Report No: AUS5495 Romania Component C3 of Romania Climate ...

Upload

rigel-craneCategory

view

21download

0description

NATIONAL BANK OF ROMANIANATIONAL BANK OF ROMANIANATIONAL BANK OF ROMANIANATIONAL BANK OF ROMANIA

I. Recent Macroeconomic Developments

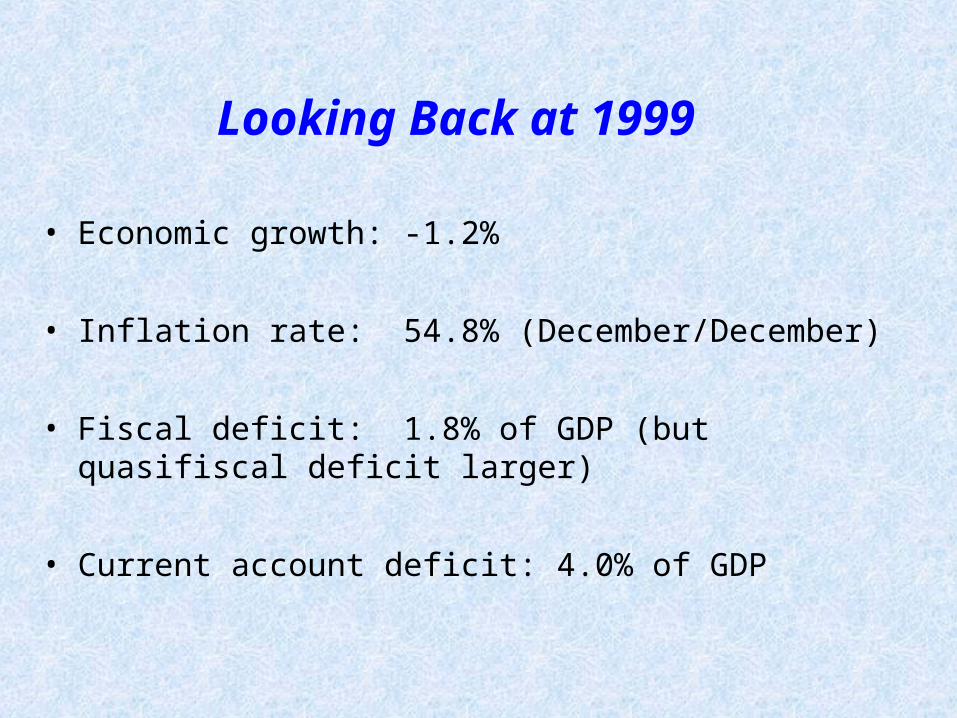

Looking Back at 1999

• Economic growth: -1.2%

• Inflation rate: 54.8% (December/December)

• Fiscal deficit: 1.8% of GDP (but quasifiscal deficit larger)

• Current account deficit: 4.0% of GDP

2000-2003:Sustainable Disinflation and Growth

• Gradual disinflation

• Robust economic growth

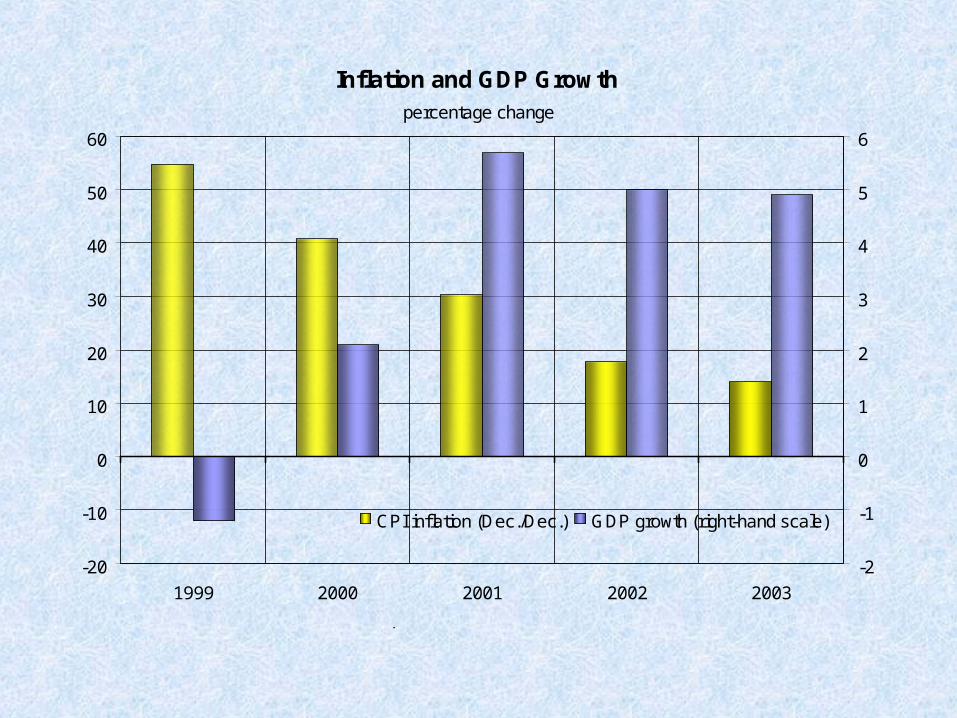

Inflation and GDP Growth

-20

-10

0

10

20

30

40

50

60

1999 2000 2001 2002 2003

percentage change

-2

-1

0

1

2

3

4

5

6

CPI inflation (Dec./Dec.) GDP growth (right-hand scale)

Source: National Institute of Statistics, National Bank of Romania

2000-2003:Sustainable Disinflation and Growth

• Gradual disinflation

• Robust economic growth

• Significant, but sustainable, current account deficits

• Moderate fiscal deficits and low public debt

Fiscal* and Current Account Deficits

0

1

2

3

4

5

6

7

8

1998 1999 2000 2001 2002 2003

Source: Ministry of Public Finance, National Institute of Statistics

fiscal current account

*) adjusted to IMF methodology

percent of GDP

Gradual Disinflation

• Smooth disinflation path, without trend reversals

• Gradual approach chosen as:– prices, tariffs and wages have recorded major adjustments

– external equilibrium has not yet been consolidated

• Supported by a consistent policy mix:– prudent monetary policy

– cautious fiscal policy

– sustainable income policy

– structural adjustments

Robust Economic Growth

• Higher GDP growth rates than in most CEE countries

• Driven initially by external demand and afterwards by domestic demand (on the back of rising wages and loans)

Moderate Fiscal Deficitsand Low Public Debt

• The official financial accounts have been maintained under control

• Fiscal deficit declined gradually from 4% of GDP in 2000 to 2.3% of GDP in 2003

• Quasifiscal losses are still significant (the quasifiscal deficit is estimated to hover around 2.5% of GDP)

• The level of public debt (around 27% of GDP at end-2003) compares favourably with that of other CEE countries

Current Account Deficits:Significant, but Sustainable

Moderate current account deficits in 2000 (3.7% of GDP) and 2002 (3.4% of GDP) due to:

• Strong export expansion

• Supportive exchange rate policy

• Beneficial influence of substantial current transfers surplus

Larger-than-foreseen current account deficit (5.8 of GDP) in 2003 due to:

• Weak external demand

• Substantial investment growth

• Rising household demand for imports

No financing difficulties

• Satisfactory coverage through FDIs - although larger productivity-enhancing FDIs desirable - and MLT external borrowings

• Adequate level of official forex reserves (covering 3.5 months of imports)

• Low foreign debt

Current Account and Foreign Direct Investment2003

-10

-8

-6

-4

-2

0

2

4

6

8

Bulgaria Czech Republic

Hungary Poland Romania Slovakia

percent of GDP

current account deficit/GDP foreign direct investment (net)/GDP

Note: GDP forecast for Hungary and Poland

Source: Websites of central banks, EBRD - Transition Report 2003

Saving and Investment Ratios

9.7

13.814.8

16.7

18.217.7

18.9

20.7

22.5

11.2

17.8

21.3

8

10

12

14

16

18

20

22

24

1998 1999 2000 2001 2002 2003

Source: National Institute of Statistics, NBR calculations

8

10

12

14

16

18

20

22

24saving ratio investment ratio

percent of GDP

Gross Official Reserves

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

1999 2000 2001 2002 2003 2004(6 May)

Source: National Bank of Romania

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

gold NBR foreign-exchange reserves

EUR million

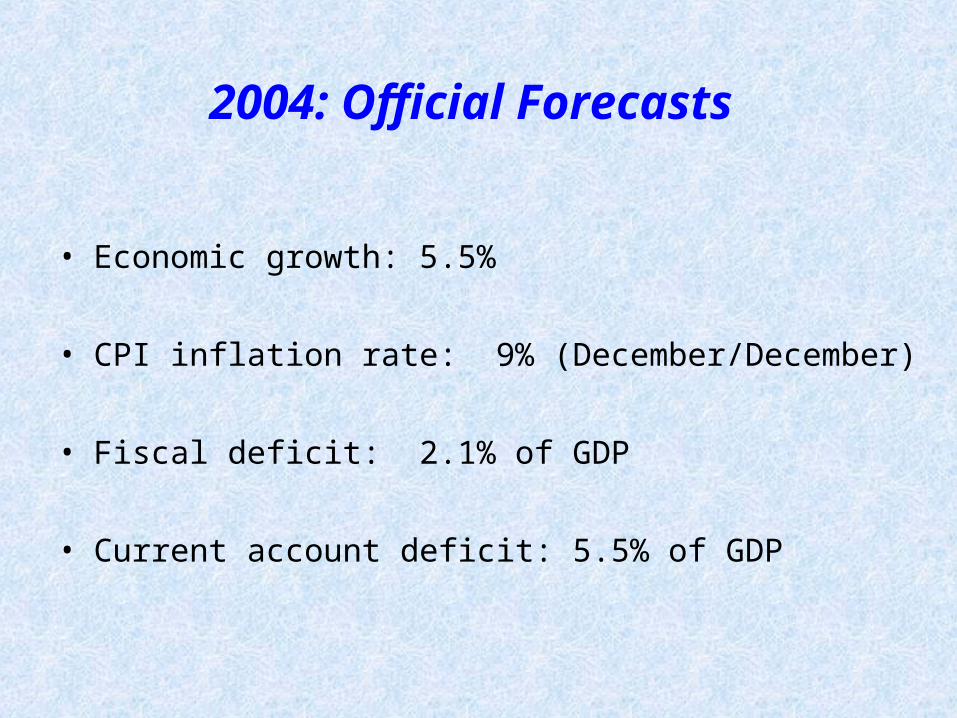

2004: Official Forecasts

• Economic growth: 5.5%

• CPI inflation rate: 9% (December/December)

• Fiscal deficit: 2.1% of GDP

• Current account deficit: 5.5% of GDP

II. Monetary Policy Coordinates

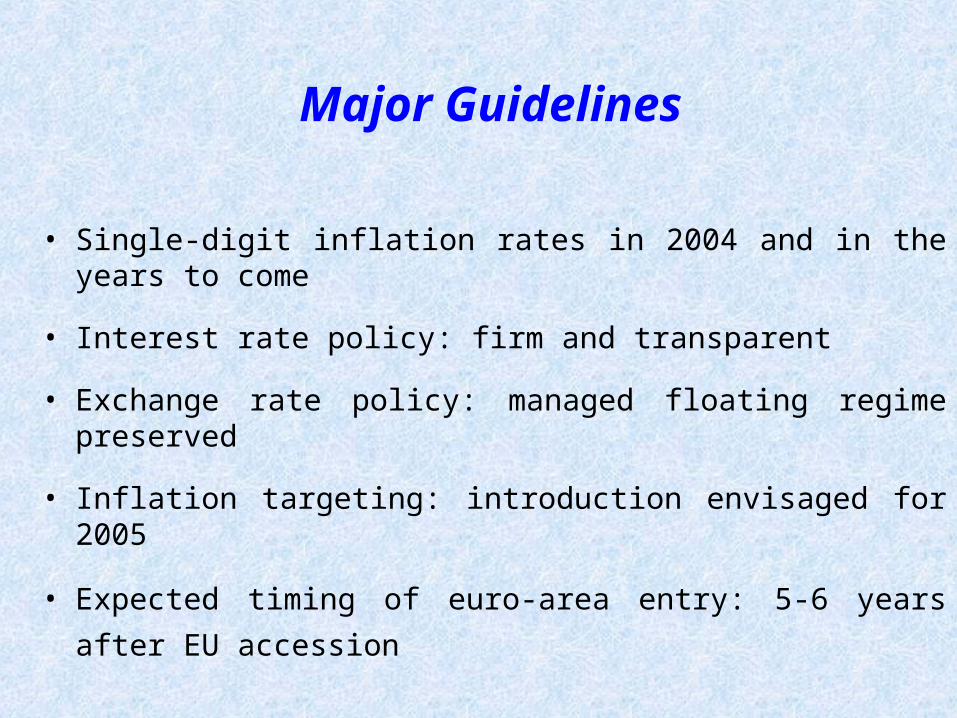

Major Guidelines

• Single-digit inflation rates in 2004 and in the years to come

• Interest rate policy: firm and transparent

• Exchange rate policy: managed floating regime preserved

• Inflation targeting: introduction envisaged for 2005

• Expected timing of euro-area entry: 5-6 years after EU accession

Inflation Rate

54.8

40.7

30.3

17.8

14.1

9.07.0

4.0

1999 2000 2001 2002 2003 2004 2005 2006

Source: National Institute of Statistics, Economic Pre-Accession Programme

CPI; Dec./Dec.

target, 2004 - 2006

Interest rate policy

• The current policy rate is high enough to encourage savings and to smooth credit expansion

• Gradual downward adjustment of the policy rate is envisaged once the disinflation trend has been confirmed

• Interest rate policy gains in transparency

Inflation Rate and Interest Rates

5

15

25

35

45

55Ja

n.0

1

Jul.0

1

Jan

.02

Jul.0

2

Jan

.03

Jul.0

3

Jan

.04

Source: National Institute of Statistics, National Bank of Romania

percent

inflation rate (percentage change againstsame year-earlier period)NBR interest rate on sterilisation operations(percent p.a.)average yield on 3M T-bills (percent p.a.)

NBR's policy rate increased to 21.25% on November 20, 2003.

5

15

25

35

45

55

Jan

.01

Jul.0

1

Jan

.02

Jul.0

2

Jan

.03

Jul.0

3

Jan

.04

percent

inflation rate (percentage change againstsame year-earlier period)average interest rate on ROL loans of non-gov't, non-bank clients (percent p.a.)

deposit rate (time deposits; percent p.a.)

Financial Intermediation and Remonetisation of the Economy

28.930.2

31.6 32.6

9.3 10.111.8

16.0

24.7 24.423.0 23.2

0

5

10

15

20

25

30

35

40

45

2000 2001 2002 2003

Source: National Institute of Statistics, National Bank of Romania

bank assets non-government credit M2

end of period, share of GDP

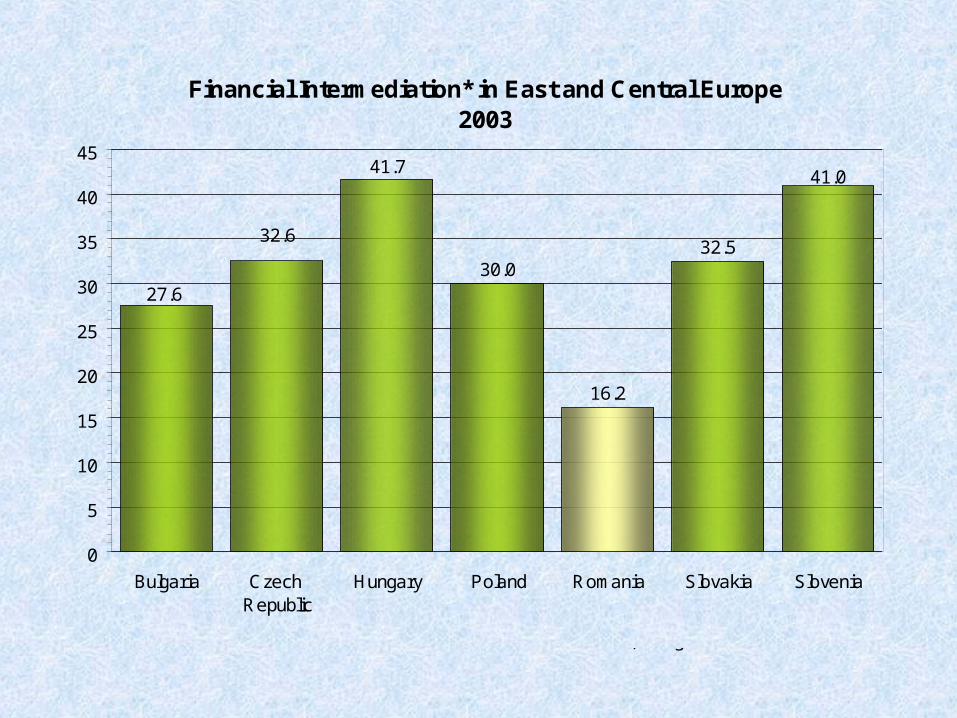

Financial Intermediation* in East and Central Europe2003

30.0

16.2

32.5

27.6

41.041.7

32.6

0

5

10

15

20

25

30

35

40

45

Bulgaria Czech Republic

Hungary Poland Romania Slovakia Slovenia

Source: Websites of national statistics institutions and central banks. *) non-government credit/GDP

Exchange rate policy

• The managed floating regime avoids excessive rate fluctuations

• Central bank foreign interventions tend to be less frequent and ample

• Euro link gets tighter – the current composition of the currency basket is EUR 75% - USD 25%

• The preferred range of real exchange rate appreciation (2-4 percent) supports disinflation without endangering external competitiveness

• The real appreciation generated by the Balassa-Samuelson effect is not counteracted through exchange rate policy

Average Real Exchange Rate of the ROL Against the Currency Basket

0

1

2

3

4

5

6

7

2001 2002 2003 2004

0

1

2

3

4

5

6

7

Source: National Bank of Romania, National Institute of Statistics (NBR calculations)

achieved

indicativerange

percentage change versus a year ago

achieved4 months

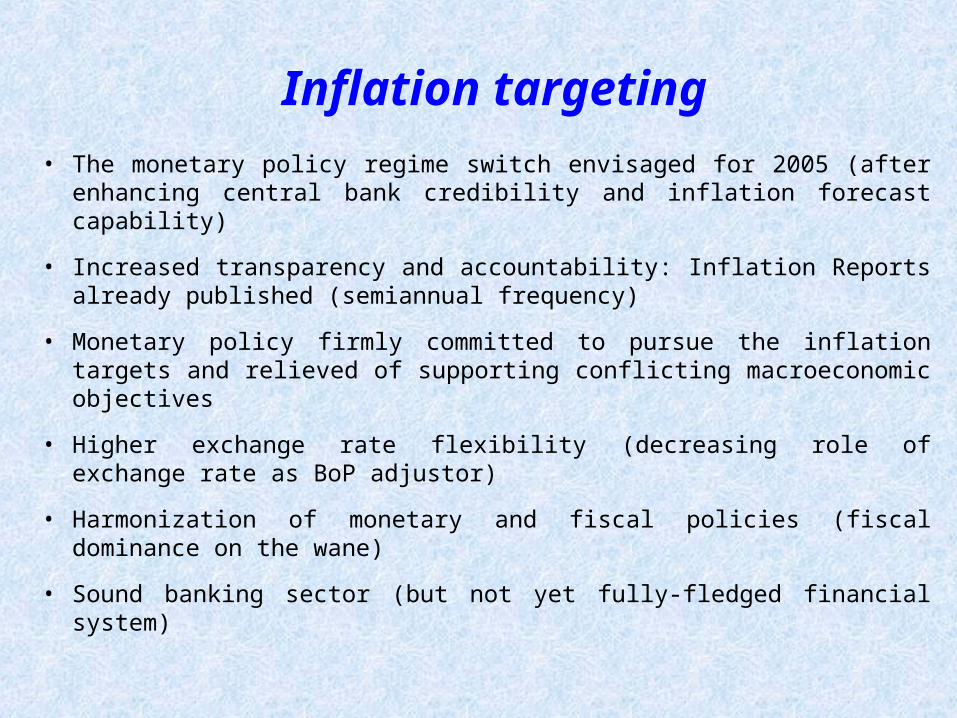

Inflation targeting

• The monetary policy regime switch envisaged for 2005 (after enhancing central bank credibility and inflation forecast capability)

• Increased transparency and accountability: Inflation Reports already published (semiannual frequency)

• Monetary policy firmly committed to pursue the inflation targets and relieved of supporting conflicting macroeconomic objectives

• Higher exchange rate flexibility (decreasing role of exchange rate as BoP adjustor)

• Harmonization of monetary and fiscal policies (fiscal dominance on the wane)

• Sound banking sector (but not yet fully-fledged financial system)

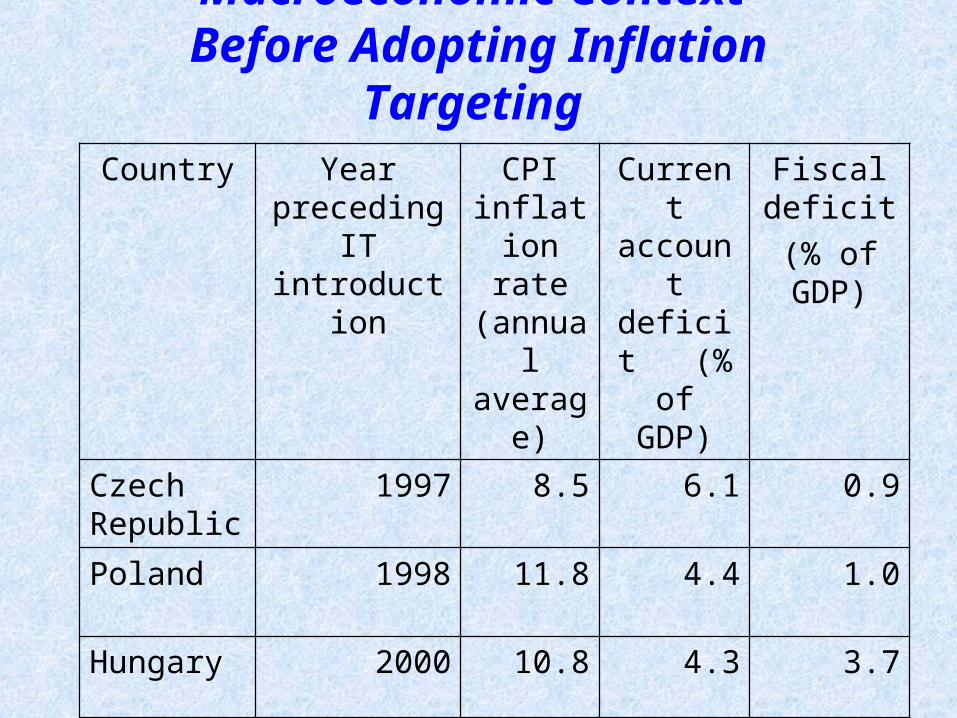

Macroeconomic Context Before Adopting Inflation Targeting Country Year

preceding IT introduction

CPI inflation

rate (annual average)

Current account deficit (% of GDP)

Fiscal deficit

(% of GDP)

Czech Republic

1997 8.5 6.1 0.9

Poland 1998 11.8 4.4 1.0

Hungary 2000 10.8 4.3 3.7

Romania (forecasts)

2004 9.0 5.5 2.1

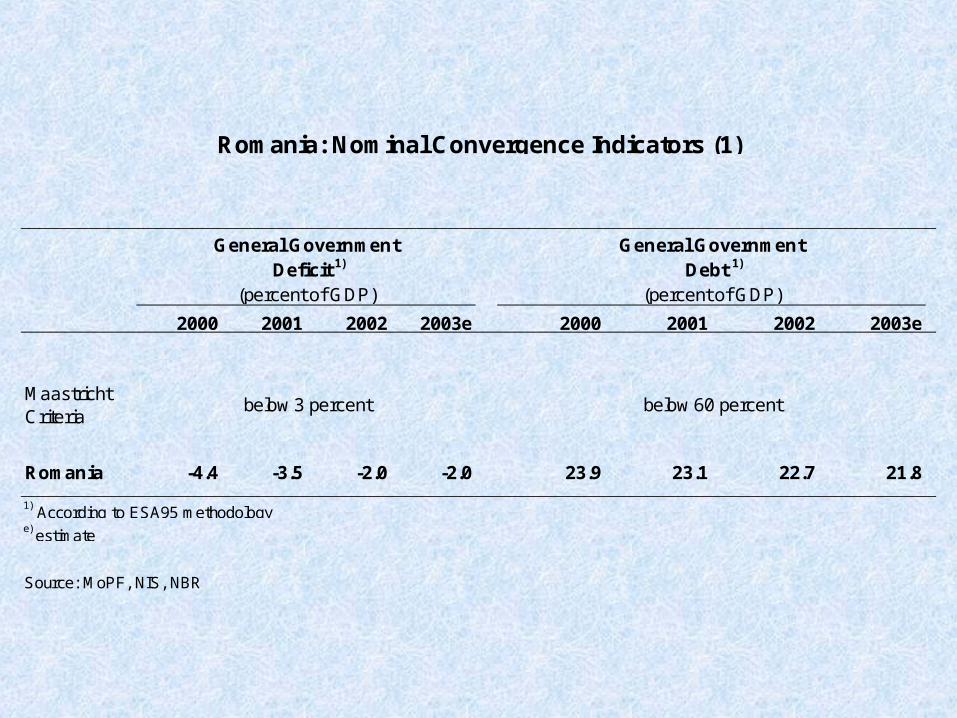

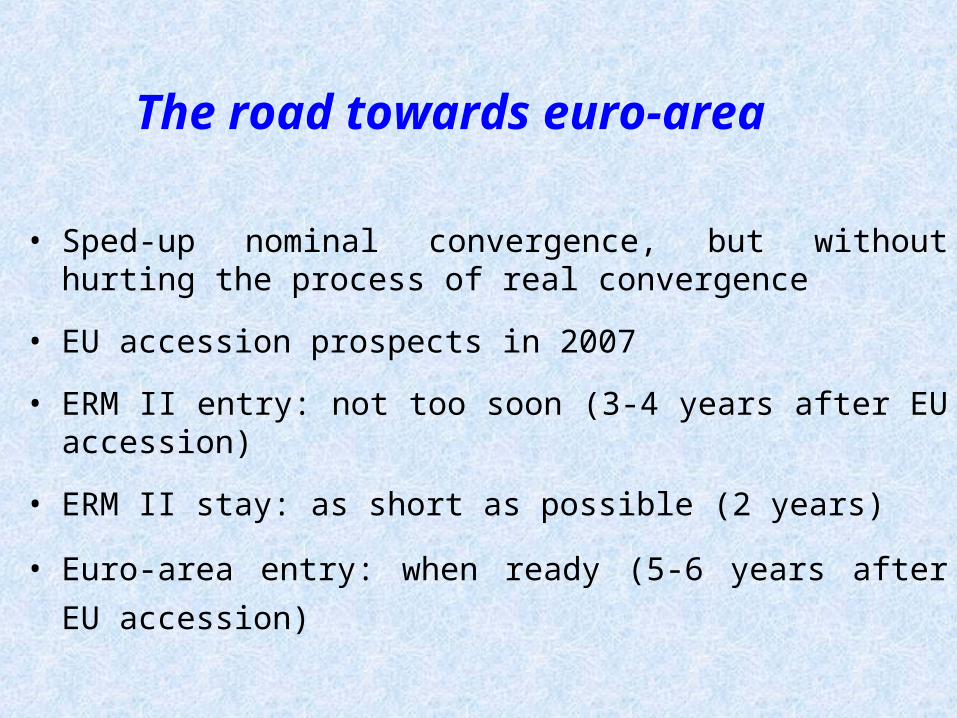

The road towards euro-area

• Sped-up nominal convergence, but without hurting the process of real convergence

2000 2001 2002 2003e 2000 2001 2002 2003e

Maastricht Criteria

Romania -4.4 -3.5 -2.0 -2.0 23.9 23.1 22.7 21.8

1) According to ESA95 methodologye) estimate

Source: MoPF, NIS, NBR

Romania: Nominal Convergence Indicators (1)

General Government

(percent of GDP)

General Government

(percent of GDP) Debt 1) Deficit 1)

below 3 percent below 60 percent

2000 2001 2002 2003 2000 2001 2002 2003 2000 2001 2002 2003

Maastricht Criteria

Romania 45.7 34.5 22.5 15.3 x x x x -18.3 -23.3 -16.7 -16.8

x = data not released

Source: NBR

(average)

<1.5 pp above the best performing three EU members

Romania: Nominal Convergence Indicators (2)

Exchange Rate (vs. euro)

(annual percentage change)

Long-term Interest Rates

(percent per annum)

Inflation rate

<2 pp above the best performing three EU members

+ / -15 percent

The road towards euro-area

• Sped-up nominal convergence, but without hurting the process of real convergence

• EU accession prospects in 2007

• ERM II entry: not too soon (3-4 years after EU accession)

• ERM II stay: as short as possible (2 years)

• Euro-area entry: when ready (5-6 years after EU accession)

![9TH WUKF EUROPEAN CHAMPIONSHIPS FOR ALL AGES [ 76 ]...(1183) naznean razvan frkwukf- romania ( romania) (1068) iorgulescu stefan frkwukf- romania ( romania) (1378) urs luciamn andrei](https://static.fdocuments.us/doc/165x107/6113116fc105242fef77af65/9th-wukf-european-championships-for-all-ages-76-1183-naznean-razvan-frkwukf-.jpg)