Role of the CFO in Ethics and Compliances of the Organisation

11

Mumbai | Pune | Hyderabad | New Delhi | Chennai | Bengaluru INDIA CFO SUMMIT 2015 ROLE OF THE CHIEF FINANCIAL OFFICER IN ETHICS AND COMPLIANCES OF THE ORGANISATION

-

Upload

ravi-nayak -

Category

Business

-

view

131 -

download

0

Transcript of Role of the CFO in Ethics and Compliances of the Organisation

Mumbai | Pune | Hyderabad | New Delhi | Chennai | Bengaluru

INDIA CFOSUMMIT 2015

ROLE OF THE CHIEF FINANCIAL OFFICER IN ETHICS AND COMPLIANCES OF THE ORGANISATION

© 2015 SKP Business Consulting LLP. All rights reserved.

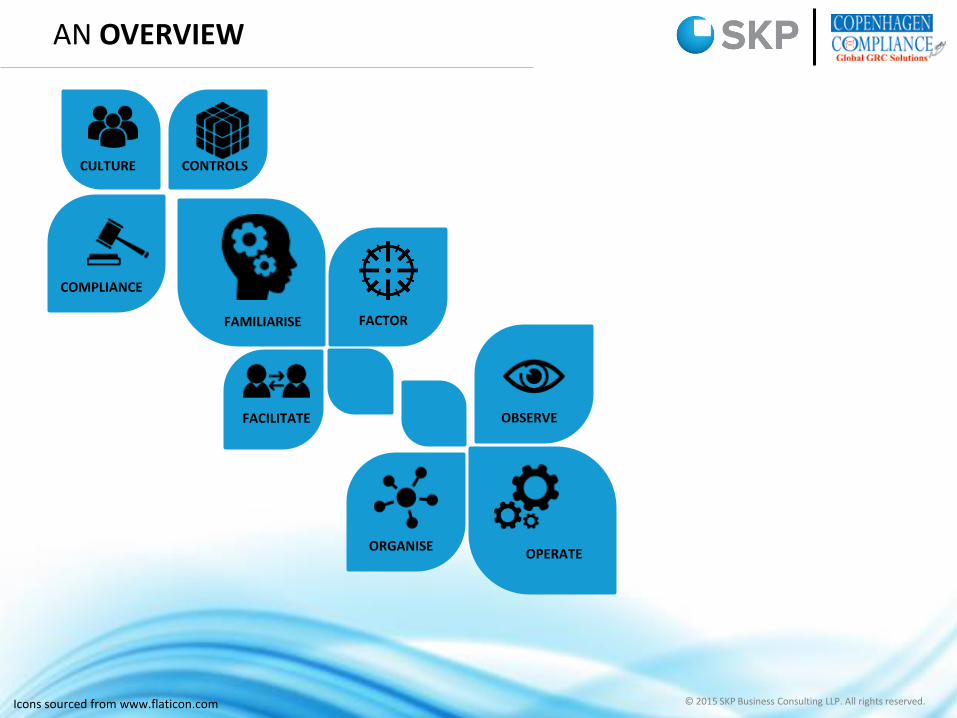

AN OVERVIEW

CULTURE CONTROLS

COMPLIANCE

FACILITATE

FACTORFAMILIARISE

ORGANISE

OBSERVE

OPERATE

Icons sourced from www.flaticon.com

© 2015 SKP Business Consulting LLP. All rights reserved.

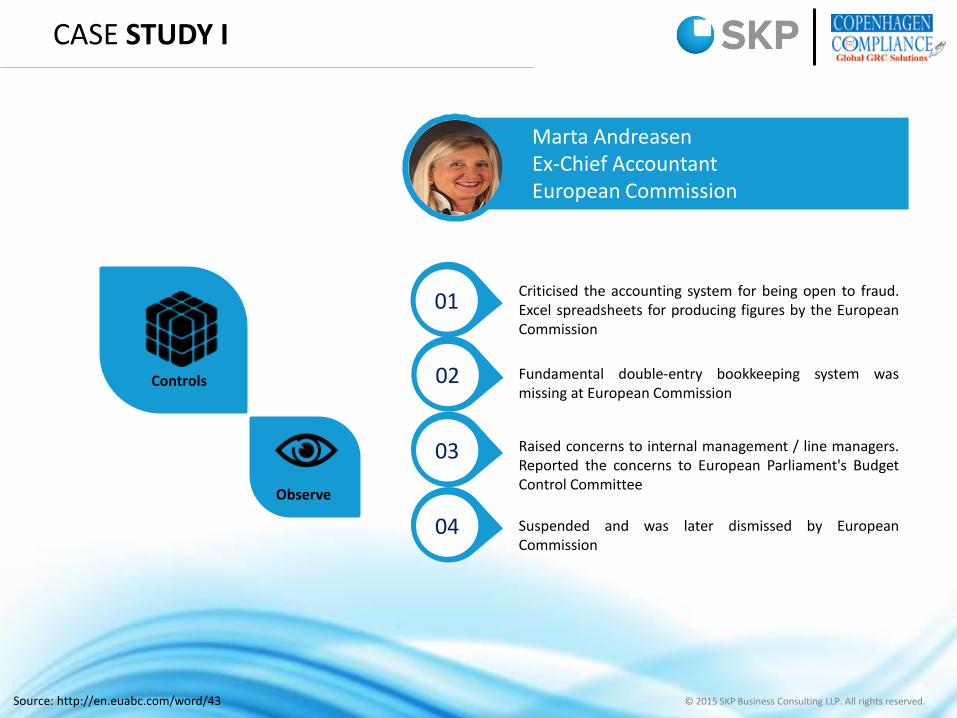

Marta AndreasenEx-Chief AccountantEuropean Commission

CASE STUDY I

Criticised the accounting system for being open to fraud.Excel spreadsheets for producing figures by the EuropeanCommission

Fundamental double-entry bookkeeping system wasmissing at European Commission

Raised concerns to internal management / line managers.Reported the concerns to European Parliament's BudgetControl Committee

Suspended and was later dismissed by EuropeanCommission

01

02

03

04

Source: http://en.euabc.com/word/43

Observe

Controls

© 2015 SKP Business Consulting LLP. All rights reserved.

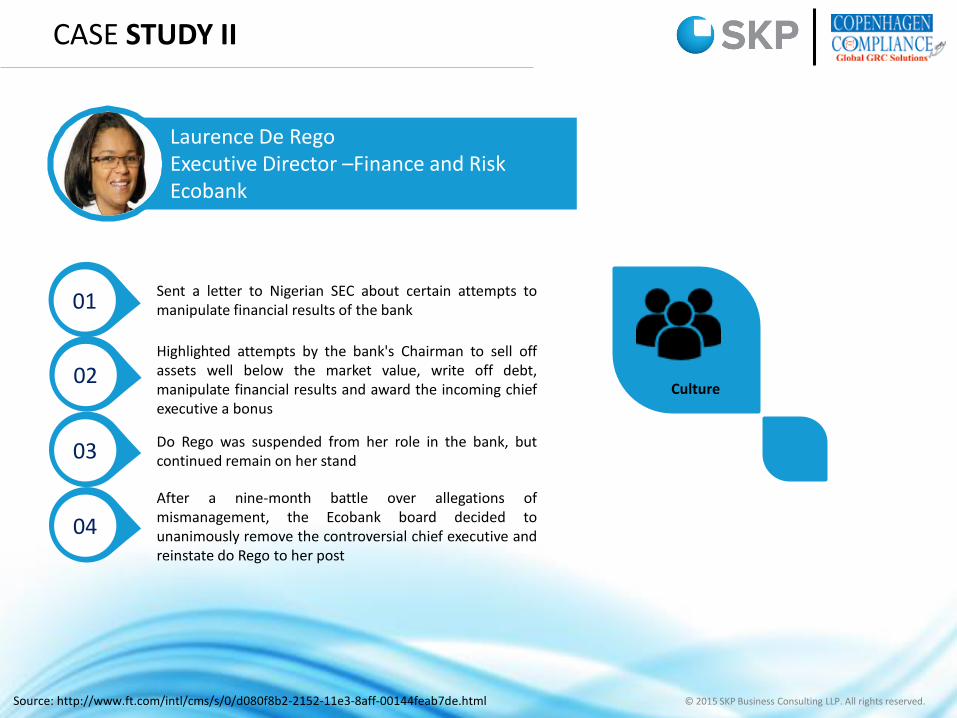

Laurence De RegoExecutive Director –Finance and RiskEcobank

CASE STUDY II

Sent a letter to Nigerian SEC about certain attempts tomanipulate financial results of the bank

Highlighted attempts by the bank's Chairman to sell offassets well below the market value, write off debt,manipulate financial results and award the incoming chiefexecutive a bonus

Do Rego was suspended from her role in the bank, butcontinued remain on her stand

After a nine-month battle over allegations ofmismanagement, the Ecobank board decided tounanimously remove the controversial chief executive andreinstate do Rego to her post

01

02

03

04

Source: http://www.ft.com/intl/cms/s/0/d080f8b2-2152-11e3-8aff-00144feab7de.html

Culture

© 2015 SKP Business Consulting LLP. All rights reserved.

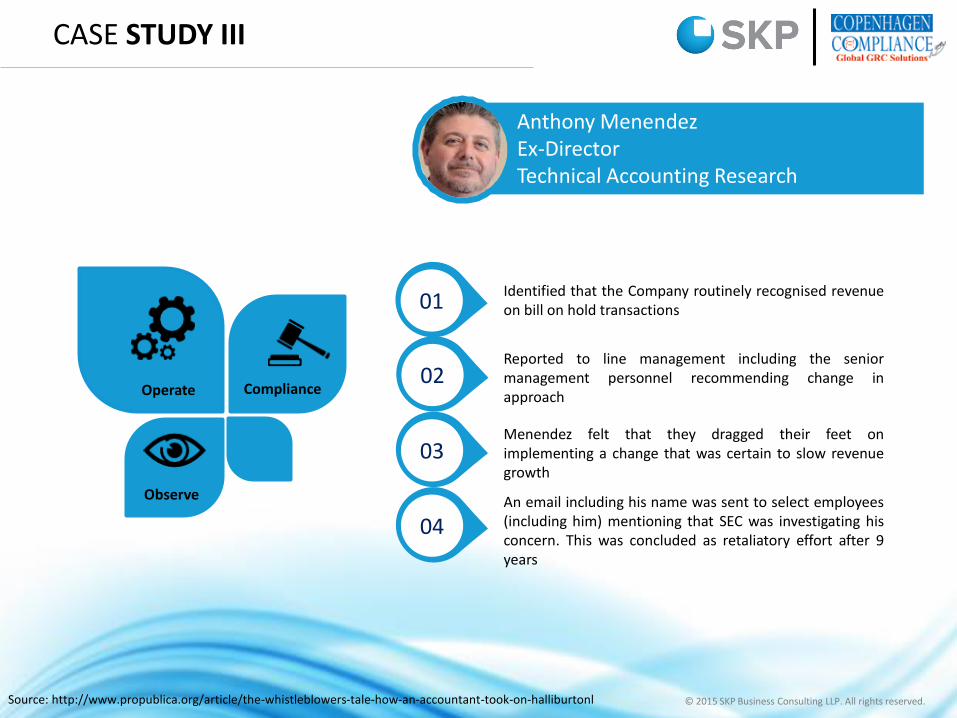

Anthony MenendezEx-Director Technical Accounting Research

CASE STUDY III

Identified that the Company routinely recognised revenueon bill on hold transactions

Reported to line management including the seniormanagement personnel recommending change inapproach

Menendez felt that they dragged their feet onimplementing a change that was certain to slow revenuegrowth

An email including his name was sent to select employees(including him) mentioning that SEC was investigating hisconcern. This was concluded as retaliatory effort after 9years

01

02

03

04

Source: http://www.propublica.org/article/the-whistleblowers-tale-how-an-accountant-took-on-halliburtonl

Observe

ComplianceOperate

© 2015 SKP Business Consulting LLP. All rights reserved.

Matthew LeeEx-Senior VP, Finance, Lehman Brothers

CASE STUDY IV

Outlined six allegations of unethical accounting in a memoto senior management.

His concerns were that monthly balance sheet listed $5bnof assets above reality, bank failed to value its inventory offinancial products, that audit-level personnel wereinadequately qualified

The allegations were unfounded and there were nomaterial issues identified – The auditor referred theoutcome of Lehman’s internal investigation.

Lehman filed bankruptcy during 2008 in the wake offinancial downturn

01

02

03

04

Source: http://www.theguardian.com/business/2010/mar/16/lehman-whistleblower-auditors-matthew-lee

Controls

FactorFamiliarize

© 2015 SKP Business Consulting LLP. All rights reserved.

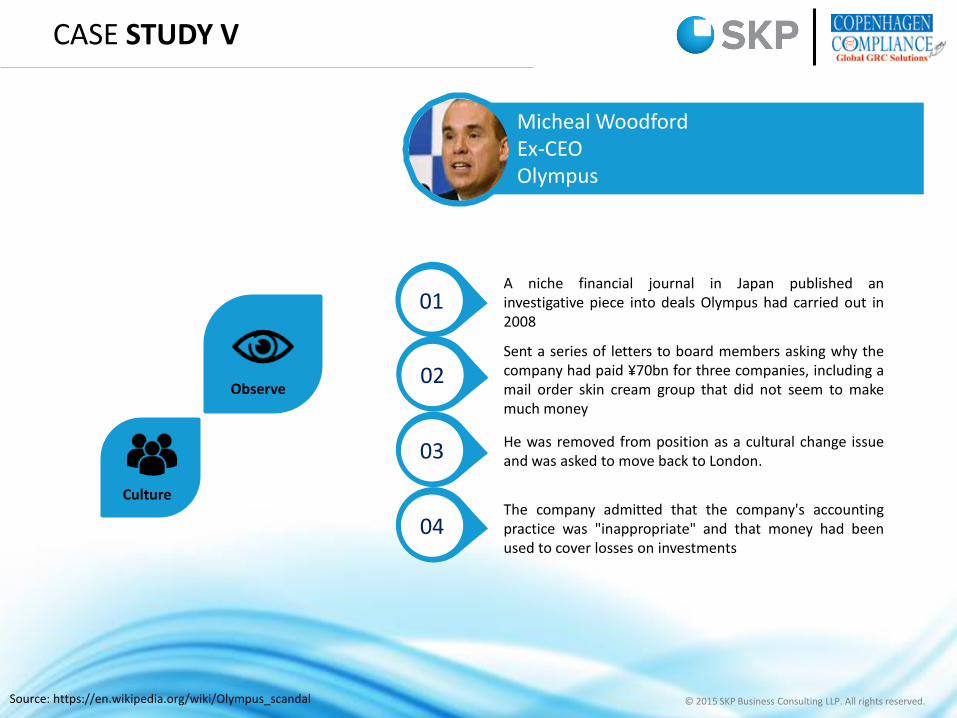

Micheal WoodfordEx-CEOOlympus

CASE STUDY V

A niche financial journal in Japan published aninvestigative piece into deals Olympus had carried out in2008

Sent a series of letters to board members asking why thecompany had paid ¥70bn for three companies, including amail order skin cream group that did not seem to makemuch money

He was removed from position as a cultural change issueand was asked to move back to London.

The company admitted that the company's accountingpractice was "inappropriate" and that money had beenused to cover losses on investments

01

02

03

04

Source: https://en.wikipedia.org/wiki/Olympus_scandal

Culture

Observe

© 2015 SKP Business Consulting LLP. All rights reserved.

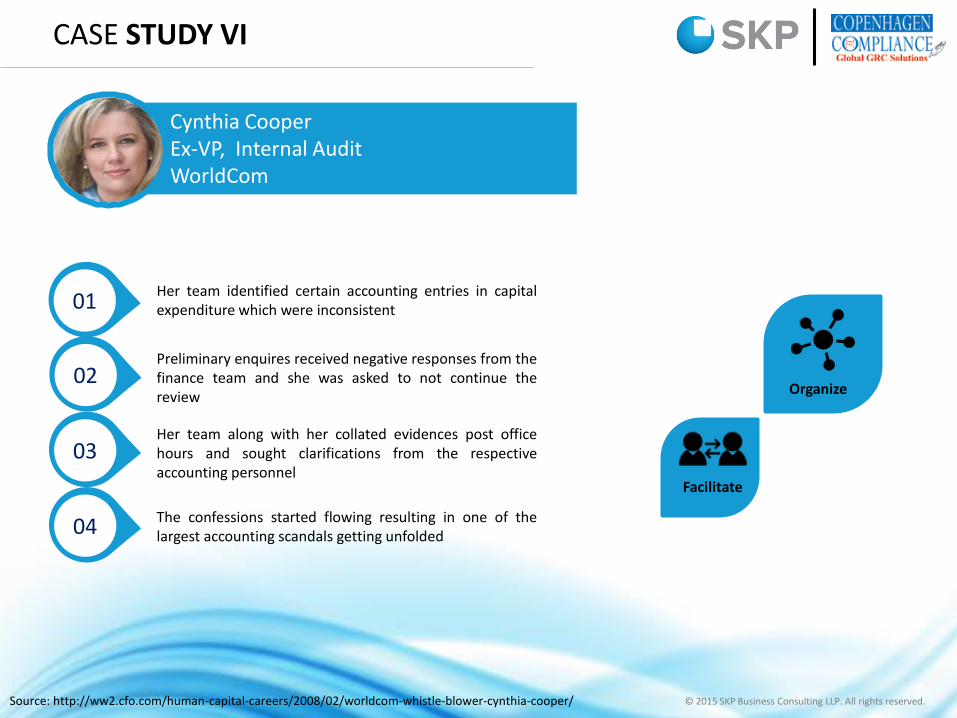

Cynthia CooperEx-VP, Internal Audit WorldCom

CASE STUDY VI

Her team identified certain accounting entries in capitalexpenditure which were inconsistent

Preliminary enquires received negative responses from thefinance team and she was asked to not continue thereview

Her team along with her collated evidences post officehours and sought clarifications from the respectiveaccounting personnel

The confessions started flowing resulting in one of thelargest accounting scandals getting unfolded

01

02

03

04

Source: http://ww2.cfo.com/human-capital-careers/2008/02/worldcom-whistle-blower-cynthia-cooper/

Organize

Facilitate

© 2015 SKP Business Consulting LLP. All rights reserved.

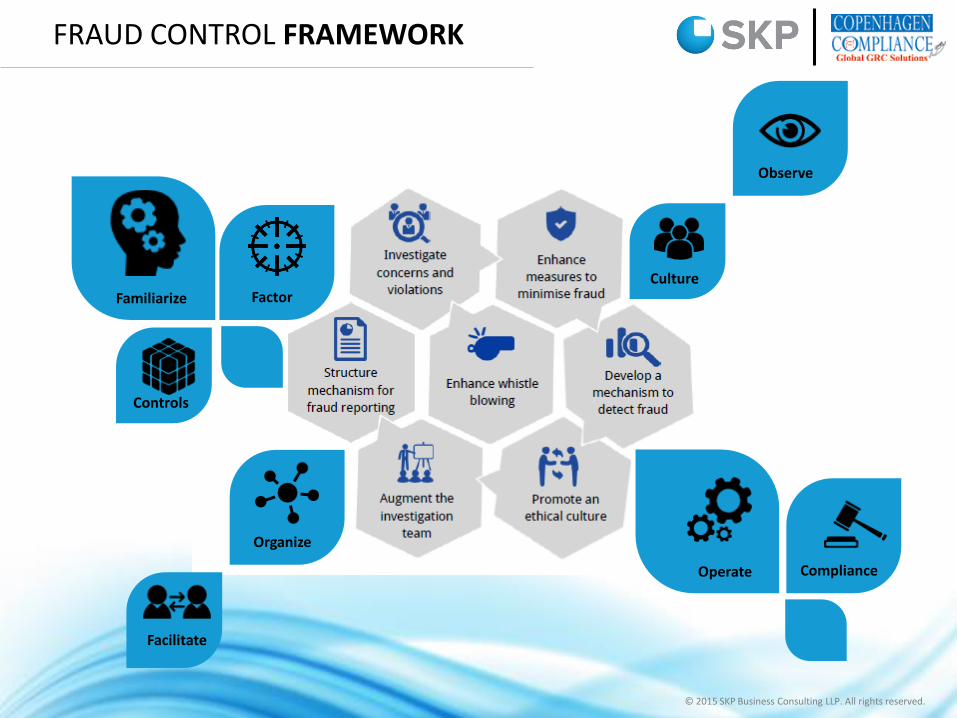

FRAUD CONTROL FRAMEWORK

Organize

Facilitate

Culture

Observe

Controls

FactorFamiliarize

ComplianceOperate

CONTACT US

19 Adi Marzban Path Ballard Estate FortMumbai 400 001Indiat: +91 22 6730 9000

Mumbai

VEN Business CentreBaner-Pashan Link RoadPashanPune 411 021Indiat: +91 20 6720 3800

Pune

6-3-249/3/1 SSK BuildingRanga Raju Lane Road 1, Banjara Hills Hyderabad 500 034Indiat: +91 40 2338 6912

Hyderabad

B-376Nirman ViharNew Delhi 110 092Indiat: + 91 11 2242 8454

New Delhi

3 Crown Court128 Cathedral RoadChennai 600 086Indiat: +91 44 4208 0337

Chennai

312/313 Barton CentreMahatma Gandhi RoadBengaluru 560 001Indiat: +91 80 4140 0131

Bengaluru

269 The East MallToronto ONM9B 3Z1Canadat: +1 647 707 5066

Toronto

www.skpgroup.com

Connect with us

Subscribe

© 2015 SKP Business Consulting LLP. All rights reserved.

The contents herein are solely meant for communicating information and notas professional advice. It may contain confidential or legally privilegedinformation. The addressee is hereby notified that any disclosure, copy, ordistribution of this material or the contents there of may be unlawful and isstrictly prohibited. Also the contents can not be considered as anyopinion/advice and should not be used basis for any decision. Before takingany decision/advice please consult a qualified professional adviser. While duecare has been taken to ensure the accuracy of the information containedherein, no warranty, express or implied, is being made by us as regards theaccuracy and adequacy of the information contained herein. SKP BusinessConsulting LLP shall not be responsible for any loss whatsoever sustained byany person who relies on this material.

© 2015 SKP Business Consulting LLP. All rights reserved.