitive retail industry focuses on

tight cost control and economies of scale. We have identified several key

accounting policies that Ross Stores, Inc. uses that relate to these strategies.

According to our analysis, these policies include but are not limited to, operating

and capital lease disclosure, company growth statistics, and inventory purchasing

and management.

Operating and Capital Lease Disclosure

In an operating lease, the firm gains only the right to use the asset and

does not assume any of the risks of ownership. In contrast, in a capital lease,

the lessee is considered to have effective ownership of the asset and so the

value of the lease is recorded on the balance sheet. Trouble occurs when leases

that should be capitalized are treated as operating leases. This can present a

false view of the company’s status. Specific disclosure policies concerning capital

versus operating leases can lead to an understatement of a firm’s liabilities

39

Ross does not have any capital leases recorded in its financial

statements, as opposed to its competitors, which do record a combination of

operating and capital leases. Ross leases the majority of its retail sites and

computer equipment. As of February 3, 2007, their total estimated lease

payments were stated at $1.7 billion.

Company Growth Statistics

Large companies have better economies of scale. As companies increase

in size, fixed costs can be spread over a wider area and bulk purchases allow for

lower input costs. Company growth statistics show how fast a company can

achieve these economies of scale and how much of their resources they put into

internal development.

Included in the 10-k of Ross Stores, Inc. are statistics on the number of

stores opened during the year and total number of stores at year-end, the sales

mix (such as Ladies apparel, home accents, etc.), fiscal amount spent on store

renovations and improvements, and the number of employees and common

stockholders at year-end. The variety of data offered gives us an overall view of

Ross’ growth. (http://pages.stern.nyu.edu)

Purchasing, Merchandise, and Inventory

In the retail industry, the bulk of a firm’s sales are directly determined by

their merchandise, and the amount of inventory possessed. Also, inventory

usually accounts for the majority of a firm’s assets on the books. In order to

understand the success of the company, it is required to understand how the

inventories move throughout the firm, the breakdown of the inventory, and how

40

the inventory is stored. As far as purchasing is involved, one of the main

concerns for a firm in the retail industry is maintaining solid supply chains in

order to efficiently turn inventory into sales.

Ross discloses information about the purchasing process that they go

through to acquire their merchandise. They reduce costs by buying on closeout

sales and placing merchandise in storage to sell next year. This practice accounts

for 38% of their inventory. Additionally, they show information on the

breakdown of sales by department. These percentages show how much of

inventory is current and how well Ross sells to its target market.

Goodwill and Hedging

It is important, when identifying key accounting policies, to look more

closely at a firm’s goodwill, and also at hedging activities. Goodwill is an

intangible asset that really does nothing more, but show how much a firm paid in

excess of the market value of a firm’s assets during an acquisition. There are

two main important details to look for when examining a firm’s goodwill. One is

the total amount of goodwill on the balance sheet and how much of their total

assets it accounts for. If goodwill accounts for a large percentage of total assets,

then there is a good chance that assets are overstated. The second thing to look

for is how often a company is impairing their goodwill. Technically a firm does

not have to write-off goodwill at any particular rate, so it is possible for a firm to

keep a large amount of goodwill on the balance sheet long after the transaction

took place where they acquired it.

In Ross’s case only 0.1% of their total assets include goodwill. This

amount is so small that it has no significant affect on the true amount of assets.

This is true for most of the other firms in the industry. As far as impairment

goes, Ross has only impaired long-term liabilities once in the last five years, and

41

this was only due to a sell of a corporate headquarters. This is fairly normal for

the industry but still requires some investigation into whether they are impairing

enough.

Hedging is a way for companies to compensate for currency risk. Firms

that have large international investments are at a high risk of declining currency

value. It is important for investors to look at a firm’s hedging activities to asses

the firm’s vulnerability to the associated risk. Ross did not have any hedging

activities as of Feb 3, 2007 (Ross 10-K). This is definitely not the industry norm,

but because Ross does not have an international scope of their business, and no

investments in foreign currency, Ross is not subject to those risks.

Potential Accounting Flexibility

Although GAAP sets forth rules for accounting, there is also room allotted

for flexibility within these standards. It is important to recognize the flexibility in

the choices the firm has made, and to evaluate how a certain choice affects the

appearance of the company.

One of the most important areas of flexibility that Ross uses to their

advantage is the choice of using operating leases instead of capital leases. An

operating lease is one where the firm does not have effective ownership of the

leased property. These generally mature before the useful life of the asset is up,

but it is possible for firms to draw up provisions for several renewals, so that

would essentially extend the lease through the asset’s useful life. Operating

lease expenses are treated as rent expense so they just go on the income

statement, and whether or not they are using the asset for its useful life, it

bypasses the balance sheet altogether. Because of the nature of operating

leases, it is possible for firms to understate liabilities.

42

Capital leases, on the other hand, are such that a firm does have effective

ownership of the property. These types of leases last for the whole useful life of

the property, and the firm acquires a liability and asset when the lease is signed.

The expense recognized for a capital lease is a combination of interest and

principal payments and depreciation expense. Since there is an initial recognition

of a liability in a capital lease, firms with a substantial amount of buildings or

equipment have a tendency to use operating leases in order to make the balance

sheet look more attractive to potential investors. Ross is no exception to this,

and by using only operating leases they are able to understate a significant

amount of liabilities.

Another area of accounting flexibility that deserves some attention is

accounting for goodwill. Goodwill is an intangible asset that is generally the

portion over the book value that is paid for a company in an acquisition. It is

said to indicate a strong brand image or good customer relations that the

acquired company had before the purchase. (www.investopedia.com) Goodwill is

a long-term, intangible asset, and like other long-term assets, is assumed to

depreciate in value over time. However, GAAP allows flexibility when it comes to

writing off goodwill. Technically, a firm does not have to write off goodwill at

any specific rate; they just write it off as the firm feels necessary. This allows

companies to overstate their assets. By never writing off goodwill, companies

are able to maintain a large number of long-term assets. In respect to Ross,

their books show an insignificant amount of goodwill. It makes up less than

0.1% of their total assets. (Ross 10-K) Other firms in the industry also have

insignificant amounts of goodwill.

Goodwill as a Percentage of Total Assets for 2006

Ross Kohl’s T.J. Maxx J.C. Penney

0.12% 0.1% 3.0% N/A

*Taken from respective 10-K’s

43

In other industries it is not uncommon for firms to accrue a large amount

of goodwill and overstate their total assets.

One more area that needs to be examined is inventory, and there are a

few areas of accounting for inventory that GAAP allows flexibility. One is the

process the firm uses to costs its inventory. Some of these methods are LIFO,

FIFO, and weighted average. Ross uses lower of cost or market with the cost

determined by weighted average. Because this process uses an average, it is

less prone to over or understate net income than FIFO or LIFO. Most other firms

in the industry use either LIFO or FIFO, which leads to more potential distortion

on the income statement. Another area of inventory flexibility that should be

looked at is how firms classify their inventory. This is another area in which Ross

is unique because they classify a portion of their inventory as “packaway”.

“Packaway” is inventory that was purchased out of season with intent of holding

the inventory until the next season. Though this system works for Ross it has a

lot of inherit risk. Inventory in the retail industry that is up to a year old can

decrease in value significantly. Though Ross is using this to their advantage in

order to provide substantial discounts on their merchandise, if Ross values the

merchandise incorrectly it can lead to distortions in inventory.

It is important to have a general understanding of the flexibility of

accounting that GAAP allows. This flexibility can sometimes lead to firms

manipulating their financial statements in order to paint a better picture for the

investor than what is really there.

44

Actual Accounting Strategy

Financial statements serve to express the economic activity of a company.

Within GAAP standards, there is a given level of discretion in which managers

may manipulate the firm’s financial standing to either depict a transparent

picture of the firm’s performance, or may use this flexibility to portray a more

positive picture of the actual business activities in order to appeal to investors.

There are many different options for recording and presenting this data. The

reports may be documented using aggressive, conservative, or a mixture of

accounting methods. Aggressive accounting seeks to minimize liabilities and

maximize revenue while conservative accounting does the opposite. While each

method has the potential to give an honest view of the company, Ross has

chosen to utilize a more aggressive documentation.

For retail industries, inventory accounts for a substantial portion of their

assets. Small changes in the method of valuing merchandise and calculating the

Cost-of-Goods Sold can have a large effect on the financial statements. Ross

Stores, Inc. uses the lower of cost or market to determine the value of inventory.

This appears to be standard practice within the industry and accurately reflects

the value of their inventory.

Many department store retailers choose to record a large number of

operating leases instead of capital leases. Usually, there is a combination of the

two; however, Ross Stores, Inc. is unusual in that it does not record any capital

leases at all. By using only operating leases, Ross Stores, Inc. keeps a substantial

portion of potential liabilities off the balance sheet. If all of these operating

leases were instead recorded as capital leases, an additional $1.37 billion of

liabilities would need to be added to the balance sheet, creating a significantly

different economic picture of the company than before. The practice of using

large amounts of operating leases is common in this industry, and is disclosed in

45

the financial report. It is considered to be an aggressive accounting tactic that

can distort the status of a company.

Qualitative Analysis of Disclosure Thanks to acts such as the Sarbanes-Oxley, and organizations like GAAP,

and FASB we have increased the transparency of a firm’s financial statements in

comparison to ten years ago. Shareholders and financial analysts often rely on

these statements to make educated business decisions in the future. These

statements also have very important economic effects such as manager’s

compensation and the quality of a company’s long-term debt obligations. The

primary qualities are that the information be relevant, and also reliable. In order

for the statements to be useful to decision makers, it must contain both qualities.

Lacking either of these two qualities in a financial statement negates the

usefulness of the information. In order for the information to be reliable, it must

be verifiable. This means that the numbers must be backed by business activities

mentioned in the 10-K. In order for the information to be relevant, it must

represent the activities being performed in a timely manner. With these elements

of quality in the financial statements, shareholders and investors can have a

greater confidence in the firm’s future projects and investments.

Accounts Receivable

In the retail industry, most sales are on a cash basis. Within our industry,

there are some accounts receivable, however they do not constitute a large

portion of assets. This being said, it is also a gateway for firms to misstate their

earnings. Accounts receivable do not guarantee that a company receives cash for

46

its credit sales, but it does increase total sales and net income. A red flag is

raised when a firm increases its accounts receivable without increasing its sales.

For the most part Ross has been consistent in reporting their receivables and has

shown incremental increases over the years, but the total amount of accounts

receivables is negligible. Therefore, their effect on the financial statements is

immaterial.

Sales Mix

Another way Ross demonstrates effective disclosure in their 10-K is by

breaking down their sales by department. This is done for many reasons, but

mainly to determine a targeted market in order to discover where the larger

profits are and also which departments are value drivers. Below is a breakdown

of Ross’ sales mix.

Sales Mix

2004 2005 2006Ladies 34% 34% 33%Home Accents, Bed, and Bath 21% 21% 22%Men's 16% 16% 15%Fine jewelry, accessories, lingerie, and fragrances 12% 11% 11%Shoes 8% 9% 10%Children's 9% 9% 9%

47

Impairment of Long Lived Assets

According to Ross’ 10-K, “During fiscal 2004, we relocated our corporate

headquarters from Newark, California, to Pleasanton, California, and sold the

facility for net proceeds of approximately $17.4 million. We recognized a net

impairment of approximately $15.8 million related to the disposal”. This raises a

“red flag” as far as disclosure is concerned. The fact that Ross was carrying the